Underwater Warfare Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

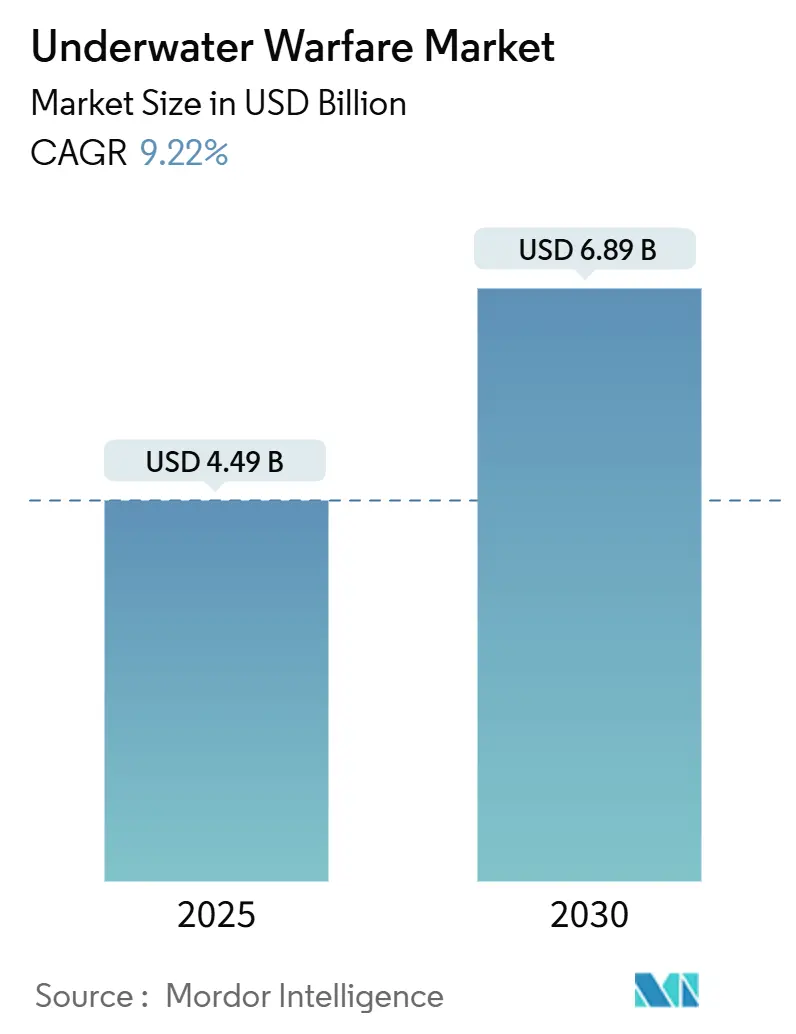

| Market Size (2025) | USD 4.49 Billion |

| Market Size (2030) | USD 6.89 Billion |

| Growth Rate (2025 - 2030) | 9.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

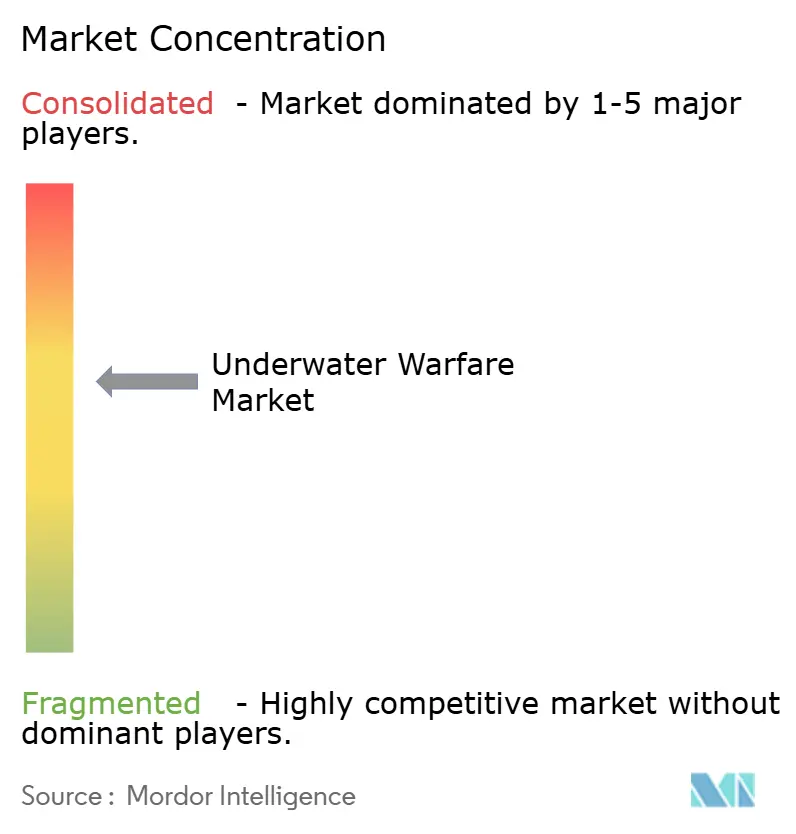

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Underwater Warfare Market Analysis by Mordor Intelligence

The underwater warfare market size stands at USD 4.49 billion in 2025 and is forecasted to reach USD 6.98 billion by 2030, reflecting a 9.22% CAGR. Persistent submarine proliferation, intensifying geopolitical rivalry in contested seas, and rapid innovation in autonomous platforms sustain demand momentum across all major procurement programs. Accelerated shipbuilding outlays such as the United States Navy’s USD 33.30 billion fiscal-2025 request and sizeable regional modernization plans in Asia-Pacific and Europe further anchor the growth outlook. Technology adoption trends emphasize artificial intelligence (AI) -driven acoustic processing, lithium-ion (Li-ion) propulsion upgrades, and distributed unmanned networks that extend underwater coverage while curbing human risk. Cost headwinds tied to nuclear-powered platforms and export-control restrictions moderate but do not derail the expansion path, as mid-tier navies turn to diesel-electric and unmanned alternatives that compress life-cycle expenditures. Competitive dynamics reveal moderate consolidation among incumbent defense primes. Yet, niche suppliers specializing in batteries, sensors, and machine learning (ML) algorithms steadily garner program wins that tilt the playing field toward collaborative, best-of-breed system architectures.

Key Report Takeaways

- By platform, submarines led the underwater warfare market with 39.74% of the share in 2024, while unmanned systems are projected to post the fastest 12.45% CAGR through 2030.

- By system type, weapon systems commanded 32.10% of the underwater warfare market in 2024; unmanned underwater vehicles should advance at a 13.40% CAGR to 2030.

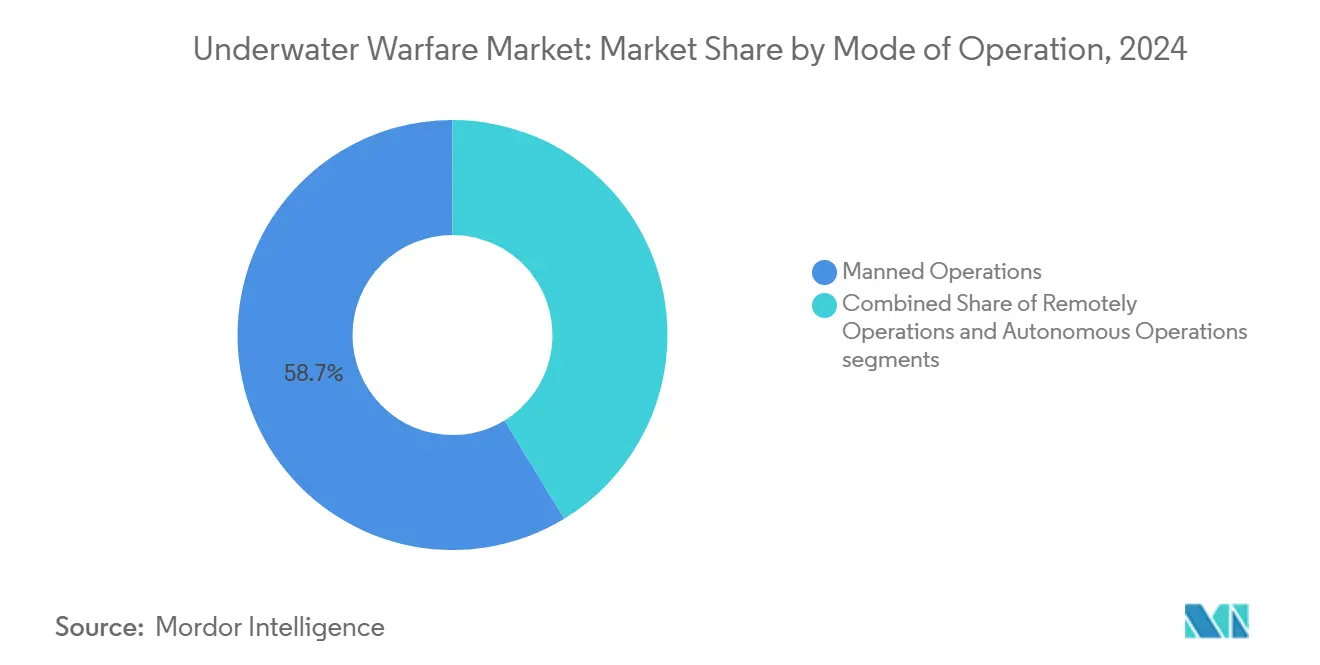

- By mode of operation, manned systems accounted for 58.70% of 2024 revenue, whereas autonomous operations are set to grow at a 12.10% CAGR during the forecast window.

- By application, anti-submarine warfare (ASW) generated 46.25% of 2024 revenue; intelligence, surveillance, and reconnaissance (ISR) applications are on course for an 11.74% CAGR to 2030.

- By geography, North America retained a 38.95% revenue lead in 2024, while Asia-Pacific is positioned for a 12.70% CAGR through 2030.

Global Underwater Warfare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising naval modernization budgets | +2.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| Growing submarine proliferation in contested littorals | +1.8% | Asia-Pacific, Europe, Middle East | Long term (≥ 4 years) |

| Rapid adoption of UUVs for persistent ISR and MCM | +1.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Demand for next-generation sonar and signal-processing suites | +1.3% | Global | Medium term (2-4 years) |

| Mini-sized “sonobuoy-AUV” hybrids enabling airborne swarm ASW | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Li-ion and solid-state battery breakthroughs | +1.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Naval Modernization Budgets

Global defense spending allocates a widening share to maritime programs, with capital flowing to hull construction, submarine procurement, and sensor refresh cycles. The United States Navy increased fiscal-2025 shipbuilding spending by 12% and earmarked USD 1.2 billion for advanced undersea technologies. Japan raised its 2024 defense allocation by 16.9% to JPY 8.9 trillion (USD 60.41 billion) to accelerate indigenous submarine and ASW helicopter upgrades. Australia’s long-horizon AUKUS roadmap valued at AUD 368 billion (USD 245.32 billion) illustrates how alliance commitments funnel resources toward nuclear-powered deterrence. Parallel fleet-recapitalization cycles across NATO members and Indo-Pacific partners enlarge order books for sonar suites, torpedoes, and combat system retrofits. Collectively, these budget expansions underpin multi-year procurement stability, shielding the underwater warfare market from cyclical volatility.

Growing Submarine Proliferation in Contested Littorals

China’s inventory crossed 60 hulls in 2024, including 12 nuclear-powered attack boats, stimulating counter-investments among Indo-Pacific navies.[1]Source: Office of Naval Intelligence, “Worldwide Submarine Challenges Report,” oni.navy.mil Smaller states such as Iran, with coastal minisubs, and North Korea, with an estimated 70-boat fleet, leverage diesel-electric technologies to threaten chokepoints. Enhanced quieting techniques and air-independent propulsion enable diesel boats to rival nuclear counterparts in acoustic discretion within shallow littorals, forcing expensive sensor upgrades on patrol assets. Regional tension elevates demand for persistent surveillance platforms, helicopter dipping sonars, and quick-reaction torpedoes able to operate effectively in cluttered acoustic environments.

Rapid Adoption of UUVs for Persistent ISR and MCM

Navies increasingly field unmanned underwater vehicles to sustain 24/7 monitoring of sea lanes without exposing crews. The US Navy’s Extra Large Unmanned Underwater Vehicle (XLUUV) program, although 64% over budget, remains central to plans for distributed undersea sensing.[2]Source: U.S. Government Accountability Office, “Navy Shipbuilding: Past Performance Provides Valuable Lessons,” gao.gov Ultra Maritime collaborates with primes on dual-role platforms that combine mine countermeasures and ASW payloads. Australia’s Ghost Shark prototype exhibits a 6,000-nautical-mile range, demonstrating how battery and autonomy advances deliver strategic reach. Networked UUV swarms triangulate acoustic signatures and relay data to surface combatants, compressing kill-chain timelines and amplifying situational awareness across theaters.

Demand for Next-Generation Sonar and Signal-Processing Suites

Lockheed Martin’s USD 502.20 million AN/SQQ-89A(V)15 contract evidences sustained spending on AI-enabled acoustic combat systems. Deep-learning models differentiate biological noise from genuine threats, cutting false-alarm rates that consume operator bandwidth. Physics-based data augmentation methods, funded by the US Navy’s SBIR office, expand training datasets when real submarine recordings are scarce.[3]Source: Office of Naval Research, “Undersea Warfare Research and Development,” onr.navy.mil Distributed acoustic sensing on seabed fiber-optic lines widens detection grids, while onboard processors initiate automated countermeasure recommendations. These enhancements collectively lift detection confidence and reduce engagement latency.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and life-cycle costs of nuclear/XLUUV platforms | -1.4% | Global | Long term (≥ 4 years) |

| Export-control and ITAR constraints on cross-border subsystem trade | -0.9% | Global | Medium term (2-4 years) |

| Shortage of skilled acoustic-AI talent for real-time threat classification | -0.7% | Developed markets | Short term (≤ 2 years) |

| Increasing vulnerability of acoustics to AI-driven counter-detection | -0.5% | Advanced naval powers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Life-Cycle Costs of Nuclear/XLUUV Platforms

Next-generation SSN(X) boats may cost USD 6 billion–USD 8 billion per hull 40% above today’s Virginia class, before accounting for nuclear refueling and depot-maintenance outlays that easily double ownership expense. Extra-large UUV prototypes exceed budgeted targets, extending delivery schedules and straining procurement portfolios. Nations lacking deep coffers postpone or shrink submarine buys, opting for incremental upgrades or small unmanned surrogates that temper overall underwater warfare market expansion.

Export-Control and ITAR Constraints on Subsystem Trade

AUKUS partners navigate protracted licensing cycles for acoustic processors and propulsion modules because US export rules tightly circumscribe technology transfer. Similar hurdles slow European integration efforts when US components underpin indigenous projects, forcing parallel R&D investments that duplicate cost and schedule. ITAR rigidity also hampers in-service support; delayed software patches or sensor replacements can ground frontline units, eroding fleet readiness and dampening procurement enthusiasm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Submarines Maintain Dominance, Unmanned Systems Accelerate

The submarine segment commanded 39.74% of 2024 revenue, anchoring the underwater warfare market through its dual role as hunter and high-value deterrent. The underwater warfare market size contribution from these platforms continues to rise on the back of planned SSN(X) procurements in the United States and conventional boat replacement cycles across Europe. Surface combatants remain essential for layered ASW, deploying towed arrays and helicopter assets that multiply detection probability in blue-water and littoral operations. Naval helicopters occupy a niche for rapid, localized prosecution, especially when equipped with updated dipping sonars and lightweight torpedoes.

Unmanned systems post the highest 12.45% CAGR, propelled by cost-effective persistence and reduced personnel risk. Breakthroughs in lithium-ion energy density, pressure-tolerant electronics, and autonomy algorithms let large-displacement UUVs shadow adversary subs for weeks. These advantages reshape force-structure planning as navies blend manned and unmanned assets to achieve 24/7 coverage at lower operating costs. Smaller coastal states also leverage modular UUV kits as an affordable entry into underwater surveillance, broadening end-user diversity and reinforcing growth for the underwater warfare market.

By System Type: Weapons Dominate as UUVs Surge

Weapon systems held a 32.10% share in 2024, reflecting the indispensability of torpedoes, rockets, and depth charges for terminal engagement. Integrated combat-system contracts, such as the AN/SQQ-89A(V)15 award, bundle these munitions with fire-control algorithms, raising average deal size and sustaining revenue concentration among platform primes. Communication and surveillance suites constitute the second-largest block, fusing acoustic sensors, secure data links, and decision-support software into cohesive kill chains.

Unmanned underwater vehicles (UUVs), at a 13.40% CAGR, bring disruptive momentum as navies shift budget priority from weapon volume to sensor persistence. The underwater warfare market share for UUVs is poised to expand sharply once XLUUVs transition from low-rate initial production to serial builds. Suppliers focusing on batteries, modular payload bays, and autonomy software increasingly partner with primes to integrate best-available tech, promoting a more open-system procurement philosophy that favors agile entrants alongside traditional leaders.

By Mode of Operation: Autonomous Systems Challenge Manned Dominance

Manned platforms represented 58.70% of revenue in 2024, underscoring current reliance on human-in-the-loop decision cycles for weapons release and threat assessment. However, the underwater warfare industry anticipates a central pivot: autonomous operations are forecast to rise at 12.10% CAGR, overtaking remotely operated systems as machine-learning classifiers achieve 95%-plus identification accuracy in sea trials. NATO’s doctrine still mandates human authorization to fire, yet patrol and data-gathering missions increasingly transition to autonomous control, freeing crewed vessels for high-value tasks.

Remotely operated vehicles (ROVs) bridge this evolution, delivering real-time teleoperation when engagement rules or complex tasks exceed current AI capabilities. The incremental autonomy approach ensures continuity of tactics, techniques, and procedures while mitigating risk, enabling navies to validate algorithms gradually before granting complete mission independence.

By Application: ASW Leads While ISR Expands

Anti-submarine warfare (ASW) applications generated 46.25% of 2024 turnover, mirroring the market’s core purpose. Asia-Pacific threat perceptions and NATO fleet-protection requirements sustain procurement of torpedoes, sonars, and combat-system upgrades, enlarging the underwater warfare market size. Mine-countermeasure platforms capitalize on overlapping technology stacks, particularly UUVs, to secure littoral approaches and harbor entrances without duplicating fleets.

Intelligence, surveillance, and reconnaissance (ISR) are the fastest-growing applications at 11.74% CAGR, driven by the demand for persistent situational awareness over vast oceans. Multi-mission sensor packages fitted to UUVs and buoy networks collect environmental and target data that feed command centers in near real time. Seabed warfare interest grows in parallel as competition for undersea infrastructure protection rises, opening incremental opportunities for cable-monitoring sensors and sabotage-resistant nodes.

Geography Analysis

North America accounted for 38.95% of 2024 revenue, reflecting the US Navy’s unmatched procurement scale, robust supplier base, and long-horizon undersea priorities. Ongoing Virginia-class builds, SSN(X) design work, and substantial R&D allocations in unmanned systems keep the underwater warfare market firmly anchored in the region. Canada adds incremental demand through NORAD coastal-defense enhancements, and Mexico slowly modernizes patrol forces, albeit at lower budget levels.

Asia-Pacific records the steepest growth trajectory at 12.70% CAGR to 2030. China’s fleet expansion compels neighboring navies to acquire advanced ASW sensors, torpedoes, and helicopter upgrades. Japan directs rising budgets toward indigenous diesel-electric boats and MH-60R modernization, while South Korea invests KRW 1.5 trillion (USD 1.08 billion) in next-generation Blue Shark torpedoes. Australia’s AUKUS pathway reshapes regional undersea strategy, stimulating domestic industrial participation and allied technology transfers.

Europe forms a mature yet innovative hub. Joint programs Belgium-Netherlands rMCM, France-Italy-UK sonar collaborations spread development cost and foster interoperability. Germany’s U212CD, Norway’s next-gen boats, and Poland’s Orka contest maintain procurement cadence for sensors and combat systems. Mediterranean and Baltic security concerns also encourage incremental purchases of helicopter dipping sonars and variable-depth arrays, sustaining mid-single-digit growth.

Competitive Landscape

The underwater warfare market features moderate consolidation, with leading contractors Lockheed Martin Corporation, RTX Corporation, L3Harris Technologies Inc., Northrop Grumman Corporation, and thyssenkrupp Marine Systems GmbH (thyssenkrupp AG) controlling sizeable portions of the sonar, combat system, and weapon segments. Prime-led portfolios integrate vertically, from acoustic arrays to software suites, leveraging longstanding security credentials and global support networks.

Emergent players exploit technology gaps in autonomy, batteries, and AI. Anduril Industries champions scalable large-UUV architectures; Kraken Robotics supplies high-density energy packs; specialist software firms refine machine-learning models for signature classification. Strategic alliances proliferate: Ultra Maritime partners with European navies for dual-purpose UUVs, and Samsung SDI teams with Hanwha Ocean on lithium-ion powertrains, illustrating how subsystem innovators embed within prime-contractor ecosystems.

Competitive tactics emphasize open-architecture interfaces, lifecycle support, and in-service upgrades. Export-control relaxation among allies could shift share away from incumbents toward multinational consortia skilled at integrating best-of-breed components agilely. Yet program risk, cybersecurity mandates, and sovereign industrial-base policies still favor established vendors for mission-critical contracts.

Underwater Warfare Industry Leaders

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

thyssenkrupp Marine Systems GmbH (thyssenkrupp AG)

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lockheed Martin Corporation was awarded a USD 502.2 million US Navy contract for the production and support of the AN/SQQ-89A(V)15 undersea warfare combat system.

- January 2025: Mazagon Dock Shipbuilders (MDL) and thyssenkrupp Marine Systems GmbH secured approval to build six advanced conventional submarines for the Indian Navy jointly.

Global Underwater Warfare Market Report Scope

| Submarines |

| Surface Ships |

| Naval Helicopters |

| Unmanned Systems |

| Weapon Systems |

| Communication and Surveillance Systems |

| Sensors and Computing |

| Countermeasure Systems and Payloads |

| Unmanned Underwater Vehicles (UUVs) |

| Manned Operations |

| Remotely Operations |

| Autonomous Operations |

| Anti-Submarine Warfare (ASW) |

| Mine Countermeasures (MCM) and Seabed Warfare |

| Intelligence, Surveillance and Reconnaissance (ISR) |

| Offensive Strike and Area-Denial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Submarines | ||

| Surface Ships | |||

| Naval Helicopters | |||

| Unmanned Systems | |||

| By System Type | Weapon Systems | ||

| Communication and Surveillance Systems | |||

| Sensors and Computing | |||

| Countermeasure Systems and Payloads | |||

| Unmanned Underwater Vehicles (UUVs) | |||

| By Mode of Operation | Manned Operations | ||

| Remotely Operations | |||

| Autonomous Operations | |||

| By Application | Anti-Submarine Warfare (ASW) | ||

| Mine Countermeasures (MCM) and Seabed Warfare | |||

| Intelligence, Surveillance and Reconnaissance (ISR) | |||

| Offensive Strike and Area-Denial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the underwater warfare market in 2025?

The market is valued at USD 4.49 billion in 2025, and is forecasted to reach USD 6.98 billion by 2030, reflecting a 9.22% CAGR.

Which platform category leads spending today?

Submarines hold the top spot with 39.74% revenue share in 2024, reflecting their central role in both offensive and defensive ASW missions.

What technology trend most accelerates future growth?

Autonomous UUVs , expanding at a 13.40% CAGR, drive persistent ISR and cost-effective patrol capabilities.

Which region will grow fastest by 2030?

Asia-Pacific is projected to advance at a 12.70% CAGR as regional navies counter expanding submarine fleets.

What is the key restraint on procurement?

High acquisition and life-cycle costs for nuclear submarines and extra-large UUVs limit budgets, particularly for mid-tier navies.

How consolidated is the supplier landscape?

Five prime contractors capture just over 60% of revenue, producing a moderate concentration level and leaving room for specialized technology challengers.

Page last updated on: