UK Military Aviation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

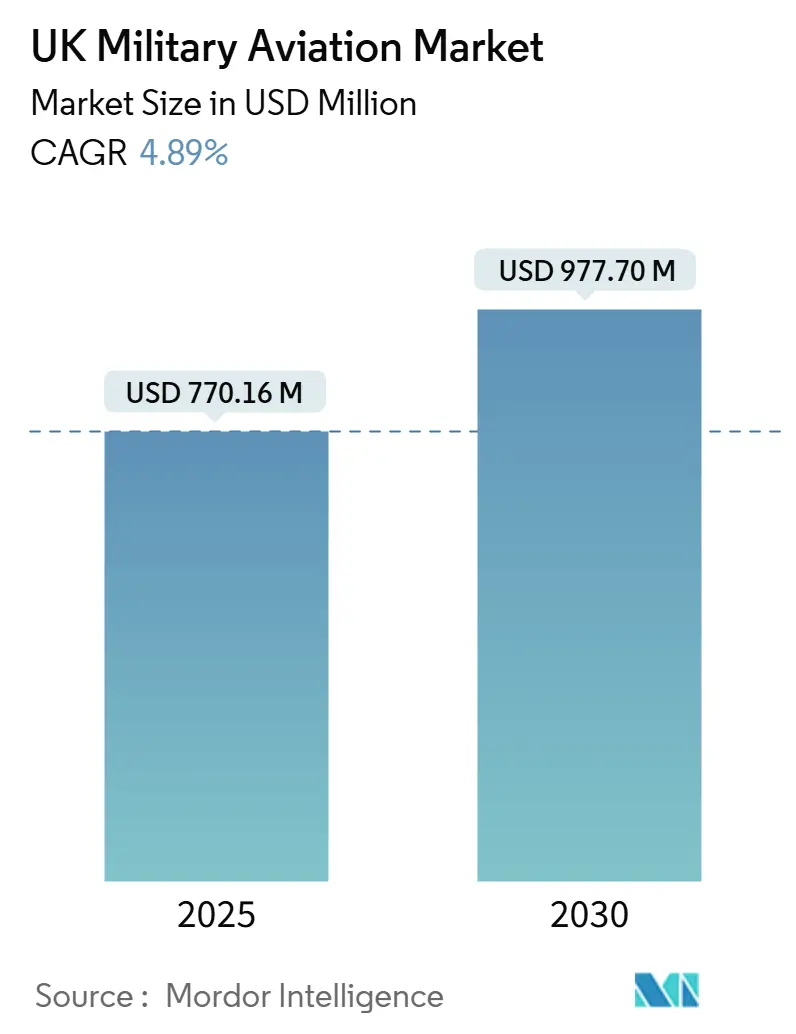

| Market Size (2025) | USD 770.16 Million |

| Market Size (2030) | USD 977.70 Million |

| Growth Rate (2025 - 2030) | 4.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Military Aviation Market Analysis by Mordor Intelligence

The UK military aviation market size stands at USD 770.16 million in 2025 and is forecasted to reach USD 977.70 million by 2030, reflecting a 4.89% CAGR. Robust outlays tied to the government’s pledge to lift defense spending to 2.5% of GDP, the GBP 2.35 billion (USD 2.87 billion) Typhoon ECRS Mk2 radar upgrade, and the GBP 1 billion (USD 1.22 billion) New Medium Helicopter (NMH) procurement sustain forward demand for platform renewal, capability enhancement, and resilient supply chains. Fixed-wing aircraft retain the largest installed base, but helicopter programs and related turboshaft propulsion upgrades now provide the steepest growth curve. Spending on synthetic training, sustainable aviation fuel (SAF), and digital maintenance unlocks new aftermarket revenue pools, while the post-Brexit regulatory regime and a widening STEM skills gap temper near-term expansion. Competitive intensity remains moderate, with BAE Systems, Leonardo, Airbus, Lockheed Martin, and Boeing leveraging long-term service contracts, local industrial footprints, and sovereign capability mandates to defend share.

Key Report Takeaways

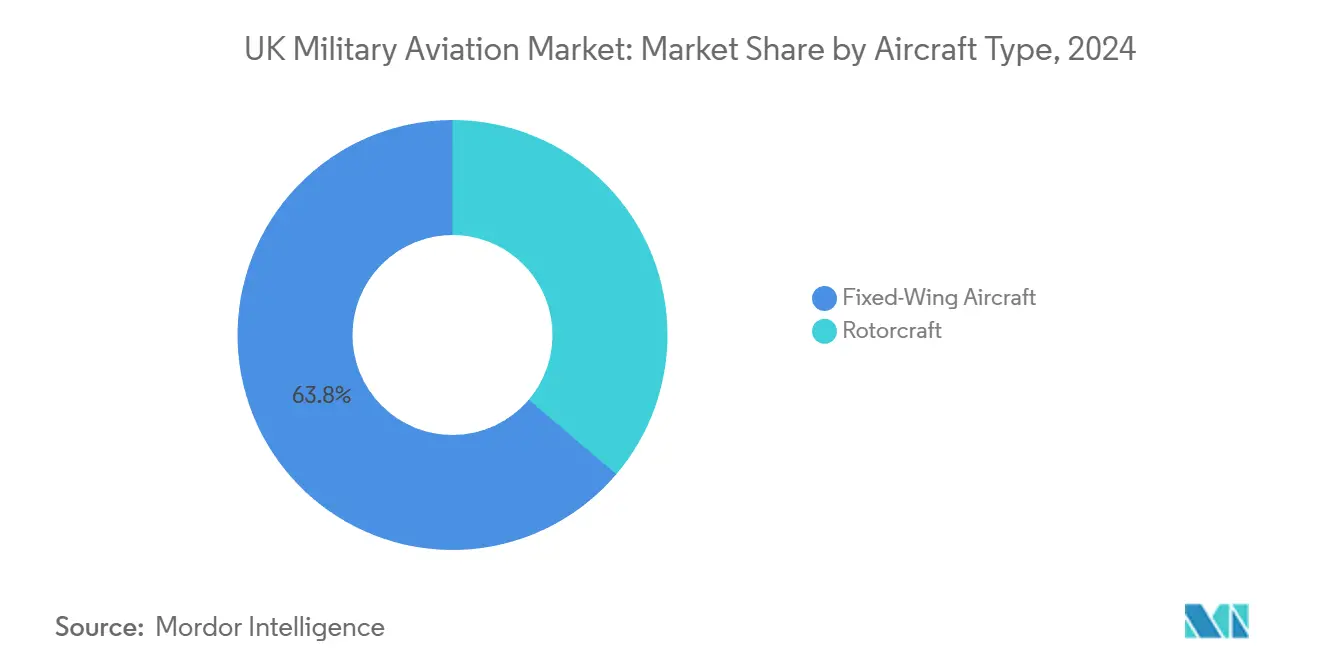

- By aircraft type, fixed-wing platforms commanded 63.79% of the UK military aviation market share in 2024, whereas rotorcraft are projected to expand at a 6.74% CAGR through 2030.

- By end-user service, the Air Force led 81.36% of the UK military aviation market share in 2024, while joint/special operations showed the fastest growth at a 5.86% CAGR to 2030.

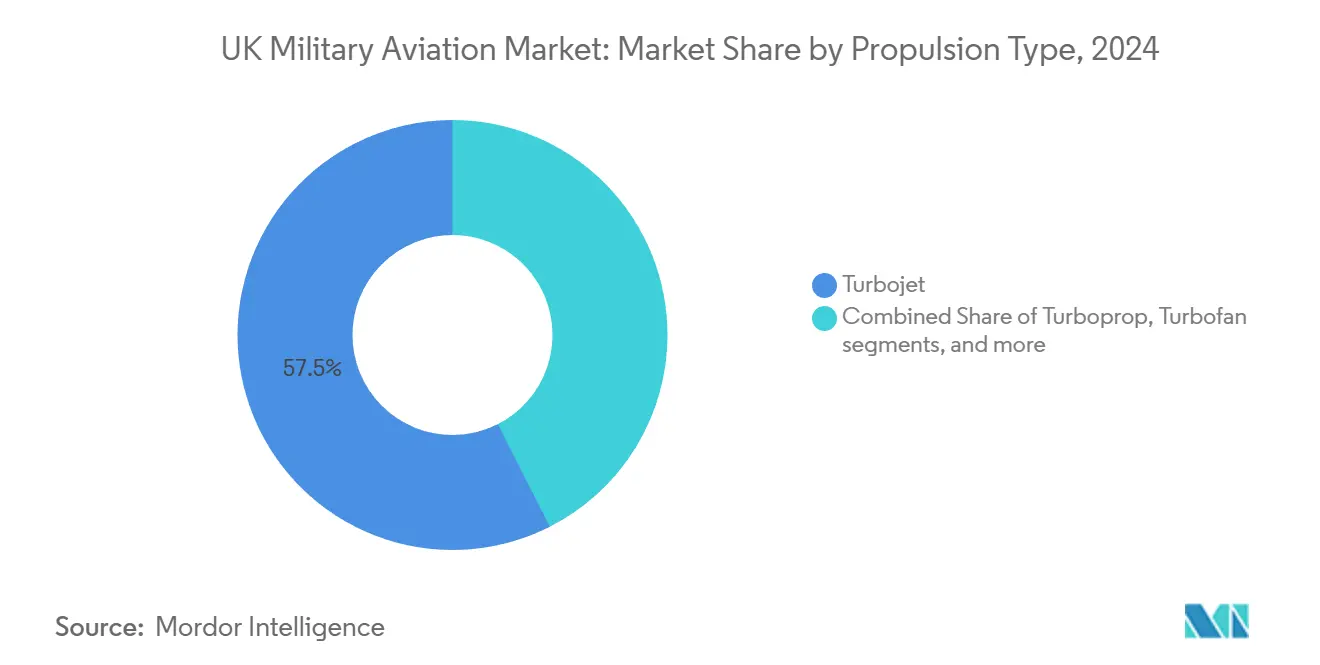

- By propulsion, turbojet engines accounted for 57.48% of the UK military aviation market size in 2024, and turboshaft units are forecasted to post a 7.43% CAGR through 2030.

UK Military Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased defense-spending roadmap | +1.2% | National, concentrated in England and Scotland defense clusters | Medium term (2-4 years) |

| Platform recapitalization | +0.9% | National, with primary impact on RAF bases and naval facilities | Long term (≥ 4 years) |

| Typhoon ECRS Mk2 upgrade and MRO cycle | +0.7% | National, focused on RAF Coningsby and Lossiemouth | Medium term (2-4 years) |

| Net-zero strategy accelerating SAF and green propulsion | +0.4% | National, early adoption at major RAF bases | Long term (≥ 4 years) |

| 30:70 synthetic training target | +0.6% | National, concentrated at RAF training establishments | Short term (≤ 2 years) |

| NMH UK build strategy | +0.5% | National, manufacturing focus in Somerset and Yorkshire | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased UK Defense Spending Drives Procurement Acceleration

The firm trajectory toward allocating 2.5% of GDP to defense by 2030 injects roughly GBP 75 billion (USD 91.5 billion) of incremental resources, around 15-20% of which historically flows into aviation programs.[1]“Autumn Statement 2024,” HM Treasury, gov.uk Predictable funding horizons reduce cyclical volatility, enabling primes and tier-ones to invest confidently in domestic production lines, digital tool chains, and sovereign intellectual property. The structured roadmap favors offerings that strengthen multi-domain integration, creating tailwinds for avionics interoperability suites, secure data links, and cyber-hardened mission systems. Unlike austerity-era reviews that trimmed capability breadth, the current framework prizes technological edge and domestic value capture, making industrial localization a decisive bid differentiator. Suppliers able to front-load R&D and scale additive manufacturing garner a head start in upcoming competitive tenders.

Platform Recapitalization Reshapes Fleet Composition

A confluence of end-of-life platforms, such as Hawk T1 trainers and Puma helicopters, and legacy transport variants compresses timelines and forces parallel procurements. Rather than sequential replacements, the Ministry of Defence (MoD) must now manage overlapping acquisition workstreams, amplifying near-term opportunity for suppliers of airframes, training systems, and integrated support equipment.[2]“UK to increase defence spending to 2.5% of GDP by 2030,” UK Government, gov.uk Modern platforms require 40-60% more sophisticated diagnostic and data analytics infrastructure than their predecessors, resulting in higher aftermarket value for original equipment manufacturers that secure prime slots on contracts. The recapitalization wave accelerates base infrastructure upgrades, including high-capacity power networks for blended live-synthetic training environments and SAF storage facilities.

Typhoon ECRS Mk2 Upgrade Anchors Long-Term Growth

The GBP 870 million (USD 1.06 billion) radar development tranche, part of the GBP 2.35 billion (USD 2.87 billion) program, cements the Typhoon fleet’s operational relevance through 2040.[3]“Typhoon ECRS Mk2 radar programme advances,” BAE Systems, baesystems.com Beyond the headline contract, the effort births an indigenous electronic-warfare ecosystem, benefitting UK component fabs and specialist SMEs. Exporting to Germany, Italy, and Spain expands revenue pools and extends sustainment cycles. Integration complexity with legacy mission computers creates high technical barriers, deterring late entrants and preserving incumbent share. The program’s maturation also seeds critical subsystems for the Global Combat Air Programme (GCAP), underpinning future multinational fighter collaborations.

Net-Zero Strategy Accelerates Sustainable Aviation Fuel Adoption

Despite cost multipliers, the RAF’s 2040 net-zero goal and successful 70% lifecycle carbon-reduction SAF trials validate operational use cases. The MoD’s GBP 165 million (USD 217.08 million) SAF infrastructure commitment signals durable demand, catalyzing venture capital inflows to domestic production sites. Military demand de-risks scale-up economics, positioning UK refiners to supply defense and commercial airlines as global mandates tighten. Adjacent funding for electric and hydrogen propulsion demonstrators in unmanned systems sparks cross-sector collaborations, widening the technological aperture for dual-use powertrains.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiscal constraint and program down-sizing | -0.8% | National, affecting all major defense procurement programs | Short term (≤ 2 years) |

| Hawk T2 engine reliability limits training throughput | -0.5% | National, concentrated at RAF Valley and RAF Linton-on-Ouse | Medium term (2-4 years) |

| Post-Brexit certification delays for aero-components | -0.3% | National, impacting European supply chains | Medium term (2-4 years) |

| STEM and digital skills shortage in aerospace workforce | -0.4% | National, acute in Southeast England and Northwest clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fiscal Constraints Force Program Prioritization

Near-term fiscal ceilings impose stricter scrutiny of value for money, despite the upward budget glide path. Independent audits reveal evaluation cycles that can span up to 24 months, prompting manufacturers to absorb pre-contract expenditures or factor in risk premiums. Competitive tendering replaces many sole-source awards, elongating procurement lead times and raising bid-preparation costs, especially for SMEs. Deferred milestone payments disrupt working-capital flows, compelling firms to limit inventory and thus elongate delivery schedules once contracts mature.

STEM Skills Shortage Constrains Production Scaling

An estimated 20,000-person shortfall in aerospace skills by the end of 2030 endangers production ramp-ups, particularly in software, systems integration, and additive manufacturing jobs. Brexit curtails EU talent inflow, and domestic graduation rates in mechanical and electronic engineering lag demand. Apprenticeship schemes and automation investments offer mitigation but require lengthy lead times before productivity gains materialize. Until then, primes and tier-ones must triage projects, potentially slowing output on non-priority programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Rotorcraft Drives Modernization Wave

Rotorcraft programs underpin the fastest-rising slice of the UK military aviation market, with the segment forecasted to post a 6.74% CAGR through 2030. Fixed-wing aircraft retained a 63.79% share of the UK military aviation market size in 2024, thanks to continuous Typhoon and F-35B induction cycles.[4]“F-35 Lightning II Programme,” Lockheed Martin, lockheedmartin.com Multi-role fighters dominate the fixed-wing cohort as the RAF pursues flexible mission sets that blend air superiority, strike, and intelligence tasks. Transport aircraft requirements remain stable; A400M Atlas deliveries cement heavy-lift capacity while C-130J variants carry tactical freight. Training fleets face pressure to refresh because Hawk-series availability is 30% below target, accelerating the integration of synthetic curricula.

The rotary segment's ascent stems from concurrent NMH procurement, Apache AH-64E upgrades, and Chinook sustainment. Multi-mission helicopters claim lion's share because they deftly pivot between combat assault, casualty evacuation, and maritime interdiction tasks. Certification processes administered by the Civil Aviation Authority's (CAA) military wing ensure emerging rotorcraft comply with evolving safety baselines. The NMH Leonardo's AW149 promises modular payload interfaces that encourage in-country retrofits, sustaining high-value maintenance and mission-system upgrade workstreams throughout the life cycle. Competitive bids from Airbus and Sikorsky also broaden prospects for industrial collaboration, augmenting downstream parts demand.

By End-User Service: Joint Operations Reshape Requirements

The Air Force formations held an 81.36% share of the UK military aviation market in 2024, anchored by their stewardship of fast-jet fleets, strategic airlift, and training infrastructure. However, Joint and Special Operations units chart the fastest climb, poised for a 5.86% CAGR through 2030 as multi-domain doctrines demand synchronized air-land-sea effects. The Army Aviation concentrates on battlefield mobility through Apache gunships and light utility helicopters, while the Naval Air Squadrons field F-35B fighters and Wildcat platforms for carrier and maritime patrol operations. Coast Guard and paramilitary agencies operate niche turboprop and light-helicopter fleets tailored for search-and-rescue and border patrol duties.

Joint Force 2025 reforms prioritize standard mission systems and shared logistics pipelines, reducing redundant inventories and life-cycle costs. The trend rewards contractors offering plug-and-play architectures that seamlessly integrate across service boundaries. Interoperability certifications now serve as gatekeepers in tender evaluations, influencing the selection of avionics, datalink, and electronic warfare (EW) suites. Platform suppliers capable of fielding upgrade packages compatible with joint standards stand to capture sustained support revenues as integrated formations mature.

By Propulsion Type: Turboshaft Engines Power Growth

Turbojet engines still underpin 57.48% of the UK military aviation market size in 2024, mirroring the fixed-wing fleet’s dominance. Yet turboshaft units top the growth chart at a 7.43% CAGR, propelled by helicopter fleet modernization and greater engine power-to-weight efficiencies. Rolls-Royce’s EJ200 and Adour series anchor the installed turbojet base supporting Typhoon and Hawk aircraft. Continuous upgrades keep these engines viable through digital health monitoring and the use of additive-manufactured spares.

The turboshaft segment benefits from GE CT7-2E1 engines on the AW149 and uprated powerplants in the Apache fleet. Next-generation units offer 15-20% fuel-burn improvements, strengthening mission endurance and lowering life-cycle costs. The European Aviation Safety Agency's certification frameworks enforce stringent reliability thresholds, prompting OEMs to adopt predictive analytics and condition-based maintenance. Vendors leveraging digital twins and cloud-hosted engine-health dashboards differentiate by boosting fleet availability and reducing unscheduled removals.

Competitive Landscape

The market structure remains moderately concentrated, with top primes capturing the bulk of platform revenue, yet they depend on a lattice of SMEs and technology specialists for subsystems and software. BAE Systems dominates combat air through Typhoon production and upgrade programs, augmented by its role in the GCAP. Leonardo leads the rotorcraft sector, owing to the AW149 NMH award and enduring support contracts for the Wildcat and Merlin. Lockheed Martin commands the fifth-generation fighter segment via F-35B deliveries, while Boeing sustains heavy-lift prowess through Chinook upgrades.

Digital transformation defines the new battleground. Patent filings in aviation AI rose 340% between 2022 and 2024, signaling accelerated R&D around autonomy, predictive maintenance, and cognitive EW. Primes collaborate with universities and software start-ups to accelerate digital twin deployments, reducing design iterations and compressing certification timelines. Post-Brexit regulatory divergence grants advantage to firms versed in navigating the UK CAA's Military Aviation Authority guidance while preserving EASA mutual recognition for exports.

Supply-chain depth and sovereign resilience now weigh heavily in contract evaluations. Firms embed additive-manufacturing hubs near RAF depots to reduce spares lead-times and demonstrate domestic industrial value. Workforce shortages spur the adoption of automation; for example, Airbus' new Filton wing-box line utilizes collaborative robots to mitigate skilled labor scarcity. Competitive positioning also hinges on SAF and net-zero pathways as the MOD embeds carbon metrics into bid assessment. Vendors offering validated SAF-compatible engines and fielded emissions-tracking software enhance win probabilities in upcoming maintenance frameworks.

UK Military Aviation Industry Leaders

Airbus SE

Lockheed Martin Corporation

The Boeing Company

BAE Systems plc

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The UK MoD announced its plans to acquire around 12 F-35A stealth fighters. These aircraft will provide the Royal Air Force (RAF) with nuclear and conventional strike capabilities from the air.

- April 2025: The UK MoD awarded Leonardo a GBP 165 million (USD 200 million) contract extension to maintain the Royal Navy's fleet of 54 Merlin helicopters. This development reflects the UK's commitment to increased defense spending.

- February 2025: The UK MoD announced its plans to award the prime contract for its NMH program.

- December 2024: Airbus delivered the final A400M Atlas, completing the 22-aircraft strategic airlift program.

UK Military Aviation Market Report Scope

| Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | |

| Transport Aircraft | |

| Other Aircraft | |

| Rotorcraft | Multi-Mission Helicopter |

| Transport Helicopter | |

| Other Helicopter |

| Air Force |

| Army Aviation |

| Naval/Marine Corps Aviation |

| Joint/Special Operations |

| Paramilitary and Coast Guard |

| Turbofan |

| Turbojet |

| Turboprop |

| Turboshaft |

| Fully Electric/Hybrid-Electric |

| By Aircraft Type | Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | ||

| Transport Aircraft | ||

| Other Aircraft | ||

| Rotorcraft | Multi-Mission Helicopter | |

| Transport Helicopter | ||

| Other Helicopter | ||

| By End-User Service | Air Force | |

| Army Aviation | ||

| Naval/Marine Corps Aviation | ||

| Joint/Special Operations | ||

| Paramilitary and Coast Guard | ||

| By Propulsion Type | Turbofan | |

| Turbojet | ||

| Turboprop | ||

| Turboshaft | ||

| Fully Electric/Hybrid-Electric | ||

Market Definition

- Aircraft Type - All the military aircraft and rotorcraft which are used for various applications are included in this study.

- Sub-Aircraft Type - For this study, sub-aircraft types such as fixed-wing aircraft and rotorcraft based on their application are considered.

- Body Type - Multi-Role Aircraft, Transport, Training Aircraft, Bombers, Reconnaissance Aircraft, Multi-Mission Helicopters, Transport Helicopters and various other aircraft and rotorcraft are considered in this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms