Military Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

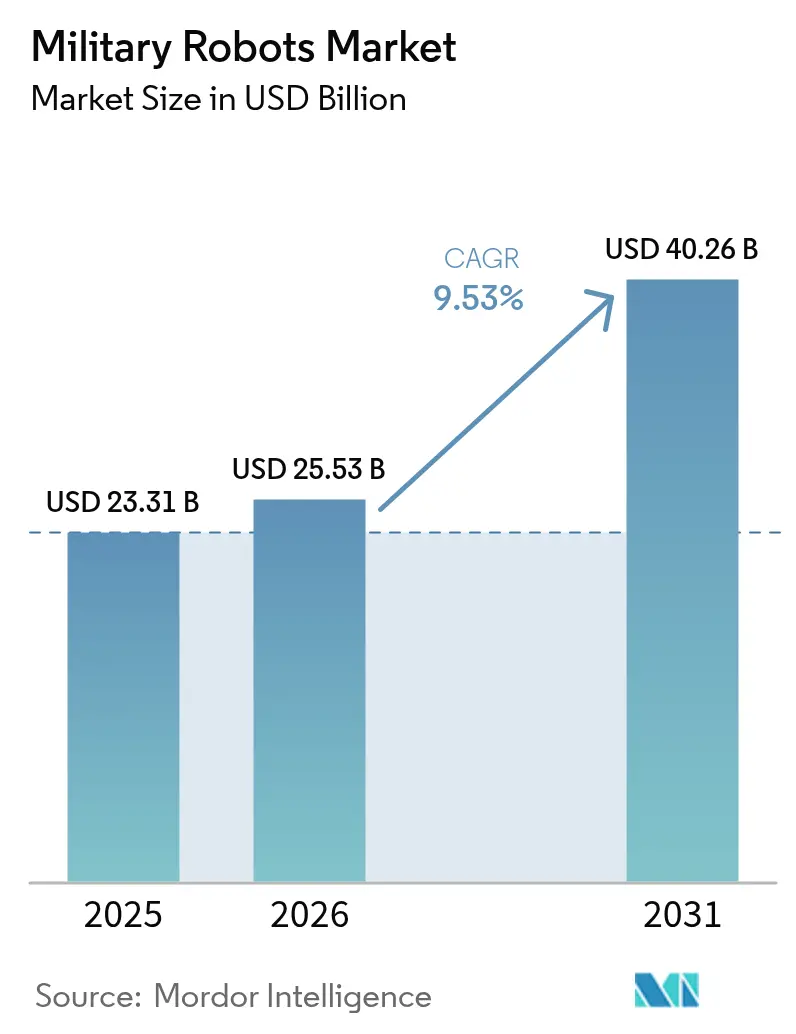

| Market Size (2026) | USD 25.53 Billion |

| Market Size (2031) | USD 40.26 Billion |

| Growth Rate (2026 - 2031) | 9.53% CAGR |

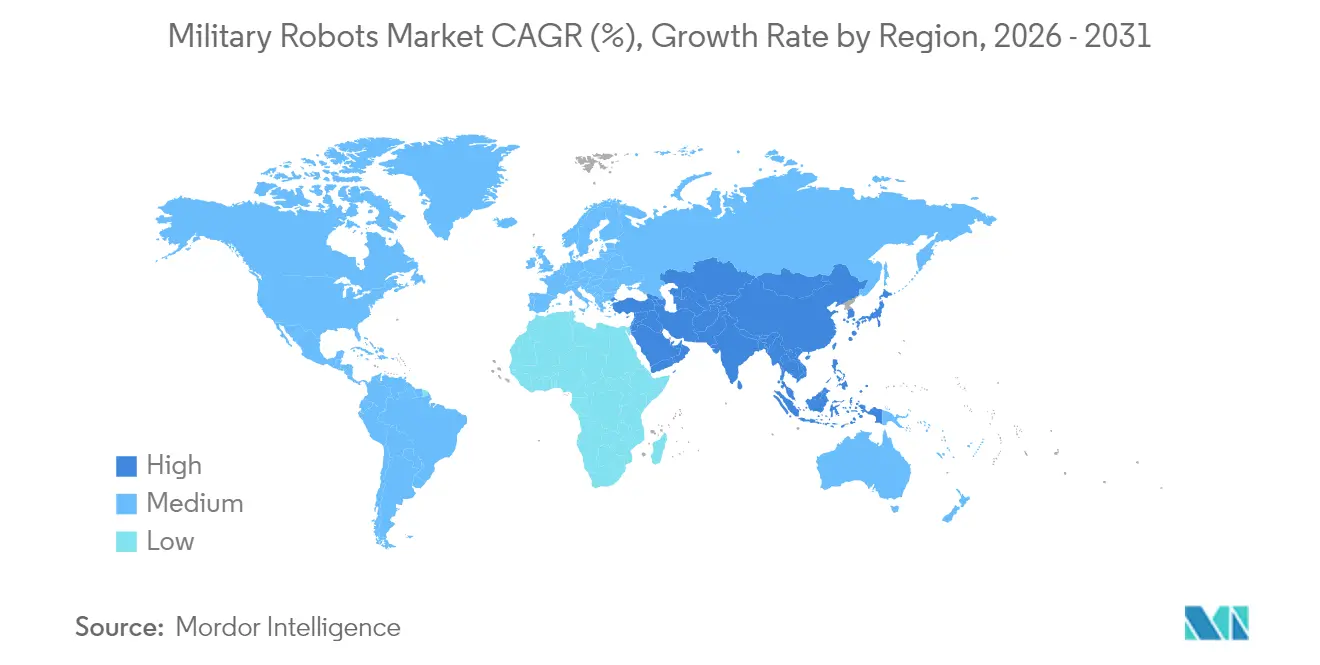

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

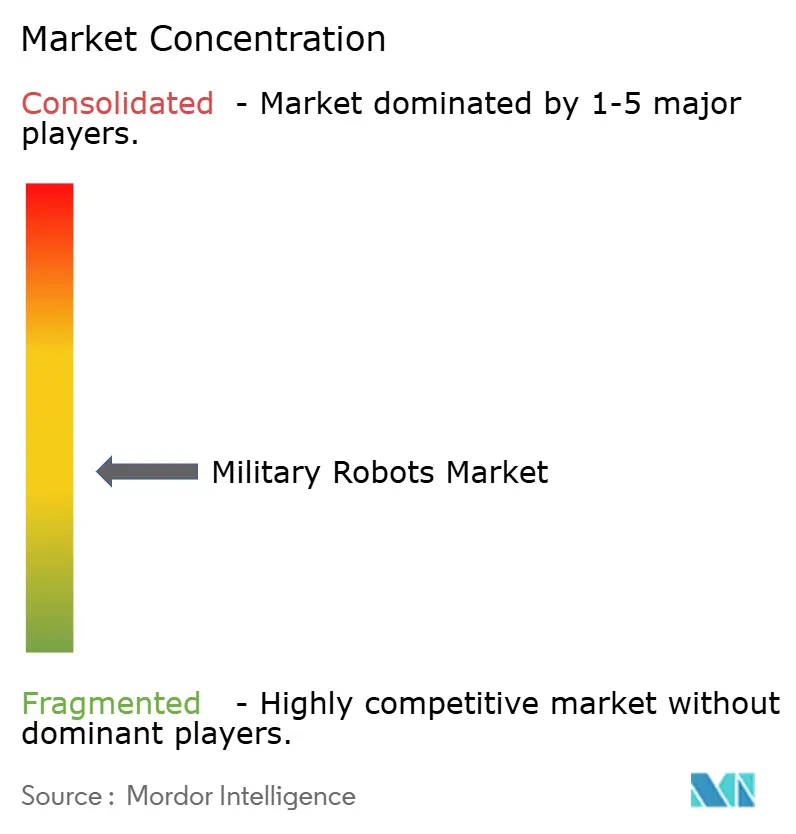

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Robots Market Analysis by Mordor Intelligence

The military robots market size is expected to grow from USD 23.31 billion in 2025 to USD 25.53 billion in 2026 and is forecast to reach USD 40.26 billion by 2031 at 9.53% CAGR over 2026-2031. Growth is powered by surging adoption of autonomous and semi-autonomous systems across air, land, and sea, reflecting lessons from the Ukraine conflict, shifting NATO and AUKUS doctrines, and rapid edge-AI innovation. Budget reallocations from traditional crewed platforms toward swarming drones and uncrewed ground vehicles (UGVs) are broadening demand. At the same time, advances in secure communications and ruggedized processors enable reliable operations in jammed environments. The Pentagon’s Replicator program is accelerating mass production of expendable systems that overwhelm adversaries by volume rather than unit sophistication. China’s civil-military fusion policies are triggering a regional response that lifts procurement across Asia-Pacific. At the same time, tightening European export rules on lethal autonomy and persistent battery-density limits in desert operations act as counterweights but have yet to derail the overall upward trajectory of the military robots market.

Key Report Takeaways

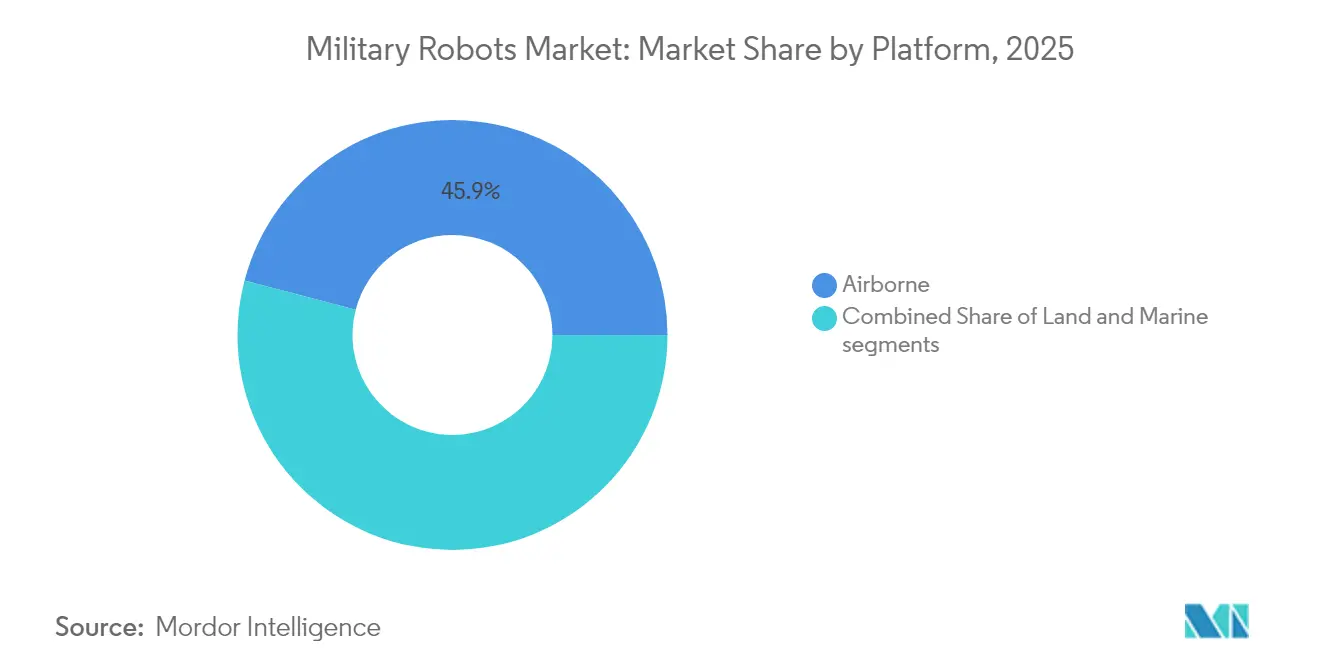

- By platform, airborne systems led with a 45.92% revenue share of the military robots market in 2025, while land platforms are projected to post the fastest 13.12% CAGR to 2031.

- By mode of operation, human-operated solutions held 55.74% of the military robots market size in 2025; fully autonomous modes are advancing at a 12.65% CAGR through 2031.

- By application, ISR accounted for 44.71% of the military robots market share in 2025, whereas logistics and EOD are set to expand at a 14.25% CAGR between 2026 and 2031.

- By payload, EO/IR sensors captured 30.21% of the military robots market size in 2025; EW pods represent the fastest-growing payload at a 11.84% CAGR.

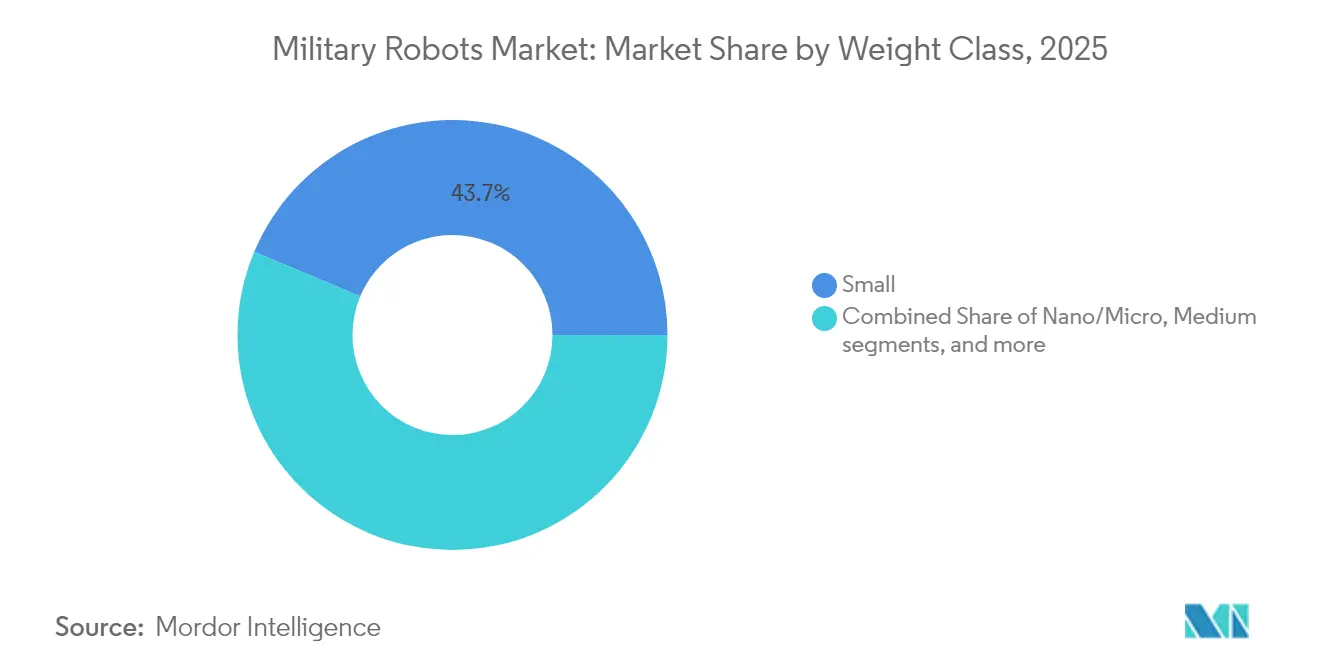

- By weight class, small (10-200 kg) vehicles commanded a 43.68% share of the military robots market size in 2025, with nano/micro platforms rising at a 9.04% CAGR.

- By mobility, tracked held a 35.02% share of the military robots market in 2025, legged/bionic platforms will accelerate at a 15.02% CAGR to 2031.

- By geography, North America led with 29.76% revenue share in 2025; Asia-Pacific is forecasted to expand at an 8.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Military Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated NATO and AUKUS battlefield-digitization programs | +2.1 | North America, Europe, Australia | Medium term (≈3-4 yrs) |

| Ukraine-war–driven demand for attritable land-drone swarms | +1.8 | Europe, with spillover to global markets | Short term (≤2 yrs) |

| US DoD “Replicator” USD 1 Bn initiative for expendable autonomous systems | +1.5 | North America, with spillover to allied nations | Medium term (≈3-4 yrs) |

| Edge-AI breakthroughs enabling compliant autonomous target recognition | +1.2 | Global, with early adoption in North America | Medium term (≈3-4 yrs) |

| Oil-infrastructure protection spurring naval USV adoption | +0.9 | Middle East, particularly GCC states | Medium term (≈3-4 yrs) |

| China’s civil-military fusion subsidies | +0.8 | Asia-Pacific, primarily China | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Accelerated NATO and AUKUS Battlefield-Digitisation Programs

Sustained increases in allied defense budgets are earmarked for network-ready unmanned platforms, with every US Army division slated to field drones by 2026 and AUKUS partners harmonizing command architectures to enable plug-and-fight interoperability.[1]U.S. Department of Defense, “Deputy Secretary Announces Replicator Details,” defense.gov Larger primes are standardizing open controllers so multiple robots can share data links, shortening integration cycles and favoring vendors that provide software-defined radios hardened against jamming. Europe’s annual defense spending now grows 6.1%, reinforcing a procurement pivot from legacy crewed assets to agile, mission-specific robots that fit within digitised formations. Collectively, these dynamics add fresh order visibility that underpins the military robots market through the end of the decade.

Ukraine-War Demand for Attritable Land-Drone Swarms

The March 2025 fully robotic assault in Donetsk proved that low-cost UGV-and-FPV combinations can neutralise heavier armour, prompting NATO front-line armies to re-engineer manoeuvre brigades around massed expendable platforms. Capital flows to start-ups able to deliver thousands of simple robots at pace, and framework contracts increasingly specify cost ceilings that assume planned loss rates. As a result, the military robots market sees rising volumes even where unit margins compress, rewarding scale players that can automate final assembly and test.

The US DoD “Replicator” USD 1 billion Initiative

Replicator accelerates concept-to-field timelines to under 24 months, engages more than 500 firms, three-quarters of which are non-traditional, and prioritises rapid software updates to counter new threats. The Navy’s establishment of a dedicated small-vessel squadron and the Air Force’s fighter-designated Collaborative Combat Aircraft show how the model reshapes force structures. Because procurement batches are larger and more frequent, suppliers that master automotive-style production reap share gains in the military robots market.

Edge-AI Breakthroughs for Compliant Target Recognition

Rugged tactical processors now fuse EO/IR, radar, and RF sensors to detect and classify threats without cloud connectivity, preserving human judgment while compressing the observe-orient-decide-act loop. Northrop Grumman’s AI-enabled FAAD and similar systems demonstrate weapon-target pairing in seconds in jammed environments.[2]AIM Research, “AI-Enabled Forward Area Air Defense Demonstrator,” aimresearch.orgExplainable-AI modules satisfy emerging policy that demands transparent algorithmic logic, positioning vendors with proven audit tools for sustained demand in the military robots market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geneva-Convention concerns delaying lethal-autonomy export clearances | -1.4 | Europe, with global regulatory impact | Medium term (≈3-4 yrs) |

| EW-jamming vulnerabilities of COTS comm-links | -1.2 | Global, particularly in contested environments | Short term (≤2 yrs) |

| Battery energy-density limits constraining desert-operations | -0.7 | Middle East, Africa, Southwest Asia | Medium term (≈3-4 yrs) |

| US export-control curbs on rad-hardened AI chips | -0.6 | Asia-Pacific, particularly China | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Geneva-Convention Concerns Delaying Lethal-Autonomy Exports

The UN Resolution 78/241 and the ICRC’s call for binding rules add compliance layers that slow European export licences, increase documentation costs, and lengthen development cycles for AI-enabled lethal payloads.[3]International Committee of the Red Cross, “ICRC Welcomes UN Resolution on Autonomous Weapons,” icrc.org While this spurs innovation in “human-on-the-loop” safeguards, it shifts some near-term orders to regions with fewer constraints, fragmenting certified demand and tempering growth momentum within the military robots market.

EW-Jamming Vulnerabilities of Commercial Links

Over half of Ukrainian drones suffered jamming incidents because widely used radios emit predictable signatures. Rapid advances in fibre-optic tethers and adaptive beamforming radars mitigate the threat but add integration complexity, particularly for nano platforms where weight budgets are tight. Vendors that cannot deliver hardened comms face procurement headwinds, trimming upside in the military robots market until secure links become standard.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Land Systems Closing the Gap on Airborne Dominance

Airborne robots generated 45.92% of the military robots market revenue in 2025. Yet, land platforms expand at a 13.12% CAGR as battle-tested UGVs prove indispensable for breaching, casualty evacuation, and sensor-relay missions. Large quadrotors such as the Ghost X still provide the reach and height essential for brigade ISR, but demand for attritable ground swarms that can absorb heavy losses is rising sharply. Ukraine’s USD 250,000 drone-carrying USVs underscore cross-domain innovation that pulls naval operators into the military robots market.

Land-robot growth is further propelled by cheaper drivetrains, lighter composite armour, and AI stacks that enable obstacle negotiation without GPS. Air platforms respond by adding multi-payload bays and electronic-attack pods to stay relevant. Although a small slice, Marine robots receive targeted spending from GCC navies focused on oil-terminal defense. The interplay across domains broadens supplier opportunities and brings fresh entrants into the military robots market.

By Mode of Operation: Spectrum of Control Widens

Human-operated robots held 55.74% of the military robots market share in 2025 because policy still requires human confirmation for lethal action. Fully autonomous modes, however, advance at 12.65% CAGR thanks to onboard neural-network accelerators that classify threats within milliseconds. Programs such as CJADC2 integrate time-sensitive networking so commanders can retask fleets from a single console without latency, representing evolutionary rather than revolutionary change.

Semi-autonomy remains the workhorse because it splits cognitive load: operators define mission goals while autonomy manages route-planning and obstacle avoidance. Overland AI’s Ultra vehicle, one soldier can control alongside multiple sister units, illustrates how duty-cycled oversight eases workforce demands. As doctrinal trust grows, the military robots market will likely see autonomously initiated engagement options bounded by predefined rulesets.

By Application: Logistics Surges on Proven Risk Reduction

ISR stayed at 44.71% of the military robots market revenue in 2025, but logistics and EOD now lead growth at 14.25% CAGR. Robots that haul ammunition, clear mines, or deliver medical supplies cut exposure for soldiers and increase tempo. The US Army’s HADES high-altitude ISR platform demonstrates how combining large crewed jets with launchable drones amplifies coverage without added risk.

Combat support robots evolved rapidly after Ukraine’s purely unmanned assault, pushing procurement offices to test swarm tactics. Sensors triangulating hostile RF emitters bolster C-EW missions, and CBRN platforms extend endurance in toxic zones. As payload modularity matures, users adapt one chassis for multiple roles, reinforcing lifecycle value and broadening the military robots market.

By Payload: EO/IR Stays Core while EW Pods Accelerate

EO/IR suites generated 30.21% of the 2025 segment revenue by supplying day/night visuals essential for precision fires and BDA. EW pods’ 11.84% CAGR stems from the doctrine that seeks spectrum dominance; lightweight jammers disrupt enemy C2 without emissions heavy enough to invite immediate targeting. The contracts for night-vision binoculars underline the continued need for soldier-worn sensors that complement robot feeds.

Lidar and SAR modules gain traction for all-weather mapping, and multi-sensor fusion reduces single-point failure. Non-lethal payloads like net-launchers help in urban site security, and optional weapon stations progress under stringent oversight rules. Together, these trends enlarge integration budgets within the military robots market.

By Weight Class: Miniaturisation Enables Distributed Ops

Small (10-200 kg) robots owned a 43.68% share in 2025, balancing payload and portability. Nano/micro platforms under 10 kg sprint ahead at 9.04% CAGR, propelled by sub-centimetre flyers weighing mere milligrams yet providing close reconnaissance. Swarm algorithms stitch many cheap sensors into one cohesive picture, stressing legacy air-defense radars.

Medium robots carry heavier armour or munitions, while heavy variants exceed 2 tons for breaching or casualty evacuation. China’s focus on mass-produced small drones and Replicator’s parallel vision for attritable quantities converge to ensure that unit counts, not platform price, drive future procurement. This quantity-centric mindset fuels volume growth across the military robots market.

By Mobility: Tracked Reliability Meets Legged Agility

Tracked chassis retained a 35.02% share in 2025 for their stability and payload capacity. Legged/bionic robots now post a 15.02% CAGR on superior locomotion over rubble and stairways. Patent peace between Boston Dynamics and Ghost Robotics frees both firms to refine quadruped designs around lighter batteries and modular sensor pods, potentially lowering acquisition cost.

Wheeled vehicles dominate convoy logistics with higher road speed, and hybrid drivetrains toggle between modes to match terrain. Recent infantry trials show legged scouts paired with tracked fire-support robots to exploit complementary strengths, underscoring the architecture diversification underpinning the military robots market.

Geography Analysis

North America remains the largest spender, anchored by USD 1 billion in Replicator funding and mandated drone deployment across all US Army divisions by 2026. Canada’s NORAD upgrade complements these efforts by fielding autonomous Arctic surveillance towers resilient to polar conditions. A mature supplier base spanning primes and start-ups sustains technology leadership, ensuring continued dominance of the military robots market in the region.

Asia-Pacific is the fastest-growing segment as China’s civil-military fusion subsidies accelerate domestic scale-out and spur responses from India, South Korea, and Japan. Beijing’s push for humanoid robots and mass-swarms shifts regional procurement toward cheap, numerous systems, while Seoul’s Hanwha Aerospace rolls out armed UGVs optimised for DMZ patrols. Maritime disputes in the South China Sea trigger parallel investment in USVs and seabed-monitoring crawlers.

Europe’s defense budgets grow 6.1% annually through 2035, driven by the lessons of the Ukraine war that validate attributable drones and ground swarms. France’s DROIDE framework and Germany’s new Bundeswehr robotics plan reflect the urgency of reinforcing NATO’s eastern flank. Export-licence scrutiny over lethal autonomy tempers shipment speed yet channels R&D funds into “human-in-the-loop” safeguards, differentiating European contributions to the military robots market.

The Middle East focuses on spending on naval USVs to guard oil terminals. Israel’s operational deployment of RobDozer and robotic M113 variants proves reliability in austere desert theatres. At the same time, the UAE’s EDGE Group builds indigenous boats and ground-robot capacity that is aligned with Vision 2030's localisation goals. Saudi Arabia’s joint ventures on autonomous patrol craft further expand a niche but lucrative slice of the military robots market.

South America invests selectively; Brazil’s USD 23.7 billion 2025 defense budget allocates funds for networked artillery and surveillance drones to police vast borders and Amazonia. Economic constraints limit volume, yet region-specific needs for anti-narcotics monitoring and disaster relief open opportunities for rugged, cost-efficient robots tailored to jungle conditions.

Regulatory Landscape

Policy for autonomy in military robotics is tightening around documented human judgment, verification, and traceability requirements. In the United States, DoD Directive 3000.09 (updated January 2023) anchors autonomy in weapon systems by prescribing governance, testing, and senior-level reviews. In June 2026, legislative activity added design, safety, and human-oversight requirements for autonomous and semi-autonomous weapon systems (S. 4697 and S. 4707), and advanced draft FY2027 NDAA language in the Senate Armed Services Committee addressed force-generation and interoperability structures for robotics and autonomous systems.

In Europe, the EU Artificial Intelligence Act (Regulation (EU) 2024/1689), in force from August 2024, functions as a horizontal compliance layer that intersects with product and safety regimes for autonomous systems. Defense-specific standardization and safety work continues through bodies such as the European Defence Agency (EDA), including initiatives to formalize safety and regulatory guidance for unmanned maritime systems and to support interoperability through EU-NATO-aligned testing and exercise constructs. These efforts influence exportability and the procurement qualification pathways for military robots.

Value Chain Analysis

The military robots value chain spans upstream critical materials (notably battery inputs and permanent magnets), propulsion and power electronics, mission sensors (EO/IR, radar, RF), communications and encryption, compute and edge-AI hardware, and autonomy software stacks, before moving into platform-level integration across airborne, land, and marine domains. Prime contractors and specialized integrators typically own system architecture, secure networking, and mission certification, while a growing set of non-traditional suppliers contribute autonomy, perception, and rapid software iteration, reflecting procurement pull from programs such as the US DoD Replicator initiative.

Downstream, defense acquisition pathways increasingly pair rapid contracting with field experimentation, which accelerates the loop from prototype to operational units. This approach pulls more of the supply base into test, verification, and cyber-hardening workflows. Recent US program actions illustrate the flow: Gecko Robotics secured a five-year US Navy and GSA IDIQ for ship inspection robotics with an initial USD 54 million award (March 2026), and Overland AI won a USD 20 million Marine Corps contract for autonomous ground vehicles tied to MADIS integration (June 2026). Together, these awards point to increased emphasis on scalable production, digital-thread sustainment tooling, and interoperability-ready autonomy for broader command architectures.

Competitive Landscape

The military robots market features a dual-speed structure. Legacy primes—Lockheed Martin Corporation, Northrop Grumman Corporation, and General Dynamics Corporation—retain an edge in complex integration and secure supply chains. Lockheed Martin reported USD 18 billion in Q1 2025 sales and a USD 173 billion backlog, underscoring durable demand for integrated systems.[4]Lockheed Martin Corporation, “First-Quarter 2025 Financial Results,” lockheedmartin.comThese primes embed open architectures and AI kernels that support plug-and-play upgrades to stay ahead.

Disruptive entrants such as Anduril and Shield AI apply Silicon Valley sprint cycles, launching new code fortnightly and leveraging commercial cloud toolchains to slash development costs. Replicator’s open solicitation funnels contracts to these firms, and 75% of initiative partners are non-traditional vendors, broadening participation across the military robots market.

Strategic alliances blur lines between old and new. The Boston Dynamics-Ghost Robotics truce redirects resources from litigation to policy advocacy, and both now lobby for a national robotics strategy that secures funding for advanced mobility research.[5]TechCrunch, “Boston Dynamics and Ghost Robotics End Patent Fight,” techcrunch.com Israeli firms—particularly Israel Aerospace Industries and Elbit Systems—lead in battle-proven ground and sensor payloads, winning export deals that validate performance under live fire.

European suppliers Rheinmetall, Saab, and Leonardo benefit from rising regional budgets and specialise in modular turrets, active protection, and anti-drone nets. South Korea’s Hyundai Rotem scales tracked UGV production, while Chinese conglomerates exploit civil-sector volume to undercut prices in Africa and South America. These forces intensify rivalry and accelerate technology diffusion throughout the military robots market.

Military Robots Industry Leaders

Lockheed Martin Corporation

AeroVironment Inc.

Israel Aerospace Industries Ltd.

General Dynamics Corporation

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in high-volume procurement and force-wide integration of attritable systems, with buyers pairing rapid acquisition with structured demonstrations and standardized interfaces. In the United States, the Pentagon outlined a USD 55 billion Defense Autonomous Warfare Group (DAWG) R&D plan for FY27 (April 2026) and progressed swarm-focused events such as the Crucible demonstration concept (June 2026). This creates direct pull for vendors supplying swarm coordination, resilient communications, and edge-AI packages that can be updated on operational timelines.

Opportunities are also forming in applied readiness and sustainment robotics, along with task-specific ground systems that reduce soldier exposure. The US Navy and Marine Corps contracting for 34 L3Harris T7 robots for EOD (January 2026) signals continued demand for proven UGVs in hazardous missions. Gecko Robotics five-year US Navy and GSA IDIQ with an initial USD 54 million award (March 2026) further indicates budgets moving toward fleet inspection and maintenance automation tied to measurable readiness outcomes. In parallel, standardization work through NATO Science and Technology Organization publications on mobility assessment methods and cryptographic trust frameworks for agentic autonomy (2026) supports interoperability-focused product roadmaps, benefiting suppliers that can certify behavior, enable secure multi-agent control, and operate in jammed or GPS-denied environments.

Recent Industry Developments

- July 2026: AeroVironment announced a three-year USD 500 million IDIQ in support of the JIATF-401 Domestic Shield program for counter-UAS capabilities. The structure supports rapid tasking and scaling of base-defense sensing and defeat packages, reinforcing demand for deployable C-UAS systems that integrate with broader security architectures.

- December 2025: AeroVironment was awarded an approximately USD 874.26 million, five-year US Army Contracting Command IDIQ to deliver UAS and C-UAS systems via foreign military sales to allied partner forces. The award expands standardized export channels for small UAS, loitering munition-adjacent systems, and counter-drone kits, supporting higher-volume production and configuration control across multiple end users.

- August 2024: AeroVironment secured a USD 990 million, five-year IDIQ linked to the US Army Lethal Unmanned Systems Directed Requirement. The contract vehicle underpins continued procurement of attritable unmanned capabilities and strengthens supply-chain commitments for high-throughput deliveries aligned to evolving operational concepts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The market covers military-use robotic systems that are bought, fielded, and supported to perform defense missions. This includes unmanned or robotized platforms and mission payload-ready configurations across land, air, and maritime environments.

Scope exclusions: This sizing excludes civilian drones, industrial robots used only in factories, and software-only command-and-control tools that are not sold as part of a military robot system.

Segmentation Overview

- By Platform

- Land

- Airborne

- Marine

- By Mode of Operation

- Human Operated

- Semi-Autonomous

- Fully Autonomous

- By Application

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Combat Support/Strike

- Logistics and EOD

- Search and Rescue

- Fire-fighting and CBRN response

- By Payload

- EO/IR Sensor Suites

- Radar and Lidar Modules

- Electronic-Warfare Pods

- Lethal Weapon Stations

- Non-lethal Systems (Tasers, Nets)

- By Weight Class

- Nano/Micro ( less than 10 kg)

- Small (10–200 kg)

- Medium (200–2,000 kg)

- Heavy (more than 2,000 kg)

- By Mobility

- Tracked Platforms

- Wheeled Platforms

- Legged/Bionic Platforms

- Hybrid (Tracked-Wheeled)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- France

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping demand through defense budgets and procurement signals, then checking how those flows show up in deployed systems and upgrades. Public sources include the Stockholm International Peace Research Institute, NATO and national defense ministry releases, US DoD budget documents, Congressional Research Service briefs, and UN Comtrade for related trade classifications where applicable.

To turn those inputs into sizing assumptions, we also review company annual reports, investor presentations, contract award announcements, defense exhibition disclosures, and reputed defense press coverage. When needed, paid subscriptions are used for company financials and intelligence coverage, patent databases, and defense contracts and tenders, mainly to confirm program timing and supplier participation. The sources named above are illustrative, and they are complemented by other public references for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test desk assumptions with people who handle programs in practice, including capability and program teams, system integrators, component suppliers, and end-user side experts involved in doctrine and deployment. Because this is a global market, we also keep views balanced across APAC, EMEA, and the Americas so regional procurement cycles and mission priorities are reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 17% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 19% | Managers: 49% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built mainly using a top-down and bottom-up combination. First, defense procurement and modernization spending are reconstructed into a military robotics demand pool, then filtered by platform adoption patterns. The totals are corroborated with selective bottom-up approximations, such as sampled unit volumes multiplied by typical program ASP bands, channel checks on payload-ready configurations, and supplier revenue exposure, which helps adjust for overcounts.

Inputs used in the model include variables like defense budget direction, unmanned program award values and delivery schedules, platform mix shifts across land, airborne, and marine robots, autonomy-level uptake (human operated to fully autonomous), and refresh cycles for mission payloads like EO/IR. For forecasting, we run scenario analysis informed by expert consensus on procurement timing, conflict-driven urgency, and technology readiness, then apply region- and platform-specific growth curves. Where bottom-up datapoints are patchy, gaps are handled using program-level proxies and conservative adoption rates that are later verified through follow-up calls.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as budget shares, publicly visible program pipelines, and historical delivery cadence so the numbers remain realistic. If a segment shows an unusual jump, we re-check currency timing, platform mix, and any one-off contract effects before sign-off, and we may re-contact experts to confirm the change.

Each report is refreshed annually, and interim updates are made when material events occur, such as large program awards, major conflicts that shift spending, or policy changes around autonomy. Before delivery, a final pass is completed so clients receive an up-to-date view rather than an older frozen estimate.

Mordor Intelligence's Military Robot Market Size Versus Other Published Estimates

Published market sizes for military robots often differ because studies do not count the same items, and they also apply different base years and currency timing. Most gaps show up around what is treated as a complete system, which platforms are included, and how fast procurement ramps are assumed to normalize.

Civilian drones, industrial manipulators, and software-only command-and-control packages sit outside Mordor Intelligence's scope. That reduces adjacent revenues that some estimates blend into military robotics, which changes the starting market value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.53 B (2026) | |

| Global Consultancy A | USD 19.68 B (2024) | Uses an earlier base year and a shorter forecast window, and the coverage appears to emphasize airborne and marine systems more strongly, which can understate land robot momentum in more recent procurement cycles. |

| Industry Publisher B | USD 18.10 B (2024) | Anchors sizing to 2024 and may treat manually operated and automated categories differently, and it can rely more on historical trend extension rather than program timing checks that capture delivery bunching. |

Across the three figures, the spread is mostly explained by base-year alignment and what each vendor counts as a full military robot system versus adjacent software or non-military robotics revenues. With scope tied to platform procurement signals, then validated using practical ASP and volume checks, the final number stays traceable to inputs that can be revisited during each update cycle.

Key Questions Answered in the Report

What is the current size of the military robots market?

The military robots market stands at USD 25.53 billion in 2026 and is projected to hit USD 40.26 billion by 2031, registering a 9.53% CAGR.

Which platform dominates revenue today?

Airborne robots hold 45.92% of 2025 revenue, though land systems are the fastest-growing at a 13.12% CAGR.

How fast are fully autonomous robots growing?

Fully autonomous modes are expanding at 12.65% CAGR between 2026-2031 as edge-AI and secure networking mature.

Why are edge-AI processors important for military robots?

They allow real-time target recognition in jammed or GPS-denied environments, reducing decision latency while retaining human oversight.

How is the Replicator programme affecting suppliers?

Replicator shifts procurement toward high-volume, expendable platforms and opens contracts to non-traditional vendors, broadening participation in the military robots market.

Which region is the fastest-growing market for military robots?

Asia-Pacific leads growth as China’s civil-military fusion strategy triggers parallel investments by India, South Korea and Japan.

Page last updated on: