Market Overview

| Study Period | 2018 - 2031 |

|---|---|

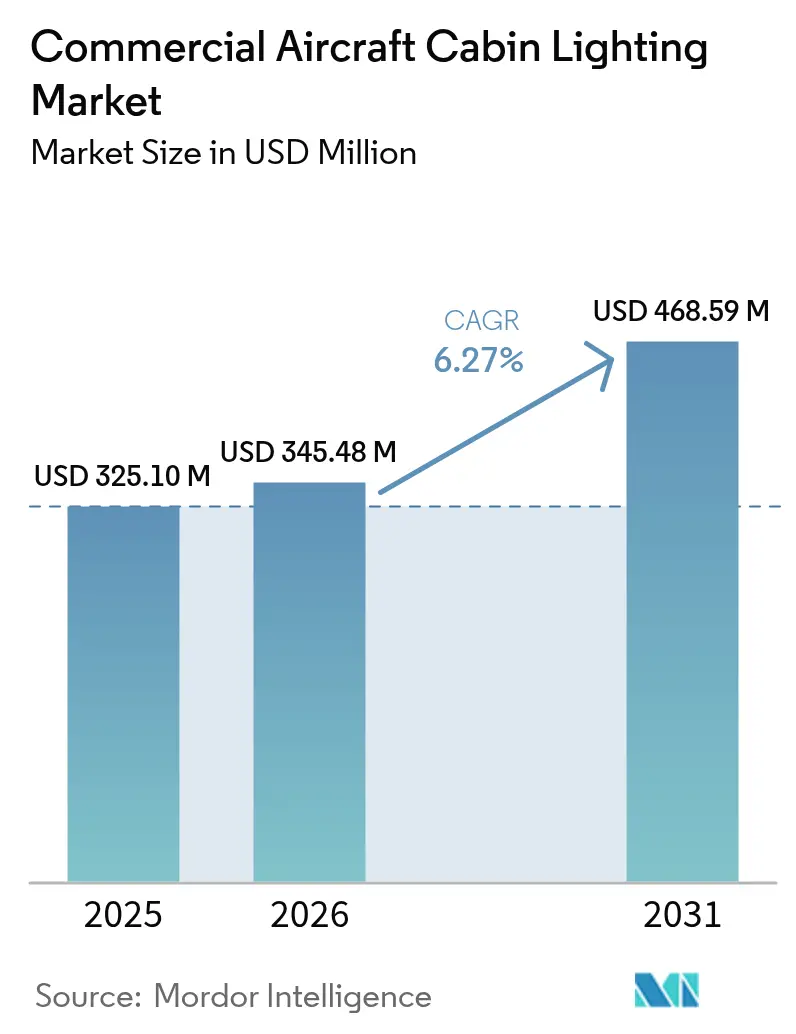

| Market Size (2026) | USD 345.48 Million |

| Market Size (2031) | USD 468.59 Million |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

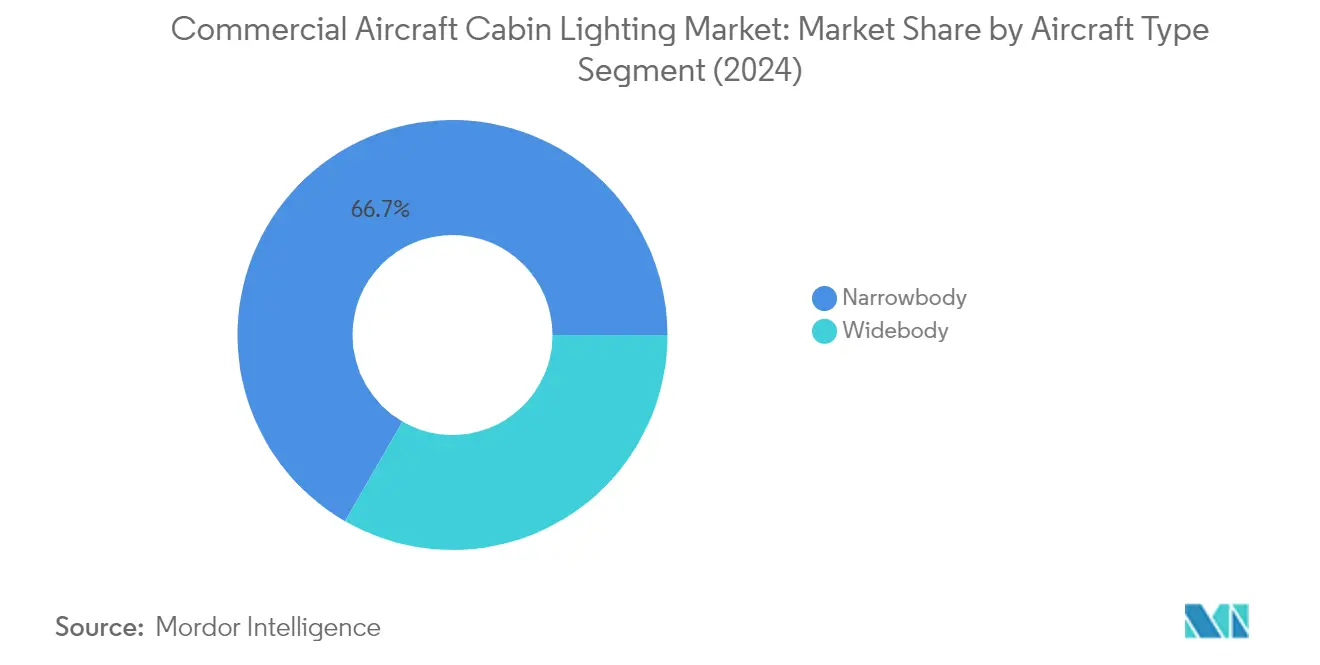

| Fastest Growing Market | Narrowbody |

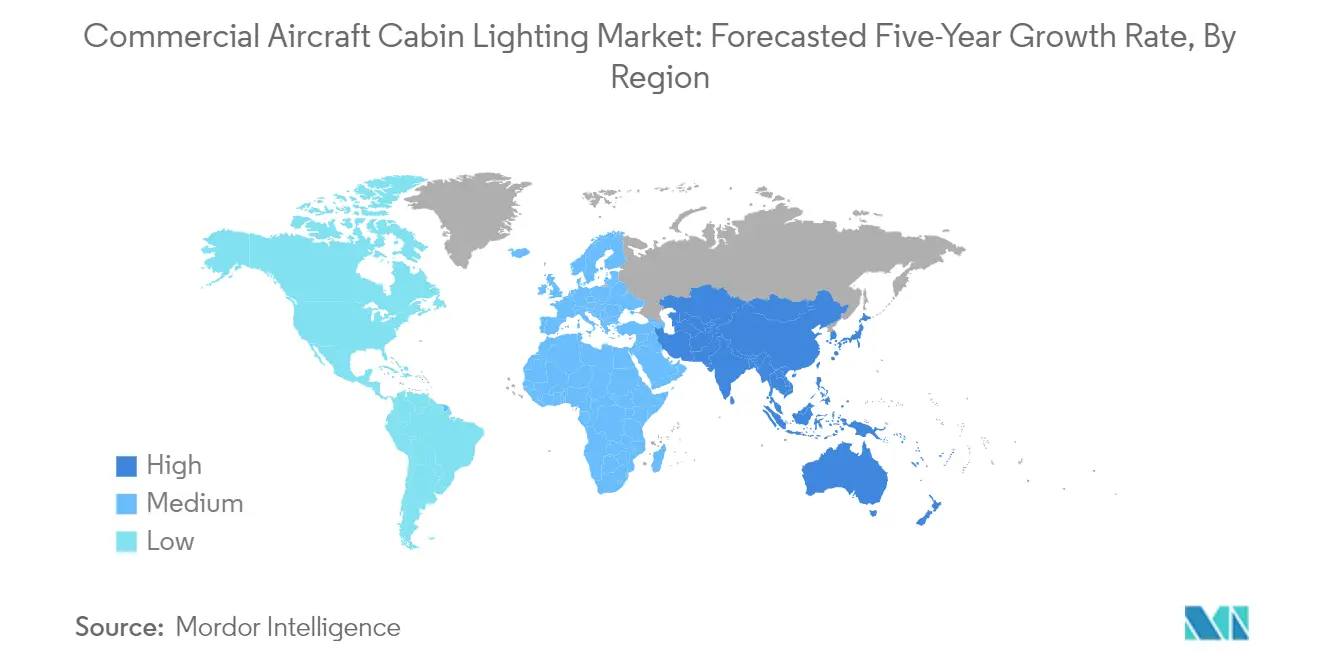

| Largest Market | Asia-Pacific |

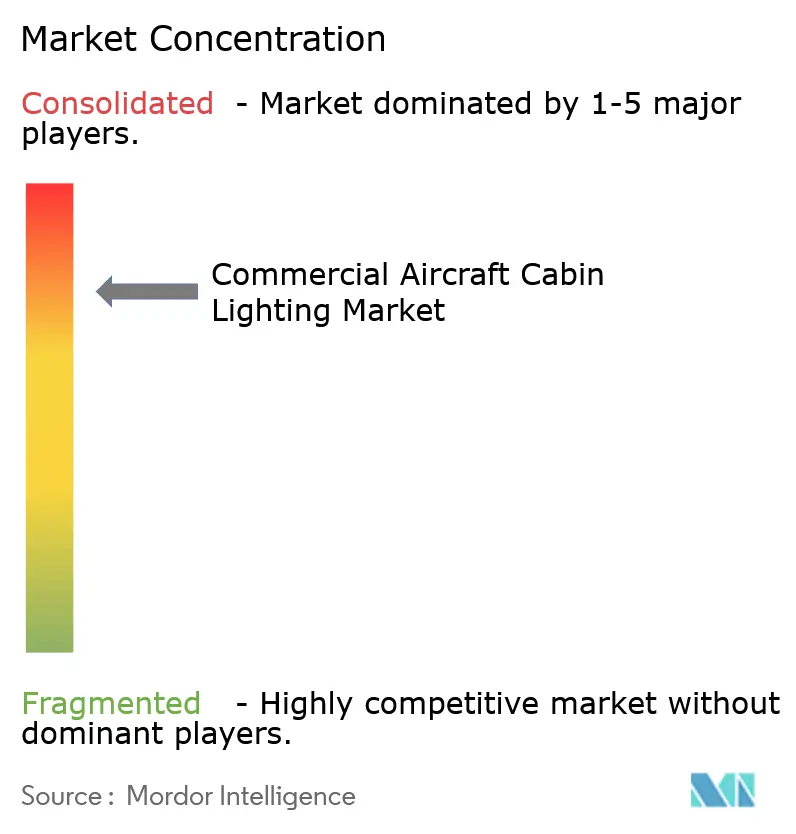

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Cabin Lighting Market Analysis by Mordor Intelligence

Commercial Aircraft Cabin Lighting Market size in 2026 is estimated at USD 345.48 million, growing from 2025 value of USD 325.10 million with 2031 projections showing USD 468.59 million, growing at 6.27% CAGR over 2026-2031.

The commercial aircraft cabin lighting market is characterized by significant consolidation, with the top five companies, Collins Aerospace, Diehl Aviation GmbH, Schott, Astronics, and Luminator Technology Group, collectively accounting for 83.5% of the market share in 2022. This concentration has fostered increased investment in research and development, resulting in rapid technological advancements in aircraft lighting solutions. The industry has witnessed a fundamental shift from traditional lighting systems to more sophisticated aircraft LED lighting solutions, driven by airlines' focus on enhancing passenger experience while reducing operational costs. The consolidated nature of the market has also enabled the standardization of aircraft lighting technologies across different aircraft platforms, facilitating easier integration and maintenance.

A significant transformation is underway in airplane cabin lighting technology, with airlines increasingly adopting LED mood lighting systems that offer superior efficiency and functionality compared to traditional incandescent bulbs. These advanced lighting systems are approximately 40% lighter than conventional options and provide energy savings while offering enhanced control over cabin ambiance. The industry has seen widespread adoption of human-centric lighting solutions, exemplified by Lufthansa's implementation of a specially programmed, flexible lighting system in its new Airbus A320neo fleet, featuring 24 variants of lighting designed to simulate natural ambient light and enhance passenger comfort.

Major airlines are undertaking comprehensive fleet modernization initiatives, incorporating advanced aircraft interior lighting technologies as a core component of their cabin enhancement strategies. United Airlines has placed an order for 270 narrowbody aircraft equipped with LED mood lighting, while Etihad Airways has announced plans to install LED mood lighting in its 15 new A350-1000 aircraft. These modernization efforts extend beyond mere lighting upgrades, encompassing complete cabin interior renovations that prioritize passenger comfort and experience. The industry is witnessing a trend toward customizable lighting scenarios that can be adjusted based on flight phases and time zones to reduce jet lag and enhance passenger well-being.

Looking ahead, the industry is poised for significant expansion with approximately 13,812 aircraft expected to be delivered between 2023 and 2030. This substantial fleet expansion is driving innovation in cabin lighting solutions, with manufacturers developing increasingly sophisticated systems that integrate with other cabin management functions. The narrowbody aircraft segment, which accounted for 83% of overall deliveries during 2017-2022, continues to dominate new aircraft orders, influencing the development of lighting solutions specifically optimized for single-aisle aircraft configurations. The industry is moving toward fully integrated aircraft lighting systems that can be controlled through touchscreen panels and automated programs, offering airlines greater flexibility in creating customized lighting environments for different routes and times of day.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Cabin Lighting Market Trends and Insights

The aviation industry's growth is fueled by the recovery of air travel and the high volume of aircraft orders placed by various airlines

- Boeing was impacted by the ongoing political tensions between China and the United States, and it plans to remarket certain 737MAX jets earmarked for Chinese customers. Boeing is facing a challenging situation as Chinese airlines are no longer ordering its jets. The Boeing delivery center in Zhoushan, China, is ready and expected to resume delivery of 737MAX aircraft. The Zhoushan plant can accommodate 100 aircraft annually.

- Airbus accumulated 1,044 net new orders (1,080 gross orders), compared to 259 net new orders (442 gross orders) in the first half of 2022. In 2022, Airbus booked 820 net new orders (1,078 gross orders), surpassing both gross orders and net new orders in 2021. In 2022, Airbus won the orders crown for the fourth consecutive year by a fairly slim margin of 46 aircraft compared to Boeing. In 2021, Airbus booked a total of 771 gross orders and received 264 cancellations, for a total of 507 net new orders. In June 2023, Airbus booked orders for a whopping 902 aircraft for 12 different customers and reported two A321neo cancellations, for a total of 900 net new orders.

- Boeing accumulated 415 net new orders (527 gross orders), compared to 186 net new orders (286 gross orders) in the first six months of the previous year. In 2022, Boeing booked 774 net new orders (935 gross orders), up from 479 net new orders (909 gross orders) in 2021. As of June 2023, Boeing booked orders from nine customers for a total of 304 jets (gross orders). However, the company also reported 16 777X cancellations, resulting in 288 net new orders.

An increase in international passenger traffic post the COVID-19 pandemic is driving market demand

- As cross-border travel was progressively restored in 2022 post the COVID-19 pandemic, the carriers in Asia-Pacific raced to increase their flights to meet runaway demand, stimulated by people's desire to travel and cash in on savings accumulated in the two years of isolation. As a result, in 2022, the air passenger traffic in the region recovered more rapidly from the pandemic than in the other regions. For instance, in 2022, air passenger traffic in the whole of Asia-Pacific was recorded at 1.9 billion, a growth of 6% compared to 2021 and 151% compared to 2020. Airline companies in the region are implementing fleet expansion plans to cater to the growing air passenger traffic in the major countries. China, India, Japan, and Indonesia accounted for 70% of the total air passenger traffic in the region, generating higher demand for new aircraft compared to other Asia-Pacific countries.

- Airlines in Asia-Pacific also witnessed a good recovery in international air passenger markets as travel demand continued to fuel growth despite increasingly challenging global economic conditions. For instance, in August 2022, the region recorded 13.1 million international air passenger traffic, an 836% increase compared to August 2021, when it was recorded at 1.4 million. The healthy growth in international passenger traffic in the first eight months of the year showed strong travel demand from business and leisure consumers. The rapid increase in air passenger traffic in the region is expected to drive the air transport industry in the future.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

Segment Analysis

Narrowbody Segment in Commercial Aircraft Cabin Lighting Market

The narrowbody segment dominates the commercial aircraft cabin lighting market, commanding approximately 66.40% of the total market share in 2025. This segment's prominence is driven by the increasing utilization of narrowbody aircraft on long-haul routes exceeding 6-7 hours, prompting airlines to focus on advanced aircraft lighting solutions that enhance the passenger experience. Major airline companies globally are implementing sophisticated lighting technologies, including LED systems that provide improved flexibility and control. The adoption of mood-based lighting in narrowbody aircraft, particularly in models like the A321 XLR, has become increasingly prevalent. Airlines are actively replacing traditional lighting systems with aircraft LED lighting solutions that offer enhanced cabin ambiance for various flight phases, including boarding, meals, sleeping, and waking. The segment's growth is further supported by substantial aircraft backlogs, with approximately 11,480 narrowbody aircraft expected to be delivered between 2023 and 2030, indicating strong future demand for cabin lighting solutions.

Widebody Segment in Commercial Aircraft Cabin Lighting Market

The widebody segment plays a crucial role in the commercial aircraft cabin lighting market, particularly on long-haul routes exceeding 6-7 hours. Airlines operating widebody aircraft are increasingly focusing on advanced cabin lighting products to provide a superior customer experience while simultaneously reducing fuel consumption, power usage, and maintenance costs. The segment has witnessed significant technological advancement with the implementation of color-changing mood lights and ceiling lights, replacing traditional bulky lighting systems with lightweight LED alternatives. Major airlines are incorporating sophisticated LED mood lighting systems in their widebody fleets to enhance passenger experience and minimize jetlag effects. These lighting systems are being designed to optimize the cabin environment according to flight phases, demonstrating the segment's commitment to passenger comfort and operational efficiency. The integration of programmable LED lighting systems in widebody aircraft has become a standard feature, particularly in new deliveries and retrofit programs, showcasing the segment's evolution towards more sophisticated aircraft interior lighting solutions.

Geography Analysis

The Asia-Pacific region represents a dynamic market for the aircraft cabin lighting market, driven by rapid aviation sector growth and an increasing focus on passenger experience. Countries like China, India, Indonesia, Japan, Singapore, and South Korea are making significant investments in modernizing their aircraft fleets with advanced lighting solutions. Airlines across the region are increasingly adopting LED lighting for aircraft systems and mood lighting technologies to enhance passenger comfort and reduce operational costs. The region's aviation market is characterized by a mix of established carriers and emerging low-cost airlines, all contributing to the growing demand for innovative cabin lighting solutions for airplanes.

China dominates the Asia-Pacific commercial aircraft cabin lighting market, holding approximately 29.70% of the regional market share in 2025. The country's aviation sector is experiencing substantial growth, supported by strong domestic travel demand and fleet expansion programs by major carriers. Chinese airlines are increasingly focusing on incorporating advanced LED lighting systems in their aircraft to enhance passenger experience and reduce maintenance costs. The country's aviation infrastructure development and the growing preference for modern aircraft with sophisticated cabin interiors continue to drive market growth. Major Chinese carriers are implementing fleet modernization programs with a particular emphasis on narrowbody aircraft equipped with state-of-the-art lighting systems.

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 10.6% from 2025 to 2031. The country's aviation sector is witnessing rapid expansion, driven by increasing air travel demand and fleet modernization initiatives by both full-service and low-cost carriers. Indian airlines are actively investing in advanced cabin lighting technologies, particularly focusing on LED systems and mood lighting capabilities. The market is benefiting from the growing trend of aircraft retrofitting programs and new aircraft deliveries, with airlines prioritizing enhanced passenger comfort through modern lighting solutions. The country's aviation sector is seeing significant investments in cabin interior improvements, with lighting playing a crucial role in overall passenger experience enhancement.

Competitive Landscape

Top Companies in Commercial Aircraft Cabin Lighting Market

The commercial aircraft cabin lighting market is characterized by continuous product innovation and strategic developments among key players like Collins Aerospace, Diehl Aviation, SCHOTT, Astronics, and Luminator Technology Group. Companies are focusing on developing advanced LED lighting solutions with enhanced efficiency, reliability, and customization capabilities to meet the evolving needs of airlines. The industry has witnessed significant investments in research and development of mood lighting systems, human-centric lighting solutions, and energy-efficient technologies. Operational agility is demonstrated through the establishment of global production facilities and service networks, particularly in high-growth regions such as the Asia-Pacific and the Middle East. Strategic moves predominantly involve agreements with aircraft manufacturers, product development initiatives, and merger and acquisition activities to strengthen market positions and expand product portfolios.

Consolidated Market with Strong OEM Relationships

The aircraft lighting market exhibits a highly consolidated structure, with major aerospace conglomerates and specialized lighting solution providers dominating the landscape. These established players have built strong relationships with aircraft manufacturers and airlines through years of collaboration and proven product reliability. The market's consolidation is further reinforced by high entry barriers, including stringent certification requirements, substantial investment needs, and the importance of maintaining a long-term track record in the aviation industry. Recent years have witnessed significant merger and acquisition activities, exemplified by strategic moves like Safran's acquisition of Zodiac Aerospace and the integration of various lighting specialists into larger aerospace groups.

The competitive dynamics are shaped by the presence of both diversified aerospace corporations that offer comprehensive aircraft interior lighting solutions and specialized lighting manufacturers focusing exclusively on aviation lighting systems. These companies compete through different strategies, with larger conglomerates leveraging their broad product portfolios and established customer relationships, while specialists emphasize technological innovation and customized solutions. The market also sees collaboration between major players and regional partners to enhance local presence and service capabilities, particularly in emerging aviation markets.

Innovation and Customer Relations Drive Success

Success in the aircraft lighting market increasingly depends on companies' ability to innovate while maintaining strong customer relationships and operational efficiency. Incumbent players must continue to invest in next-generation lighting technologies, particularly in areas such as mood lighting, energy efficiency, and integration with broader cabin management systems. The development of customizable solutions that allow airlines to differentiate their passenger experience while maintaining cost-effectiveness is becoming crucial. Companies also need to strengthen their aftermarket service capabilities and maintain close relationships with both aircraft manufacturers and airlines to secure long-term contracts and repeat business.

For contenders looking to gain market share, focusing on specific market segments or innovative technologies presents the most viable path forward. This includes developing specialized solutions for particular aircraft types or cabin classes, or introducing breakthrough technologies that address specific airline pain points. Building strong relationships with emerging airlines and aircraft manufacturers in growing markets, particularly in the Asia-Pacific and Middle East regions, presents significant opportunities. Success also requires establishing robust supply chain networks and obtaining necessary certifications while maintaining competitive pricing strategies. The increasing focus on sustainability and passenger experience creates opportunities for companies that can deliver innovative, energy-efficient lighting solutions that enhance the overall flying experience.

Commercial Aircraft Cabin Lighting Industry Leaders

Astronics Corporation

Collins Aerospace

Diehl Aerospace GmbH

Luminator Technology Group

SCHOTT Technical Glass Solutions GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2022: Collins Aerospace launched its Hypergamut™ Lighting System which is scheduled for entry into service in early 2024.

- February 2021: Diehl Aviation has secured a contract extension from Boeing for the delivery of the interior lighting system for the Boeing 787 Dreamliner.

Global Commercial Aircraft Cabin Lighting Market Report Scope

Narrowbody, Widebody are covered as segments by Aircraft Type. Asia-Pacific, Europe, Middle East, North America are covered as segments by Region.Aircraft Type

| Narrowbody |

| Widebody |

Region

| Asia-Pacific | By Country | China |

| India | ||

| Indonesia | ||

| Japan | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Europe | By Country | France |

| Germany | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Country | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| North America | By Country | Canada |

| United States | ||

| Rest of North America | ||

| Rest of World |

| Aircraft Type | Narrowbody | ||

| Widebody | |||

| Region | Asia-Pacific | By Country | China |

| India | |||

| Indonesia | |||

| Japan | |||

| Singapore | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Europe | By Country | France | |

| Germany | |||

| Spain | |||

| Turkey | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Country | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| North America | By Country | Canada | |

| United States | |||

| Rest of North America | |||

| Rest of World | |||

Market Definition

- Product Type - The interior lights of aircraft which provide illumination for instruments, cabins, and other sections that are occupied by passengers are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms