Anti-Reflective Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.98 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 6.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

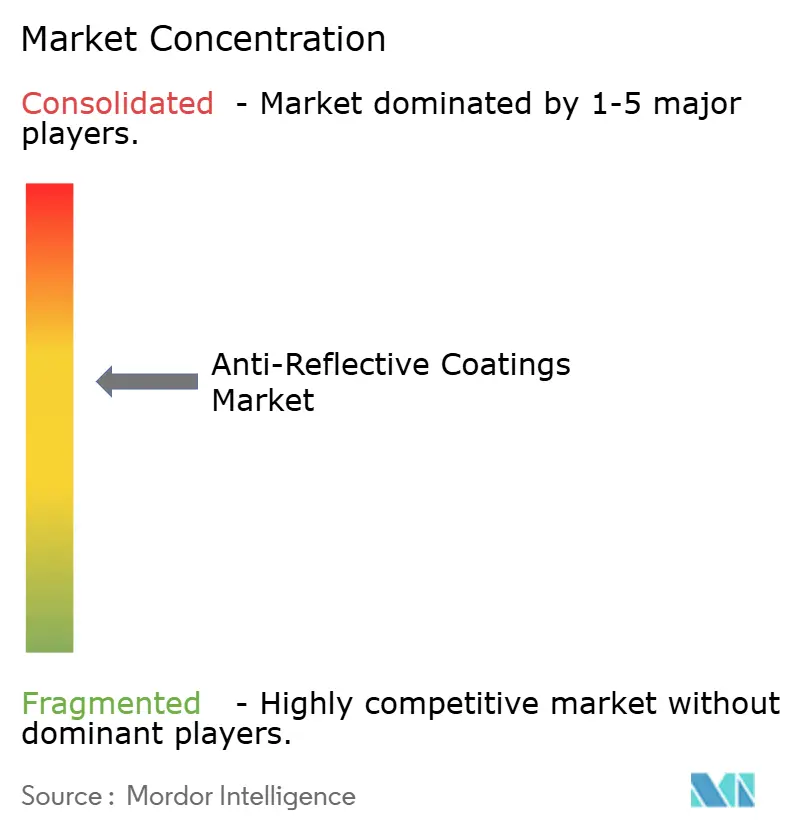

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Anti-Reflective Coatings Market Analysis by Mordor Intelligence

The anti-reflective coatings market size was valued at USD 5.63 billion in 2025 and estimated to grow from USD 5.98 billion in 2026 to reach USD 8.09 billion by 2031, at a CAGR of 6.26% during the forecast period (2026-2031). Demand is scaling because glare suppression and higher light transmission are essential in precision optics, photovoltaic glass, and advanced consumer displays. Manufacturers are intensifying investments in sputtering lines that deposit dense, low-defect films at high throughput, while solar developers are doubling coating area per module as bifacial architectures become mainstream. Regulatory pressure on fluorinated chemistries is reshaping raw-material portfolios, yet suppliers that qualify non-fluorinated stacks first are winning design slots. Competitive dynamics favor companies that combine deposition equipment scale with recipe expertise, enabling them to pivot between commodity glass and custom multilayer stacks without lengthy retooling.

Key Report Takeaways

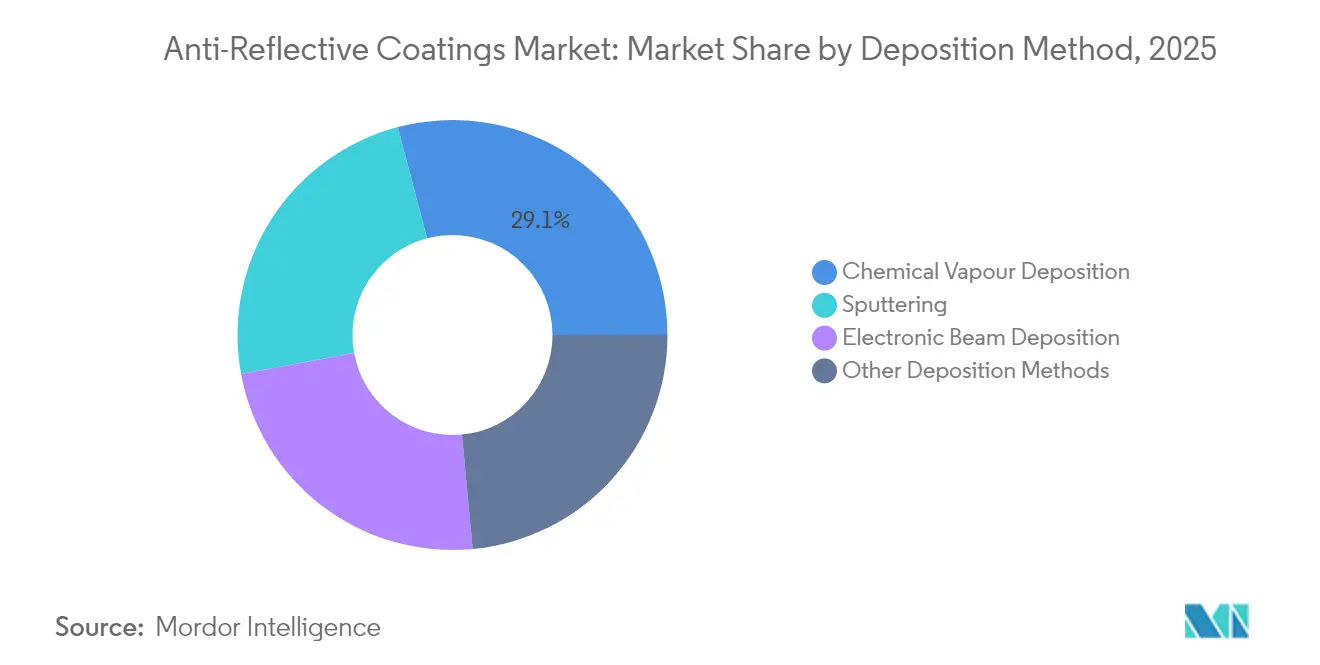

- By deposition method, chemical vapor deposition retained 29.10% revenue share in 2025; sputtering is forecast to register the fastest 6.47% CAGR through 2031.

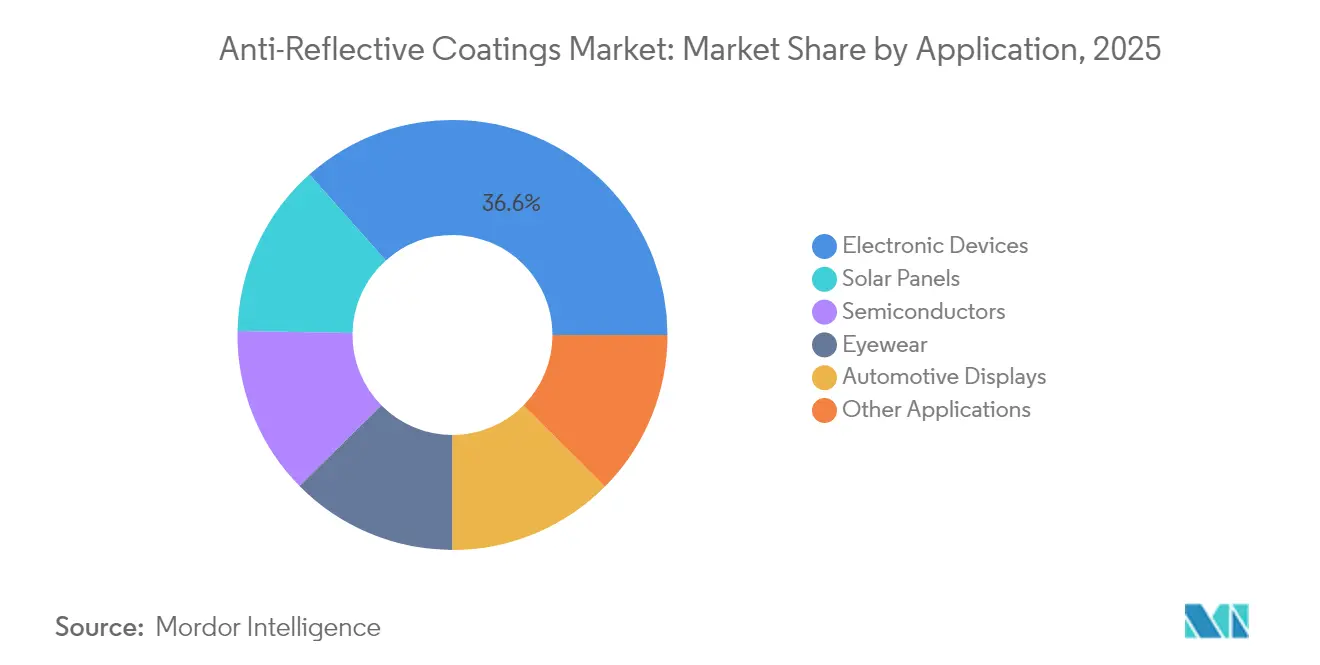

- By application, electronic devices led the anti-reflective coatings market with a 36.60% share in 2025; solar panels are expected to post the highest CAGR of 7.95% from 2026 to 2031.

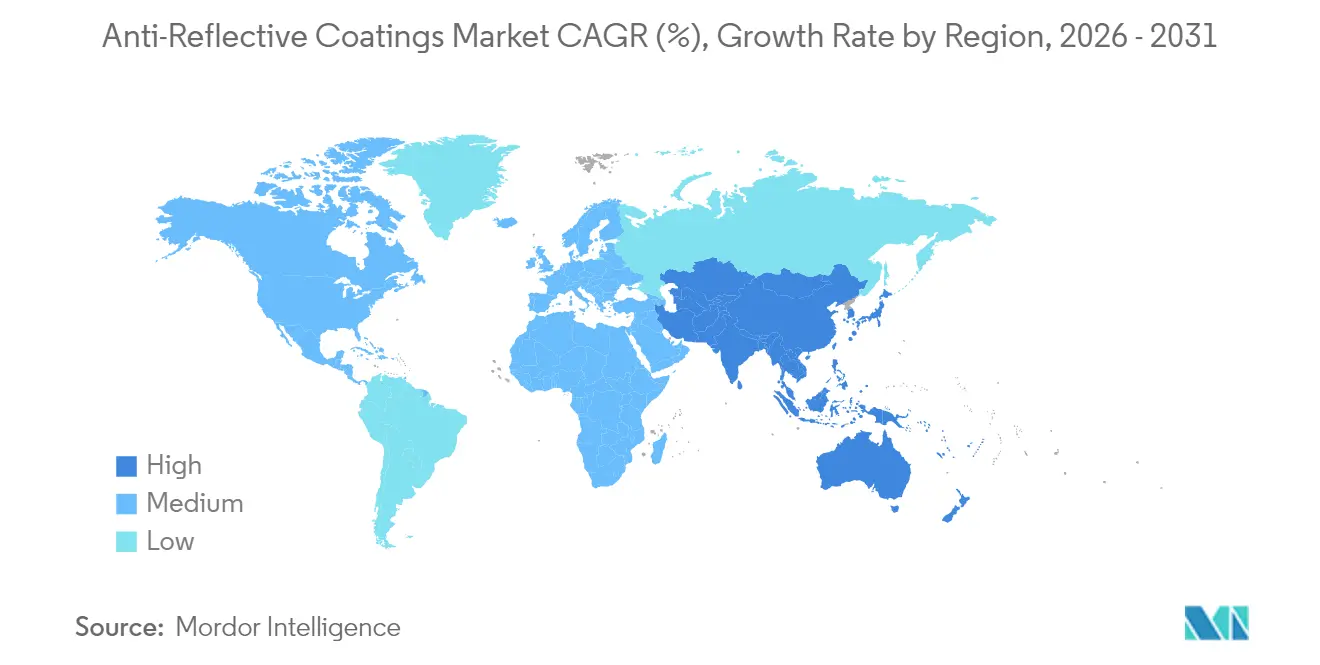

- By geography, the Asia-Pacific region accounted for a 34.10% revenue share in 2025 and is projected to expand at a 7.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-Reflective Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Augmented Reality (AR)/Virtual Reality (VR) and smart-glass adoption | +1.2% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| LiDAR optics in autonomous vehicles | +0.9% | North America, Europe, China | Medium term (2-4 years) |

| Rising demand from solar PV installations | +1.5% | Asia-Pacific, Middle East, Latin America | Long term (≥4 years) |

| Growth in ophthalmic eyewear prescriptions | +1.3% | Asia-Pacific, Middle-East and Africa | Medium Term (2-4 years) |

| Surge in high-resolution consumer displays | +1.3% | Global, concentrated in Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

AR/VR and Smart-Glass Adoption Driving Precision Optics Demand

Headset shipments reached 9.6 million units in 2024, and enterprise use cases, including training and remote collaboration, are broadening the addressable customer base. Optical stacks must now deliver average reflectance below 1% across the visible spectrum while maintaining color fidelity and scratch resistance. Zhejiang University researchers reported multilayer sol-gel stacks with a reflectance of less than 1% and a hardness exceeding 15 GPa, demonstrating durability suitable for consumer wearables[1]Optical Interference Coatings Conference Proceedings, “Sol-Gel Hard Coatings with Sub-1% Reflectance,” Zhejiang University, zju.edu.cn. Coating houses capable of tuning layer thickness in sub-nanometer steps are winning premium contracts, because waveguide combiners and pancake lenses require angle-specific suppression of ghost images. As content providers optimize for spatial computing, headset OEMs specify broadband, low-scatter coatings that withstand perspiration, temperature cycling, and frequent cleaning, creating a sustained demand for high-performance anti-reflective formulations.

LiDAR Optics Enabling Autonomous-Vehicle Perception

Automotive LiDAR modules operating at 905 nm and 940 nm utilize low-reflectance transmit and receive optics to extend their detection ranges beyond 200 m. A Nature Communications study demonstrated that vertical-cavity lasers can reach a peak output of 400 W with six-junction anti-reflective stacks that have survived 6,000 hours of high-temperature testing[2]Nature Communications, “High-Power VCSEL with Six-Junction Anti-Reflective Stack,” Nature Publishing Group, nature.com . As system prices drop toward the USD 100 target, Tier 1 suppliers demand coatings that boost signal-to-noise while passing IATF 16949 audits. Qualification hinges on sustaining performance between -40 °C and +105 °C, as well as withstanding road-salt corrosion. Vendors that can document low lot-to-lot variation in refractive index and thickness uniformity gain preferred-supplier status during platform rollouts scheduled for 2026-2027.

Solar PV Installations Amplifying Efficiency Gains

A 2025 IEEE paper quantified that broadband anti-reflective glass lifts silicon-module efficiency by 2.3%, reducing the levelized cost of energy over 25 years. The International Energy Agency projects bifacial panels to exceed 70% of global output by 2033, doubling the coating area per module. Developers in India, the Middle East, and Latin America deploy single-axis trackers with bifacial glass to increase capacity factors above 30%, driving the specification of dual-sided, abrasion-resistant coatings. Formulators are shifting from vacuum evaporation to plasma-enhanced chemical vapor deposition, which bonds tenaciously to glass and survives desert sandstorms and high UV flux.

Surge in High-Resolution Consumer Displays

OLED panels integrate the color filter atop the emissive layer, increasing surface reflectivity and necessitating aggressive anti-reflective treatment to preserve contrast in bright offices. Panel makers now require simultaneous anti-glare and anti-fingerprint attributes, forcing coating suppliers to develop multifunctional stacks that deliver <1.5% reflectance, <65 ° contact angle for fingerprints, and hardness >9H. Magnetron sputtering enables graded-index layers across Gen 8.7 glass, while atmospheric plasma top-coats add oleophobic functionality without extra thermal budget. Laptop and monitor brands plan to market “reflection-managed” SKUs as a premium upsell in 2026, suggesting steady demand for high-value stacks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and equipment cost | −0.8% | Global, particularly North America and Europe | Short term (≤2 years) |

| Stringent REACH and fluorochemicals regulation | −0.5% | Europe with global spillover | Medium term (2-4 years) |

| Durability issues on flexible polymer substrates | -0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production and Equipment Cost Constraining Entry

Electron-beam evaporators, magnetron sputtering chambers, and plasma reactors each cost upwards of USD 1 million and require Class 100 cleanroom facilities. Smaller coaters struggle to amortize capital outlays, driving consolidation around mega-fabs in China, South Korea, and the United States. Scheduled maintenance interrupts throughput, and skilled technicians command premium wages, further elevating fixed costs. The economics deter geographic diversification even when OEMs request local supply in Southeast Asia or Latin America, reinforcing the dominance of incumbent hubs.

REACH and Fluorochemicals Regulation Forcing Reformulation

The European Union is phasing out per- and polyfluoroalkyl substances, which have historically been favored for oleophobic top coats. Suppliers must now qualify non-fluorinated stacks that can pass salt-spray and UV-aging tests, a process that adds 9-12 months to product cycles. Parallel portfolios for EU and non-EU markets inflate inventory and compliance costs, thereby squeezing margins for independent firms. Vertically integrated conglomerates leverage in-house research and development teams, as well as regulatory expertise, to navigate this transition, thereby widening the capability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deposition Method: Sputtering Extends Throughput Advantage

Sputtering posted a 6.47% CAGR between 2026 and 2031, faster than the overall anti-reflective coatings market. Magnetron architectures deposit dense films at >10 nm per minute across Gen 8.7 glass, cutting takt time for display and photovoltaic fabs. The anti-reflective coatings market share for chemical vapor deposition remained 29.10% in 2025 because its superior conformality is indispensable for fiber-optic preforms and MEMS cavities. Hybrid production lines now combine plasma-enhanced chemical-vapor deposition for coverage on 3-D geometries with sputter sources for planar panels, maximizing equipment utilization. Ion-beam sputtering, though slower, enables atomic-scale smoothness essential for reticle blanks used in 193-nm lithography, where <0.2% residual reflectance prevents standing-wave defects. Process selection increasingly hinges on substrate thermal budget and whether plasma exposure is acceptable, prompting fabs to dual-source recipes to hedge risk.

Sputtering’s expansion is also driven by flexible-display programs that specify 300 mm-wide rolls of polymer film rather than rigid glass. Rotatable targets in roll-to-roll sputtering lines enable the switch in composition mid-run, allowing for graded-index stacks that balance broadband performance with mechanical resilience. Conversely, chemical vapor deposition gains share in automotive lidar lenses molded from heat-sensitive polymers, where plasma bombardment would warp the optical figure. Capital-equipment vendors forecast sputter cathode upgrades that increase power density by 15%, resulting in thinner dead zones at target ends and improved material utilization, which further reduces per-square-meter coating cost.

By Application: Solar Panels Surge Ahead of Consumer Electronics

Electronic devices generated 36.60% of 2025 revenue; however, growth is flattening as smartphone replacement cycles extend to 40 months in mature markets. Solar panels, in contrast, are on track for the highest 7.95% CAGR because each bifacial module requires coatings on both faces, and new gigawatt-scale plants deploy glass sizes up to 2.6 m × 1.4 m. The anti-reflective coatings market size for photovoltaic glass is projected to surpass USD 2.32 billion by 2031, as governments in India and Brazil subsidize high-efficiency modules to accelerate decarbonization. Eyewear remains a stable niche—EssilorLuxottica integrated anti-reflective treatments into most of its 559 million prescription lenses in 2024. Automotive displays require coatings that withstand sunlight and thermal cycling; shipments of vehicle center-stack screens are expected to reach approximately 720 million units per year, and head-up display glass is growing at double-digit rates as automakers adopt augmented-reality overlays.

Semiconductor photolithography presents a high-margin pocket where bottom anti-reflective coatings suppress notching at sub-7 nm nodes. Although its volume share is modest, unit price per square centimeter is an order of magnitude above that for architectural glass. Medical-imaging optics, aerospace visors, and telecom filters round out the demand portfolio, each with rigorous reliability requirements that favor specialty coaters able to certify multilayer stacks for decades of service. Suppliers that pivot capacity toward solar and automotive optics while retaining small-batch agility for semiconductor tools are positioned to outgrow peers.

Geography Analysis

The Asia-Pacific region generated 34.10% of global revenue in 2025 and is projected to accelerate at a 7.62% CAGR through 2031, outpacing the average growth rate of the anti-reflective coatings market. China’s Gen 10.5 LCD and OLED fabs in Guangdong and Jiangsu concentrate demand for large-area sputtering targets, while South Korea’s premium smartphone-panel makers dictate ultralow-defect requirements. Japan’s optical-glass heritage supports demand for camera-module and eyewear coatings, and India’s solar assembly boom adds dual-sided coated glass volumes. Local content rules are nudging multinational vendors to site sputter lines near Vietnam and Malaysia, even though capital intensity remains a barrier.

North America captures a smaller volume but commands higher average selling prices because aerospace and defense programs specify low-scatter, broadband stacks and meticulous traceability. Silicon Valley’s AR headset developers contract for brief production runs that require pattern-specific coatings applied with photomasks, an area where nimble U.S. coaters maintain an edge. Mexico benefits from its proximity to automotive assembly, but most large-area coatings still ship from Asia due to the established scale. Canada’s demand centers on lidar sensors for mining and forestry automation, though absolute volumes remain modest.

Europe’s market is shaped by REACH regulation, which is forcing coating formulators to qualify PFAS-free alternatives ahead of other regions. Germany’s premium vehicle makers specify anti-reflective glass for head-up displays that integrate polarization control, raising the performance bar. Utility-scale solar in Spain and Greece is adopting bifacial modules, yet much of the coated glass still arrives from Asia, prompting EU initiatives to localize supply by 2027. Eastern Europe’s optics clusters in Poland and the Czech Republic specialize in defense lenses, providing a small but stable demand base.

Middle East and Africa remain nascent: Saudi Arabia’s gigawatt solar tenders and South Africa’s mining-helmet visor upgrades are the primary drivers, usually served through imports given the limited cleanroom infrastructure. Latin America is gathering momentum—Brazil and Chile are expanding solar capacity and specifying anti-reflective glass to lift yield in high-irradiance zones—yet coating application still occurs offshore, leaving room for regional investments should consistent order pipelines materialize.

Competitive Landscape

The anti-reflective coatings market is moderately consolidated, with large vertically integrated glass and chemicals companies sitting alongside niche optical-service bureaus. AGC and Guardian dominate the commodity glass coatings market through economies of scale and a vertically integrated float-glass supply. Strategic patterns center on technology differentiation: ion-beam sputtering achieves <0.1% scatter for semiconductor reticles, plasma-enhanced chemical-vapor deposition offers conformal coverage in MEMS cavities, and atomic-layer deposition delivers sub-10 nm precision for emerging nano-photonics. Cross-licensing of target materials with equipment vendors accelerates recipe rollouts, while backward integration into substrate manufacturing ensures a secure glass supply in tight markets. White space persists in curved automotive head-up display glass, where coatings must maintain broadband suppression without introducing birefringence, and in foldable OLED phones, where flexible substrates necessitate low-temperature, crack-resistant stacks. Regulatory compliance is escalating: ISO 14001 environmental management, ISO 50001 energy management, and IATF 16949 automotive quality are now baseline requirements for Tier 1 approval in Europe and North America. Smaller independents lacking the scale to absorb audit costs are entering partnerships or being acquired.

Anti-Reflective Coatings Industry Leaders

-

EssilorLuxottica

-

HOYA VISION CARE COMPANY (HOYA Corporation)

-

Zeiss International

-

PPG Industries

-

AGC Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ZEISS expanded its premium-tier lens coating portfolio with the launch of DuraVision Gold UV. This advanced coating enhances lens performance by offering superior cleanability, durability, and optical clarity. Featuring a refined golden reflex hue, it delivers a sophisticated aesthetic appeal. For eye care professionals, this innovation creates new opportunities to upsell and effectively meet the growing demand for personalized eyewear solutions.

- November 2024: POLYRISE announced the launch of a patented high-performance anti-reflective coating designed to address the specific requirements of the automotive, optics, and photonics industries. This innovation utilizes SAMES’ advanced spray technology, delivering superior quality and enhanced industrial productivity, reinforcing POLYRISE's commitment to technological advancement and industry excellence.

Global Anti-Reflective Coatings Market Report Scope

| Chemical Vapour Deposition |

| Electronic Beam Deposition |

| Sputtering |

| Other Deposition Methods |

| Semiconductors |

| Electronic Devices |

| Eyewear |

| Solar Panels |

| Automotive Displays |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Deposition Method | Chemical Vapour Deposition | |

| Electronic Beam Deposition | ||

| Sputtering | ||

| Other Deposition Methods | ||

| By Application | Semiconductors | |

| Electronic Devices | ||

| Eyewear | ||

| Solar Panels | ||

| Automotive Displays | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the anti-reflective coatings market in 2026?

It stands at USD 5.98 billion and is on track to reach USD 8.09 billion by 2031, reflecting a 6.26% CAGR.

Which segment grows fastest within anti-reflective coatings?

Solar panels lead with a 7.95% CAGR through 2031 as bifacial modules double the coated area per panel.

Why is sputtering gaining share against chemical vapor deposition?

Magnetron sputtering deposits dense films quickly across large glass sizes, trimming takt time and lowering cost per square meter.

How will EU REACH rules impact coating formulations?

Suppliers are phasing out fluorochemicals, investing in PFAS-free layers that still deliver oleophobic and anti-smudge performance.

Which regions contribute the highest growth?

Asia-Pacific expands fastest at 7.62% CAGR, driven by display fabs in China and solar deployments across India and Southeast Asia.

What is the outlook for AR/VR headsets in coating demand?

Rising enterprise adoption pushes optical-stack requirements for reflectance below 1%, sustaining premium demand for precision multilayer coatings.

Page last updated on: