Commercial Aircraft Interior Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

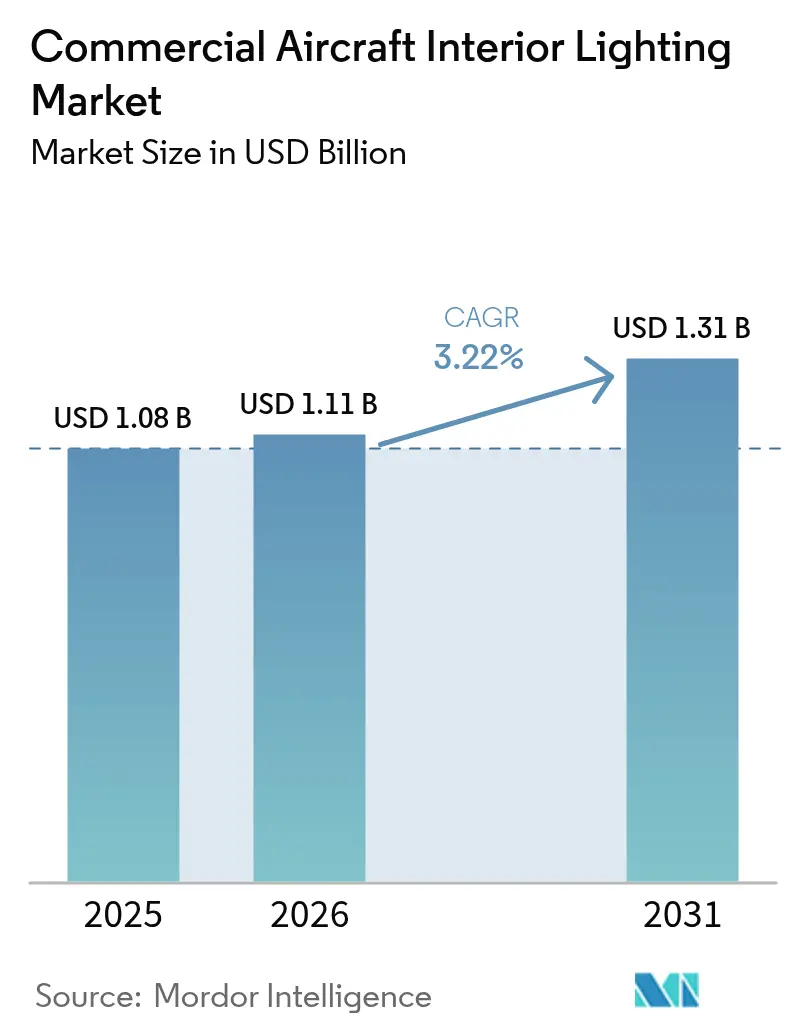

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Interior Lighting Market Analysis by Mordor Intelligence

Market Analysis

The commercial aircraft interior lighting market size was valued at USD 1.08 billion in 2025 and estimated to grow from USD 1.11 billion in 2026 to reach USD 1.31 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031). Airlines invest in LED retrofits that cut power draw, trim weight, and unlock mood-lighting features that sharpen brand experience, even as post-pandemic capacity rationalization tempers overall fleet growth. Narrowbody platforms dominate new deliveries because low-cost carriers (LCCs) continue to up-gauge seat density on short-haul routes. At the same time, retrofit activity accelerates within North America’s mature fleets as carriers refresh cabins instead of ordering expensive widebody aircraft. Semiconductor shortages slow delivery schedules, prompting operators to turn to plug-and-play lighting kits that can be installed overnight. Certification lead times remain a headwind, yet suppliers with multiple STCs gain meaningful speed-to-market advantages. Despite these constraints, rising ESG commitments and regulatory moves away from mercury-based fluorescents position LEDs as the unquestioned technology baseline for the next decade of growth in the commercial aircraft interior lighting market.

Key Report Takeaways

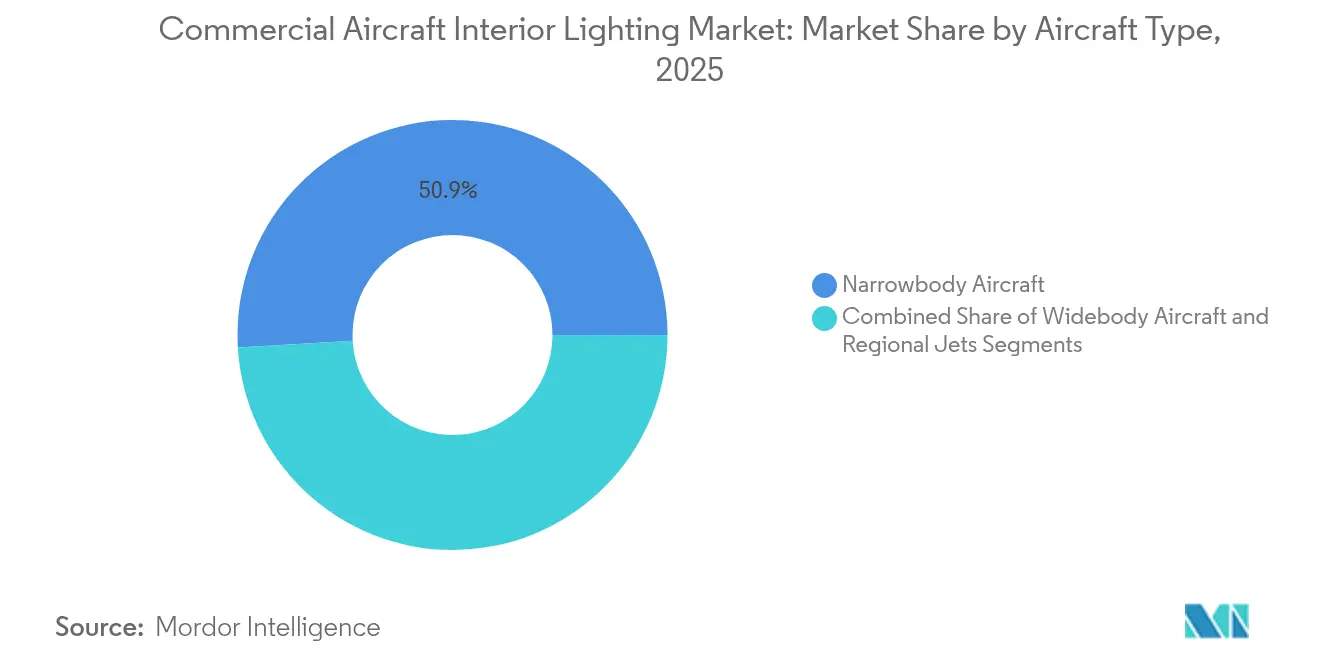

- By aircraft type, narrowbody jets held 50.92% of the commercial aircraft interior lighting market share in 2025, whereas widebody aircraft are projected to post the quickest 3.62% CAGR through 2031.

- By light type, ceiling and wall installations captured 43.35% of the commercial aircraft interior lighting market size in 2025; reading lights are set to advance at a 3.98% CAGR over the same horizon.

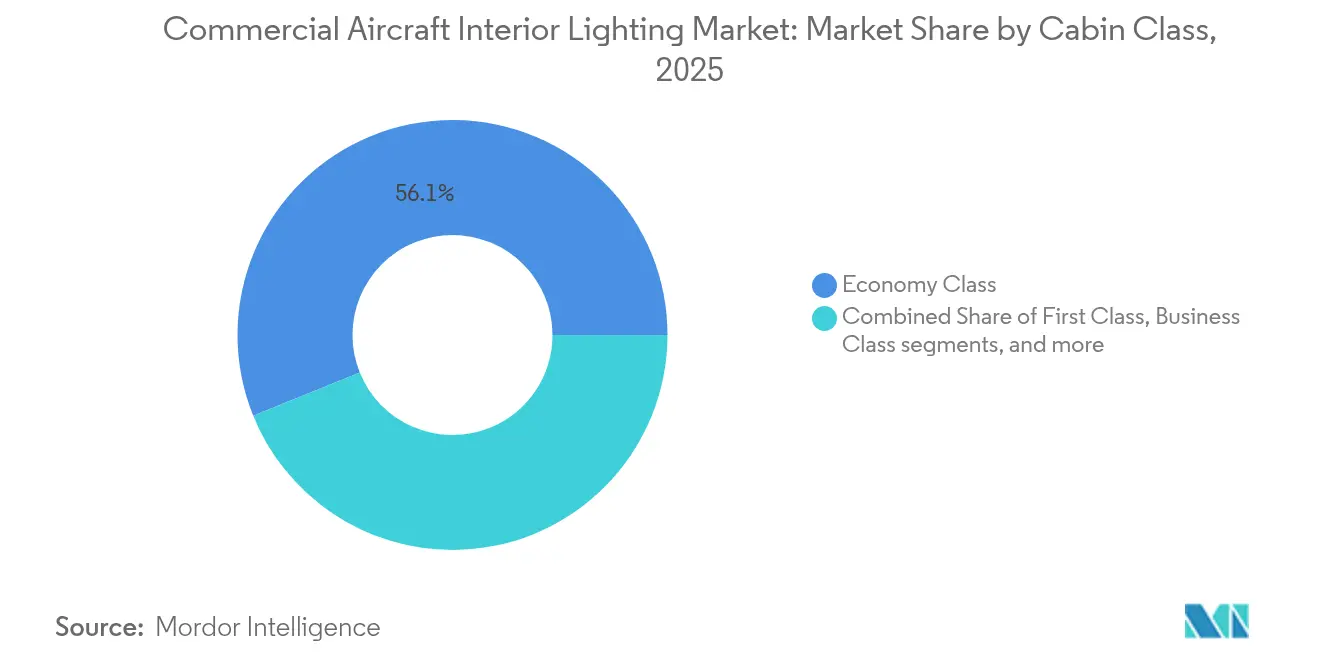

- By cabin class, economy accounted for 56.12% of revenue in 2025, while premium economy led growth at a 3.71% CAGR.

- By end user, OEM line-fit represented 51.55% of the commercial aircraft interior lighting market size in 2025; aftermarket retrofits are expanding faster at 3.97% CAGR.

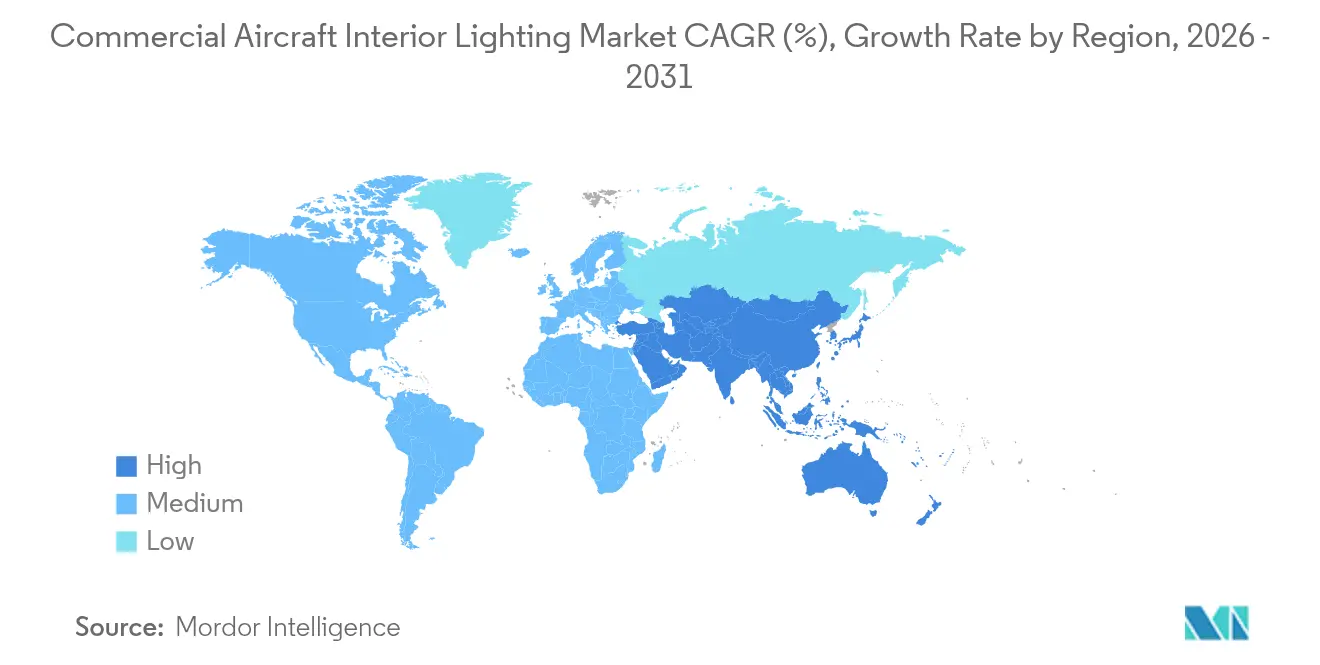

- Regionally, North America commanded 38.55% of 2025 revenue; Asia-Pacific is forecasted to log the highest 4.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Interior Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated narrowbody fleet expansion among LCCs | +0.8% | Asia-Pacific core, spill-over to MEA and Europe | Medium term (2-4 years) |

| Retrofit wave toward LED mood-lighting for cabin refresh | +0.6% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Shift from fluorescent to energy-efficient, RoHS-compliant LEDs | +0.5% | Global regulatory compliance driven | Long term (≥ 4 years) |

| IoT-enabled smart lights enabling predictive maintenance | +0.4% | North America and EU advanced markets first | Long term (≥ 4 years) |

| Airline ESG targets favoring ultra-light photoluminescent floor paths | +0.3% | Global, concentrated in sustainability-focused carriers | Medium term (2-4 years) |

| Government stimulus for airport infrastructure upgrades post-COVID | +0.2% | North America, Europe, select APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated narrowbody fleet expansion among LCCs

LCCs across Asia-Pacific are driving unprecedented demand for narrowbody aircraft interior lighting systems through massive fleet expansion programs that prioritize operational efficiency and passenger density optimization. IndiGo operates 388 aircraft with orders for 260 A320neos, 390 A321neos, and 30 A350-900s, representing one of aviation's largest single-operator backlogs while transitioning from single-cabin to dual-class configurations requiring sophisticated zone-based lighting control.[1]Airways, “CEO Pieter Elbers on IndiGo’s Transformation,” airwaysmag.com This expansion pattern extends beyond India, with flyadeal targeting 100 aircraft by 2030 from its current 40 A320s, configured at 186-240 seats in high-density layouts that demand lightweight, energy-efficient LED systems.[2]PAX International, “Wizz Air Takes Delivery of First A321XLR,” pax-intl.com The LCC model's emphasis on rapid turnaround schedules creates demand for plug-and-play retrofit solutions that minimize aircraft downtime, with installation times as short as 12 hours for complete cabin lighting upgrades. Airlines prioritize systems that reduce maintenance complexity while supporting premium economy offerings within single-aisle aircraft, as demonstrated by IndiGo's "Stretch" product requiring differentiated lighting zones. The trend toward ultra-high-density configurations, with some LCCs achieving 240 seats in A321 aircraft, necessitates advanced lighting control systems that maintain passenger comfort despite reduced personal space allocations.

Retrofit wave toward LED mood-lighting for cabin refresh

Airlines embrace LED mood lighting retrofits as cost-effective alternatives to comprehensive cabin overhauls, delivering immediate passenger experience improvements without the capital intensity of full interior replacements that can cost USD 2-4 million per widebody aircraft. Delta's fleet-wide retrofit program incorporates phase-specific lighting schemes, including warm boarding illumination, candlelit dining ambiance, and circadian-aligned sleep transitions across diverse aircraft types to create consistent brand experiences. STG Aerospace's liTeMood system exemplifies this trend, offering plug-and-play LED replacements that achieve 30 kg weight savings per aircraft while reducing power consumption by 40% compared to fluorescent predecessors.[3]STG Aerospace, “ArkeFly Retrofits B737NG with liTeMood,” stgaerospace.com The retrofit approach enables airlines to modernize aging fleets cost-effectively, with Cobalt Spectrum installations requiring no wiring modifications and delivering 500,000-hour mean time between failures. Aircraft refurbishment specialists report booming demand as airlines seek environmental benefits and passenger appeal through cabin lighting upgrades rather than fleet replacement programs. The trend reflects airlines' strategic focus on maximizing existing asset utilization while delivering contemporary passenger experiences that compete with newer aircraft deliveries, particularly important as aircraft retirement schedules extend due to supply chain constraints.

Shift from fluorescent to energy-efficient, RoHS-compliant LEDs

Regulatory compliance requirements accelerate the transition from legacy fluorescent cabin lighting to RoHS-compliant LED systems that eliminate hazardous materials while delivering superior energy performance and operational reliability. The FAA's LED initiative, driven by the Energy Independence and Security Act of 2007, demonstrates regulatory momentum toward solid-state lighting adoption across aviation applications, with similar mandates emerging globally.[4]Federal Aviation Administration, “LED Initiative,” faa.gov LED systems offer dramatic efficiency improvements, with modern fixtures consuming 24-29 watts compared to 45 watts for equivalent halogen systems, while extending operational life from 1,000 to 50,000 hours and reducing maintenance intervals by up to 90%. Compliance frameworks increasingly emphasize mercury-free construction and end-of-life recyclability, positioning LED technology as the only viable long-term solution for commercial aviation interior lighting applications. Airlines report operational benefits beyond compliance, including eliminating ballast-related failures, improved color rendering that enhances passenger comfort during extended flights, and reduced heat generation that supports cabin climate control efficiency. The regulatory trajectory suggests fluorescent lighting will become obsolete within the forecast period, creating replacement demand across global commercial fleets estimated at over 25,000 aircraft requiring interior lighting upgrades.

IoT-enabled smart lights enabling predictive maintenance

Connected lighting systems are emerging as critical components of broader aircraft health management strategies, enabling predictive maintenance capabilities that reduce operational disruptions and maintenance costs. Astronics' Smart Aircraft System demonstrates IoT integration potential, using wireless sensors to monitor cabin environmental conditions and equipment status in real-time. Collins Aerospace's predictive analytics platform can reduce maintenance-driven delays by up to 30% for covered systems, benefiting lighting components from continuous health monitoring and failure prediction algorithms. Smart lighting systems enable remote diagnostics, automated failure reporting, and proactive component replacement scheduling that aligns with planned maintenance windows. The technology supports airlines' operational efficiency objectives by minimizing unscheduled maintenance events that disrupt flight schedules and passenger services. Integration with cabin management systems allows dynamic lighting control based on flight phases, passenger loads, and environmental conditions, optimizing energy consumption while maintaining service quality standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent widebody production backlog and delivery delays | -0.7% | Global, concentrated in major hub markets | Medium term (2-4 years) |

| Lengthy STC certification cycles for novel lighting systems | -0.4% | Global regulatory bottleneck | Long term (≥ 4 years) |

| Supply-chain tightness for high-CRI LED chips and driver ICs | -0.3% | Global semiconductor constraint | Short term (≤ 2 years) |

| Capital reallocation toward IFEC/connectivity over lighting | -0.2% | Global, prioritizing revenue-generating systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent widebody production backlog and delivery delays

Widebody aircraft production constraints significantly impact the commercial aircraft interior lighting market by delaying new aircraft deliveries and forcing airlines to extend existing fleet operations beyond planned retirement schedules, creating mixed demand effects across market segments. B777X program faces continued delays with first deliveries now pushed to 2026, nearly five years after first flight, due to thrust-link design issues affecting all test aircraft and requiring comprehensive redesign and re-testing protocols. The program's extended certification timeline, complicated by post-B737 MAX regulatory scrutiny and EASA redundancy requirements, affects over 500 aircraft on order from major carriers, including Emirates, Qatar Airways, and Lufthansa, representing billions in delayed lighting system installations. Production stabilization challenges extend beyond Boeing, with Airbus acknowledging supply chain constraints that prevent achieving targeted A320-family production rates of 50 aircraft monthly. At the same time, small cabin parts shortages, including lighting components and wiring harnesses, explicitly contribute to delivery delays. Airlines respond by extending existing aircraft operations through heavy maintenance visits and pursuing retrofit programs to maintain service standards, creating increased aftermarket demand that partially offsets delayed new aircraft installations. The constraint particularly affects premium cabin lighting segments where widebody aircraft command higher per-unit values and more sophisticated lighting system specifications than narrowbody alternatives.

Lengthy STC certification cycles for novel lighting systems

Supplemental Type Certificate (STC) processes for innovative lighting technologies create significant market entry barriers and delay technology deployment. Typically, certification timelines extend 9-12 months for standard modifications and potentially years for complex systems requiring extensive testing and validation protocols. The FAA's eight-step STC process requires comprehensive design substantiation, prototype installation, inspection protocols, and foreign validation procedures that substantially increase development costs and time-to-market for lighting innovations, particularly affecting smaller suppliers and startups. Interior lighting modifications face particular complexity due to multiple regulatory requirements covering emergency lighting, exit arrangements, placards, occupant protection, and flammability standards that must be validated across diverse aircraft configurations. Collins Aerospace processes approximately 200 STCs annually across 30+ airframe models, illustrating the certification workload required for widespread lighting system deployment and the competitive advantages of established suppliers with existing certification capabilities. The regulatory burden particularly affects innovative technologies like IoT-enabled smart lighting systems and circadian rhythm optimization features that require novel certification approaches and extensive human factors validation. International harmonization challenges compound delays, as EASA and other regulatory bodies often require separate validation processes that extend global market entry timelines for new lighting technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody dominance drives market evolution

Narrowbody aircraft command 50.92% market share in 2025, reflecting their central role in global aviation networks and the ongoing shift toward point-to-point connectivity models. The segment's dominance stems from airlines' preference for operational flexibility and route optimization capabilities that narrowbody platforms provide across diverse market conditions. Wizz Air's first A321XLR delivery exemplifies this trend, featuring Airbus Airspace cabin lighting with programmable settings for boarding, dining, relaxing, and sleeping phases across extended 4,700-nautical-mile routes.

While representing 49.08% of the market share, widebody aircraft demonstrate the fastest growth at 3.62% CAGR through 2031, driven by long-haul market recovery and airlines' focus on premium passenger experiences. The B777X program, despite delivery delays to 2026, incorporates sophisticated LED lighting systems designed to mimic destination time zones for jet lag mitigation. Qantas' Project Sunrise A350 installations feature 12 tailored lighting scenes developed through extensive testing at Airbus' Customer Definition Centre, demonstrating widebody platforms' capacity for advanced circadian lighting implementations. The widebody segment benefits from longer flight durations that justify sophisticated lighting investments and passengers' willingness to pay premiums for enhanced comfort features during extended travel periods.

By Light Type: Ambient systems lead market transformation

Ceiling and wall lights dominate with 43.35% market share in 2025, reflecting their fundamental role in establishing cabin ambiance and supporting airlines' branding strategies through customizable color schemes and intensity control. This segment encompasses the primary mood lighting systems that define passenger experience across all flight phases, from boarding through disembarkation. Reading lights emerge as the fastest-growing segment at 3.98% CAGR through 2031, driven by technological innovations integrating ambient and task lighting functions within single fixtures.

Schott's Jade Reading Light exemplifies this convergence trend, combining touch operation with no moving parts to reduce maintenance costs by up to 90% compared to traditional flex-and-stay designs. Signage lights benefit from regulatory requirements and safety compliance mandates, while lavatory lights increasingly incorporate smart features like occupancy detection and automated activation sequences. Floor-path lighting strips represent a specialized segment with growth potential through photoluminescent technologies that eliminate electrical requirements while providing emergency guidance capabilities. Lufthansa Technik's GuideU system demonstrates this approach, achieving 60% weight savings versus predecessors while maintaining maintenance-free operation through ambient light charging.

By Cabin Class: Premium segments drive innovation adoption

Economy class maintains 56.12% market share in 2025, reflecting its numerical dominance across global commercial aviation fleets and airlines' focus on maximizing passenger capacity within existing aircraft configurations. The segment's lighting requirements emphasize durability, energy efficiency, and standardized operation that minimizes crew training requirements and maintenance complexity. Premium economy emerges as the fastest-growing segment at 3.71% CAGR through 2031, driven by airlines' yield management strategies and passengers' willingness to pay incremental premiums for enhanced comfort features.

Business class installations demand sophisticated zone-based lighting control systems that enable individual passenger customization while maintaining overall cabin ambiance coordination. Qantas' A350 First Suites feature fully customizable lighting, allowing passengers to select preferred time zone settings throughout the flight, demonstrating premium segment expectations for personalized environmental control. First class represents the most technologically advanced segment, incorporating integrated lighting within privacy suites and entertainment systems that create immersive passenger environments. The premium segments serve as technology proving grounds for innovations that eventually migrate to economy class installations, creating a natural pathway for lighting system advancement across cabin configurations.

By End User: Aftermarket retrofits accelerate growth

OEM linefit installations command 51.55% market share in 2025, reflecting their integration advantage during aircraft manufacturing and airlines' preference for factory-installed systems that ensure warranty coverage and certification compliance. Original equipment installations benefit from streamlined integration with aircraft power systems, cabin management networks, and maintenance protocols established during initial certification processes. Aftermarket retrofits demonstrate faster growth at 3.97% CAGR through 2031, driven by airlines' need to modernize existing fleets without incurring new aircraft acquisition costs.

The retrofit segment benefits from technological advancement cycles that enable superior performance compared to original installations, with LED systems offering dramatic improvements over legacy fluorescent technologies. BermudAir's Cobalt Spectrum installation required only four technicians working a 12-hour shift to complete fleet-wide mood lighting upgrades, demonstrating retrofit efficiency advantages. Regulatory compliance requirements, particularly RoHS mandates for hazardous material elimination, create replacement demand that favors aftermarket suppliers capable of delivering compliant solutions for aging aircraft. The segment's growth trajectory reflects broader industry trends toward asset optimization and lifecycle extension strategies that maximize existing fleet utilization rather than pursuing capital-intensive fleet renewal programs.

Geography Analysis

North America maintains market leadership with a 38.55% share in 2025, supported by extensive retrofit programs and regulatory frameworks encouraging LED adoption across commercial fleets. The region benefits from established supply chains, certification expertise, and airlines' willingness to invest in passenger experience differentiation through advanced lighting systems. Delta's comprehensive fleet refresh program exemplifies North American market characteristics, incorporating sophisticated mood lighting across diverse aircraft types to create consistent brand experiences.

Asia-Pacific demonstrates the fastest growth at 4.69% CAGR through 2031, driven by unprecedented LCC expansion and new aircraft delivery schedules that favor modern lighting installations. IndiGo's transformation from single-cabin operations to dual-class configurations with business-class "Stretch" products illustrates regional market evolution toward premium service offerings that demand sophisticated lighting capabilities. The region's growth trajectory reflects broader economic development patterns, increasing passenger traffic, and airlines' focus on operational efficiency through modern fleet configurations. Air India's post-privatization transformation under Tata ownership emphasizes cabin product improvements through new aircraft deliveries and retrofit programs, supported by the carrier's 470-aircraft order in 2023. These markets benefit from hub-and-spoke network strategies that concentrate passenger traffic through major airports, creating demand for premium cabin experiences that justify sophisticated lighting investments.

Middle East and other emerging markets demonstrate strong growth potential through aggressive fleet modernization and capacity expansion programs pursued by regional carriers. Middle East carriers like Etihad pursue aggressive fleet modernization programs, with USD 7 billion investment plans targeting B777 retrofits and capacity expansion from 92 to 170 aircraft by 2030. European markets demonstrate steady growth through established carriers' fleet renewal programs and LCC expansion, with regulatory frameworks supporting environmental compliance through energy-efficient lighting mandates. Regional carriers' focus on long-haul operations and premium service differentiation drives the adoption of advanced circadian lighting systems and mood control technologies that enhance passenger comfort during extended flights.

Competitive Landscape

Competitive Landscape

The commercial aircraft interior lighting market exhibits moderate fragmentation across specialized suppliers, systems integrators, and aircraft manufacturers, with no single player commanding a dominant market position due to diverse customer requirements and certification complexities. Market concentration remains limited as airlines pursue multi-vendor strategies to ensure supply chain resilience and competitive pricing. At the same time, regulatory barriers create natural protection for established suppliers with existing STC portfolios. Collins Aerospace processes approximately 200 STCs annually across 30+ airframe models, demonstrating the certification workload required for market participation. Competition intensifies around retrofit solutions, where suppliers like STG Aerospace, Cobalt Spectrum, and Luminator Technology compete on installation simplicity, weight savings, and energy efficiency metrics that directly impact airline operational costs.

Strategic patterns emphasize plug-and-play retrofit capabilities that minimize aircraft downtime and certification complexity, with successful suppliers offering complete turnkey solutions, including installation support and maintenance training. White-space opportunities emerge in IoT-enabled predictive maintenance systems and circadian lighting technologies that address passenger wellness concerns during ultra-long-haul flights. Diehl Aviation's bionic-inspired ceiling structures achieve 30% weight reductions while integrating large-area LED floods, demonstrating how materials innovation creates competitive differentiation. Emerging disruptors focus on sustainable materials and circular economy principles, with suppliers like Gen Phoenix achieving 80% carbon emission reductions through recyclable seat cover materials that complement LED lighting efficiency gains. Technology deployment centers on semiconductor integration for smart lighting control, wireless connectivity for cabin management systems, and advanced materials supporting performance and environmental compliance requirements.

Commercial Aircraft Interior Lighting Industry Leaders

Safran SA

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Astronics Corporation

SCHOTT AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Satair and Collins Aerospace announced a four-year extension of their distribution agreement for cabin interior components. This renewed contract also encompasses lighting solutions.

- March 2025: Diehl Aviation showcased its state-of-the-art cabin illumination technologies at the AIX in Hamburg. These advancements, which include accent lighting and high-quality materials, aim to significantly enhance the passenger experience.

- June 2023: STG Aerospace announced the launch of the Curve, a new flexible cabin lighting product from STG Aerospace's universal lighting family. The Curve is intended for the business jet cabin market.

Global Commercial Aircraft Interior Lighting Market Report Scope

Cabin lighting systems create an atmosphere of comfortable illumination for passengers and crew members. The study includes lighting solutions for aircraft cabins. Premium economy class lighting is included within the economy class segment.

The commercial aircraft interior lighting market is segmented based on aircraft type, light type, cabin class, and geography. By aircraft type, the market is segmented into narrow-body, wide-body, and regional aircraft. By light type, the market is segmented into reading lights, ceiling and wall lights, signage lights, lavatory lights, and floor path lighting stripes. By cabin class, the market is classified as economy class, business class, and first class. The market sizing and forecasts have been provided in value in USD million.

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional jets |

| Reading Lights |

| Ceiling and Wall Lights |

| Signage Lights |

| Lavatory Lights |

| Floor-path Lighting Strips |

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

| OEM Linefit |

| Aftermarket/Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional jets | |||

| By Light Type | Reading Lights | ||

| Ceiling and Wall Lights | |||

| Signage Lights | |||

| Lavatory Lights | |||

| Floor-path Lighting Strips | |||

| By Cabin Class | First Class | ||

| Business Class | |||

| Premium Economy Class | |||

| Economy Class | |||

| By End User | OEM Linefit | ||

| Aftermarket/Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the commercial aircraft interior lighting market in 2026?

It is valued at USD 1.11 billion and is projected to reach USD 1.31 billion by 2031.

Which aircraft segment purchases the most lighting systems?

Narrowbody jets hold 50.92% of 2025 revenue due to rapid LCC fleet growth and dense route networks.

Why are airlines rushing to retrofit LEDs?

LED retrofits cut power use by 40%, lower maintenance, and meet emerging regulations that phase out mercury-based fluorescents.

What region grows fastest over the forecast period?

Asia-Pacific is forecasted to expand at a 4.69% CAGR through 2031, driven by record aircraft orders and rising passenger demand.

How do IoT features enhance cabin lighting?

Smart fixtures stream health data to predictive analytics platforms, reducing unscheduled maintenance and improving reliability.

What limits new technology adoption today?

Lengthy STC certification cycles and semiconductor shortages slow deployment of advanced lighting innovations.

Page last updated on: