Middle East Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

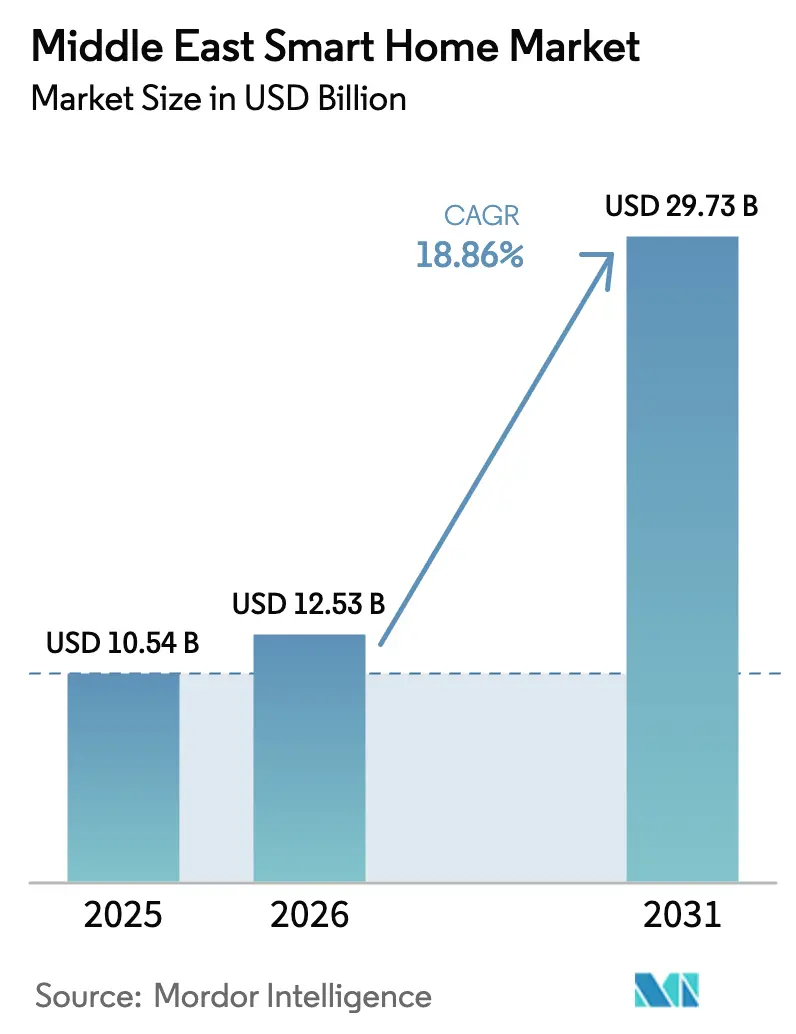

| Base Year Market Size (2025) | USD 10.54 Billion |

| Market Size (2026) | USD 12.53 Billion |

| Market Size (2031) | USD 29.73 Billion |

| Growth Rate (2026 - 2031) | 18.86% CAGR |

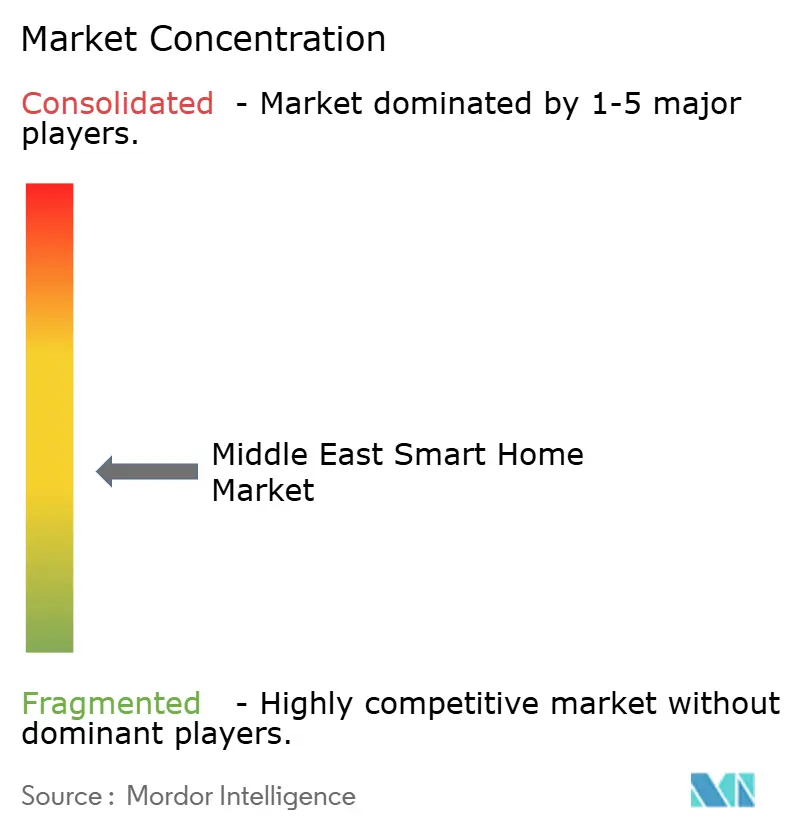

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East Smart Home Market Analysis by Mordor Intelligence

The Middle East smart home market size is projected to expand from USD 10.54 billion in 2025 and USD 12.53 billion in 2026 to USD 29.73 billion by 2031, registering a CAGR of 18.86% between 2026 to 2031. Robust sovereign-fund backing for greenfield smart-city programs, near-universal fiber-to-the-home coverage in the Gulf, and tariff reforms that expose households to real electricity costs are converting connected-home solutions from lifestyle upgrades into mandatory infrastructure. Municipal megaprojects such as NEOM, Lusail City, and Expo City Dubai embed device interoperability, cybersecurity, and energy-efficiency specifications into building codes, effectively creating captive demand channels that bypass slow retail adoption curves. Telcos are turning fiber roll-outs into cross-selling engines through device-as-a-service bundles, while AI-powered predictive maintenance algorithms demonstrate measurable 15-37% energy savings that shorten payback periods for middle-income buyers. Standards consolidation around Matter further reduces vendor lock-in, lifting the final technical barrier that kept households from expanding beyond single-purpose gadgets.

Key Report Takeaways

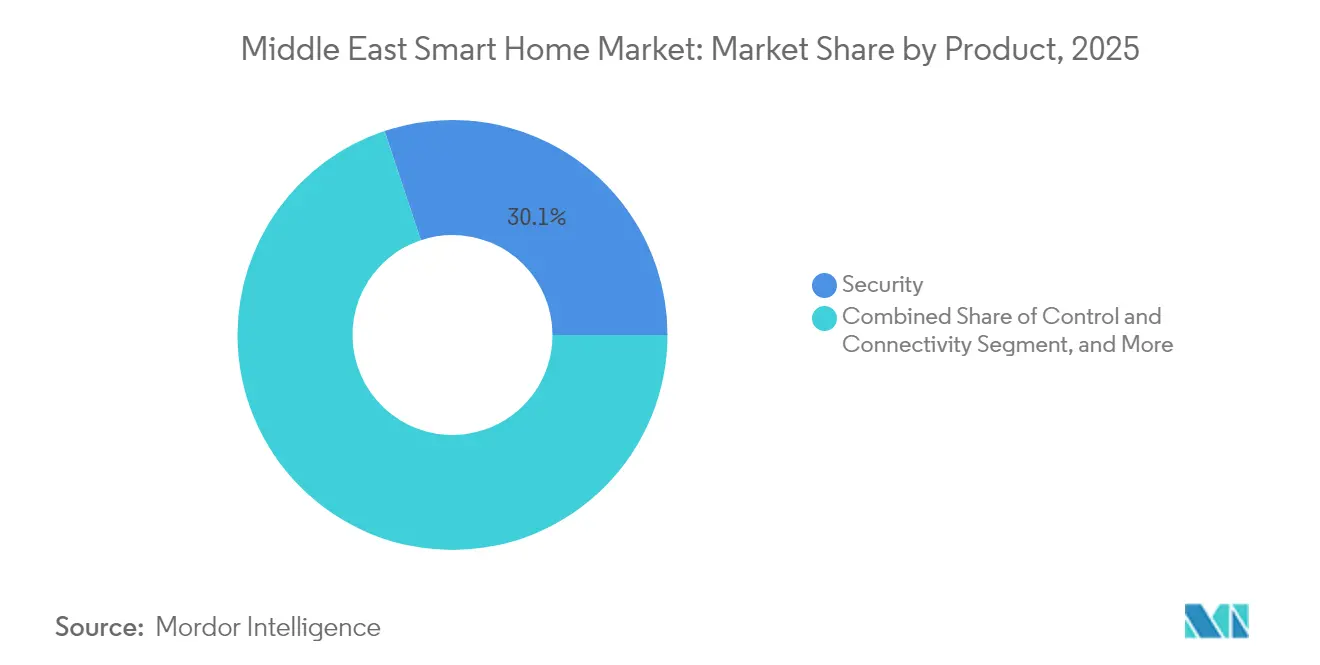

- By product category, security commanded 29.86% of 2025 revenue, while energy management is forecast to advance at a 19.13% CAGR through 2031.

- By connectivity technology, Wi-Fi held 57.21% of 2025 deployments, yet Matter is projected to grow at a 20.14% CAGR to 2031.

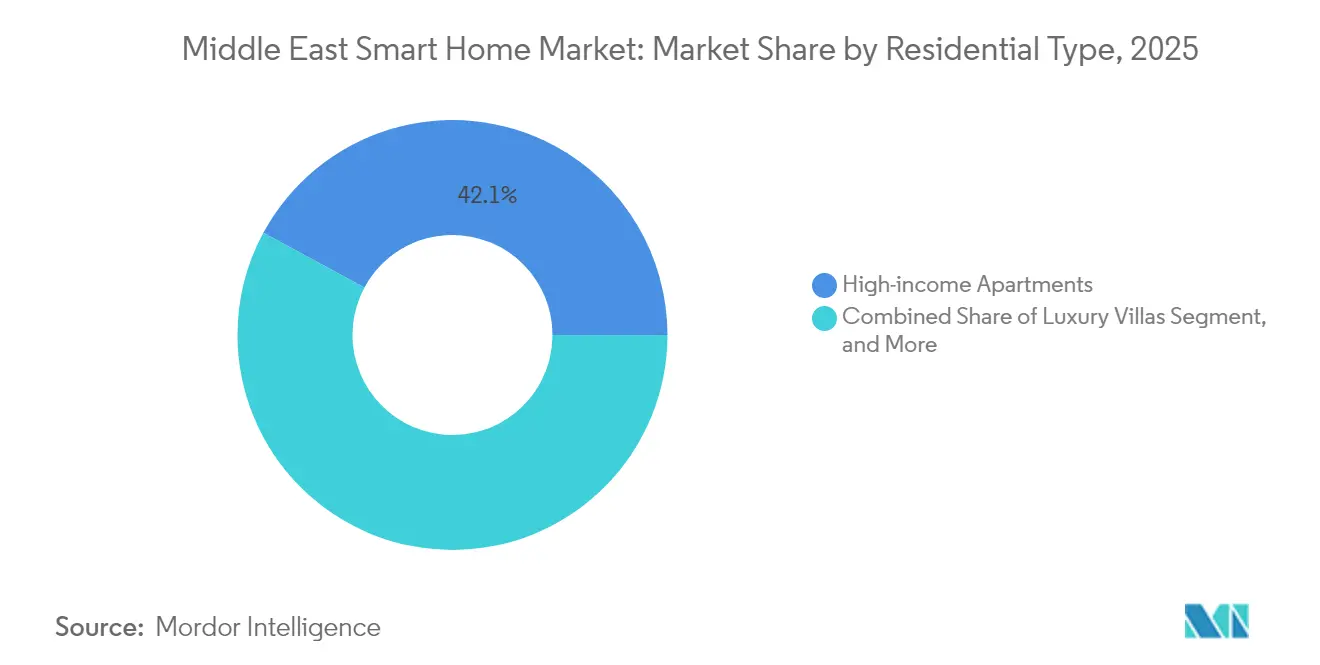

- By residential type, high-income apartments accounted for 42.63% of 2025 installations, whereas low-income housing is set to post a 19.43% CAGR to 2031.

- By sales channel, direct-to-consumer online purchases captured 38.12% of 2025 turnover, but telco bundled services are expected to accelerate at a 20.16% CAGR through 2031.

- By country, the United Arab Emirates led with 28.13% 2025 revenue, while Saudi Arabia is forecast to expand at a 19.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Vision 2030 Smart-City Initiatives | +5.2% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Rapid Deployment of 5G and Fibre Infrastructure | +4.1% | UAE, Saudi Arabia, Qatar, Kuwait | Medium term (2-4 years) |

| Real-Estate Developers Bundling Smart-Home Solutions | +3.3% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| AI-Powered Predictive Maintenance Reducing Energy Bills | +2.8% | Saudi Arabia, UAE, Turkey | Short term (≤ 2 years) |

| High Electricity Tariffs Driving Energy-Management Adoption | +2.1% | Saudi Arabia, UAE, Bahrain | Short term (≤ 2 years) |

| Converged Broadband-Wi-Fi Bundles From Telcos | +1.9% | UAE, Saudi Arabia, Qatar, Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Vision 2030 Smart-City Initiatives

Saudi Arabia and Qatar are recasting connected-home technology as a prerequisite for occupancy permits rather than an optional upgrade. NEOM specifies full-home automation for 9 million future residents, while Lusail City is wiring 650 000 IoT endpoints into a 24 hour command center that combines building management, district cooling, and residential automation in one stack. UAE pilots such as Msheireb Downtown Doha’s predictive analytics showcase pre-emptive fault detection that cuts operating costs and underpins green-building certifications. Developers that fail to meet GSAS or similar benchmarks face exclusion from public tenders, shifting competitive advantage toward platforms capable of seamless interoperability, long upgrade horizons, and embedded cybersecurity.

Rapid Deployment of 5G and Fiber Infrastructure

Fiber-to-the-home already covers 99.5% of UAE households, and Qatar’s near-total internet penetration enables high-bandwidth 4K video feeds, real-time HVAC optimization, and edge-based AI analytics. Saudi Arabia’s grid-of-microgrids architecture dovetails with smart meters to balance renewable generation and residential demand in real time. These dense networks lower latency, raise reliability, and drive down the marginal cost of connecting every new appliance, spurring adoption in adjacent markets such as EV-charger load management and behind-the-meter battery storage.

Real-Estate Developers Bundling Smart-Home Solutions

Leading Gulf developers negotiate volume contracts with vendors such as Siemens and Legrand to pre-install lighting control, energy dashboards, and security systems before handover. Volume procurement yields cost savings that are rolled into homeowners association fees, eliminating fragmented DIY installations and mitigating device incompatibility risks.[1]State Information Service, "PM reviews with Schneider Electric initiative to create 1,000 smart homes," sis.gov.eg Qatar’s mandate that every Lusail residence connect to the citywide management system further moves decision-making upstream to architects and master planners, forcing hardware suppliers to win design-phase specifications rather than compete on retail shelves.

AI-Powered Predictive Maintenance Reducing Energy Bills

Peer-reviewed studies confirm 15-37% electricity savings from AI-driven HVAC algorithms that learn occupancy patterns and tariff cycles. Voice assistants localized for Arabic commands, such as Amazon Alexa’s prayer-time automations, strengthen daily engagement and anchor households in proprietary ecosystems. Vendors are migrating intelligence from discrete devices to whole-home orchestration: GE Appliances now meshes panel-level load balancing with appliance-level insights, preventing costly breaker upgrades while maximizing solar and battery utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and Data-Privacy Concerns | -2.4% | UAE, Saudi Arabia, Qatar, Turkey | Short term (≤ 2 years) |

| Fragmented Technology Standards | -1.8% | Global, with acute impact in UAE and Saudi Arabia | Medium term (2-4 years) |

| Subsidised Utility Prices Reducing ROI | -1.2% | Kuwait, Bahrain, select Saudi regions | Medium term (2-4 years) |

| Limited Skilled-Installer Ecosystem in Secondary Cities | -0.9% | Turkey, Saudi Arabia (non-core cities), Rest of Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Data-Privacy Concerns

The UAE, Saudi Arabia, and Qatar now fine violators up to EUR 1.2 million (USD 1.3 million) for data-protection lapses, forcing vendors to embed end-to-end encryption and over-the-air patching as standard features. Academic audits still uncover router backdoors and unencrypted camera streams, keeping adoption cautious among high-net-worth users and government staff. Subscription fees for compliant cloud storage, such as Ring’s Premium tier, add to ownership costs and may slow upgrade cycles until economies of scale lower secure-cloud pricing.

Fragmented Technology Standards

Competing stacks—Wi-Fi, Zigbee, Z-Wave, Thread, and proprietary RF force consumers to juggle compatibility charts. Samsung’s SmartThings Home Dubai showcases localized routines such as Sandstorm Mode, but these remain proprietary to Samsung hardware.[2]Samsung Electronics, “Samsung Unveils SmartThings Home Dubai,” news.samsung.com Until Matter reaches critical mass, households will rely on multi-protocol hubs that add cost and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Security Leads, Energy Management Accelerates

Security systems captured 29.86% of 2025 revenue as gated communities demanded video doorbells, smart locks, and AI-enabled cameras. The Middle East smart home market size for security is projected to grow steadily, yet its share will dilute as households diversify into energy dashboards and comfort controls. Energy-management devices are set to post the fastest 19.13% CAGR through 2031, as predictive HVAC optimization and panel-level load orchestration lower electricity bills in tariff-reformed Gulf states. Vendors therefore bundle security with thermostats and smart plugs, converting one-off hardware sales into multi-service subscription ecosystems.

Second-generation entertainment hubs, white-goods integration, and tunable LED lighting now feed unified routines where, for instance, a motion-triggered camera activates corridor lights and prompts the thermostat to ease cooling in unoccupied zones. This convergence compels manufacturers either to open APIs or surrender share to platform players that can orchestrate cross-category experiences.

By Connectivity Technology: Wi-Fi Dominates, Matter Gains Momentum

Wi-Fi accounted for 57.21% of 2025 node connections due to the ubiquity of routers and the high bandwidth required for video feeds. However, congestion and power-draw disadvantages give Matter-over-Thread and Zigbee headroom for battery-operated sensors. Matter’s 20.14% projected CAGR reflects vendor commitments from Amazon, Google, Samsung, and Aqara, each adding compatibility layers that smooth consumer expansion paths. The growing Matter footprint will gradually boost the Middle East smart home market share of multi-vendor ecosystems while shrinking proprietary silos.

Multi-radio hubs remain crucial in the transition phase. They preserve backward compatibility, aggregate telemetry for AI engines, and allow over-the-air protocol upgrades that extend device lifespans a value proposition that resonates with price-sensitive Turkish and Bahraini buyers wary of orphaned hardware.

By Residential Type: High-Income Apartments Lead, Low-Income Housing Surges

Developer-installed ecosystems in luxury towers secured 42.63% of 2025 deployments, cementing high-income apartments as the single largest addressable pool. These units often include enterprise-grade KNX backbones and concierge dashboards that feed building-wide energy optimization. Meanwhile, government-subsidized initiatives such as Saudi Sakani and telco device-as-a-service models are tilting growth toward lower-income segments, propelling a 19.43% CAGR for smart-device penetration in entry-level housing.

Rising penetration in low-income brackets is redefining feature sets toward essential bundles—thermostats, leak sensors, and security cams—delivered through predictable monthly fees. Conversely, villa owners continue to pursue bespoke solutions that integrate irrigation, solar inverters, and gate automation, keeping custom integrators active in the premium tier of the Middle East smart home market.

By Sales Channel: Telco Bundles Narrow the Gap With Direct-to-Consumer

Direct-to-Consumer websites accounted for 38.12% of 2025 revenue, anchoring the largest Middle East smart home market share at the point of purchase where buyers consult peer reviews and benefit from next-day delivery. This channel remains price-competitive because global brands such as Ring launch region-specific models on Amazon.ae first, then syndicate the same listings to localized marketplaces that handle Arabic language support and warranty logistics. Mall-based retailers including Jumbo Electronics and Virgin Megastore complement online storefronts with live demonstration booths, which shorten the evaluation cycle for first-time buyers of multi-protocol hubs. Contractors and custom installers cater to luxury villas by integrating Crestron or KNX systems during construction, bundling long-term service contracts that raise average selling price but limit volume scalability. Despite this fragmentation, Direct-to-Consumer sites still captured the largest slice of the Middle East smart home market size in 2025, reflecting the region’s high broadband penetration and mobile-first shopping habits.

Telco Bundled Services are projected to expand at a 20.16% CAGR through 2031, closing the gap as operators fold smart-home devices into fiber subscriptions and amortize hardware costs over 24-month contracts. E&, STC and Ooredoo technicians now install routers, cameras and voice assistants during the same visit that activates gigabit fiber, enabling zero-touch provisioning and immediate app control. System integrators ride this wave by white-labeling their dashboards for telcos, while developers in megaprojects such as Lusail City embed telco-managed gateways behind the drywall so owners inherit a live ecosystem on handover. The financing convenience and bundled customer support inherent in this channel appeal to low- and middle-income households, propelling telcos toward leadership in new installations even as Direct-to-Consumer sites maintain the broadest catalog depth.

Geography Analysis

The United Arab Emirates accounted for 28.13% of 2025 revenue on the strength of its nationwide fiber backbone, rigorous data-protection law, and affluent consumer base. Amazon reported a 28% year-over-year rise in active Alexa users, aided by Arabic skill localization that reinforces daily engagement. Partnerships such as LG Electronics with Expo City Dubai show how marquee developments function as live demo grounds for next-gen living standards.

Saudi Arabia is forecast to log the region’s fastest 19.43% CAGR through 2031. Vision 2030 channels USD 1.8 trillion into infrastructure, including NEOM’s USD 500 billion zero-carbon metropolis where fully automated residences are the baseline. The grid-of-microgrids design enables real-time demand response, and local manufacturing incentives from entities like Schneider Electric suggest supply-chain localization will become a competitive advantage.

Qatar’s digital spend is set to reach USD 5.7 billion by 2026, with Lusail City integrating 650 000 endpoints into a single operating platform that manages district cooling, lighting, and in-home automation. High digital-infrastructure ratings and GSAS sustainability mandates create fertile ground for vendors that pass rigorous interoperability and cybersecurity audits. Secondary markets such as Bahrain and Kuwait trail in absolute size yet benefit from telco partnerships that bundle devices with fiber subscriptions, nudging adoption faster than pure retail models.

Competitive Landscape

Regional competition is intensifying as appliance giants, platform vendors and network operators jostle for ecosystem control. LG Electronics and Schneider Electric formed a Gulf-wide alliance in July 2025 to mesh LG ThinQ appliances with the EcoStruxure KNX backbone, targeting mandatory building-efficiency codes that reward whole-home load orchestration.[3]MENAFN, "LG Electronics And Schneider Electric Partner To Drive The Future Of Smart Home Automation," menafn.com The partnership gives LG access to Schneider’s installer network, while Schneider gains differentiated content for its energy dashboards, illustrating how hardware-plus-software bundles can satisfy municipal procurement rules that favor open protocols over closed vertical stacks.

Telecommunications operators are emerging as de-facto systems integrators. eand’s Device-as-a-Service plans fold cameras, smart plugs and AI speakers into monthly fiber bills, lifting recurring revenue and slashing churn as customers grow dependent on a unified mobile app. STC and Ooredoo mirror the model, sourcing white-label hubs from Asian ODMs that support Wi-Fi, Zigbee and Matter out of the box, then layering Arabic voice skills on top to lock subscribers into localized ecosystems. This telco push compresses margins for standalone gadget brands, which now compete not only on hardware features but also on the ability to integrate with operator billing and customer-support back ends.

Niche players still capture value by solving vertical problems. GE Appliances integrated ABB’s ReliaHome Smart Panel with its SmartHQ app in February 2025, creating panel-level load balancing that utilities can tap for demand-response incentives. Aqara’s Matter-compatible Panel Hub S1 Plus, unveiled at CES 2025, positions the firm as a protocol bridge for households unwilling to abandon older Zigbee sensors. Yet the absence of any vendor exceeding a 10% regional share indicates a market still open to disruption by players that pair certified cybersecurity, energy-saving proof points and frictionless installation at scale.

Middle East Smart Home Industry Leaders

-

Schneider Electric SE

-

Honeywell International Inc.

-

ABB Ltd.

-

Johnson Controls International plc

-

Google LLC (Nest)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ring launched AI-powered Smart Video Search in the UAE, enabling natural-language queries for archived footage.

- November 2025: LG Electronics Gulf partnered with Expo City Dubai to deploy integrated smart-city and smart-home solutions.

- October 2025: Eand UAE and Honeywell agreed to deliver 5G-enabled, AI field solutions for small and medium businesses.

- September 2025: LG Electronics secured a data-center cooling deal for NEOM, aligning with its residential automation ambitions.

Middle East Smart Home Market Report Scope

A smart home uses internet-connected devices to enable remote management and automation of household systems such as lighting, heating, security, and entertainment. These devices, which can be controlled via smartphones, tablets, or voice assistants, communicate with each other to optimize energy usage, enhance convenience, and improve security. The integration of IoT technology allows for seamless interaction and personalized control, making everyday tasks more efficient and convenient.

The Middle East Smart Home Market Report is Segmented by Product (Comfort and Lighting, Control and Connectivity, Energy Management, Home Entertainment, Security, Smart Appliances), Connectivity Technology (Wi-Fi, Bluetooth, Zigbee, Z-Wave, Thread, Matter, Other Technologies), Residential Type (Luxury Villas, High-Income Apartments, Middle-Income Apartments, Low-Income Housing), Sales Channel (Direct-to-Consumer Online, Retail Brick-and-Mortar, Contractors and Installers, System Integrators, Telco Bundled Services), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Turkey, Kuwait, Bahrain, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

| Comfort and Lighting |

| Control and Connectivity |

| Energy Management |

| Home Entertainment |

| Security |

| Smart Appliances |

| Wi-Fi |

| Bluetooth |

| Zigbee |

| Z-Wave |

| Thread |

| Matter |

| Other Technologies |

| Luxury Villas |

| High-Income Apartments |

| Middle-Income Apartments |

| Low-Income Housing |

| Direct-to-Consumer (Online) |

| Retail (Brick-and-Mortar) |

| Contractors and Installers |

| System Integrators |

| Telco Bundled Services |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Turkey |

| Kuwait |

| Bahrain |

| Rest of Middle East |

| By Product | Comfort and Lighting |

| Control and Connectivity | |

| Energy Management | |

| Home Entertainment | |

| Security | |

| Smart Appliances | |

| By Connectivity Technology | Wi-Fi |

| Bluetooth | |

| Zigbee | |

| Z-Wave | |

| Thread | |

| Matter | |

| Other Technologies | |

| By Residential Type | Luxury Villas |

| High-Income Apartments | |

| Middle-Income Apartments | |

| Low-Income Housing | |

| By Sales Channel | Direct-to-Consumer (Online) |

| Retail (Brick-and-Mortar) | |

| Contractors and Installers | |

| System Integrators | |

| Telco Bundled Services | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current size and growth outlook for the Middle East smart home market?

The market stands at USD 12.53 billion in 2026 and is forecast to reach USD 29.73 billion by 2031, reflecting an 18.86% CAGR.

Which product category is growing the fastest?

Energy-management devices are projected to rise at a 19.13% CAGR as tariff reforms and AI-driven HVAC optimization shorten payback periods.

How are telcos influencing adoption?

Operators such as eand and STC bundle devices with fiber plans, offer zero-touch provisioning, and shift costs to monthly fees, driving a 20.16% CAGR for bundled channels.

Why is Matter important for regional consumers?

Matter unifies connectivity across brands, reducing incompatibility issues and enabling households to expand ecosystems without vendor lock-in.

What are the key cybersecurity requirements in Gulf markets?

UAE, Saudi Arabia, and Qatar mandate end-to-end encryption, over-the-air patching, and substantial fines up to USD 1.3 million for non-compliance, elevating secure-by-design solutions.

Which country will contribute most incremental revenue by 2031?

Saudi Arabia, helped by Vision 2030 megaprojects and the Sakani subsidy program, is expected to add the largest absolute gains to regional revenue.

Page last updated on: