Bio-degradable Polymers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

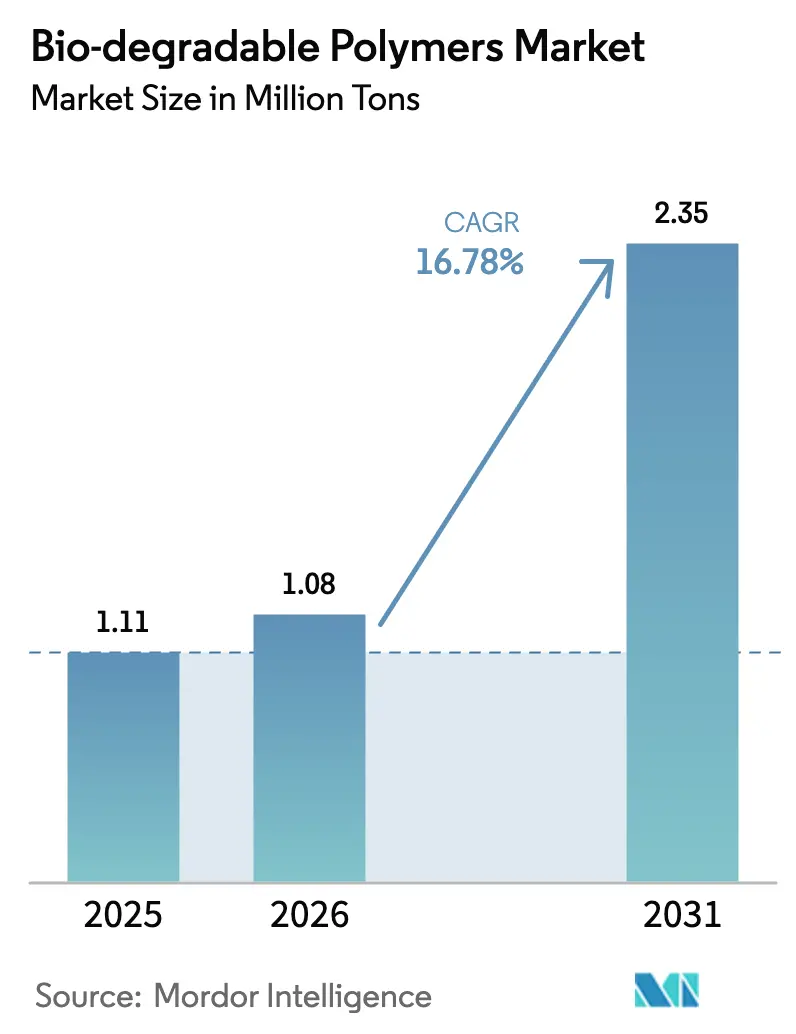

| Market Volume (2026) | 1.08 Million tons |

| Market Volume (2031) | 2.35 Million tons |

| Growth Rate (2026 - 2031) | 16.78% CAGR |

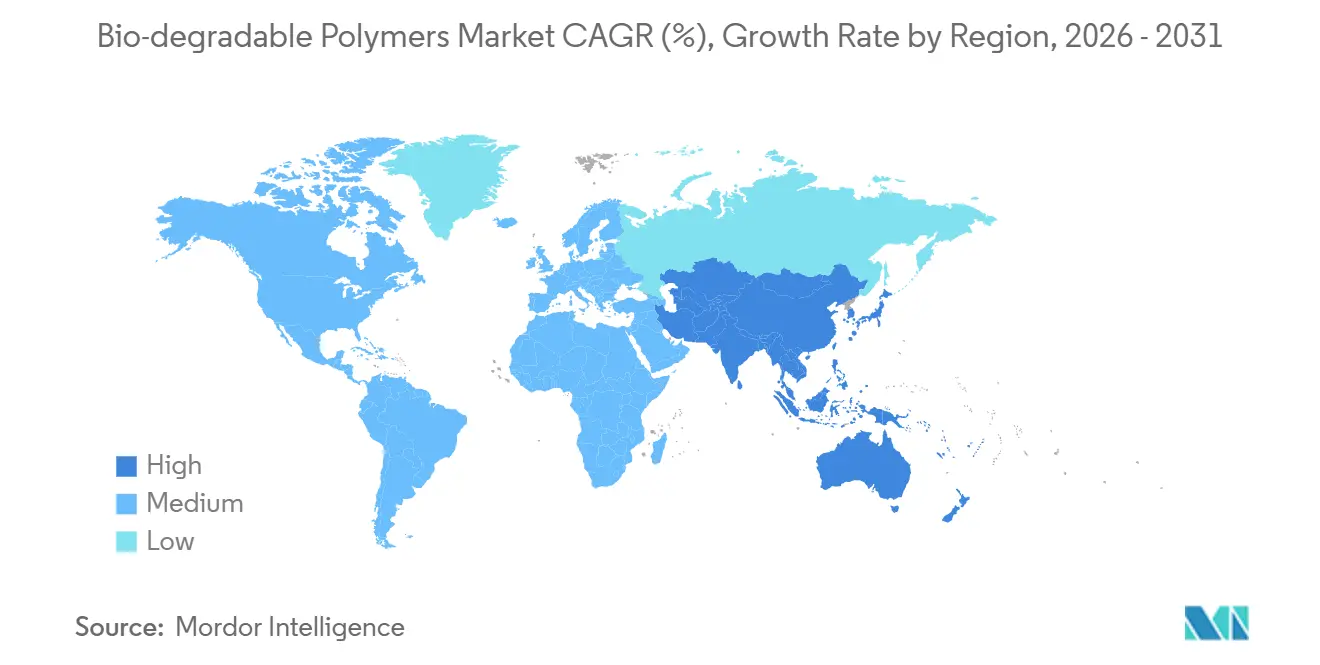

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

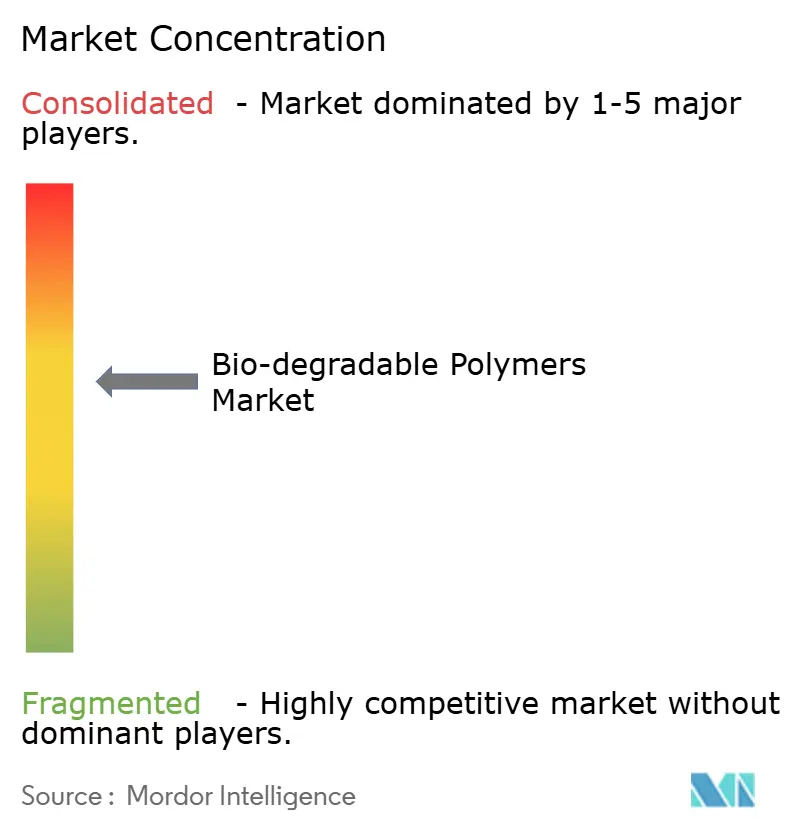

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-degradable Polymers Market Analysis by Mordor Intelligence

The Bio-degradable Polymers Market size is expected to increase from 1.11 Million tons in 2025 to 1.08 Million tons in 2026 and reach 2.35 Million tons by 2031, growing at a CAGR of 16.78% over 2026-2031. This outlook positions the bio-degradable polymers market size for rapid scale-up as price-focused substitution gives way to performance-driven adoption in packaging, consumer goods, agriculture, and healthcare applications. Brand mandates, carbon-pricing mechanisms, and carbon-capture-derived monomers are reshaping supplier economics, while Asia-Pacific capacity additions compress margins in starch-based and PLA grades. Europe retains first-mover advantages in certification infrastructure, yet China and India are set to invert geographic leadership on tonnage through 2031. Competitive strategies now bifurcate between high-volume PLA and PBAT lines and premium PHA portfolios that command 40–60% price uplifts for marine or medical biodegradability assurance.

Key Report Takeaways

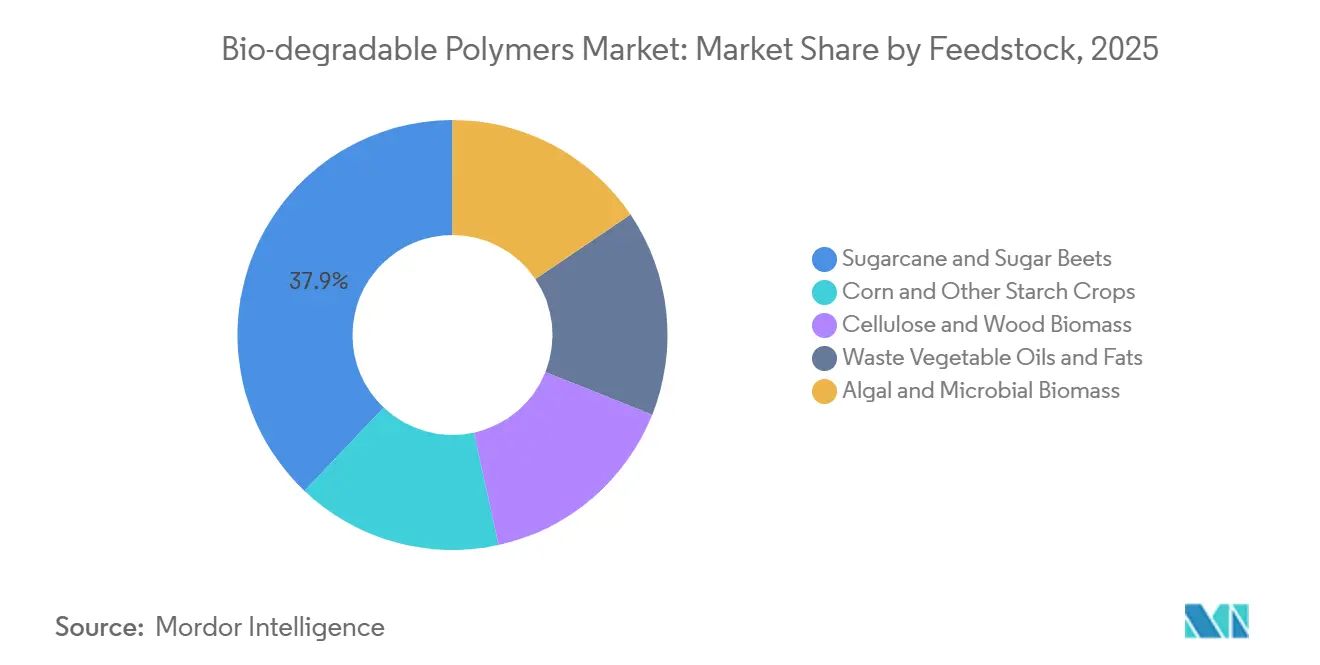

- By feedstock, sugarcane and sugar beets led with a 37.91% bio-degradable polymers market share in 2025, while algal and microbial biomass is forecast to advance at an 18.26% CAGR through 2031.

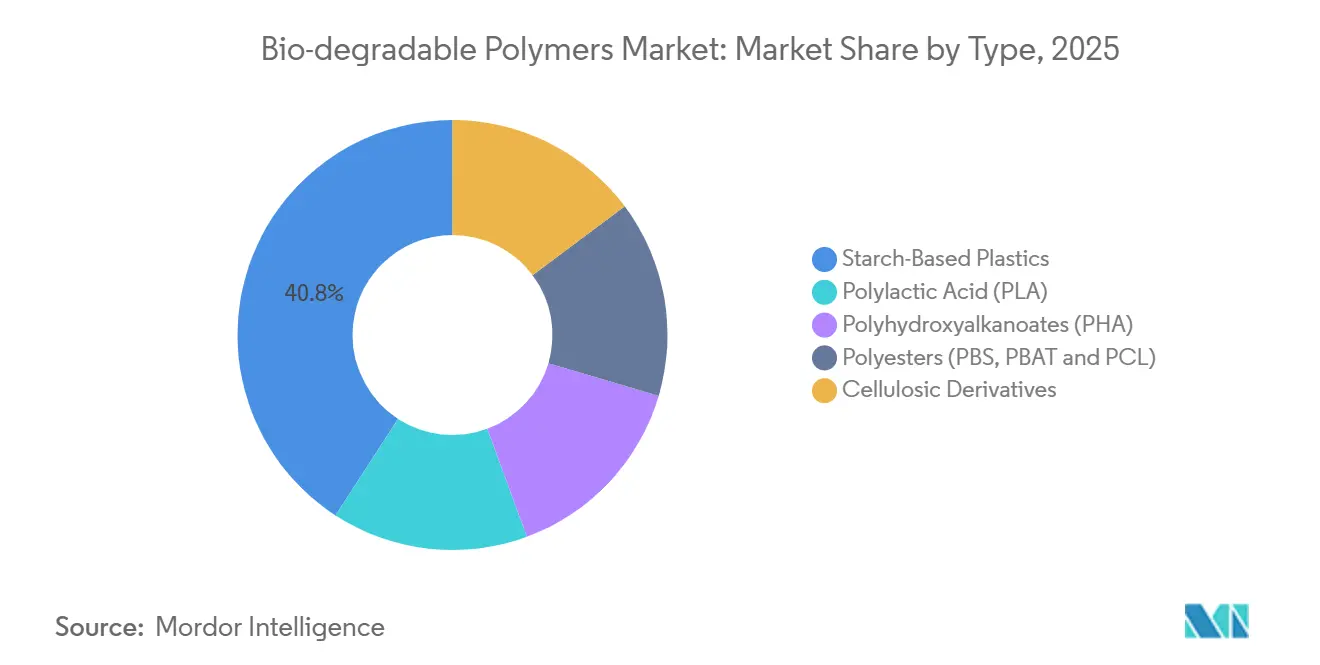

- By type, starch-based plastics captured 40.85% of the biodegradable polymers market size in 2025, while Polyhydroxyalkanoates (PHA) are forecast to advance at a 20.84% CAGR to 2031.

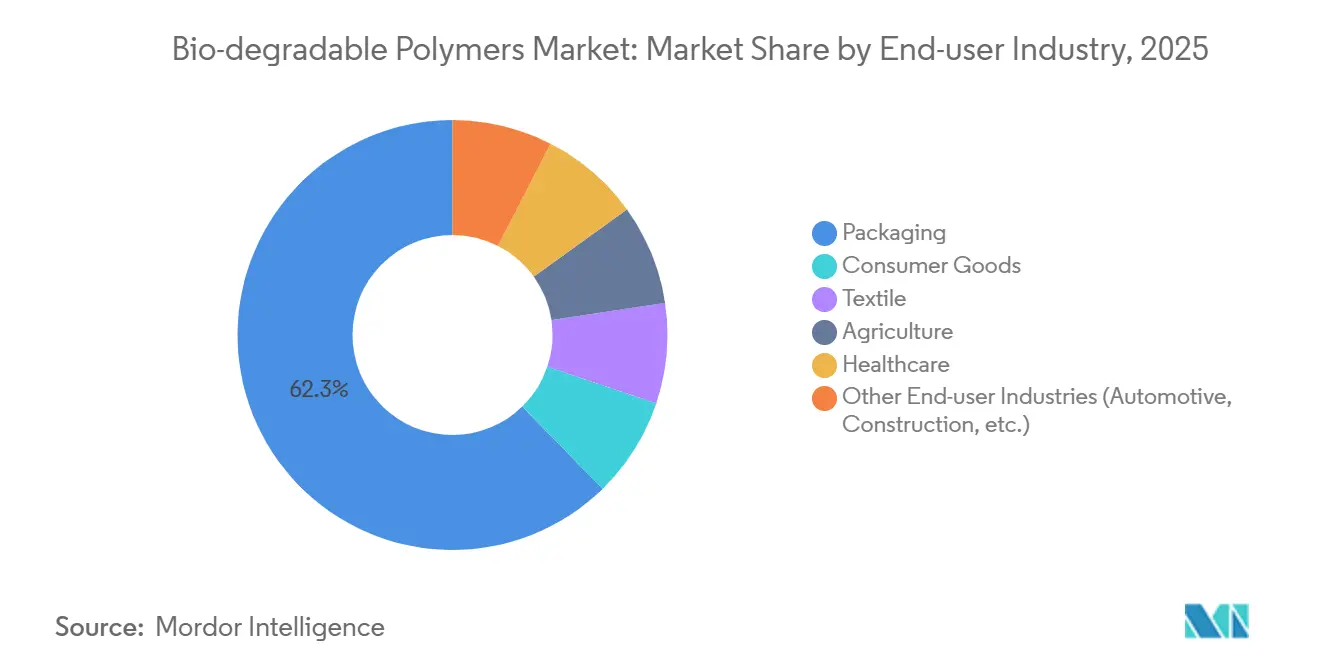

- By end-user industry, packaging held 62.31% of 2025 volume; consumer goods is set to expand at a 19.36% CAGR to 2031.

- By geography, Europe captured 38.95% of the bio-degradable polymers market size in 2025, while Asia-Pacific is projected to record the fastest 19.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bio-degradable Polymers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Regulations Banning Single-Use Plastics | +4.2% | Global, led by EU, China, India | Short term (≤ 2 years) |

| Rising Demand for Sustainable, Eco-Friendly Packaging | +5.8% | North America, Europe, APAC urban centers | Medium term (2–4 years) |

| Accelerating Adoption in Healthcare Applications | +3.1% | North America, Europe, Japan | Medium term (2–4 years) |

| Growing Use of Biodegradable Films in Agriculture | +2.9% | APAC (China, India), Mediterranean Europe, Latin America | Long term (≥ 4 years) |

| Carbon-Capture–Derived Monomers Enabling Negative-Emission Plastics | +4.3% | North America, Northern Europe, early pilots in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Regulations Banning Single-Use Plastics

The EU Single-Use Plastics Directive, fully enforced from January 2024, eliminated oxo-degradable items across ten categories and lifted PLA and starch-film demand above 180,000 tons in 2025. China’s nationwide plastic-bag ban and restrictions on non-degradable mulch films injected provincial subsidies that added 320,000 tons of PLA and PBAT nameplate capacity by 2025[1]National Development and Reform Commission, “Further Strengthening Plastic Pollution Control,” ndrc.gov.cn . India’s 2024 amendment to the Plastic-Waste Rules barred thin single-use plastics, opening a 95,000-ton starch-blend opportunity that meets IS 17088 criteria. Producers now co-locate near high-enforcement regions: NatureWorks’ Thailand PLA plant supplies ASEAN, while Danimer Scientific’s Kentucky PHA line targets U.S. coastal markets.

Rising Demand for Sustainable, Eco-Friendly Packaging

Unilever pledged to convert 35% of its flexible films to certified-compostable materials by 2027, securing multi-year offtakes with TotalEnergies Corbion and BASF. Nestlé trials PHA-coated paperboard wrappers for confectionery in Europe, creating a 22,000-ton barrier-grade PHA window by 2026. Procter & Gamble’s 2024 patent on marine-degradable PLA-PBAT detergent pods adds a coastal disposal solution. Amazon disclosed that 18% of its North American shipments already use starch loose-fill and PLA mailers, displacing 43,000 tons of polyethylene in 2025. Brand-owner demand increasingly specifies industrial, home, or marine degradation pathways, fragmenting certification needs and widening portfolio complexity.

Accelerating Adoption in Healthcare Applications

The U.S. FDA cleared 14 PHA-based sutures and implants in 2024–2025, up from six approvals in the prior biennium, validating ISO 10993 biocompatibility. Danimer Scientific’s nodax® PHA earned CE marking for resorbable stents in 2025, opening a USD 340 million niche. Japan authorized Teijin’s PLA bone screws in 2024, citing radiolucency and bioresorption benefits. Mitsubishi Chemical’s BioPBS blister packs gained child-resistant certification in 2025, replacing PVC for OTC drugs. Extended approval cycles and clinical testing sustain specialty margins above 40%.

Growing Use of Biodegradable Films in Agriculture

China mandates 100% biodegradable mulch films across 15 provinces by 2027, driving 210,000 tons of PBAT-starch demand. India subsidizes half the cost of biodegradable films for smallholders, boosting yields in Punjab and Haryana. EU eco-schemes link subsidy payments to sustainable inputs, lifting consumption by 38,000 tons in 2025. Israeli producers now offer UV-stable PHA greenhouse films that cut disposal outlays of USD 450 per hectare. Quality seals from DIN CERTCO and TÜV Austria justify 15–20% price premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Cost Vs. Conventional Plastics | -2.7% | Global, most acute in price-sensitive APAC and South America | Short term (≤ 2 years) |

| Limited Mechanical Performance for Automotive Parts | -1.4% | North America, Europe, Japan (major automotive hubs) | Medium term (2–4 years) |

| Feedstock-Price Volatility from Non-Food Biomass Demand | -1.8% | North America (corn belt), Brazil (sugarcane), EU (waste oils) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost vs. Conventional Plastics

Commodity PLA sells at USD 2.80–3.50 per kg versus USD 1.20–1.40 for polyethylene, maintaining a 90–140% premium that restricts uptake outside mandated or fee-burdened streams. Marine-grade PHA commands USD 5.00–6.50 per kg, reflecting fermentation complexity. Corn-starch price spikes of 28% in 2024 compressed NatureWorks and Cargill gross margins to 24%[2]U.S. Department of Agriculture, “Grain Market Report December 2025,” usda.gov . Greenfield PHA plants require USD 180–220 million per 50,000-ton line, double comparable polyethylene units, slowing new entrant traction. Learning rates of 12–15% per capacity doubling lag conventional plastics, prolonging parity timelines.

Limited Mechanical Performance for Automotive Parts

PLA and PHA heat-deflection temperatures top out at 65 °C under ASTM D648, below the 90–110 °C threshold for interior components, limiting adoption to trim insert panels. Notched Izod impact for PHA averages 25–35 J/m, far from ABS levels of 200+ J/m, restricting structural uses. Volkswagen and Toyota trials delivered 12–18% weight savings but encountered durability failures over simulated ten-year cycles. Flame-retardant additives that achieve FMVSS 302 compliance can add up to USD 1.20 per kg and dilute biodegradability. Small-scale opportunities exist in EV battery enclosures where PHA meets UL 94 V-0, yet annual volume remains below 5,000 tons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Sugarcane Dominance Meets Algal Upside

Sugarcane and sugar beets delivered 37.91% of 2025 volume, anchored by Brazil’s vast cane acreage and European beet output that supply fermentable sugars at USD 0.32–0.38 per kg. This cost base underpins the bio-degradable polymers market size for PLA and bio-PE production in both hemispheres. Corn and other starch crops are benefiting from established wet-milling and rail logistics in the United States and Northeast China.

Algal and microbial biomass is expanding at an 18.26% CAGR on titers above 120 g/L for PHA, a trajectory that could lift its bio-degradable polymers market share as fermentation costs near PLA parity. Cellulose residues secured moderate share as Nordic pulp mills valorize waste streams, while waste oils face tightening supplies from renewable-diesel mandates.

By Type: Starch Volume Leadership, PHA Momentum

Starch-based plastics held 40.85% of 2025 volume thanks to thermoplastic starch blends priced 25–30% below PLA. PLA is propelled by large single-site capacities that support rigid packaging and fiber.

PHA is the growth standout, sprinting at 20.84% CAGR as marine-degradability certifications unlock fishing-gear and coastal-packaging niches. Polyesters such as PBS and PBAT are valued for high elongation in film, while cellulosic derivatives face flat demand where cigarette-filter regulation looms.

By End-user Industry: Packaging Saturation, Consumer Surge

Packaging absorbed 62.31% of 2025 consumption across films, containers, and loose-fill, driven by brand commitments that added incremental PLA and PBAT demand. Consumer goods are forecast to grow at a 19.36% CAGR as electronics makers pilot PHA housings that industrially compost in 180 days.

Textiles secured PLA staple fiber demand in hygiene and apparel, while agriculture is expanding due to mulch-film mandates. Healthcare is also advancing year over year on resorbable implants that reduce second surgeries by USD 2,500–4,000.

Geography Analysis

Europe accounted for 38.95% of 2025 volume, supported by harmonized certification, robust composting infrastructure, and national bans that elevate average selling prices by 12–18% over non-certified imports. Germany’s market is driven by BASF’s ecovio® integration and stringent DIN CERTCO requirements that favor local supply. France and Italy followed demand as carrier-bag and mulch-film regulations accelerated substitution.

Asia-Pacific is poised to overturn European dominance with a 19.24% CAGR. China’s capacity additions during 2024–2025 and India’s single-use bans together underpin projected incremental tonnage. Zhejiang Hisun’s 100,000-ton PBAT line and NatureWorks’ planned Thai expansion illustrate capital allocation toward regional self-sufficiency. ASEAN agricultural-film subsidies further expand addressable demand.

North America captured moderate consumption, with California, New York, and Washington leading bag and food-service bans. Canada’s federal prohibition bolstered demand, while Mexico City and Jalisco state measures lifted Mexico’s consumption. South America and the Middle East and Africa remain smaller but benefit from cane-based bio-PE in Brazil and emerging circular-economy policies in Saudi Arabia and South Africa.

Regulatory Landscape

Regulation increasingly differentiates biodegradability claims from certified compostability and ties market access to validated end-of-life pathways. In the European Union, the Packaging and Packaging Waste Regulation (EU) 2025/40 tightens the compliance burden for compostable packaging by pushing revisions to EN 13432 (including stricter composting timeframes and limits on microplastic release) and by defining where compostable formats can be allowed (for example, select items such as tea bags and very lightweight plastic bags, contingent on bio-waste infrastructure). In the United States, the FTC Green Guides (16 CFR 260.8) restrict unqualified degradable claims for products likely to enter solid-waste streams, requiring substantiation that complete decomposition occurs within one year, which elevates the role of third-party testing and documentation for packaging and consumer goods.

China continues to formalize identification and performance thresholds through national standards such as GB/T 41010-2021, which sets identification requirements and biodegradation performance targets (including a 90% relative biodegradation rate benchmark), supporting enforcement of provincial and national anti-pollution measures. In parallel, the US EPA regulatory framework still treats “polymers designed to be biodegradable” differently in chemical reporting and compliance, and these materials do not automatically benefit from certain polymer exemption pathways under 40 CFR 723.250. Across regions, compliance is moving toward proof-based labeling, certified test methods, and infrastructure-linked permissions, which increases the strategic value of certification dossiers (industrial vs home composting, and in select cases marine or soil biodegradation claims) alongside food-contact and product safety clearances.

Value Chain Analysis

The value chain starts with feedstock production and aggregation (sugarcane, sugar beets, corn, and other starch crops, plus emerging agricultural-waste and microbial routes), followed by fermentation or chemical conversion to platform intermediates (for example, lactic acid and lactide for PLA, and fermentation-derived monomers for PHA). Polymerization/compounding is the main value pool, concentrated among a limited set of scaled producers due to high capex, long qualification cycles, and the need for certification and food-contact compliance. A notable upstream-to-downstream integration step occurred in April 2026 when NatureWorks commenced operations at its fully integrated Ingeo PLA facility in the Nakhon Sawan Biocomplex in Thailand (75,000 tons/year), linking regional sugar-based inputs to lactic acid, lactide, and PLA output and reducing reliance on cross-region resin flows for packaging and fibers.

Downstream, resin is converted by film extruders, thermoformers, fiber makers, and injection molders into packaging, agriculture films, and select medical and consumer goods, then distributed through converters and brand-owner supply chains into retail and institutional channels. Regulation-driven demand signals and infrastructure readiness (industrial composting vs home composting vs mixed recycling streams) act as gating factors that influence grade selection and converter investments. Partnerships are increasingly used to de-risk scale-up and broaden application pull-through, as seen in September 2025 when Avantium, LVMH, and Tereos formed an alliance to scale PEF production for packaging end uses, and in December 2025 when CARBIOS and Wankai New Materials signed a definitive agreement to form a joint venture for a 50,000-ton PET biorecycling plant in China. While PET biorecycling is adjacent to biodegradable polymers, these moves shape converter decision-making and investment prioritization in sustainable packaging materials, heightening competition for qualified capacity, brand commitments, and compliant labeling claims.

Competitive Landscape

Global capacity is moderately concentrated: the top five suppliers-BASF, NatureWorks, TotalEnergies Corbion, Eni S.p.A., and Mitsubishi Chemical Group Corporation-held 60% share in 2025. Scale players pursue vertical integration, with BASF producing carbon-capture 1,4-butanediol and TotalEnergies Corbion securing cane offtakes to hedge feedstock risk. Danimer Scientific, GENECIS, and Mango Materials concentrate on high-margin PHA niches, leveraging proprietary strains and carbon-negative routes to sustain gross margins above 40%.

Technology differentiation is intensifying. Evonik’s P(3HB-co-4HB) achieved 95% marine biodegradation and landed pilot salmon-net orders, while PTT MCC Biochem and Mitsubishi Chemical expand BioPBS™ capacity by 30,000 tons. Joint ventures such as Braskem–Gerdau’s steel-gas-to-ethylene plant illustrate cross-sector alliances that monetize industrial CO₂ streams.

Regulatory moats matter: REACH dossiers and FDA food-contact approvals can cost up to USD 2.5 million and extend 24 months, favoring incumbents with established portfolios. Sovereign industrial policy deepens fragmentation as China subsidizes starch-based lines and the EU’s Carbon Border Adjustment Mechanism prioritizes carbon-negative imports.

Bio-degradable Polymers Industry Leaders

NatureWorks LLC

BASF

Mitsubishi Chemical Group Corporation

TotalEnergies Corbion

Eni S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity sits at the intersection of regulation, labeling clarity, and end-of-life infrastructure: packaging formats that regulators explicitly address and municipalities can process at scale. The EU’s Packaging and Packaging Waste Regulation (EU) 2025/40 creates a clear compliance pathway for specific compostable applications (for example, where bio-waste collection and treatment are in place) while also tightening compostability proof requirements through EN 13432 revisions, opening whitespace for resin suppliers and converters that can document performance under stricter timeframes and microplastic limits. In the United States, the FTC Green Guides (16 CFR 260.8) discourage broad “degradable” marketing, which raises the commercial value of certified, qualified claims and application-specific sell sheets for retailers and consumer brands.

Supply localization and technology programs are creating additional whitespace in Asia-Pacific and Europe for tailored grades and regional sourcing. NatureWorks’ April 2026 start-up of a fully integrated 75,000-ton/year PLA facility in Thailand strengthens local availability for converters serving packaging and fibers, supporting shorter lead times and potentially broader qualification activity among ASEAN and broader Asia-Pacific processors. On the innovation side, EU Horizon Europe initiatives such as Bio2PEs (project updates beginning January 2026) and ECOSYSTEM (updated March 2026) are advancing waste-derived feedstocks and multifunctional biopolyesters for food packaging and agricultural films, highlighting a pipeline of formulations aimed at performance gaps (barrier, functionality, and agriculture durability) while maintaining biodegradation or compostability targets. As these programs mature, they expand the range of certified end-of-life options that brand owners can specify, particularly in agricultural films and regulated packaging items where disposal pathways and labeling are under closer scrutiny.

Recent Industry Developments

- April 2026: NatureWorks announced the grand opening of its fully integrated Ingeo PLA biopolymer manufacturing facility at the Nakhon Sawan BioComplex in Thailand, with about 75,000 metric tons of annual capacity. The site integrates key steps from local feedstock conversion through polymer production, strengthening regional supply for packaging and fibers and reducing dependence on single-region manufacturing.

- March 2025: NatureWorks launched the Ingeo Extend PLA platform aimed at biaxially oriented film applications, targeting improved processing latitude for packaging converters. The launch supports a shift from basic compostable substitution toward performance-tuned grades that can compete in higher-throughput film lines.

- June 2024: BASF advanced its biopolymers portfolio positioning for compostable applications, aligning with tightening packaging and waste requirements across major markets. The move reinforces incumbent advantages tied to certification-ready grades and established converter relationships in flexible packaging.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers biodegradable polymer materials sold for use in finished products, where the polymer is designed to break down under defined biological conditions and is supplied in commercial form such as resin or compound.

Scope exclusions: We exclude durable goods made mainly from conventional plastics, as well as recycling-only solutions that do not rely on biodegradation behavior.

Segmentation Overview

- By Feedstock

- Sugarcane and Sugar Beets

- Corn and Other Starch Crops

- Cellulose and Wood Biomass

- Waste Vegetable Oils and Fats

- Algal and Microbial Biomass

- By Type

- Starch-Based Plastics

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polyesters (PBS, PBAT and PCL)

- Cellulosic Derivatives

- By End-user Industry

- Packaging

- Consumer Goods

- Textile

- Agriculture

- Healthcare

- Other End-user Industries (Automotive, Construction, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame demand and supply for biodegradable polymers, and to keep input assumptions realistic across packaging, agriculture, consumer goods, and other end uses. Public materials such as US EPA waste and materials content, Eurostat and national statistics office publications, UN Comtrade trade data, OECD environment indicators, and peer-reviewed polymer science journals were referenced to understand policy signals, trade flows, and adoption momentum.

Alongside these, we reviewed company annual reports, investor presentations, product specification sheets, and credible press coverage to map capacity announcements and commercialization timing. Where needed, paid subscriptions for company financials and intelligence, patent databases, and import-export shipment level intelligence were used to cross-check supplier presence, technology focus, and the direction of pricing. These examples are not exhaustive, and other sources were used to collect, validate, and clarify the data that feeds the model.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with resin producers, compounders, converters, distributors, and large end users, so we could confirm what is being bought and what drives selection versus conventional alternatives. For a global market like this, respondent inputs were checked across APAC, EMEA, and the Americas to validate adoption differences linked to regulation, composting infrastructure, and brand commitments, then to close gaps where public data is thin.

Respondent feedback also helped clarify how companies describe biodegradable polymer grades in procurement, since category definitions vary by region and downstream application.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 14% | Managers: 48% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built with a top-down view first. We used production and trade signals to reconstruct a realistic global demand pool for biodegradable polymer resin consumption, then split it by major use areas where adoption is most visible. To keep this grounded, we corroborated totals with selective bottom-up approximations, such as sampled supplier volume indications, channel checks with converters, and ASP times volume checks for high-usage polymer families. Those cross-checks were used to adjust any over- or under-counting.

The model uses market fingerprints that can be checked in practice, including compostability regulation rollouts, food service and retail packaging conversion activity, composting and industrial treatment capacity availability, reported capacity additions by polymer family, and typical price spreads versus conventional plastics. Forecasting relies mainly on scenario analysis, since policy timing and infrastructure buildout can change the growth path. Scenarios were aligned to what primary respondents see as feasible in their regions. When bottom-up inputs were missing for smaller countries or niche uses, we applied proxies using per-capita packaging demand and industry mix, then reviewed them again during validation.

Data Validation & Update Cycle

Validation was done by checking model outputs against independent signals, such as trade direction, capacity changes, and end-use conversion activity, so totals do not drift away from what the industry can physically supply and consume. When variances were large, the assumptions behind them were re-tested through follow-up calls, especially where a country showed adoption patterns that did not match its policy or infrastructure readiness.

Before sign-off, the model and written logic go through multi-step analyst reviews where calculations, unit conversions, and year-on-year movements are checked for consistency. Reports are refreshed annually, with interim updates when a material event occurs, such as a major capacity start-up, a policy change, or a sustained price shift. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Bio Degradable Polymers Market Size Measured Against Other Published Estimates

Published market values for biodegradable polymers can differ widely because the scope can shift between volume-based sizing and revenue-based sizing, and because polymer boundaries are not always treated the same way across studies. The benchmark table makes the spread easy to see, and it also provides context for why numbers diverge once you look at what each source counts.

The table shows a volume-based market size here, while some other sources publish revenue totals, which move with assumed ASP progression, currency timing, and product mix. In Mordor Intelligence's model, the market is kept tied to biodegradable polymer resin volumes (in tons), and revenue-style expansions such as adjacent substrates or broad packaging value chains are not blended into the total, which is a common reason for higher published USD figures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.08 M (2026) | |

| Global Consultancy A | USD 11.60 B (2025) | Reported as a value market in USD, which is sensitive to assumed ASP progression and product mix, and the sizing basis does not clearly separate resin volume from downstream packaging value. |

| Industry Data Platform B | USD 10.86 B (2024) | Uses a revenue framing with broad segment buckets, so differences in what counts as a biodegradable polymer category and how substrates are treated can lift the total versus a resin volume approach. |

Taken together, the gap is less about math and more about definitions, units, and what sits inside the counted boundary. By keeping inputs tied to observable adoption signals and documenting the main assumption switches, the estimate stays traceable and repeatable when the market is updated.

Key Questions Answered in the Report

What is the projected global volume for bio-degradable polymers by 2031?

Market is forecast to reach 2.35 million tons in 2031, reflecting a 16.78% CAGR from 2026 to 2031.

Which polymer type is expanding the quickest?

Polyhydroxyalkanoates (PHA) are advancing at a 20.84% CAGR on the strength of marine-degradability certifications and medical approvals.

How do prices compare with conventional plastics?

Commodity PLA averages USD 2.80–3.50 per kg, versus USD 1.20–1.40 for virgin polyethylene, while premium PHA grades sell for USD 5.00–6.50 per kg.

Which region will add the most capacity through 2031?

Asia-Pacific is set to post a 19.24% CAGR as China and India commission large PBAT, PLA, and starch-blend lines.

Page last updated on: