Modular Laboratory Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

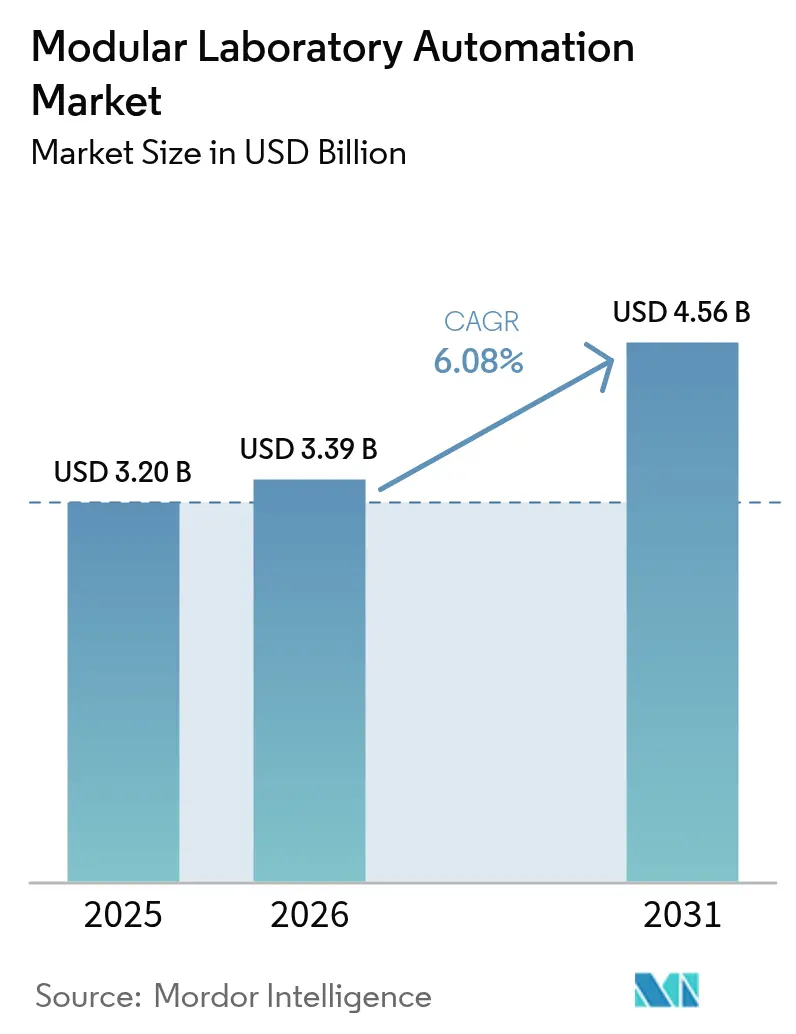

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 4.56 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

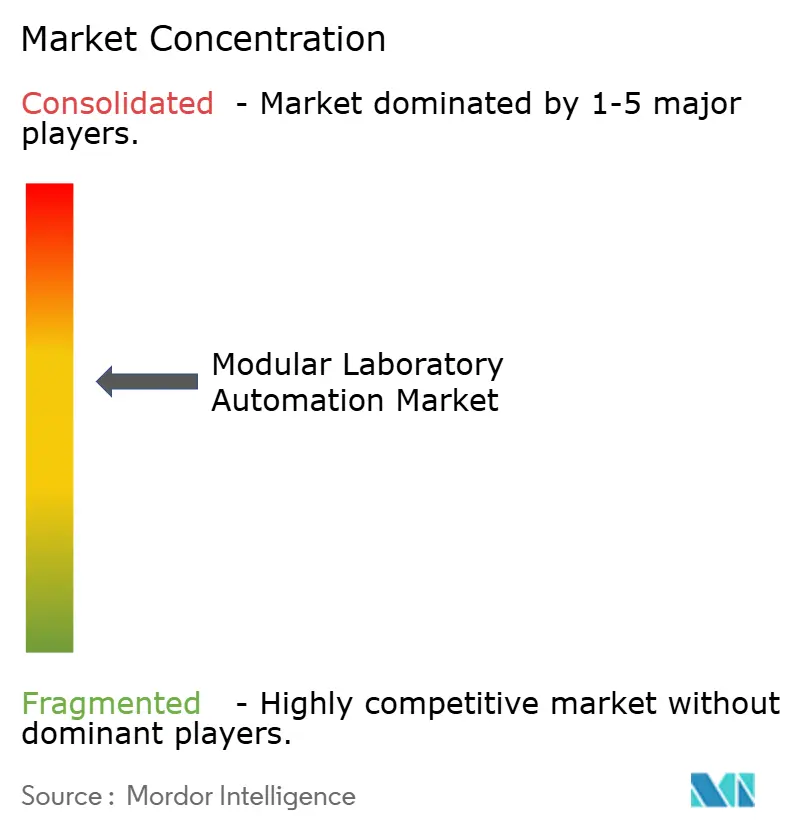

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modular Laboratory Automation Market Analysis by Mordor Intelligence

The modular laboratory automation market size was valued at USD 3.2 billion in 2025 and estimated to grow from USD 3.39 billion in 2026 to reach USD 4.56 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031). Heightened regulatory scrutiny, a shrinking laboratory workforce, and the growing need for reproducible data position automated, network-ready work cells as critical infrastructure for life-science innovation. Suppliers now bundle artificial-intelligence software with robotics, allowing laboratories to standardize protocols, capture complete audit trails, and shorten testing cycles. Pharmaceutical manufacturers are accelerating adoption to satisfy the EU GMP Annex 1 contamination-control requirements, while hospital networks favour modular deployments that scale distributed testing without lengthy construction projects. In parallel, federal support such as the NIH MATChS program signals that laboratory automation is no longer discretionary but a strategic enabler for biomedical research.

Key Report Takeaways

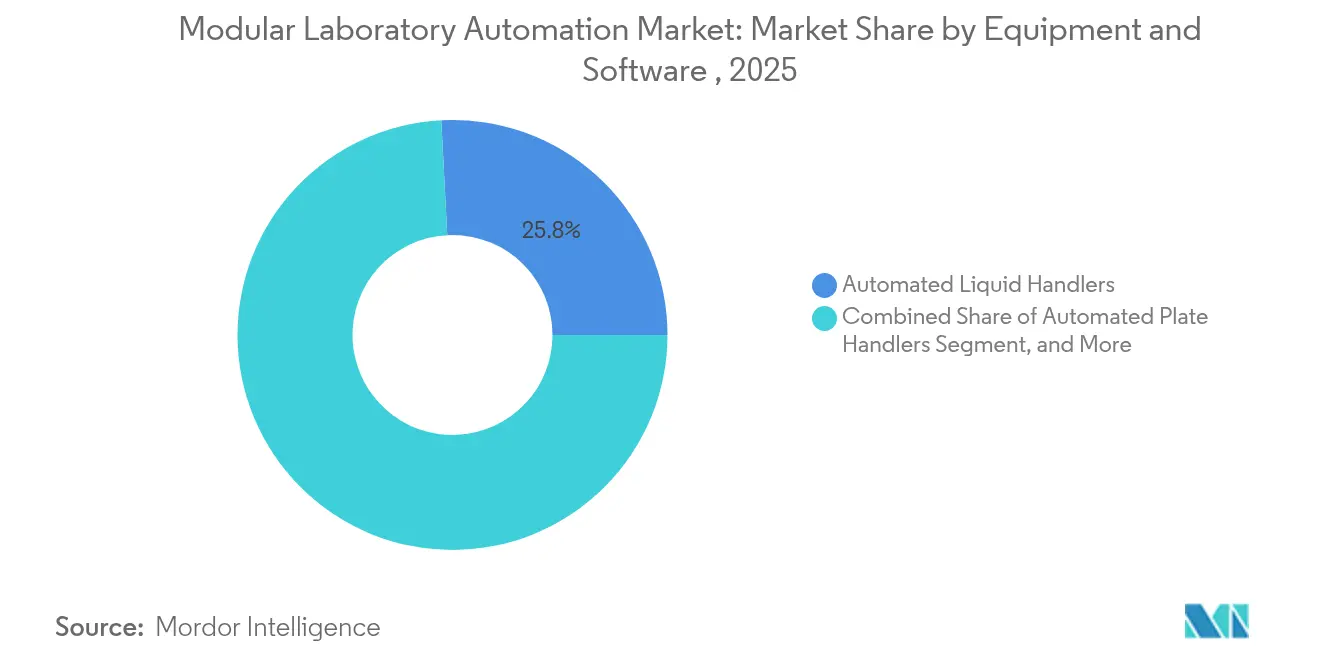

- By equipment & software, automated liquid handlers accounted for 25.83% of the modular laboratory automation market share in 2025; automated storage & retrieval systems are on track for a 6.94% CAGR through 2031.

- By field of application, clinical diagnostics held 28.12% revenue share in 2025, while cell & gene therapy workflows are projected to expand at a 9.21% CAGR to 2031.

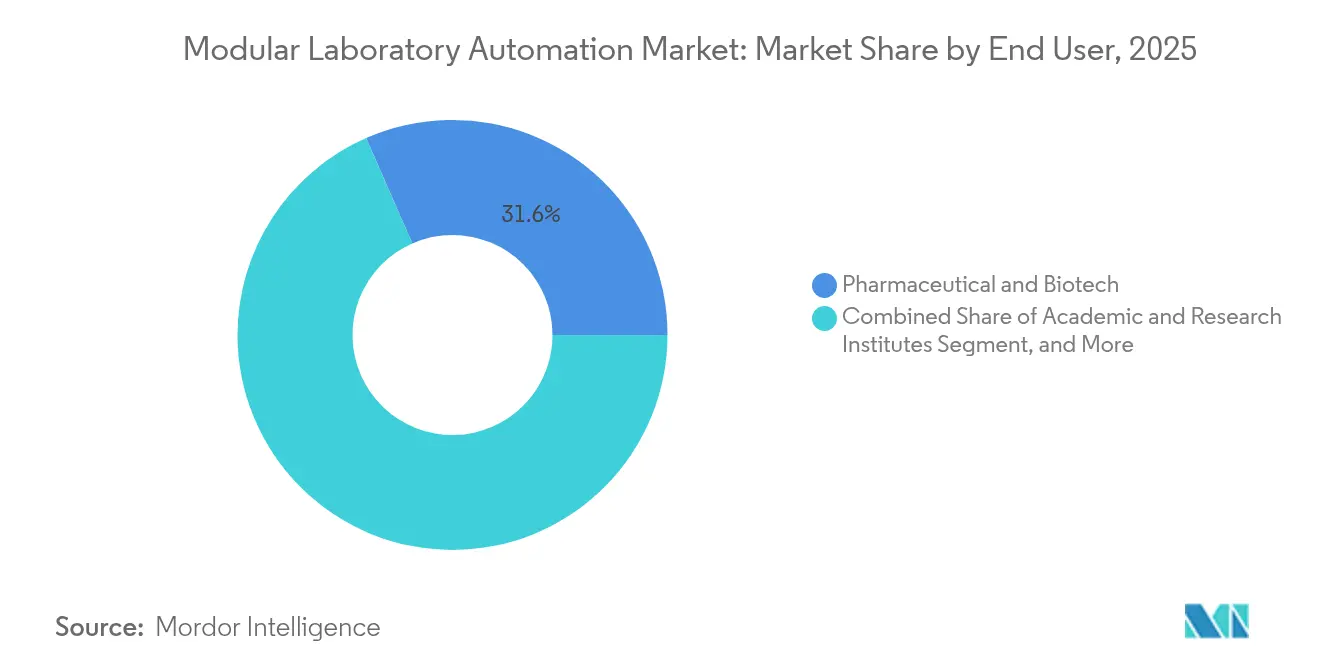

- By end user, pharmaceutical & biotech companies captured 31.58% of the modular laboratory automation market size in 2025; contract research organizations are forecast to grow at an 8.2% CAGR through 2031.

- By automation type, modular work cells led with 28.74% revenue share in 2025, whereas mobile/cloud-connected robots are set to grow at a 8.77% CAGR by 2031.

- By geography, North America commanded 41.15% of global revenue in 2025; the Asia–Pacific region is the fastest-growing territory through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Modular Laboratory Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising need for reproducibility & data integrity | +1.8% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Chronic skilled-labour shortages in life-science labs | +2.1% | Global, acute in North America & APAC | Short term (≤2 years) |

| High-throughput genomics & cell-therapy pipelines | +1.5% | North America & Europe, spreading to APAC | Medium term (2-4 years) |

| EU GMP Annex 1 contamination-control mandates | +1.2% | Europe with global spillover | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Need for Reproducibility & Data Integrity

Automated platforms impose strict process control, cutting variability that manual techniques often introduce. The Mayo Clinic’s sorting system moves 6,000 tubes per hour without mis-sorts, demonstrating zero-defect data capture. Such results are indispensable as regulators demand granular audit trails for every assay. Multi-site consortia use standardized robotic workflows to compare results confidently, boosting collaborative studies. Vendors increasingly embed blockchain-ready logs to safeguard raw data. These capabilities elevate laboratory credibility when submitting evidence to regulatory agencies.

Chronic Skilled-Labor Shortages in Life-Science Labs

Vacancies nearing 25,000 positions across North America have pushed labs toward automation that reassigns repetitive tasks to machines while scientists focus on interpretation. Clarapath’s robotic microtomy lets one technician oversee multiple slide-prep stations, tripling output capacity. Such labour-multiplying benefits shorten testing backlogs and support 24/7 operations without overtime premiums. Automation also institutionalizes tacit knowledge by encoding protocols into software, reducing onboarding time for new hires. With retirement rates climbing, the economic rationale for modular laboratory automation market investments strengthens further. [1]Clarapath, “Clarapath Automates Slide Preparation and Microtomy Workflow,” The Dark Report, api.clarapath.com

High-Throughput Genomics & Cell-Therapy Pipelines

Large-scale sequencing studies and cell-therapy trials demand a pace impossible with manual pipetting. Automated liquid handlers now assemble sequencing libraries for thousands of samples in parallel, slashing per-sample cost. For CAR-T production, Danaher’s closed-loop robots maintain sterile boundaries while executing precise cell manipulations. Partnerships such as Astellas–YASKAWA leverage dual-arm robots to unify motion planning with inline analytics. The fusion of AI with machine-vision allows real-time error correction, pushing yields higher and reinforcing the modular laboratory automation market as the backbone of precision medicine manufacturing.

EU GMP Annex 1 Contamination-Control Mandates

Regulations effective since 2023 elevate robotics from optional to essential in sterile suites. New gloveless isolators integrate with autonomous arms that dispense, cap, and inspect vials without human contact. Continuous environmental monitoring sensors feed data into cloud dashboards that alert operators before particulates breach thresholds. Companies standardize on these robot-centric workflows globally, ensuring every batch meets the strictest jurisdiction. The regulatory tailwind accelerates procurement cycles, locking the modular laboratory automation market into long-term capital investment plans. [2]OPTIMA, “Annex 1 – Solutions for Successful Implementation,” OPTIMA, optima-packaging.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex & long ROI cycles | -1.4% | Global, hardest on smaller labs | Short term (≤2 years) |

| Integration complexity with legacy instruments & LIMS | -1.1% | Global, greater in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex & Long ROI Cycles

Entry-level robotic benches cost USD 100,000–300,000, while full lines exceed USD 1 million, straining academic and midsize budgets. Payback often stretches past three years because benefits like error-free data or staff redeployment resist simple monetization. Leasing schemes and usage-based pricing partially lower the barrier, yet maintenance contracts, validation, and operator training still elevate total cost of ownership. Finance committees therefore stage investments in phases, favouring the modular laboratory automation market approach that lets sites bolt on capacity incrementally.

Integration Complexity with Legacy Instruments & LIMS

Many instruments pre-date modern APIs, forcing labs to build middleware that maps file formats and reconciles barcodes. Custom coding inflates project timelines and risks data silos if vendors change protocols. Cloud-native LIMS platforms promise plug-and-play connectivity, but migrating decades of historical results raises validation burdens. Without enterprise data governance plans, the full productivity gains of the modular laboratory automation market remain unrealized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment and Software: Liquid Handlers Drive Market Foundation

Automated liquid handlers generated 25.83% of the modular laboratory automation market size in 2025, cementing their role as the backbone of assay preparation. Laboratories favour these platforms because precision pipetting ensures downstream data quality while freeing staff for analytical tasks. Demand for integrated software that optimizes deck layouts and predicts tip consumption is growing, reducing consumable waste and unplanned downtime. Automated storage & retrieval systems, projected to grow at 6.94% CAGR, solve the chronic challenge of sample archiving by delivering samples to work cells just-in-time. Vendors now combine low-temperature warehouses with AI route planning, minimizing freeze–thaw events and safeguarding biomolecule integrity.

Software innovation shapes competitive differentiation as vendors embed machine-learning algorithms that flag anomalies before assay failures propagate. Thermo Fisher’s Vulcan platform illustrates how combining robotic arms with self-tuning workflows elevates throughput. Analysers capable of inline mass spectrometry or fluorescence detection compress total turnaround time, letting labs condense multi-day protocols into single shifts. The net effect is a structural rise in demand for cohesive ecosystems rather than single-purpose boxes, reinforcing supplier emphasis on modular laboratory automation market ecosystems that orchestrate hardware and data in one pane of glass.

By Field of Application: Clinical Diagnostics Lead Automation Adoption

Clinical diagnostics contributed 28.12% revenue in 2025, underpinned by high-volume chemistries and strict accreditation criteria that reward reproducible automation. Hospital laboratories integrate conveyor-linked work cells with middleware that posts verified results directly to electronic health records, shortening patient care cycles. Cell & gene therapy workflows, forecast for 9.21% CAGR, need closed-system robots that minimize contamination risk during lengthy culture periods. Robots equipped with environmental sensors and AI classifiers maintain sub-micron cleanliness, preventing batch failures that could cost millions of USD.

Drug-discovery groups continue to deploy high-throughput screens on 1,536-well plates, while genomics consortia automate library prep for population cohorts. Proteomics is emerging as laboratories automate sample digestion and LC-MS loading. Cross-disciplinary platforms that support reagent-agnostic protocols are gaining traction, as they let sites pivot capacity between diagnostic, discovery, and manufacturing workloads. This versatility reinforces investment in the modular laboratory automation market because a single capital outlay serves many revenue streams.

By End User: Pharmaceutical & Biotech Companies Anchor Market Demand

Pharmaceutical and biotech firms captured 31.58% of 2025 spending, driven by regulatory obligations for data integrity and the need to compress development timelines. High-throughput biology paired with electronic batch records accelerates IND submissions and reduces failure risk in late-stage trials. CROs, expanding at an 8.2% CAGR, deploy flexible automation that handles client-specific methods without long validation cycles. Their purchasing power incentivizes vendors to standardize plug-ins that swap liquid classes and deck configurations in minutes.

Academic institutes adopt modular work cells to stretch limited grants yet still meet peer-review expectations for reproducibility. Clinical laboratories, pressured by test-volume growth and workforce gaps, use pre-analytical robots that decamp tubes and aliquot specimens automatically. Food and environmental laws require ruggedized systems that resist acidic or particulate-laden samples; this niche sustains a specialized subset within the modular laboratory automation market, often delivered as compact benchtop units.

By Automation Type: Modular Work cells Balance Flexibility and Integration

Modular work cells accounted for 28.74% of revenue in 2025, validating the premise that stepwise deployment balances cost and capability. Laboratories often start with a liquid-handling core, add plate movers, then integrate analytics as volumes scale. Mobile or cloud-connected robots, expected to expand at a 8.77% CAGR, traverse multiple benches and share resources across departments, making capital use more efficient. Their onboard cameras support remote service diagnostics, a feature valued in geographically dispersed networks.

Standalone instrument automation remains relevant where single-analysis precision outweighs throughput. Integrated work cells deliver linear sample paths ideal for reference laboratories with predictable demand curves. Total laboratory automation lines occupy the premium tier; although costly, they virtually eliminate human touch points, achieving the highest possible workflow velocity. Regardless of configuration, security-hardened firmware and role-based access control are now standard, reflecting cybersecurity expectations in the modular laboratory automation market.

Geography Analysis

North America sustained a 41.15% revenue share in 2025, reflecting the concentration of biopharmaceutical headquarters, generous NIH funding, and a mature regulatory environment that favours technology investments. Recent federal grants, such as the USD 2.15 million MATChS award, confirm public-sector endorsement of intelligent automation. Tier-1 hospitals are integrating decentralized work cells, pushing specimen processing closer to patient intake to reduce logistics delays. Canada’s life-science clusters leverage provincial tax credits to upgrade research infrastructure, though staffing shortages remain acute; automation therefore offers a pragmatic path to maintain throughput despite limited headcount. Mexico, seeking export accreditation for sterile injectables, is piloting robotic isolators to meet Annex 1 requirements and secure contract manufacturing deals.

Asia–Pacific registers the highest growth trajectory as governments subsidize biotech infrastructure and encourage local manufacturing of advanced therapies. China invests in national sequencing hubs that adopt fully automated, closed-loop pipelines, reducing per-genome costs and accelerating precision-medicine pilot programs. Japan’s aging population elevates demand for diagnostic automation capable of handling chronic-disease panels. India’s contract-manufacturing sector implements modular isolators that comply with global sterility standards, positioning domestic plants for regulated-market exports. South Korea focuses on cell-therapy centers of excellence that combine dual-arm robots with AI analytics, bringing complex biologics to market more swiftly. Collectively, these initiatives underpin sustained demand across the modular laboratory automation market throughout the region.

Europe remains a pivotal market because Annex 1 lifts technical barriers in favour of robotics, driving upgrades across legacy fill-finish lines. Germany’s engineering base integrates high-precision mechatronics with cloud-native MES platforms, while the United Kingdom channels research funding into university-hospital partnerships that validate AI-directed work cells. France modernizes public-sector laboratories through stimulus packages that offset upfront capex. Italy and Spain prioritize total laboratory automation in blood-bank operations to curb transfusion errors. The regulatory commonality across the European Economic Area encourages cross-border standardization, letting suppliers offer uniform validation packages and thereby expedite procurement across multiple sites within the modular laboratory automation market.

Regulatory Landscape

Modular laboratory automation is shaped by data integrity, interoperability, and validated performance expectations in regulated environments, including clinical diagnostics and GMP manufacturing. In Europe, the EU GMP Annex 1 contamination-control expectations (effective since 2023) have pushed adoption of robotics, closed systems, and continuous monitoring to reduce human interventions in sterile workflows. Clinical and diagnostic deployments also map to quality-management and competence frameworks (for example, ISO 15189:2022), and where automation software functions as part of an IVD workflow, the EU IVDR adds further compliance and documentation requirements.

In the United States, interoperability is increasingly tied to recognized consensus standards, with the FDA maintaining a catalog of recognized standards relevant to communication with automated clinical laboratory systems. Standards bodies also provide anchors for validation and terminology, including ISO 23783-1:2022 for automated liquid handling systems. Supply-chain governance is emerging as a more visible purchasing factor, with BIS export controls under the EAR introducing new restrictions (effective January 16, 2025) for certain biotechnology equipment categories. At the same time, the BIOSECURE Act discussion highlights procurement and disclosure considerations for organizations interfacing with federally funded programs and external sequencing or automation service providers.

Value Chain Analysis

The value chain begins with enabling inputs and subsystems, including robotics, motion control, sensors and vision, embedded compute, and cybersecurity-hardened connectivity. It then runs through modular equipment, such as liquid handlers, plate handlers, robotic arms, ASRS modules, and analyzers, supported by orchestration software that connects devices to ELN/LIMS and data platforms. System integration, method development, and validation services add most of the value, since many laboratories need middleware to bridge legacy instruments with modern APIs. Interoperability initiatives, led by consortia such as SiLA (SiLA 2) and efforts around OPC Foundation LADS, are aimed at reducing integration friction and supporting multi-vendor deployments.

Downstream, channel partners and OEM ecosystems deliver configured workcells, and recurring revenue comes from consumables, service contracts, qualification, software maintenance, and workflow updates. Recent partner activity reinforces a move toward software-led connected labs: HighRes Biosolutions partnered with Cenevo (June 2026) to unify Cellario OS with Mosaic, while the SiLA Consortium launched an ELN/LIMS interoperability feature-descriptor project supported by Benchling, RSpace, and Chemotion (April 2026). On the application side, alliances such as Chemspeed with Iktos (March 2026) and Biocytogen with MegaRobo (August 2025) show how AI orchestration, automation hardware, and domain workflows are packaged together, affecting vendor selection and improving time-to-deployment for modular cells.

Competitive Landscape

The modular laboratory automation market shows moderate consolidation; the top three suppliers hold substantial but not monopolistic positions. Thermo Fisher integrates robotics, consumables, and cloud software into turnkey offerings, as reflected in its USD 10.36 billion Q1 2025 revenue. Danaher advances AI-assisted workflows that predict assay failures and auto-correct pipetting parameters, shielding clients from costly reruns. Tecan leverages open-API policies to foster third-party ecosystem growth, a key attraction for institutes blending legacy instruments with new automation.

Strategic acquisitions intensify competition. Siemens’ USD 5.1 billion purchase of Dotmatics injects AI LIMS capabilities that converge design, execution, and data analytics under one roof. Grifols teams with Inpeco to unveil FlexLab X, bringing transfusion medicine into the era of open automation. QuidelOrtho pursues rapid molecular diagnostics that dovetail with existing chemistry-analyser fleets, expanding footprint without fresh floor-space commitments. Start-ups differentiate through mobile robotics and service-based pricing, appealing to mid-tier labs that resist heavy capital outlays.

Cybersecurity emerges as a new battleground. Vendors harden firmware, embed encrypted communications, and offer SOC-as-a-service to reassure regulated industries. Ecosystem partnerships also matter; consumables suppliers co-design reagent kits optimized for specific robot platforms, locking in recurring revenue. In this environment, vendor ability to deliver validated, end-to-end solutions will determine share capture within the modular laboratory automation market over the next five years.

Modular Laboratory Automation Industry Leaders

Thermo Fisher Scientific

Danaher (Beckman Coulter)

Tecan Group AG

Agilent Technologies

Hamilton Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A recurring whitespace is reducing the integration and validation burden for multi-vendor modular workcells, particularly for laboratories that cannot fund bespoke engineering. Standardization programs offer practical routes forward, including SiLA 2 device communication and OPC Foundation LADS for interoperability. NIST is also developing standards covering sample management, instrument control, communication, and data management to support more modular and autonomous laboratory ecosystems. As these efforts progress, vendors that can provide pre-validated connectors, role-based access controls, and audit-ready data pipelines can expand adoption beyond large, proprietary installations into a wider set of clinical, academic, and distributed pharma networks.

Opportunity also exists in workforce enablement and operationalization of automation, since consistent SOP execution supports scaling modular deployments across sites. In January 2026, SLAS received a USD 199,884 Alfred P. Sloan Foundation grant to develop lab automation educational guidelines, indicating structured training infrastructure for automated science. In parallel, the formation of a SiLA AI Working Group (January 2026) supports a clearer integration layer for AI-driven orchestration and documentation practices, which aligns with buyer requirements for reproducibility, complete audit trails, and secure, network-ready work cells in regulated workflows such as clinical diagnostics and cell and gene therapy manufacturing.

Recent Industry Developments

- May 2026: Thermo Fisher Scientific unveiled an integrated platform to advance scalable cell therapy manufacturing, including the Gibco CTS DynaXS single-use bioreactor as an expansion-focused module. The release supports demand for closed, modular, and cGMP-aligned automation components that can be added as capacity grows, tightening supplier positioning in high-value cell and gene therapy workflows.

- February 2026: Beckman Coulter Life Sciences (Danaher) partnered with Automata to integrate Beckman technologies across liquid handling, genomics, and cell analysis with Automata's LINQ automation ecosystem. The collaboration broadens access to AI-ready orchestration and standardized integration for multi-instrument workcells, supporting labs seeking modular scale-up without rebuilding entire tracks.

- December 2025: Tecan announced the acquisition of Wako Automation assets, including Director scheduling software and related hardware modules, to expand its robotic workcell offering. Bringing scheduling and execution software closer to the hardware stack strengthens Tecan's ability to deliver more unified, configurable cells and compete on deployment speed and workflow reliability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the modular lab automation market covers revenue from modular hardware and control layers that automate specific laboratory workflow steps. These modules can be added to an existing lab without building a full end-to-end automation line.

Scope exclusions: We exclude stand-alone benchtop instruments that are not automation modules, pure software-only LIMS tools, and full conveyor-based total lab automation tracks.

Segmentation Overview

- By Equipment and Software

- Automated Liquid Handlers

- Automated Plate Handlers

- Robotic Arms

- Automated Storage and Retrieval Systems (ASRS)

- Analyzers

- Software

- By Field of Application

- Drug Discovery

- Genomics

- Proteomics

- Clinical Diagnostics

- Other Applications

- By End User

- Pharmaceutical and Biotech Companies

- Academic and Research Institutes

- Clinical and Diagnostic Laboratories

- Contract Research Organisations

- Food and Environmental Testing Labs

- By Automation Type

- Standalone Instrument Automation

- Modular Workcells

- Integrated Workcells

- Total Laboratory Automation (TLA) Lines

- Mobile/Cloud-connected Robots

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a practical view of demand, funding, and installed lab activity before modeling revenue. We typically start with public science and health statistics such as those from the World Health Organization, OECD health and R&D indicators, and the World Bank, and then align them with customs and trade data such as UN Comtrade to understand how automated lab equipment flows by region.

To keep assumptions grounded, we also review filings and investor materials from relevant manufacturers, along with methods and throughput discussions found in peer-reviewed journals and patent databases. Trade groups and regulator websites, such as those linked to clinical laboratory standards and lab accreditation, help us understand adoption requirements that can change purchasing cycles. For extra company-level financial context, we also use a paid subscription focused on company financials and another paid subscription focused on patent intelligence. These examples are illustrative and not exhaustive, and many other sources were also used to collect data, validate inputs, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test desk assumptions and fill the gaps that public sources cannot answer clearly, such as typical module bundling, software attach rates, and replacement timing. We spoke with a mix of lab operations leaders, automation engineers, procurement teams, distributors, and integration partners across Americas, EMEA, and APAC, so the regional workflow differences were reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 38% |

| Mid tier: 46% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 15% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where global and regional lab activity is reconstructed using R&D spending signals, clinical testing volumes, and automation adoption rates by lab type, which are then translated into modular system demand. Once that demand pool is clear, the model applies typical module mix and average selling price ranges to estimate revenue by region.

To make sure totals are not drifting, we also run selective bottom-up checks using supplier revenue clues, channel feedback on shipment momentum, and sampled configurations where modules and software are priced as a bundle. Key inputs used in the model include the share of labs expanding throughput, the shift toward walk-away workflows, average modules per installation, software orchestration attach rates, and service and maintenance add-ons that follow system deployment. When data is thin for smaller countries, we gap-fill using proxy indicators such as laboratory density and healthcare or pharma output, and then results are rechecked with regional interview feedback.

For forecasting, we use scenario analysis supported by multivariate relationships between adoption, funding cycles, and capital equipment purchasing trends. We then align the final growth path with what respondents expect for budgets and automation roadmaps.

Data Validation & Update Cycle

Validation is done through a set of cross-checks so the market number stays tied to real demand signals. Our analysts compare modeled revenue against independent indicators such as import patterns for relevant automation equipment, public R&D and healthcare spending movements, and reported lab capacity expansion activity.

Outliers are reviewed, and assumptions are adjusted only when at least two independent signals support the change. This is followed by an internal peer review before sign-off. The report is refreshed each year, and if a material event changes pricing, supply, or purchasing behavior, we re-contact sources and update key inputs. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Global Modular Lab Automation Market Market Size Measured Against Other Published Estimates

Published market sizes for modular lab automation can differ because each publisher draws the scope differently around modules, software, and adjacent lab automation categories, and they also use different base years and currency conversion timing. Pricing assumptions can vary too, especially when software is treated as a one-time license versus a recurring subscription.

Some published figures appear to fold in adjacent items such as consumables, broader automation ecosystems, or conveyor-based systems. Mordor Intelligence counts modular workcells, automation modules (like liquid handling, plate handling, robotics, and storage-retrieval units), and the orchestration layer, and it keeps stand-alone benchtop tools and full total lab automation tracks outside scope so the number stays tied to modular deployments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.39 B (2026) | |

| Industry Research Publisher A | USD 5.80 B (2024) | Uses a broader component basket that explicitly includes consumables and accessories, and it also emphasizes software solutions as a recurring revenue pool. The earlier base year can also shift pricing levels versus later-year current values. |

| Market Research Publisher B | USD 5.27 B (2024) | Lists conveyor systems and a wider set of laboratory instruments under the component definition, which moves the total closer to broader lab automation spend rather than modular add-on deployments. A different base year and forecast framing can further change the starting market value. |

The table shows that the biggest driver of variation is what gets counted, particularly software and adjacent systems that sit next to modular automation in real lab budgets. When scope is limited to modular deployments and their control layer, and then checked against demand and pricing signals, the resulting total is easier to reconcile across regions and time.

Key Questions Answered in the Report

What is the current size of the modular laboratory automation market?

The modular laboratory automation market stands at USD 3.39 billion in 2026 and is projected to reach USD 4.56 billion by 2031.

Which segment holds the largest share of the modular laboratory automation market?

Automated liquid handlers lead with 25.83% revenue share, reflecting their central role in most laboratory workflows.

Why are pharmaceutical companies investing heavily in modular laboratory automation systems?

Pharmaceutical firms need reproducible data, regulatory compliance, and accelerated development timelines; modular automation delivers these benefits while supporting high-throughput screening and sterile manufacturing requirements.

How do EU GMP Annex 1 requirements influence automation purchasing decisions?

The revised guideline favours robotic isolators and continuous monitoring, prompting European and global manufacturers to invest in automation that ensures contamination control.

What financial barriers do smaller laboratories face when adopting automation?

Upfront capital costs can exceed USD 1 million, and ROI may extend beyond three years, making leasing or phased deployment attractive alternatives.

How are cybersecurity concerns addressed in networked laboratory robots?

Vendors embed encrypted communications, role-based access controls, and offer security-operations-center services to mitigate unauthorized access risks in connected automation systems.

Page last updated on: