Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

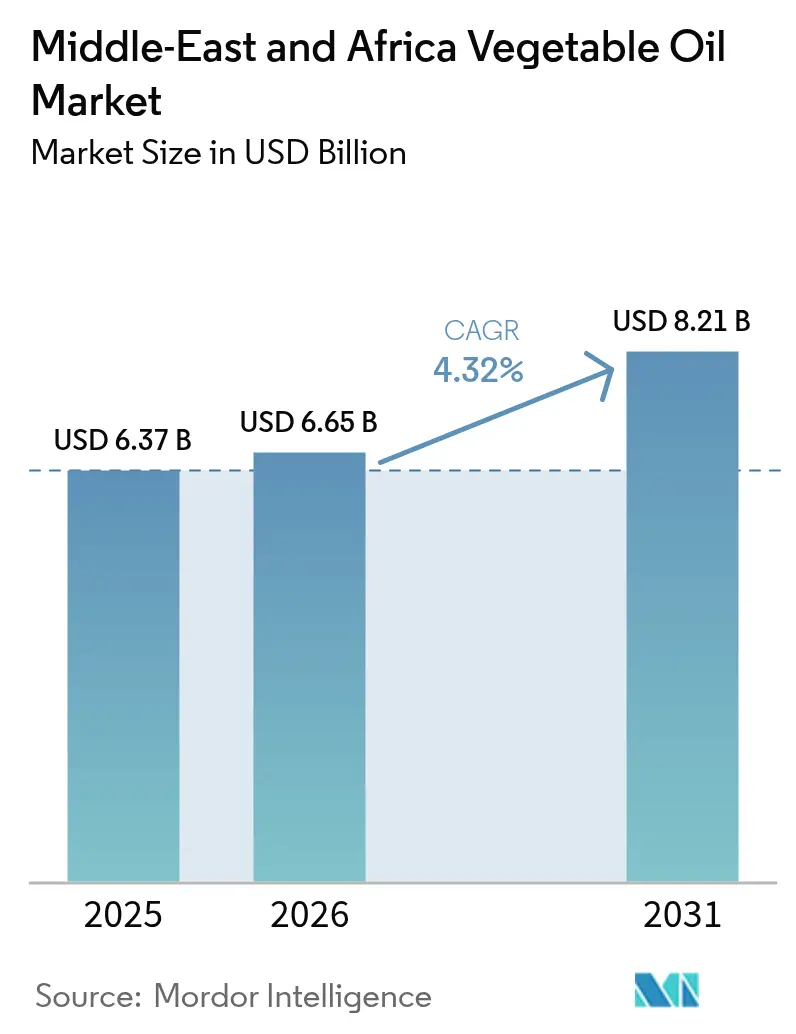

| Base Year Market Size (2025) | USD 6.37 Billion |

| Market Size (2026) | USD 6.65 Billion |

| Market Size (2031) | USD 8.21 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

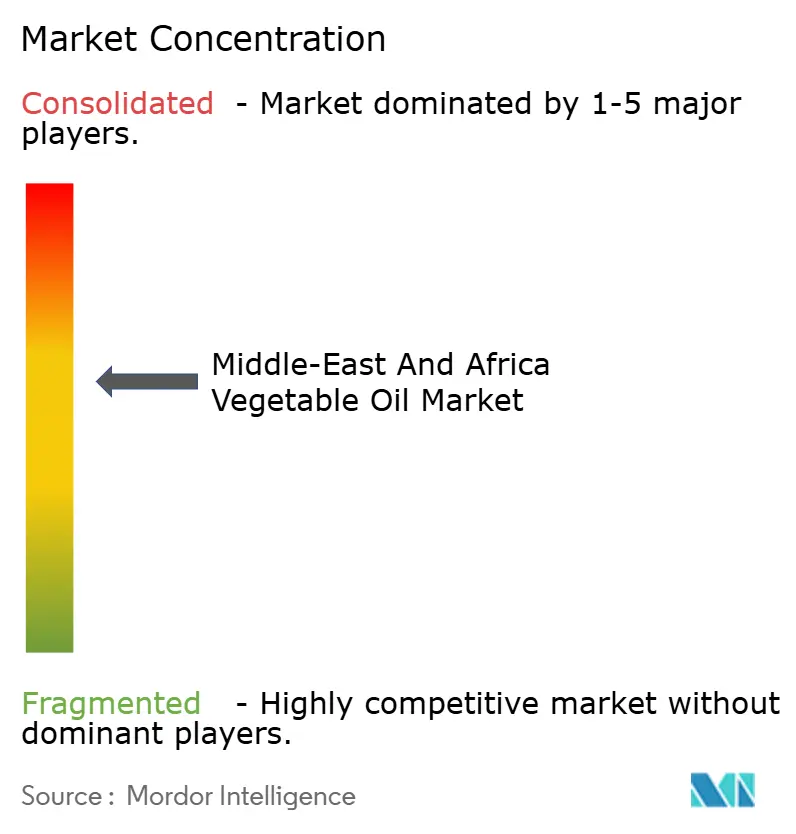

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Vegetable Oil Market Analysis by Mordor Intelligence

Middle East and Africa vegetable oil market size in 2026 is estimated at USD 6.65 billion, growing from 2025 value of USD 6.37 billion with 2031 projections showing USD 8.21 billion, growing at 4.32% CAGR over 2026-2031. Robust urban population growth, a widening middle-income base, and the region’s role as a strategic transit corridor for global vegetable oil shipments continue to propel demand. Government food-security agendas, most visibly in Saudi Arabia, the UAE, and Egypt, encourage domestic crushing and refining projects that shorten supply chains and soften currency-driven import pressures. Momentum is reinforced by quick-service restaurant expansion, surging biofuel mandates, and stepped-up investment in alternative logistics corridors that mitigate Red Sea risks. Layered on top is a marked consumer tilt toward oils with favorable fatty-acid profiles, a shift that is elevating sunflower oil without dislodging price-advantaged palm oil from its leading position.

Key Report Takeaways

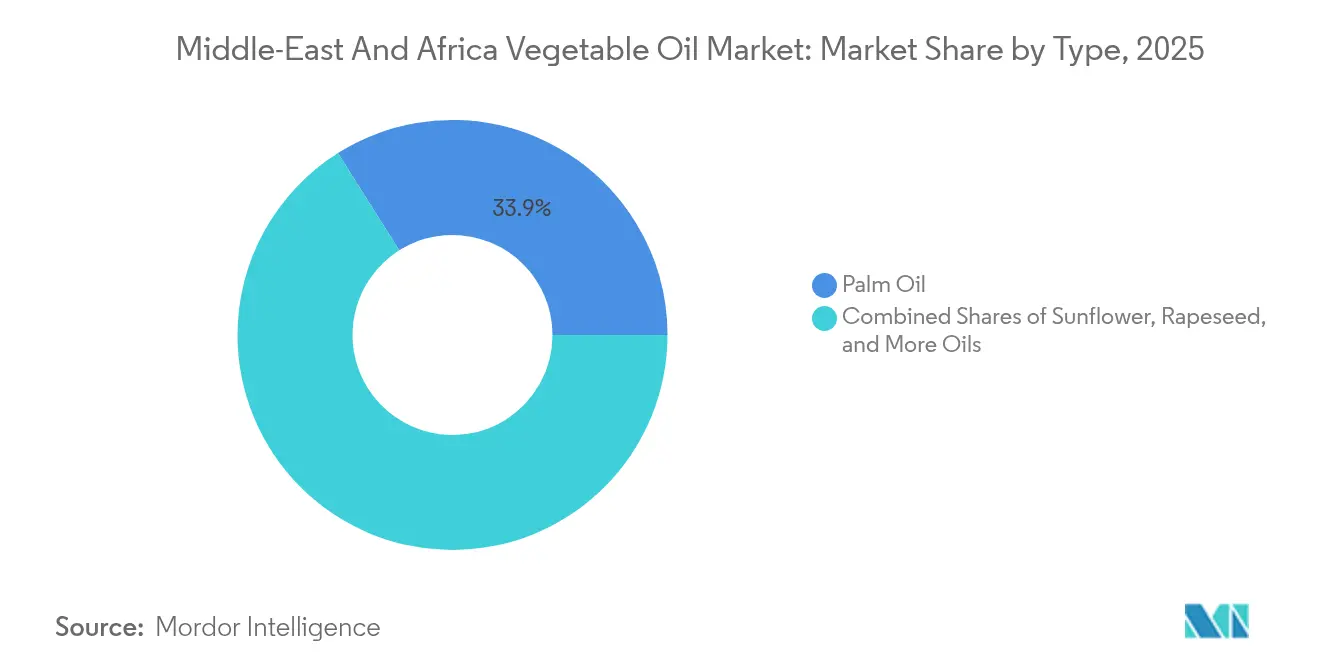

- By type, palm oil captured 33.94% of the Middle East and Africa vegetable oil market share in 2025, and sunflower oil is projected to achieve a 5.27% CAGR to 2031.

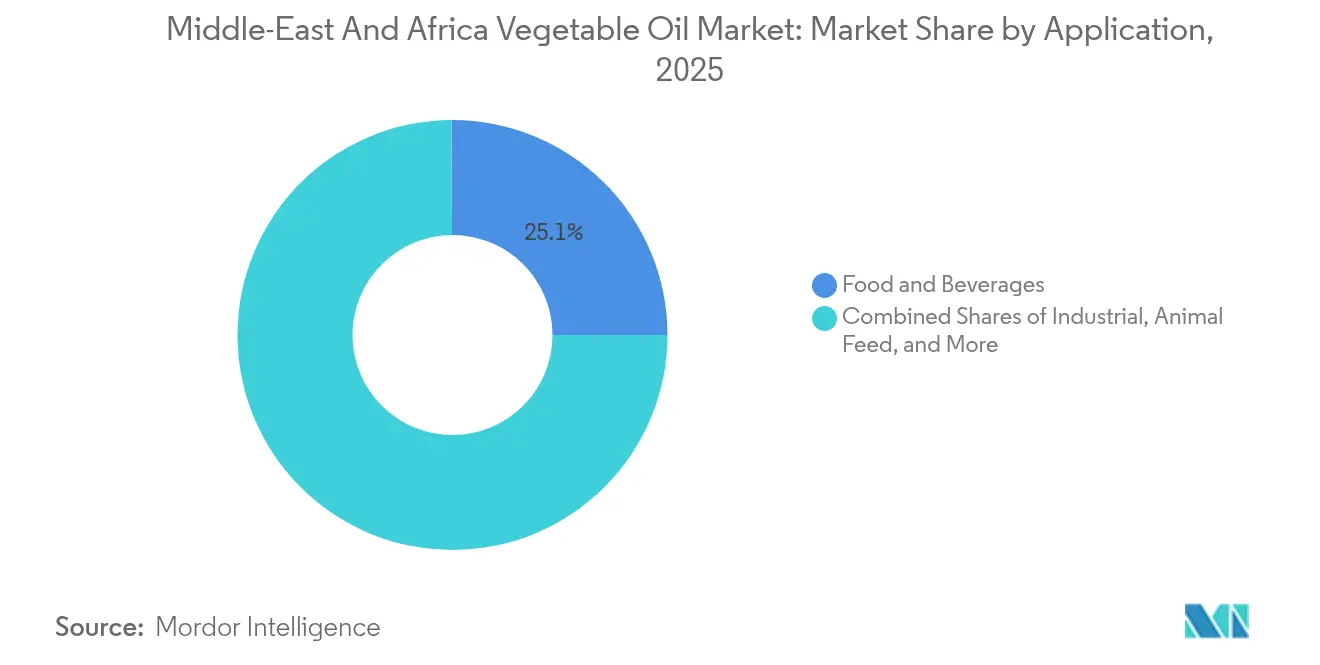

- By application, food and beverages accounted for 25.08% of the Middle East and Africa vegetable oil market share in 2025, whereas the industrial segment is advancing at a 5.92% CAGR through 2031.

- By geography, South Africa led with 34.05% market share in 2025, while Nigeria is on track for the fastest 6.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East And Africa Vegetable Oil Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for cooking oils and processed foods | +1.2% | Global, with highest impact in Nigeria, Egypt, Saudi Arabia | Medium term (2-4 years) |

| Government initiatives supporting local production | +0.8% | Saudi Arabia, UAE, Egypt, Nigeria | Long term (≥ 4 years) |

| Expansion of food service and hospitality industries | +0.7% | UAE, Saudi Arabia, South Africa, Turkey | Short term (≤ 2 years) |

| Technological advancements in refining, processing, and packaging | +0.5% | South Africa, UAE, Saudi Arabia | Medium term (2-4 years) |

| Rising applications in biofuels and other applications | +0.6% | South Africa, Nigeria, Egypt | Long term (≥ 4 years) |

| Expanding strategic trade and logistics hubs | +0.4% | UAE, Saudi Arabia, Egypt, Djibouti | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Cooking Oils and Processed Foods

Urban populations in key markets across the Middle East and Africa have exceeded 60%, driving significant changes in consumption patterns. This shift has led to increased demand for convenience foods and premium cooking oils. Nigeria's population is expected to reach 440 million by 2050, resulting in a growing need for affordable vegetable oils. Concurrently, rising disposable incomes are creating opportunities for value-added products. In the Gulf Cooperation Council countries, the processed food sector is expanding rapidly, fueled by changing lifestyles and a large expatriate population, which is boosting demand for international cuisine ingredients and specialty oils. In Kenya, government efforts to cut cooking oil imports by 50% through enhanced local production highlight how demographic changes are shaping policy decisions and transforming supply chains, as noted by the USDA Foreign Agricultural Service[1]USDA Foreign Agricultural Service, “Kenya Edible Oil Investment Opportunities,” apps.fas.usda.gov. These demographic trends present a dual opportunity: increased demand for basic cooking oils and a shift toward premiumization in processed food applications. This development has significant implications for refining capacities and distribution networks across the region.

Government Initiatives Supporting Local Production

Governments worldwide are addressing strategic food security concerns by significantly increasing investments in domestic vegetable oil production. This shift comes as nations confront the risks of import-dependent supply chains, highlighted by recent global disruptions. For instance, the UAE's Comprehensive Economic Partnership Agreement with Indonesia not only facilitates palm oil trade but also strengthens the UAE's domestic refining capacity, led by entities like ADVOC and supported by the UAE Ministry of Economy[2] UAE Ministry of Economy, “UAE-Indonesia Comprehensive Economic Partnership Agreement,” moec.gov.ae. Similarly, Egypt is offering incentives for biodiesel production facilities to reduce import dependency while enhancing renewable energy feedstock production. In Uganda, government-backed processing infrastructure, as revealed by an edible oil industry mapping, aims to transition the country from a raw material exporter to a value-added producer, potentially altering regional trade patterns. These initiatives signify a critical shift from trade-reliant strategies to production-oriented food security approaches, creating opportunities for technology transfer partnerships and joint ventures between international stakeholders and local manufacturers. Additionally, Iran's success in reducing trans fats through domestic fractionation technology highlights how government-driven programs can achieve both health improvements and industrial advancements.

Expansion of Food Service and Hospitality Industries

Gulf states are witnessing a surge in demand for food service-grade vegetable oils as they recover from the pandemic and implement economic diversification strategies. Dubai and Riyadh are positioning themselves as global hospitality hubs, driving the need for advanced supply chain solutions. This growth is not confined to traditional tourism markets. Nigeria's expanding quick-service restaurant industry and South Africa's established food service infrastructure are fueling demand for specialized products such as high-stability frying oils and portion-controlled packaging. Similarly, Ghana's hospitality sector highlights the broader potential in West Africa, where urbanization and a growing middle class are increasing the demand for processed food inputs and cooking oils in commercial applications, as noted by the USDA Foreign Agricultural Service. These trends are particularly important as food service applications typically offer higher profit margins and require advanced supply chain capabilities. This complexity creates barriers to entry, benefiting established players with strong distribution networks.

Rising Applications in Biofuels and Other Applications

Renewable energy mandates and climate commitments across the region are significantly boosting the demand for vegetable oils as biodiesel feedstock. The UAE's initiatives in converting waste cooking oil into biodiesel highlight the sector's potential within a circular economy, as noted by the UAE Ministry of Energy and Infrastructure. Similarly, South Africa's biofuel industry development efforts and Egypt's biodiesel investment incentives reflect governmental recognition of the strategic importance of vegetable oils beyond food applications. This shift is creating new revenue opportunities for producers and processors. The industrial applications segment demonstrates increasing demand for bio-based lubricants, cosmetic ingredients, and specialty chemicals derived from vegetable oils. This trend is driven by sustainability regulations that prioritize renewable feedstocks over petroleum-based alternatives. Nigeria, with its abundant palm oil resources, is well-positioned to meet domestic biofuel demand and capitalize on export opportunities in markets with renewable fuel mandates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy dependence on imports exposes the market to price and supply fluctuations | -1.1% | Egypt, Nigeria, Saudi Arabia, UAE | Short term (≤ 2 years) |

| Volatility of raw material prices | -0.9% | Global, with highest impact in import-dependent markets | Short term (≤ 2 years) |

| Health concerns over certain oils high in saturated fats | -0.4% | Saudi Arabia, UAE, South Africa | Medium term (2-4 years) |

| Technological disruption with alternative edible oils or substitutes capturing market share | -0.3% | South Africa, UAE, Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy Dependence on Imports Exposes the Market to Price and Supply Fluctuations

Egypt's recent supply crisis, caused by global export bans, highlights the region's susceptibility to external shocks due to its significant dependence on imported vegetable oils. Red Sea shipping disruptions have altered trade patterns, forcing importers to bear an additional USD 1 million per round trip for Cape of Good Hope routing and extending delivery times by 10-14 days, according to the Centre for Economic Policy Research. The concentration of global vegetable oil production in a few countries creates systemic risks. Disruptions such as Ukraine's sunflower oil supply issues and Indonesia's intermittent palm oil export restrictions demonstrate how geopolitical events can impact regional supply chains. Import-dependent markets face challenges from currency volatility and commodity price fluctuations. Local currency depreciation exacerbates the effect of global price increases on domestic consumers. To address this vulnerability, there is a growing shift toward regional sourcing and increasing domestic production. However, the substantial capital and time required for these transitions leave markets temporarily exposed to ongoing supply chain disruptions.

Volatility of Raw Material Prices

Renewable fuel mandates are driving new demand sources, with CME Group data revealing a stronger correlation between energy prices and vegetable oil futures, highlighting increased commodity price volatility. Weather-related production disruptions in major growing regions, coupled with inventory speculation and financial market activity, are causing price fluctuations that challenge traditional procurement and pricing strategies for regional processors and distributors. The financialization of commodity markets has expanded the factors influencing vegetable oil prices, moving beyond basic supply and demand to include currency fluctuations, energy prices, and macroeconomic policy decisions in leading economies. Regional processors often face margin pressures as raw material costs rise faster than they can adjust finished product prices, particularly in markets with price-sensitive consumers and limited capacity to pass on cost increases. This volatility is prompting greater investment in risk management capabilities and supply chain diversification. Simultaneously, companies with advanced forecasting and hedging expertise are capitalizing on opportunities to gain competitive advantages through more stable pricing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Palm Oil Dominance Faces Sunflower Challenge

In 2025, palm oil holds a significant 33.94% market share, driven by its cost-efficiency and adaptability across various applications, including food processing and industrial uses. However, its leading position faces growing challenges from health-conscious consumers and advocates for sustainability. Sunflower oil, although more expensive than palm oil, is projected to grow at an impressive 5.27% CAGR through 2031, reflecting a shift in consumer preferences toward oils with healthier fatty acid profiles and cleaner production processes. Soybean oil continues to see stable demand in food manufacturing, while rapeseed oil caters to niche markets, particularly in premium cooking and specialty food products.

Regulatory frameworks are playing an increasingly pivotal role in shaping competition among oil types. For example, the World Health Organization's initiative to eliminate trans fats is driving the industry away from partially hydrogenated oils and toward naturally stable alternatives. Additionally, oils such as coconut, cottonseed, and olive target specialized segments where premium positioning and distinct nutritional profiles command higher margins. However, their growth is limited by supply constraints and price sensitivity. The growing preference for sunflower oil reflects broader health-conscious trends and the influence of European dietary preferences in urban markets. This shift creates opportunities for suppliers capable of ensuring consistent quality and reliable supply chains, even amid geopolitical disruptions affecting traditional sunflower oil exporters.

By Application: Industrial Segment Drives Future Growth

In 2025, food and beverage applications hold a significant 25.08% market share, spanning from everyday cooking oils to specialized ingredients for processed foods. This highlights the sector's critical role in regional nutrition and food security. The industrial segment, with an impressive 5.92% CAGR, stands out as the market's fastest-growing area. This growth is driven by biofuel mandates, renewable energy initiatives, and the increasing use of bio-based chemicals and lubricants, leveraging the sustainable properties of vegetable oils. Within the food and beverage sector, categories such as dairy, bakery and confectionery, snacks, and meat products have distinct requirements for oil functionality and quality.

Personal care and cosmetics are benefiting from rising consumer interest in natural ingredients and sustainability. At the same time, the animal feed sector provides a consistent demand base, mitigating the impact of production fluctuations and price volatility. The industrial segment's growth is further supported by government policies promoting renewable energy and circular economy principles. Efforts like waste cooking oil collection and biodiesel production not only support sustainability but also create new value streams within the vegetable oil supply chain, as noted by the UAE Ministry of Energy and Infrastructure. Furthermore, technical and specialty applications are emerging as promising areas for innovation, enabling the development of unique value propositions and premium pricing opportunities.

Geography Analysis

In 2025, South Africa holds a leading 34.05% market share, driven by its advanced refining infrastructure and well-established distribution networks. These networks support both domestic consumption and exports across sub-Saharan Africa. The country's strong regulatory framework and high-quality standards attract international partnerships and technology transfers. Additionally, South Africa's diversified economy ensures consistent demand across food service, retail, and industrial sectors. Nigeria, Africa's most populous nation, is experiencing a notable 6.66% CAGR projected through 2031. This growth is propelled by urbanization rates exceeding 50% and a growing middle class, which is fueling significant demand for processed foods and cooking oils. Nigeria's abundant palm oil resources and government initiatives promoting local production create opportunities for import substitution and value-added processing. However, market participants face challenges related to infrastructure limitations and regulatory complexities.

Turkey's strategic location, bridging European and Middle Eastern markets, positions it as both a processing hub and a distribution center for regional vegetable oil flows. This advantage is supported by Turkey's advanced manufacturing capabilities and favorable trade agreements. Egypt, with its large domestic market, also serves as a key distribution hub for North African markets. However, recent supply chain disruptions have exposed vulnerabilities associated with import-dependent strategies. In Saudi Arabia and the UAE, premium markets are characterized by health-conscious consumers and a sophisticated food service sector, driving demand for specialty oils and value-added products. At the same time, government-led food security initiatives are fostering investments in domestic production and processing. The broader Middle East and Africa region features diverse markets, ranging from Morocco's established olive oil traditions to Kenya's emerging processing capabilities. Each market offers unique opportunities and challenges, requiring localized strategies and partnerships. Disruptions in Red Sea shipping have accelerated the development of alternative trade routes and regional processing capabilities. These changes are reshaping traditional supply chain dynamics and introducing new competitive landscapes. The region's collective growth reflects broader economic progress, infrastructure development, and regulatory harmonization efforts, which are creating more integrated and efficient vegetable oil markets that extend beyond traditional geographic boundaries.

Competitive Landscape

The vegetable oil market in the Middle East and Africa is moderately concentrated, offering opportunities for consolidation and strategic alliances. Global players compete with established regional leaders to expand market share and strengthen supply chain control. Companies like Cargill, Wilmar, and Bunge utilize their global sourcing expertise and advanced processing technologies to serve large-scale customers. In contrast, regional players such as ADVOC, Savola Group, and IFFCO Group leverage their deep understanding of local markets, extensive distribution networks, and strong government relationships.

A growing trend is the focus on vertical integration and enhancing supply chain resilience. Firms are investing in upstream production, improving logistics infrastructure, and exploring alternative sourcing strategies to mitigate risks exposed by recent global disruptions. Technology adoption is becoming a key competitive factor in the industry. Leading companies are investing in advanced refining technologies, automated packaging systems, and digital supply chain management tools to enhance efficiency, improve product quality, and reduce operational costs.

White-space opportunities are emerging in specialized segments such as biofuels, cosmetic ingredients, and premium cooking oils, where innovation and product development can drive unique value propositions and premium pricing. Bunge's integrated approach, spanning sourcing to refining, reflects this shift. Their sustainability initiatives, including achieving 100% traceability of soy in priority Brazilian regions by the end of 2024, illustrate how regulatory compliance and ESG commitments are evolving into competitive advantages. Additionally, alternative protein companies and biotechnology firms are developing novel oil sources, but their impact remains limited in the short term due to challenges related to scale and cost.

Middle-East And Africa Vegetable Oil Industry Leaders

Cargill, Incorporated

Sime Darby Plantation Berhad

Wilmar International Limited

ADVOC (ABU DHABI VEGETABLE OIL COMPANY)

Savola Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Olam Agri has expanded its soybean program in Nigeria, integrating 5,000 smallholder farmers into its supply chain in Kwara State. This move is part of the company's strategy to bolster its edible oil business.

- August 2024: Angola opened a new vegetable and palm oil factory in Luanda. The country invested USD 90 million in this expansion. This expansion was aimed at strengthening the market presence for vegetable oils.

- May 2024: Wilmar Edible Oil Refineries completed the first phase of its edible oils refining plant (Wilmar Processing SA) located in the Richards Bay Industrial Development Zone (RBIDZ) Special Economic Zone. Richards Bay's deep-water port, with its direct pipeline connection to the tank farm, enables the company to efficiently receive imported oils. This setup allows for the direct unloading of raw materials and crude oil from large vessels straight to the company's plant.

- March 2023: Wilmar International Ltd (WILMAR) initiated the construction of an edible oil plant located in Richards Bay, KwaZulu-Natal, South Africa. This USD 81 million project encompasses the development of a fractionator, a shortening plant, and a packaging facility. Notably, this endeavor commenced in 2020.

Middle-East And Africa Vegetable Oil Market Report Scope

The Middle-East and Africa vegetable oil market has been segmented by product type, which includes palm oil, soybean oil, rapeseed oil, sunflower oil, olive oil, and other product types. Based on application, the market is segmented into food, feed, and industrial. The study also involves the regional level analysis of the main countries such as South Africa, the United Arab Emirates, and Rest of Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

Type

| Palm Oil |

| Soybean Oil |

| Rapeseed Oil |

| Sunflower Oil |

| Other Oil Types (Cottonseed Oil, Olive Oil, Coconut Oil) |

Application

| Food and Beverages | Dairy products |

| Bakery and Confectionery | |

| Snacks and Savory Products | |

| Meat Products | |

| Other Types | |

| Personal Care and Cosmetics | |

| Animal Feed | |

| Industrial | |

| Other Applications |

Geography

| Saudi Arabia |

| South Africa |

| Turkey |

| Nigeria |

| Egypt |

| Rest of Middle East and Africa |

| Type | Palm Oil | |

| Soybean Oil | ||

| Rapeseed Oil | ||

| Sunflower Oil | ||

| Other Oil Types (Cottonseed Oil, Olive Oil, Coconut Oil) | ||

| Application | Food and Beverages | Dairy products |

| Bakery and Confectionery | ||

| Snacks and Savory Products | ||

| Meat Products | ||

| Other Types | ||

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Industrial | ||

| Other Applications | ||

| Geography | Saudi Arabia | |

| South Africa | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Middle East and Africa vegetable oil market?

The market is valued at USD 6.65 billion in 2026.

Which country currently leads regional share?

South Africa leads with a 34.05% share in 2025.

Which oil type is growing fastest?

Sunflower oil shows a forecast 5.27% CAGR through 2031.

Why are logistics hubs important?

New hubs in Djibouti, Saudi Arabia, and Egypt shorten lead times, diversify routes, and enable value-added processing.

Page last updated on: