Military Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

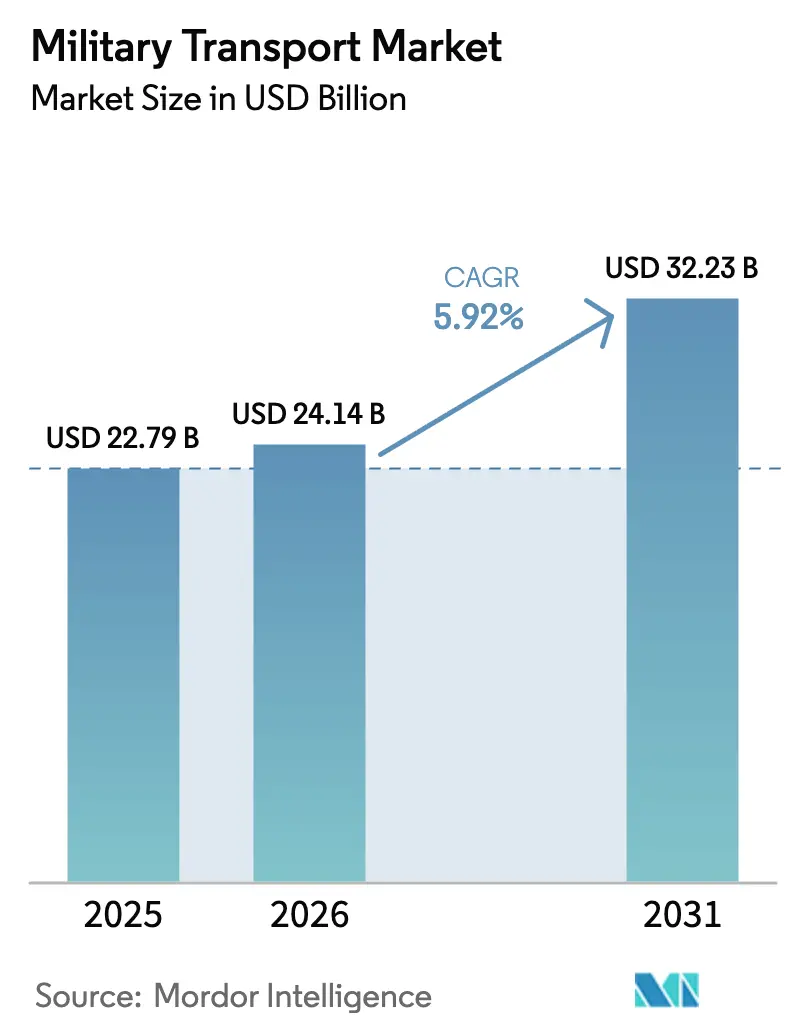

| Market Size (2026) | USD 24.14 Billion |

| Market Size (2031) | USD 32.23 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

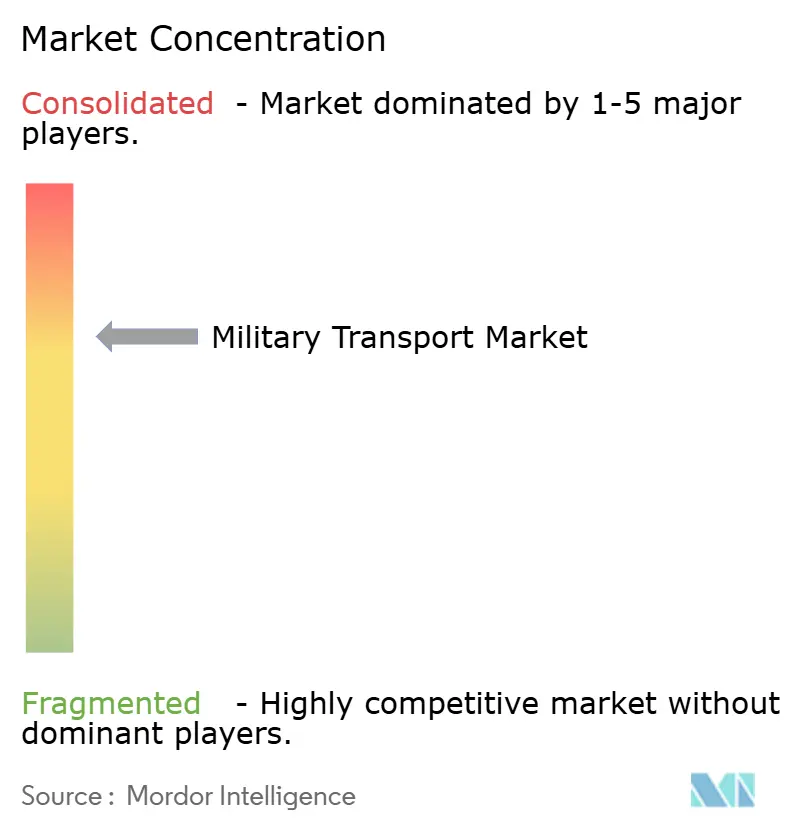

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Transport Market Analysis by Mordor Intelligence

The military transport market size in 2026 is estimated at USD 24.14 billion, growing from 2025 value of USD 22.79 billion with 2031 projections showing USD 32.23 billion, growing at 5.92% CAGR over 2026-2031. Fleet recapitalization, hybrid-electric propulsion adoption, and AI-enabled maintenance software accelerate the pace of military upgrades to logistics platforms. Programs such as the US Army’s USD 214.8 million FMTV A2 procurement and Germany’s USD 165 million A400M upgrade reflect how governments are replacing aging vehicles and aircraft while embedding digital health-monitoring systems to cut downtime. The military transport market benefits from expanding humanitarian operations—exemplified by 8.7 million kg of aid moved to Gaza via the US Joint Logistics Over-the-Shore pier—which showcases demand for flexible lift assets. Consolidation is reshaping supplier dynamics, with Leonardo’s EUR 1.7 billion (USD 1.96 billion) Iveco Defence takeover and Rheinmetall’s USD 950 million Loc Performance acquisition broadening European and US product portfolios.

Key Report Takeaways

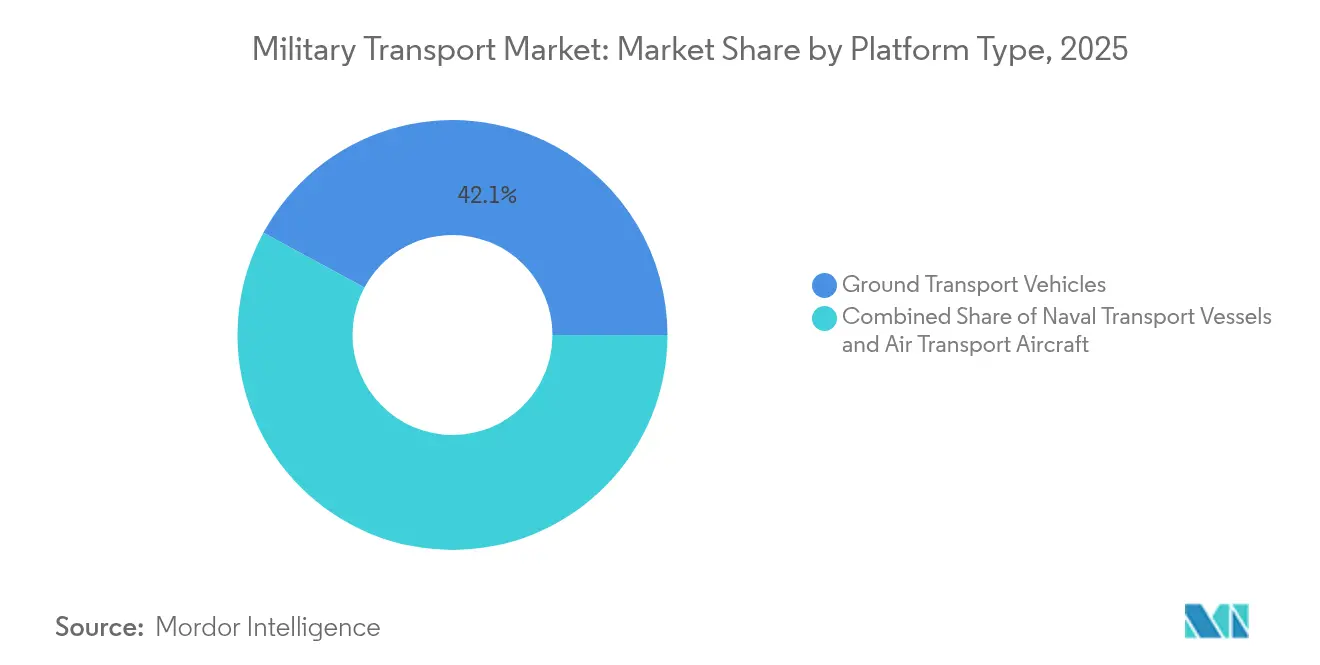

- By platform, ground transport vehicles held 42.12% of the military transport market share in 2025 and are forecast to register the highest segment CAGR at 9.52% through 2031.

- By application, cargo and equipment transport commanded a 45.73% revenue share in 2025; humanitarian and disaster relief represents the highest-growth application, with a 7.06% CAGR to 2031.

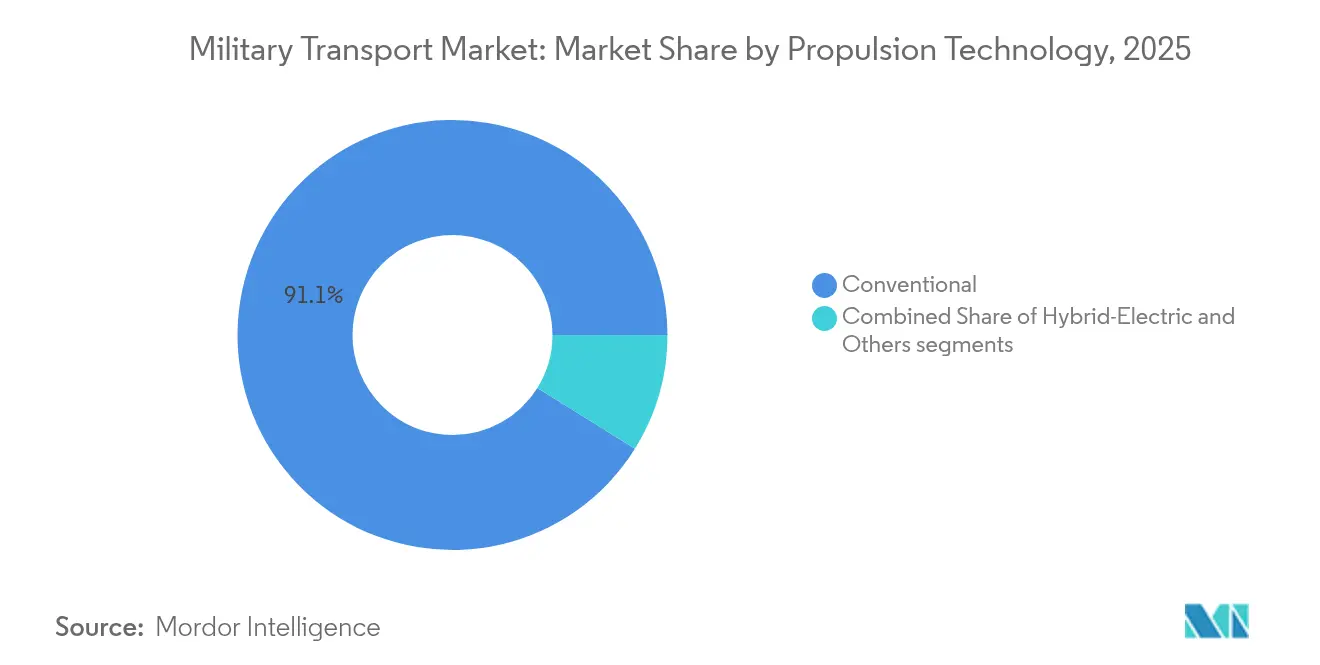

- By propulsion technology, hybrid-electric propulsion is the single fastest-growing propulsion category, expanding at a 10.63% CAGR through 2031 while conventional systems keep the largest 91.12% share of the military transport market size in 2025.

- By end user, the army end-user segment accounted for 48.23% of the military transport market size in 2025, whereas the air force segment records the highest service-level CAGR at 6.95% to 2031.

- By geography, North America remained the largest market with a 32.12% share in 2025, while Asia-Pacific posts the highest regional CAGR at 7.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Military Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global demand for strategic and tactical airlift capabilities | +1.8% | Asia-Pacific and Europe | Medium term (2-4 years) |

| Operational shift toward rapid deployment in decentralized warfare environments | +1.2% | Indo-Pacific and Eastern Europe | Short term (≤ 2 years) |

| Modernization and recapitalization of aging military transport fleets | +0.9% | North America and Europe | Long term (≥ 4 years |

| Rising frequency of global humanitarian and disaster relief missions | +0.7% | Conflict-prone regions worldwide | Medium term (2-4 years) |

| Increased adoption of dual-use transport platforms with civil certification pathways | +0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Integration of AI-driven predictive maintenance to optimize life-cycle costs | +0.5% | Technology-intensive militaries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Global Demand for Strategic and Tactical Airlift Capabilities

Japan’s decision to add 13 KC-46A tankers and 17 CH-47 Block II Chinooks underscores rising lift requirements for Indo-Pacific missions.[1]Australian Defence Magazine, “Japan Ups Its Emphasis on Aerial Refuelling with KC-46A Procurements,” australiandefence.com.au China promotes its Y-20B airlifter to states like Nigeria, expanding competition beyond traditional suppliers. A decade of A400M Atlas service with the RAF validates the platform’s 37-ton payload and 8,900 km unrefuelled range for combat and humanitarian tasks. Demand is reinforced by multinational exercises that move heavy equipment across long distances, compelling air forces to enlarge their fleets. These procurements steadily widen the addressable base for maintenance, training, and ground-support contracts within the military transport market.

Operational Shift Toward Rapid Deployment in Decentralized Warfare Environments

Doctrine now centers on agile units able to disperse and re-aggregate quickly across multiple domains. The US Army’s Next Generation Tactical Vehicle-Hybrid offers Silent Drive and Watch modes, permitting covert convoy movement and on-board power generation. Australia’s Talisman Sabre exercise, involving 35,000 personnel from 19 countries, highlighted how US watercraft supported littoral logistics quickly. China integrates high-speed rail into mobilization plans, reducing transit times for brigades traversing vast distances.[2]IDST, “High-Speed Rail in Military Logistics,” idstch.com Such concepts push demand for versatile platforms that load and unload quickly, reinforcing procurement pipelines for tactical trucks, tilt-rotors, and mobile port equipment within the military transport market.

Modernization and Recapitalization of Aging Military Transport Fleets

The US Marine Corps is spending USD 360 million to extend 360 MV-22B Ospreys to the 2050s through the ReVAMP program, a blueprint other services emulate for legacy aircraft. Poland’s C-295M upgrade contract enhances NATO interoperability with new avionics and SATCOM links. The US Air Force is pivoting to cargo-aircraft recapitalization now that tanker modernization has entered maturity. Such long-cycle investments create sustained replacement demand and spur contiguous orders for simulators, spares, and digital twins across the military transport market.

Rising Frequency of Global Humanitarian and Disaster-Relief Missions

Military lift assets now deploy as first responders to conflict and climate emergencies. India executed multiple evacuations—Operation Ajay, Kaveri, and Ganga—between 2024 and 2025, demonstrating how air and sea transport underpin national crisis diplomacy. Despite rough seas, the US Gaza pier delivered 8.7 million kg of aid within 20 days, proving afloat offload concepts for contested littorals. New Zealand’s USD 1 billion enhanced sealift vessel will incorporate a well dock to speed aid delivery across the Pacific. Humanitarian operations enlarge the mission set for cargo aircraft, landing platform docks, and tactical trucks, strengthening revenue visibility in the military transport market.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain vulnerabilities affecting aerospace-grade material availability | −0.8% | Western manufacturers | Short term (≤ 2 years) |

| Budgetary shifts toward unmanned systems amid rising defense inflation | −0.6% | North America and Europe | Medium term (2-4 years) |

| Limited global shipyard capacity for large roll-on/roll-off vessel construction | −0.4% | Global | Long term (≥ 4 years) |

| Stricter emission regulations delaying upgrades of legacy propulsion systems | −0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerabilities Affecting Aerospace-Grade Material Availability

Material shortages undermine production schedules for aircraft, trucks, and naval hulls that demand aerospace-grade aluminum, titanium, and rare-earth alloys. The Pentagon has listed 280 critical material dependencies, many tied to Chinese supply chains, exposing programs that rely on specialty metals and electronic components. European manufacturers are adopting dual-sourcing and accepting longer lead times, with Airbus revising A400M delivery calendars while Rheinmetall buys US suppliers to secure titanium feedstock and machining capability. Semiconductor scarcity exacerbates the problem; lead times for military-grade chips have stretched from 12 weeks to more than 52 weeks, forcing avionics engineers to redesign boards around whatever parts can be sourced. Mitigation measures such as the US CHIPS Act and the European Critical Raw Materials Act promise fresh capacity. Yet, new foundries and processing plants will not reach volume for at least three years, keeping near-term production risk elevated. These constraints delay the fielding of new lift assets and reduce the annual delivery profile that underpins the military transport market.

Budgetary Shifts Toward Unmanned Systems Amid Rising Defense Inflation

Defense ministries are channeling a larger share of procurement toward autonomous platforms, crowding out funding for traditional transport assets. The US Department of Defense raised unmanned-systems allocations from USD 7.5 billion in FY2021 to USD 10.1 billion in FY2025, a 34.7% jump that outstrips growth in manned programs. Initiatives such as the Army’s Autonomous Ground Resupply trucks and the Navy’s Large Unmanned Surface Vessel directly compete with future tactical truck and sealift vessel buys. Inflation amplifies the squeeze; specialized metals, skilled labor, and certification costs push military transport prices up 8-12% yearly, forcing managers to cut quantities or slip schedules. European trends mirror this pivot, with Germany’s EUR 100 billion (USD 115.57 billion) Sondervermögen and France’s naval budgets steering new money toward unmanned and cyber capabilities rather than conventional amphibious hulls. Successful battlefield performance of drones in Ukraine strengthens political momentum for autonomous logistics, intensifying the budgetary headwinds faced by legacy military transport fleets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Ground Vehicles Lead Hybrid-Electric Revolution

Ground vehicles captured 42.12% of the military transport market share in 2025 while registering the fastest 9.52% CAGR projection to 2031. Programs such as the USD 1.54 billion FHTV V contract and continued FMTV A2 orders are refreshing heavy and medium truck fleets with enhanced payload protection and digital diagnostics. The military transport market size for heavy tactical trucks is primed to rise as armies adopt modular architectures that integrate power distribution units for directed-energy or command-and-control payloads. Hybrid-electric conversions are cascading across light and medium platforms. GM Defense’s Next Generation Tactical Vehicle-Hybrid delivers silent-watch functionality and exportable 120 kW power, supporting sensors and unmanned systems in austere sites. Armored logistics carriers such as Rheinmetall’s TGS-Mil Protected unite NATO Level 3 protection with 4×4 drivetrains optimized for expeditionary ops.

Naval transport vessels continue to evolve through roll-on/roll-off hull forms and enhanced beaching capabilities. India’s 200 m Landing Platform Dock program integrates electric propulsion and 60-day endurance, offering humanitarian assistance scalability for Indo-Pacific settings. Concurrently, airlift platforms such as the A400M Atlas mark milestones that validate multi-domain integration, with Airbus now showcasing a variant able to network swarming drones. These advances widen capability gaps that drive procurement of blended fleets across the military transport market.

By Application: Humanitarian Missions Drive Fastest Growth

Cargo and equipment transport preserved a 45.73% revenue lead in 2025, underpinning the routine movement of ammunition, bridging systems, and armored vehicles worldwide. Within this segment, the C-17 Globemaster and A400M Atlas remain indispensable for outsize loads and austere-strip operations, maintaining robust utilization rates during exercises such as Australia’s Pitch Black and multinational relief sorties.

Humanitarian and disaster-relief missions are expected to grow faster than any other application, recording a 7.06% CAGR to 2031. The Gaza pier operation validated Joint Logistics Over-the-Shore constructs, spurring fresh interest in modular causeways and sealift connectors. India’s evolution from regional responder to global evacuator underscores political value in fast, credible lift. Autonomous casualty evacuation robots, like the Expeditionary Modular Autonomous Vehicle, showcase how unmanned ground systems can shorten the critical care timeline, raising tactical and strategic stakes within the military transport market size for humanitarian tasks. Personnel transport continues to absorb investment, particularly for rotary-wing fleets that hoist troops into dispersed landing zones. Medevac and emergency rescue variants leverage augmented-reality medical displays and secure telemetry links that improve in-flight triage. These upgrade cycles ensure the broader military transport industry addresses complex scenarios ranging from urban search-and-rescue to expeditionary peacekeeping.

By Propulsion Technology: Hybrid-Electric Surge Challenges Conventional Dominance

Conventional propulsion retained 91.12% of the military transport market in 2025, due to mature supply chains and worldwide diesel distribution networks. Diesel engines and gas turbines remain embedded in doctrine and logistics manuals, emphasizing reliability during high-tempo operations.

Hybrid-electric technology, however, is advancing at a 10.63% CAGR through 2031, injecting stealth and fuel-burn savings into operational concepts. The forthcoming M1E3 Abrams will become the US Army’s first series-production hybrid-electric tank, integrating batteries that support silent surveillance while trimming logistic convoys. GE Aerospace’s megawatt-class demonstrator connects a CT7 turboshaft to an electric motor, illustrating how rotary-wing platforms can gain 20% fuel efficiency without sacrificing hot-and-high performance. The push toward battery-dominant designs is furthered by the service goal of fielding an all-electric non-tactical vehicle fleet before 2035, an initiative that seeds supplier ecosystems across the military transport market.

By End User: Air Force Growth Outpaces Traditional Army Dominance

Armies controlled 48.23% of spending in 2025, reflecting extensive requirements for line-haul trucks, fuel bowsers, and engineering equipment. Recent orders for 240 additional FMTV tactical trucks amplify capacity for both active and National Guard units.

Air forces are forecasted to grow faster, posting a 6.95% CAGR during the period. Japan’s USD 882 million CH-47 purchase and 13 KC-46A acquisition illustrate renewed emphasis on aerial refueling and airlift self-sufficiency. The US Air Force’s planned cargo-aircraft recapitalization will shape future contests between the C-130J, C-390, and potential clean-sheet entrants, enlarging the military transport market size dedicated to fixed-wing fleets. Navies and marines invest in landing platform docks, expeditionary transfer docks, and connector craft to support littoral campaigns. Seabasing strategies rely on large-volume sealift to shuttle munitions, fuel, and disaster-relief stores across archipelagos, pushing demand for afloat medical facilities and roll-on/roll-off ramps. This distribution helps balance service-level spending patterns across the military transport market.

Geography Analysis

North America held 32.12% of the military transport market in 2025, powered by the United States' USD 214.8 million FMTV A2 truck buy, USD 360 million MV-22B modernization, and multiple aerial refueler programs. Canada is fielding Arctic patrol ships and joint support vessels that strengthen NATO's resilience in the High North. The region's leadership in AI diagnostics and hybrid-electric propulsion positions domestic suppliers to capture export orders, further enlarging the military transport market.

Asia-Pacific is projected to be the fastest-growing region at 7.18% CAGR. China inducts next-generation heavy trucks, advances Y-20B airlifter production, and integrates high-speed rail into mobilization doctrine. Japan's multibillion-dollar airlift and helicopter purchases and South Korea's USD 8.8 billion procurement approvals signal a broad commitment to logistics modernization. Historical investment since 2019 shows a steady shift from platform quantity to capability depth, reinforcing growth prospects for the military transport market in the region.

Europe maintains robust demand via multinational frameworks and national programs. Germany's EUR 3.5 billion (USD 4.05 billion) vehicle agreement underpins continental logistics readiness. The trilateral Future Mid-Size Tactical Cargo initiative allocates EUR 30 million (USD 34.71 million) to design a C-130 replacement by 2040, demonstrating collaborative innovation. Consolidation moves such as Leonardo's Iveco Defence purchase concentrate expertise and align supply chains, keeping Europe a pivotal contributor to the military transport market.

Competitive Landscape

The military transport market is moderately concentrated, fortifying leading primes by government ties and multidecade production runs. Partnerships accelerate technology diffusion. Lockheed Martin Corporation and General Dynamics Corporation have pooled solid-rocket motor know-how to buttress the US munitions base. At the same time, Lockheed and Rheinmetall will produce missiles in Europe, ensuring supply autonomy. Joby Aviation’s tie-up with L3Harris on hybrid VTOL aircraft offers an alternate path for vertical lift, challenging legacy helicopter OEMs.

Leonardo’s acquisition of Iveco Defence creates a land-systems powerhouse that rivals US and German incumbents, expanding product breadth from multirole trucks to 8×8 armored carriers. Rheinmetall’s purchase of Loc Performance positions the firm to bid aggressively on the XM30 infantry vehicle and Common Tactical Truck, programs valued at over USD 60 billion.

Military Transport Industry Leaders

Lockheed Martin Corporation

The Boeing Company

BAE Systems plc

Airbus SE

Oshkosh Defense, LLC (Oshkosh Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Oshkosh Defense, LLC, a subsidiary of Oshkosh Corporation, received orders from the US Army Contracting Command – Detroit Arsenal (ACC-DTA) for additional Family of Medium Tactical Vehicle A2 (FMTV A2) trucks and trailers. The orders, valued at USD 214.8 million, support the US Army's modernization initiatives.

- July 2024: The German military awarded Rheinmetall a seven-year framework contract worth USD 3.77 billion for delivering up to 6,500 military trucks. The agreement enables flexible procurement of military logistics vehicles, including the UTF 5t and UTF 15t all-terrain trucks.

Global Military Transport Market Report Scope

Military transport vehicles are crucial for maintaining supply lines to forward bases that are difficult to reach otherwise. These vehicles are specifically designed to military standards and are rugged versions of their commercial counterparts. Military transport vehicles are generally used to carry troops, staff, (mounted) weapons, supplies, evacuate wounded soldiers, and many other diverse roles. Heavily specialized variants of such vehicles and aircraft can also be used for carrying out strategic and tactical missions.

The military transport market is segmented by type, application, and geography. By type, the market is segmented into ground transport vehicles, naval transport vessels, and air transport aircraft. By application, the market is segmented into personnel transport, cargo transport, and emergency rescue. By geography, the market covers the developments in North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. The report offers market size and forecast in terms of value (USD Billion) for all the above segments.

| Ground Transport Vehicles | Heavy Tactical Trucks |

| Light Utility Vehicles | |

| Armored Logistics and MRAPs | |

| Naval Transport Vessels | Roll-on/Roll-off (Ro-Ro) and Sealift Ships |

| Landing Platform Docks (LPD/LHD) | |

| Auxiliary Cargo and Replenishment Ships | |

| Air Transport Aircraft | Fixed-Wing |

| Rotary and Tilt-Rotor |

| Personnel Transport |

| Cargo/Equipment Transport |

| Emergency Rescue and Medevac |

| Humanitarian and Disaster-relief |

| Conventional |

| Hybrid-Electric |

| Others |

| Army |

| Navy |

| Air Force |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform Type | Ground Transport Vehicles | Heavy Tactical Trucks | |

| Light Utility Vehicles | |||

| Armored Logistics and MRAPs | |||

| Naval Transport Vessels | Roll-on/Roll-off (Ro-Ro) and Sealift Ships | ||

| Landing Platform Docks (LPD/LHD) | |||

| Auxiliary Cargo and Replenishment Ships | |||

| Air Transport Aircraft | Fixed-Wing | ||

| Rotary and Tilt-Rotor | |||

| By Application | Personnel Transport | ||

| Cargo/Equipment Transport | |||

| Emergency Rescue and Medevac | |||

| Humanitarian and Disaster-relief | |||

| By Propulsion Technology | Conventional | ||

| Hybrid-Electric | |||

| Others | |||

| By End User | Army | ||

| Navy | |||

| Air Force | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and 2031 forecast for the military transport market?

The military transport market size is USD 24.14 billion in 2026 and is projected to reach USD 32.23 billion by 2031, reflecting a 5.92% CAGR.

Which platform category will grow fastest to 2031?

Ground vehicles are forecasted to expand at a 9.52% CAGR as hybrid-electric drivetrains and AI diagnostics enter tactical trucks.

Why is humanitarian transport demand rising?

Increased natural disasters and conflict zones require rapid aid delivery; recent Gaza pier and Indian evacuation missions highlight this trend.

Which region offers the highest growth opportunity through 2031?

Asia-Pacific leads with a 7.18% CAGR, driven by Chinese, Japanese and South Korean modernization programs.

What propulsion technology is attracting the most investment?

Hybrid-electric systems are advancing at a 10.63% CAGR as they improve stealth and fuel efficiency across land, air and sea platforms.

Page last updated on: