Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

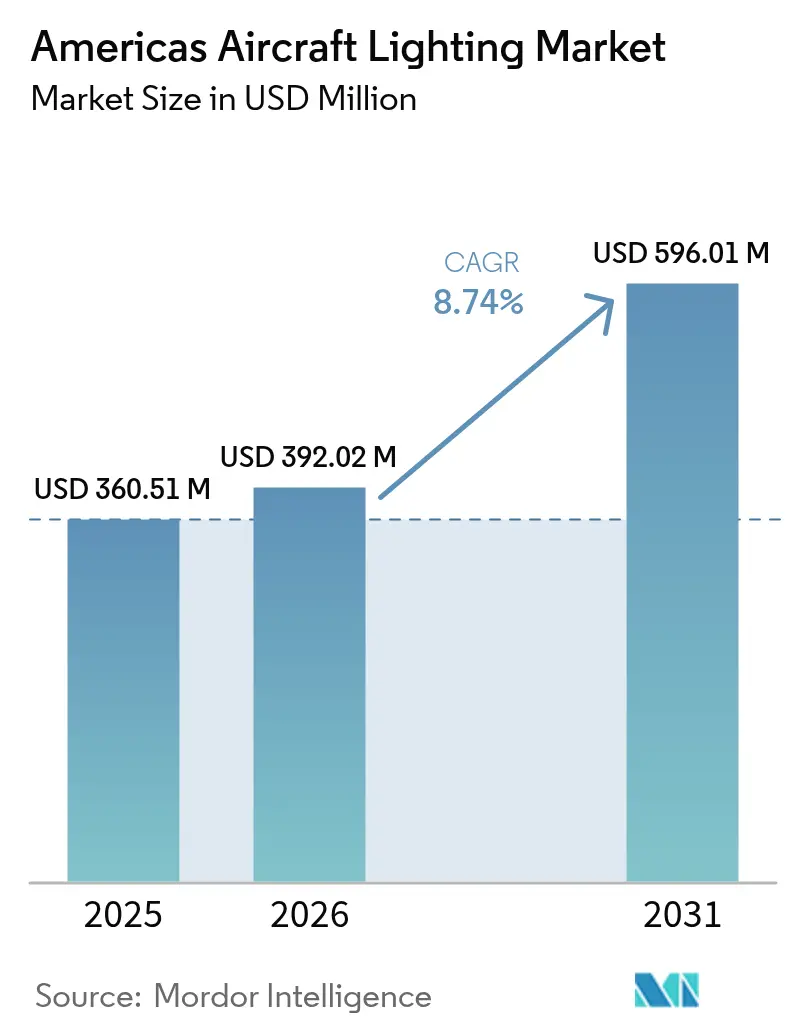

| Base Year Market Size (2025) | USD 360.51 Million |

| Market Size (2026) | USD 392.02 Million |

| Market Size (2031) | USD 596.01 Million |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Aircraft Lighting Market Analysis by Mordor Intelligence

Americas Aircraft Lighting Market size in 2026 is estimated at USD 392.02 million, growing from 2025 value of USD 360.51 million with 2031 projections showing USD 596.01 million, growing at 8.74% CAGR over 2026-2031.

Market Analysis

Rising fleet-modernization budgets, synchronized mercury-free regulations, and continued passenger-traffic recovery underpin this growth trajectory. Carriers prioritize LED retrofits that reduce power draw by 85% and cut recurring maintenance, while OEM deliveries stimulate linefit demand as Boeing, Airbus, and Embraer clear backlogs. North American dominance in aircraft production couples with Latin American narrowbody expansion, creating a dual-engine dynamic that anchors the Americas aircraft lighting market. Supply-chain pressure for qualified LED drivers and rare-earth phosphors presents near-term turbulence. However, accelerated FAA certification pathways now reduce approval cycles to 6-12 months, enabling quicker monetization of proven lighting platforms.

Key Report Takeaways

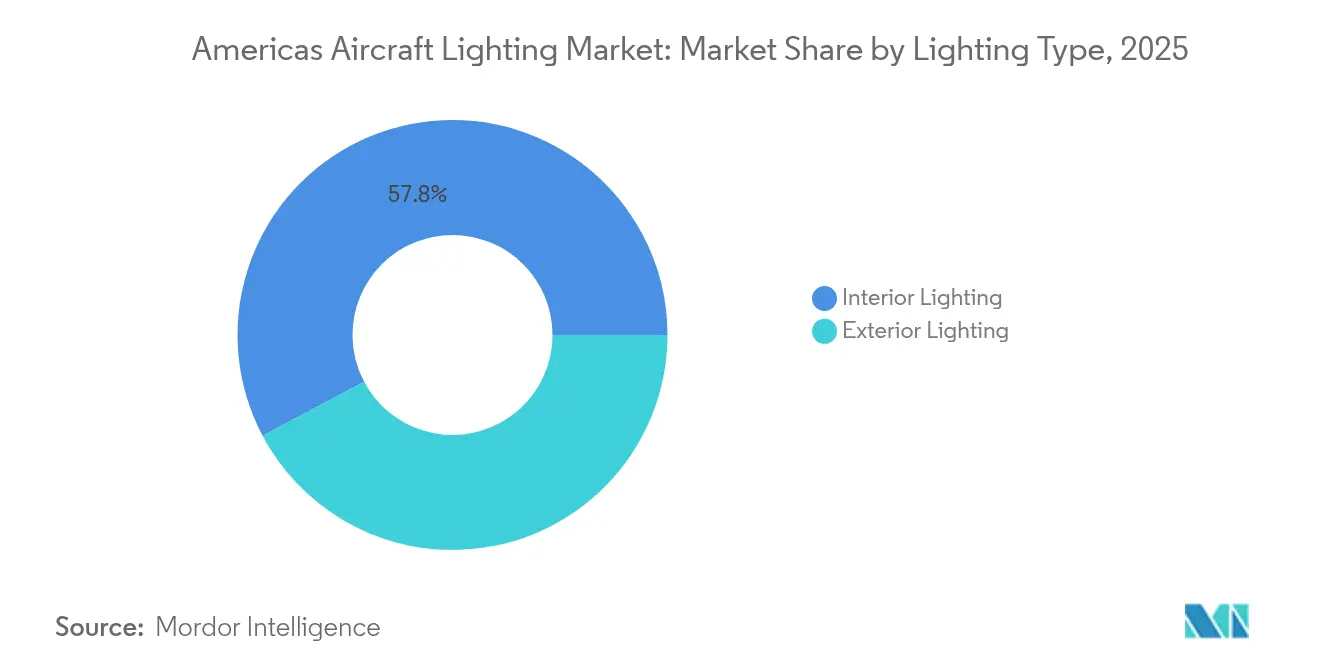

- By lighting type, interior lighting systems captured 57.76% of the Americas aircraft lighting market share in 2025; exterior lighting is projected to expand at a 7.12% CAGR through 2031.

- By aircraft type, narrowbody jets led the Americas aircraft lighting market, with 56.03% of the size in 2025, while business jets show the highest forecast CAGR, at 8.96% to 2031.

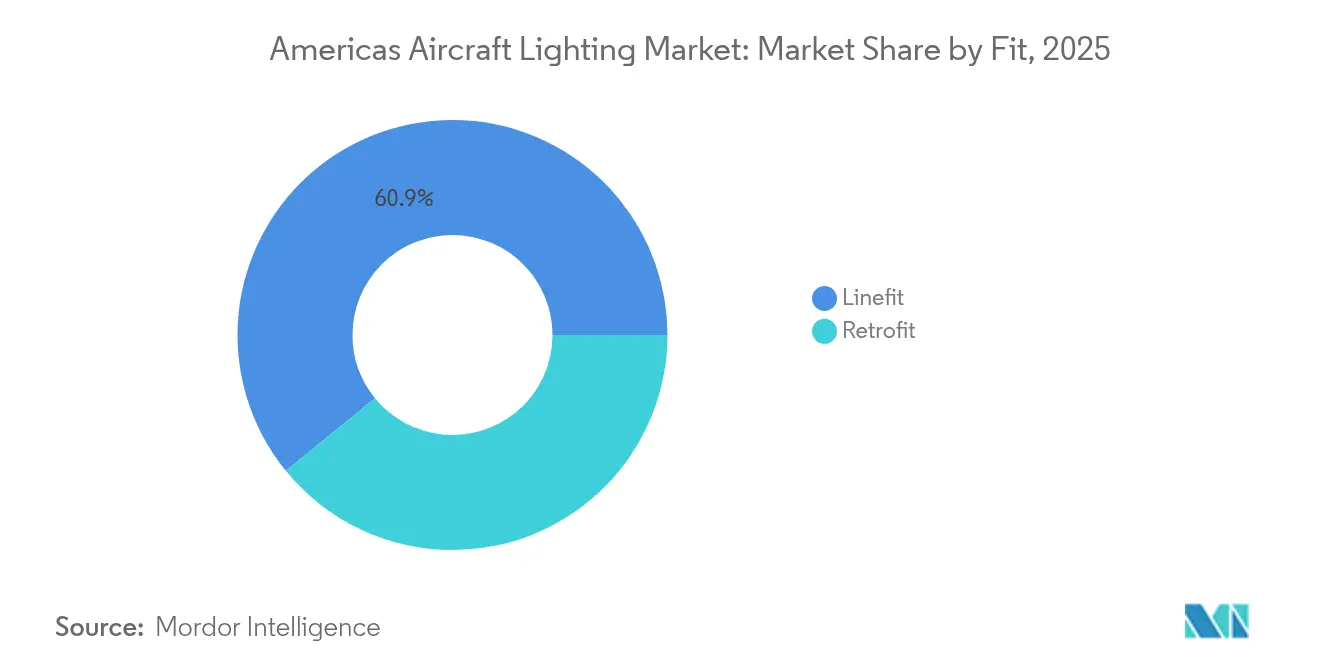

- By fit, linefit installations accounted for 60.88% of revenue in 2025; retrofit solutions advanced fastest, with a 7.26% CAGR through 2031.

- By technology, LED products dominated with 79.75% of America's aircraft lighting market share in 2025 and are growing at a 9.68% CAGR to 2031.

- By geography, the United States held 57.65% of regional revenue in 2025, whereas Brazil registered the fastest forecast CAGR of 8.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Americas Aircraft Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet-wide LED retrofit programs gaining regulatory push | +2.1% | North and Latin America | Medium term (2-4 years) |

| Airlines’ cabin revamp for premium passenger experience | +1.8% | United States and Brazil | Short term (≤ 2 years) |

| Surging narrowbody aircraft orders in Latin America | +1.5% | Mexico and Brazil | Medium term (2-4 years) |

| Airline ESG and sustainability targets accelerating shift to low-power, mercury-free lighting | +1.3% | Canada and United States | Long term (≥ 4 years) |

| Increasing adoption of mood-lighting and circadian systems | +1.0% | North America and premium Latin carriers | Medium term (2-4 years) |

| Integrated cockpit-display backlighting in next-gen avionic suites | +0.8% | OEM centers across region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fleet-wide LED retrofit programs gaining regulatory push

Transport Canada’s mercury-free deadline of December 31, 2025, aligns with the European Union’s (EU's) 2024 ban, eliminating route-based loopholes and compelling carriers to accelerate LED conversions.[1]Government of Canada, “Products Containing Mercury Regulations (SOR/2024-109),” tc.gc.ca Airlines benefit from 85% lower power draw, translating into measurable fuel savings on long-haul missions. Streamlined FAA TSO-C30c approvals now cut typical certification cycles from 24 months to under 12, allowing compliance programs to conclude before regulatory grace periods expire.[2]Federal Aviation Administration, “14 CFR 25.812 Emergency Lighting,” faa.gov Early adopters gain cost leadership and lower carbon footprints, strengthening ESG disclosures that resonate with investors and eco-conscious travelers.

Airlines’ cabin revamp for premium passenger experience

Delta’s 2024 interior refresh leveraged dynamic circadian lighting that modulates color temperature through all flight phases, improving arrival comfort and willingness to pay premium fares.[3]Delta Air Lines, “Delta Unveils Updated Cabin Interiors,” news.delta.com LED architecture enables scene changes via software rather than hardware swaps, supporting high aircraft utilization. Comparable upgrades in business aviation command 15-20% price premiums but yield demonstrable gains in charter rates and net promoter scores. Lighting synchronization with in-flight entertainment elevates ambience, making cabin illumination a revenue-generating amenity rather than a pure cost center. The trend reinforces high-margin demand for configurable LED systems across linefit and retrofit channels.

Surging narrowbody aircraft orders in Latin America

Copa Airlines committed to 6 B737-8 jets and LATAM ordered 10 B787s during 2024, underscoring a regional fleet-renewal cycle that doubles Latin America’s fleet by 2042. Daily utilization exceeding 10 hours accelerates lighting wear, boosting replacement demand. Mexican carriers’ pivot toward Embraer expands supplier opportunities across multiple platforms, while longer aircraft retention in Latin America sustains the aftermarket for LED retrofits. Diversified fleet profiles incentivize lighting vendors with multi-platform certification to penetrate burgeoning OEM lines and refurbishment programs.

Airline ESG and sustainability targets accelerating shift to low-power, mercury-free lighting

Carriers integrate lighting upgrades into net-zero roadmaps because verified LED deployments deliver quantifiable fuel and carbon savings, aligning with mandatory ESG reporting.[4]Collins Aerospace, “LED Lighting Systems,” collinsaerospace.com Procurement teams now require documented conflict-free sourcing of rare-earth materials and closed-loop manufacturing. Airlines marketing eco-friendly branding on eco-tourism routes use mercury-free cabins as proof points. Data-logging luminaires facilitate granular energy reporting, ensuring lighting sits within broader sustainability dashboards that track emissions from flight to ground operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain bottlenecks of qualified LED drivers | -1.2% | Region-wide, OEM heavy | Short term (≤ 2 years) |

| Certification costs and multi-year design-approval cycles | -0.8% | Primarily North America | Medium term (2-4 years) |

| Volatility in raw-material prices (rare-earth phosphors) | -0.7% | Region-wide, strongest where LED supply chains cluster | Medium term (2-4 years) |

| Cabin weight-saving mandates limiting power budgets | -0.6% | United States and Canada aviation regulators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-chain bottlenecks of qualified LED drivers

Wolfspeed’s silicon-carbide production delays magnified a scarcity of aerospace-grade drivers, stretching lead times to 52 weeks and forcing lighting OEMs to redesign around alternate chips. High-power exterior lights demand extreme thermal and EMI tolerances, narrowing the supplier pool. Airlines respond by stockpiling drivers, tying up working capital, and raising total installed costs, especially for regional operators with thinner balance sheets. Although capacity expansions are slated for 2026, intermittent shortages may crimp near-term installation volumes.

Certification costs and multi-year design-approval cycles

FAA and EASA approvals exceed USD 2 million per lighting suite and can span three years, discouraging small entrants and slowing disruptive innovation. With avionics life cycles shortening, a product may be near obsolescence by the time certification clears. Retrofit supplemental type certificates require extensive flight testing, adding further cost. Large tier-1 suppliers absorb these hurdles through diversified portfolios, widening the moat against emerging competitors and keeping pricing power concentrated among incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lighting Type: Interior systems maintain market leadership

Interior solutions provided 57.76% of 2025 revenue for the Americas aircraft lighting market, driven by mandatory exit-path illumination and value-added mood scenes. Airlines use programmable LEDs to align cabin ambience with brand colors and partner advertising, unlocking ancillary revenue and customer-experience gains. Longer refurbishment cycles, averaging 8-12 years, secure a predictable aftermarket stream that cushions OEM fluctuations.

Exterior lighting posts the 7.12% CAGR edge as carriers replace halogen strobes with LEDs that slash maintenance events by 90%. New anti-collision and navigation units meet stringent luminosity rules while consuming one-tenth the power, giving operators immediate payback.

By Aircraft Type: Narrowbody dominance meets business-jet upside

Narrowbody platforms, the backbone of regional and domestic routes, commanded 56.03% of the Americas aircraft lighting market share in 2025 as high daily cycles accelerate lamp wear. Widebodies gravitate toward multi-zone mood packages to differentiate premium cabins on long-haul corridors, ensuring high content per tail.

Business jets capture a 8.96% CAGR through 2031 as owners specify fully customizable color palettes, fiber-optic accents, and app-controlled scenes. Helicopter operators, from offshore energy to EMS, continue migrating to sealed-beam LEDs that withstand vibration and salt spray.

By Fit: Linefit reigns, retrofit gains speed

Linefit secured 60.88% of 2025 revenue thanks to Boeing, Airbus, and Embraer throughput. Still, retrofit is the growth pacesetter at 7.26% CAGR as carriers seek immediate fuel and maintenance savings without waiting for new deliveries. The STG liTeMood kit illustrates the retrofit promise, trimming 30 kg per B737 and recovering investment inside two years. Additionally, the demand for more fuel-efficient operations continues to drive innovation in retrofit solutions, enabling airlines to stay competitive in a challenging market. As environmental regulations tighten, these upgrades not only improve operational efficiency but also contribute to sustainability efforts within the aviation industry.

By Technology: LED supremacy deepens

LED units carried 79.75% of the Americas aircraft lighting market share in 2025 and will climb further as a 9.68% CAGR eclipses fluorescent holdouts. Honeywell’s LED FACL retrofit cuts power draw by 85% and stretches operating life to 50,000 hours, underscoring LED economics. Smart LED nodes now embed health-monitoring sensors, paving the way for predictive maintenance dashboards that integrate lighting into broader digital twin schemes. As the industry evolves, advancements in LED technology are expected to enhance efficiency and safety further, making air travel more sustainable.

Geography Analysis

The US remains the primary demand center, driven by large-scale renewal programs such as American Airlines' 260-unit order and an active general-aviation fleet exceeding 200,000 aircraft. OEM linefit contracts benefit from Boeing's production footprint, while retrofit providers leverage dense MRO clusters that streamline installation logistics. The US further influences certification standards through FAA leadership, giving domestic suppliers early adoption opportunities and export leverage across the Americas aircraft lighting market.

Canada's enforceable mercury-free lighting mandate, effective December 2025, accelerates LED penetration and sets a precedent for neighboring markets. Operators leverage transport-development grants to fund retrofits suited for harsh winter operations, driving demand for high-luminance and vibration-resistant assemblies. Bilateral regulatory harmonization with Brazil facilitates South America's technology transfer and supplier localization.

Brazil and Mexico jointly outpace the regional average, propelled by LATAM's Dreamliner acquisition and Copa's B737-8 deliveries. Domestic manufacturers, notably Embraer, cultivate local supply chains that welcome lighting co-production under offset frameworks, enhancing regional value retention. Argentina, Colombia, and the wider Caribbean sustain steady retrofit demand as tourism rebounds, though macro-economic fluctuations may shift installation timelines. The Americas aircraft lighting market finds geographic growth nodes distributed across North and Latin America, balancing mature replacement cycles with emerging fleet expansions.

Competitive Landscape

Competitive Landscape

Tier-1 suppliers Collins Aerospace, Honeywell, and Safran dominate through vertically integrated portfolios covering interior, exterior, and cockpit lighting. Their regulatory rapport and certification resources discourage smaller entrants, especially given multi-million-dollar approval costs. Honeywell’s 2025 AI-driven avionics collaboration with NXP embeds advanced back-lighting, locking future wins across numerous flight-deck programs.

Safran’s USD 1.8 billion acquisition of Collins’ actuation unit in July 2025 expands systems integration leverage, allowing bundled lighting, flight controls, and power distribution bids that appeal to OEM cost-reduction mandates. Diehl Aviation champions accessibility-oriented lighting, winning awards for Space³ concepts that guide visually impaired passengers through illuminated pathways, indicating niche differentiation potential.

Disruptive threats come from specialized LED chipmakers targeting aerospace with automotive-grade economies of scale. Yet, stringent DO-160 environmental testing and protracted FAA oversight limit immediate penetration. Smart-lighting incumbents continue investing in sensor fusion and data analytics, embedding proprietary protocols that lock customers into long-term service contracts and solidify competitive moats within the Americas aircraft lighting market.

Americas Aircraft Lighting Industry Leaders

Honeywell International Inc.

Astronics Corporation

Collins Aerospace (RTX Corporation)

Safran SA

Diehl Stiftung & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Satair and Collins Aerospace announced a four-year extension of their distribution agreement for cabin interior components. This renewed contract also encompasses lighting solutions.

- March 2025: Diehl Aviation showcased its state-of-the-art cabin illumination technologies at the AIX in Hamburg. These advancements, which include accent lighting and high-quality materials, aim to enhance the passenger experience significantly.

- June 2023: STG Aerospace announced the launch of the Curve, a new flexible cabin lighting product from STG Aerospace's universal lighting family. The Curve is intended for the business jet cabin market.

Americas Aircraft Lighting Market Report Scope

Aircraft lighting systems provide exterior and interior illumination. Exterior lights illuminate operations such as night landing, inspection of icing conditions, and midair collision safety. Interior lights illuminate instrumentation, cockpit, cabin, and other areas occupied by crew members and passengers. Some specific lights, including indicator and warning lights, indicate the working status of equipment.

The Americas aircraft lighting market is segmented based on lighting type, application, and geography. By lighting type, the market is segmented into exterior light and interior light. By application, the market is segmented into commercial aircraft and general aviation aircraft. The report also offers the market size and forecasts for five countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD).

By Lighting Type

| Interior Lighting | Cabin Lighting |

| Cockpit Lighting | |

| Emergency and Exit Lighting | |

| Cargo/Baggage Lighting | |

| Exterior Lighting | Navigation and Position Lights |

| Landing and Taxi Lights | |

| Anti-Collision and Strobe Lights | |

| Logo and Wing Inspection Lights |

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Business Jets |

| Helicopters |

| Unmanned Aerial Vehicles (UAVs) |

By Fit

| Linefit |

| Retrofit |

By Technology

| Light-Emitting Diode (LED) |

| Fluorescent |

| Incandescent/Halogen |

By Geography

| United States |

| Canada |

| Mexico |

| Brazil |

| Argentina |

| Rest of Americas |

| By Lighting Type | Interior Lighting | Cabin Lighting |

| Cockpit Lighting | ||

| Emergency and Exit Lighting | ||

| Cargo/Baggage Lighting | ||

| Exterior Lighting | Navigation and Position Lights | |

| Landing and Taxi Lights | ||

| Anti-Collision and Strobe Lights | ||

| Logo and Wing Inspection Lights | ||

| By Aircraft Type | Narrowbody Aircraft | |

| Widebody Aircraft | ||

| Regional Jets | ||

| Business Jets | ||

| Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| By Fit | Linefit | |

| Retrofit | ||

| By Technology | Light-Emitting Diode (LED) | |

| Fluorescent | ||

| Incandescent/Halogen | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Brazil | ||

| Argentina | ||

| Rest of Americas | ||

Key Questions Answered in the Report

What is the projected value of the Americas aircraft lighting market by 2031?

The Americas aircraft lighting market is forecasted to reach USD 596.01 million by 2031, expanding at a 8.74% CAGR.

Which technology dominates sales?

LED solutions held 79.75% market share in 2025 and continue expanding due to efficiency and regulatory incentives.

Why are retrofit programs accelerating?

Mercury-free mandates effective in 2025 and compressed FAA approvals make LED conversions both mandatory and cost-effective.

Which countries show the fastest growth rates?

Brazil shows the highest CAGR at 8.05% through 2031 on large narrowbody orders and domestic manufacturing support.

What is the biggest supply-chain challenge?

Shortages of aerospace-grade LED drivers, driven by limited silicon-carbide capacity, extend delivery timelines.

How does lighting support airline ESG goals?

LEDs cut power draw up to 85%, lowering fuel burn and carbon emissions while eliminating hazardous mercury content.

Page last updated on: