United Arab Emirates Data Center Cooling Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

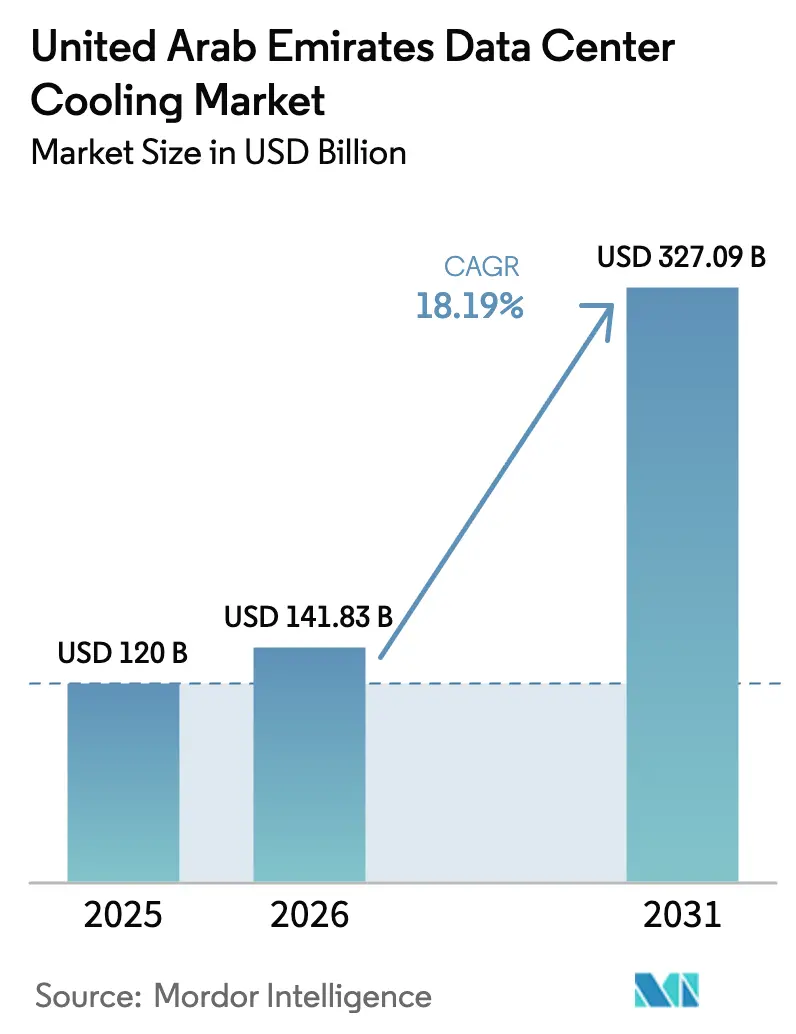

| Base Year Market Size (2025) | USD 120 Billion |

| Market Size (2026) | USD 141.83 Billion |

| Market Size (2031) | USD 327.09 Billion |

| Growth Rate (2026 - 2031) | 18.19% CAGR |

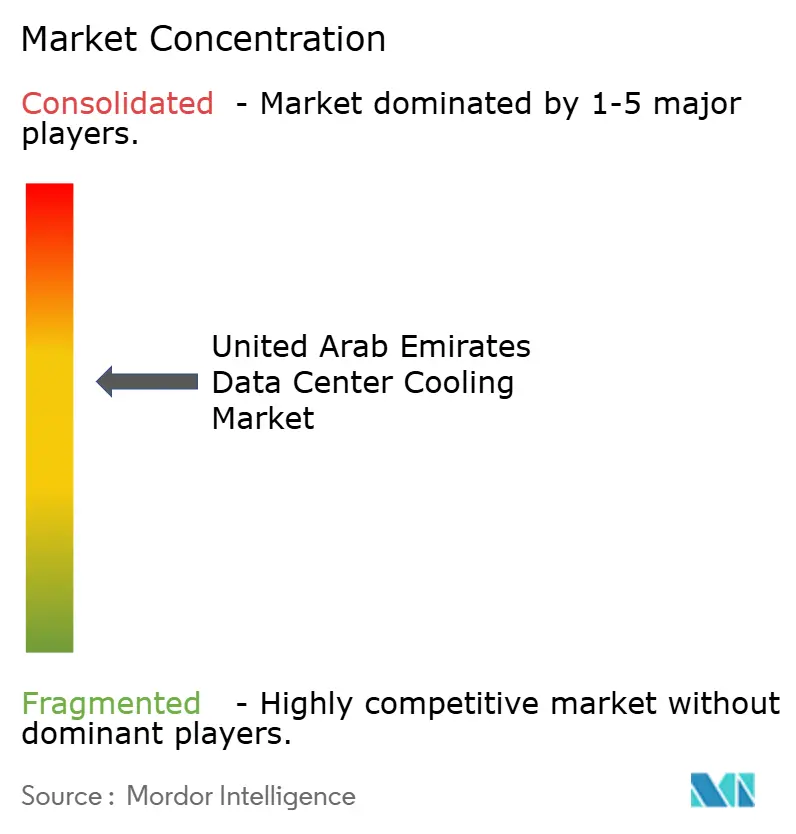

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Data Center Cooling Market Analysis by Mordor Intelligence

The UAE data center cooling market size in 2026 is estimated at USD 141.83 million, growing from 2025 value of USD 120 million with 2031 projections showing USD 327.09 million, growing at 18.19% CAGR over 2026-2031. This nation-level expansion reflects the Emirates’ strategy of becoming the digital heart of the Middle East, a goal that demands robust cooling infrastructure to safeguard mission-critical workloads against ambient temperatures that often exceed 45 °C. Tiered regulatory instruments—chiefly the Dubai Universal Blueprint for Artificial Intelligence, unveiled in 2024—set efficiency thresholds that force data-center operators to transition from conventional air systems to liquid-based solutions capable of maintaining power-usage-effectiveness (PUE) targets below 1.2. Hyperscalers’ 5 GW UAE-US AI Campus in Abu Dhabi exemplifies this shift, creating large-scale demand for liquid cooling and modular prefabricated plants that can be installed rapidly on constrained plots. At the same time, the federal Climate Change Reduction Law, effective May 2025 intensifies scrutiny over greenhouse-gas emissions, prompting operators to integrate district cooling tie-ins and renewable-powered free-cooling loops to achieve compliance and unlock tariff incentives. These policy levers, coupled with the escalating heat load from artificial-intelligence (AI) chipsets, position the UAE data center cooling market for sustained double-digit expansion throughout the forecast horizon.

Key Report Takeaways

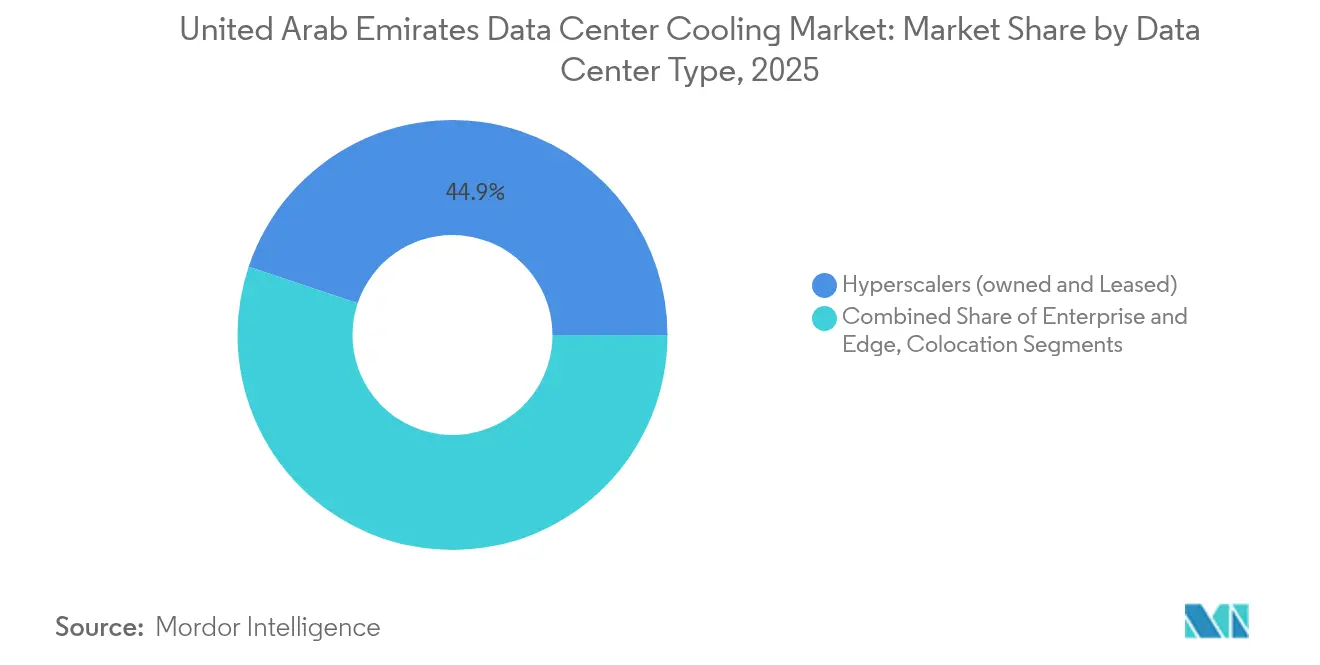

- By data center type, hyperscalers captured 44.85% of UAE data center cooling market share in 2025 and are on track to expand at a 19.18% CAGR through 2031.

- By tier type, Tier 3 facilities held 62.55% of UAE data center cooling market share in 2025, whereas Tier 4 is projected to rise fastest at an 18.45% CAGR to 2031.

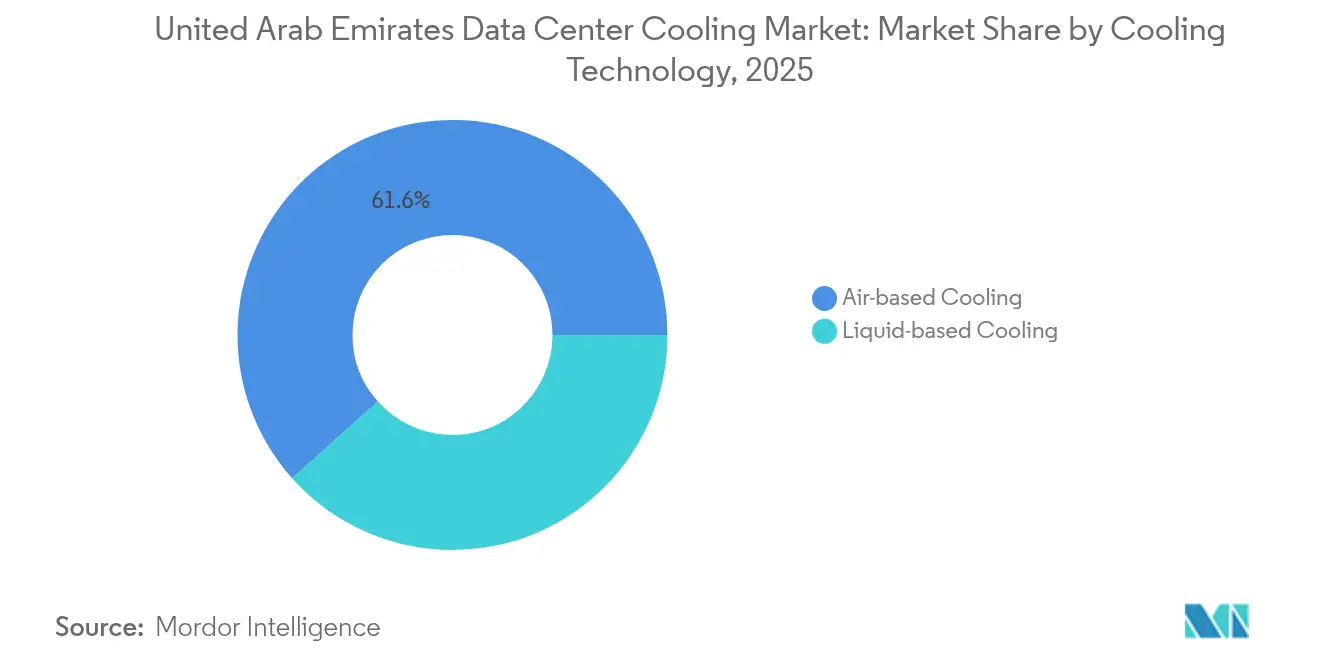

- By cooling technology, air-based systems accounted for 61.60% share of UAE data center cooling market size in 2025, while liquid solutions are forecast to grow at 18.82% CAGR.

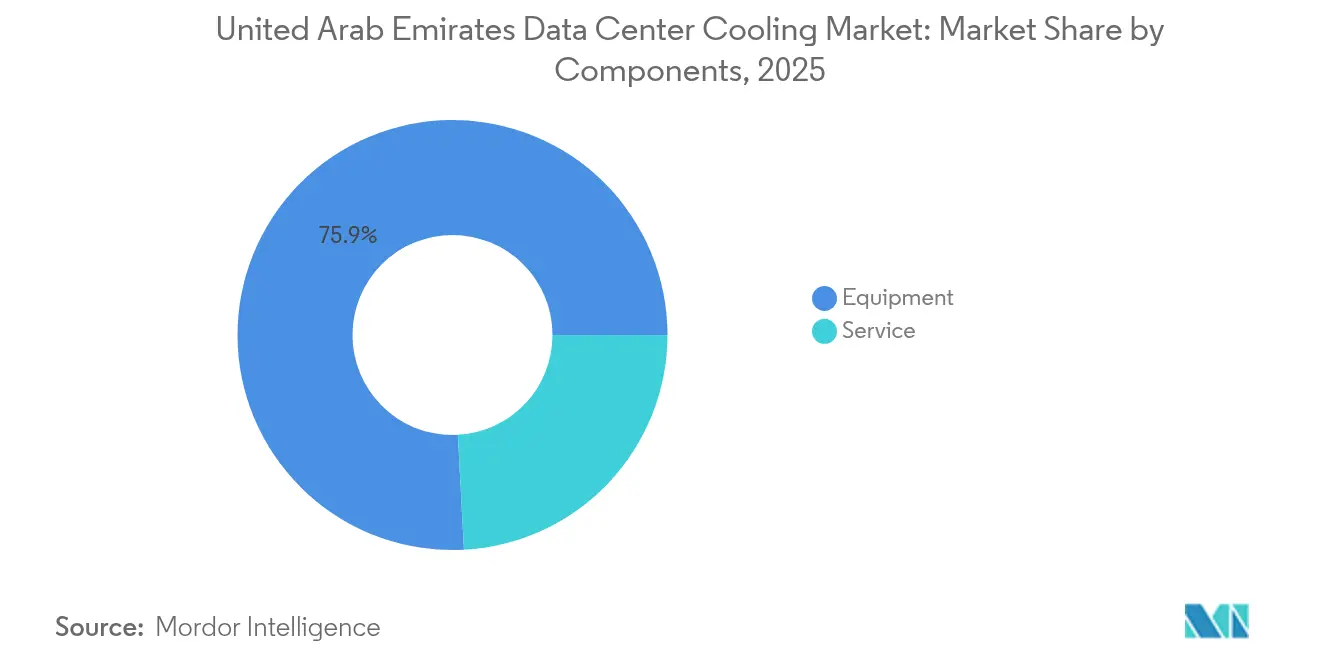

- By component, equipment sales represented 75.85% share of UAE data center cooling market size in 2025, with services advancing at an 18.21% CAGR as complexity intensifies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Data Center Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital-transformation mandates accelerating hyperscale builds | +4.2% | UAE (Dubai, Abu Dhabi) | Medium term (2-4 years) |

| Cloud-first strategies among UAE enterprises | +3.8% | UAE, spillover to GCC | Short term (≤ 2 years) |

| Mandatory PUE efficiency targets from 2025 | +3.1% | UAE nationwide | Short term (≤ 2 years) |

| District-cooling tie-ins lowering lifecycle costs | +2.7% | Dubai & Abu Dhabi urban cores | Medium term (2-4 years) |

| AI/HPC density spike requiring liquid-cooling retrofits | +3.9% | UAE hyperscale & enterprise | Short term (≤ 2 years) |

| Renewable-linked tariff incentives favoring indirect free-cooling | +2.1% | Solar-park zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digital-Transformation Mandates Accelerating Hyperscale Builds

Government mandates stemming from the Dubai Universal Blueprint for Artificial Intelligence compel data-center operators to exceed legacy thermal specifications, driving adoption of immersion and direct-to-chip cooling that sustain rack densities above 40 kW while meeting PUE targets under 1.2. Projects such as the 5 GW UAE-US AI Campus in Abu Dhabi and Khazna’s 100 MW AI-optimized facility in Ajman establish a nationwide baseline that private data centers must match to stay competitive.[1]G42, “Khazna Ajman AI-Optimized Facility Fact Sheet,” g42.ai As these public-sector anchors demonstrate compliance, hyperscale tenants intensify procurement of specialized liquid-cooling modules, accelerating the broader UAE data center cooling market’s migration away from chilled-water CRAHs and into sealed dielectric systems.

Cloud-First Strategies Among UAE Enterprises

Enterprise migration to cloud platforms is reshaping cooling demand by concentrating workloads in a handful of large sites rather than dispersed on-premise server rooms. UAE enterprises already contribute 12% of the country’s non-oil GDP via digital activities, a figure expected to grow to 20% by 2030, fueling cumulative demand for hyperscale facilities equipped with energy-efficient cooling. Microsoft’s USD 544 million partnership with du to build an Abu Dhabi region underscores the trend, as the facility deploys modular coolant distribution units to accommodate enterprise workloads shifting from legacy data centers. For cooling OEMs, enterprise cloud-first agendas translate into longer-term service contracts tied to outcome-based performance metrics, lifting service revenue within the UAE data center cooling market.

Mandatory PUE Efficiency Targets from 2025

Dubai’s directive to cut energy intensity by 30% by 2030, in tandem with the federal Climate Change Reduction Law, establishes legal accountability for every kilowatt consumed in IT halls and mechanical rooms. Operators must now disclose emissions in annual filings, incentivizing rapid rollouts of immersion baths and rear-door heat exchangers that can sustain PUE scores close to 1.05. LiquidStack’s Hong Kong reference site—posting a 1.02 PUE—illustrates the high-water mark many UAE builds aim to replicate in desert conditions.[2] LiquidStack, “Case Study: Immersion Cooling PUE 1.02,” liquidstack.com Compliance pressure is creating a two-tier vendor landscape, where solution providers with proven sub-1.2 PUE track records command price premiums, while traditional air-cooled systems risk marginalization.

District-Cooling Tie-ins Lowering Lifecycle Cooling Costs

Dubai’s bulk cooling utility Empower, operating 1.55 million refrigeration tons (RT), enables data-center tenants to rent chilled water instead of building on-site chiller plants, trimming up-front capital outlays and smoothing peak load on the UAE grid. District connections cut data-center cooling energy by up to 50%, deliver redundancy via thermal-energy-storage tanks, and satisfy a growing pool of ESG investors scrutinizing water consumption metrics. Facilities Management Middle East reports Empower’s unmanned Jumeirah Village Circle plant stores 10,000 RT-hours nightly, displacing daytime compressor runs and improving grid stability. Consequently, site-selection teams increasingly prioritize plots located within walking distance of district loops, giving Dubai and Abu Dhabi a strategic edge over interior regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for advanced systems in desert climate | −2.8% | UAE inland zones | Medium term (2-4 years) |

| Refrigerant phase-down compliance complexity | −1.9% | UAE nationwide | Short term (≤ 2 years) |

| Scarcity of liquid-cooling-skilled technicians | −2.3% | UAE urban hubs | Medium term (2-4 years) |

| Water-use restrictions on evaporative towers | −1.7% | Water-scarce emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Advanced Systems in Desert Climate

Desert temperatures often breach 45 °C, compelling operators to invest in corrosion-resistant exchangers, oversized heat-rejection loops, and particulate filters that add up to a 40% premium over temperate-zone designs.[3] Global supply-chain bottlenecks for large-diameter coolant manifolds further inflate costs, stretching lead times for 1 MW coolant distribution units beyond 12 months. Operators must therefore weigh higher depreciation schedules and maintenance budgets against long-run energy savings, slowing some capital-spending decisions.

Scarcity of Liquid-Cooling-Skilled Technicians

Immersion baths and direct-to-chip loops demand specialized training in dielectric handling, seal integrity, and coolant quality, yet the UAE’s HVAC labor pool remains steeped in legacy chilled-water practices. Data Center Frontier notes that fewer than 300 liquid-cooling-certified engineers serve the entire GCC market, creating bottlenecks for commissioning new pods and constraining post-installation support. Iceotope’s 2024 launch of the first dedicated liquid-cooling lab aims to bridge this talent gap by providing certification pathways for thermal-management technicians. Until these programs scale, manpower scarcity will temper uptake rates for advanced cooling within the UAE data center cooling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscalers Drive Cooling Innovation

Hyperscalers owned or leased in the UAE captured 44.85% of UAE data center cooling market share in 2025 and are forecast to grow at 19.18% CAGR to 2031, reflecting sizable expansions such as Microsoft’s USD 544 million region with du. This cohort’s push toward sub-1.2 PUE thresholds underpins robust demand for immersion baths and coolant distribution units, turning the hyperscaler slice into the prime revenue generator for OEMs. Enterprise and edge sites collectively account for less than one-third of UAE data center cooling market size, yet their disparate workloads necessitate modular racks that blend air and liquid loops, opening a consultation-heavy opportunity set for services vendors.

Hyperscalers’ preference for high-density racks exceeding 40 kW is propelling vertical integration, wherein operators design proprietary immersion tanks to bypass the limitations of airborne heat transfer. The surge forces equipment suppliers to standardize quick-disconnect manifolds and leak-proof busways that reduce downtime during GPU swap-outs. Edge facilities, typically located in telecom exchange buildings, embrace sealed rear-door heat exchangers to conserve floor area. Across customer archetypes, the unrelenting rise in AI traffic cements liquid cooling’s role as the UAE data center cooling market’s fastest-growing technology stack.

By Tier Type: Tier 4 Drives Premium Cooling Demand

Tier 3 halls held 62.55% of UAE data center cooling market share in 2025 due to balanced redundancy and cost profiles, while Tier 4 footprints are climbing at 18.45% CAGR on the back of hyperscale leasing commitments that stipulate concurrent maintainability across cooling plants. Tier 1 and Tier 2 rooms remain niche, mostly serving latency-sensitive edge deployments where cost control supersedes 99.995% uptime promises.

Tier 4 designs incorporate 2N cooling redundancy, automated valve sequencing, and predictive analytics that model coolant quality in real time. Abu Dhabi Municipality’s Tier-IV certified disaster-recovery build, running Huawei FusionModule2000 prefabricated pods, illustrates the capital intensity required to guarantee no single point of cooling failure. Tier 3 operators typically opt for N+1 chiller arrays—lowering initial spend but retaining resilience through spare capacity. This tier stratification motivates cooling OEMs to bundle tier-specific service agreements, thereby monetizing advanced diagnostics while keeping mean-time-to-repair below contractual thresholds.

By Cooling Technology: Liquid Cooling Disrupts Traditional Market

Air-based chillers, CRAH units, and economizers still command 61.60% of UAE data center cooling market size in 2025, yet immersion and direct-to-chip solutions are advancing at 18.82% CAGR, propelled by AI racks generating heat fluxes unsustainable for air alone. Liquid cooling’s superior thermal conductivity enables facilities to eliminate raised floors and fans, shrinking mechanical PUE contribution from 35% to under 10% in best-practice builds.

Microsoft’s global two-phase immersion rollouts, achieving 5%–15% power savings and zero water consumption in cooling, spotlight the sustainability gains that resonate with UAE regulators. Rear-door heat exchangers form a bridge technology for mixed workloads, allowing operators to delay full immersion conversions while still meeting incremental PUE targets. Meanwhile, air solutions evolve toward adiabatic free-coolers paired with UV filtration to combat desert particulates, illustrating that legacy platforms retain relevance via iterative enhancements even as liquid systems capture incremental spend.

By Component: Services Growth Reflects Complexity Increase

Equipment sales absorbed 75.85% of UAE data center cooling market size in 2025, yet services revenue is growing faster at 18.21% CAGR as operators outsource design, installation, and predictive maintenance for unfamiliar liquid technologies. Engineering-procurement-construction (EPC) firms report a 20% year-over-year rise in demand for turnkey coolant-loop commissioning packages.

Installation teams now integrate vibration-free dielectric pumps, leak-detection fiber ribbons, and BAS-compatible smart valves, deepening overall project scope and pulling consultancy into earlier design stages. After deployment, service contracts link fees to uptime and PUE compliance, incentivizing vendors to invest in remote-monitoring centers staffed by thermal analytics specialists. This evolution realigns the UAE data center cooling industry’s business model from hardware transfer to lifecycle performance delivery.

Geography Analysis

Dubai remains the nucleus of UAE data center cooling market activity, buoyed by 99% internet penetration and business-friendly free-zones that attract cloud regions demanding scalable cooling. Empower’s 1.55 million-RT district network enables data-center developers to forego capital-intensive chiller yards, instead tapping pre-chilled supply loops that trim OPEX and expedite building permits. The emirate’s stacked skyscraper footprint impels operators to adopt vertical immersion tanks that conform to high-rise floorplates, an architectural quirk that favors prefabricated modules.

Abu Dhabi’s AI concentration presents a complementary growth axis. The 5 GW UAE-US AI Campus and Khazna’s 100 MW Ajman build pull cooling innovation toward two-phase immersion baths rated for 1,500 W chips. Renewable integration gives Abu Dhabi a cost advantage: the world’s largest solar-powered data center at Mohammed bin Rashid Al Maktoum Solar Park relies on indirect free-cooling loops exploiting nighttime desert temperature drops. These geographic synergies produce a corridor of liquid-cooling demand stretching from Dubai Marina to the Al Dhafra desert.

Competitive Landscape

The UAE data center cooling market remains moderately fragmented. Global stalwarts Schneider Electric, Vertiv, and Stulz leverage broad product lines and service networks yet confront disruptive entrants specializing in immersion and direct-to-chip solutions. Schneider Electric fortified its position by acquiring Motivair Corporation in October 2024, adding high-capacity coolant distribution units to its EcoStruxure stack. Vertiv answers with MegaMod CoolChip, a prefabricated, liquid-ready pod designed for 50% faster deployment cycles and PUE gains of up to 25%.

Specialists such as LiquidStack, Submer, and Iceotope anchor the vanguard by demonstrating sub-1.1 PUE operations and 95% reductions in cooling energy versus legacy air architectures. Partnerships bridge the divide: Munters and ZutaCore co-develop sealed evaporative-liquid hybrids for AI racks, while Iceotope collaborates with Schneider Electric and Avnet to embed dielectric tanks in OEM-grade containers. Market leadership will increasingly hinge on service depth namely, the capacity to furnish 24/7 remote diagnostics, immersion-fluid quality testing, and warranty-backed uptime commitments rather than merely hardware availability.

United Arab Emirates Data Center Cooling Industry Leaders

Stulz GmbH

Asetek A/S

Schneider Electric SE

Vertiv Group Corp.

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: du and Microsoft signed a USD 544 million contract for an Abu Dhabi hyperscale region equipped with immersion-ready cooling infrastructure.

- March 2025: ADQ and ECP launched a USD 25 billion venture to expand power generation for data centers, ensuring sufficient electricity for high-density liquid cooling.

- January 2025: OpenAI partnered with UAE entities to construct “Stargate UAE,” a 1 GW AI cluster in Abu Dhabi, requiring liquid cooling to handle 200 MW of initial capacity.

- November 2024: Vertiv and Compass Datacenters introduced CoolPhase Flex, a hybrid air-liquid system targeting 400 W GPUs.

United Arab Emirates Data Center Cooling Market Report Scope

Data center cooling is a system that helps maintain optimal operating temperatures in data center environments. It is critical, as data center facilities house many computer servers and network equipment that generate heat during operation. Efficient cooling systems are used to dissipate this heat and prevent equipment from overheating, ensuring continued reliable operation of the data center. Methods such as air conditioning, liquid cooling, and hot/cold aisle containment are commonly used to control temperature and humidity in data centers.

The UAE data center cooling market is segmented by technology (air-based cooling [chiller and economizer, CRAH, cooling towers, and other air-based cooling technologies] and liquid-based cooling [immersion cooling, direct-to-chip cooling, and rear-door heat exchanger]), type of data center (hyperscale, enterprise, and colocation), and end-user industry (it and telecom, retail and consumer goods, healthcare, media and entertainment, federal and institutional agencies, and other end-user industries). The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Hyperscalers (owned and Leased) |

| Enterprise and Edge |

| Colocation |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Air-based Cooling | Chiller and Economizer (DX Systems) |

| CRAH | |

| Cooling Tower (covers direct, indirect and two-stage cooling) | |

| Others | |

| Liquid-based Cooling | Immersion Cooling |

| Direct-to-Chip Cooling | |

| Rear-Door Heat Exchanger |

| By Service | Consulting and Training |

| Installation and Deployment | |

| Maintenance and Support | |

| By Equipment |

| By Data Center Type | Hyperscalers (owned and Leased) | |

| Enterprise and Edge | ||

| Colocation | ||

| By Tier Type | Tier 1 and 2 | |

| Tier 3 | ||

| Tier 4 | ||

| By Cooling Technology | Air-based Cooling | Chiller and Economizer (DX Systems) |

| CRAH | ||

| Cooling Tower (covers direct, indirect and two-stage cooling) | ||

| Others | ||

| Liquid-based Cooling | Immersion Cooling | |

| Direct-to-Chip Cooling | ||

| Rear-Door Heat Exchanger | ||

| By Component | By Service | Consulting and Training |

| Installation and Deployment | ||

| Maintenance and Support | ||

| By Equipment | ||

Key Questions Answered in the Report

What is the current value of the UAE data center cooling market?

The market is valued at USD 141.83 million in 2026, reflecting rapid infrastructure expansion linked to hyperscale and AI projects.

How fast is the UAE data center cooling market expected to grow?

It is forecast to advance at an 18.19% CAGR between 2026 and 2031, reaching USD 327.09 million by the end of the period.

Which cooling technology is growing fastest in the UAE?

Liquid cooling—encompassing immersion and direct-to-chip approaches is growing at 18.82% CAGR due to AI workloads that exceed air-cooling thermal limits.

What challenges hinder adoption of advanced cooling in the UAE?

High capital costs for desert-grade equipment and a shortage of technicians trained in liquid cooling slow deployment despite clear efficiency gains.

Page last updated on: