Mine Warfare Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.28 Billion |

| Market Size (2030) | USD 6.71 Billion |

| Growth Rate (2025 - 2030) | 4.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mine Warfare Market Analysis by Mordor Intelligence

The mine warfare market size stood at USD 5.28 billion in 2025 and is forecasted to reach USD 6.71 billion by 2030, translating into a 4.91% CAGR. Robust defense modernization programs, rising geopolitical frictions, and the widespread shift toward autonomous counter-mine systems reinforce demand across naval forces. Large-scale investments under initiatives such as the US Navy’s Replicator program underscore how artificial intelligence and unmanned platforms now anchor procurement roadmaps. Decision-makers view precision, crew risk reduction, and long-range standoff deployment as central advantages that sustain momentum in the mine warfare market. Modular system architectures further accelerate upgrade cycles and shorten fielding timelines, keeping the competitive field dynamic.

Key Report Takeaways

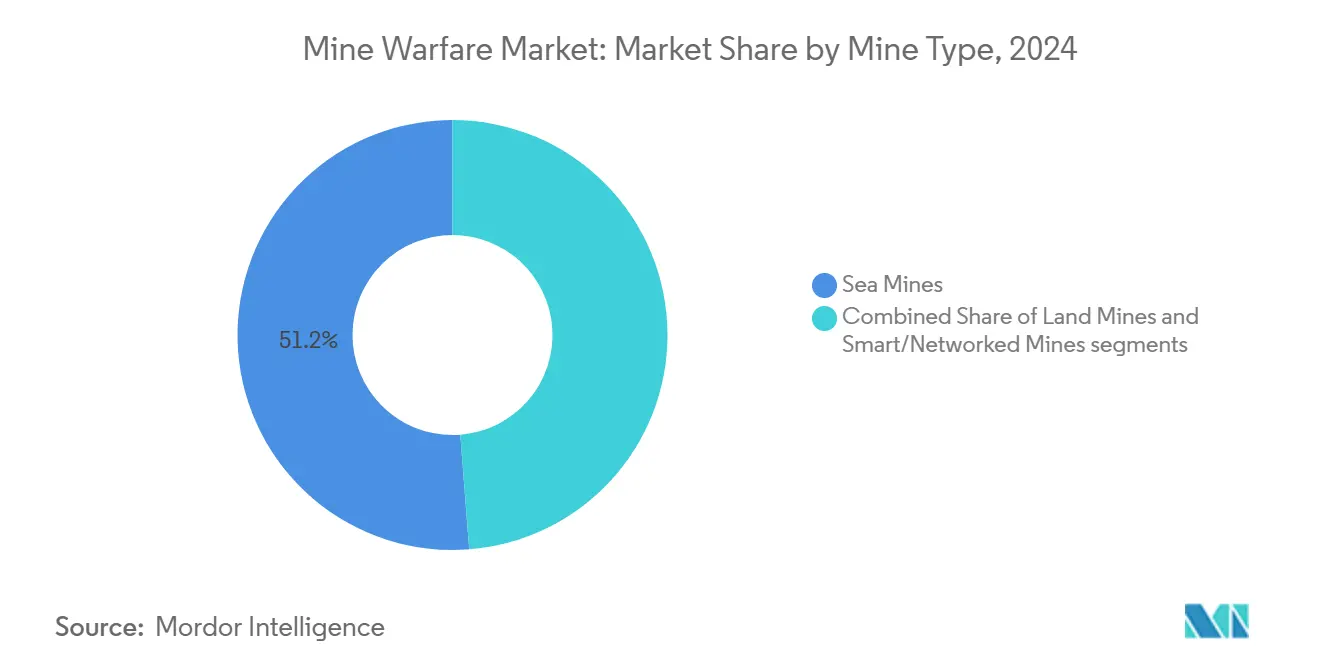

- By mine type, sea mines led with 51.24% of the mine warfare market share in 2024; smart and networked mines are projected to expand at a 7.35% CAGR to 2030.

- By platform, surface mine-countermeasure (MCM) vessels held 36.27% of 2024 revenue, while unmanned underwater vehicles (UUVs) are advancing at a 6.29% CAGR through 2030.

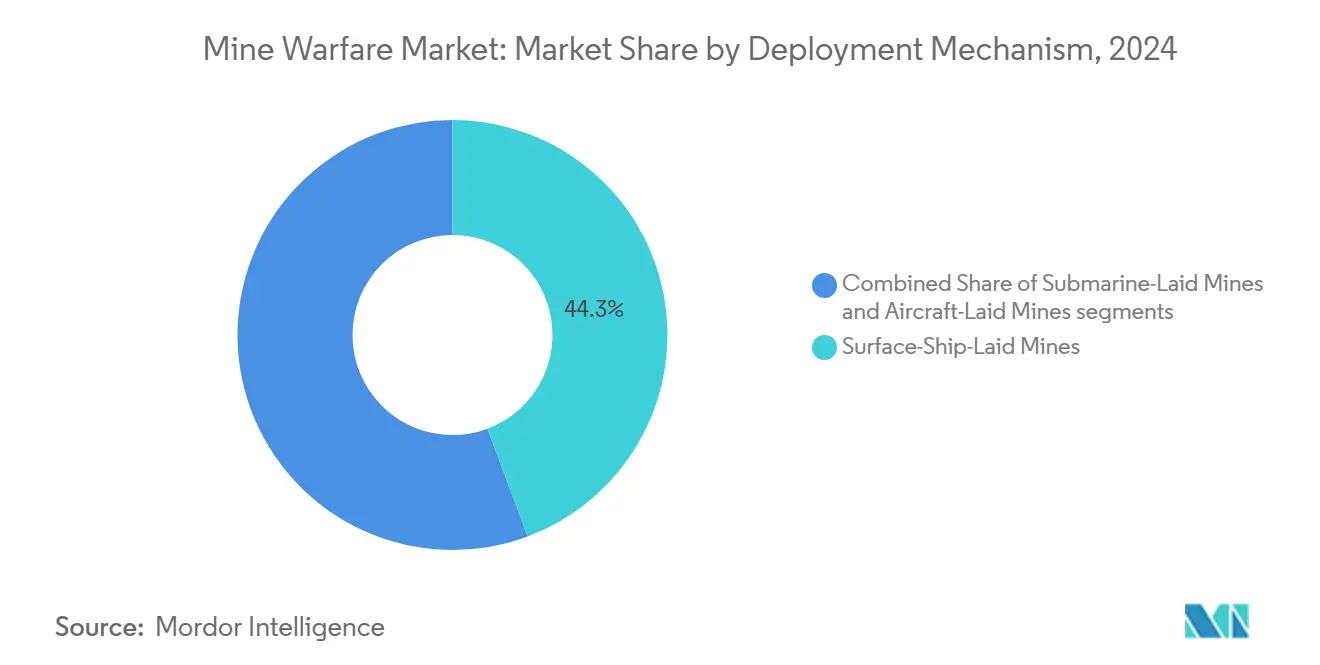

- By deployment mechanism, surface-ship-laid mines accounted for 44.31% of 2024 revenue; aircraft-laid mines recorded the fastest growth at a 7.36% CAGR to 2030.

- By application, defensive mining captured 42.38% of 2024 revenue, whereas mine clearance is forecasted to post a 6.72% CAGR through 2030.

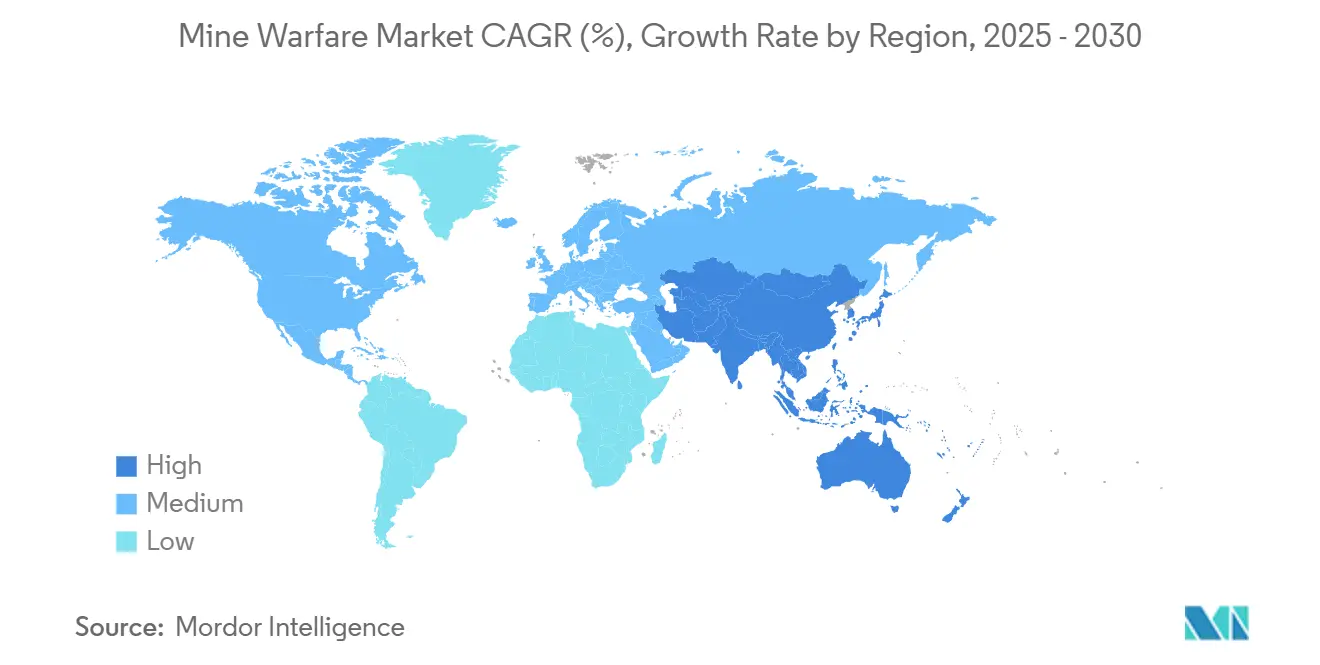

- By geography, North America held 30.25% revenue share in 2024; Asia-Pacific is set to climb at a 7.01% CAGR to 2030.

Global Mine Warfare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense modernization and recapitalization efforts worldwide | +1.2% | NATO members, Asia-Pacific | Medium term (2-4 years) |

| Escalating global defense budgets in response to evolving security threats | +1.0% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Growing demand for precision-guided and extended-range mine warfare capabilities | +0.8% | North America, Europe, advanced Asia-Pacific | Medium term (2-4 years) |

| Expanding adoption of autonomous mine countermeasure (MCM) platforms and drones | +0.9% | Early adoption in North America and Europe | Long term (≥ 4 years) |

| Increasing strategic importance of Arctic maritime routes | +0.4% | Arctic nations: US, Canada, Russia, Nordic countries | Long term (≥ 4 years) |

| Advancements in micro-mine swarming concepts for area-denial operations | +0.3% | Advanced military powers: US, China, Russia, European allies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Modernization and Recapitalization Efforts Worldwide

Armed forces are retiring obsolescent Avenger-class ships and similar legacy assets, channeling funds into autonomous or optionally crewed systems that integrate machine learning, high-resolution sonar, and real-time data fusion. European navies echo the pattern by procuring motherships with containerized mission bays, ensuring rapid swap-out of toolkits for evolving threats. This wave boosts electronics suppliers that deliver low-power processors and encryption modules certified for NATO networks. Standardization frameworks streamline multinational deployments, allowing allied forces to share autonomous craft and standard operator consoles during joint exercises. Procurement pipelines lengthen vendor visibility yet intensify compliance audits, favoring established integrators.

Escalating Global Defense Budgets in Response to Evolving Security Threats

Record outlays in 2024 showcased Japan’s 26.3% budget jump, with a prominent slice earmarked for maritime domain awareness and MCM assets.[1]Japan Ministry of Defense, “Defense Budget 2024,” MOD, mod.go.jp The South China Sea, the Baltic approaches, and the Arctic sea lanes drive similar prioritization among blue-water and regional navies. Policy makers highlight that conventional surface combatants remain susceptible to low-cost mines, compelling the procurement of specialized sensors and neutralizers. Multi-year funding commitments cushion vendors from short-term fiscal swings, sustaining the mine warfare market even when other naval programs face rescheduling. Elevated appropriation levels also encourage second-tier suppliers to invest in up-skilling and certification, broadening the industrial base.

Growing Demand for Precision-Guided and Extended-Range Mine Warfare Capabilities

Quickstrike-ER trials illustrate the strategic appeal of stand-off mine drops from beyond defended airspace, which widens operational envelopes for fixed-wing and rotary aircraft. Modern influence mines embed multi-axis magnetometers, pressure sensors, and acoustic arrays that permit target discrimination down to specific hull signatures. Programmable fuzes allow dynamic activation windows, enabling commanders to align deterrent effects with political objectives. The documentation burden rises because each software block must satisfy weapon-safety certifications, creating an ecosystem where prime contractors orchestrate niche component vendors. Research funding also targets resilient power systems that keep inert mines ready for activation over multi-year deployments.

Expanding Adoption of Autonomous MCM Platforms and Drones

Contracts worth several hundred million euros awarded to Exail in 2025 confirmed market appetite for unmanned surface and underwater drones that can sweep or neutralize mines while crews remain outside threat envelopes.[2]Exail Communications, “Exail Secures Major Contracts for Autonomous Systems,” Exail, exail.com The Littoral Combat Ship (LCS) program bundles unmanned vehicles, towed sonars, and expendable neutralizers, illustrating how host ships now serve as command nodes rather than sweeping assets. Autonomy software continuously refines object-recognition models, leveraging mission logs that feed cloud-based trainers once security protocols permit. Although regulators still refine legal frameworks, early adopters benefit from iterative trials that de-risk operational doctrines. Suppliers that couple edge processing with secure mesh networking gain a competitive edge as navies demand swarm coordination among heterogeneous vehicles.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict adherence to international arms control treaties | −0.8% | Ottawa Convention signatories | Medium term (2-4 years) |

| High procurement and life-cycle costs of advanced influence mines and MCM kits | −1.1% | Navies with limited budgets | Short term (≤ 2 years) |

| Operational challenges due to false-positive rates in counter-mine detection systems | -0.5% | Global, affecting all users of automated detection systems | Medium term (2-4 years) |

| Supply chain vulnerabilities in critical components such as rare-earth magnetometers | -0.6% | Global, with particular impact on Western manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Adherence to International Arms Control Treaties

Although naval mines fall outside the Ottawa Convention, political scrutiny over mine deployment obliges signatories to justify risk-mitigation measures and civilian-safety safeguards.[3]International Committee of the Red Cross, “Anti-Personnel Mines: Overview,” ICRC, icrc.org Legal reviews add layers of documentation, verification testing, and export-license approvals that slow startup market entry. Sophisticated discrimination logic helps meet humanitarian expectations yet inflates cost and complexity. Certification milestones require instrumented range tests that only a handful of governments operate, creating bottlenecks in validation capacity. Established primes, therefore, retain an advantage because they maintain treaty-compliance teams and long-standing rapport with arms-control inspectors.

High Procurement and Life-Cycle Costs of Advanced Influence Mines and MCM Kits

Program experiences with the LCS’s mission package reveal hidden integration expenses as sensor suites, launch-and-recovery systems, and data links must interoperate flawlessly. Influence mines packing multi-sensor arrays, solid-state recorders, and long-life power modules cost multiples of legacy contact mines. Sustaining these assets demands specialized spares, software patches, and periodic re-certification, escalating total ownership outlays. Smaller navies often postpone upgrades, opting for partial capability gaps rather than incur high bills. Despite growing threat awareness, this cost barrier narrows the addressable customer base of the mine warfare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mine Type: Sea Mines Retain Primacy while Smart Mines Accelerate

Sea mines captured 51.24% revenue in 2024, underscoring their low procurement cost and psychological impact that compels adversaries to divert assets toward clearance. The segment forms a dependable recurring base for the mine warfare market because even a modest inventory can deny access to straits or ports for extended periods. Land mines remain niche, tied to littoral choke points and port approaches. In contrast, smart and networked mines are on a 7.35% CAGR path to 2030 as defense planners adopt programmable influence logic to minimize collateral risk.[4]DARPA Communications, “Smart Mine Technology Development,” DARPA, darpa.mil

Smart mines combine on-board processing, secure wireless updates, and inertial navigation correction, enabling precision lethality without indiscriminate area denial. Suppliers able to harden electronics against saltwater corrosion and electromagnetic interference achieve higher margins. Because these devices embed export-controlled semiconductors, the mine warfare market observes strict end-user vetting. Interoperability with maritime command architectures also grows more crucial, steering development budgets toward open standards for command-and-control links. The shift in threat complexity ensures that smart mine sub-vendors specializing in AI inference firmware can enter the mine warfare industry through strategic partnerships with legacy ordnance makers.

By Platform: Surface Vessels Hold Share as Unmanned Underwater Vehicles Surge

Surface mine-countermeasure ships (MCM) controlled 36.27% of revenue in 2024 due to their mission bay volume, embarked command teams, and endurance that sustain multi-day sweeping operations. Their crews oversee sonar-towed bodies, remotely operated vehicles, and mine neutralization charges during complex missions. Nevertheless, unmanned underwater vehicles (UUVs) posted a 6.29% CAGR through 2030, reflecting navies’ desire to remove sailors from minefields. Platform miniaturization allows motherships or even rigid-hull inflatable boats to deploy small AUV swarms that map seabeds at high resolution.

As autonomy matures, the mine warfare market size for UUV solutions is projected to expand steadily, enabling persistent surveillance over hours that surface vessels cannot match. Manufacturers invest in adaptive mission-planning software that allocates search tracks based on probability grids updated in real time. The modular payload bay concept extends platform life by permitting future sensor inserts without hull cuts. This upgrade path encourages navies to adopt leasing or capability-as-a-service arrangements that convert capital expenditure into operating expense, widening the customer pool. Hybrid architectures where a surface craft hosts multiple tetherless AUVs illustrate how traditional ships can coexist with autonomous assets during transition.

By Deployment Mechanism: Surface-Ship Mining Dominates though Aircraft Methods Gain Traction

Surface-ship-laid mines comprised 44.31% of 2024 revenue, rapidly leveraging existing combatant fleets to lay dense minefields. Commanders value the capacity to mix moored, bottom, and rising mines in intricate patterns that challenge clearance forces. Submarine-laid mines provide stealth but are limited by torpedo-tube inventory and competing mission priorities. Aircraft-laid systems, advancing at a 7.36% CAGR, benefit from standoff munitions such as the Quickstrike-ER that allow bomber crews to mine straits without entering hostile airspace.

Precision GPS guidance ensures individual weapons land within narrow lanes, reducing the count needed to achieve blockage probability. The mine warfare market now sees avionics houses collaborating with ordnance divisions to integrate seeker heads capable of terrain contour updates mid-flight. Such integration secures incremental contracts as air forces retrofit legacy aircraft with carriage and release kits. The broadening of delivery options encourages planners to adopt layered mining doctrines, combining surprise aerial seeding and covert submarine drops. This multidimensional concept complicates adversary clearance planning and sustains long-term demand for modeling and simulation software that optimizes field geometry.

By Application: Defensive Mining Leads, Clearance Capabilities Accelerate

Defensive mining represented 42.38% of 2024 revenue, reflecting its established role in shielding naval bases, offshore energy platforms, and undersea cables against incursion. The legal clarity surrounding sovereign waters and recognized exclusion zones supports quick authorization of defensive fields. Offensive mining remains smaller yet strategically potent, shaping sea control during high-end conflict scenarios. Clearance operations deliver a 6.72% CAGR through 2030 as commercial shipping and humanitarian norms compel rapid obstacle removal.

The modern clearance toolkit includes synthetic aperture sonar, expendable detonation devices, and AI-enabled post-mission analysis that slashes false-positive rates. Consequently, navies allocate rising budgets to mine warfare market size segments focused on clearance, aiming to reopen strategic routes within hours rather than days. Companies that bundle training simulators, data analytics, and deployable command posts capture service contracts that outlast initial equipment sales. Humanitarian demining initiatives also tap these technologies, stimulating dual-use demand in regions emerging from conflict and reinforcing year-round revenue streams for defense primes and their civil subsidiaries.

Geography Analysis

North America retained leadership with 30.25% of global revenue in 2024, underpinned by the US Navy’s multibillion-dollar procurement of next-generation sweep, hunt, and neutralize systems. The region benefits from a dense network of software, sensor, and shipbuilding firms clustered around coastal innovation hubs. Canada’s Arctic patrol strategy and Mexico’s coastal security upgrades add incremental orders, broadening the regional customer base.

Europe constitutes a mature yet continuously innovating arena. Joint NATO programs standardize communication interfaces and data formats, enabling pooled mission packages aboard Belgian, Dutch, and French motherships. The United Kingdom’s Multi-Role Ocean Surveillance Ship and Germany’s investment in modular hulls illustrate a commitment to rapid refresh cycles. European contractors often emphasize dual-use payloads suitable for civil hydrography, an approach that spreads fixed costs across defense and commercial segments of the mine warfare market.

Asia-Pacific delivers the fastest regional CAGR at 7.01%. China channels extensive resources into smart mines and autonomous undersea vehicles to reinforce anti-access strategies around the first island chain. India’s Make in India scheme fosters local assembly lines for influence mines, supported by technology-transfer agreements. Japan sustains elevated maritime budgets, while Australia’s submarine program indirectly boosts local suppliers of undersea sensors. South Korea leverages its commercial shipbuilding prowess to prototype small unmanned surface drones configured for counter-mine tasks. The region’s threat perception and industrial depth heterogeneity create a mosaic of partnerships and offsets that enlarge the mine warfare market.

Competitive Landscape

The mine warfare market features moderate consolidation. Legacy primes like Northrop Grumman Corporation secure multiyear awards, including a USD 3.46 billion contract in 2024 that bundles survivability upgrades with autonomous systems. These firms leverage classified test ranges, export-control compliance teams, and vertically integrated sensor lines to defend incumbency. Yet a vibrant cadre of smaller technology houses delivers AI inference engines, fiber-optic gyros, and swarm-control protocols, often via teaming agreements that let primes refresh capability while preserving contractual share.

Strategic moves center on modularity. Vendors design open-architecture payload bays and software-defined sonars that accept algorithm updates during routine maintenance. This approach locks in follow-on service revenue and extends platform relevance beyond initial specifications. Partnerships between shipyards and autonomy specialists also gain traction, as illustrated by Textron Systems’ common unmanned surface craft that serves both MCM and electronic warfare (EW) missions.

Regional alignment shapes competition. European primes co-develop baseline designs to satisfy standard NATO staff requirements, whereas US firms tailor export variants to comply with Foreign Military Sales (FMS) rules. Asian yards increasingly pursue indigenous sensor content to avoid ITAR constraints, opening white-space opportunities for component firms outside the traditional defense orbit. Collectively, these maneuvers maintain a dynamic competitive equilibrium that stimulates continuous innovation across the mine warfare market.

Mine Warfare Industry Leaders

Thales Group

Northrop Grumman Corporation

BAE Systems plc

RTX Corporation

Saab AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Thales Group secured a contract to provide the Republic of Singapore Navy (RSN) with its Pathmaster autonomous MCM system. This system enables navies to detect, classify, and locate mines in maritime environments. This capability is particularly significant for Singapore, which operates in one of Asia's busiest maritime straits.

- May 2025: The US Navy awarded Bollinger Shipyards Lockport LLC a USD 65.7 million contract modification to expand production and implement engineering enhancements for the Navy’s MCM USVs.

Global Mine Warfare Market Report Scope

| Sea Mines |

| Land Mines |

| Smart/Networked Mines |

| Surface Mine-Countermeasure (MCM) Vessels |

| Unmanned Surface Vehicles (USV-MCM) |

| Unmanned Underwater Vehicles (UUV/AUV-MCM) |

| Airborne MCM |

| Land-Based Clearance Systems |

| Submarine-Laid Mines |

| Surface-Ship-Laid Mines |

| Aircraft-Laid Mines |

| Offensive Mining |

| Defensive Mining |

| Mine Clearance |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Mine Type | Sea Mines | ||

| Land Mines | |||

| Smart/Networked Mines | |||

| By Platform | Surface Mine-Countermeasure (MCM) Vessels | ||

| Unmanned Surface Vehicles (USV-MCM) | |||

| Unmanned Underwater Vehicles (UUV/AUV-MCM) | |||

| Airborne MCM | |||

| Land-Based Clearance Systems | |||

| By Deployment Mechanism | Submarine-Laid Mines | ||

| Surface-Ship-Laid Mines | |||

| Aircraft-Laid Mines | |||

| By Application | Offensive Mining | ||

| Defensive Mining | |||

| Mine Clearance | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the mine warfare market in 2030?

The mine warfare market size stood at USD 5.28 billion in 2025 and is forecasted to reach USD 6.71 billion by 2030, translating into a 4.91% CAGR.

Which region is expanding the fastest in mine warfare procurement?

Asia-Pacific is expected to register a 7.01% CAGR through 2030 because of rising Chinese, Indian, and Japanese investments.

Which mine type currently generates the largest revenue?

Sea mines led with 51.24% revenue share in 2024 because of their cost advantage and deterrent impact.

Which platform segment shows the highest growth momentum?

Unmanned underwater vehicles (UUVs) post a 6.29% CAGR due to risk reduction and covert operating profiles.

How are treaties influencing procurement decisions?

Ottawa Convention principles push navies toward smart mines with advanced discrimination, adding compliance costs and favoring established vendors.

What technological trend is reshaping mine countermeasure doctrine?

The integration of autonomous surface and underwater drones enables distributed, crew-safe clearance operations and drives new procurement priorities.

Page last updated on: