Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

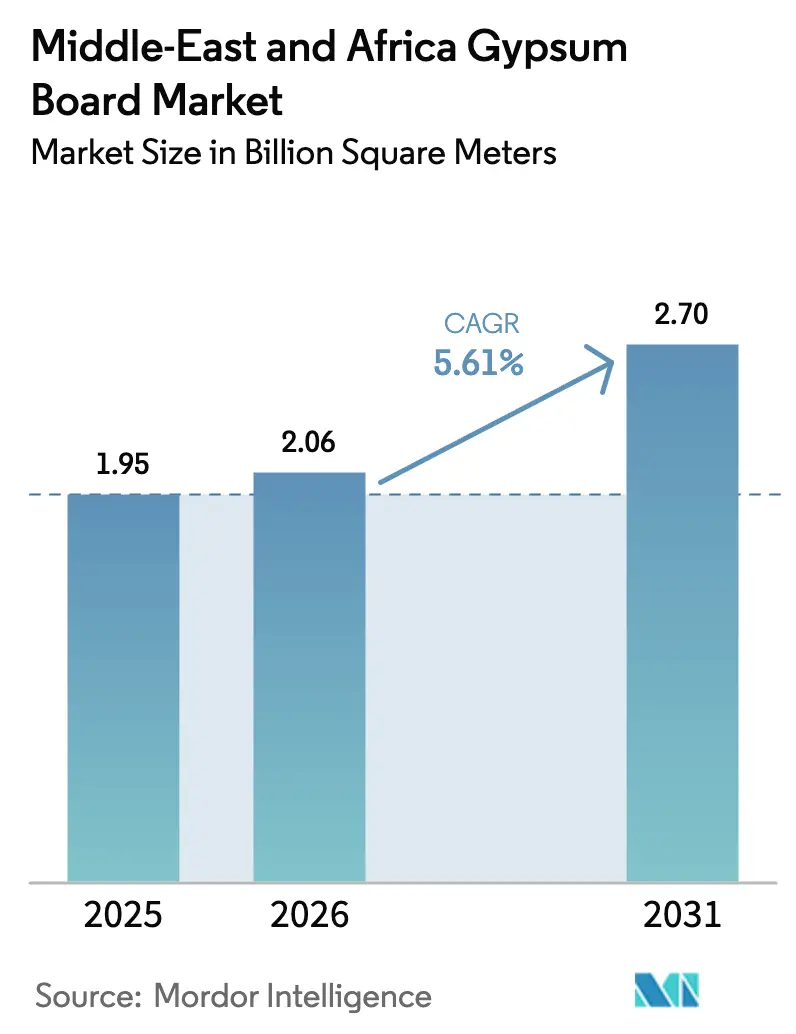

| Base Year Market Size (2025) | 1.95 Billion square meters |

| Market Volume (2026) | 2.06 Billion square meters |

| Market Volume (2031) | 2.70 Billion square meters |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

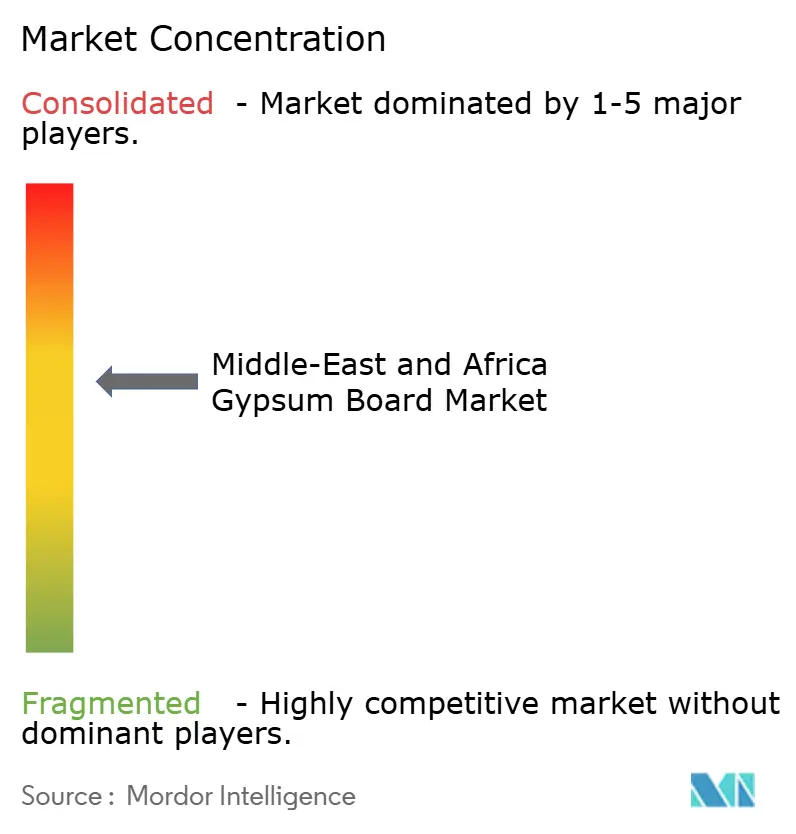

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Gypsum Board Market Analysis by Mordor Intelligence

The Middle-East And Africa Gypsum Board Market size is expected to grow from 1.95 Billion square meters in 2025 to 2.06 Billion square meters in 2026 and is forecast to reach 2.70 Billion square meters by 2031 at 5.61% CAGR over 2026-2031. This trajectory shows that government-backed mega-projects, green-building mandates, and a pivot toward off-site fabrication are lifting structural demand beyond ordinary construction cycles. Rapid hotel and resort build-outs in Saudi Arabia, the United Arab Emirates, and Qatar have made fire-rated and moisture-resistant drywall a default interior solution because it installs faster than wet plaster and reduces labor on site. Distributors also report double-digit growth in factory-finished panels that align with modular production lines now required on development programs such as NEOM, New Murabba, and the Red Sea Project. Further downstream, e-commerce fulfillment centers in Nigeria, Egypt, and the Gulf free zones are setting tighter occupancy deadlines, so contractors are abandoning blockwork for lightweight partitions that can be relocated when logistics layouts change. At the same time, natural-gypsum leases in Oman and Saudi Arabia protect the cost base of vertically integrated manufacturers, allowing them to hold margins even when energy or freight costs spike.

Key Report Takeaways

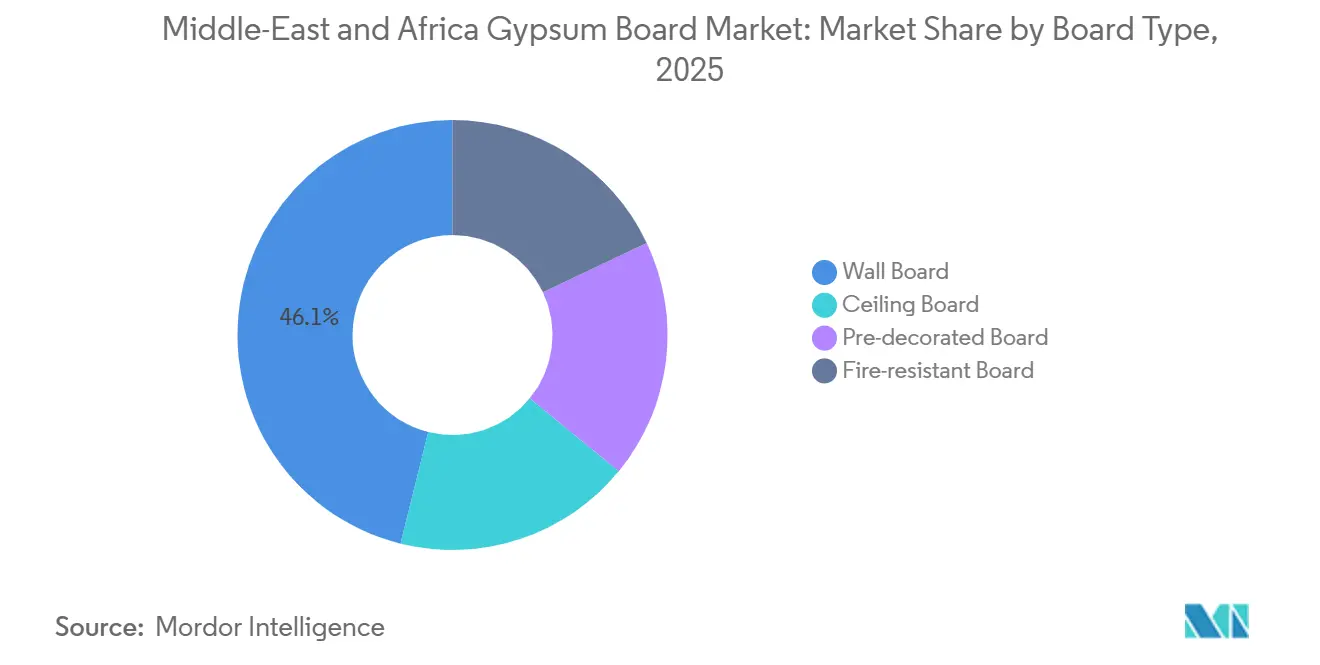

- By board type, wall board led with 46.12% of the Middle-East and Africa gypsum board market share in 2025, while fire-resistant board recorded the highest growth at a 6.68% CAGR through 2031.

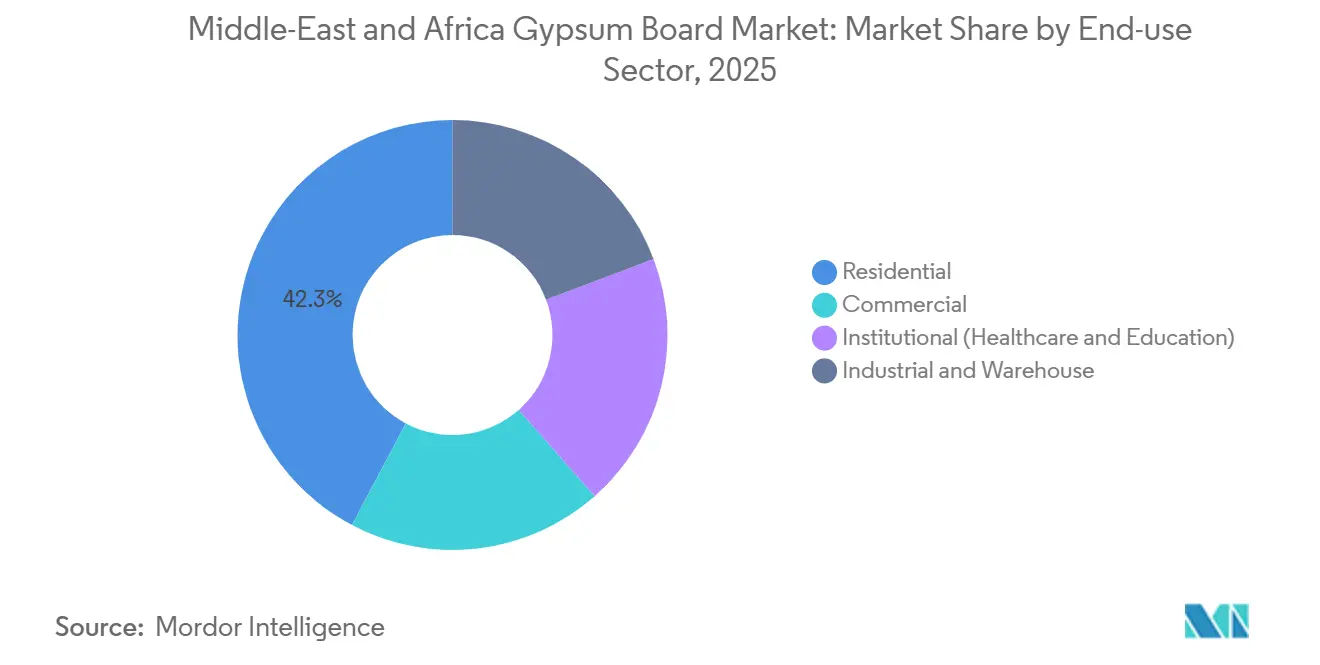

- By end-use sector, residential construction accounted for 42.25% of the Middle-East and Africa gypsum board market size in 2025, whereas the industrial and warehouse segment is advancing at a 6.23% CAGR to 2031.

- By geography, Saudi Arabia held 35.10% of the regional volume in 2025, and Nigeria is projected to expand at a 6.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle-East And Africa Gypsum Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Funded Pipeline Megaprojects in Saudi Arabia and UAE | +1.8% | Saudi Arabia, UAE, with spillover to Qatar | Medium term (2-4 years) |

| Tourism-Led Demand for Drywall Fit-Outs in GCC Hospitality Assets | +1.2% | GCC core (Saudi Arabia, UAE, Qatar, Bahrain), emerging in Oman | Medium term (2-4 years) |

| Fast-Track Prefab and Modular Construction Uptake Across MEA | +1.0% | Saudi Arabia, UAE, South Africa; pilot adoption in Egypt, Nigeria | Long term (≥ 4 years) |

| Mandated Energy-Efficient Building Codes | +0.9% | UAE, Saudi Arabia, Qatar; gradual rollout in Egypt, Kenya | Short term (≤ 2 years) |

| Circular-Economy Push for Gypsum Recycling and Synthetic Gypsum Quotas | +0.4% | UAE, Saudi Arabia (policy frameworks emerging); limited near-term impact in Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Funded Pipeline Megaprojects in Saudi Arabia and UAE

Massive sovereign programs exceeded USD 55 billion in awarded contracts during the first three quarters of 2023 and have locked in phased delivery schedules that rely on standardized, lightweight partitions for faster close-out. NEOM alone mandates factory-made interior wall assemblies for roughly 30% of its residential units, pulling board demand forward several years. The Red Sea Project, New Murabba, and Qiddiya add millions of square meters of ultra-fast-track floor area, and Dubai 2040 is layering commercial towers, schools, and health-care facilities on an already deep pipeline. Developers opt for fire-rated drywall because it satisfies new GCC test standards without adding structural weight, a critical concern in high-rise design. Lenders and insurers now embed these standards into covenants, effectively institutionalizing demand for specialty boards across the Middle-East and Africa gypsum board market.

Tourism-Led Demand for Drywall Fit-Outs in GCC Hospitality Assets

Qatar welcomed 4 million visitors in 2025, a surge that has prompted a QAR 10 billion (USD 2.75 billion) hotel funding plan and raised the bar for rapid refurbishments. The Wynn Resort on Al Marjan Island in Ras Al Khaimah is scheduled for early 2027 opening and alone requires more than 150,000 square meters of fire-resistant drywall in guestrooms and back-of-house corridors. Vision 2030 aims for 100 million annual visitors to Saudi Arabia, which translates into roughly 500,000 new hotel keys; each room carries an average of 150 square meters of board when corridors and amenity areas are included. Project teams favor pre-decorated and moisture-resistant panels because they compress punch-list cycles and minimize downtime during periodic upgrades. These specifications lock premium-priced, high-performance SKUs into work-breakdown structures, underpinning year-round shipments in the Middle-East and Africa gypsum board market.

Fast-Track Prefab and Modular Construction Uptake Across MEA

Modular school buildings in Cape Town cut schedules by 60% and achieved 30% cost savings, proving that off-site fabrication can unlock margins even in price-sensitive markets. JAFZA’s Logistics Park Phase 2 in Dubai wrapped 360,000 square feet of warehouse space in less than nine months by integrating large-format gypsum boards into precast wall panels. NEOM extends this model, requiring modular delivery on a gigascale, so board suppliers that co-locate near panel yards gain freight and lead-time advantages. Plants running ISO 9001 processes can hold tighter dimensional tolerances, which are necessary for robotic panel assembly lines now arriving in Abu Dhabi and Riyadh. As more investors insist on guaranteed completion dates, factory-made panels become a standard, elevating board volumes above traditional stick-built baselines in the Middle-East and Africa gypsum board market.

Mandated Energy-Efficient Building Codes

The GCC Standardization Organization harmonized ASTM C840 application rules in April 2024, and Dubai’s Green Building Regulations require 20% energy reduction versus a 2010 baseline, both of which reward insulated drywall assemblies. Saudi Arabia’s updated Building Code caps wall U-values in high-rise cores, making multi-layer gypsum systems with mineral wool infill the most economical route to compliance. The International Energy Agency confirms that the UAE, Saudi Arabia, and Qatar now demand energy-performance certificates for all new buildings, institutionalizing specification of lightweight, thermally efficient interiors. Short permitting windows mean contractors gravitate toward pre-tested gypsum assemblies that ship with fire and acoustic ratings already certified. These code shifts add a stable demand increment that cushions the Middle-East and Africa gypsum board market against cyclical slowdowns in bare-shell construction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Susceptibility of Paper-Faced Boards to Water and Mold Damage | -0.7% | Coastal GCC (UAE, Qatar, Bahrain, Oman), humid African zones (Nigeria coastal, Kenya coast) | Short term (≤ 2 years) |

| Volatile Natural-Gypsum Mining Royalties and Freight Costs | -0.5% | Oman, Saudi Arabia, Egypt (mining hubs); freight impacts all import-dependent markets | Medium term (2-4 years) |

| Rising Availability of Cement-Fiber and Calcium-Silicate Substitutes | -0.6% | UAE, Saudi Arabia, South Africa; expanding in Egypt, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Susceptibility of Paper-Faced Boards to Water and Mold Damage

Relative humidity above 80% accelerates fungal growth on paper facings, and field audits in Gulf apartments have found visible mold on standard boards within two years. Builders can specify fiberglass-mat or cement-fiber alternatives, but those carry 15-25% price premiums and are not yet mandatory in most municipal codes. Renovation work is especially exposed because existing HVAC systems rarely maintain 50-60% humidity. Premature replacement costs dent the total-cost-of-ownership narrative that once favored gypsum over masonry.

Volatile Natural-Gypsum Mining Royalties and Freight Costs

Governments in Oman and Saudi Arabia periodically lift royalty rates to capture resource rents, and swings of 15-25% feed straight into board production costs[1]USGS, “Mineral Commodity Summaries 2025 – Gypsum,” usgs.gov . The World Bank notes that dry-bulk freight rates spiked 40% in 2024 before easing, illustrating how exposed non-integrated plants remain to shipping volatility. Smaller African entrants often lack long-term mining contracts and therefore absorb both royalty and freight shocks, squeezing cash flow and hindering investment in quality upgrades. If shipping markets tighten again, price-sensitive contractors could switch to cement-fiber panels or autoclaved aerated concrete, trimming gypsum demand. Integrated Gulf producers can hedge with captive quarries, but import-dependent markets from Kenya to Angola remain vulnerable, eroding the moderate growth potential in the Middle-East and Africa gypsum board market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Board Type: Fire Codes Propel Specialized Variants

Fire-resistant board is growing at a 6.68% CAGR to 2031 and is outpacing the 5.61% baseline because 2024 updates to GCC fire-test standards require Type X or C assemblies in high-rise cores. Wall board still represented 46.12% of the Middle-East and Africa gypsum board market share in 2025, but its dominance is slipping as ceiling and pre-decorated panels climb the specification ladder, particularly in hospitality retrofits and modular pods. Architects value the fact that Type C panels combine higher core density with glass fiber to maintain structural integrity for two-hour ratings, something insurers now demand since a series of façade fires in Dubai. Premium ceiling boards such as Glasroc X sell at 30-40% price premiums yet win bids where acoustic performance and sag resistance matter, for example in airport concourses and resort lobbies.

Specialty boards also carry lower embodied carbon than cementitious alternates, so they earn points under UAE Estidama and Saudi Arabia’s updated SBC 601 energy chapter. Manufacturers therefore prioritize kilns that can toggle between standard and fire-resistant batches with minimal downtime, helping them meet mixed order profiles common on NEOM multi-package contracts. As modular factories scale, large-format boards will migrate from 1.20 × 2.40 meter staples to custom 3 meter lengths that reduce vertical joints, trimming labor minutes per square meter. That shift embeds product differentiation that protects margins even when wall board becomes more commoditized in the Middle-East and Africa gypsum board market.

By End-Use Sector: Logistics Hubs Outpace Housing

The industrial and warehouse segment is rising at a 6.23% CAGR through 2031, eclipsing gains in residential starts as Gulf and West African governments pour capital into free-zone logistics parks and e-commerce hubs. Non-load-bearing drywall meets insurers’ one-hour fire partition minimums and can be re-configured when pick-and-pack lines change, so operational flexibility outweighs the small cost premium versus concrete block. The residential sector still anchored 42.25% of the Middle-East and Africa gypsum board market size in 2025, bolstered by Saudi Arabia’s Sakani housing program and UAE villa communities. Yet average apartment sizes are shrinking, so board volume per unit is flat even when key-handovers rise.

Commercial offices are recovering as Dubai revamps Expo City assets into mixed-use campuses and Qatar funnels QR 12 billion (USD 3.3 billion) into public-private partnerships building schools and clinics. Institutional buyers specify antimicrobial and impact-resistant laminated cores in classrooms, operating theaters, and corridors, supporting value mix even at modest volume. Over the forecast horizon, industrial and warehouse fit-outs will claim a growing slice of Middle-East and Africa gypsum board market share, while residential settles into a mid-thirty-percent range as unit economics favor modular production and lightweight partitions that compress loan-to-rent conversion cycles.

Geography Analysis

Saudi Arabia leads volume because its USD 3.1 trillion project pipeline places drywall specifications directly into giga-project tender documents. Local firms United Mining Industries, National Gypsum, and Mada Gypsum expanded combined nameplate capacity by 40 million square meters between 2024 and 2025, ensuring captive supply for mega-cities under development. In the UAE, Dubai 2040 and Expo City retrofit programs pull premium, glass-mat boards into hospitality and retail corridors, and Gypsemna’s single-site plant can scale exports when GCC tariff schedules align.

Qatar’s regulatory push is already evident in drywall bid packages that now prefer local assembly where possible[2]Ashghal, “Five-Year Infrastructure Plan 2025–2029,” ashghal.gov.qa . Kuwait’s New Kuwait 2035 vision revives stalled commercial towers, though average project size remains smaller than in the UAE or Saudi Arabia. Egypt’s dual role as miner and board fabricator, plus Saint-Gobain’s upcoming plant, positions the Suez Canal Economic Zone as an export springboard into East Africa where port infrastructure is still nascent. Nigeria’s fast growth is supported by federal import-substitution incentives and a logistics corridor that shortens internal delivery times from Lagos to Abuja to under 48 hours.

The rest of the Middle-East and Africa markets, such as Morocco, Algeria, and Angola, absorb leftover Gulf capacity and remain price-driven. Here, standard wall board dominates because developers cannot pass cost premiums to end users. As income divergence widens, suppliers that run two-tier brands—premium for high-spec GCC markets and value lines for Africa—are best placed to stabilize revenue across the broader Middle-East and Africa gypsum board market.

Competitive Landscape

Industry structure is moderately concentrated. Saint-Gobain, Knauf, and Etex leverage regional plants but must match Gulf specialists Gypsemna, National Gypsum, and Mada Gypsum who enjoy quarry integration that buffers margin against commodity gyrations. Saint-Gobain’s July 2024 acquisition of WinChem Middle-East shows a strategy to bundle board with complementary chemicals and sell system warranties, elevating switching costs for contractors. Knauf published a unified GCC price sheet in 2025, signaling willingness to defend distributor relationships even if tariffs shift. Etex supports West Africa through Nigerite’s cement-fiber board lines, giving it an alternate channel in moisture-prone markets.

Innovations cluster around recycled core formulations and glass-mat facings that extend service life in humid zones. However, only multinationals fund full-scale R&D, so smaller Gulf and African entrants primarily compete on price. NEOM’s requirement that 30% of residential walls be factory-produced opens a white space for any board maker willing to co-locate panel lines near the project, an opportunity not yet seized in 2026. Overall, the top five suppliers hold about 60-65% of regional volume, confirming moderate concentration in the Middle-East and Africa gypsum board market.

Middle-East And Africa Gypsum Board Industry Leaders

Mada Gypsum Company

Saint-Gobain

Knauf Group

National Gypsum Services Company

KCC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: United Mining Industries began commercial operations at its gypsum board plant in Saudi Arabia. This marked a notable development in meeting market demands.

- February 2025: National Gypsum Services Company began pilot operations at its gypsum board production line in Riyadh. This initiative aims to integrate advanced technologies and achieve an annual production capacity of up to 15 million square meters, catering to the growing demand for gypsum boards in the Middle-East and Africa region.

Middle-East And Africa Gypsum Board Market Report Scope

A Gypsum board or drywall is a panel made of calcium sulfate dihydrate, with or without additives, typically extruded between thick sheets of facer and backer paper, used in the construction of interior walls and ceilings. The Middle-East and Africa gypsum board market is segmented by board type, end-use sector, and geography. By board type, the market is segmented into wall board, ceiling board, pre-decorated board and fire-resistant board. By end-use sector, the market is segmented into the residential, commercial, institutional, and industrial and warehouse. The report also covers the market sizes and forecasts for the gypsum board market in 9 countries across the region. For each segment, the market sizing and forecasts have been done based on volume (square meters).

By Board Type

| Wall Board |

| Ceiling Board |

| Pre-decorated Board |

| Fire-resistant Board |

By End-use Sector

| Residential |

| Commercial |

| Institutional (Healthcare and Education) |

| Industrial and Warehouse |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Egypt |

| Iran |

| South Africa |

| Nigeria |

| Kenya |

| Rest of Middle-East and Africa |

| By Board Type | Wall Board |

| Ceiling Board | |

| Pre-decorated Board | |

| Fire-resistant Board | |

| By End-use Sector | Residential |

| Commercial | |

| Institutional (Healthcare and Education) | |

| Industrial and Warehouse | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Egypt | |

| Iran | |

| South Africa | |

| Nigeria | |

| Kenya | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

How large will gypsum board demand in the Middle-East and Africa be by 2031?

Volume is forecast to reach 2.70 billion square meters by 2031, up from 2.06 billion square meters in 2026, equal to a 5.61% compound annual growth rate.

Which board type is growing fastest in the region?

Fire-resistant board is progressing at a 6.68% CAGR because updated GCC test standards make Type X or C assemblies mandatory in many high-rise and hospitality projects.

Why are industrial and warehouse projects important for board suppliers?

Developers of fulfillment centers and logistics parks prioritize partitions that can be re-configured quickly, lifting industrial and warehouse growth to 6.23% CAGR, the highest among end-uses.

What is the main challenge for gypsum board in coastal climates?

Paper-faced boards are prone to mold in humidity above 80%, which drives demand for fiberglass-mat or cement-fiber alternatives in Gulf and West African coastal cities.

Page last updated on: