Main Battle Tank Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.96 Billion |

| Market Size (2031) | USD 7.97 Billion |

| Growth Rate (2026 - 2031) | 2.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Main Battle Tank Market Analysis by Mordor Intelligence

Main battle tank (MBT) market size in 2026 is estimated at USD 6.96 billion, growing from 2025 value of USD 6.77 billion with 2031 projections showing USD 7.97 billion, growing at 2.75% CAGR over 2026-2031. This measured growth reflects the MBT market’s heavy dependence on long-term government procurement cycles, amplified defense spending across Europe and the Indo-Pacific, and heightened emphasis on hybrid-electric propulsion to reduce frontline fuel exposure. Intensified geopolitical risk following the Ukraine conflict has accelerated acquisition timelines, yet rising unit costs, drone-enabled anti-armor threats, and ESG-linked financing barriers moderate the overall expansion trajectory. Producers prioritize scalable production lines, modular digital architectures, and active protection integration, while export-oriented nations increasingly leverage credit facilities to secure deals in emerging regions. Consolidation among prime contractors and growing public-private partnerships strengthen industrial resilience, positioning the MBT market to weather cyclical budget pressures without severe capacity contractions.

Key Report Takeaways

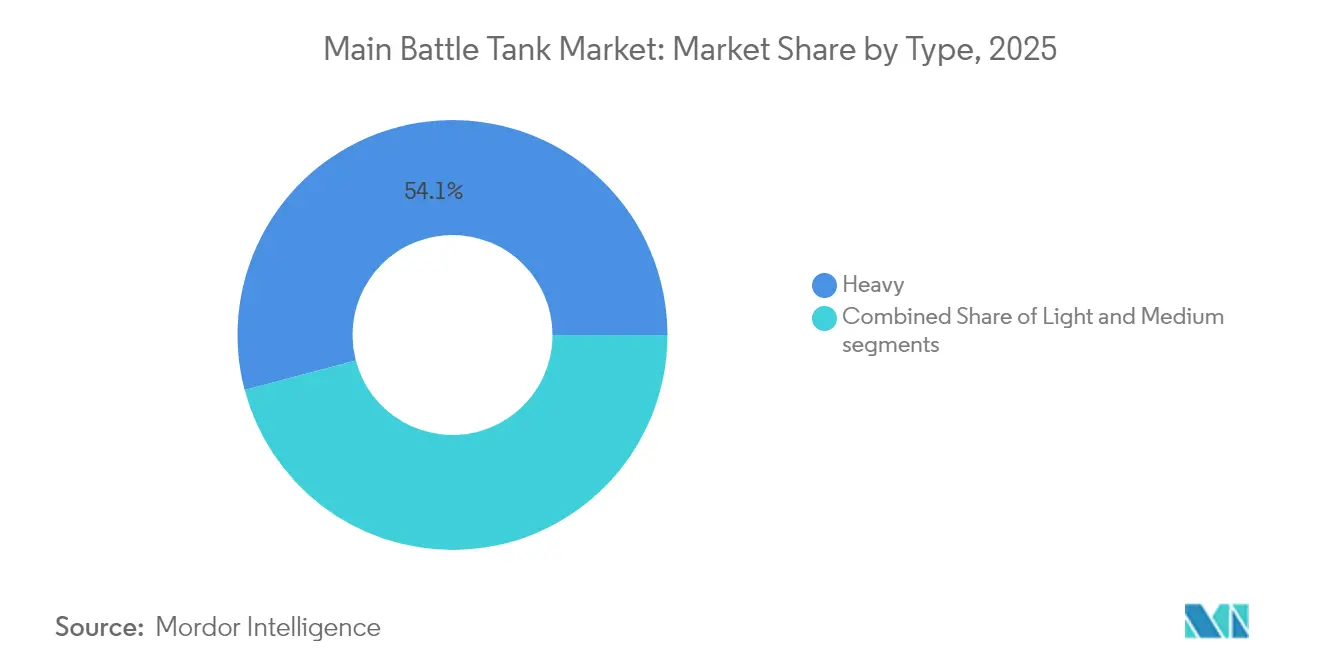

- By type, heavy platforms held 54.12% of the MBT market share in 2025, while light tanks are projected to advance at a 3.11% CAGR through 2031.

- By propulsion, conventional diesel engines accounted for 93.22% of the MBT market size in 2025, yet hybrid-electric systems are set to expand at a 6.18% CAGR during 2026-2031.

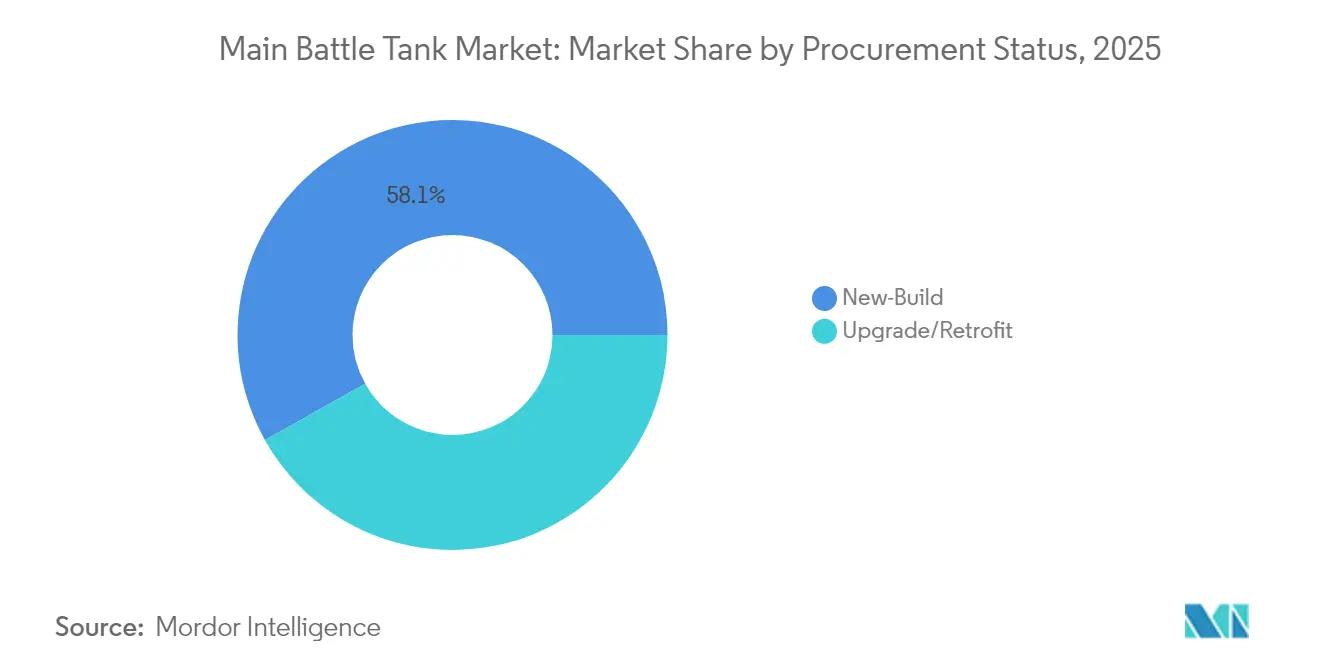

- By procurement status, new-build programs commanded 58.12% revenue in 2025; upgrade and retrofit initiatives show a 3.31% CAGR outlook to 2031.

- By component, hull and armor modules led spending with 31.89% in 2025, whereas fire-control and vetronics are forecasted to post the fastest 3.14% CAGR through 2031.

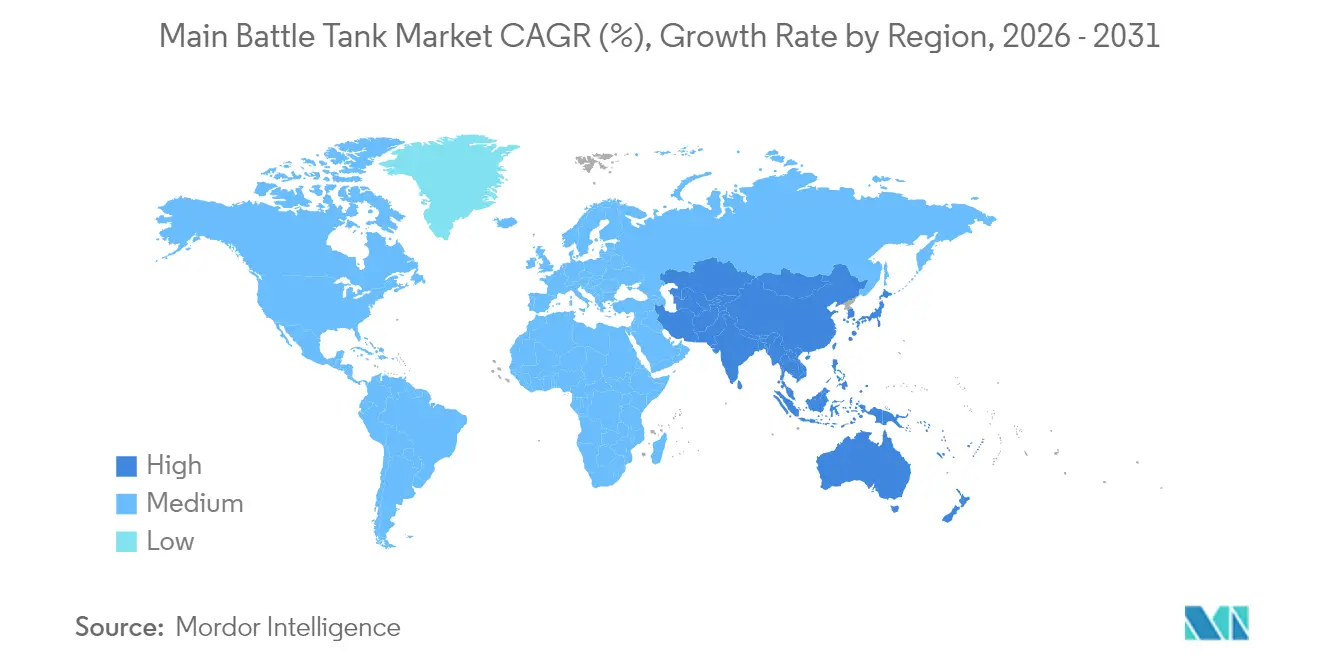

- By geography, Europe generated 30.98% of 2025 revenue, while Asia-Pacific is poised for the quickest 3.41% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Main Battle Tank Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating geopolitical tensions driving new MBT acquisitions | +0.8% | Global, concentrated in NATO and Indo-Pacific allies | Short term (≤ 2 years) |

| Replacement demand for aging Cold War-era armored fleets | +0.6% | Europe, Eastern Europe, select Asia-Pacific nations | Medium term (2-4 years) |

| Increasing need for active protection system (APS)-compatible platforms | +0.5% | North America, Europe, Middle East | Medium term (2-4 years) |

| Adoption of hybrid-electric propulsion to reduce logistical burden | +0.4% | North America, select European programs | Long term (≥ 4 years) |

| Integration of digital twin and predictive maintenance technologies to lower lifecycle costs | +0.3% | Global, advanced militaries | Long term (≥ 4 years) |

| Availability of export credit facilities supporting international MBT sales | +0.2% | Emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Geopolitical Tensions Drive Urgent Procurement

Russia’s 2022 invasion of Ukraine compressed NATO tank acquisition timelines by 18 to 24 months, pushing Poland to finalize a USD 6.5 billion K2 order and Germany to authorize 105 Leopard 2A8 units within a single budget cycle. The MBT market now faces backlogs stretching beyond 36 months, a significant deviation from pre-crisis 24-month norms. US Congressional approval of USD 2 billion for Abrams line modernization assures surge capacity, yet supply chains for armor steel, thermal imagers, and power-pack castings remain fragile.[1]“US Government to allocate USD 2 billion for modernization of Abrams tank production facility,” Defence Industry Europe, defence-industry.eu Rising delivery lead times compel buyers to place multi-year block orders, locking in pricing but limiting flexibility for later technology insertions. Producers respond by dual-sourcing subsystems and pre-financing long-lead items to avoid penalties, reinforcing the MBT market’s trend toward industrial consolidation and vertically integrated risk sharing.

Cold War Fleet Replacement Accelerates Modernization Cycles

NATO inventories still field roughly 8,000 legacy MBTs requiring replacement or deep overhaul before 2030. Programs in Bulgaria, the Czech Republic, and Romania illustrate the scale: unit upgrades cost 40–60% of new builds yet extend service life by only 15–20 years. This calculus steers wealthier states toward fresh platforms that embed active protection, open architecture vetronics, and hybrid drives from inception. Mid-tier allies, unable to fund clean-sheet development, pursue incremental modernization, thereby sustaining a parallel demand stream for retrofit kits. The dual-track approach enlarges the MBT market by blending high-value new-build contracts with lower-margin upgrade work, stabilizing OEM production rates and sparing governments from capability gaps.

Active Protection Systems Integration Reshapes Platform Requirements

Combat data from Gaza and Ukraine propelled Trophy, Iron Fist, and domestic APS into baseline specifications for Western programs. The US M1E3 Abrams embeds APS wiring looms and auxiliary power allocation at the concept stage, avoiding retrofit weight penalties that add 1.5-2 tons and USD 2–3 million per tank. Israeli experience validates APS lethality, but weight and power growth pressures engineers to adopt lighter composite armor to remain under Europe’s 72-ton bridge class limit. Suppliers of radar panels, hard-kill interceptors, and high-rate power converters now enjoy multiyear visibility, while maintenance planners confront higher training and diagnostic workloads. APS diffusion bolsters the MBT market by reinforcing demand for new hulls optimized around these protective suites.

Adoption of Hybrid-Electric Propulsion Addresses Logistical Vulnerabilities

Fuel convoys constituted 40-50% of coalition logistics in recent US operations, exposing armor formations to improvised explosive threats. Hybrid-electric propulsion in the M1E3 promises 20–30% fuel savings and silent mobility for ambush scenarios, albeit at a USD 1–2 million premium over diesel variants. China’s Type 99A prototype and South Korea’s K-engine research highlight global convergence toward similar solutions. Nevertheless, hybrid systems require lithium-ion (Li-ion) safety protocols, electromagnetic interference shielding, and high-voltage technician training that militaries lack at scale. Early adopters will limit fielding to reconnaissance or rapid-reaction units, gradually seeding maintenance expertise before fleet-wide rollout, sustaining a long-tail revenue stream within the MBT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and operating costs compared to other defense priorities | -0.7% | Global, budget-constrained nations | Short term (≤ 2 years) |

| Rising vulnerability to drone-based top-attack and loitering munitions | -0.5% | Global, accelerated by Ukraine lessons | Short term (≤ 2 years) |

| Infrastructure limitations due to bridge-load and mobility constraints in emerging regions | -0.3% | Emerging regions | Medium term (2-4 years) |

| ESG and climate-related policies restricting access to defense capital | -0.2% | Europe, select developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Operating Costs Compared to Other Defense Priorities

Unit prices for Western MBTs routinely exceed USD 12 million, while through-life support may quadruple that figure over 30 years. When juxtaposed with cheaper precision-guided artillery or unmanned systems, many treasuries hesitate to allocate scarce funds to armor. Fuel, track wear, and depot-level maintenance further strain budgets; for instance, the US Army annually costs USD 115,000 in fuel per M1 at 2025 prices. Such economics limit order sizes, impeding economies of scale and perpetuating cost inflation, restraining MBT market expansion.

Rising Vulnerability to Drone-Based Top-Attack and Loitering Munitions

FPV drones costing USD 1,000 destroyed multiple Russian MBTs in Ukraine, yielding a cost-exchange ratio exceeding 1:10,000. High-angle loitering munitions evade frontal armor, forcing crews to retrofit cage defenses that impair turret rotation and add weight. Nations now explore mast-mounted jammers and mini-point defense interceptors, but these countermeasures are still immature. The perception of reduced survivability challenges long-standing doctrines emphasizing heavily armored breakthroughs, encouraging some militaries to divert funds toward dispersed firepower and mobile short-range air defense instead of large MBT fleets, constraining MBT market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Heavy Platforms Reinforce High-Intensity Capabilities

Heavy MBTs commanded 54.12% of 2025 revenue, reflecting entrenched preferences for maximal protection, 120/125 mm main guns, and layered active protection. These tanks constitute the backbone of NATO deterrence formations and dominate premium export orders to Eastern Europe and the Gulf. Though smaller in revenue, light MBTs register the swiftest 3.11% CAGR on the strength of expeditionary requirements, urban maneuverability, and lower infrastructure demands. The US M10 Booker illustrates the class’s ability to deliver direct fire while air-deployable within a C-17 load plan. Emerging doctrines envision mixed brigades where light units secure flanks and penetrate complex terrain. At the same time, heavy spearheads exploit breakthroughs, ensuring the MBT market addresses a spectrum of threat environments.

Operational data suggests heavy types endure longer when facing advanced anti-tank guided missiles thanks to modular composite armor, whereas light variants rely on mobility and sensor fusion. Asian buyers with archipelagic territories, such as the Philippines, favor lighter hulls to traverse limited bridge networks, while European states bordering Russia insist on Leopard 2A8-equivalent protection levels. The bifurcation sustains parallel production lines, expanding supplier opportunities for tailored drivetrains, suspension systems, and gun-mount configurations. Consequently, both weight classes are expected to coexist through 2030, supporting a resilient MBT market that pivots between strategic depth and tactical agility.

By Propulsion: Diesel Dominance Confronts Hybrid Momentum

Conventional diesel engines powered 93.22% of deliveries in 2025 owing to their maturity, established depot infrastructure, and lower procurement costs. The MTU 883, Caterpillar C32, and Ukrainian 6TD families remain standard across NATO and non-aligned inventories. However, hybrid-electric prototypes record a 6.18% CAGR outlook as nations pursue reduced fuel logistics and enlarged onboard electrical reserves for sensors and directed-energy defense. Early modeling indicates 20–30% fuel savings and silent-watch endurance of >8 hours, an attractive radar signature mitigation asset.

While battery thermal-runaway risks and high-voltage maintenance complexities curb immediate mass adoption, the US M1E3’s 2025 preliminary design review validates a path toward serial production by 2029. Europe’s MGCS consortium and Korea’s K-drive project plan have similar architectures, suggesting a tipping point in the late 2020s when hybrid propulsion penetrates frontline units. Providers of power electronics, cooling subsystems, and energy management software gain leverage, expanding the MBT market size for propulsion-adjacent solutions.

By Procurement Status: New-Build Supremacy Endures Amid Fiscal Realism

New-build orders captured 58.12% of 2025 spending, propelled by Poland’s K2 program, Germany’s Leopard 2A8 tranche, and continuing US Foreign Military Sales (FMS) for M1A2 SEPv3. These contracts reward impossible capabilities to embed economically in legacy hulls, such as integrated APS, open C4ISR backbones, and hybrid power packs. Nevertheless, retrofit activity, growing at 3.31% CAGR, provides a lifeline to countries with constrained budgets yet urgent operational needs. Upgrades typically include armor packages, third-generation thermal sights, and data-bus conversion, costing 40–60% of a new unit and extending service life by roughly 15 years.

The dichotomy sustains a dual revenue stream: high-margin, technologically advanced new builds and steady, volume-driven upgrade kits. OEMs leverage commonality strategies—installing similar fire-control computers across variants—to optimize inventory and training. This blended approach shelters the MBT market from cyclical defense downturns, as retrofit demand often peaks when capital budgets tighten, smoothing utilization of assembly lines and sustaining skilled labor pools.

By Component: Armor Dominance Meets Electronics Ascendancy

Hull and armor modules led the 2025 spending at 31.89%, driven by escalating ballistic threats and the adoption of modular reactive or composite tiles. Next-generation armor suites cost USD 2–4 million per vehicle, underscoring their revenue heft. Yet electronics—specifically fire-control and vetronics—register the quickest 3.14% CAGR, propelled by AI-assisted target recognition, 360° situational awareness, and digitized maintenance logging. The MBT market increasingly values software-definable capabilities, allowing mid-life upgrades through line-replaceable units rather than structural overhauls.

Powerpack and drivetrain segments benefit from hybrid transition, spurring demand for high-density motors, inverters, and thermal management. Turret and central gun systems experience incremental growth as programmable ammunition and autoloader designs proliferate. Suppliers that bundle armor, electronics, and propulsion into cohesive upgrade paths strengthen competitive moats, signaling a gradual shift from discrete component sales toward integrated capability packages across the MBT market.

Geography Analysis

Europe generated 30.98% of 2025 revenue, driven by Germany’s commitment to defense spending at 3.5% of GDP by 2029 and large-scale Leopard 2A8 procurements. The Franco-German MGCS program aligns industrial champions KNDS, Rheinmetall, and Thales in a flagship collaboration that is expected to define future European requirements. Simultaneous Eastern European demand, motivated by proximity to the Ukraine conflict, further reinforces continental dominance in the MBT market.

Asia-Pacific presents the most dynamic outlook with a 3.41% CAGR, underpinned by India’s 10% defense budget hike, Japan’s record allocations, and Korea’s K2 export momentum to Poland and prospective customers in the Gulf. Australia’s LAND 400 Phase 3 and the Philippines’ armored modernization add breadth, while China’s indigenous production ensures regional competitive pressure. North America retains strategic importance through continuous Abrams upgrades and the transformational M1E3 project, whereas the Middle East exhibits selective, high-value acquisitions balanced by fiscal reforms and localization mandates. Africa’s demand remains episodic due to infrastructure and finance constraints, limiting its contribution to the global MBT market.

Competitive Landscape

The Main Battle Tank (MBT) market demonstrates moderate concentration, with General Dynamics Corporation, Rheinmetall AG, Hyundai Rotem Company, KNDS N.V., and Uralvagonzavod controlling the bulk of active production lines. These firms leverage decades of machining expertise, vertically integrated supply chains, and privileged government relationships to secure repeat orders. Recent mergers—Leonardo’s EUR 1.7 billion (USD 2 billion) acquisition of Iveco Defence and Rheinmetall’s USD 950 million purchase of Loc Performance—expand capacity for hull fabrication, suspension systems, drivetrain assembly, streamlining cost structures.

Strategic alliances reshape competition: the MGCS consortium aligns Franco-German competencies, while Leonardo-Rheinmetall Military Vehicles positions Italy for domestic replacement programs and export campaigns. Technology differentiation revolves around hybrid propulsion, AI-enabled fire control, and open-architecture vetronics, with suppliers racing to embed cybersecurity-hardened Ethernet backbones that allow software upgrades without invasive rewiring. Active protection remains a decisive discriminator; firms offering integrated hard-kill plus soft-kill suites command pricing premiums exceeding 15% per unit, reinforcing profitability in the MBT market.

Export barriers include ITAR, EU dual-use rules, and ESG financing hurdles; consequently, primes cultivate offset packages and licensed production to satisfy local-content regulations. Smaller competitors such as John Cockerill leverage niche turret expertise to partner with regional chassis makers, while Hanwha Defense exploits competitive K2 pricing bolstered by Korean export credits. The interplay of consolidation, innovation, and policy constraints yields a dynamic but disciplined MBT market environment resistant to disruptive new entrants yet sufficiently competitive to restrain monopolistic pricing.

Main Battle Tank Industry Leaders

General Dynamics Corporation

KNDS N.V.

Rheinmetall AG

Dzerzhinsky Uralvagonzavod Research and Production Corporation (Rostec)

Hyundai Rotem Company (Hyundai Motor Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Czech Republic signed a EUR 1.34 billion (USD 1.57 billion) contract with the German Federal Office of Bundeswehr Equipment and KNDS Deutschland for 44 Leopard 2A8 MBTs, with an option for 14 more, deliveries starting in 2028.

- July 2025: General Dynamics Corporation received a USD 150 million contract for the Abrams Engineering Program to develop new technologies for the US Army's M1E3 Abrams next-generation MBT.

- May 2025: Poland received 19 M1A2 SEPv3 Abrams MBTs from the US. The tanks will integrate into the Polish Army's operational formations, enhancing the country's armored capabilities.

Global Main Battle Tank Market Report Scope

Main battle tanks are pivotal assets in contemporary military arsenals. These tanks, designed to fulfill both maneuver and armor-protected direct-fire roles, are at the forefront of many nations' defense strategies. With escalating national security apprehensions, countries are increasingly investing in advanced battle tanks and enhancing their existing military hardware. These modern main battle tanks are typically grouped into armored units, often working in tandem with infantry forces. Moreover, they are frequently deployed in conflict regions, bolstered by surveillance and ground aircraft.

The main battle tank market is segmented by type and geography. By type, it is divided into light, medium, and heavy. The report also covers the market sizes and forecasts for the main battle tank market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Light |

| Medium |

| Heavy |

| Conventional Diesel |

| Hybrid-Electric |

| New-Build |

| Upgrade/Retrofit |

| Hull and Armor Modules |

| Turret and Main Gun Systems |

| Powerpack and Drivetrain |

| Fire-Control and Vetronics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Light | ||

| Medium | |||

| Heavy | |||

| By Propulsion | Conventional Diesel | ||

| Hybrid-Electric | |||

| By Procurement Status | New-Build | ||

| Upgrade/Retrofit | |||

| By Component | Hull and Armor Modules | ||

| Turret and Main Gun Systems | |||

| Powerpack and Drivetrain | |||

| Fire-Control and Vetronics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the Main Battle Tank Market?

The Main Battle Tank (MBT) market size is expected to reach USD 6.96 billion in 2026 and grow at a CAGR of 2.75% to reach USD 7.97 billion by 2031.

What is the current Main Battle Tank Market size?

In 2026, the MBT market size is expected to reach USD 6.96 billion.

Who are the key players in Main Battle Tank Market?

General Dynamics Corporation, BAE Systems plc, Rostec, Hyundai Rotem Company and KNDS N.V. are the major companies operating in the MBT market.

Which is the fastest growing region in Main Battle Tank Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Main Battle Tank Market?

In 2025, the Europe accounts for the largest market share in MBT market.

Page last updated on: