Research Department Explosive Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

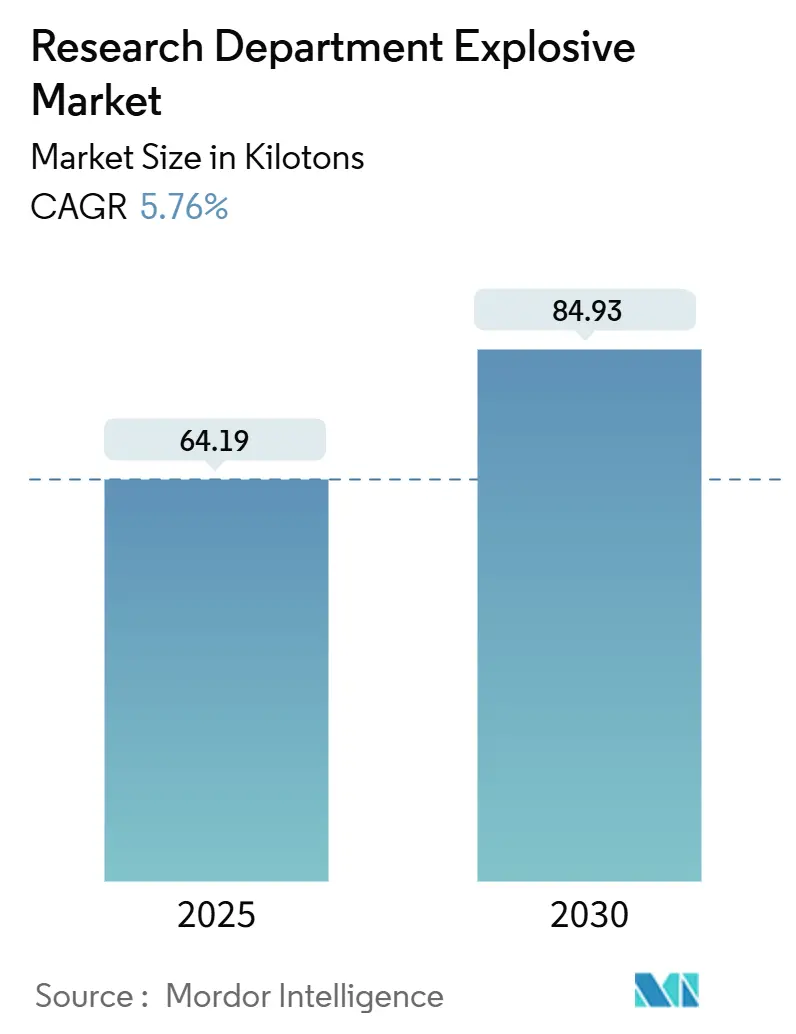

| Market Volume (2025) | 64.19 kilotons |

| Market Volume (2030) | 84.93 kilotons |

| Growth Rate (2025 - 2030) | 5.76% CAGR |

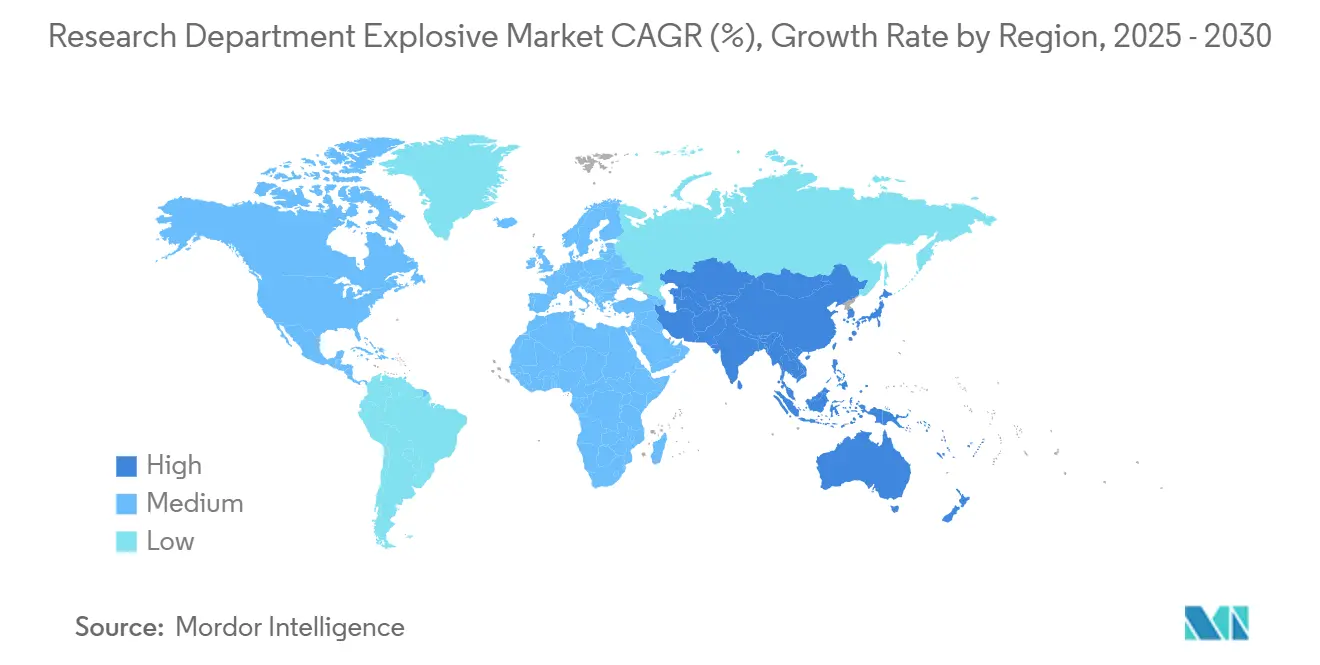

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Research Department Explosive Market Analysis by Mordor Intelligence

The Research Department Explosive Market size is estimated at 64.19 kilotons in 2025, and is expected to reach 84.93 kilotons by 2030, at a CAGR of 5.76% during the forecast period (2025-2030). Sustained investments in force-modernization, particularly the Pentagon’s USD 6.9 billion hypersonic weapons budget, support steady uptake of nano-crystallized RDX warheads. Plastic-bonded explosives (PBX-RDX) retain the volume lead because they satisfy NATO insensitive-munitions safety standards, while pellets and castings post the quickest growth as precision-guided munitions expand. Regionally, North America dominates procurement, yet Asia-Pacific records the strongest expansion on the back of India’s Make-in-India defense initiatives and South Korea’s export-oriented energetic-materials capacity. Contract awards worth USD 8.8 billion to BAE Systems for Holston Army Ammunition Plant operations underscore how incumbents keep supply chains aligned with rising demand.

Key Report Takeaways

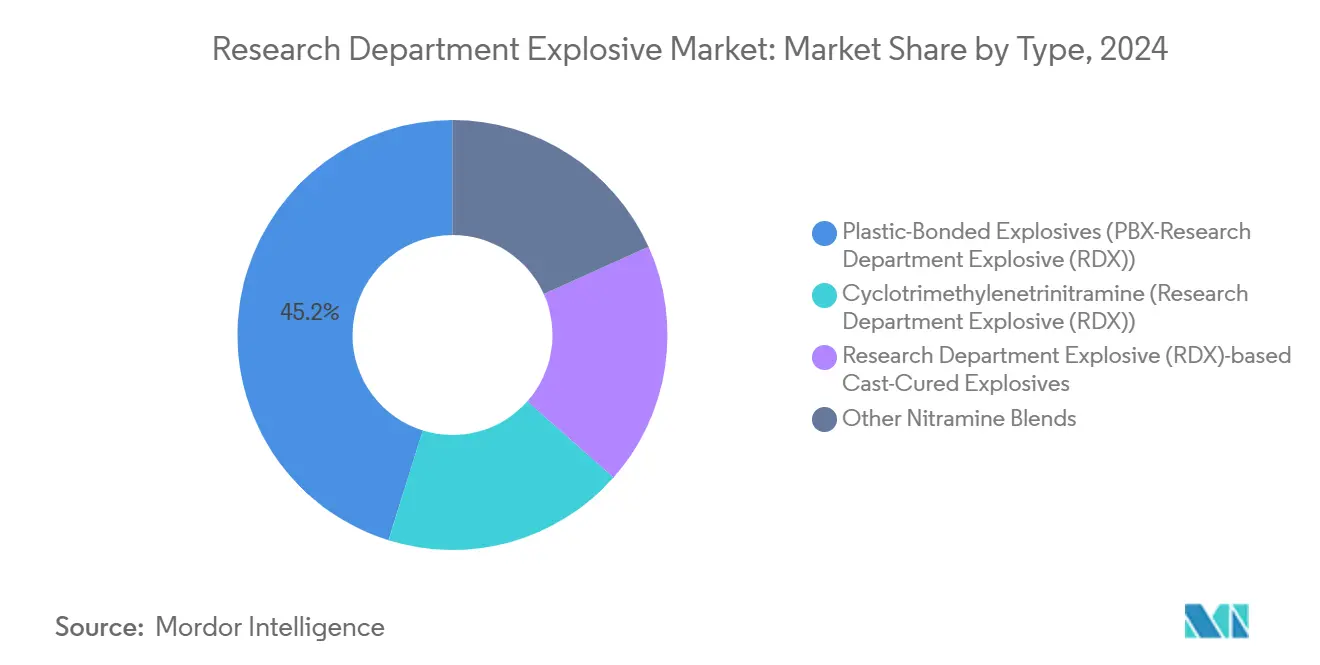

- By type, plastic-bonded explosives led with 45.18% of the Research Department Explosive market share in 2024; other nitramine blends are projected to expand at a 6.67% CAGR through 2030.

- By form, powder/crystalline explosives accounted for a 54.47% share of the Research Department Explosive market size in 2024, while pellets and castings are advancing at a 6.19% CAGR through 2030.

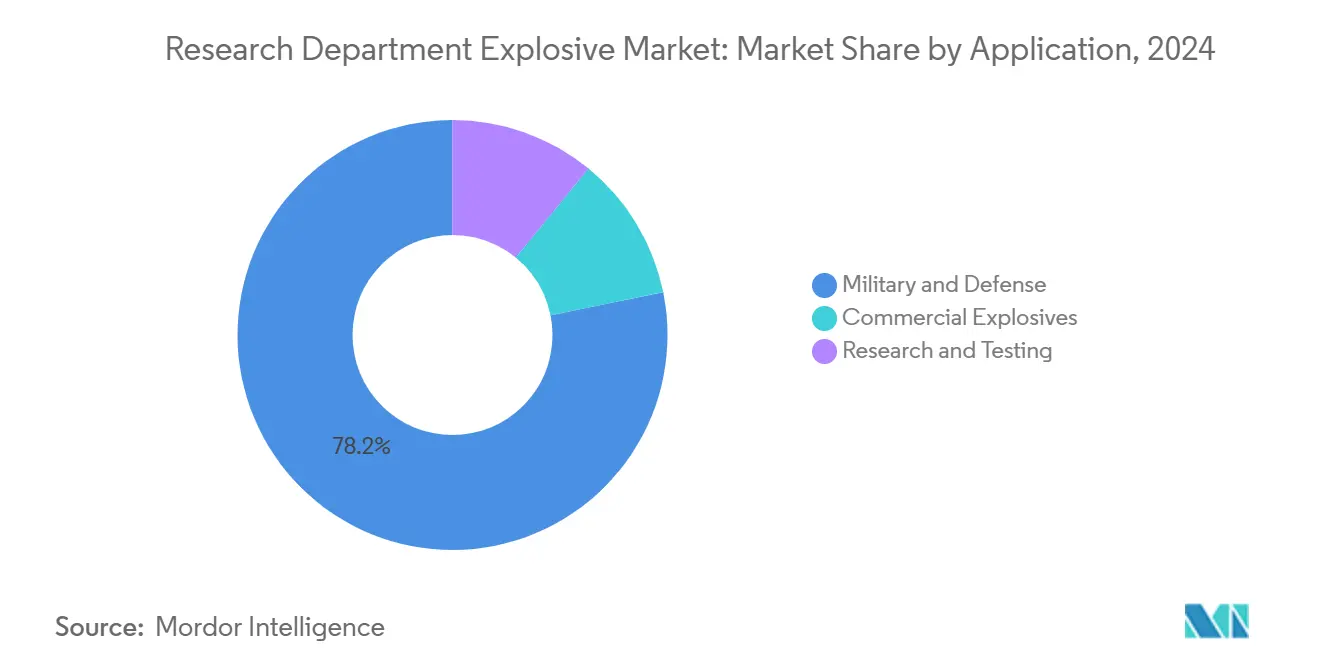

- By application, military and defense captured 78.19% of the Research Department Explosive market in 2024; research and testing is forecast to grow at a 6.72% CAGR to 2030.

- By geography, North America held 38.39% of the Research Department Explosive market in 2024, whereas Asia-Pacific is projected to post a 6.51% CAGR through 2030.

Global Research Department Explosive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Defense Expenditure and Force Modernization | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Demand for High-Performance Insensitive Munitions | +1.2% | North America and EU, spill-over to APAC | Long term (≥ 4 years) |

| Expansion of Energetic-Material Plants in Emerging Economies | +0.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Nano-Crystallised RDX for Hypersonic and Loitering Munitions | +0.7% | North America, selective APAC markets | Long term (≥ 4 years) |

| RDX Reclamation from Demilitarised Ordnance Enables Circular Supply | +0.4% | Global, with early adoption in North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Defense Expenditure and Force Modernization

Global military outlays reached USD 2.4 trillion in 2024, and budgets continue to prioritize precision-guided munitions that rely on engineered RDX variants[1]Stockholm International Peace Research Institute, “SIPRI Military Expenditure Database 2025,” sipri.org . The U.S. Department of Defense earmarked USD 192.5 million to strengthen domestic chemical-feedstock capacity, mitigating supply risks uncovered during recent conflicts. European countries accelerated stockpiling, as shown by Estonia’s explosives-factory program and France’s 2025 powder-line commissioning. These initiatives channel procurement toward plastic-bonded and nano-crystallized formulations that meet insensitive-munitions norms. Suppliers that specialize in high-purity RDX benefit from premium pricing as military buyers shift from commodity explosives to performance-engineered solutions.

Demand for High-Performance Insensitive Munitions

Modern doctrine favors survivability, prompting NATO to enforce STANAG 4439 testing sequences that elevate plastic-bonded explosives over melt-cast TNT. The U.S. Army’s USD 990 million Switchblade program illustrates institutional commitment to platforms that integrate low-sensitivity warheads. European producers scale capabilities; Rheinmetall recently secured nitrocellulose assets that support next-generation ammunition. Research into nano-crystallized RDX enables safer handling without sacrificing detonation velocity, resolving the safety-versus-lethality dilemma. As adoption widens, demand shifts toward binders that retain mechanical integrity under thermal cycling, enhancing lifecycle reliability.

Expansion of Energetic-Material Plants in Emerging Economies

Strategic-autonomy policies across Asia-Pacific propel domestic production lines. India’s Premier Explosives Limited formed a joint venture with Nibe Ordnance to serve both national and export needs. In South Korea, Hanwha leverages seven-decade explosives expertise to win contracts in Australia and Poland. Localization shortens lead times and aligns formulations to regional threat profiles, elevating competitive pressure on Western incumbents. Emerging suppliers deploy modern automation that lowers variance in crystal size, giving them an edge in precision-guided segments. Incumbents must innovate or cede share to cost-effective regional challengers.

Nano-Crystallized RDX for Hypersonic and Loitering Munitions

Hypersonic warheads require detonations that remain stable at Mach 5+ thermal loads. Nano-crystallized RDX delivers tight particle-size distribution, improving burn uniformity and shock-wave coherence. The Pentagon’s USD 6.9 billion hypersonic allocation funds energetic-material research, including Common Hypersonic Glide Body components. Loitering munitions such as Switchblade adopt lightweight, high-density pellets that maximize terminal effects while limiting collateral damage. Yet nano-crystallization scales slowly because it relies on solvent-free continuous-flow reactors with stringent quality controls. Early suppliers gain first-mover advantage but face capital-intensive barriers as demand migrates from prototyping toward serial production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Dual-Use and Export-Control Regimes | -0.8% | Global, with strictest enforcement in North America and EU | Short term (≤ 2 years) |

| Toxic Nitramine Liabilities Under Emerging Soil-Quality Laws | -0.5% | EU core, expanding to North America | Medium term (2-4 years) |

| Nitric-Acid and Hexamine Price Volatility amid Green-Ammonia Transition | -0.3% | Global, with acute impact in Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Dual-Use and Export-Control Regimes

Revisions to U.S. ITAR and EAR now classify many energetic-material process steps, lengthening export-license cycles to 6-12 months. Compliance demands favor large contractors with in-house legal teams, while smaller firms struggle to finance documentation and secure surety bonds. Joint development projects face heightened scrutiny, limiting technology transfers that once fueled multinational programs. Asian suppliers encounter extra hurdles when sourcing high-precision crystallizers or vacuum-static mixers from U.S. OEMs. These frictions can delay deliveries and influence procurement preference toward domestic sources even when costlier.

Toxic Nitramine Liabilities Under Emerging Soil-Quality Laws

Groundwater studies link RDX residues to ecological harm, prompting EU agencies to draft proposals that may reclassify nitramines as probable carcinogens. Operators would then incur costly remediation and reformulation, raising barriers for legacy plants. An explosion at an Indian facility in January 2025 amplified public focus on nitramine safety lapses, accelerating calls for tighter oversight. Companies invest in greener binders and in-process recycling to curb discharge levels, yet retrofit expenses can narrow margins. Legal contingencies complicate M&A valuations as buyers discount assets facing latent cleanup liabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Plastic-Bonded Explosives Drive Innovation

Plastic-bonded explosives led with a 45.18% share of the Research Department Explosive Market in 2024, underscoring their alignment with insensitive-munitions mandates. Cyclotrimethylenetrinitramine serves legacy artillery niches, while RDX-based cast-cured grades support warheads requiring complex geometries. Other nitramine blends, including CL-20 and NTO combinations, advance at a 6.67% CAGR, reflecting customer pursuit of higher energy density. The Research Department Explosive market size attributable to plastic-bonded grades broadens as polymer-binder research focuses on adhesion and thermal-expansion parity to curb void formation. Patents in glycidyl-nitramine elastomers indicate future formulations that combine safety with mechanical toughness.

Automation upgrades allow real-time spectroscopic control of explosive-to-binder ratios, squeezing batch variance and lowering rework costs. Suppliers that master nano-scale particle coating guard against hot-spot initiation under impact, enhancing qualification odds in NATO trials. Customers increasingly stipulate ESD-safe pack-out formats, driving ancillary demand for conductive packaging films. As hypersonic programs mature, plastic-bonded grades with melt points exceeding 200 °C gain preference, positioning innovators for premium contracts in 2026-2030.

By Form: Powder Dominance Faces Precision Challenges

Powder/crystalline products held 54.47% of the Research Department Explosive Market share in 2024 because they dovetail with existing filling lines. Yet nano-crystalline powders introduce sensitivity risks that compel antistatic handling protocols. Granular grades fill seismic exploration and civil-blasting orders, while pellets and castings advance at the fastest 6.19% CAGR, mirroring growth in precision-strike weapons. The Research Department Explosive market size for pellets expands as computer-controlled presses achieve ±1% density uniformity, vital for blast consistency.

Thermal-pressure coupling solidification fixes historic void issues in melt-cast charges, expanding use in unitary warheads. Pellet lines capitalize on servo-drive compaction that reduces cracking, lowering inspection rejects. Casting shops adopt dinitroanisole binders to replace toxic TNT, satisfying looming EU soil-quality rules. Powder suppliers respond by investing in glove-box crystallization bays that keep particle size below 10 µm without agglomeration, catering to hypersonic applications that demand tight detonation-wave coherence.

By Application: Military Dominance Drives Specialization

Military and defense captured 78.19% of the Research Department Explosive Market in 2024 as modernization agendas champion precision-guided munitions. Commercial blasting remains regulated, capping volume upside in developed regions. Research and testing accelerates at a 6.72% CAGR because hypersonic prototypes and directed-energy countermeasures require novel energetic chemistries. Customer specifications increasingly call for tailored formulations matched to operational envelopes ranging from sub-zero Arctic theaters to high-humidity equatorial deployments.

Long-term U.S. Army commitments, such as the USD 288 million Switchblade call-off, lock in demand for low-shock explosives optimized for tube-launch platforms. Universities and defense -labs broaden pilot-plant trials for nitrate-ester-free propellants, sustaining R&D reagent consumption. Meanwhile, commercial-mining demand in Latin America opens pockets for lower-grade RDX blends when local regulations permit. Suppliers segment their portfolios, earmarking high-purity lots for missile warheads and secondary-grade lots for quarry blasting to maximize asset utilization.

Geography Analysis

North America retained a 38.39% slice of the Research Department Explosive Market in 2024. The United States anchors demand through large-scale programs such as the hypersonic glide body, while Canada upgrades stockpiles to meet NATO response-force targets. Holston Army Ammunition Plant’s USD 8.8 billion operating contract secures domestic throughput and offers buffer capacity for allied contingencies. Mexico’s civil-blasting consumption climbs as infrastructure projects multiply, though dual-use controls restrict high-energy RDX exports. Supply-chain initiatives—including Repkon USA’s USD 109 million TNT project—cushion the region from nitric-acid volatility.

Europe experiences tighter supply as security concerns inflate demand for insensitive munitions. Forcit’s USD 200 million TNT plant in Finland tackles a chronic continental shortfall. Germany’s Rheinmetall partners with Lockheed Martin to establish a rocket center of excellence that pools expertise across casting, pressing, and warhead integration. France recommissioned a gunpowder line in January 2025 to reinforce sovereignty. Regulatory scrutiny intensifies; proposed REACH amendments could reclassify nitramines, pressing manufacturers to adopt greener binders. Investments in continuous-flow nitrators aim to cut NOx emissions and align with EU climate goals.

Asia-Pacific advances fastest at a 6.51% CAGR through 2030, spearheaded by India, China, South Korea, and Australia. India’s joint venture between Premier Explosives and Nibe Ordnance extends capacity for artillery shell fillers and missile warheads. South Korea exploits competitive cost structures to supply Australia’s Guided Weapons Enterprise, while Chinese producers commercialize high-density CL-20 blends, though export-license barriers constrain international reach. Japan raises defense allocations to 2% of GDP, channeling funds toward domestic energetic-materials plants. Australia pursues strategic partnerships to localize energetics in support of AUKUS commitments. Collectively, Asia-Pacific suppliers upgrade analytics and automation, positioning the region to challenge Western incumbents in high-performance segments.

Competitive Landscape

The Research Department Explosive Market shows high concentration, with tier-one contractors locking in multiyear volume guarantees through government frameworks. BAE Systems’ breakthrough dry-blend technology lifts RDX output per batch by 16-fold, trimming cycle times and reinforcing its lead position. Lockheed Martin collaborates with Rheinmetall on a German center of excellence to combine rocket-motor casting with advanced warhead filling, demonstrating how cross-border alliances streamline NATO-standard supply. Kratos Defense and RAFAEL formed Prometheus Energetics to produce solid rocket motors in the United States, highlighting reshoring momentum.

Innovation gravitates toward insensitive eutectic compositions, as illustrated by US Patent 8663406B1 that covers DETN and MeNQ melt-cast systems[2]Google Patents, “Insensitive Eutectic Explosive Compositions,” patents.google.com . Suppliers also explore elastomeric binders that tolerate wider service-temperature windows without micro-cracking. Circular-economy entrants reclaim RDX from decommissioned stockpiles, offering lower-carbon inputs that align with defense sustainability goals. Asian challengers such as Hanwha leverage cost advantages and government financing to penetrate export markets, prompting incumbents to automate legacy lines and adopt in-line NIR spectroscopy to guarantee batch conformity. Market leadership will hinge on insulation from feed-stock volatility, mastery of nano-scale crystallization, and capability to certify products under evolving eco-toxicity standards.

Research Department Explosive Industry Leaders

Chemring Group PLC

Hanwha Group

Nitro-Chem S.A.

MAXAMCorp Holding S.L.

BAE Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BAE Systems has announced plans to increase domestic production of Research Department Explosives, used in 155mm artillery shells, to minimize dependence on imports from the United States and France.

- January 2023: A new RDX (Research Department Explosive) manufacturing facility is under construction in Várpalota, Hungary, utilizing technology from Rheinmetall Denel Munition of South Africa. The facility, established as a joint venture between Rheinmetall and Hungarian company N7 Holding, will produce RDX explosives for artillery, tank, and mortar ammunition.

Global Research Department Explosive Market Report Scope

| Plastic-Bonded Explosives (PBX-Research Department Explosive (RDX)) |

| Cyclotrimethylenetrinitramine (Research Department Explosive (RDX)) |

| Research Department Explosive (RDX)-based Cast-Cured Explosives |

| Other Nitramine Blends |

| Powder / Crystalline |

| Granular |

| Pellets and Castings |

| Military and Defense |

| Commercial Explosives |

| Research and Testing |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Plastic-Bonded Explosives (PBX-Research Department Explosive (RDX)) | |

| Cyclotrimethylenetrinitramine (Research Department Explosive (RDX)) | ||

| Research Department Explosive (RDX)-based Cast-Cured Explosives | ||

| Other Nitramine Blends | ||

| By Form | Powder / Crystalline | |

| Granular | ||

| Pellets and Castings | ||

| By Application | Military and Defense | |

| Commercial Explosives | ||

| Research and Testing | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected volume of the Research Department Explosive market by 2030?

The market is forecast to reach 84.93 kilotons by 2030, up from 64.19 kilotons in 2025.

Which product type currently contributes the largest share?

Plastic-bonded explosives lead with 45.18% of 2024 volume because they comply with insensitive-munitions safety standards.

Which geographic region is growing fastest?

Asia-Pacific shows the quickest expansion at a 6.51% CAGR, driven by indigenous manufacturing and defense stockpiling.

Why are pellets and castings gaining popularity?

Precision-guided munitions need uniform density and geometry, and pellets or cast parts offer those characteristics, resulting in a 6.19% CAGR for the segment through 2030.

Page last updated on: