Mobility As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 374.55 Billion |

| Market Size (2031) | USD 716.30 Billion |

| Growth Rate (2026 - 2031) | 13.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobility As A Service Market Analysis by Mordor Intelligence

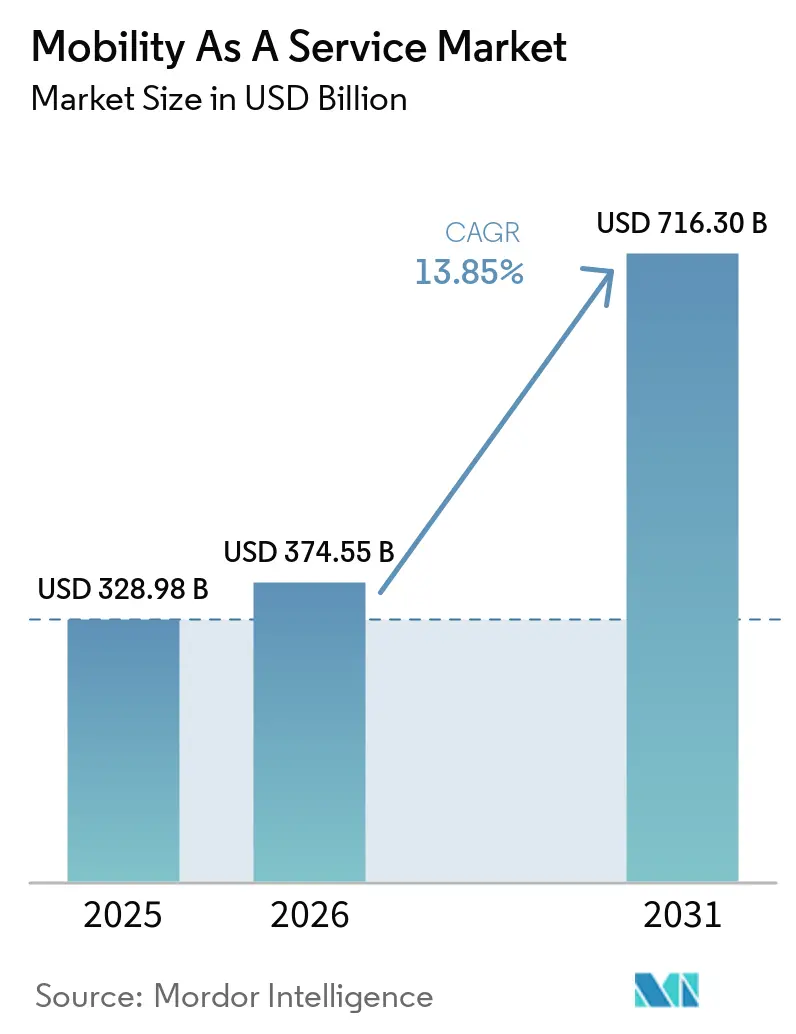

The mobility as a service market size is expected to grow from USD 328.98 billion in 2025 to USD 374.55 billion in 2026 and is forecast to reach USD 716.3 billion by 2031 at 13.85% CAGR over 2026-2031. Strong urban population growth, continuous smartphone adoption, and heightened environmental awareness are shifting consumers from private vehicle ownership toward integrated, shared, and multimodal transport offerings. API standardization, electric and hydrogen propulsion adoption, and seamless payment innovation are accelerating platform interoperability, improving customer experience, and driving provider revenue diversification. Policymakers are pushing zero-emission goals that prioritize public–private partnerships and stimulate large-scale deployments of electric fleets, while 5G and IoT upgrades enable real-time fleet orchestration and predictive journey management. Intensifying competition between incumbent ride-hailing leaders and emerging specialized MaaS orchestrators is prompting aggressive investment in artificial intelligence, data monetization, and subscription models as companies seek defensible differentiation.

Key Report Takeaways

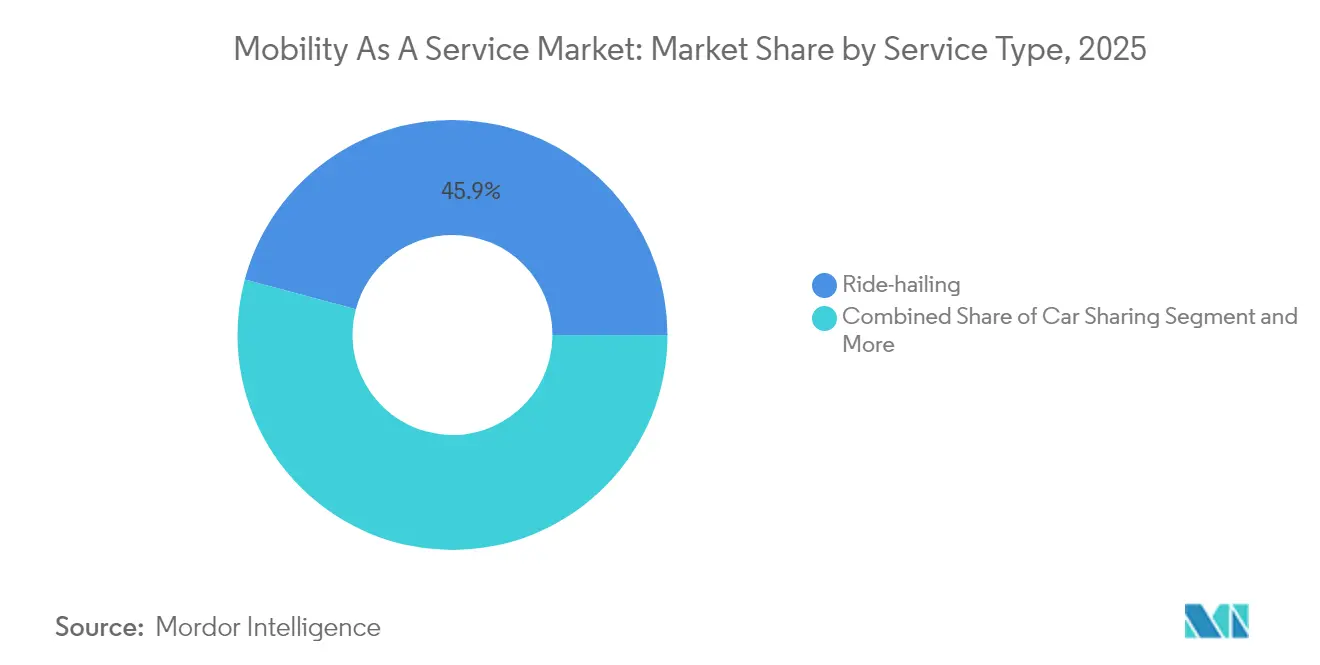

- By service type, ride-hailing captured 45.85% of the mobility as a service market share in 2025; micro-mobility is projected to expand at a 19.12% CAGR to 2031.

- By solution, technology platform solutions held 37.72% revenue share in 2025; payment and wallet services are forecast to grow at 20.95% CAGR through 2031.

- By vehicle type, passenger cars accounted for a 56.63% share of the mobility as a service market in 2025, while autonomous pods advanced at a 22.74% CAGR to 2031.

- By transportation type, private transportation led with a 61.34% share in 2025; public transportation is anticipated to post a 14.93% CAGR over 2026-2031.

- By business model, pay-as-you-go represented 67.25% of 2025 revenue; subscription bundles are rising at 23.88% CAGR through 2031.

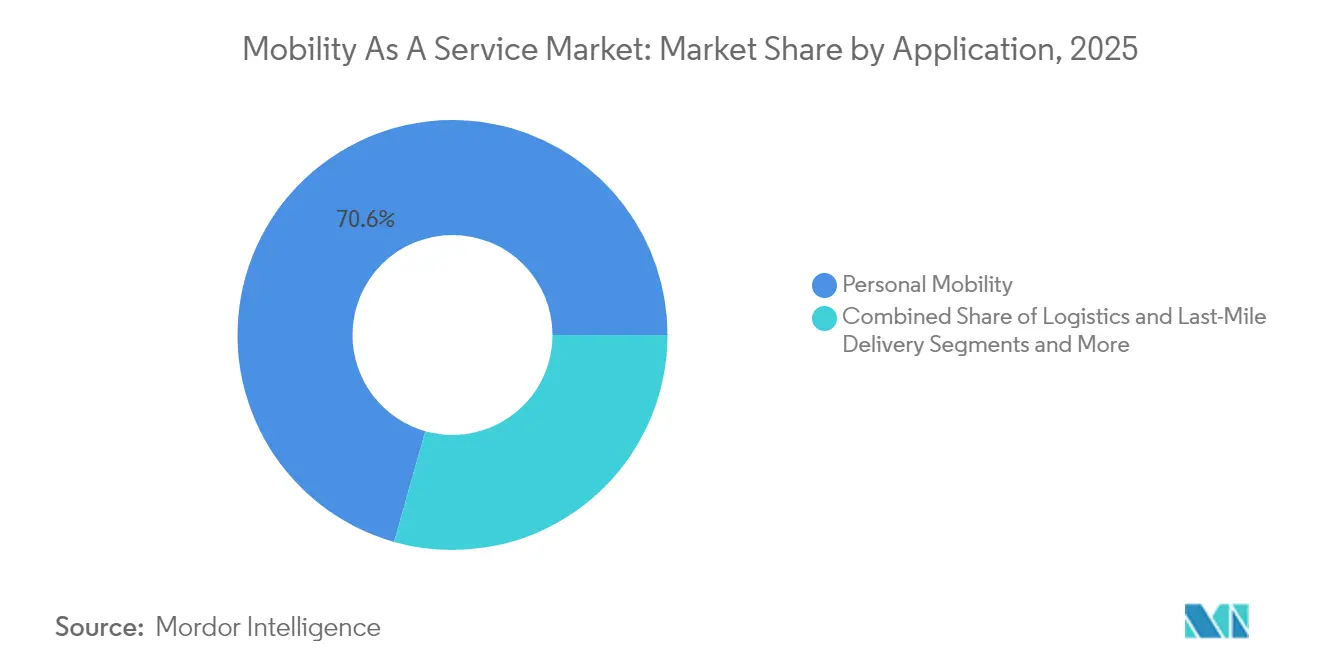

- By application, personal mobility commanded 70.62% of the mobility as a service market size in 2025, and logistics/last-mile delivery will grow at a 20.53% CAGR to 2031.

- By end-user, individuals held 77.46% share in 2025; enterprise adoption is gaining momentum at a 16.96% CAGR to 2031.

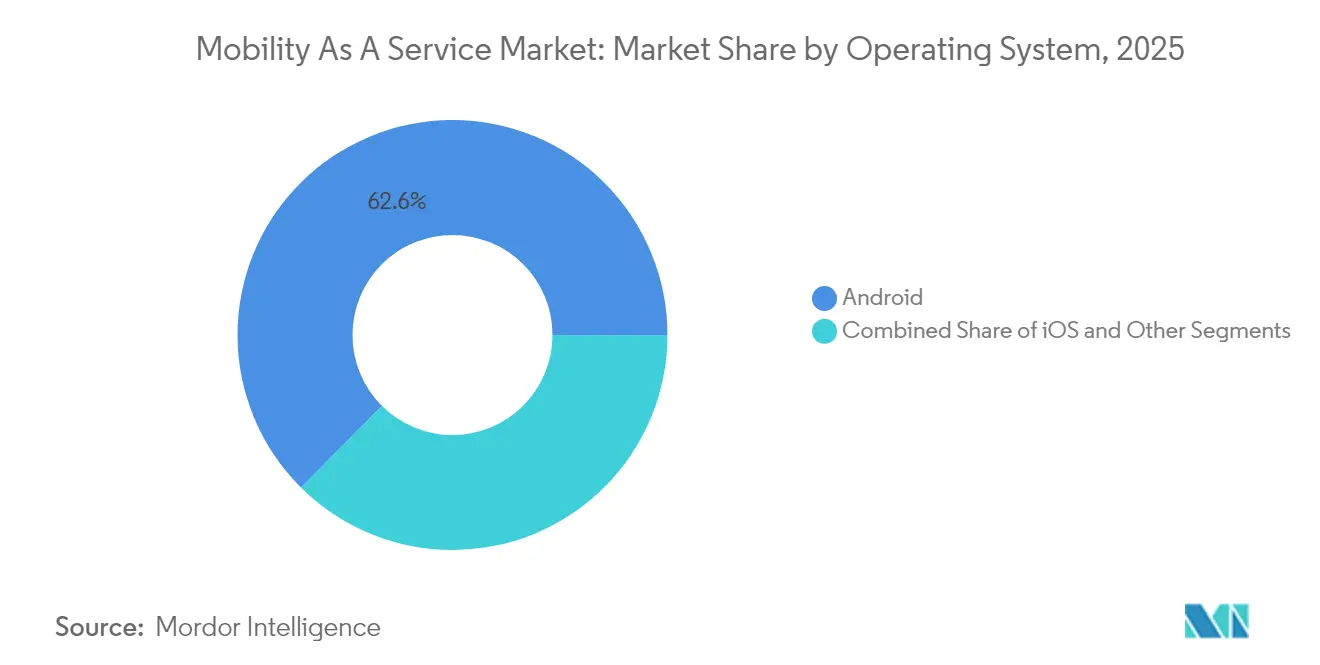

- By operating system, Android controlled 62.55% share in 2025; other platforms including HarmonyOS and PWAs are set to expand at 23.05% CAGR through 2031.

- By propulsion, electric powertrains represented 41.58% share in 2025; hydrogen fuel-cell vehicles are expected to post a 25.42% CAGR during 2026-2031.

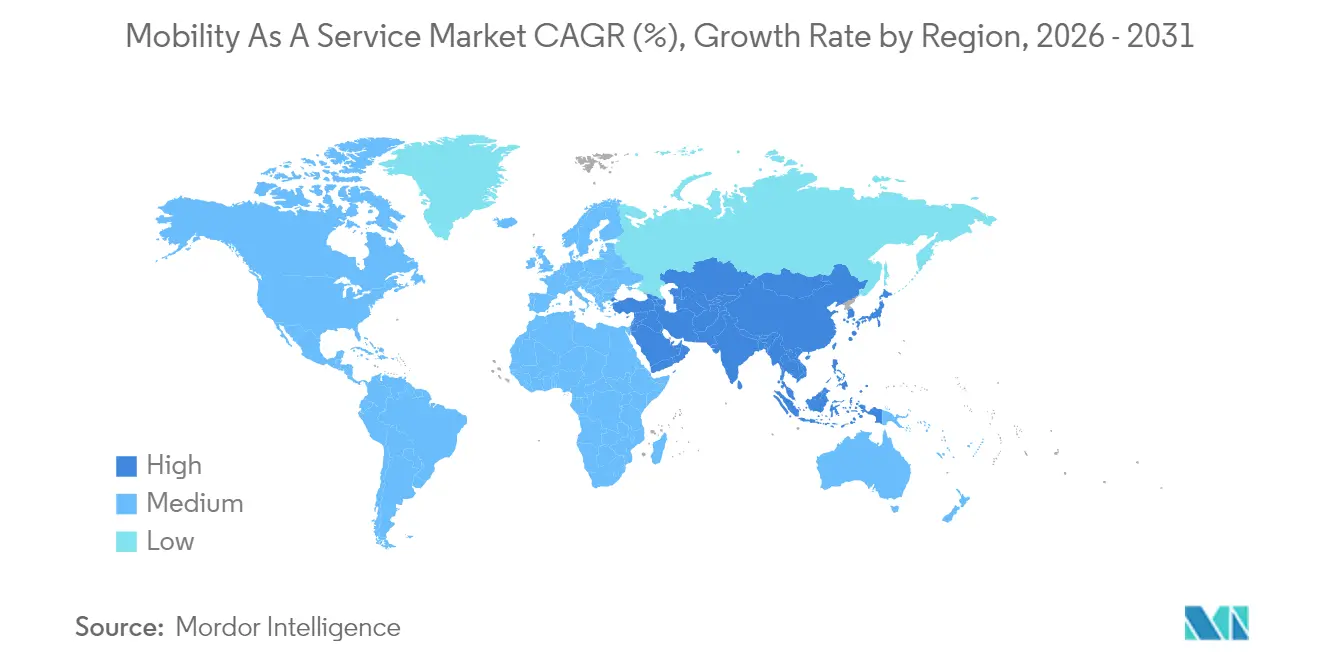

- By geography, Asia Pacific secured 34.12% of mobility as a service market share in 2025; the Middle East and Africa is positioned as the fastest growing region at 14.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobility As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of Micro-Mobility and Public Transit Across European Cities | +3.2% | Europe, with spillover to North America | Medium term (2-4 years) |

| Government Zero-Emission Targets Fueling EV-Centric MaaS Bundles (APAC) | +2.9% | Asia Pacific, Europe | Long term (≥ 4 years) |

| API Standardization (NeTEx, GTFS-RT) Enabling Account-Based Ticketing | +2.5% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Surge in VC Funding for South America MaaS Super-Apps | +2.1% | South America, particularly Brazil and Chile | Short term (≤ 2 years) |

| 5G/IoT-Driven Real-Time Mobility Orchestration | +1.6% | North America, Europe, Advanced Asian markets | Medium term (2-4 years) |

| Corporate Travel Sustainability Mandates in North America | +1.5% | North America, with spillover to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration of Micro-Mobility and Public Transit Across European Cities

The seamless integration of micro-mobility options with traditional public transit systems creates multimodal transportation networks that significantly enhance first-mile/last-mile connectivity. European cities like Helsinki and Vienna are pioneering this integration, with public transport authorities actively incorporating bike-sharing and e-scooter services into unified mobility platforms. This integration is yielding remarkable results, with the International Transport Forum reporting that properly integrated micro-mobility can increase public transit ridership by up to 35% in urban corridors.[1] “Transition to Shared Mobility: How Cities Can Deliver Inclusive Transport Services,” International Transport Forum, itf-oecd.org. The most successful implementations feature standardized docking stations strategically positioned near transit hubs, unified payment systems, and real-time availability data. Beyond improving transit accessibility, this integration is reshaping urban planning priorities, with cities like Barcelona redesigning street infrastructure to accommodate micro-mobility lanes that connect directly to transit stations.

Government Zero-Emission Targets Fueling EV-Centric MaaS Bundles

Stringent emission reduction targets across regions such as Asia-Pacific are catalyzing the development of electric vehicle-focused offerings in the Mobility as a Service Market, combining EV ride-hailing, electric car-sharing, and e-bike rentals into comprehensive mobility packages. China's mandate for 40% of vehicles to be electric by 2030 has prompted companies like Didi to launch "Green Alliance" MaaS bundles that exclusively feature zero-emission transportation options. These EV-centric services are gaining significant traction, with TÜV SÜD reporting that electric mobility services can reduce urban transport emissions by up to 70% compared to conventional vehicle usage.

API Standardization (NeTEx, GTFS-RT) Enabling Account-Based Ticketing

The widespread adoption of standardized data exchange protocols like NeTEx (Network Timetable Exchange) and GTFS-RT (General Transit Feed Specification Real-Time) is revolutionizing account-based ticketing systems, enabling seamless multimodal journeys without needing multiple tickets or payment methods. These standards provide a common language for disparate transportation systems to communicate, allowing real-time data synchronization across modes. The MaaS Alliance reports that cities implementing these standards have seen a 40% increase in cross-modal transfers and a 25% reduction in ticketing-related customer service inquiries. Beyond operational efficiencies, these standards enable innovative fare models like mobility credits and dynamic pricing based on real-time demand. The Metropolitan Transportation Commission in San Francisco has demonstrated that standardized APIs can reduce the time to integrate new mobility services into existing platforms by up to 60%, significantly accelerating MaaS ecosystem expansion.

Surge in VC Funding for South America MaaS Super-Apps

South America is experiencing unprecedented venture capital investment in MaaS super-apps that combine transportation, food delivery, and financial services into unified platforms tailored to the region's unique mobility challenges. This funding surge enables rapid expansion of services in previously underserved markets, with Brazil and Mexico leading adoption. According to Papermark's analysis of top mobility investors, South American MaaS startups secured over USD 1.2 billion in funding during 2024 alone, focusing on integrating informal transit networks into digital platforms. These super-apps address critical regional challenges, including limited banking access, by incorporating alternative payment methods and micro-lending features specifically for transportation. The integration of previously informal transit options like "collectives" in Mexico and "kombis" in Brazil into digital platforms is formalizing these services while enhancing their reliability and safety, creating a more inclusive mobility ecosystem that serves diverse socioeconomic segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regulatory Frameworks Across U.S. States | -1.9% | North America, particularly United States | Medium term (2-4 years) |

| GDPR/CCPA-Driven Data-Privacy Compliance Costs | -1.7% | Europe, North America | Short term (≤ 2 years) |

| Profitability Challenges from Driver/Provider Subsidies | -1.5% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Legacy Transit IT Systems Limiting Integration Depth | -1.4% | Global, particularly in established transit markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Frameworks Across U.S. States

The inconsistent patchwork of transportation regulations across U.S. states is creating significant operational challenges for MaaS providers attempting to scale nationally. Each state imposes different licensing requirements, insurance mandates, and operational restrictions. This regulatory fragmentation forces companies to develop state-specific operational models, substantially increasing compliance costs and slowing market penetration. The Federal Highway Administration highlights that this lack of regulatory harmonization has resulted in up to 35% higher operational costs for multi-state MaaS providers than those operating in more unified regulatory environments.

GDPR/CCPA-Driven Data-Privacy Compliance Costs

The implementation of stringent data protection regulations like the European Union's General Data Protection Regulation (GDPR) and California's Consumer Privacy Act (CCPA) is imposing substantial compliance costs on MaaS providers, who must navigate complex requirements for data collection, storage, and sharing. These regulations are particularly challenging for MaaS platforms that rely on extensive user data to optimize routes, predict demand, and personalize services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Micro-Mobility Disrupting Urban Transit Patterns

Ride-hailing dominates the MaaS market with a 45.85% share in 2025, leveraging its established user base and extensive driver networks to maintain market leadership. However, micro-mobility services (scooter/bike sharing) are emerging as the fastest-growing segment with a projected CAGR of 19.12% from 2026 to 2031, driven by their effectiveness in addressing first-mile/last-mile connectivity challenges. The IAA Mobility report indicates that micro-mobility solutions equipped with IoT connectivity and high-performance batteries significantly enhance user experience through improved stability and real-time availability tracking. This growth is further supported by city governments increasingly allocating dedicated infrastructure for micro-mobility lanes and parking zones.

The car sharing segment is witnessing substantial innovation through the introduction of flexible, free-floating models that eliminate fixed pickup and drop-off locations, while bus sharing services are gaining traction in corporate environments and campus settings. The scooter sharing segment, despite regulatory challenges in some markets, is expanding rapidly due to its low implementation costs and high user adoption rates.

By Solution: Payment Innovations Driving Seamless Mobility

Technology platforms lead this segment with 37.72% market share in 2025, serving as the foundational infrastructure that enables service integration and user interface. Meanwhile, payment and wallet solutions are experiencing the fastest growth at a 20.95% CAGR (2026-2031), as they address a critical friction point in the multimodal journey experience. The emergence of open-loop payment systems is particularly transformative, with PaymentGenes reporting that MaaS platforms implementing these systems see up to 40% higher user retention compared to those using closed-loop systems. These systems eliminate the need for users to preload funds or maintain multiple payment methods across different services.

Trip planning and navigation solutions continue to evolve with the integration of artificial intelligence that can predict disruptions and suggest alternatives in real-time. Connectivity and telematics solutions are enabling enhanced vehicle tracking and fleet management capabilities, while insurance and support services are expanding to address the unique needs of shared mobility users.

By Vehicle Type: Autonomous Pods Poised for Breakthrough Growth

Passenger cars maintain their dominance with 56.63% market share in 2025, reflecting the continued importance of ride-hailing and car-sharing services in the MaaS ecosystem. However, autonomous pods are projected to achieve the highest growth rate at 22.74% CAGR from 2026-2031, as they offer a compelling solution for controlled environments and first/last-mile connectivity. Research published in the IEEE Intelligent Transportation Systems Magazine demonstrates that autonomous modular vehicle technology can reduce operational costs by up to 40% compared to traditional fixed-route transit while improving service flexibility.These self-driving pods are particularly effective in campus environments, business parks, and planned communities where infrastructure can be optimized for autonomous operation.

Micro-mobility vehicles (e-bikes, e-scooters) continue to gain market share, particularly in dense urban areas where they offer superior maneuverability and parking convenience. Shuttles and buses are evolving with the introduction of on-demand routing algorithms that optimize occupancy rates and reduce wait times.

By Transportation Type: Public Sector Innovation Accelerating Growth

Private transportation options account for 61.34% of the MaaS market in 2025, driven by the flexibility and convenience they offer compared to fixed-route alternatives. However, public transportation is growing faster at 14.93% CAGR (2026-2031), as transit agencies increasingly embrace digital transformation and service integration. The American Public Transportation Association's study of European MaaS implementations reveals that public transit agencies that position themselves as the backbone of MaaS ecosystems can increase ridership by up to 25% while expanding their relevance beyond traditional service models. This growth is supported by significant investments in contactless payment systems, real-time tracking, and API development, enabling seamless integration with private mobility services.

By Business Model: Subscription Bundles Transforming Consumer Relationships

The pay-as-you-go model dominates with 67.25% market share in 2025, appealing to occasional users and those testing MaaS services. However, subscription bundles are experiencing dramatic growth at 23.88% CAGR (2026-2031), as they create predictable revenue streams for providers while offering cost savings and convenience for frequent users.

Peer-to-peer models are gaining traction in markets with high vehicle ownership costs, enabling private vehicle owners to monetize idle capacity. Ticketing-only aggregator models serve as entry-level MaaS offerings that focus on simplifying payment across multiple transit services without full service integration.

By Application: Last-Mile Logistics Emerging as Growth Engine

Personal mobility applications command 70.62% of the market in 2025, reflecting the primary focus of most MaaS platforms on moving people rather than goods. However, logistics and last-mile delivery applications are growing at a 20.53% CAGR (2026-2031), as e-commerce growth drives demand for efficient urban delivery solutions.

Business/corporate mobility applications are evolving beyond traditional corporate car services to encompass comprehensive mobility management platforms that support diverse employee transportation needs. The logistics and last-mile delivery segment is benefiting from innovations in route optimization and load consolidation that enable more efficient resource utilization, with particular growth in electric cargo bikes that can replace up to 30% of urban truck deliveries in suitable environments.

By End-User: Enterprise Adoption Driving B2B Growth

Individuals represent 77.46% of the MaaS market in 2025, as consumer-focused ride-hailing and micro-mobility services continue to dominate the landscape. However, the enterprise segment is growing faster at 16.96% CAGR (2026-2031), driven by corporate sustainability mandates and the desire to optimize employee mobility costs. Research from the University of Stockholm, based on 77 interviews with corporate MaaS users, reveals that well-implemented enterprise mobility programs can reduce corporate transportation costs by up to 30% while significantly improving employee satisfaction. These enterprise solutions typically include features like centralized billing, policy enforcement, and analytics that help organizations manage their mobility spending more effectively.

Government and municipal agencies are increasingly adopting MaaS platforms to enhance public service delivery and optimize resource allocation. The individual segment continues to evolve with more personalized offerings that adapt to user preferences and travel patterns over time. Enterprise adoption is particularly strong in sectors with distributed workforces or significant business travel requirements, with American Express Global Business Travel reporting that 67% of corporate travel managers are now incorporating MaaS options into their programs to support sustainability goals and enhance traveler experience

By Operating System: Emerging Platforms Challenging Duopoly

Android dominates the MaaS market with a 62.55% share in 2025, benefiting from its wider global adoption, particularly in emerging markets where MaaS growth is accelerating. However, alternative operating systems (HarmonyOS, KaiOS, Windows/PWAs) are growing fastest at 23.05% CAGR (2026-2031), as they address specific regional needs and overcome limitations of mainstream platforms. Progressive Web Apps (PWAs) are particularly significant in this growth, as they offer cross-platform compatibility without requiring dedicated app development for each operating system. This approach reduces development costs while ensuring broader accessibility across device types.

iOS maintains a significant market share, particularly in high-income regions where Apple devices are more prevalent. The "others" category, including emerging platforms like HarmonyOS, is gaining traction in markets where these systems have strong ecosystem support.The diversity of operating systems presents challenges for MaaS providers, who must ensure consistent user experiences across platforms. However, the rise of platform-agnostic development approaches is mitigating these challenges, with MaaS providers increasingly adopting responsive design principles that adapt to different screen sizes and operating systems while maintaining core functionality.

By Propulsion: Hydrogen Fuel-Cell Driving Zero-Emission Innovation

Electric propulsion leads with a 41.58% market share in 2025, driven by expanding charging infrastructure and favorable regulatory environments. However, hydrogen fuel-cell propulsion is experiencing the highest growth rate at 25.42% CAGR (2026-2031), as it addresses range and refueling time limitations of battery electric vehicles. Linde reports that countries are implementing ambitious hydrogen mobility targets. Japan plans to establish a supply chain producing 300,000 tons of hydrogen by 2030 to support 800,000 fuel-cell cars and 1,200 fuel-cell buses.

Internal combustion engine (ICE) vehicles still maintain significant market share, particularly in regions with limited electric charging infrastructure. Hybrid vehicles serve as a transitional technology, offering improved efficiency without requiring dedicated charging infrastructure. The emergence of hydrogen fuel-cell technology in the MaaS ecosystem is particularly significant for high-utilization applications like shuttle services and taxi fleets, where minimizing downtime is critical. UC Riverside's launch of the nation's only hydrogen-powered carshare program demonstrates the practical application of this technology in MaaS contexts, offering zero-emission mobility with refueling times comparable to conventional vehicles.

Geography Analysis

Asia-Pacific contributed 34.12% of the mobility as a service market share in 2025, capitalizing on dense cities, advanced digital payments, and coordinated infrastructure investments. China’s restriction on vehicle registrations in major metros nudges commuters toward shared platforms, while India’s expanding middle class embraces affordable ride-hailing. Singapore’s Smart Nation blueprint integrates public transit, micro-mobility, and unified payments into a single citizen app that exemplifies best-practice integration.

North America ranks second in market size. High ownership costs, renewed urban densification, and corporate travel sustainability mandates propel shared mobility growth, though state-by-state regulatory divergence slows national platform scale. Technology leadership in San Francisco, Austin, and Toronto supports early adoption of predictive analytics and autonomous pilots. Government incentives for electric vehicle fleets further strengthen the region’s mobility shift.

The Middle East and Africa presents the fastest regional expansion at 14.05% CAGR through 2031. Gulf Cooperation Council governments prioritize MaaS within smart-city megaprojects like NEOM and Expo City, allocating capital for autonomous shuttles and integrated fare systems. The Memorandum of Understanding between Abdul Latif Jameel and Joby Aviation to deploy up to 200 electric vertical take-off aircraft signals nascent aerial mobility ambition, augmenting ground-based services and reinforcing multimodal networks.

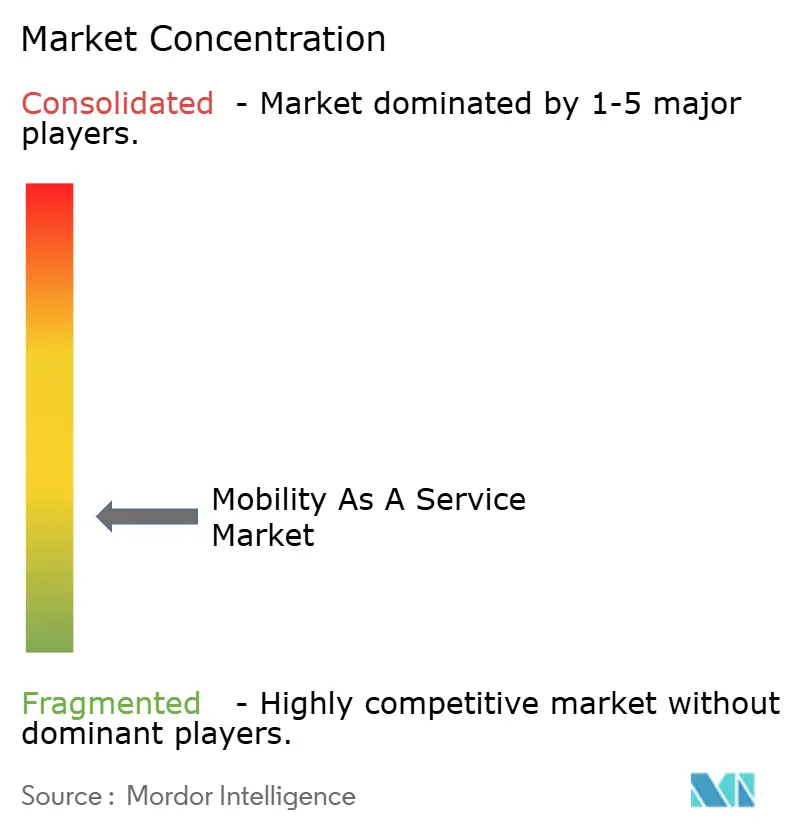

Competitive Landscape

Competition in the mobility as a service market is moderate and shifting from single-mode dominance to platform orchestration. Ride-hailing incumbents Uber and Lyft are integrating transit schedules and scooter rentals into their apps to broaden stickiness. Transit agencies are launching branded MaaS hubs that retain fare revenue while offering private add-ons. Strategic data alliances, such as Uber’s partnership with May Mobility for autonomous fleets, underscore the pivot toward technology synergy rather than outright asset ownership.

Industry white-space remains in niche verticals like healthcare patient transfers, tourism bundles, and rural demand-responsive services, where incumbents have limited reach. Data monetization is emerging as a standalone revenue stream as platforms analyze anonymized origin-destination flows for planners and retailers. Providers that master local regulatory navigation and maintain secure data governance are better positioned to secure long-term contracts with municipalities.

Artificial intelligence investment is accelerating for demand prediction, surge pricing calibration, and multimodal routing. Companies pursuing open API ecosystems invite third-party innovators to enrich trip-planning features, reinforcing network effects. Operators that align their roadmaps with public policy objectives decarbonization, accessibility, and equity gain preferential treatment in tender awards and pilot programs.

Mobility As A Service Industry Leaders

Uber Technologies Inc.

Didi Chuxing

Avis Budget Group

Enterprise Holdings, Inc.

The Hertz Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Uber and WeRide announced an expansion of their strategic partnership to bring autonomous vehicles to 15 additional cities globally over the next five years, focusing on markets outside the US and China. This initiative aims to enhance the availability of Robotaxi services through the Uber app, with Uber managing fleet operations, significantly advancing the integration of autonomous mobility into mainstream MaaS platforms.

- March 2025: The MaaS Alliance released a comprehensive white paper on Corporate Mobility as a Service (C-MaaS), outlining strategies and frameworks for integrating corporate mobility solutions into existing transport systems. This initiative aims to enhance the efficiency and sustainability of corporate transportation options, addressing the growing demand for environmentally responsible business travel solutions.

- March 2025: Enterprise Mobility announced a significant expansion in Southwest England, opening a new branch in St Austell, Cornwall, as part of an investment program responding to rising customer demand. The expansion includes the creation of eight new jobs and aims to provide more flexible vehicle access options, including the Enterprise Car Club, supporting diverse transport needs across urban and rural areas.

Global Mobility As A Service Market Report Scope

Mobility as a service integrates various forms of transportation services. It allows a variety of transportation services access, including public transport, ride-share, and rental.

The Mobility as a Service Market is Segmented by Service Type (Car, Bus, and Bike), Transportation Type (Public and Private), and Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The report offers market size and forecasts for Mobility as a Service in terms of value (USD billion) for all the above segments.

| Ride-Hailing |

| Car Sharing |

| Bike Sharing |

| Scooter Sharing |

| Bus Sharing |

| Technology Platform |

| Payment and Wallet |

| Trip Planning and Navigation |

| Connectivity and Telematics |

| Insurance and Support Services |

| Passenger Cars |

| Micro-Mobility Vehicles (E-Bikes, E-Scooters) |

| Shuttles and Buses |

| Autonomous Pods |

| Public |

| Private |

| Subscription (Mobility Bundles, Corporate Plans) |

| Pay-As-You-Go |

| Peer-to-Peer |

| Ticketing-Only Aggregator |

| Personal Mobility |

| Business/Corporate Mobility |

| Logistics and Last-Mile Delivery |

| Individuals |

| Enterprises |

| Government and Municipal Agencies |

| iOS | |

| Android | |

| Others | HarmonyOS |

| KaiOS | |

| Windows/PWAs |

| Internal Combustion Engine (ICE) |

| Electric |

| Hybrid |

| Hydrogen Fuel-Cell |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Ride-Hailing | |

| Car Sharing | ||

| Bike Sharing | ||

| Scooter Sharing | ||

| Bus Sharing | ||

| By Solution | Technology Platform | |

| Payment and Wallet | ||

| Trip Planning and Navigation | ||

| Connectivity and Telematics | ||

| Insurance and Support Services | ||

| By Vehicle Type | Passenger Cars | |

| Micro-Mobility Vehicles (E-Bikes, E-Scooters) | ||

| Shuttles and Buses | ||

| Autonomous Pods | ||

| By Transportation Type | Public | |

| Private | ||

| By Business Model | Subscription (Mobility Bundles, Corporate Plans) | |

| Pay-As-You-Go | ||

| Peer-to-Peer | ||

| Ticketing-Only Aggregator | ||

| By Application | Personal Mobility | |

| Business/Corporate Mobility | ||

| Logistics and Last-Mile Delivery | ||

| By End-User | Individuals | |

| Enterprises | ||

| Government and Municipal Agencies | ||

| By Operating System | iOS | |

| Android | ||

| Others | HarmonyOS | |

| KaiOS | ||

| Windows/PWAs | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Electric | ||

| Hybrid | ||

| Hydrogen Fuel-Cell | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the mobility-as-a-service market?

The mobility as a service market is valued at USD 374.55 billion in 2026 and is forecast to reach USD 716.3 billion by 2031, reflecting a 13.85% CAGR.

Which region is the largest contributor to MaaS revenue?

Asia-Pacific leads with 34.12% share in 2025, powered by rapid urbanization, smartphone penetration and extensive smart-city investments.

Which service type holds the biggest share today?

Ride-hailing commands 45.85% of 2025 revenue, supported by widespread driver networks and a large installed user base.

Why are subscription bundles gaining traction?

They deliver predictable revenue for providers and offer cost savings for frequent users, driving a 23.88% CAGR for the model from 2026-2031.

Page last updated on: