Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

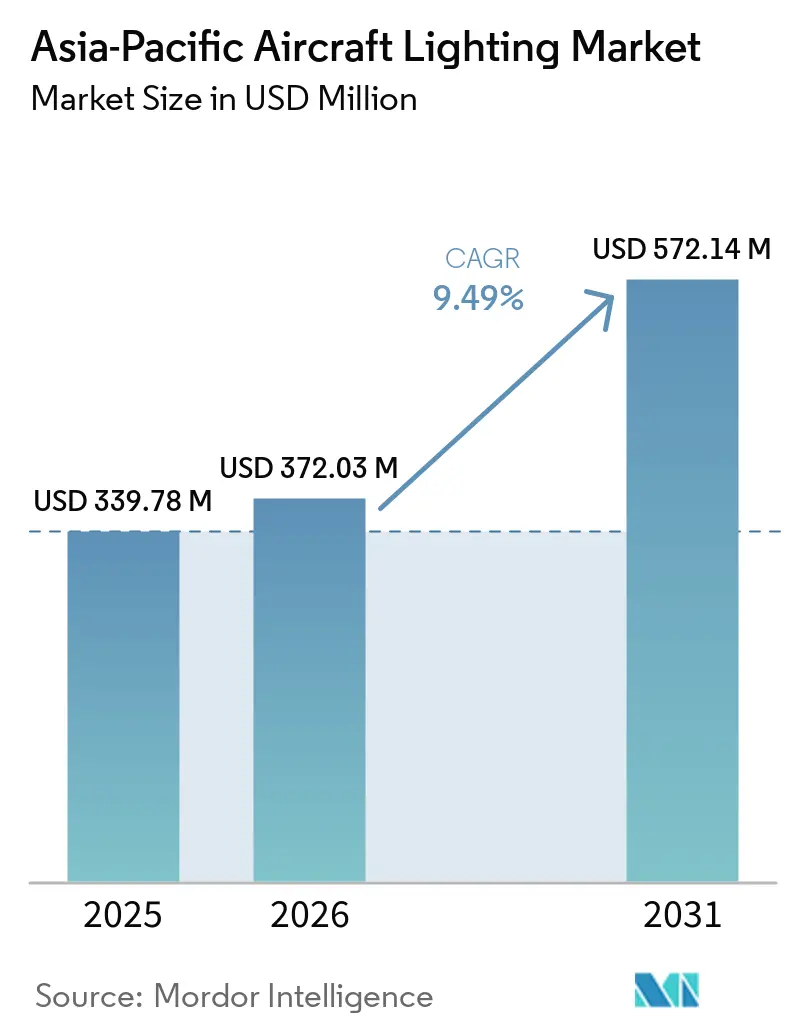

| Base Year Market Size (2025) | USD 339.78 Million |

| Market Size (2026) | USD 372.03 Million |

| Market Size (2031) | USD 572.14 Million |

| Growth Rate (2026 - 2031) | 9.49% CAGR |

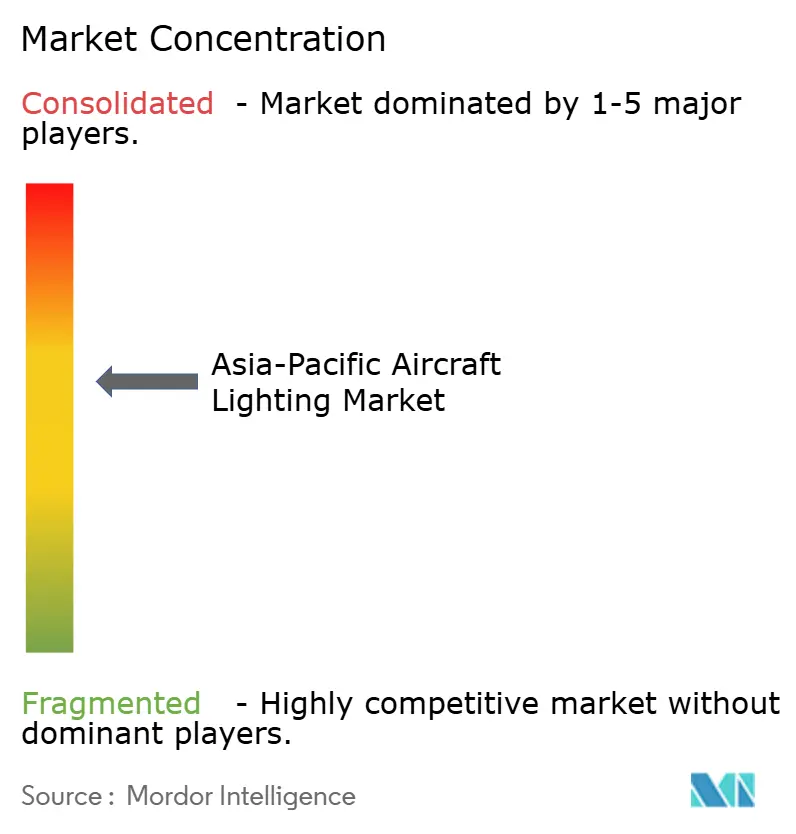

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Aircraft Lighting Market Analysis by Mordor Intelligence

The Asia-Pacific aircraft lighting market size is expected to grow from USD 339.78 million in 2025 to USD 372.03 million in 2026, and is forecasted to reach USD 572.14 million by 2031 at a 9.49% CAGR over 2026-2031. The 2025 base was USD 339.78 million, indicating an acceleration in spending on new platforms and cabin upgrades across the region. Growth is tied to faster airframe electrification, higher emergency-evacuation performance requirements, and sovereign aerospace programs that localize component supply. LED systems lead the transition with deep penetration, while retrofit momentum reflects cost-out targets and cabin refresh cycles. China remains the largest buyer, and Vietnam shows the fastest growth among key markets.

Key Report Takeaways

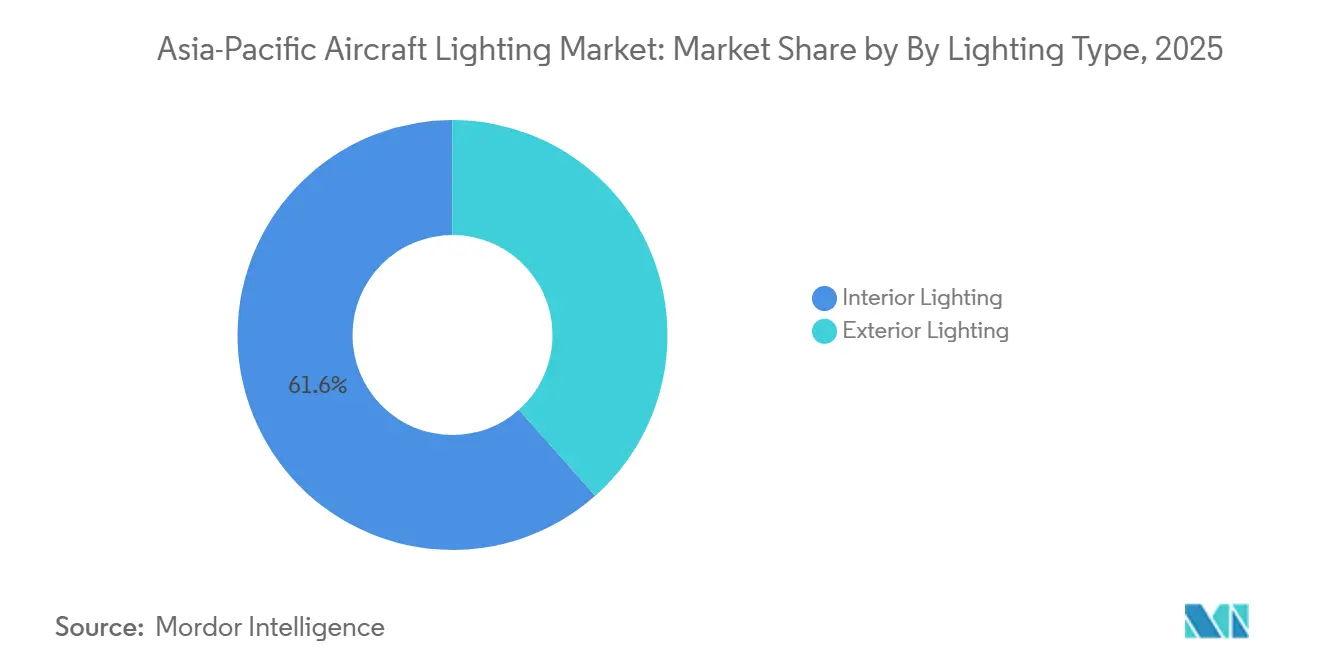

- By lighting type, interior systems led with a 61.55% revenue share in 2025, and exterior lighting is forecast to grow at a 9.89% CAGR through 2031.

- By aircraft type, narrowbody aircraft accounted for 56.76% of the market share in 2025, and regional jets are projected to expand at a 10.95% CAGR through 2031.

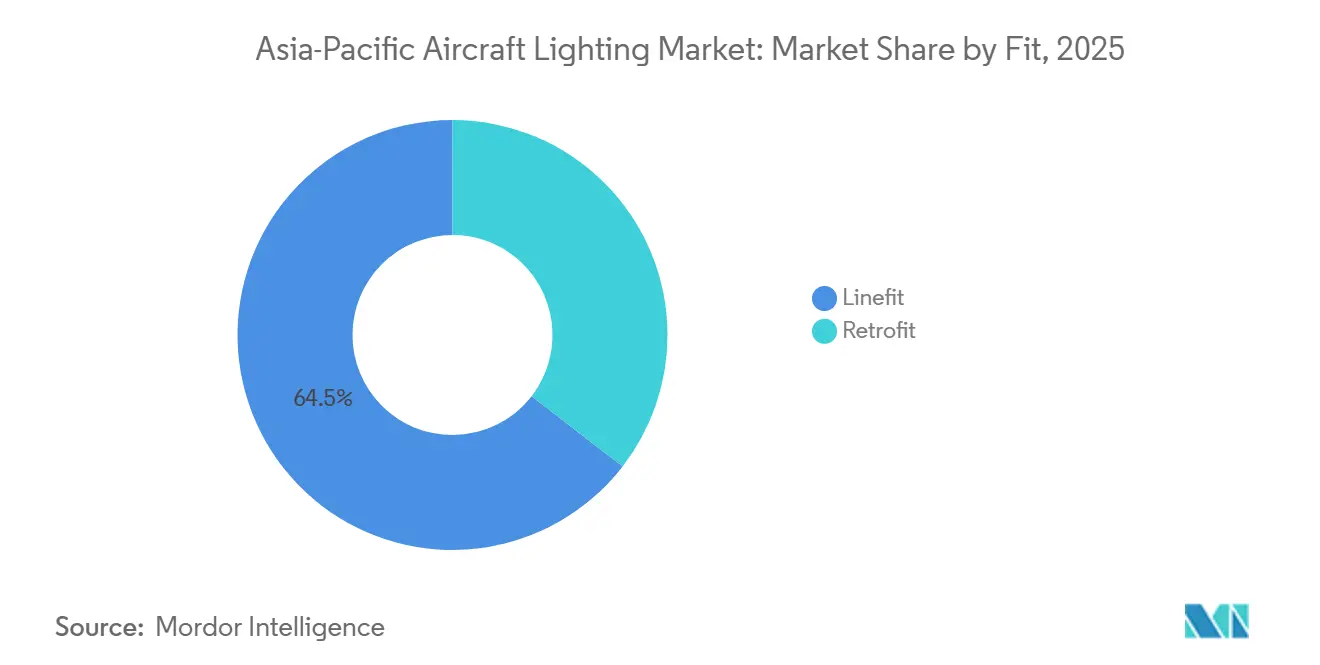

- By fit, linefit commanded 64.53% of the market share in 2025, and retrofit is forecast to advance at a 10.76% CAGR through 2031.

- By technology, LED captured 90.87% of the Asia-Pacific aircraft lighting market in 2025, and is projected to grow at an 11.25% CAGR to 2031.

- By geography, China held 46.76% market share in 2025, and Vietnam is projected to witness the highest growth at an 11.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Aircraft Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained LED-retrofit wave across Asia-Pacific commercial fleets | +1.6% | Pan-Asia, strongest in China, India, Vietnam | Short term (≤ 2 years) |

| OEM push for lighter, energy-efficient cabin and exterior systems | +1.8% | Global, with linefit gains in China, South Korea, Japan | Medium term (2-4 years) |

| Regulatory mandates on emergency/exit lighting performance | +1.4% | APAC-wide, mirroring FAA/EASA standards | Long term (≥ 4 years) |

| Record aircraft production backlogs at Airbus and COMAC | +1.7% | Global OEM supply, China-centric for C919 | Medium term (2-4 years) |

| Smart human-centric mood lighting to boost passenger wellness | +1.2% | Premium carriers (Singapore, Cathay, ANA, Air India) | Medium term (2-4 years) |

| Refurbishment cycles among low-cost carriers (LCCs) after COVID-19 | +0.8% | ASEAN, India, secondary Chinese cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustained LED-retrofit wave across APAC commercial fleets

Airlines across the region accelerated LED upgrades to cut power draw, extend maintenance intervals, and refresh cabin ambiance, with several operators standardizing on pre-certified kits to minimize aircraft downtime. Astronics reported 18.5% year-over-year growth in commercial transport sales in Q4 2025, underscoring strong demand for lighting and safety products tied to retrofit pipelines.[1]Astronics Corporation, “Astronics Corporation Reports Strong Fourth Quarter Finish,” Astronics Investors, investors.astronics.com Plug-and-play installation has proven central, with STG Aerospace indicating that liTeMood kits for major Airbus platforms can be installed in under six hours, enabling carriers to align upgrades with scheduled maintenance windows. Operators cite the long service life and controllability of LED solutions as additional drivers, as tunable lighting supports brand scenes and reduces unscheduled replacements compared with legacy technologies. Air India introduced chakra-inspired mood lighting on its first linefit B787-9 in January 2026. The airline is committed to retrofitting 26 B787-8 aircraft by mid-2027, signaling a broad shift toward wellness-aligned lighting across its mixed fleet. Singapore Airlines’ multi-year A350 retrofit program, budgeted at SGD 1.1 billion (USD 869.20 million), illustrates the scale at which Asia-Pacific full-service carriers (FSCs) are refreshing cabins, with lighting upgrades embedded in larger interior programs.

OEM push for lighter, energy-efficient cabin and exterior systems

Airframers and Tier-1 suppliers are embedding lighter, power-efficient lighting into new-build programs, thereby setting a new standard that operators seek to mirror across the in-service fleet. Airbus is preparing an A350 retrofit wave as aircraft age toward key thresholds, with upgrade options such as mood-lighting software that aligns with cabin refreshes and helps standardize the passenger experience across deliveries. Collins and other Tier-1s provide linefit-ready LED solutions across Airbus, Boeing, and regional platforms, complementing digital power and control architectures that support predictive maintenance. As Chinese programs gain share in regional narrowbody demand, suppliers embedded at the linefit level, including through local partnerships, anchor multi-year spares-and-services revenue for LED components.

Regulatory mandates on emergency/exit lighting performance

Civil aviation authorities across the Asia-Pacific have aligned more closely with FAA and EASA benchmarks, with visibility, anti-collision, and emergency-egress performance pushing airlines and OEMs toward certified LED platforms. Suppliers design to DO-160 and comparable standards to ensure electromagnetic compatibility, thermal resilience, and vibration tolerance, which lengthen development cycles but yield reliable in-service performance.[2]D.L.S. Electronic Systems, “RTCA DO-160 EMI/EMC Testing,” D.L.S. Electronic Systems, dlsemc.com Cabin illumination recommendations, such as SAE AIR512E, reinforce standards for boarding, movement, reading, lavatory use, and emergency exiting, and are often reflected in airline specification baselines for retrofits. The adoption of CAAC airworthiness codes by Brunei’s aviation authority in October 2025 extends China’s certification footprint in Southeast Asia and influences documentation pathways for components on Chinese-built platforms. LED portfolios from major suppliers emphasize compliant beam patterns, stable photometrics, and reduced maintenance relative to legacy xenon and halogen components, supporting airline safety cases and operating-cost goals. Defense applications in the region also pull through ruggedized lighting that meets strict environmental standards, reinforcing the case for solid-state solutions with high reliability.

Record aircraft production backlogs at Airbus and COMAC

Persistent order backlogs keep production slots tight and stretch delivery schedules, which in turn support both linefit shipments and retrofit programs as operators extend the life of in-service aircraft. Airbus expects a growing pool of A350s approaching mid-life by 2028 and has scoped cabin upgrade options, including lighting software updates, enabling fleets to maintain consistent cabin standards. Delivery slippages also nudge airlines to modernize cabins and lighting to remain competitive while awaiting new aircraft. In parallel, the growth of Chinese programs sustains linefit opportunities for suppliers positioned within domestic certification frameworks and local joint ventures. Airlines are bundling lighting changes with broader interior programs, as seen in Japan Airlines’ 787-9 retrofit initiative in February 2026 that aligns existing aircraft with updated cabin designs and new connectivity. This dual revenue stream for suppliers, spanning linefit and retrofit, underpins multi-year visibility for LED lighting in Asia-Pacific fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front retrofit cost and grounding time for operators | -0.7% | Budget carriers across APAC | Short term (≤ 2 years) |

| Complex DO-160/EASA CS-25 certification hurdles | -0.9% | New vendors lacking certification history | Long term (≥ 4 years) |

| Semiconductor and specialty-LED supply-chain volatility | -1.1% | Taiwanese and Korean fabs, ripple effects in China | Medium term (2-4 years) |

| EMI/EMC compliance issues in high-density cabins | -0.5% | Widebody and premium-economy retrofits | Medium term (2 |

| Source: Mordor Intelligence | |||

Up-front retrofit cost and grounding time for operators

The initial cash outlay for LED kits, installation labor, and lost revenue hours remains a headwind for carriers that run high daily utilization. LCCs are particularly sensitive to grounding time, which is why under-six-hour installation options are gaining traction on narrowbodies. Financing and balance-sheet constraints also shape timing for cabin investments when macro conditions tighten or when engine and component backlogs push up maintenance reserves. Airlines try to mitigate these costs by aligning retrofits with planned checks and by using supplemental type certificate packages that streamline engineering and regulatory steps. Even so, smaller operators may defer lighting retrofits to conserve cash, which slows adoption compared with FSCs that monetize premium cabins. Over time, fuel and maintenance savings improve the payback case, supporting broader uptake once aircraft have scheduled downtime.

Complex DO-160/EASA CS-25 certification hurdles

New entrants face extensive test programs for EMI/EMC, lightning, thermal stability, and vibration performance before equipment qualifies for installation, which adds cost and time to market. DO-160 lays out environmental and interference test protocols that require specialized labs and expert engineering support to demonstrate compliance. European pathways align with CS-25 and associated approvals, while cabins also reference standards such as SAE AIR512E, which codify illumination requirements for safety and passenger use. High-density cabins add complexity, given the mix of lighting power supplies, IFE systems, USB power, and cockpit avionics that must coexist without harmful interference. Airlines and MROs often favor established suppliers with existing certification pedigrees to reduce integration risk and shorten approval cycles. Document harmonization across jurisdictions can still create additional administrative steps for pan-Asian deployments, discouraging small manufacturers from entering.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lighting Type: Interior Systems Lead Passenger Experience Revolution

Interior lighting systems held 61.55% share in 2025, reflecting strong use of mood lighting, ambient washes, reading lights, and emergency pathfinding that support wellness and branding. Airlines in the Asia-Pacific aircraft lighting market are standardizing tunable cabin lighting to improve sleep cycles and align service touchpoints with time-of-day scenes on long-haul flights. Emergency and exit lighting remains a regulated niche, led by photoluminescent and LED solutions, supported by established approvals and an extensive global installed base. The Asia-Pacific aircraft lighting market also includes lavatory and galley task-lighting upgrades, where small changes improve crew workflow and customer satisfaction as part of broader refurbishments. Cockpit lighting remains smaller in revenue but critical in reliability and human factors, where precise beam control and longevity are key selection criteria.

Exterior systems are expected to post the fastest growth, with a 9.89% CAGR through 2031, as authorities enforce visibility and anti-collision thresholds and power-efficient LEDs replace xenon and halogen units. Suppliers offer navigation, position, landing, taxi, and strobe solutions with stable photometrics and long life to cut unscheduled removals and keep aircraft in service. Branding-oriented logo lighting and wing inspection lights gain attention for reliability and color accuracy, especially for carriers with high night operations. Combined with digital cabin power and monitoring, exterior LED packages simplify line maintenance and reduce the variety of spares within mixed fleets. Asia-Pacific carriers link these changes to safety and sustainability goals, building a strong pipeline for both linefit and retrofit over the forecast horizon.

By Aircraft Type: Narrowbody Dominance Reflects Regional Travel Boom

Narrowbodies captured 56.76% of 2025 revenues as short-haul frequency, route density, and fleet standardization make cabin and exterior LED upgrades a high-ROI priority. kits that improve energy efficiency and reduce maintenance touchpoints are particularly attractive for high-cycle single-aisle aircraft in the Asia-Pacific aircraft lighting market. Twin-aisle aircraft serve premium long-haul routes, where mood lighting creates measurable brand value and supports wellness positioning, leading to higher per-aircraft spend for interior systems. The Asia-Pacific aircraft lighting market is further reinforced by widebody refreshes that align legacy cabins with new deliveries, including reading lights and long-lasting accent lighting.

Regional jets are poised for the highest growth, with a 10.95% CAGR through 2031, as secondary-city links expand and governments promote connectivity, which benefits compact LED solutions tailored to smaller cabins and lower power budgets. Business jets remain a smaller but premium segment where bespoke lighting and fast tech adoption push spend above commercial averages. Helicopter operations require ruggedized exterior lights for demanding environments, while UAVs draw interest for lightweight anti-collision beacons that meet evolving rules. As delivery delays persist, operators across these categories are leaning on retrofits to improve efficiency and preserve the passenger experience, keeping lighting demand steady across platforms.

By Fit: Linefit Installations Dominate New Aircraft Programs

Linefit accounted for 64.53% in 2025 as OEMs embed LED systems into production with integrated power and controls that reduce post-delivery modification needs. The Asia-Pacific aircraft lighting market benefits from linefit standardization, as suppliers offer compliant, warranty-backed solutions for Airbus, Boeing, and regional programs, simplifying maintenance and certification paths for airlines. Integrated lighting in premium seats and monuments from leading interiors providers also raises embedded content at delivery. OEM initiatives to prepare retrofit options for mid-life aircraft further lock in supplier ecosystems and streamline upgrade decisions

Retrofit is projected to outpace linefit at 10.76% CAGR through 2031 as near-term energy savings, cabin refresh goals, and delivery slippages converge. Asia-Pacific carriers are adopting pre-certified LED kits that avoid wiring changes and reduce installation time to single-digit hours on certain narrowbody types, which limits revenue disruption. Programs led by FSCs and select budget carriers combine lighting with IFE and monument changes to align cabin standards across mixed fleets. Airline engineering teams and MRO partners are leveraging established STCs to compress schedules and reduce rework for regional regulators, which, in turn, reinforces retrofit as a durable growth lane for the Asia-Pacific aircraft lighting market even as OEM deliveries climb.

By Technology: LED Systems Achieve Market Dominance

LED technology held a 90.87% share in 2025 and is expected to grow at a 11.25% CAGR, reflecting deep advantages in energy efficiency, longevity, and controllability across interior and exterior applications. Airlines in the Asia-Pacific aircraft lighting market prioritize LED solutions that support precise beam control and mood scenes while cutting power draw compared with halogen or fluorescent options. Premium carriers lean on tunable palettes for brand expression and circadian alignment, while MROs favor long-life components that reduce unscheduled removals and line maintenance. Exterior LEDs also deliver stable photometrics across duty cycles and under adverse conditions, enhancing safety performance and uptime.

Fluorescent, incandescent, and halogen solutions persist mainly in older aircraft awaiting upgrade slots, though migration pressure is rising as pre-certified LED kits close on price and minimize installation time. OEM and supplier roadmaps phase out legacy bulbs across product families, anchoring LEDs as the default linefit for new deliveries in the Asia-Pacific aircraft lighting market. As digital monitoring becomes standard, airlines also value predictive alerts for lumen degradation that preempt faults and avoid in-service disruptions. Supply-chain risks around semiconductors remain a watch item, but dual sourcing and localized subassemblies are helping stabilize lead times in the region.

Geography Analysis

China accounted for 46.76% of the Asia-Pacific aircraft lighting market in 2025, driven by sovereign aerospace programs, strong linefit demand, and active retrofit activity at major state-backed carriers. Lighting suppliers are tailoring platforms to Chinese certification and passenger preferences while strengthening local presence to improve service and approval timelines. Regulatory dynamics include selective regional adoption of Chinese codes, as Brunei’s 2025 move to CAAC airworthiness standards underscores Beijing’s growing technical influence in Southeast Asia. As fleets diversify across domestic and export platforms, suppliers embedded early in linefit slots position for long-run spares and upgrade opportunities. This shaping of certification and sourcing preferences sustains a robust pipeline for LED lighting across interior and exterior systems.

India is the second-largest buyer in the Asia-Pacific aircraft lighting market, helped by large-scale cabin programs and fast-growing narrowbody fleets that prioritize efficient, brand-consistent lighting. Air India’s introduction of the B787-9 in 2026, featuring chakra-inspired mood lighting, and its planned retrofits across 26 B787-8s highlight how national flag carriers combine cultural design with advanced LED capabilities. LCCs are adopting plug-and-play LED solutions to reduce installation time and keep aircraft available for dense short-haul schedules. Larger retrofits are being synchronized with broader interior changes, which support lighting upgrades as part of standardized cabin experiences on long-haul and regional routes. Strong local engineering and emerging localization in subassemblies continue to shorten timelines for approvals and installation.

Vietnam is the fastest-growing market, with an 11.75% CAGR outlook through 2031, as leisure demand grows and airport investments advance, lifting both linefit and retrofit lighting demand. Japan and South Korea anchor premium-cabin innovation and safety-first operating models that value high-performance cockpit and exterior LED solutions. Singapore’s long-haul A350 retrofits illustrate how regional hubs are setting benchmarks for wellness-centric lighting at scale. Across ASEAN, humidity and tropical weather have pushed specifications toward robust enclosures and corrosion-resistant harnesses, supporting joint work between Tier-1s and local distributors. Diverging regulatory preferences shape supplier strategies by platform category, with FAA/EASA-aligned pathways still dominant for widebodies and business jets, and CAAC influence rising in select markets.

Competitive Landscape

The Asia-Pacific aircraft lighting market remains moderately consolidated around Honeywell International Inc., Collins Aerospace (RTX Corporation), and Safran S.A., whose certifications, OEM partnerships, and R&D investments raise switching costs and protect linefit positions. Collins provides broad LED portfolios across interior and exterior applications, supporting Airbus, Boeing, and regional platforms with compliant, high-reliability products. These Tier-1s leverage long-standing linefit positions to secure aftermarket share for spares and upgrades.

White-space remains in retrofit acceleration, where Astronics, STG Aerospace, and Diehl are winning with pre-certified, plug-and-play kits designed to minimize installation time and documentation burden. Astronics’ late-2025 results reflect healthy demand for lighting and safety products that help operators achieve power and maintenance savings goals. Aerospace expanded its regional footprint through a Wholly Foreign Owned Enterprise in Shanghai to serve major Chinese carriers and deepen support for photoluminescent and LED systems.[3]STG Aerospace, “STG Aerospace Opens New Subsidiary in China,” STG Aerospace, stgaerospace.com As airlines standardize across legacy and new cabins, ease of integration and proven documentation speed are competitive differentiators.

Supply-chain resilience and documentation experience also shape wins in the Asia-Pacific aircraft lighting market. Suppliers emphasize dual sourcing for LEDs and electronics, closer fab relationships, and stronger local support for regulatory submissions to mitigate approval and logistics risks. Regulatory frameworks that mirror those of the FAA and EASA drive demand for certified LED platforms with stable photometrics and robust EMI/EMC performance. Airlines link lighting with seat and IFE timelines in upcoming retrofit waves, reinforcing the case for integrated hardware-plus-software offerings. In this context, established incumbents and agile retrofit specialists both find room to grow as fleets expand and age across the region.

Asia-Pacific Aircraft Lighting Industry Leaders

Honeywell International Inc.

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Astronics Corporation

Safran S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: STG Aerospace introduced its latest innovation, the E1, the world's first sustainable emergency floor path marking system, as part of its "eco everything" concept at the Aircraft Interiors Expo (AIX) 2025 in Hamburg, Germany.

- March 2025: Diehl Aviation showcased its state-of-the-art cabin-illumination technologies at AIX in Hamburg. These advancements, which include accent lighting and high-quality materials, aim to significantly enhance the passenger experience.

Asia-Pacific Aircraft Lighting Market Report Scope

The Asia-Pacific aircraft lighting market encompasses the design, manufacturing, integration, and supply of lighting systems installed on aircraft to ensure operational safety, regulatory compliance, and improved passenger experience. Aircraft lighting systems provide both exterior and interior illumination, serving safety, operational efficiency, and cabin comfort. Exterior lighting supports functions like landing, taxiing, navigation, anti-collision, and inspection. In contrast, interior lighting is used for cockpit instrumentation, cabin areas, lavatories, galleys, signage, and other spaces occupied by crew and passengers. Advanced lighting solutions, including LED-based and smart ambient systems, are increasingly adopted to improve energy efficiency and enhance brand differentiation. Additionally, indicator and warning lights communicate equipment status and operational conditions.

The Asia-Pacific aircraft lighting market is segmented by lighting type, aircraft type, fit, technology, and geography. By lighting type, the market is segmented into exterior lighting and interior lighting. By aircraft type, the market is segmented into narrowbody aircraft, widebody aircraft, regional jets, business jets, helicopters, and unmanned aerial vehicles (UAVs). By fit, the market is segmented into linefit and retrofit. By lighting technology, the market is segmented into light-emitting diode (LED), fluorescent, and incandescent/halogen. The report also provides market size and forecasts for seven countries within the region. For each segment, the market size and forecasts are provided in terms of value (USD).

By Lighting Type

| Interior Lighting | Cabin Lighting |

| Cockpit Lighting | |

| Emergency and Exit Lighting | |

| Cargo/Baggage Lighting | |

| Exterior Lighting | Navigation and Position Lights |

| Landing and Taxi Lights | |

| Anti-Collision and Strobe Lights | |

| Logo and Wing Inspection Lights |

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Business Jets |

| Helicopters |

| Unmanned Aerial Vehicles (UAVs) |

By Fit

| Linefit |

| Retrofit |

By Technology

| Light-Emitting Diode (LED) |

| Fluorescent |

| Incandescent/Halogen |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Singapore |

| Vietnam |

| Rest of Asia-Pacific |

| By Lighting Type | Interior Lighting | Cabin Lighting |

| Cockpit Lighting | ||

| Emergency and Exit Lighting | ||

| Cargo/Baggage Lighting | ||

| Exterior Lighting | Navigation and Position Lights | |

| Landing and Taxi Lights | ||

| Anti-Collision and Strobe Lights | ||

| Logo and Wing Inspection Lights | ||

| By Aircraft Type | Narrowbody Aircraft | |

| Widebody Aircraft | ||

| Regional Jets | ||

| Business Jets | ||

| Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| By Fit | Linefit | |

| Retrofit | ||

| By Technology | Light-Emitting Diode (LED) | |

| Fluorescent | ||

| Incandescent/Halogen | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific aircraft lighting market?

The Asia-Pacific aircraft lighting market size is USD 372.03 million in 2026 and is expected to reach USD 572.14 million by 2031 at a 9.49% CAGR.

Which technology leads adoption across Asia-Pacific fleets?

LED systems dominate with 90.87% share in 2025 and are forecasted to grow at 11.25% CAGR through 2031, driven by efficiency, longevity, and controllability.

Which segments are growing fastest in Asia-Pacific aircraft lighting?

Exterior lighting is the fastest-growing by lighting type at 9.89% CAGR, regional jets lead by aircraft type at 10.95% CAGR, and retrofit leads by fit at 10.76% CAGR.

Which countries are most significant for demand today?

China accounted for 46.76% of 2025 spending and Vietnam is the fastest growing with an 11.75% CAGR through 2031, while India remains the second-largest buyer.

How are airlines using lighting to enhance passenger experience?

Carriers deploy tunable mood lighting to align with circadian rhythms and brand identity, as seen with Air India’s 787-9 implementation and Singapore Airlines’ A350 program.

What are the primary barriers to faster adoption of LED upgrades?

The main barriers are up-front retrofit costs, grounding time, and certification complexity for EMI/EMC and environmental tests under standards such as DO-160 and CS-25.

Page last updated on: