Point-of-Care Molecular Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

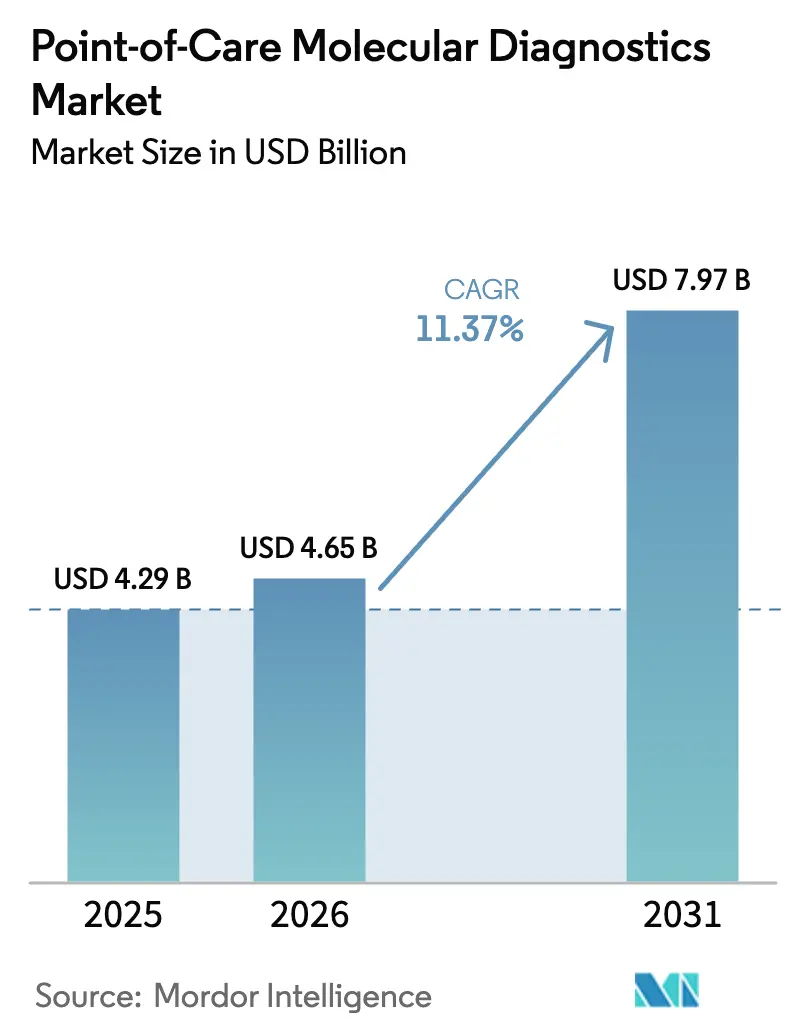

| Market Size (2026) | USD 4.65 Billion |

| Market Size (2031) | USD 7.97 Billion |

| Growth Rate (2026 - 2031) | 11.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Point-of-Care Molecular Diagnostics Market Analysis by Mordor Intelligence

The point-of-care molecular diagnostics market size was valued at USD 4.29 billion in 2025 and is estimated to grow from USD 4.65 billion in 2026 to reach USD 7.97 billion by 2031, at a CAGR of 11.37% during the forecast period (2026-2031). The growing deployment of sample-to-answer instruments in emergency departments, pharmacies, and physician offices shortens result times from days to minutes, underpinning this outlook. Public-sector stockpiling initiatives, led by the U.S. Biomedical Advanced Research and Development Authority, are shifting procurement toward decentralized platforms that can be field-deployed within 72 hours of a public-health threat. Technology maturation from lyophilized reagents that tolerate room-temperature shipping to AI-enabled cloud dashboards that monitor instrument health continues to reduce ownership costs, opening the door for small clinics and remote facilities. In parallel, regulatory bodies in the United States, Europe, and Japan have expanded CLIA waiver, IVDR, and reimbursement pathways, respectively, providing physicians with new financial incentives to order molecular panels at the point of care rather than outsourcing samples to centralized laboratories.

Key Report Takeaways

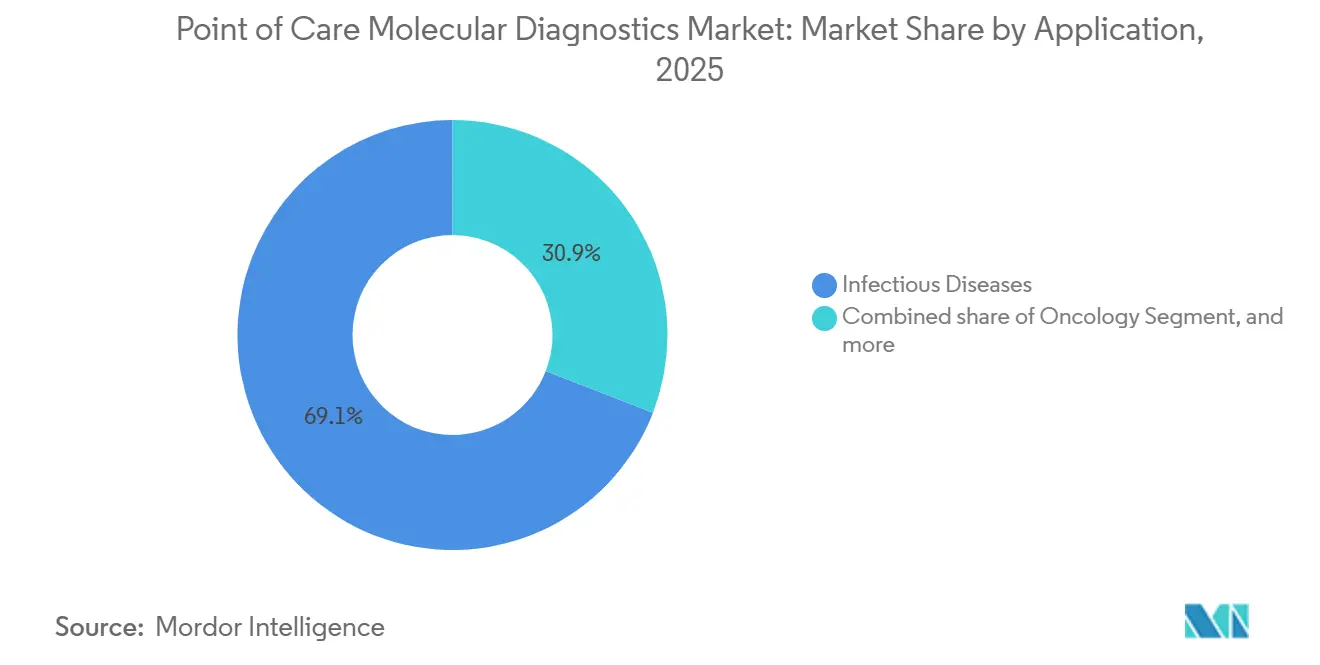

- By application, infectious diseases led the point-of-care molecular diagnostics market with 69.12% of the market share in 2025, while oncology is expected to expand at a 14.18% CAGR through 2031.

- By 2025, PCR-based technology held a 70.49% share of the point-of-care molecular diagnostics market size, and INAAT technology is projected to rise at a 14.13% CAGR through 2031.

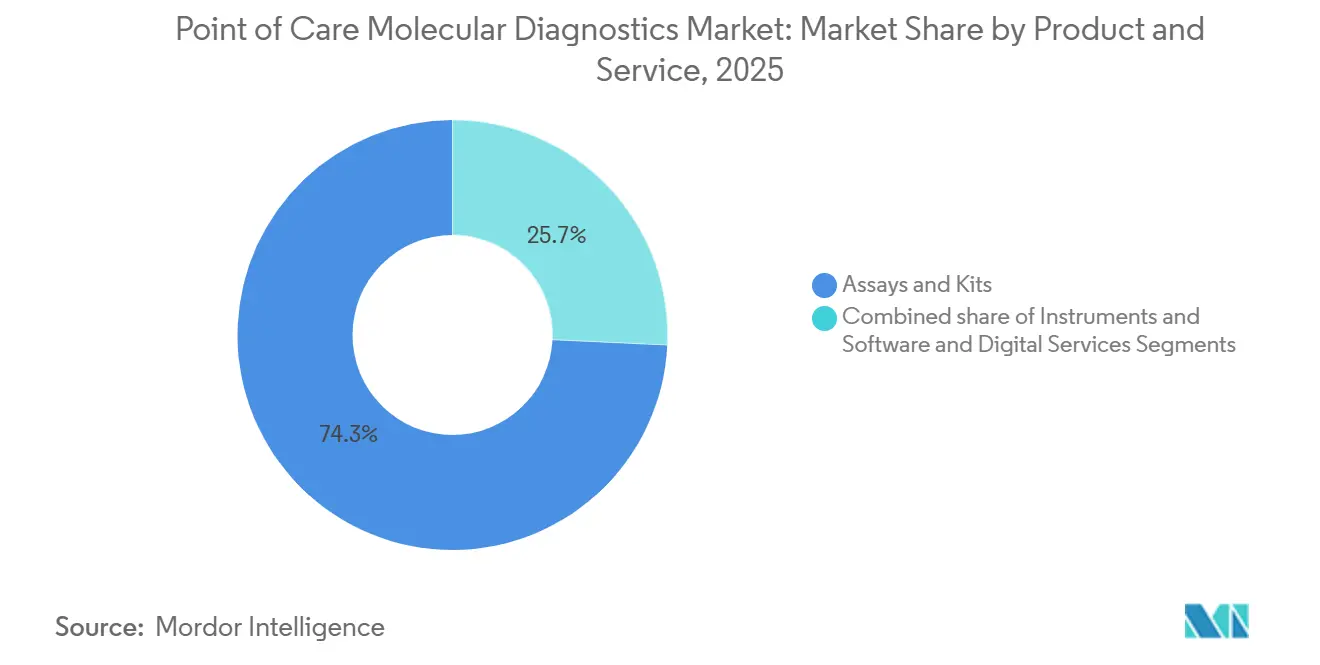

- By product & service, assays & kits commanded 74.26% of the revenue in 2025; instruments/analyzers are forecast to grow at a 12.04% CAGR between 2026 and 2031.

- By end user, hospitals accounted for 55.49% spending in 2025, whereas home care settings are projected to record an 13.34% CAGR through 2031.

- By geography, North America retained 43.64% revenue share in 2025, and Asia-Pacific is expected to post the fastest 13.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Point-of-Care Molecular Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of infectious diseases | +2.1% | Global, with acute pressure in APAC and Sub-Saharan Africa | Short term (≤ 2 years) |

| Government funding and pandemic programs | +1.8% | North America, Europe, Japan, South Korea, Singapore | Medium term (2-4 years) |

| Tech advances in sample-to-answer PCR | +1.5% | Global, early U.S. and European uptake | Long term (≥ 4 years) |

| Expansion of CLIA-waived multiplex panels | +1.3% | United States, early spillover to Canada | Medium term (2-4 years) |

| AI-driven cloud connectivity | +0.9% | North America, Western Europe, urban APAC hubs | Long term (≥ 4 years) |

| Home-based molecular self-testing | +0.7% | North America and select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Infectious Diseases and Need for Rapid Diagnosis

Delayed pathogen identification drives empiric antibiotic use, accelerates the development of resistance, and increases hospital costs. The World Health Organization documented a 12% year-over-year increase in drug-resistant tuberculosis cases across Southeast Asia in 2024, prompting ministries of health to mandate four-hour turnaround molecular susceptibility testing at district hospitals[1]World Health Organization, “Global Tuberculosis Report 2024,” who.int. Visby Medical’s 30-minute PCR panel for the three most common sexually transmitted infections cut loss-to-follow-up from 28% to under 5% in U.S. pilot clinics. During the 2024-2025 season, infant hospitalizations for respiratory syncytial virus (RSV) exceeded the 2019 baseline by 18%, thereby increasing demand for multiplex panels that can simultaneously separate RSV, influenza, and SARS-CoV-2 in a single run. The Centers for Disease Control and Prevention added 120 community hospitals to its Laboratory Response Network in 2025, each equipped with sample-to-answer instruments to bypass reference-lab bottlenecks during outbreaks.

Government Funding and Pandemic Preparedness Programs

Federal agencies committed USD 1.2 billion during 2024-2025 to stockpile instruments and cartridges after centralized capacity collapsed under COVID-19 surges. Europe’s HERA earmarked EUR 400 million (USD 430 million) to co-fund platform roll-outs in rural hospitals with fewer than 50,000 residents. Japan increased reimbursement to JPY 15,000 (approximately USD 100) per POC molecular test when results guide isolation within two hours, tripling prior rates and shifting emergency departments toward on-site testing. The NIH Rapid Acceleration of Diagnostics Technology program allocated USD 85 million across 12 consortia to compress sample collection, extraction, amplification, and detection into single-use cartridges[2]National Institutes of Health, “RADx Tech Awards,” nih.gov.

Technological Advancements in Sample-To-Answer PCR Platforms

Roche’s palm-sized cobas Liat delivers flu-A/B and RSV results in 20 minutes without external calibration, broadening respiratory testing to physician offices. Cepheid extended the ambient shelf life to 18 months by lyophilizing reagents in its Xpert cartridges, a breakthrough for low-resource environments. Abbott’s ID NOW, weighing only 3 kilograms, leverages isothermal amplification to eliminate the need for thermal cyclers and has surpassed 50,000 U.S. placements. ISO 20166-3, published in 2024, established a harmonized performance framework, facilitating expedited regulatory submissions across the United States, Europe, and Japan.

Expansion of CLIA-Waived Multiplex Panels in Physician Offices

QuidelOrtho’s Solana Respiratory Viral Panel received a CLIA waiver in 2024 and now reaches 200,000 U.S. practices, granting front-line clinicians PCR-level sensitivity without certified lab personnel. CMS raised reimbursement to USD 45 per waived molecular panel in 2025, narrowing the gap with moderate-complexity rates and strengthening return on investment for clinics. Pediatric offices doubled adoption rates over adult practices in 2024 as parents demanded single-visit diagnoses that cut unnecessary antibiotics by 40%. The American Academy of Family Physicians advised its members in 2025 to use rapid molecular tests for all acute respiratory cases during flu season, citing a 22% reduction in emergency-department referrals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented reimbursement and regulation | -1.4% | Global, most acute in emerging markets and U.S. private payers | Medium term (2-4 years) |

| High cost of consumables and instruments | -1.1% | Global, stronger effect in low-income nations | Long term (≥ 4 years) |

| Supply-chain vulnerability of cartridges | -0.8% | Global, risk concentrated in APAC manufacturing hubs | Short term (≤ 2 years) |

| Data-privacy concerns with cloud connected POC | -0.5% | Europe (GDPR), North America (HIPAA), selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Reimbursement and Regulatory Hurdles

Reimbursement rates vary from USD 25 to USD 90 per test among U.S. private insurers, fostering price opacity that deters physician office adoption despite proven clinical value[3]Centers for Medicare & Medicaid Services, “Clinical Laboratory Fee Schedule 2025,” cms.gov. Europe’s IVDR requires third-party conformity assessments; however, only 12 notified bodies are accredited for Class C devices, which stretches review timelines beyond 18 months. India requires imported POC molecular platforms to undergo local clinical validation, which adds approximately USD 200,000 to launch costs and extends timelines by one year. A 2025 Health Affairs analysis quantified 35% lower utilization of POC molecular tests in U.S. ambulatory settings owing to reimbursement uncertainty compared with send-out PCR.

High Cost of Consumables and Instruments

Instrument pricing ranges from USD 5,000 to USD 50,000, and single-use cartridges often exceed USD 30, which can squeeze rural clinics, small practices, and low-resource countries. Abbott’s ID NOW analyzer sells for USD 3,500, yet each cartridge costs USD 40, requiring 500 annual tests for break-even against send-out PCR priced at USD 25, including courier fees. Cepheid’s preferential pricing brings tuberculosis cartridges down to USD 9.98 for low-income countries, yet middle-income nations such as Brazil pay USD 14.90, restricting broad uptake. WHO estimates that scaling POC molecular testing to 80% of district hospitals in Sub-Saharan Africa would demand USD 2.1 billion in equipment and USD 800 million per year in consumables, 40% above combined national laboratory budgets. Group purchasing organizations now negotiate 30% rebates, forcing manufacturers to extend service intervals and lengthen replacement cycles from five to seven years, raising downtime risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Infectious Diseases Anchor Revenue, Oncology Accelerates

Infectious diseases accounted for 69.12% of the revenue in 2025 and continue to dominate routine testing across respiratory infections, sexually transmitted diseases, and hospital-acquired pathogens, underscoring their centrality to the Point-Of-Care Molecular Diagnostics market. Oncology, although a smaller slice today, is on a 14.18% CAGR path, driven by 90-minute liquid-biopsy cartridges that enable infusion centers to initiate targeted therapy during the same visit. Prenatal and neonatal applications remain constrained by reimbursement caps, while hematology is advancing with venture funding for minimal residual disease assays that may supplant serial bone marrow biopsies.

The migration of tumor genotyping to the bedside aligns with payer push for time-to-treatment metrics embedded in bundled payments, boosting the point-of-care molecular diagnostics market size for oncology cartridges over the forecast horizon. Infectious-disease revenue is expected to remain steady as new antimicrobial stewardship mandates favor rapid pathogen identification, while sexually transmitted infection panels gain traction in retail clinics. Pharmacogenomics tests, although regulatory-intensive, offer a long-term upside once companion diagnostic rules converge across agencies.

By Technology: PCR Dominates, INAAT Builds Momentum

PCR-based platforms accounted for 70.49% of the revenue in 2025, reflecting three decades of clinical validation, broad FDA clearances, and entrenched laboratory workflows. INAAT is growing at a 14.13% CAGR, reducing instrument footprints and per-test costs by approximately 25%, advantages that are particularly notable in urgent-care and disaster-response settings.

INAAT’s simplified thermodynamics eliminates bulky thermal cyclers, allowing sub-4 kg analyzers that run on battery power in mobile clinics. However, patent thickets surrounding loop-mediated isothermal amplification require smaller firms to license technology. PCR incumbents safeguard their market share through a large installed base, estimated at 180,000 instruments worldwide, and continuous menu expansion. However, new INAAT entrants are capitalizing on relaxed WHO performance targets, which trade marginal sensitivity for speed in tuberculosis and respiratory assays.

By Product & Service: Consumables Drive Revenue, Instruments Accelerate

Assays & Kits captured 74.26% of 2025 revenue, reflecting razor-and-blade economics where proprietary cartridges sell at multiples of production cost. Instruments, however, are tracking an 12.04% CAGR as growth shifts toward Asia-Pacific and Latin America, and as first-generation analyzers in North America hit replacement age, adding momentum to the Point-Of-Care Molecular Diagnostics market size for capital equipment.

The first FDA-cleared biosimilar GeneXpert cartridge hit the U.S. market in 2025 at 40% below Cepheid’s list price, foreshadowing the gradual erosion of consumable monopolies. Software-as-a-service revenues remain under 5% today, but could compound quickly as hospitals link connectivity subscriptions to quality-based reimbursement incentives. Cartridge price discounting, however, risks compressing gross margins and may push suppliers to bundle software analytics as a defensive moat.

By End User: Hospitals Lead, Homecare Disrupts

Hospitals absorbed 55.49% of the 2025 spending, driven by the emergency department's reliance on rapid results to guide isolation, admission, and therapy decisions. Home care is the breakout story, on an 13.34% CAGR, propelled by the FDA’s streamlined home-use guidance and employer sponsorship that circumvents payer deadlocks.

Retail pharmacies and urgent-care centers represent additional high-growth niches as chain operators deploy instruments to cross-sell prescriptions and vaccinations. Physician offices benefit from wider CLIA waivers but often lack throughput to justify capital outlay, a gap that manufacturers address via reagent-rental plans and micro-leasing offers. Home-use cartridges must overcome the hurdles of cold-chain and app-guided collection. Yet, consumer willingness to self-test for influenza and strep in under 30 minutes has been validated in multiple employer clinics, suggesting a potential for broader mainstream uptake over time.

Geography Analysis

North America generated 43.64% of 2025 revenue, thanks to reimbursement parity with central-lab PCR under the Clinical Laboratory Fee Schedule and to ASPR contracts that embedded 5,000 FilmArray systems in the Strategic National Stockpile. Canada’s CAD 180 million initiative equipped remote Indigenous facilities with sample-to-answer instruments, trimming tuberculosis diagnosis from 14 days to four hours and reinforcing regional momentum. Yet private-payer fragmentation keeps ambulatory uptake uneven, with test prices swinging nearly fourfold across insurers for identical assays.

The Asia-Pacific is the fastest-growing region, with a 13.29% CAGR, driven by China’s CNY 12 billion township-hospital modernization and India’s public-private rollout of tier-2 POC hubs that bypass cold-chain deficits. Japan’s reimbursement tripling to JPY 15,000 (USD 100) for two-hour isolation decisions accelerated emergency department adoption. At the same time, Southeast Asian governments work with World Bank loans to localize cartridge production after export bottlenecks during COVID-19. Australia harmonized approvals with FDA timelines, clearing 15 devices in 2024 and attracting multinational entrants.

Europe, the Middle East & Africa, along with South America, complete the global picture. Europe’s full enforcement of the IVDR consolidates the market share of quality-system-strong incumbents but creates 18-month backlogs that deter start-ups. Germany’s updated payer schedules now cover POC sexual-health tests across 40,000 GP clinics, while Global Fund grants subsidize HIV and hepatitis cartridges in Sub-Saharan Africa. Brazil piloted dengue and Zika panels in 50 primary-care clinics, recording training completion rates of only 15%, which highlights the workforce deficit that still limits decentralized adoption.

Competitive Landscape

The point-of-care molecular diagnostics market remains moderately fragmented; the top three players, Danaher’s Cepheid, Abbott, and Roche, together hold roughly 40% share, leaving ample headroom for regional specialists and assay innovators. Strategies are increasingly centered on menu breadth, cartridge pricing, and cloud-connectivity subscriptions that lock users into proprietary ecosystems. Danaher’s tie-up with Oxford Nanopore brings nanopore sequencing into the Xpert format, targeting 90-minute antimicrobial-resistance genotyping, a value-add PCR cannot offer. Abbott’s ID NOW platform enjoys widespread adoption yet faces 30% rebate pressure from hospital group purchasing organizations that demand electronic health record interoperability.

Disruptors such as Visby Medical, Binx Health, and T2 Biosystems collectively raised USD 180 million in 2024 to commercialize single-use, battery-powered devices priced under USD 100 per test, challenging capital-intensive incumbents. The first FDA-approved generic GeneXpert cartridge signals that consumable strongholds will weaken as patent cliffs emerge. Meanwhile, FDA draft guidance on Software as a Medical Device compels cloud-powered platforms to separate decision-support algorithms from core diagnostics, reshaping product roadmap priorities across the field.

Supply-chain risks also influence competitive tactics; most cartridge plastics are sourced from three APAC contract manufacturers, prompting incumbents to dual-source tooling and prequalify secondary suppliers. Data-privacy regulations, such as GDPR and HIPAA, further complicate cloud-connectivity rollouts, prompting European platforms to default to edge processing that never leaves hospital firewalls, whereas U.S. vendors lobby for business-associate agreement exemptions to speed up deployment.

Point-of-Care Molecular Diagnostics Industry Leaders

F. Hoffmann-La Roche Ltd

Danaher Corporation

Thermo Fisher Scientific Inc.

BioMérieux SA

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Co-Diagnostics, Inc., a molecular diagnostics company, presented the Point-of-Care Testing 2025 Exhibition and Conference in Boston, MA. The company specializes in developing molecular diagnostic tests using its patented platform. The news highlights Co-Dx's ongoing engagement in the diagnostics industry.

- June 2025: QuidelOrtho Corporation, a global provider of innovative in vitro diagnostic technologies designed for point-of-care settings, clinical labs, and transfusion medicine, announced a strategic shift in its molecular diagnostics focus. The company plans to acquire full ownership of LEX Diagnostics after FDA clearance for about USD 100 million.

- January 2025: bioMérieux acquired SpinChip, a company specializing in point-of-care diagnostic technology. This move aims to enhance bioMérieux's offerings in rapid diagnostics, particularly for acute care situations such as myocardial infarction. The integration of SpinChip's innovative platform is expected to improve diagnosis speed and patient outcomes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the point-of-care molecular diagnostics (POC-MDx) market as all cartridge- or chip-based systems and associated assays that amplify or detect nucleic acids (PCR, LAMP, INAAT, and similar chemistries) at or near the patient site, delivering actionable results inside two hours without routing specimens to a central laboratory.

Scope exclusion: visually read lateral-flow immunoassays and large bench-top molecular analyzers housed only in core labs are not covered.

Segmentation Overview

- By Product & Service

- Assays & Kits

- Instruments / Analyzers

- Software & Digital Services

- By Application

- Infectious Diseases

- Oncology

- Hematology

- Prenatal & Neonatal Testing

- Endocrinology

- Pharmacogenomics & Companion Dx

- Other Applications

- By Technology

- PCR-Based

- INAAT

- Other Technologies

- By End User

- Hospitals

- Homecare Settings

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infectious-disease clinicians, emergency physicians, community-pharmacy owners, and quality managers at decentralized labs across North America, Europe, Asia, and Latin America. Conversations clarified real-world cartridge usage, typical instrument uptime, and likely ASP compression, letting us adjust secondary assumptions that looked optimistic and fill hard data gaps.

Desk Research

We anchored secondary evidence in open, high-credibility repositories such as the WHO Global Tuberculosis Report, CDC FluView, ECDC Surveillance Atlas, and the FDA 510(k)/EUA database, which list test volumes, positivity rates, and new device clearances. Trade groups like AdvaMed and the Asia Pacific Medical Technology Association supplied unit shipment trends, while hospital utilization data from HCUP and Eurostat helped us parse bedside versus laboratory testing patterns. Company 10-Ks, investor decks, and patent analytics from Questel offered pricing bands and pipeline clues. Select insights were cross-checked in D&B Hoovers and Dow Jones Factiva for revenue sanity. These references are illustrative; many additional sources informed data gathering and validation.

Market-Sizing & Forecasting

We initiated a top-down model that reconstructs the global demand pool from disease incidence and testing penetration by care setting. We then reconciled it with sampled supplier shipments multiplied by blended ASPs to create a bottom-up checkpoint. Variables such as installed POC PCR analyzers, average cartridges per instrument per day, regulatory approvals issued each year, respiratory-infection seasonality, and the share of decentralized testing in total molecular tests drive the model. A multivariate regression links these inputs to revenue, and scenario analysis captures policy or reimbursement shocks. Data voids in shipment counts were bridged with median utilization ratios surfaced during primary calls before being stress-tested against trade stats.

Data Validation & Update Cycle

Outputs pass a three-layer review: automatic variance flags, senior-analyst peer checks, and a manager sign-off. We re-contact sources when deviations exceed preset thresholds. Our numbers refresh annually; however, material events such as a major assay recall trigger an interim update, and a final audit occurs just before each publication.

Why Mordor's Point-Of-Care Molecular Diagnostics Baseline Earns Trust

Published estimates often diverge because firms pick different device sets, apply unlike ASP curves, or freeze models for many quarters.

Key gap drivers include whether non-PCR chemistries are counted, how aggressively future menu expansions are priced, and the cadence at which COVID-era volumes are normalized. Mordor Intelligence updates models yearly, applies uniform currency conversions, and removes non-molecular assays, which together create a steadier baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.98 B (2025) | Mordor Intelligence | - |

| USD 4.30 B (2025) | Global Consultancy A | Includes near-patient but non-PCR antigen tests, raising totals |

| USD 8.73 B (2025) | Industry Publisher B | Rolls central-lab 'near-patient' platforms into POC scope and assumes slower ASP decline |

The comparison shows that once heterogeneous scopes and price paths are adjusted, our USD 3.98 billion figure sits midway between aggressive and conservative scenarios, giving decision-makers a balanced, transparent starting point grounded in variables they can trace and replicate.

Key Questions Answered in the Report

How large is the Point-Of-Care Molecular Diagnostics market today?

The Point-Of-Care Molecular Diagnostics market size is USD 4.65 billion in 2026 and is projected to rise to USD 7.97 billion by 2031.

Which application area is growing the fastest?

Oncology panels are forecast to grow at a 14.18% CAGR through 2031 as infusion centers adopt 90-minute liquid-biopsy cartridges for same-visit therapy decisions.

What technology is displacing PCR in new installations?

Isothermal Nucleic Acid Amplification Technology is expanding at a 14.13% CAGR because it removes thermal cyclers, shrinking instrument size and cutting per-test costs.

Why is Asia-Pacific the quickest-expanding region?

Government modernization programs in China and India, alongside Japan's higher reimbursement for rapid isolation decisions, drive a 13.29% CAGR across Asia-Pacific.

What limits adoption in low-resource countries?

High cartridge prices, fragmented reimbursement, and reliance on a narrow APAC supply base constrain uptake despite clear clinical benefits.

Page last updated on: