Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.39 Billion |

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 4.38 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

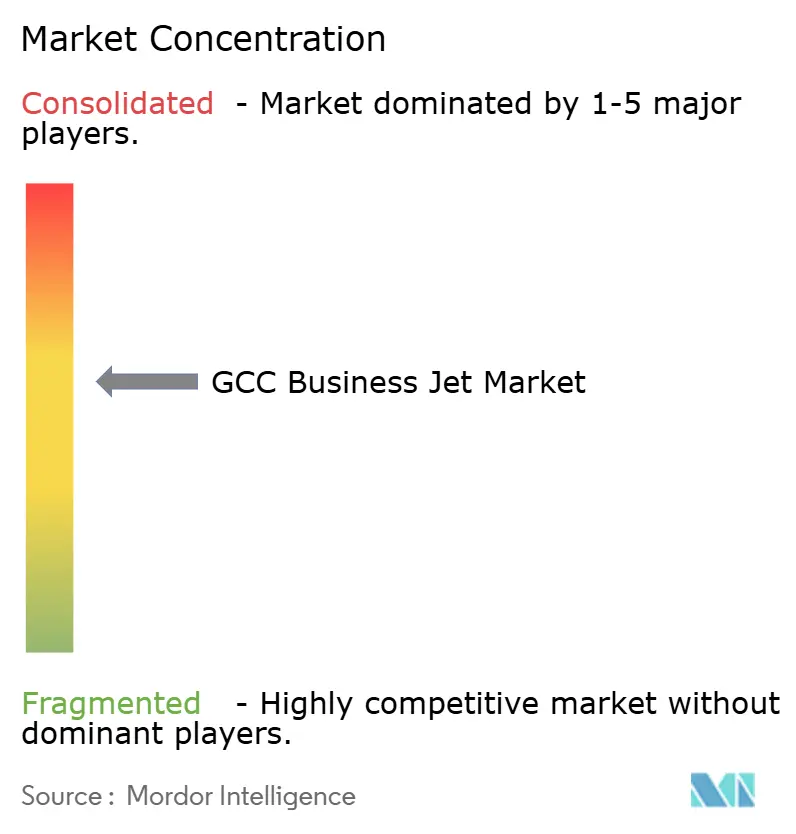

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Business Jet Market Analysis by Mordor Intelligence

The GCC business jet market size is expected to grow from USD 3.39 billion in 2025 to USD 3.47 billion in 2026 and is forecasted to reach USD 4.38 billion by 2031 at a 4.79% CAGR over 2026-2031. This growth is driven by a shift from discretionary luxury to essential infrastructure, as ultra-high-net-worth individuals (UHNWIs) and family offices prioritize time-sensitive mobility as a strategic advantage. The addition of 9,800 high-net-worth (HNW) residents to the UAE by 2025, along with sovereign diversification initiatives under Saudi Vision 2030, supports a steady demand pipeline for buyers and charter users, even during global economic slowdowns. Increased investments in maintenance, repair, and overhaul (MRO) facilities across Dubai World Central, Sharjah, Muscat, and AlUla are expanding service capacity and boosting aftermarket revenues. Additionally, supply chain disruptions at OEMs have extended lead times, driving up pre-owned aircraft values and encouraging more users to adopt jet-card and fractional ownership programs.

Key Report Takeaways

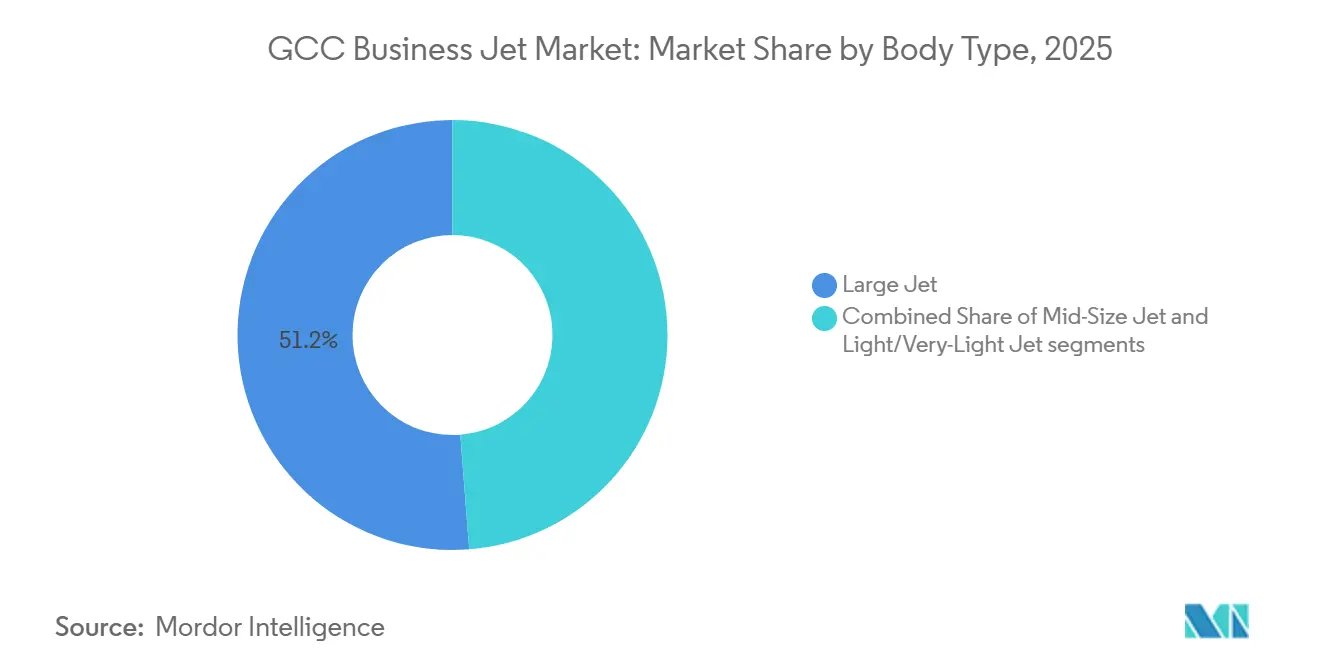

- By body type, large-cabin platforms accounted for 51.24% of the GCC business jet market share in 2025, while light and very-light jets are expected to grow at the fastest CAGR of 5.34% through 2031.

- By end user, businesses and corporate fleets accounted for 39.59% of the GCC business jet market in 2025, with charter and air-taxi operators projected to grow at a CAGR of 5.94% by 2031.

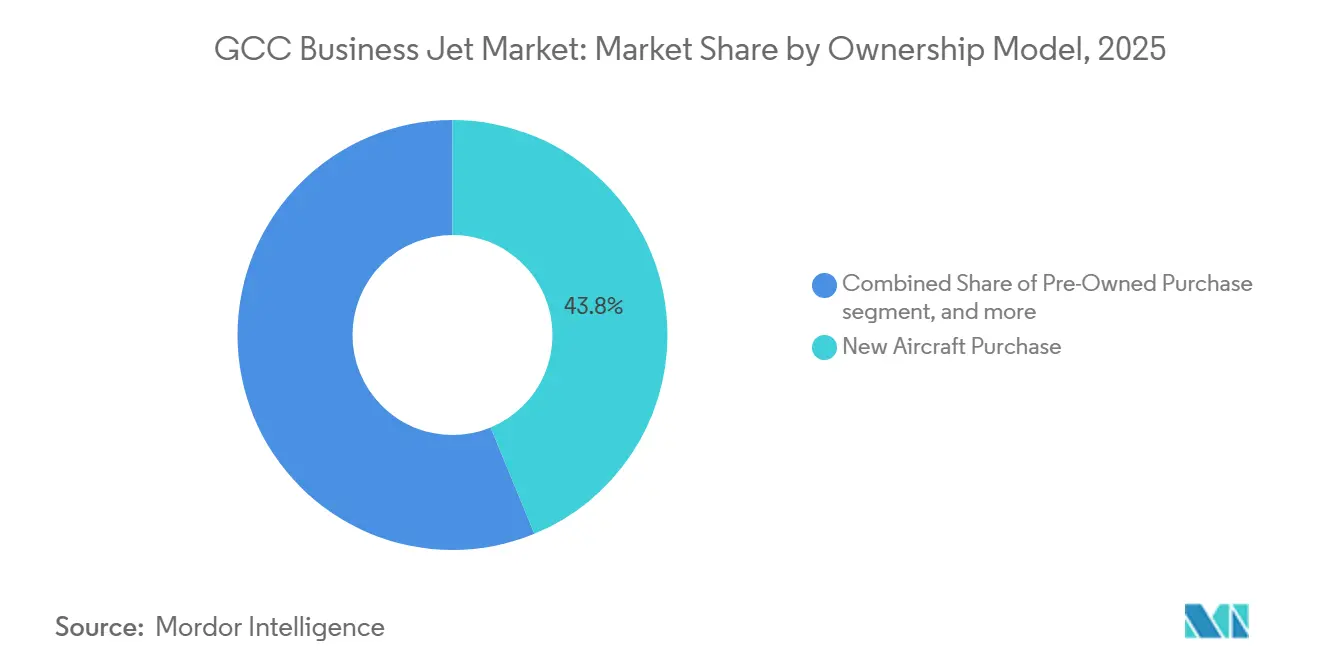

- By ownership model, new-aircraft acquisitions accounted for 43.78% of the GCC business jet market size in 2025, while jet cards and membership plans are expected to increase at a CAGR of 7.01% through 2031.

- By geography, the United Arab Emirates accounted for 36.59% of the revenue in 2025, whereas Oman is projected to achieve the highest CAGR of 5.81% by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Business Jet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising UHNW and family-office wealth concentration | +1.20% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Vision-2030 linked corporate mobility programs | +0.90% | Saudi Arabia | Medium term (2-4 years) |

| Expansion of dedicated FBO and MRO infrastructure | +0.70% | UAE, Saudi Arabia, Oman | Medium term (2-4 years) |

| OEM supply-chain bottlenecks pushing pre-owned uptake | +0.60% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| SAF-ready long-range jets favored by ESG-conscious firms | +0.40% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Islamic finance-backed operating lease structures | +0.50% | Saudi Arabia, UAE, Qatar, Bahrain, Kuwait | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising UHNW and Family-Office Wealth Concentration

In 2025, UAE billionaires controlled USD 169 billion, while their Saudi counterparts managed USD 81 billion. Additionally, heirs are expected to inherit an additional USD 153 billion within the next 15 years, ensuring steady demand for private aviation.[1]UBS, “Billionaire Report 2025,” ubs.com Dubai is home to 120 family offices overseeing approximately USD 1.2 trillion in assets, with these entities perceiving aircraft as tools for deal execution rather than luxury items. According to Knight Frank, the UAE experienced an inflow of 7,200 millionaires in 2024, driving sustained demand for seat hours and indicating that the GCC business jet market remains resilient to short-term macroeconomic fluctuations. The need for mobility is further emphasized by the fact that 36% of regional billionaires have relocated at least once, making private jets a practical safeguard against geopolitical uncertainties. Cross-border investment roadshows also contribute to increased flight activity, particularly on routes connecting Dubai, Riyadh, London, and Singapore.

Vision-2030-Linked Corporate Mobility Programs

Saudi Arabia recorded 23,612 business-jet movements in 2024, representing a 24% year-over-year increase, driven by the headquarters rule requiring multinationals to establish senior teams in Riyadh.[2]GACA, “General Aviation Roadmap,” gaca.gov.sa The regulatory roadmap aims to develop a USD 2 billion general aviation economy and create 35,000 jobs by 2030, including the establishment of six dedicated business-aviation airports and nine terminals. The liberalization of cabotage in May 2025 allowed foreign carriers to operate domestic city pairs, with VistaJet being the first to capitalize on this opportunity, achieving a 32% increase in Saudi Program Members during the first half of 2025. Riyadh now accounts for approximately two-thirds of private-jet traffic, strengthening hub-and-spoke patterns that boost charter hours and MRO activities. King Salman International Airport, projected to handle 120 million passengers by 2030, includes a private-aviation apron, underscoring the government's view of the sector as essential infrastructure rather than a niche luxury.

Expansion of Dedicated FBO and MRO Infrastructure

Sharjah's new Gama Aviation FBO and MRO complex became operational in mid-2025, addressing overflow from the slot-constrained Dubai International Airport.[3]Gama Aviation, “Sharjah FBO Launch,” gamaaviation.com Falcon Aviation allocated USD 100 million for an MRO facility at Al Maktoum International. At the same time, Jetex inaugurated Saudi Arabia's first FBO at Red Sea International Airport, reflecting a growing trend toward multi-hub redundancy. The Public Investment Fund supported Saudia Technic's 1 million square meter MRO village in Jeddah, which is expected to generate USD 2.7 billion over the next 10 years. In December 2024, Comlux opened a 20,000-square-meter service center at Dubai South, and Alliance Aviation launched an FBO in AlUla in October 2025, expanding its geographic coverage for inbound tourism. These developments collectively enhance hangar capacity, reduce maintenance ferry times, and improve overall fleet dispatch reliability in the GCC business jet market.

OEM Supply-Chain Bottlenecks Pushing Pre-Owned Uptake

Gulfstream delivered 113 aircraft during the first nine months of 2025 but fell short of its 2024 target due to delays in Rolls-Royce Pearl 700 engines, resulting in multi-quarter backlogs. Jetcraft projects 11,202 pre-owned transactions valued at USD 73.9 billion between 2025 and 2029, with large-cabin units accounting for 20% of the market as buyers seek immediate availability. Extended lead times have prompted corporations to adopt jet-card programs as temporary solutions until factory production slots become available. Embraer retained its leadership in the Phenom 300 family, delivering 65 units in 2024; however, even this high production line cannot fully meet latent demand, creating a seller’s market for younger airframes, particularly models such as the G650ER, Global 7500, and Falcon 7X, driving up residual values across the GCC business jet market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slot and airspace congestion at key GCC hubs | -0.80% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| High import tariffs/VAT on pre-owned imports | -0.50% | UAE, Saudi Arabia, spillover to Qatar, Bahrain, Kuwait | Medium term (2-4 years) |

| Emerging carbon-accounting mandates on corporate travel | -0.30% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Qualified pilot shortage in Arabic-language ATP pool | -0.40% | Saudi Arabia, UAE, Oman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slot and Airspace Congestion at Key GCC Hubs

Dubai International imposes restrictions on general aviation movements during peak periods. It applies a 50% surcharge on landing fees, encouraging operators to use Dubai World Central, where five FBOs compete for available slots. Airport Coordination Limited classifies Dubai, Abu Dhabi, and 26 Saudi airports as Level 3, indicating significant capacity constraints. The planned transition of commercial flights to Dubai World Central by 2030 is expected to further limit slot availability in the interim, while King Salman International Airport in Riyadh is not anticipated to be fully operational until later in the decade. Secondary hubs such as Sharjah, AlUla, and Muscat are already handling overflow traffic; however, repositioning flights to these locations increases crew and fuel costs. In the short term, congestion remains the primary operational challenge for the GCC business jet market.

High Import Tariffs/VAT on Pre-Owned Imports

The UAE imposes a 5% VAT on aircraft transferred from free zones to the mainland. Additionally, assets valued at over AED 5 million (approximately USD 1.36 million) are subject to the Capital Asset Scheme, which requires multi-year adjustments, thereby discouraging private buyers. While zero-rating applies to commercial transport, it does not extend to pre-owned jets used for personal purposes, thereby limiting the pool of potential individual owners. In Saudi Arabia, the absence of a harmonized duty schedule persists; however, alignment with the GACA roadmap is anticipated once dedicated business aviation airports become operational, which could lead to increased costs. The complexity of compliance drives buyers to register aircraft in jurisdictions like the Isle of Man or San Marino, resulting in longer ferry sectors for maintenance. These fiscal policies collectively reduce the forecasted CAGR of the GCC business jet market by an estimated 0.5%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Body Type: Large Cabin Dominance Meets Light-Jet Efficiency

Large-cabin airframes accounted for 51.24% of the GCC business jet market share in 2025, driven by their ability to connect GCC capitals with destinations like London, New York, and Singapore in a single flight. This segment represents the upper tier of the GCC business jet market, with fleets such as Qatar Executive’s six G700s and 15 G650ERs contributing to a 26% revenue increase over the past 12 months. Demand remains strong due to the preference of sovereign entities, energy companies, and global banks for nonstop range and conference-style cabin configurations.

Light and very-light jets are expected to grow at a rate of 5.34% through 2031, benefiting from lower operating costs and faster turnaround times at congested airports. Embraer’s Phenom 300 maintained its position as the world’s best-selling light jet for the eleventh consecutive year, with regional buyers favoring it for owner-operated missions or short-haul charters.

Mid-size jets, such as Bombardier’s Challenger 604 and Dassault’s Falcon 2000 families, offer a balance between capacity and cost for intra-GCC routes. Additionally, Dassault’s upcoming Falcon 10X, with a 7,500 nm range and a 16.2-m cabin, is set to address ultra-long-haul routes upon its entry into service in 2027.

By End User: Corporate Fleets Yield to Charter Flexibility

Corporate entities held a 39.59% share of the GCC business jet market in 2025, supported by relocation mandates that required multinational companies to station senior executives in Riyadh and Dubai. However, this share is gradually declining as asset-light charter solutions gain popularity. Charter and air-taxi operators are projected to grow at a 5.94% CAGR, with Saudi cabotage reforms driving growth. For instance, VistaJet’s domestic Saudi operations reported a 32% year-on-year increase in memberships during the first half of 2025.

Individual ownership remains significant among UHNWIs, who view private aircraft as a safeguard against geopolitical uncertainties. While training institutions remain a niche segment, programs like those offered by Etihad and Qatar Airways are expanding talent pipelines.

Government and special-mission fleets, such as Royal Jet’s upcoming ACJ320neo deliveries, are selectively growing to accommodate high-profile events like COP28, which increase diplomatic travel demand.

By Ownership Model: Fractional and Membership Programs Gain Traction

New aircraft acquisitions accounted for 43.78% of 2025 revenue but face challenges due to extended OEM backlogs. Pre-owned aircraft trading is expected to remain robust, with 11,202 deals projected globally through 2029 as buyers prioritize immediate availability.

Membership plans are forecasted to grow by 7.01%, appealing to corporations exploring private aviation options before committing to full ownership. AviLease’s USD 2.5 billion Islamic-finance facility highlights the growing preference for operating leases, which reduce balance-sheet impact.

Managed-fleet operators, such as DC Aviation Al-Futtaim and Empire Aviation Group, are expanding inventory access without direct asset ownership, adding complexity to the traditional buy-versus-lease decision-making process.

Geography Analysis

The United Arab Emirates accounted for 36.59% of 2025 revenue, supported by Dubai’s network of 120 family offices managing USD 1.2 trillion in assets and the Emirates Group’s USD 34.8 billion turnover in FY 2024-25. Dubai World Central accommodates over 40 business jets, while new facilities like Comlux’s 20,000-square-meter service center and Gama Aviation’s Sharjah FBO help alleviate slot constraints.

Saudi Arabia recorded 23,612 business jet flights in 2024 and is advancing its aviation infrastructure with the development of King Salman International Airport, six dedicated business aviation airports, and nine terminals, all under a USD 2 billion plan. Jetex’s Red Sea FBO and Jubail’s new general aviation designation extend the country’s reach beyond Riyadh and Jeddah, solidifying its position as the second-largest market in the GCC.

Oman is projected to achieve the fastest growth, with a 5.81% CAGR through 2031, driven by Vision 2040 initiatives and the opening of a dedicated MRO facility in Muscat in mid-2025. Qatar, Bahrain, and Kuwait provide additional capacity, with Qatar Executive’s 24-aircraft fleet achieving a 26% revenue increase following the FIFA World Cup. Bahrain leverages free-zone incentives to attract MRO startups. These secondary markets collectively support the UAE and Saudi Arabia by offering additional capacity, enhancing the resilience of the GCC business jet network.

Competitive Landscape

The market concentration is moderate, with key original equipment manufacturers (OEMs) such as Gulfstream, Bombardier, Dassault, Embraer, and Textron dominating supply. Gulfstream's delivery of 113 aircraft within the first nine months of 2025 highlights strong demand, despite challenges such as engine bottlenecks. Early adoption strategies, exemplified by Qatar Executive's introduction of the G700 as the first operator globally, indicate that operators prioritize technological advancements alongside cabin volume.

Infrastructure development is a critical factor in competition among service providers. Falcon Luxe is allocating USD 100 million to establish an MRO facility at Dubai World Central and plans to expand its fleet by 40 aircraft by 2026. Meanwhile, Alliance Aviation and Jetex are focusing on capturing tourist traffic at emerging destinations, such as AlUla and the Red Sea developments. Additionally, Islamic-finance-backed lessors, such as AviLease, are diversifying their portfolios by shifting from commercial aviation to business jets, aiming to mitigate risk concentration.

Market disruptors are capitalizing on niche opportunities to establish a foothold in the market. For instance, DC Aviation Al-Futtaim has introduced a Global 7500, one of only two available for charter in the Middle East, and is scaling operations through managed aircraft to minimize asset exposure. Fixed-base operators (FBOs) are differentiating themselves by offering carbon-offset programs, driven by the UAE's Measurement, Reporting, and Verification (MRV) law, which is increasing demand for emissions accounting. Overall, the GCC business jet market reflects a balance between the oligopolistic supply from OEMs and a fragmented yet rapidly evolving service ecosystem.

GCC Business Jet Industry Leaders

Gulfstream Aerospace Corporation

Bombardier Inc.

Dassault Aviation SA

Textron Inc.

Embraer S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: The General Authority of Civil Aviation (GACA) of Saudi Arabia introduced a General Aviation roadmap at the 2024 Future Aviation Forum (FAF 2024). This initiative aims to increase the GDP contribution of the general aviation sector tenfold, reaching USD 2 billion by 2030. The roadmap encompasses the business jet segment, including charter, private, and corporate jets, and aligns with Saudi Arabia’s goal of becoming a prominent global business and tourist destination.

- April 2024: Jet Aviation obtained the General Authority of Civil Aviation (GACA) Part 125 Certificate in Saudi Arabia. This certification enables the company to operate commercial transport for private jets based in the Kingdom, in compliance with ICAO standards. It marks a significant step in expanding Jet Aviation's presence in the growing Saudi aviation market and aligns with Vision 2030 objectives to promote premium tourism and aviation. The Part 125 Operator's Certificate, now mandatory for all private aircraft operators in Saudi Arabia, ensures safe and compliant operations.

GCC Business Jet Market Report Scope

Business jets are fixed-wing aircraft designed to transport small groups of passengers on demand. These aircraft typically feature customized cabins and operate from dedicated or shared business aviation facilities across the Gulf Cooperation Council (GCC) region.

The GCC business jet market is segmented by body type, end-user, ownership model, and geography. By body type, the market is segmented into large jets, mid-size jets, and light/very-light jets, By end user, the market is segmented into individual owners, businesses and corporate entities, charter/air-taxi operators, training and academic institutions, and government and special mission operators By ownership model, the market is segmented into new aircraft purchase, pre-owned purchase, fractional ownership, and jet cards/membership programs. The report also offers market sizes and forecasts for six countries across the region. For each segment, the market sizes and forecasts have been done based on value (USD).

By Body Type

| Large Jet |

| Mid-Size Jet |

| Light/Very-Light Jet |

By End User

| Individual Owners |

| Businesses and Corporate Entities |

| Charter/Air-Taxi Operators |

| Training and Academic Institutions |

| Government and Special Mission Operators |

By Ownership Model

| New Aircraft Purchase |

| Pre-Owned Purchase |

| Fractional Ownership |

| Jet Cards/Membership |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Bahrain |

| Oman |

| Kuwait |

| By Body Type | Large Jet |

| Mid-Size Jet | |

| Light/Very-Light Jet | |

| By End User | Individual Owners |

| Businesses and Corporate Entities | |

| Charter/Air-Taxi Operators | |

| Training and Academic Institutions | |

| Government and Special Mission Operators | |

| By Ownership Model | New Aircraft Purchase |

| Pre-Owned Purchase | |

| Fractional Ownership | |

| Jet Cards/Membership | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Bahrain | |

| Oman | |

| Kuwait |

Key Questions Answered in the Report

How big is the GCC business jet market in 2026?

The GCC business jet market size reaches USD 3.47 billion in 2026 and is projected to grow to USD 4.38 billion by 2031.

What is the expected CAGR for GCC private aviation through 2031?

The market is forecasted to register a 4.79% CAGR during the 2026-2031 period.

Which body-type segment leads regional demand?

Large-cabin jets maintained 51.24% market share in 2025 thanks to nonstop GCC-to-Europe and GCC-to-North America missions.

Why are charter operators growing faster than corporate fleets?

Cabotage liberalization in Saudi Arabia and slot constraints in Dubai push businesses toward flexible, asset-light charter models that expand at a projected 5.94% CAGR.

Which GCC country provides the strongest growth runway?

Oman is forecasted to expand at 5.81% CAGR through 2031 as Vision 2040 infrastructure and a new Muscat MRO facility unlock capacity.

How are sustainability rules affecting fleet choices?

ReFuelEU and UAE emissions laws accelerate orders for SAF-ready long-range jets such as Gulfstream’s G700 and G800, encouraging operators to modernize fleets sooner.

Page last updated on: