Smart Home Hub Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

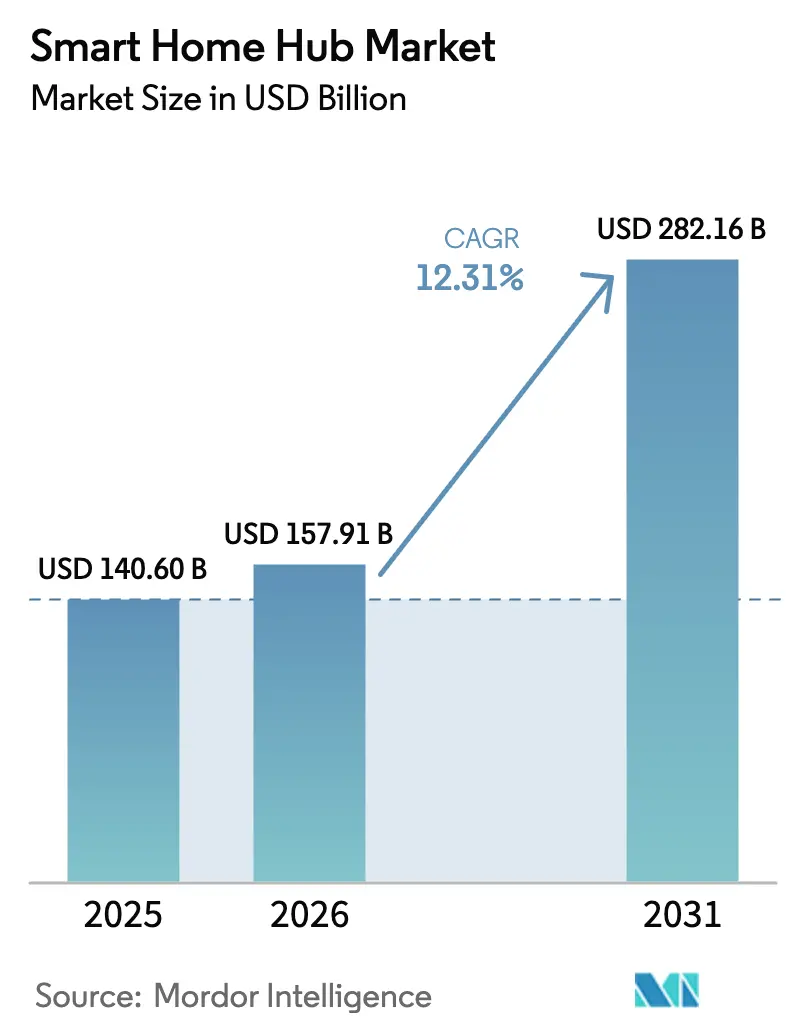

| Market Size (2026) | USD 157.91 Billion |

| Market Size (2031) | USD 282.16 Billion |

| Growth Rate (2026 - 2031) | 12.31% CAGR |

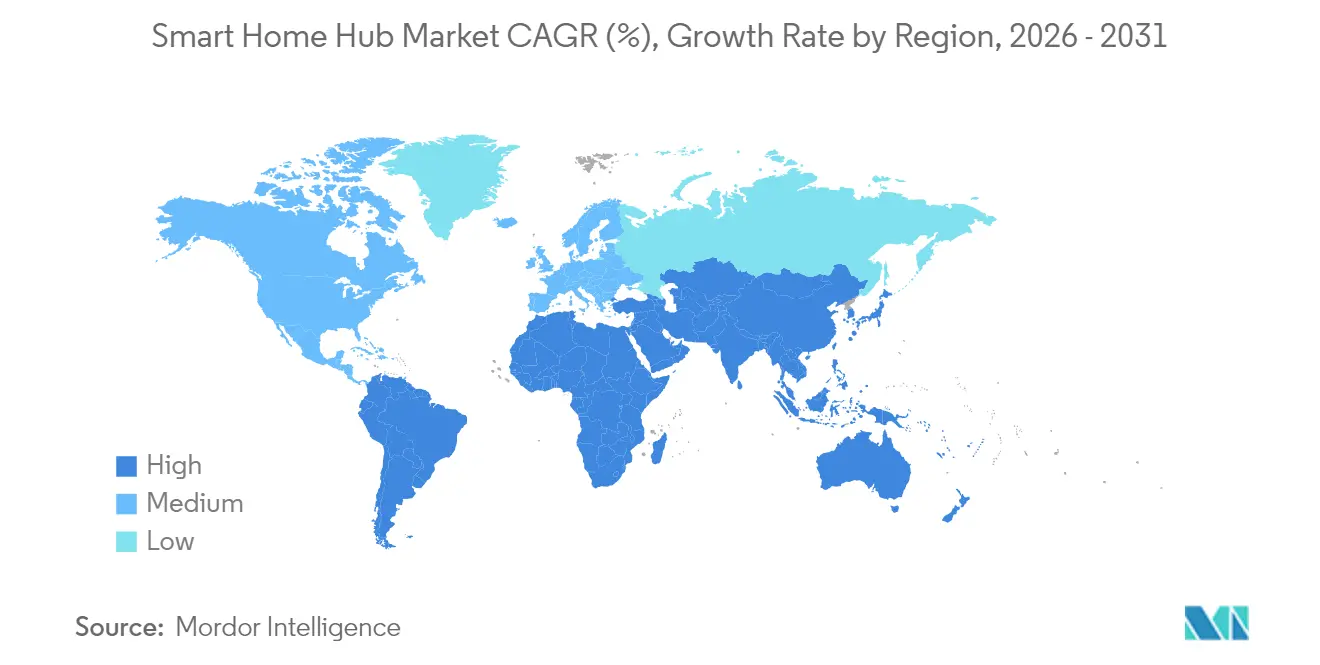

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Home Hub Market Analysis by Mordor Intelligence

smart home hub market size in 2026 is estimated at USD 157.91 billion, growing from 2025 value of USD 140.6 billion with 2031 projections showing USD 282.16 billion, growing at 12.31% CAGR over 2026-2031. Robust growth is tied to three converging forces: mass-market voice–assistant penetration, Matter/Thread interoperability, and utility-backed energy-management bundles that collectively lower adoption friction and raise perceived value. Platform-centric hubs command the largest revenue share because their ecosystems turn each device addition into a stickier user experience, while edge-AI hubs are scaling fastest as consumers seek on-device inference and lower latency. Regionally, North America remains the revenue leader thanks to an installed base of more than 600 million Alexa devices, but Asia-Pacific is accelerating on the back of government digital-infrastructure programs and local manufacturing scale. On the competitive front, Amazon, Google, Apple, Samsung, and Xiaomi continue to add generative-AI features that make contextual automation a must-have rather than a differentiator. Cost headwinds tied to lithium supply and EU e-waste directives are partially offset by falling Wi-Fi/BLE chipset ASPs and insurance-backed premium discounts.

Key Report Takeaways

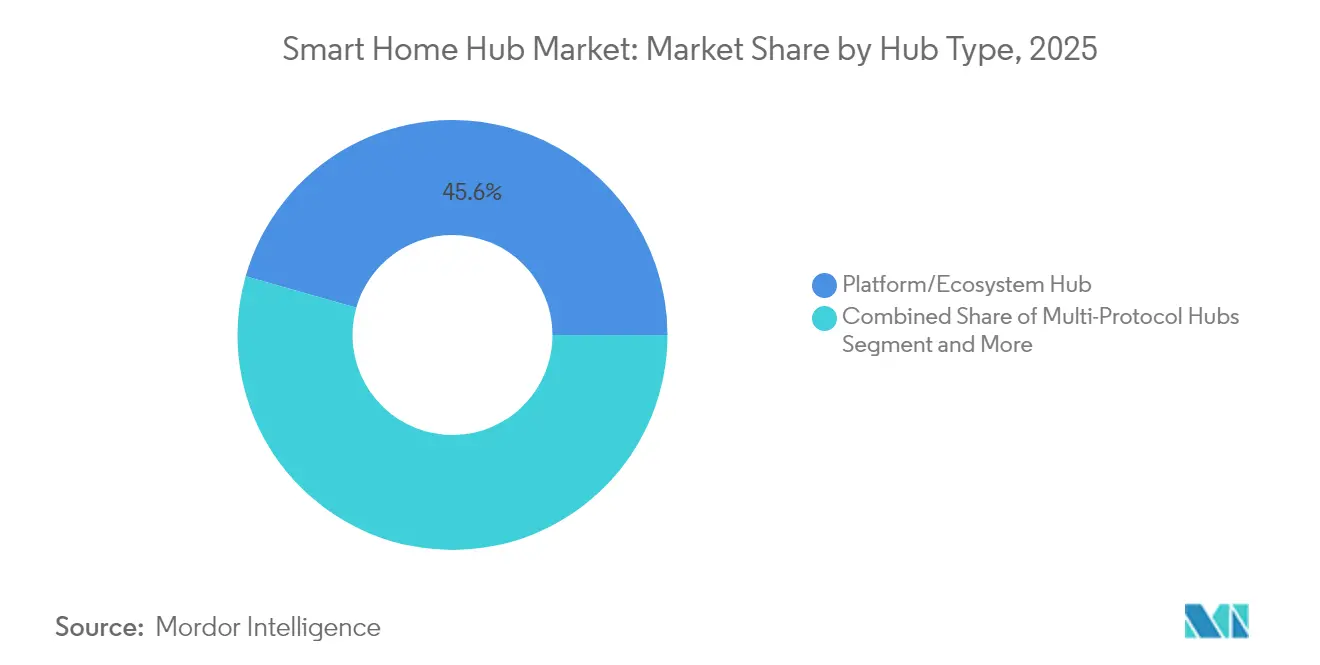

- By hub type, Platform/Ecosystem hubs held 45.60% of the smart home hub market share in 2025, while Edge-AI-enabled hubs are projected to grow at an 17.92% CAGR through 2031.

- By connection technology, Wi-Fi captured 52.40% revenue share in 2025; Thread/Matter is on track for a 16.98% CAGR to 2031.

- By control interface, Voice-only hubs led with 60.20% share in 2025, whereas hybrid voice-plus-display interfaces are advancing at 16.87% CAGR.

- By application, Security and Access Control accounted for a 37.50% slice of the smart home hub market size in 2025; Energy and HVAC Management is forecast to expand at a 16.45% CAGR.

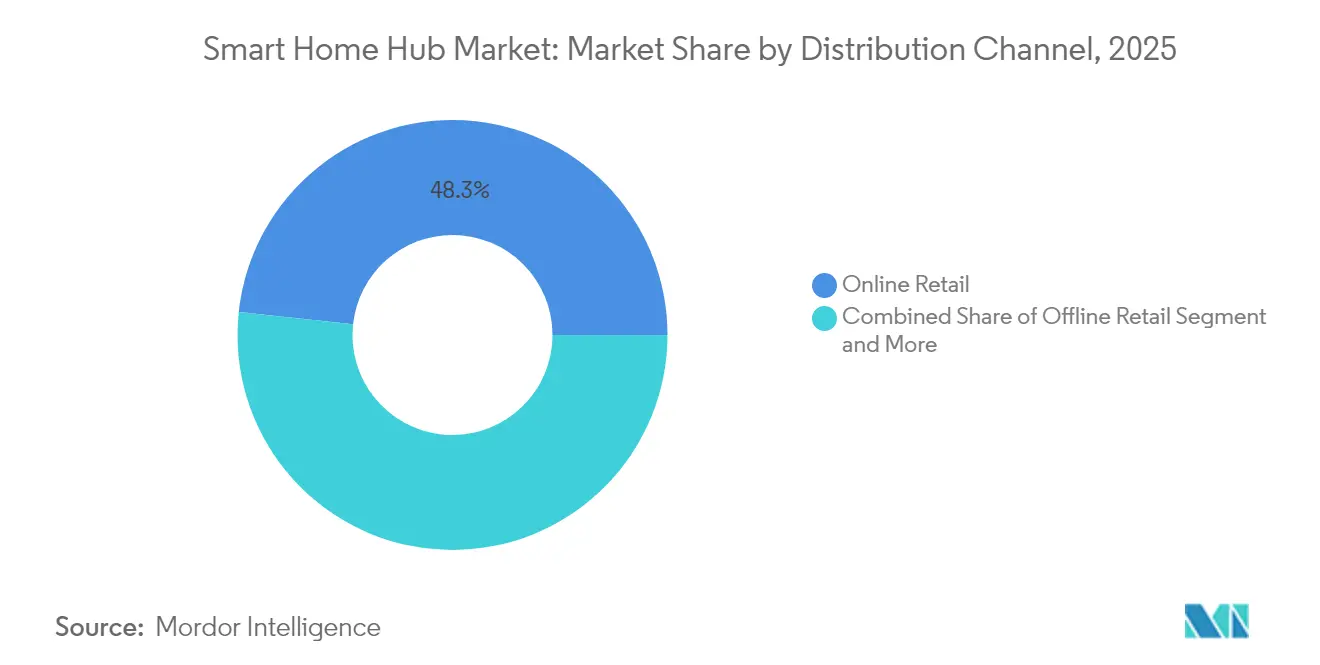

- By distribution channel, Online retail represented 48.30% of 2025 sales, while service-provider bundles are rising at a 14.84% CAGR.

- By end user, Residential single-family homes held 54.30% of the smart home hub market size in 2025; assisted-living and healthcare settings will post 18.76% CAGR growth through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Home Hub Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Mass-market voice-assistant adoption surge | +2.8% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Proliferation of Matter/Thread interoperability | +2.1% | Global, strongest in North America and APAC | Long term (≥ 4 years) |

| Bundled energy-management programs from utilities | +1.9% | North America and Europe core, expanding to APAC | Medium term (2-4 years) |

| Falling ASPs for Wi-Fi/BLE chipsets | +1.4% | Global, with cost benefits concentrated in APAC manufacturing | Short term (≤ 2 years) |

| Insurance-backed smart-hub discounts | +0.8% | North America and Europe, pilot programs in APAC | Medium term (2-4 years) |

| Generative-AI-based contextual automation | +1.2% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mass-market voice-assistant adoption surge

Amazon has surpassed 600 million Alexa devices, and Alexa+ now layers generative AI onto voice control, lifting consumer expectations for natural interaction and proactive automation.[1]Andy Jassy, “Amazon CEO Andy Jassy’s 2024 Letter to Shareholders,” aboutamazon.comThe migration from app-centric to conversational control reduces friction, fuels replacement cycles, and embeds platform lock-in. Google Cloud’s 28% year-over-year jump shows the infrastructure lift behind real-time speech processing. Each additional device enlarges network effects, translating into higher ARPU and upsell opportunities.

Proliferation of Matter/Thread interoperability

The May 2024 release of Matter 1.3 added automation scenes and energy-metering commands, resolving many early reliability gaps.[2]Mark Trayer, “CSA Releases Matter 1.3 Specification,” Samsung Research, research.samsung.com Router-level Thread upgrades slated for 2025 promise plug-and-play onboarding, which in turn lowers support costs and broadens the smart home hub market. Open standards diminish proprietary moats but channel innovation toward edge compute and service layers.

Bundled energy-management programs from utilities

Carrier and Google Cloud are packaging AI-driven HVAC hubs that store energy off-peak and feed demand-response markets, illustrating how utilities can turn residences into virtual power plants.[3]Carrier Global Corporation, corporate.carrier.com These programs create recurring service revenue, slash consumer bills, and reinforce the smart home hub market’s value proposition amid rising grid-reliability concerns.

Falling ASPs for Wi-Fi/BLE chipsets

Volume scaling and shorter process nodes are pushing dual-band Wi-Fi/BLE solutions into sub-USD 3 ranges, enabling even entry-level hubs to support multiple protocols. The 2024 quartz-mine disruption in Spruce Pine, however, exposed supply-chain fragility for RF filters. Price declines shift differentiation toward software, AI, and ecosystem reach.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent data-privacy breaches and hacking | -1.8% | Global, with strongest regulatory responses in Europe | Short term (≤ 2 years) |

| Protocol fragmentation beyond Matter 1.3 | -1.4% | Global, particularly affecting cross-ecosystem integration | Medium term (2-4 years) |

| Rising e-waste regulations limiting refresh cycles | -0.9% | Europe leading, expanding to North America and APAC | Long term (≥ 4 years) |

| Lithium-shortage driven battery-backup cost spikes | -0.7% | Global, with manufacturing concentrated in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent data-privacy breaches and hacking

Academic work calls for meta-assistants that give users granular control after a run of high-profile IoT hacks. Reputational scars slow adoption and raise compliance overhead—particularly under Europe’s GDPR and California’s CCPA.

Protocol fragmentation beyond Matter 1.3

Many legacy Z-Wave or Zigbee devices lack upgrade paths, forcing dual-stack hubs and bloating BOM costs. Consumer confusion raises return rates, dampening near-term growth until universal firmware bridges mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hub Type: Ecosystem Platforms Maintain Lead

Platform/Ecosystem hubs generated 45.60% of 2025 revenue. Their deep service integration—from music to shopping—locks users in and drives repeat spend. Edge-AI units are scaling at 17.92% CAGR, adding on-device inference that appeals to privacy-conscious buyers and regions with patchy broadband. Conversely, “bridge” multi-protocol nodes cushion legacy device owners during the Matter transition. Security-centric hubs retain loyal installer channels but must now fold in AI analytics to stay relevant. The smart home hub market size for Edge-AI units is projected to swell notably as voice-assistant latency falls below 100 milliseconds, proving the value of silicon upgrades. Meanwhile, platform hubs defend a 45-plus smart home hub market share percentage by bundling photo storage, streaming, and cloud backups.

Second-order effects are reshaping supplier power. Silicon vendors now court firmware partners to differentiate tensor-compute blocks, while cloud giants pre-install subsidy coupons to keep churn low. Hardware margins compress, but lifetime value grows via premium skills, device-health monitoring, and subscription security feeds.

By Connection Technology: Wi-Fi Dominance Under Siege

Wi-Fi held 52.40% of 2025 shipments thanks to router ubiquity and falling 6E chipset costs. Yet Thread/Matter combos will record a 16.98% CAGR as battery devices pivot to low-power mesh topologies. The smart home hub market size tied to Thread radios will double by 2030, unlocking hubless device models that rely on always-on border routers. Zigbee remains stable in LED and meter retrofits, while proprietary Z-Wave clings to pro-installer niches. For vendors, multi-stack RF front-ends add bill-of-materials pressure but open upsell paths toward energy dashboards and occupancy analytics.

Interoperability progress is also recasting certification economics. CSA’s logo now appears next to Wi-Fi, driving co-marketing synergies. At the same time, Bluetooth LE Audio piggybacks on hub processors to enable spatial-audio alerts, stretching use cases beyond utility-centric functions.

By Control Interface: Voice Pivots to Hybrid

Voice-only hubs represented 60.20% of shipments in 2025, but hybrid units—combining microphones, LCDs, and motion sensors—are forecast to climb 16.87% CAGR. Visual feedback solves setup pain points and supports glanceable energy or security tiles. Touch-display niches persist in assisted living, where large fonts and tactile cues aid accessibility. Mobile-app-only bridges cater to retrofit dwellings or renters scared off by installation. Over the period, voice latency improvements below 70 milliseconds and speaker diarization will enhance multi-occupant experiences. As a result, the smart home hub industry will see UX budgets migrate from static dashboards to conversational design toolkits.

Developers, meanwhile, embrace multi-modal SDKs to create once-build-everywhere experiences. This reduces fragmentation and lowers support tickets, nudging ROI upward for independent software vendors.

By Application: Security Peaks, Energy Ascends

Security and Access Control ruled 2025 with 37.50% share, driven by insurer rebates and robust burglary-deterrence marketing. Yet Energy and HVAC Management is the star performer through 2031, climbing 16.45% CAGR as utilities roll out real-time pricing and carbon-intensity APIs. The smart home hub market share for energy-specific SKUs will likely double, bolstered by federal tax credits and virtual-power-plant pilots. Entertainment and Lighting bundles retain entry-level appeal but face commodity pricing. Elderly-care stacks intertwine fall detection, vitals monitoring, and caregiver alerts, winning grants under aging-in-place programs.

Regulatory carrots amplify these shifts: Europe’s Fit-for-55 plan and U.S. DOE’s demand-flexibility initiatives offer hubs a seat in grid services. In parallel, AI-powered anomaly detection reframes hubs as preventive-maintenance sentinels, slashing HVAC downtime.

By Distribution Channel: Bundles Reshape Go-to-Market

Online retail still booked 48.30% of 2025 revenue, but telco and utility bundles will grow 14.84% CAGR after 5G fixed-wireless ISPs pre-install hubs for churn reduction. Professional integrators upsell SMBs on centralized dashboards, while big-box stores court DIYers via demo kiosks. For OEMs, channel mix diversification improves cash-flow predictability; however, it also demands tailored SKUs—white-label for telcos, margin-lite for e-commerce, and feature-rich for pro channels.

Data-sharing agreements emerge as currency: utilities want anonymized load data, insurers want incident telemetry, and platforms want behavioral cues. Success therefore hinges on flexible consent frameworks and modular API exposure.

By End User: Assisted-Living Growth Outpaces Core Residential

Single-family homes held 54.30% of 2025 spend, but demographic shifts push assisted-living to 18.76% CAGR as fall-detection, medication reminders, and remote vitals caretaking reduce staffing costs. Multi-family adoption lags due to tenant churn and retrofit complexity, though landlord-level bulk installs are rising in rent-controlled metros seeking amenities differentiation. Hospitality leverages hubs for occupancy-based HVAC and mobile-key tie-ins, while SMB retail chains deploy hubs for integrated security and energy savings.

Government pilots under Japan’s Society 5.0 and EU’s Ageing Well directives funnel grants toward elderly-care ecosystems, reinforcing demand. In turn, OEMs partner with medical-device makers to secure HIPAA-compliant cloud connectors.

Geography Analysis

North America retained 39.40% share in 2025, underpinned by high broadband penetration and more than 600 million Alexa devices in circulation. Utility demand-response programs and insurer rebates enhance ROI, while state-level privacy statutes inject compliance complexity. Apple’s USD 7.5 billion Wearables, Home and Accessories haul in Q2 2025 underscores premium appetite. Ongoing lithium and quartz supply scares remain the wild card for hub BOM stability, but U.S. CHIPS-Act-funded fabs could offset some dependence on imported semiconductors.

Competitive Landscape

The smart home hub market displays moderate concentration: the top five firms held roughly 58% of 2024 shipments, translating to a market-concentration score of 6. Amazon leads by leveraging Prime, Alexa Skills, and low-cost Echo hardware, while Google differentiates through Gemini-powered contextual services and Nest’s energy-partner integrations. Apple monetizes privacy-first positioning and tight vertical integration, recording USD 95.4 billion in Q2 2025 revenue with a sizable share from HomePod and Apple TV hubs.

Samsung rides SmartThings and Matter evangelism, embedding hubs in TVs and appliances. Xiaomi capitalizes on cost leadership and retail expansion, spending RMB 16.6 billion on R&D in 2024 to bridge smartphones, EVs, and home devices. Smaller specialists—Homey, Hubitat, and Aqara—target power users with local-first automation and granular rule engines. Telcos, led by Comcast and SoftBank, bundle white-label hubs into broadband for stickiness.

Strategic moves center on AI and services. Google’s 2025 revamp folded the Gemini app team into device engineering to shorten feature rollouts. Amazon expanded same-day shipping for home hubs, trimming delivery costs and boosting attach rates. Carrier and Google Cloud’s HVAC hub collaboration shows vertical integration into energy services. EU compliance is catalyzing second-life battery ecosystems, prompting Samsung to trial refurb programs in Germany. M&A watchlists include chipset vendors with low-power AI accelerators and software startups specializing in privacy-preserving analytics.

Smart Home Hub Industry Leaders

Samsung SmartThings

Google LLC (Google Nest)

Amazon.com, Inc. (Amazon Echo)

Apple Inc.

Xiaomi Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Carrier and Google Cloud unveil AI-powered Home Energy Management Systems that integrate battery-enabled HVAC units with WeatherNext forecasting to bolster grid resilience.

- March 2025: Xiaomi tops CNY 104.1 billion in 2024 IoT & lifestyle revenue and accelerates offline retail to anchor its Human × Car × Home strategy.

- January 2025: Samsung, Apple, Google, and Amazon implement Matter 1.3, extending support to water-control and energy-reporting devices.

- December 2024: Apple reports a 60% carbon-emission cut over 10 years, buoyed by USD 7.5 billion Wearables, Home & Accessories sales.

Global Smart Home Hub Market Report Scope

Smart home hubs are the central command for home automation networks, facilitating smooth communication and control among connected devices. These hubs, whether connected locally or via the cloud, are crucial for Internet of Things (IoT) devices. They utilize protocols like Zigbee, Z-Wave, or Bluetooth, moving beyond Wi-Fi reliance. This study monitors the revenue from hardware and software solutions that link smart home devices. Additionally, it examines growth trends and macroeconomic factors influencing the market.

The smart home hub market segments include type (multi-protocol hubs and platform/ecosystem hubs), connection type (Zigbee, Z-Wave, Wi-Fi, and Bluetooth), and geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and the Middle East and Africa). Market sizes and forecasts are presented in USD value for each segment.

| Platform / Ecosystem Hubs |

| Multi-Protocol Hubs |

| Edge-AI-Enabled Hubs |

| Security-Focused Hubs |

| Wi-Fi |

| Zigbee |

| Z-Wave |

| Thread / Matter |

| Bluetooth / BLE |

| Voice-Only |

| Touch-Display |

| Mobile-App-Only |

| Hybrid |

| Security and Access Control |

| Energy and HVAC Management |

| Entertainment and Lighting |

| Elderly Care and Health Monitoring |

| Online Retail |

| Offline Retail |

| Service-Provider Bundled |

| Professional Installer / Integrator |

| Residential - Single Family |

| Residential - Multi-Family |

| Hospitality |

| Assisted-Living / Healthcare |

| Commercial - SMB |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Hub Type | Platform / Ecosystem Hubs | |

| Multi-Protocol Hubs | ||

| Edge-AI-Enabled Hubs | ||

| Security-Focused Hubs | ||

| By Connection Technology | Wi-Fi | |

| Zigbee | ||

| Z-Wave | ||

| Thread / Matter | ||

| Bluetooth / BLE | ||

| By Control Interface | Voice-Only | |

| Touch-Display | ||

| Mobile-App-Only | ||

| Hybrid | ||

| By Application | Security and Access Control | |

| Energy and HVAC Management | ||

| Entertainment and Lighting | ||

| Elderly Care and Health Monitoring | ||

| By Distribution Channel | Online Retail | |

| Offline Retail | ||

| Service-Provider Bundled | ||

| Professional Installer / Integrator | ||

| By End-User | Residential - Single Family | |

| Residential - Multi-Family | ||

| Hospitality | ||

| Assisted-Living / Healthcare | ||

| Commercial - SMB | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the smart home hub market?

The smart home hub market is valued at USD 157.91 billion in 2026 and is projected to hit USD 282.16 billion by 2031 at a 12.31% CAGR.

Which hub type generates the most revenue today?

Platform/Ecosystem hubs lead with 45.60% revenue share, owing to their integrated voice-assistant and service ecosystems.

Why is Asia-Pacific the fastest-growing region?

Government digital-infrastructure funding, cost-efficient manufacturing, and rising middle-class demand drive a 14.36% regional CAGR.

What application segment will grow fastest through 2031?

Energy & HVAC Management, expanding at 16.45% CAGR, thanks to utility demand-response programs and real-time pricing.

How are e-waste regulations impacting product design

EU directives mandate removable batteries and digital product passports, pushing manufacturers toward modular, durable hub designs.

Which companies dominate the competitive landscape

Amazon, Google, Apple, Samsung, and Xiaomi collectively control about 58% of global shipments, leveraging ecosystem breadth and AI innovation.

Page last updated on: