Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

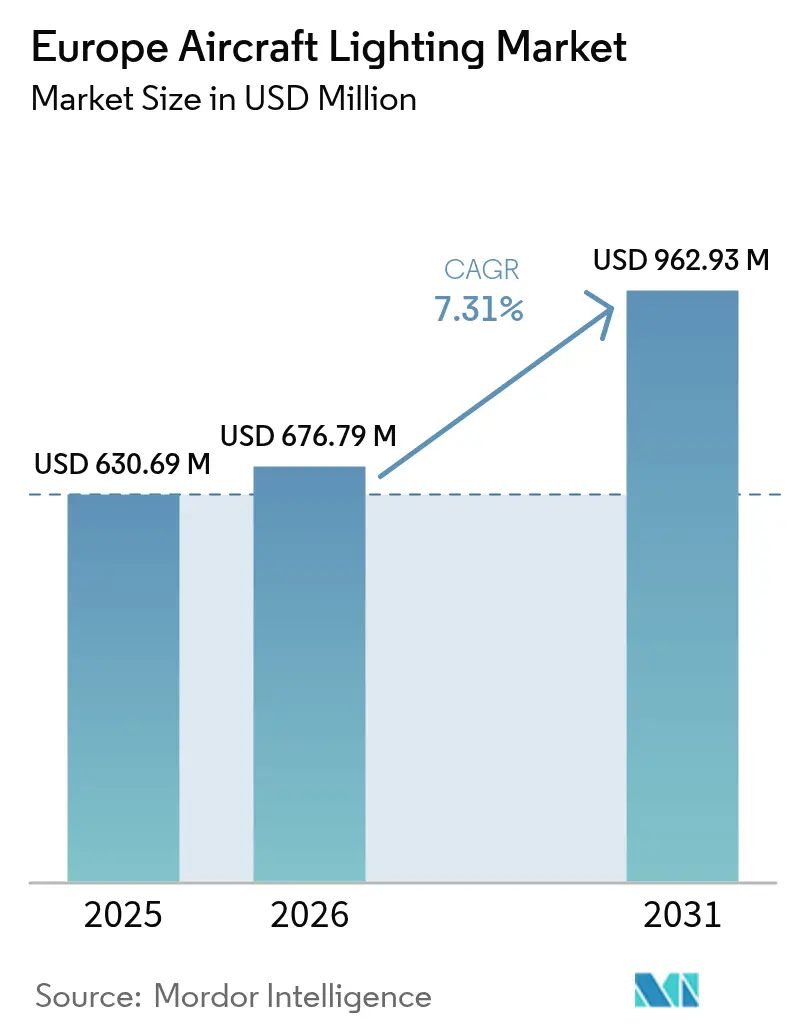

| Base Year Market Size (2025) | USD 630.69 Million |

| Market Size (2026) | USD 676.79 Million |

| Market Size (2031) | USD 962.93 Million |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aircraft Lighting Market Analysis by Mordor Intelligence

Market Analysis

The European aircraft lighting market size was valued at USD 630.69 million in 2025 and estimated to grow from USD 676.79 million in 2026 to reach USD 962.93 million by 2031, at a CAGR of 7.31% during the forecast period (2026-2031). Fleet modernization programs, rapid LED adoption, and EASA-driven safety regulations continue to anchor growth. Airlines view cabin lighting as an essential brand asset that supports passenger well-being on long-haul routes, while OEMs and Tier-1 suppliers work on smart, sensor-rich solutions that cut maintenance events. Germany’s large aerospace manufacturing base sustains robust original-equipment demand, and Spain’s rising regional jet activity fuels retrofit opportunities. LED systems already dominate the installed base and offer up to 75% lower energy draw than legacy solutions, making them the default choice for both commercial and military operators. Moderate consolidation lets major vendors capture integration synergies, yet niche players still find room in eVTOL and specialty-exterior lighting niches.

Key Report Takeaways

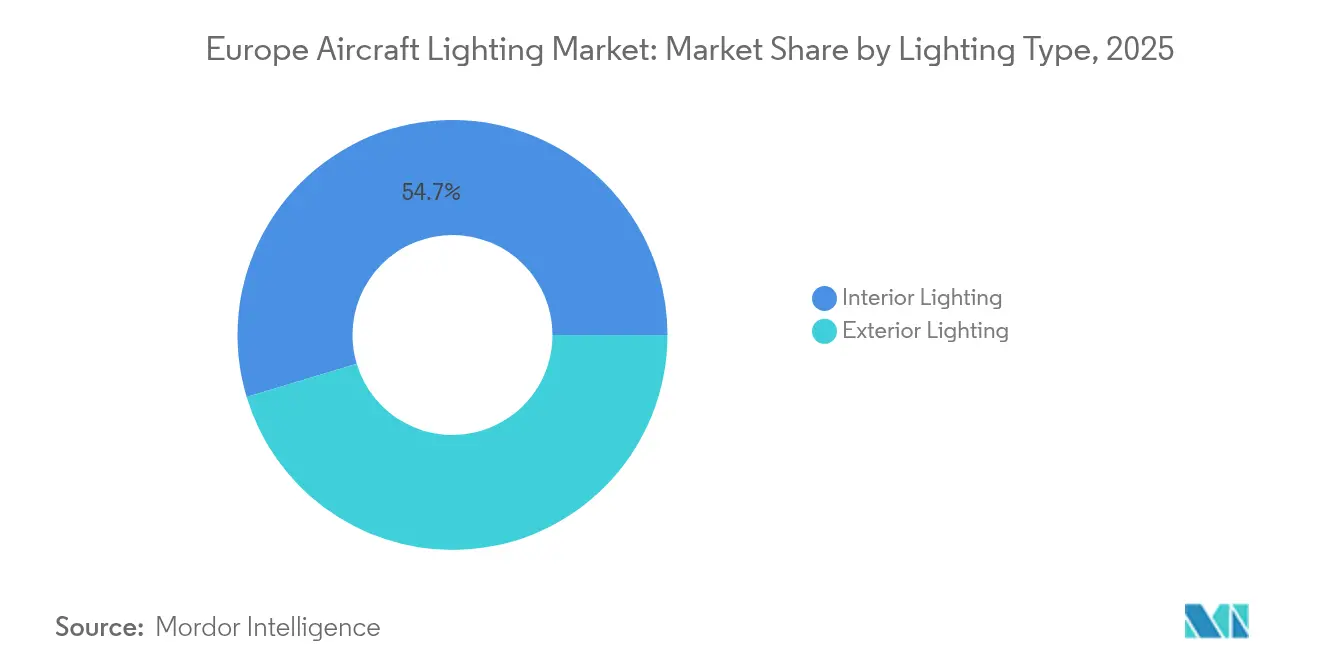

- By lighting type, interior lighting captured 54.65% of the European aircraft lighting market share in 2025; exterior lighting is projected to grow at an 8.05% CAGR through 2031.

- By aircraft type, narrowbody platforms held 53.12% of the European aircraft lighting market size in 2025, while business jets are advancing at a 6.31% CAGR to 2031.

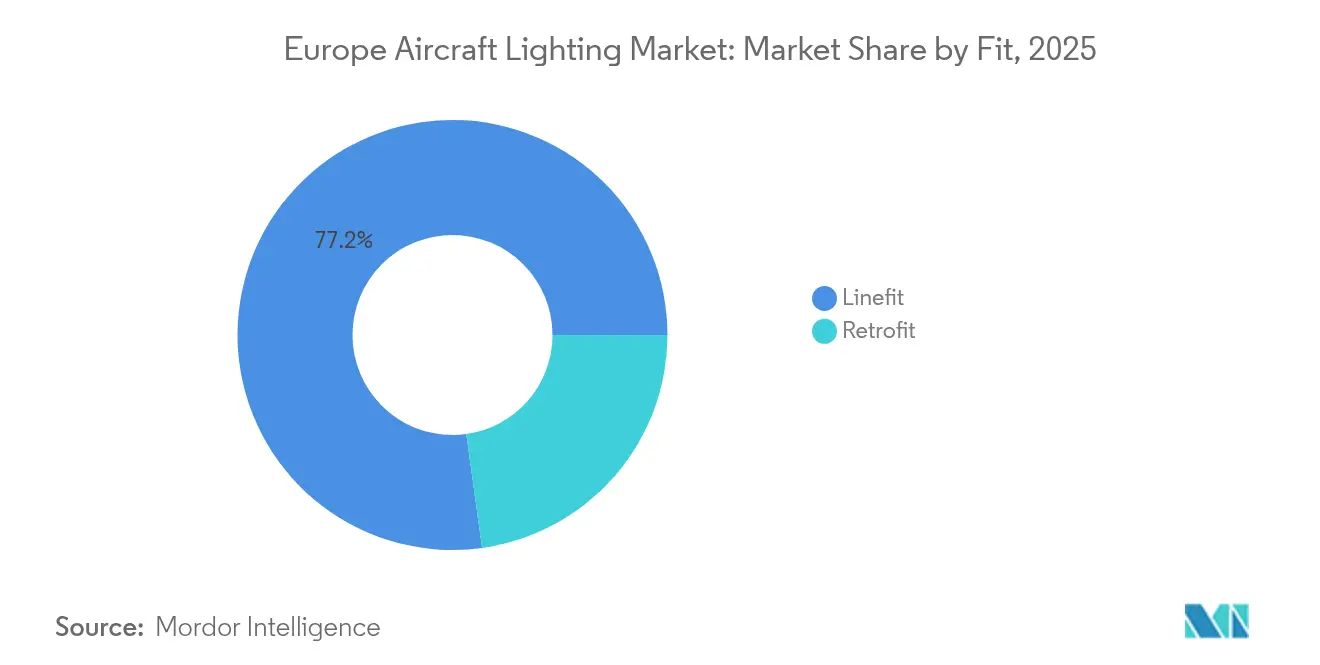

- By fit, linefit installations accounted for 77.20% of the European aircraft lighting market size in 2025; retrofit demand is expanding at a 7.1% CAGR.

- By technology, LED systems commanded 77.60% revenue in 2025 and will post a 9.85% CAGR through 2031.

- By geography, Germany led with a 30.10% revenue share in 2025, whereas Spain is forecasted to log the highest 7.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Aircraft Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet modernization and LED adoption | +1.8% | Germany, France, UK | Medium term (2-4 years) |

| Passenger demand for mood-enhancing cabin ambience | +1.2% | Western Europe | Long term (≥ 4 years) |

| Regulatory mandates on safety-critical lighting upgrades | +1.5% | EU-wide | Short term (≤ 2 years) |

| Smart, sensor-integrated lighting enabling predictive maintenance | +0.9% | Germany, France, Netherlands | Medium term (2-4 years) |

| eVTOL growth creating specialized lighting demand | +0.7% | Urban hubs in Germany, France, UK, Italy | Long term (≥ 4 years) |

| Advanced manufacturing capabilities and R&D investments | +1.1% | Germany, France, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet Modernization and LED Adoption

Airlines in Germany, France, and the UK accelerate fleet renewal to cut fuel burn and improve passenger comfort. Replacing incandescent or halogen fixtures with LED kits yields up to 75% energy savings and component life beyond 50,000 hours.[1]Collins Aerospace, “LED Reading Light Upgrade Kit,” collinsaerospace.com Modular retrofit products let carriers install upgrades during regular checks, avoiding long ground time. Interior LEDs with variable color temperatures help airlines deliver a premium in-flight ambience that rivals Gulf competitors. Strong production runs of A320neo family jets ensure sustained OEM demand, while rising retrofit cycles on mature fleets enlarge aftermarket revenue pools.

Passenger Demand for Mood-Enhancing Cabin Ambience

European flyers place a higher value on wellness and brand cues during travel. Dynamic lighting scenes that mimic daylight changes support circadian alignment on long-haul routes, reducing jet lag complaints. Premium carriers configure cabin zones with distinct hues, reinforcing corporate identity and segment differentiation. STG Aerospace introduced eco-friendly packaging for its saf-Tglo emergency lights, underscoring airlines’ focus on sustainability alongside aesthetics.[2]STG Aerospace, “saf-Tglo Eco Packaging,” stgaerospace.com Business jets add fully programmable LED strips that let owners personalize ambience without structural modification.

Regulatory Mandates on Safety-Critical Lighting Upgrades

EASA updated ETSO C30, C96, C85, C141, and C168 standards, tightening performance thresholds for exit, emergency, and exterior lights.[3]European Union Aviation Safety Agency, “ETSO Updates for Lighting Systems,” easa.europa.eu Operators of older aircraft must replace legacy fixtures or pursue costly exemptions, prompting predictable retrofit demand. Suppliers with pre-certified LED portfolios benefit from abbreviated approval cycles, shortening airline decision time. The directive heightens urgency for cargo operators still running halogen-based systems, accelerating LED penetration in freighter cabins and holds.

Smart, Sensor-Integrated Lighting Enabling Predictive Maintenance

Leading vendors embed IoT sensors that track temperature, shock events, and usage hours, feeding data to airline health-monitoring dashboards. Predictive algorithms flag degradation early, letting maintenance teams swap modules before in-flight failures. Airlines cut unscheduled removals and shrink spares inventory, generating measurable operational savings. German manufacturers collaborate with national research labs to refine sensor packaging that withstands high-cycle narrowbody flights. The approach aligns with Europe’s push toward data-driven maintenance under the clean aviation program.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification and compliance costs | -1.4% | EU-wide | Short term (≤ 2 years) |

| Semiconductor supply chain constraints | -1.1% | Germany and France plants | Short term (≤ 2 years) |

| Thermal management limits for high-power LEDs | -0.8% | Nordic markets | Medium term (2-4 years) |

| Weight penalties of dynamic lighting for regional fleets | -0.6% | Spain, Italy, Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Certification and Compliance Costs

EASA’s exhaustive testing regime requires vibration, electromagnetic, and temperature cycling across thousands of hours, adding millions of euros to product qualification budgets.[4]Inside Lighting, “Dialight Supply Chain Dispute,” inside.lighting Smaller innovators struggle to finance the entire process, slowing the pace at which disruptive ideas reach airlines. Lengthy documentation adds overhead for each variant, discouraging highly customized solutions. Even established Tier-1s face stretched engineering teams as they requalify entire families for evolving cybersecurity and fire-safety clauses.

Semiconductor Supply Chain Constraints

COVID-era chip shortages linger into 2025, pushing lead times for LED drivers and micro-controllers beyond 50 weeks for some part numbers. European lighting assembly sites remain exposed to Asian wafer fabs for specialized components. ams OSRAM’s Premstätten expansion will add regional capacity, but output will ramp only after 2026. Until then, suppliers carry larger raw-material inventories and airlines defer some non-critical retrofits, tempering short-term order volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lighting Type: Interior systems drive current revenue

Interior systems held 54.65% of Europe's aircraft lighting market share in 2025, driven by persistent cabin retrofit programs and large installed bases among legacy narrowbody aircraft. Cabin, cockpit, and emergency lights form the bulk of sales as airlines seek energy savings and a differentiated ambiance. Interior LEDs integrate with in-flight entertainment controls, letting crews adjust brightness by cabin zone. Europe's aircraft lighting market size for interior applications is forecasted to climb at a 6.55% CAGR through 2031 as retrofit kits proliferate across low-cost carriers.

Exterior lights represented 45.35% revenue in 2025 but will outpace interiors at an 8.05% CAGR, lifted by stringent anti-collision visibility rules and eVTOL design needs. High-intensity LEDs now rival xenon bulbs for landing-light candela output while cutting maintenance labor. Sensor-driven brightness modulation improves energy efficiency during taxi phases. OEM programs such as the Airbus A321XLR adopt smart exterior packages as standard, ensuring steady volume for suppliers.

By Aircraft Type: Narrowbody aircraft dominate, business jets surge

Narrowbody units represented 53.12% of 2025 shipments, reflecting A320neo and B737 MAX build rates. Operators standardize LED configurations to streamline spares across fleets, accelerating line-fit volumes. Europe's aircraft lighting market share for narrowbodies benefits from low-cost carriers upgrading cabins to differentiate amid fare competition.

Business jets deliver the fastest 6.31% CAGR as charter demand and corporate travel rebound. Owners specify bespoke reading lamps, ceiling washes, and accent lights that integrate with smart-cabin apps. Sustainable aviation-fuel initiatives spur new airframe programs that embed ultra-efficient LEDs.

By Fit: Linefit still dominant but retrofit gains momentum

Linefit accounted for 77.20% of the 2025 value, driven by direct supplier-OEM contracts that bundle lighting into electrical-system shipsets. Integrated design cuts wiring weight and simplifies certification, preserving the segment’s lead.

Retrofit activity, at 22.80%, is rising at a 7.1% CAGR as carriers realize quick payback from LED conversions. Drop-in kits reduce modification man-hours, and predictive maintenance dashboards help airlines plan provisioning. The European aircraft lighting market will increasingly pivot toward the aftermarket as the installed fleet swells and sustainability targets tighten.

By Technology: LEDs cement market transformation

LED platforms held 77.60% share in 2025 and will accelerate at a 9.85% CAGR. Smart drivers allow dim-to-warm profiles and Bluetooth commissioning, streamlining MRO workflows. Diehl Aviation’s Lightshifter concept projects dynamic light carpets that guide boarding and deplaning, underscoring experiential design trends.

Incandescent, halogen, and fluorescent solutions collectively decline as spares dwindle and energy penalties grow. Some cockpit indicators still rely on incandescent bulbs pending certification of LED alternatives, but suppliers expect a complete phase-out before 2030.

Geography Analysis

Germany retained a 30.10% lead in 2025 thanks to its concentrated aerospace cluster around Hamburg, Munich, and Bremen. Proximity to Airbus final-assembly lines and Diehl’s engineering centers accelerates codevelopment cycles. Government support for Clean Aviation and national hydrogen-flight roadmaps underpins long-term lighting R&D budgets. EU Chips Act incentives channel semiconductor investment into Saxony and Bavaria, supporting future LED driver availability.

Spain posts a brisk 7.62% CAGR through 2031, fueled by Iberia and Vueling fleet renewals and substantial regional jet utilization. Vertiport pilots in Barcelona and Madrid attract specialty-lighting prototypes designed for urban air taxis. Local MRO hubs in Andalusia and Galicia expand retrofit hangar capacity, capturing overflow work from saturated facilities in Northern Europe.

France and the UK hold roughly one-quarter of the 2025 value, anchored by Toulouse and Bristol capabilities. Brexit-driven customs checks elongate some inbound electronics flows, yet long-standing Airbus programs continue to secure lighting volumes for French suppliers. Italy benefits from Leonardo’s helicopter manufacturing and Piaggio’s business jet line, while Eastern Europe climbs steadily as OEMs pursue cost-competitive labor and industrial-park incentives.

Competitive Landscape

Competitive Landscape

The market shows moderate concentration. Collins Aerospace, Honeywell, and Safran integrate optics, electronics, and predictive maintenance software to deepen their share of wallet with OEMs. Safran's purchase of Microtecnica's actuation assets widens its systems portfolio and cross-selling opportunities. Diehl Aviation's Space³ cabin concept illustrates the supplier's drive toward holistic passenger-experience modules. Collins Aerospace launched modular LED reading lights that airlines can retrofit without cabin structural work, underscoring the retrofit wave.

Midsize specialists maintain relevance by addressing eVTOL, infrared, or specialty-cargo niches. Oxley and Aveo Engineering deliver rugged exterior strobes approved for helicopter rescue missions, while UK-based Beadlight focuses on high-end business jet reading lamps. Semiconductor reliability remains a key differentiator as airlines demand proven MTBF statistics. Boeing's USD 4.7 billion bid for Spirit AeroSystems signals broader consolidation of aerospace supply chains, potentially reshaping tier allocation and joint sourcing strategies for lighting packages.

Europe Aircraft Lighting Industry Leaders

Honeywell International Inc.

Astronics Corporation

Collins Aerospace (RTX Corporation)

Safran SA

Diehl Stiftung & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Heads Up Technologies (HUT) acquired Innovative Advantage, a cabin management systems (CMS) specialist, enhancing its capabilities in the business jet sector.

- March 2025: Diehl Aviation showcased its state-of-the-art cabin illumination technologies at the AIX in Hamburg. These advancements, which include accent lighting and high-quality materials, aim to enhance the passenger experience significantly.

- June 2023: STG Aerospace announced the launch of the Curve, a new flexible cabin lighting product from STG Aerospace's universal lighting family. The Curve is intended for the business jet cabin market.

Europe Aircraft Lighting Market Report Scope

Aircraft lighting systems provide exterior and interior illumination. Exterior lights illuminate operations such as night landing, inspection of icing conditions, and midair collision safety. Interior lights illuminate instrumentation, cockpit, cabin, and other areas occupied by crew members and passengers. Some specific lights, including indicator and warning lights, indicate the working status of equipment.

The Europe aircraft lighting market is segmented based on lighting type, application, and geography. By lighting type, the market is segmented into exterior light and interior light. By application, the market is segmented into commercial aviation and general aviation. The report also offers the market size and forecasts for five countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD).

By Lighting Type

| Interior Lighting | Cabin Lighting |

| Cockpit Lighting | |

| Emergency and Exit Lighting | |

| Cargo/Baggage Lighting | |

| Exterior Lighting | Navigation and Position Lights |

| Landing and Taxi Lights | |

| Anti-Collision and Strobe Lights | |

| Logo and Wing Inspection Lights |

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Business Jets |

| Helicopters |

| Unmanned Aerial Vehicles (UAVs) |

By Fit

| Linefit |

| Retrofit |

By Technology

| Light-Emitting Diode (LED) |

| Fluorescent |

| Incandescent/Halogen |

By Geography

| United Kingdom |

| France |

| Germany |

| Spain |

| Italy |

| Russia |

| Rest of Europe |

| By Lighting Type | Interior Lighting | Cabin Lighting |

| Cockpit Lighting | ||

| Emergency and Exit Lighting | ||

| Cargo/Baggage Lighting | ||

| Exterior Lighting | Navigation and Position Lights | |

| Landing and Taxi Lights | ||

| Anti-Collision and Strobe Lights | ||

| Logo and Wing Inspection Lights | ||

| By Aircraft Type | Narrowbody Aircraft | |

| Widebody Aircraft | ||

| Regional Jets | ||

| Business Jets | ||

| Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| By Fit | Linefit | |

| Retrofit | ||

| By Technology | Light-Emitting Diode (LED) | |

| Fluorescent | ||

| Incandescent/Halogen | ||

| By Geography | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will the Europe aircraft lighting market be in 2031?

The Europe aircraft lighting market is projected to reach USD 962.93 million by 2031, advancing at a 7.31% CAGR during 2026-2031.

Which technology dominates aircraft lighting across Europe?

LED platforms hold 77.60% revenue share and continue to expand thanks to energy efficiency and predictive-maintenance capabilities.

Why is Spain the fastest-growing market within Europe?

Expanding regional jet networks, rising retrofit activity, and early eVTOL test programs drive Spain’s 7.62% CAGR outlook.

How does EASA regulation influence lighting upgrades?

Updated ETSO standards mandate higher performance for emergency and exterior lights, prompting predictable retrofit cycles across older fleets.

What role does predictive maintenance play in aircraft lighting?

Sensor-integrated LED fixtures stream operating data that lets airlines replace units before failure, cutting unscheduled maintenance and inventory costs.

Page last updated on: