Middle East Biodegradable Plastics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

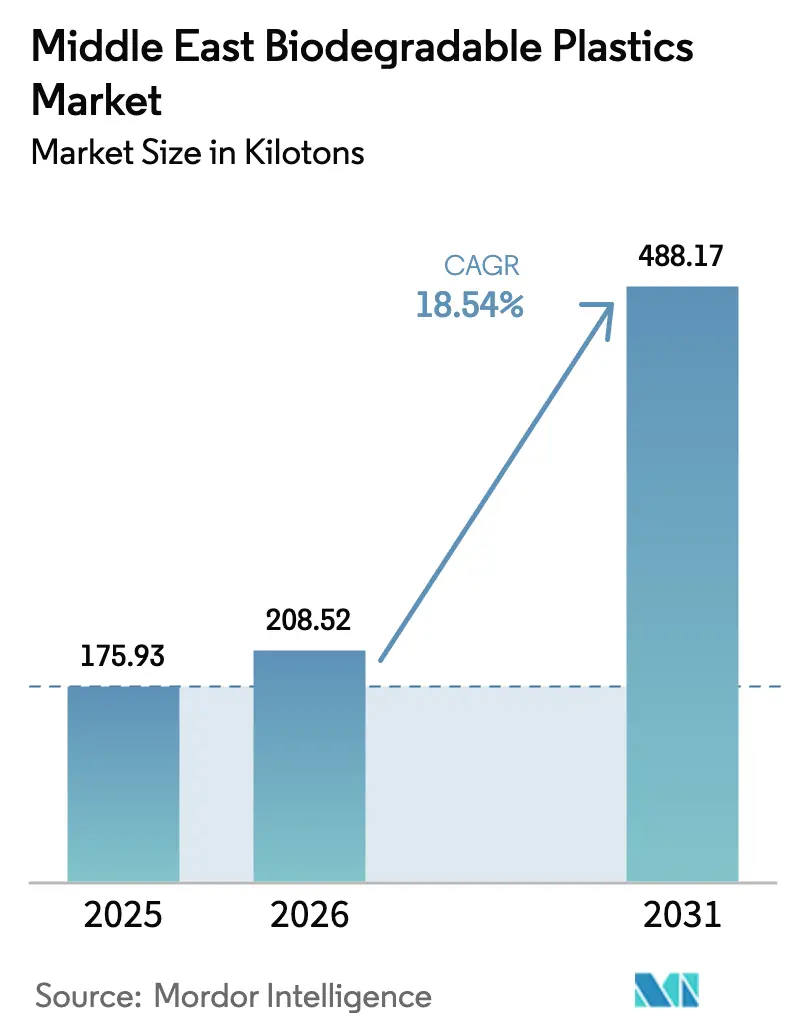

| Base Year Market Size (2025) | 175.93 kilotons |

| Market Volume (2026) | 208.52 kilotons |

| Market Volume (2031) | 488.17 kilotons |

| Growth Rate (2026 - 2031) | 18.54% CAGR |

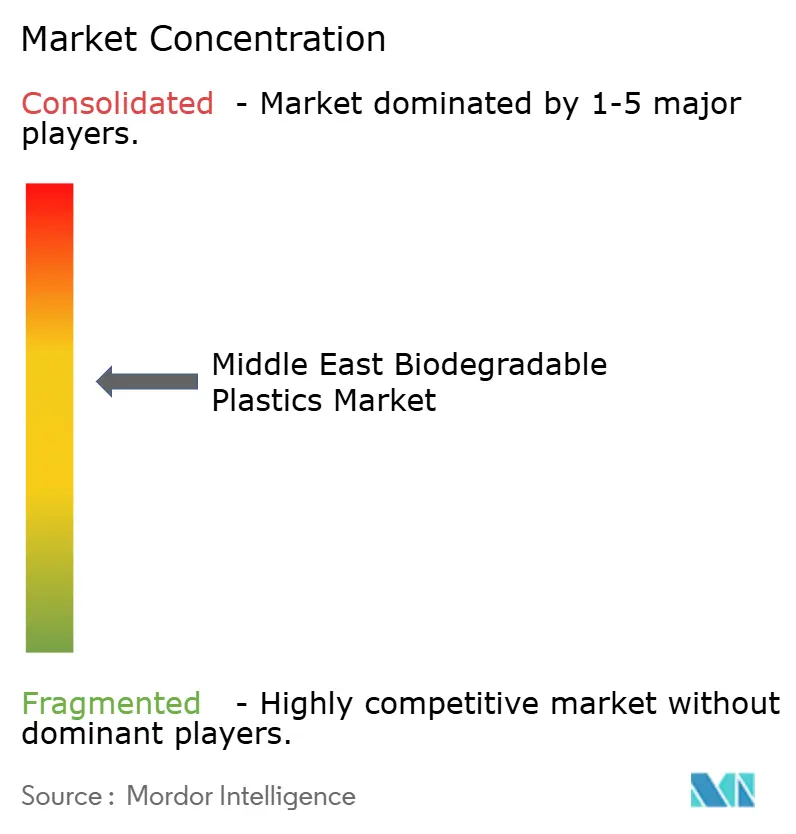

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Biodegradable Plastics Market Analysis by Mordor Intelligence

The Middle East biodegradable plastics market size was valued at 175.93 kilotons in 2025 and estimated to grow from 208.52 kilotons in 2026 to reach 488.17 kilotons by 2031, at a CAGR of 18.54% during the forecast period (2026-2031). Legislated bans on single-use petroleum plastics, sovereign circular economy mandates, and retail procurement standards drive demand, while local bio-refinery investments shorten supply lead times and mitigate currency-linked freight risk. Corporate sustainability scorecards from hypermarket chains accelerate substitution, and consumer surveys show widening willingness to pay a premium for eco-labeled packs in urban GCC centers. Converter margins hinge on resin cost parity: biodegradable polyesters still command a 20–50% premium to commodity polyethylene, yet imports from Asia face voyage delays and freight surcharges that erode the gap. Infrastructure readiness remains the wild card; only a handful of industrial composting projects in Dubai and Riyadh operate at pilot scale, so end-of-life certainty varies by city and by polymer grade.

Key Report Takeaways

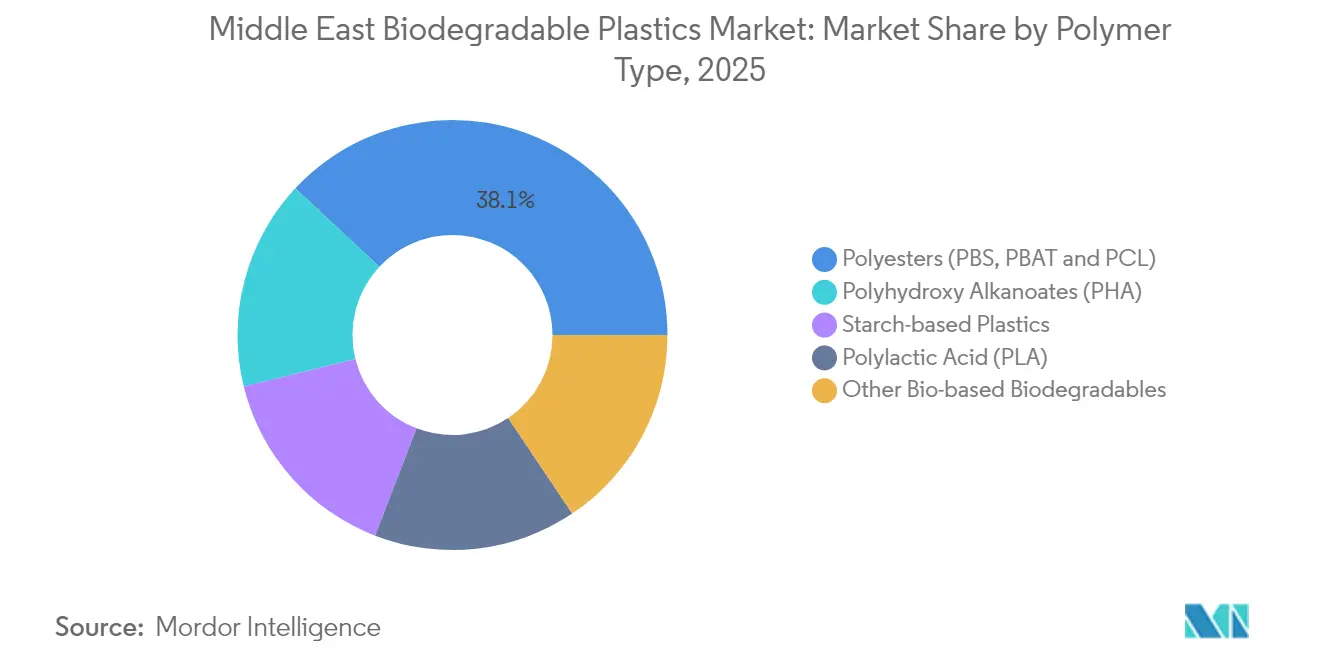

- By polymer type, polyesters captured 38.05% of the Middle East biodegradable plastics market share in 2025, while Polyhydroxyalkanoates (PHAs) are forecast to expand at a 19.34% CAGR through 2031.

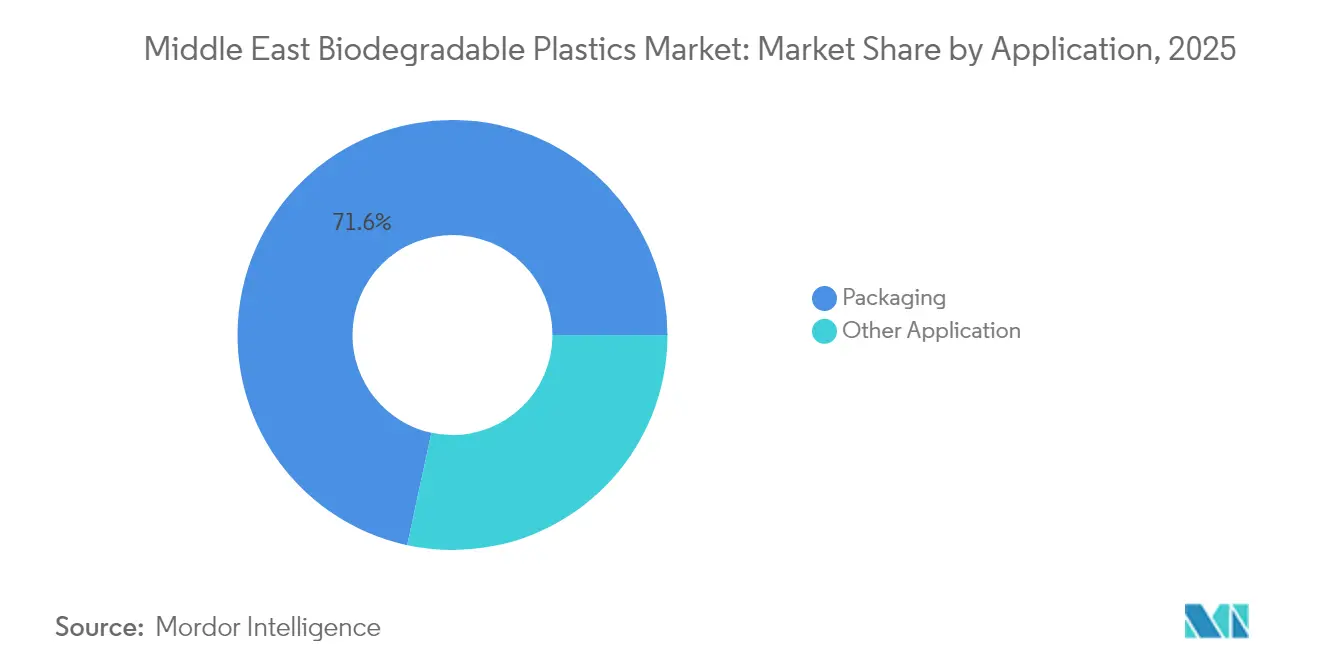

- By application, packaging accounted for 71.62% of the Middle East biodegradable plastics market size in 2025, while other applications are projected to rise at a 19.01% CAGR between 2026 and 2031.

- By geography, Saudi Arabia accounted for 41.10% of regional volume in 2025, while the UAE is projected to grow at a 19.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Biodegradable Plastics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government bans on single-use plastics (UAE, KSA) | +4.5% | UAE (Dubai, Abu Dhabi), Saudi Arabia (Riyadh, Jeddah), with spillover to Qatar, Oman | Short term (≤ 2 years) |

| Corporate sustainability targets from FMCG and retail | +3.2% | GCC-wide, concentrated in the UAE and Saudi Arabia retail hubs | Medium term (2-4 years) |

| Rising consumer demand for eco-friendly packaging | +2.8% | Urban centers across GCC (Dubai, Riyadh, Doha), expanding to secondary cities | Medium term (2-4 years) |

| Industrial composting projects in GCC | +2.5% | UAE (Dubai, Abu Dhabi), Saudi Arabia (Riyadh cluster), pilot sites in Qatar | Long term (≥ 4 years) |

| Saudi Vision 2030 funding bio-refineries | +3.0% | Saudi Arabia (industrial clusters in Eastern Province, Jubail), with regional technology spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Bans on Single-Use Plastics Drive Substitution Demand

Dubai enforced its single-use plastic ban in June 2024, and Carrefour UAE reported a 70% drop in carrier bag usage during the first quarter of compliance[1]Gulf Business, “Carrefour Records 70% Drop in Single-Use Bags,” gulfbusiness.com. Saudi Arabia is introducing mirror regulations through the National Center for Waste Management, which aims to achieve 90% landfill diversion by 2040 and allocates capital for expanding composting capacity in the five largest urban clusters. Retail audits and import checkpoints, rather than producer levies, ensure compliance, so cost pressure shifts downstream to converters. Larger FMCG brand owners absorb the resin premium in exchange for label differentiation, but small converters struggle with cash-flow lockups. The policy trajectory hints at future bans on rigid containers and food-service ware once composting throughput ramps.

Corporate Sustainability Targets Reshape Procurement Specifications

Majid Al Futtaim phased out single-use plastics in its Lifestyle division in 2024 and intends to extend this policy across its owned properties by 2025, requiring suppliers to source resins certified to ISO 14855 or EN 13432. Lulu Group is piloting edible film wraps that disintegrate in hot water, a marketing play that doubles as a compliance hedge. TotalEnergies Corbion’s Luminy PLA boasts an 85% lower cradle-to-gate carbon footprint compared to petroleum plastics, and its 100% recycled-content grade features a negative footprint, providing procurement officers with a ready-made lifecycle narrative. Retail Green Star leases link tenant ratings to sustainable materials, pushing ecological metrics deep into mall supply chains and signaling that sustainability clauses will soon be standard in GCC commercial property.

Rising Consumer Willingness to Pay for Eco-Labeled Products

An Ipsos study found that 82% of UAE consumers are willing to compromise for environmental benefits, yet many remain uncertain about the actionable steps they can take. Retail promotions close the knowledge gap: Plastic-Free July discounts on juco bags at Carrefour boosted reusable-bag adoption, and loyalty-card tie-ins convert eco-intent into measurable sales. Performance parity is critical; early starch blends failed moisture tests, but next-gen PLA-PBS blends keep barrier integrity in desert logistics. Premium health-food categories now feature fully compostable pouches without volume loss, demonstrating that urban consumers will accept a 5–7% price differential as performance concerns subside.

Industrial Composting Infrastructure Determines End-of-Life Viability

Saudi Arabia has earmarked more than 840 waste-treatment facilities by 2040; yet, only a fraction will be composting plants with the residence time required for PLA or PBAT conversion. Dubai malls operate food digesters that convert kitchen waste into gray water and fertilizer, but they do not reach the 58 °C threshold required for ISO-grade polymer breakdown. Without fit-for-purpose sites, biodegradable films may either enter landfill methane pathways or contaminate PET recycling streams, undercutting the green narrative. The policy debate now centers on extended producer responsibility schemes that would shift capital expenditures from municipalities to resin sellers, but petrochemical lobbyists argue for technology-neutral frameworks that give chemical recycling equal weight.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost premium over petroleum plastics | -2.5% | GCC-wide, most acute in price-sensitive segments (commodity packaging, agricultural films) | Short term (≤ 2 years) |

| Limited regional composting / recycling infrastructure | -2.0% | All Middle East geographies, with infrastructure gaps most severe outside UAE and Saudi Arabia urban centers | Medium term (2-4 years) |

| Petrochemical lobby influence on policy | -1.5% | Saudi Arabia, UAE (where petrochemical sector represents significant GDP share and employment) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Premium Constrains Adoption in Price-Sensitive Segments

Biodegradable resins sell at a 20–50% markup to virgin polyethylene and polypropylene due to high feedstock costs and lower line throughput. FMCG giants absorb the delta to meet ESG targets, but commodity packagers that serve low-margin staples cannot. In the absence of EPR subsidies, the market tends to skew toward premium categories and pilot hospitality programs rather than mass retail. Distributors attempt to mitigate freight costs by transshipping from Asia in break-bulk lots; however, spot rates on the Far East-Gulf lane remain volatile. Local PLA capacity, once operational, will narrow the premium by saving on freight and duties; until then, price remains the primary barrier.

Limited Composting Infrastructure Creates End-of-Life Uncertainty

Pilot composting tunnels in Riyadh and Dubai handle mixed food waste but lack polymer certifications, so most compostable packs still exist in retail, often mixed with black-bag streams. Discover Applied Sciences reports that enzymatic depolymerization pilots struggle with feedstock contamination and skilled-operator shortages. If packs fail to degrade, consumer trust erodes, and recyclers complain about cross-polymer contamination, lobbying regulators to slow biodegradable mandates. Saudi municipal tenders for composting plants list 2028–2030 commissioning windows, indicating a multi-year lag between policy and infrastructure implementation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Polyester Dominance, PHA Rising

Polyesters secured 38.05% of the Middle East biodegradable plastics market share in 2025 because PBS and PBAT drop seamlessly into existing film lines, and converters appreciate their toughness in extreme Gulf summer logistics. The segment also benefits from ASEAN supply chains that deliver ready-compounded grades with food-contact status. Local poly-butylene succinate synthesis remains limited, but PET resin majors contemplate debottlenecking to run bio-succinate.

PHA is projected to enjoy the fastest growth at a 19.34% CAGR. Its marine biodegradability suits coastal tourism zones under pressure to curb plastic litter. Emirates Biotech has signaled interest in PHA copolymer expansion once its PLA trains are settled, reflecting the converter's appetite for resins that degrade in seawater. Still, fermentation yields lag PLA, keeping PHA price points at a premium. Technology partnerships with enzyme specialists aim to increase yields and make PHA viable for high-volume items, such as straw wraps and snack films, by the late 2020s.

By Application: Packaging Dominates, Other Uses Accelerate

Packaging accounted for 71.62% of the Middle East biodegradable plastics market size in 2025, driven by carrier bag bans and retailer scorecards. Barrier-improved PLA–PBAT blends are now replacing PET trays for salads and cold cuts, while heat-stable stereocomplex PLA trials are proceeding for dairy tubs. Consumers reward these shifts with measurable basket lifts in organic aisles. Most user awareness campaigns continue to link bag charges to mangrove replanting, reinforcing behavioral change.

Other Applications grow at a 19.01% CAGR, influenced by greenhouse horticulture. Soil-degradable mulch films spare farmers the USD 150–200 per hectare retrieval cost of PE films. Saudi date growers are trialing PHA-coated fertilizer pellets that release micronutrients as the coating decomposes. The adoption of disposable serviceware rose in premium hotels catering to sustainability-conscious tourists; however, coffee-cup lids remained dominated by PLA-coated paper imports until local thermoformers mastered high-flow PCL blends.

Geography Analysis

Saudi Arabia accounted for a 41.10% share of the Middle East biodegradable plastics market in 2025, benefiting from Vision 2030’s USD 20 billion allocation to the waste sector, a population of 35 million, and policy targets aiming for 90% landfill diversion. Riyadh alone produces 25.8 million tons of waste annually and plans to establish 80 treatment centers, six of which will include composting tunnels. Procurement frameworks reward domestic content, so resin makers with local presence secure early offtake. Municipal tenders, however, bundle composters with anaerobic digesters, slowing award cycles.

The UAE is the fastest-growing geography at a 19.43% CAGR. Dubai’s June 2024 carrier-bag ban cut single-use volumes by 70% within a quarter at Carrefour and set the reference model for Abu Dhabi’s follow-on regulation. Kezad has attracted USD 40 million in pledges for biodegradable polymers, including a 30,000 tons per year PLA line from Emirates Biotech, which is scheduled to be commissioned in early 2028. Retail chains, such as Majid Al Futtaim, incorporate sustainability clauses into leases, ensuring that packaging substitution cascades to tenants.

Rest-of-Middle-East markets remain fragmented. Qatar’s hospitality drives niche demand, but its small population limits volume. Oman positions itself as a maleic anhydride hub with a 50,000 tons per year plant in Salalah that feeds polyester roots. Sanctions curb Iran’s access to Western fermentation technology, although academic labs are piloting starch-blend mulch for pistachio orchards. Kuwait and Bahrain follow GCC norms before acting, so adoption spikes will likely lag behind those of Saudi and the UAE by several years.

Competitive Landscape

The Middle East biodegradable plastic market is moderately consolidated. Global incumbents dominate the upstream resin. Global majors such as BASF offer technical service hubs in Dubai and Riyadh. Downstream, over 70 small converters compete in contract film tolling, facing working capital stress as resin lead times lengthen. Import distributors face thinner margins once regional plants start, prompting strategic pivots: some sign multi-year offtake agreements to lock in volumes, while others diversify into PHA or biomass coatings. Local converters hedge by securing dual-source supply contracts that cover both biodegradable and recycled PET feedstocks, thereby maintaining agility against policy fluctuations.

Middle East Biodegradable Plastics Industry Leaders

BASF

TotalEnergies Corbion

Al Bayader International

ECOWAY GLOBAL L.L.C.

Avani Eco

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: TotalEnergies Corbion appointed Multi Trade Group as main Luminy PLA distributor across the Gulf.

- February 2024: Khalifa Economic Zones Abu Dhabi (KEZAD Group), the largest operator of integrated and purpose-built economic zones, has announced the inclusion of Gulf Biopolymers Industries Ltd. (GBI) into its ecosystem. This development positions GBI as the first producer in the Middle East to manufacture biomass-based, recyclable, and biodegradable polymers, aligning with KEZAD's commitment to fostering innovative and sustainable industries.

Middle East Biodegradable Plastics Market Report Scope

Biodegradable plastics are plastics that can be decomposed by living organisms like microbes or in other specific conditions. The Middle East biodegradable plastics market is segmented by polymer type, application, and geography. By polymer type, the market is segmented into starch-based plastics, polylactic acid (PLA), polyhydroxyalkanoates (PHA), polyesters (PBS, PBAT, and PCL), and other bio-based biodegradable plastics. By application, the market is segmented into packaging and other applications. The market sizing and forecasts have been done on the basis of volume (kilo tons).

| Starch-based Plastics |

| Polylactic Acid (PLA) |

| Polyhydroxy Alkanoates (PHA) |

| Polyesters (PBS, PBAT and PCL) |

| Other Bio-based Biodegradables |

| Packaging |

| Other Applications |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Iran |

| Rest of Middle-East |

| By Polymer Type | Starch-based Plastics |

| Polylactic Acid (PLA) | |

| Polyhydroxy Alkanoates (PHA) | |

| Polyesters (PBS, PBAT and PCL) | |

| Other Bio-based Biodegradables | |

| By Application | Packaging |

| Other Applications | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Iran | |

| Rest of Middle-East |

Key Questions Answered in the Report

What volume does the Middle East biodegradable plastics market reach by 2031?

The market is projected to reach 488.17 kilotons by 2031, driven by sustained policy and retail demand.

Which polymer type grows fastest through 2031?

Polyhydroxyalkanoates (PHA) are forecast to post a 19.34% CAGR, driven by their marine biodegradability credentials.

Why is UAE growth outpacing the region?

Dubai’s carrier-bag ban, Kezad’s local resin capacity, and retail procurement mandates push UAE volume at a 19.43% CAGR.

How does infrastructure readiness affect adoption?

Limited industrial composting capacity delays end-of-life validation, restraining mass adoption despite strong policy signals.

What is the key cost barrier?

Biodegradable resins carry a 20–50% premium over petroleum-based plastics, challenging converters in low-margin packaging applications.

Page last updated on: