Optical Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.99 Billion |

| Market Size (2031) | USD 33.71 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

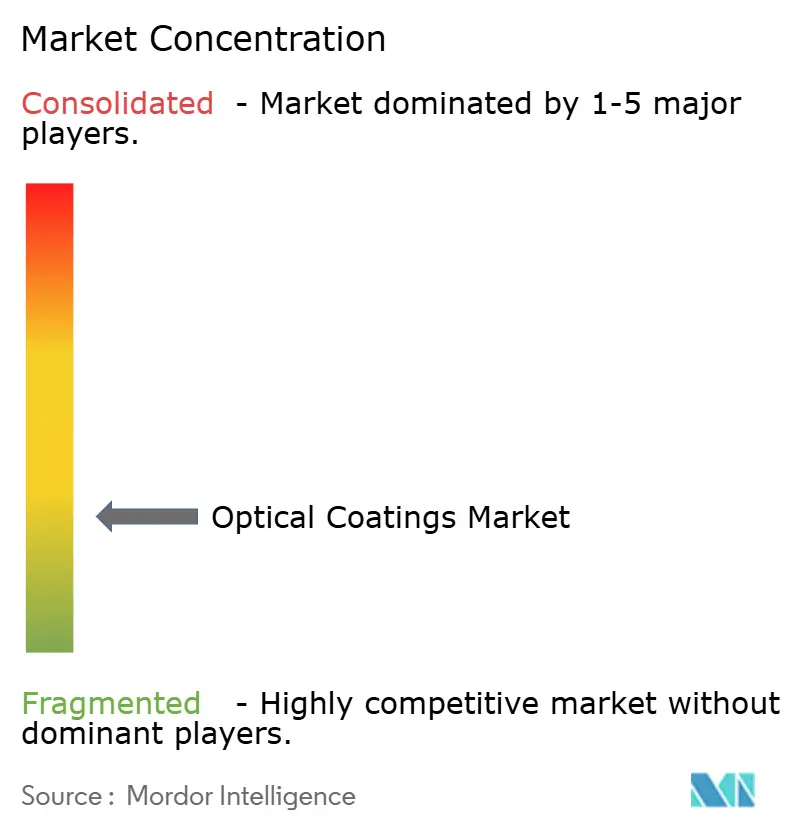

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Coatings Market Analysis by Mordor Intelligence

The Optical Coatings Market size was valued at USD 23.54 billion in 2025 and is estimated to grow from USD 24.99 billion in 2026 to reach USD 33.71 billion by 2031, at a CAGR of 6.17% during the forecast period (2026-2031). Demand rises as the industry pivots from commodity thin films to engineered stacks that unlock emerging photonics, including bifacial solar modules, metasurface waveguides for augmented-reality headsets, and ultra-low-loss filters for 6G photonic circuits. Anti-reflective coatings hold 37.94% of 2025 revenue, and their 6.46% growth outlook positions them as both the largest and fastest advancing product category. Chemical vapor deposition (CVD) retains a 41.88% share thanks to scalability on Gen 10.5 glass, yet ion-beam sputtering is set to accelerate at 6.81% as aerospace and defense programs demand sub-nanometer precision. Asia-Pacific contributes 34.78% of 2025 sales and expands at 8.11% as China’s display-fab build-out and South Korea’s OLED leadership create regional equipment hubs, while North America and Europe focus on high-value niches such as 6G photonic integrated circuits and automotive LiDAR optics.

Key Report Takeaways

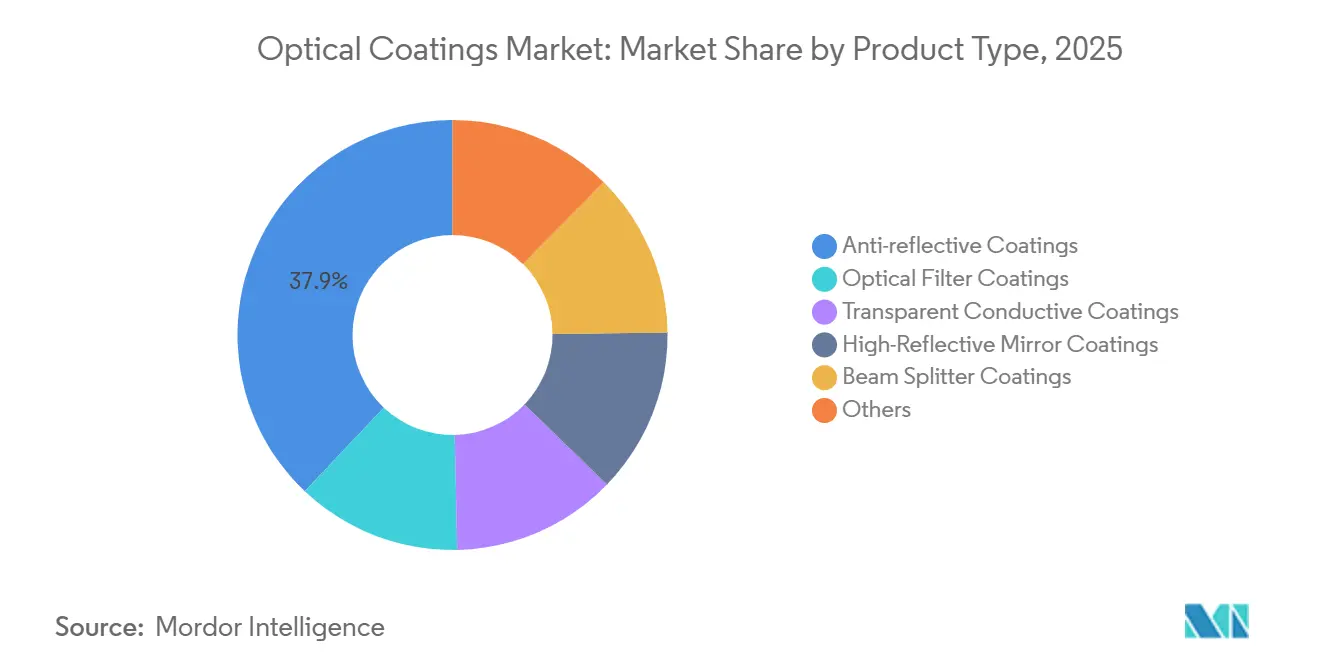

- By product type, anti-reflective coatings led with 37.94% optical coatings market share in 2025; the same segment is forecast to expand at a 6.46% CAGR through 2031.

- By deposition technology, chemical vapor deposition accounted for 41.88% of the optical coatings market size in 2025, whereas ion-beam sputtering records the highest projected CAGR at 6.81% through 2031.

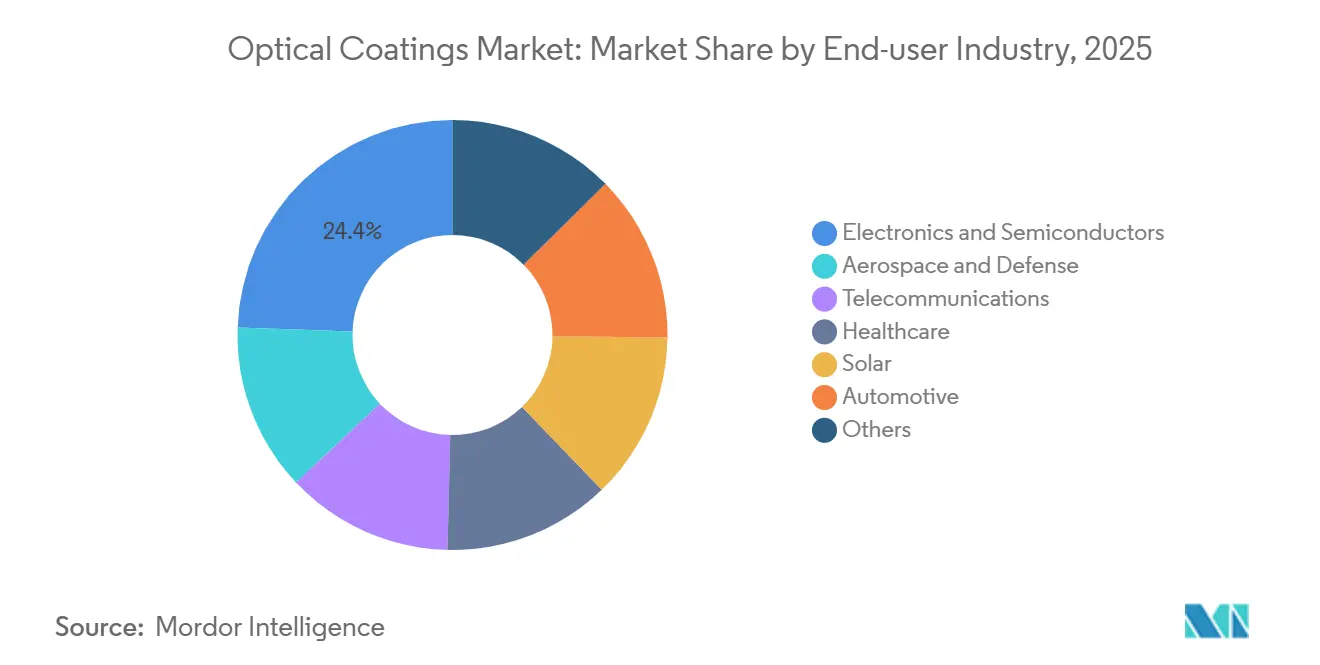

- By end-user, electronics and semiconductors held 24.44% of the 2025 optical coatings market share, while aerospace and defense is forecast to grow fastest at 7.64% to 2031.

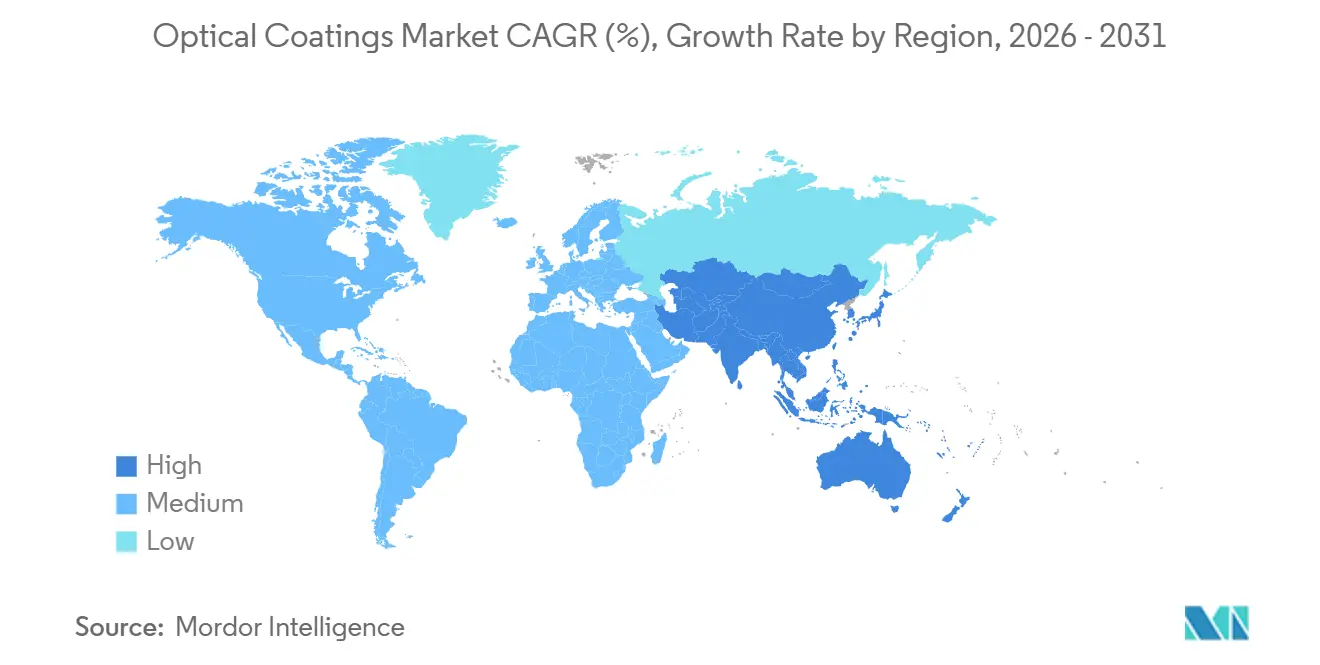

- By geography, Asia-Pacific captured 34.78% of revenue in 2025 and is advancing at an 8.11% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Optical Coatings Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solar-grade anti-reflective films slash LCOE in bifacial PV modules | +1.2% | Global, with concentration in APAC (China, India) and emerging markets | Medium term (2–4 years) |

| AR/HR meta-coatings enabling AR/VR waveguides for consumer headsets | +0.9% | North America and EU for Research and Development; APAC for volume manufacturing | Short term (≤ 2 years) |

| 6G-ready ultra-low-loss filter stacks for photonic integrated circuits | +0.7% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Military hyperspectral imaging demand for broad-band filter coatings | +1.1% | North America, EU, select Middle East nations | Medium term (2–4 years) |

| Mainstream demand surge from OLED/µLED displays | +1.4% | APAC core (China, South Korea), spill-over to North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Solar-Grade Anti-Reflective Films Slash LCOE in Bifacial PV Modules

Bifacial photovoltaic modules equipped with dual-sided anti-reflective stacks now exceed 25% cell efficiency, pushing the levelized cost of energy below USD 0.03 per kilowatt-hour in high-irradiance zones. Tongwei Solar’s 25.5% tunnel-oxide passivated-contact cell, announced in 2025, attributed 0.8 percentage points of gain to optimized front- and rear-surface coatings that minimize reflection from 300 to 1,200 nanometers. Higher output cuts balance-of-system costs, prompting India’s National Institute of Solar Energy to note 18% greater annual yield for bifacial arrays in desert climates. Module manufacturers are internalizing coating steps to secure stack recipes, tightening supply for independent coaters, and favoring players that amortize plasma-enhanced CVD capital across gigawatt-class lines.

AR/HR Meta-Coatings Enabling AR/VR Waveguides for Consumer Headsets

Metasurface waveguides replace bulky multilayer stacks with sub-wavelength nanostructures that slim optical engines below 5 millimeters. Meta Platforms documented a 92%-efficient titanium-dioxide design in 2024[1]Meta Platforms, “Holographic Waveguide Metasurfaces,” nature.com, and Samsung Research followed with a holographic variant in 2025, delivering a 50-degree field of view compatible with eyeglasses. Brands that secure meta-coating intellectual property and align with ion-beam sputtering specialists will control forthcoming consumer-electronics bill of materials, whereas legacy AR vendors face obsolescence unless they invest in nano-fabrication capacity.

6G-Ready Ultra-Low-Loss Filter Stacks for Photonic Integrated Circuits

Telecom operators preparing for 6G trials stipulate insertion loss below 0.1 decibel per centimeter on silicon-nitride waveguides, a target that traditional sputtering fails to meet. Nokia Bell Labs validated coherent transmission at 300 gigahertz using such coatings in 2025, while Ericsson highlighted ±2-nanometer stack-thickness uniformity as the bottleneck for terahertz-band filters. Ion-beam sputtering and ALD deliver the precision but entail capital-intensive, low-throughput tools, igniting regional races; Japan’s AIST and South Korea’s ETRI both aim for 10-wafer-per-hour ALD lines by 2027.

Military Hyperspectral Imaging Demand for Broad-Band Filter Coatings

Defense programs specify coatings that pass narrow spectral bands across 400–2,500 nanometers with out-of-band rejection above 10⁴. The US Navy’s 2024 SBIR call required salt-fog-resistant filters enduring -40 to 70 °C cycles[2]U.S. Navy, “SBIR Topic N241-105,” navy.mil. Army Research Laboratory tests in 2025 showed ion-beam-sputtered coatings on germanium remaining stable after 500 thermal cycles, whereas plasma-sputtered versions drifted 12 nanometers. NATO’s 2024 standard fixed ±1-nanometer uniformity across 100-millimeter apertures, effectively excluding CVD. Vendors that balance high-value, low-volume defense demand with lower-spec commercial sensors will defend margins.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Indium-tin-oxide supply vulnerability | -0.8% | Global, acute in North America and EU due to import dependence | Short term (≤ 2 years) |

| Stricter PFAS bans hitting fluoride-based hard coats | -0.5% | EU, North America; limited impact in APAC | Medium term (2–4 years) |

| CAPEX intensity of atomic-layer deposition lines | -0.6% | Global, most acute in regions with limited fab subsidies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Indium-Tin-Oxide Supply Vulnerability

China controls 60% of refined indium, and the United States imported 100% of its need in 2024 according to the US Geological Survey. A 35% price jump in 2023–2024 reflects tightened export quotas, while recycling captures less than 15% of scrap. Display makers fund alternatives such as graphene and silver nanowires, yet none match ITO’s conductivity-transparency balance at mass scale. Samsung Display allocated USD 120 million to ITO-free research, but commercial release is unlikely before 2028, leaving coaters exposed to raw-material inflation.

Stricter PFAS Bans Hitting Fluoride-Based Hard Coats

The US Environmental Protection Agency labelled select PFAS hazardous substances in April 2024, and the European Chemicals Agency added four to its REACH candidate list the same year. Replacements such as siloxanes exhibit 30% higher Taber-wear indices, lowering smartphone-screen durability. Corning is qualifying PFAS-free formulations for Gorilla Glass but expects 12–18 months of additional customer testing, disproportionately burdening small coating houses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Anti-Reflective Coatings Lead Across Solar and Display

Anti-reflective coatings commanded 37.94% of revenue in 2025, and the segment is projected to expand at a 6.46% CAGR through 2031. Dual-sided stacks on bifacial solar glass and low-reflectance layers on OLED panels account for nearly two-thirds of consumption. Transparent conductive coatings, hindered by indium constraints, still post mid-single-digit growth as microLED head-up displays and wearables mature. High-reflective mirror coatings remain specialized for laser systems, while beam splitters support machine-vision cameras in industrial automation. Specialty filters servicing biophotonics and quantum optics sustain gross margins above 50%.

Momentum is shifting from broadband AR stacks toward wavelength-selective metasurface films that reduce reflection below 0.5% with sub-10-nanometer thickness. Samsung Research unveiled a flexible variant in 2024, and Tokyo Electron is scaling nano-imprint tools that pattern 300-millimeter wafers at 20-per-hour throughput. Coaters tied solely to CVD or sputtering lack sub-50-nanometer pattern capabilities and risk commoditization as Asian fabs internalize multilayer recipes.

By Deposition Technology: CVD Dominates, Ion-Beam Sputtering Gains in Precision Niches

CVD generated 41.88% of 2025 revenue, underpinned by uniform deposition across 3-meter glass for OLED encapsulation. Plasma-enhanced CVD achieves ±2% thickness control, serving Gen 10.5 lines at BOE and LG Display. Ion-beam sputtering, while capturing only 14% of sales, delivers sub-nanometer roughness and is projected to expand at 6.81% through 2031, led by defense lasers and hyperspectral imaging. Plasma sputtering fills automotive and consumer-electronics needs where speed outweighs atomic-scale precision, whereas ALD remains indispensable for flexible OLED barriers and high-aspect photonics structures.

Sub-wavelength structured surfaces threaten conventional stacks by eliminating vacuum films. Canon’s 2025 300-millimeter nano-imprint tool achieves 10-wafer-per-hour throughput. If metasurfaces displace layers in foldable screens and AR headsets, value will migrate from deposition to lithography-etch toolmakers, pressing coaters to diversify or license metasurface IP.

By End-User Industry: Electronics Lead, Aerospace Grows Fastest

Electronics and semiconductors consumed 24.44% of optical coatings in 2025, driven by OLED, smartphone cameras, and laptop displays. Samsung Display and LG Display alone processed 18,000 metric tons of ITO in 2024, equal to 40% of global indium refining. Aerospace and defense will outpace all sectors at a 7.64% CAGR as hyperspectral imaging and directed-energy optics demand coatings with 10⁵ out-of-band rejection. Solar contributes through bifacial modules, while automotive shifts from anti-glare cabin displays toward LiDAR and AR windshields requiring low-loss coatings at 905 and 1,550 nanometers.

Automotive advanced driver-assistance systems integrate eight cameras and four LiDAR sensors per vehicle, each calling for multilayer AR stacks tuned to infrared bands. Continental’s 2024 roadmap and Bosch’s 2025 partnership with Zeiss target less than 0.5% reflection for all-weather range. Healthcare optics and telecom photonics are advancing, with Olympus and Karl Storz applying ALD anti-fog layers on endoscopes, while Nokia concentrates on 6G-ready filter stacks.

Geography Analysis

Asia-Pacific held 34.78% of 2025 revenue and is advancing at an 8.11% CAGR to 2031, adding more than USD 3 billion to the optical coatings market size during the period. China, South Korea, and Japan anchor regional dominance through OLED production, solar module assembly, and precision metrology toolmaking. India’s National Institute of Solar Energy reported that locally coated bifacial glass trims module costs by USD 0.02 per watt, stimulating domestic coating-line investment. Southeast Asia emerges as a secondary hub as brands diversify away from China, although limited semiconductor infrastructure restrains photonic-grade growth.

Military optics and photonic integrated circuits propel North America's optical coatings market growth. The US Department of Defense allocated USD 1.8 billion in 2024 for electro-optical and infrared systems, driving demand for ion-beam coatings that survive harsh environments. Materion and Coherent leverage classified-program credentials to secure contracts, while Canada’s photonics cluster leverages National Research Council grants for coating development. Mexico attracts automotive-coating projects such as PPG’s USD 45 million expansion in Tlaxcala, serving Ford and GM plants.

Europe accounts for a significant share of the global optical coatings market as Germany, France, and the United Kingdom dominate automotive and industrial optics. Schott and Zeiss supply PFAS-free conformal layers following the EU’s tightened chemical regulations. The Middle East and Africa are witnessing rising demand for optical coatings due to solar mega-projects like Saudi Arabia’s NEOM, which incorporates 5 gigawatts of bifacial modules requiring dual-side coatings.

Competitive Landscape

The global optical coatings market is higly fragmented. Vertical integration by display giants BOE, Samsung Display, and LG Display siphons margin from merchant suppliers. Technology adoption is decisive. Firms that master ion-beam and ALD for aerospace yet maintain CVD throughput for consumer electronics hold pricing power, whereas single-technology specialists face commoditization. Regulatory leadership offers another edge: European suppliers achieving PFAS-free coatings ahead of 2027 REACH deadlines secure automotive contracts, while laggards risk withdrawals. Mergers and acquisitions are expected as larger players acquire process IP and customer bases, leaving niche specialists and captive lines to dominate by 2030.

Optical Coatings Industry Leaders

Zeiss International

Materion Corporation

PPG Industries Inc.

DuPont

VIAVI Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: PPG Industries announced a USD 45 million expansion of its Tlaxcala, Mexico facility to supply anti-reflective coatings for automotive head-up displays and camera lenses to Ford, GM, and Stellantis.

- June 2024: Materion Corporation secured a multi-year, USD 50 million contract with a U.S. defense prime to deliver ion-beam-sputtered coatings for airborne and space hyperspectral sensors.

Global Optical Coatings Market Report Scope

Optical coatings are ultra-thin layers of materials, such as oxides or metals, applied to optical components like lenses and mirrors. These coatings optimize light interaction by reducing or enhancing reflection, filtering wavelengths, or splitting beams, thereby improving the functionality of products ranging from eyeglasses to lasers.

The optical coating market is segmented by product type, deposition technology, end-user industry, and geography. By product type, the market is segmented into optical filter coatings, anti-reflective coatings, transparent conductive coatings, high-reflective mirror coatings, beam splitter coatings, and others. By deposition technology, the market is segmented into chemical vapor deposition, ion-beam sputtering, plasma sputtering, atomic layer deposition, and sub-wavelength structured surfaces. By end-user industry, the market is segmented into aerospace and defense, electronics and semiconductors, telecommunications, healthcare, solar, automotive, and others. The report also covers the market size and forecasts for the optical coatings market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Optical Filter Coatings |

| Anti-reflective Coatings |

| Transparent Conductive Coatings |

| High-Reflective Mirror Coatings |

| Beam Splitter Coatings |

| Others |

| Chemical Vapor Deposition |

| Ion-beam Sputtering |

| Plasma Sputtering |

| Atomic Layer Deposition |

| Sub-wavelength Structured Surfaces |

| Aerospace and Defense |

| Electronics and Semiconductors |

| Telecommunications |

| Healthcare |

| Solar |

| Automotive |

| Others |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Optical Filter Coatings | |

| Anti-reflective Coatings | ||

| Transparent Conductive Coatings | ||

| High-Reflective Mirror Coatings | ||

| Beam Splitter Coatings | ||

| Others | ||

| By Deposition Technology | Chemical Vapor Deposition | |

| Ion-beam Sputtering | ||

| Plasma Sputtering | ||

| Atomic Layer Deposition | ||

| Sub-wavelength Structured Surfaces | ||

| By End-user Industry | Aerospace and Defense | |

| Electronics and Semiconductors | ||

| Telecommunications | ||

| Healthcare | ||

| Solar | ||

| Automotive | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the optical coatings market in 2026?

The optical coatings market size is USD 24.99 billion in 2026, with a forecast to reach USD 33.71 billion by 2031.

Which product segment contributes the most revenue?

Anti-reflective coatings dominate, holding 37.94% of 2025 revenue and projected to expand at a 6.46% CAGR.

Which deposition technology is growing fastest?

Ion-beam sputtering shows the highest growth outlook at 6.81% due to aerospace and defense demand for sub-nanometer precision.

Why is Asia-Pacific outpacing other regions?

Concentrated OLED production, solar module assembly, and semiconductor packaging give Asia-Pacific a 34.78% share and 8.11% CAGR through 2031.

What is the main supply-chain risk for coaters?

Dependence on indium-tin-oxide, with China controlling 60% of refining and the United States importing 100% of its needs, exposes the sector to price spikes and geopolitical risk.

How strict are upcoming PFAS regulations?

The U.S. EPA labeled certain PFAS hazardous in 2024, and the EU plans broad restrictions by 2027, prompting coaters to reformulate hard-coat chemistries.

Page last updated on: