Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

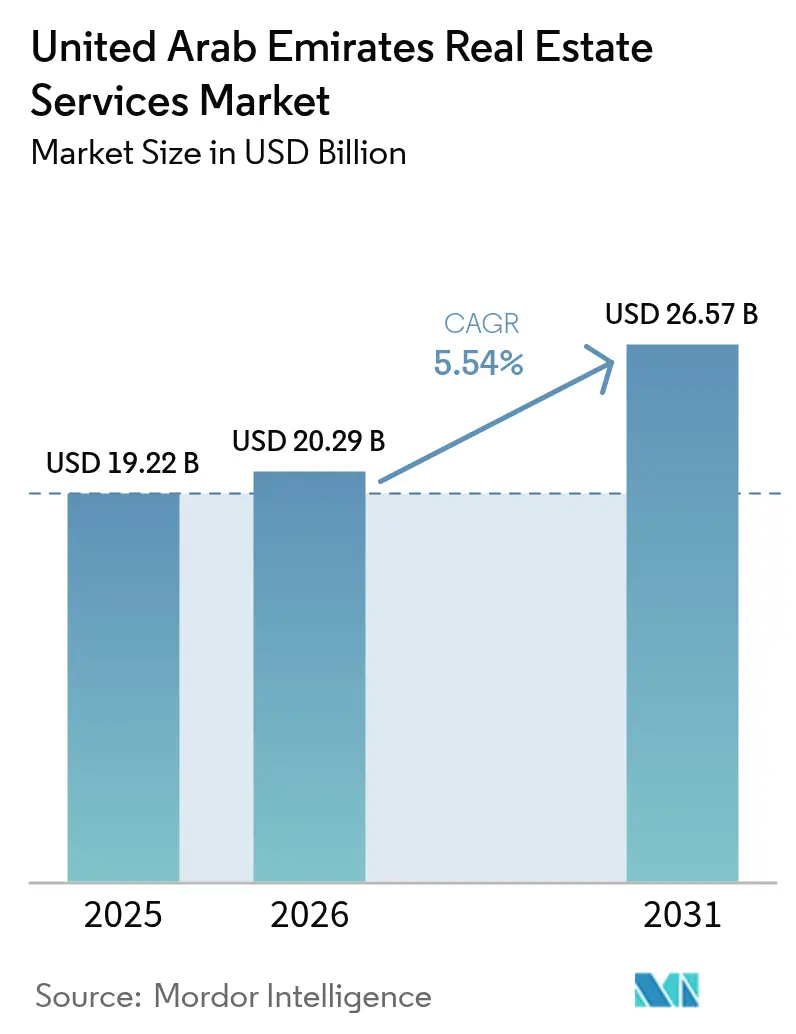

| Base Year Market Size (2025) | USD 19.22 Billion |

| Market Size (2026) | USD 20.29 Billion |

| Market Size (2031) | USD 26.57 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Real Estate Services Market Analysis by Mordor Intelligence

The United Arab Emirates Real Estate Services Market size is projected to be USD 19.22 billion in 2025, USD 20.29 billion in 2026, and reach USD 26.57 billion by 2031, growing at a CAGR of 5.54% from 2026 to 2031.

Surging off-plan residential sales, corporate migration into Grade A offices, and technology-enabled facilities management are tilting the revenue mix away from one-off brokerage fees toward recurring property-management contracts. Office rents jumped 16.8% in Dubai and 31.3% in Abu Dhabi through Q3 2025, while logistics yields held near 7%, widening the advisory opportunity in commercial assets. Foreign buyers accounted for 62% of Abu Dhabi’s residential sales growth in 2025, intensifying the need for RICS-compliant valuation and cross-border portfolio services. At the same time, 6,714 new brokers entered Dubai during H1 2025, compressing commissions even as private developers lifted off-plan fees to 10-12%. Digital portals, led by Property Finder’s AI-driven marketplace and Dubai Land Department’s tokenization pilot, are automating listings and settlements, nudging intermediaries to pivot toward high-skill advisory mandates.

Key Report Takeaways

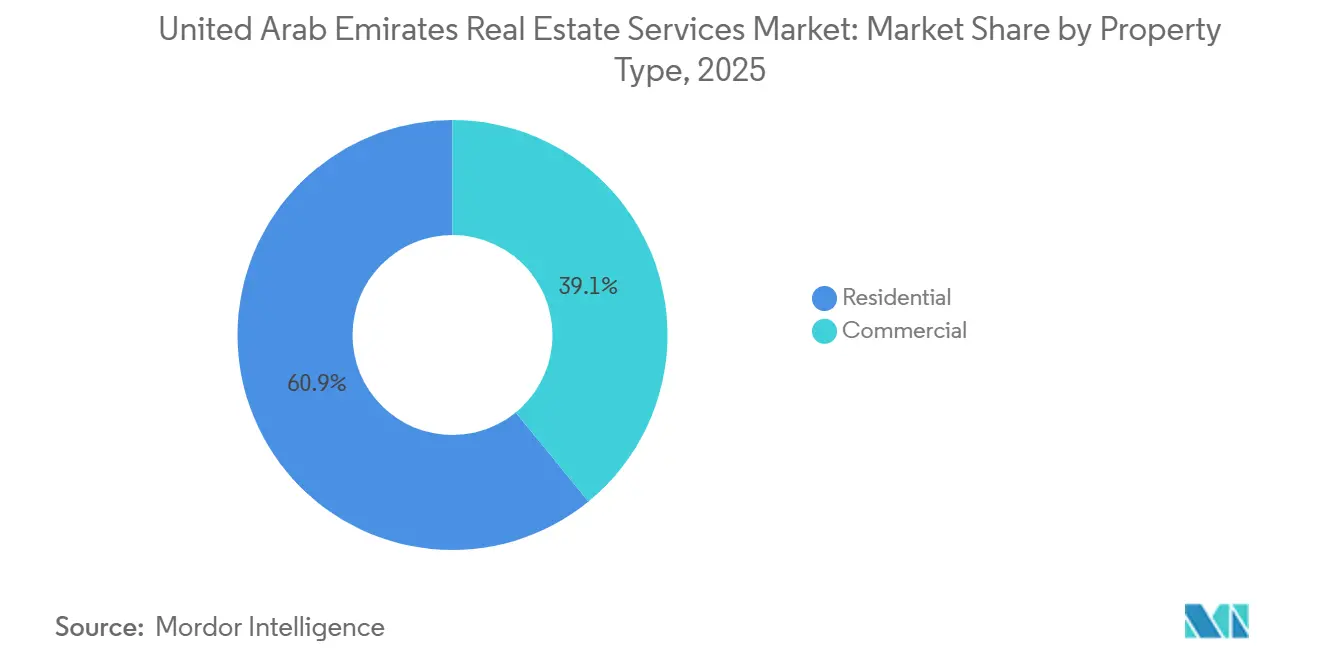

- By property type, residential services led with 60.9% of the UAE real estate services market share in 2025, while commercial services are projected to expand at a 5.89% CAGR to 2031.

- By service, brokerage accounted for a 42.3% share of the UAE real estate services market size in 2025, and property management is advancing at a 6.12% CAGR through 2031.

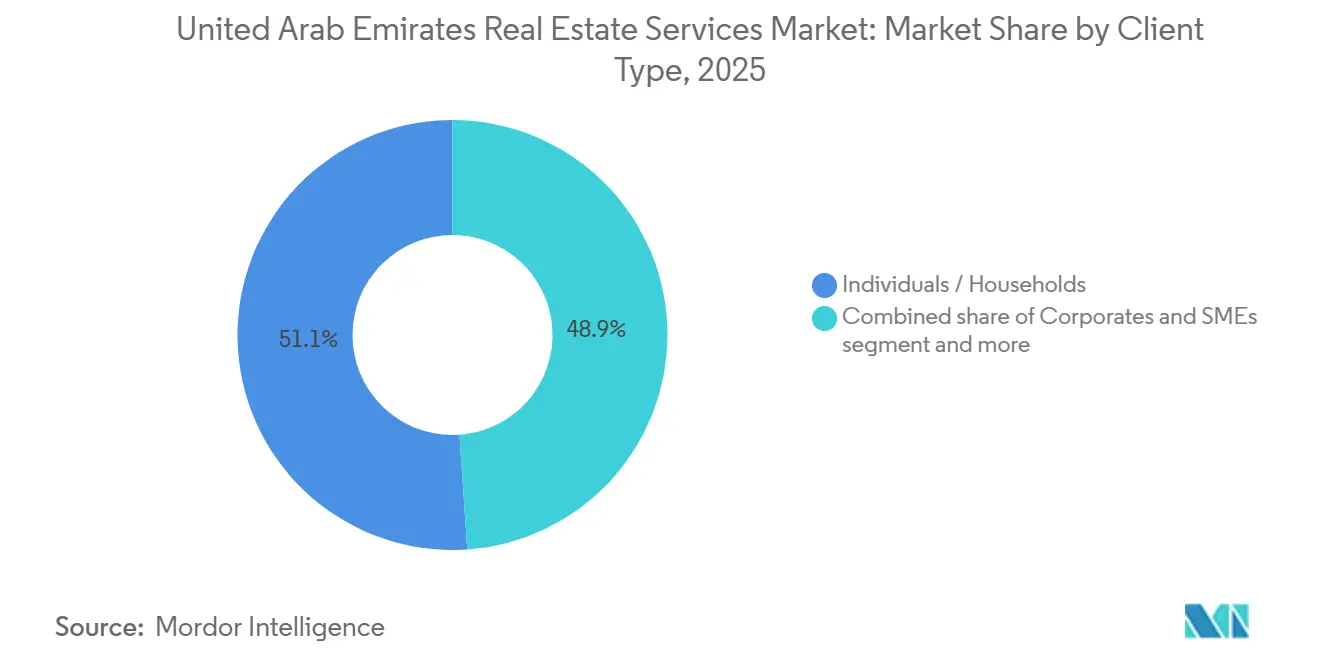

- By client type, individuals and households held 51.1% of the UAE real estate services market share in 2025, whereas corporates and SMEs are forecast to grow at a 6.23% CAGR to 2031.

- By geography, Dubai commanded 58.4% revenue share in 2025, and Ras Al Khaimah is set to post the fastest 6.48% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Real Estate Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of rental and mixed-use portfolios is boosting asset and facilities management demand | +1.3% | Dubai, Abu Dhabi, Ras Al Khaimah | Long term (≥ 4 years) |

| High residential and off-plan transaction volumes are driving brokerage and advisory revenues | +1.2% | Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Foreign investor inflows are increasing demand for valuation and property management services | +1.0% | Abu Dhabi, Dubai | Medium term (2–4 years) |

| Government digital land and tenancy platforms streamlining transaction processes | +0.8% | Nationwide | Medium term (2–4 years) |

| Rising PropTech adoption is enhancing digital marketing and leasing efficiency | +0.7% | Nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Expansion of Rental and Mixed-Use Portfolios Boosting Asset and Facilities Management Demand

Developers are retaining stock to chase yield, pivoting revenue toward long-term asset management. Nakheel manages 55,000 units, and Dubai Holding oversees 18,000 units across maturing communities that now require predictive maintenance and energy benchmarking. Aldar and Mubadala’s USD 2.4 billion retail platform and USD 816 million Masdar City joint venture bundle leasing, FM, and ESG oversight within the capital stack. Specialist FM firms such as Farnek locked USD 187.7 million in 2024 contracts by offering drone façade checks and IoT sensors. Players investing in data-driven operations rather than low-cost manpower secure longer, higher-margin mandates.

High Residential and Off-Plan Transaction Volumes Driving Brokerage and Advisory Revenues

Off-plan deals captured 65% of Dubai’s residential volume in 2025 and generated USD 77.8 billion, pushing brokerage commissions to USD 878 million in the first half alone[1]Dubai Land Department, “Off-Plan Transactions H1 2025,” dubailand.gov.ae. Private developers raised commission slabs to 10-12% to accelerate absorption, while 129,600 new investors entered the emirate, enlarging the prospect pool. Abu Dhabi mirrored the momentum with USD 38.6 billion in transactions, up 44% year on year, as foreign buyers fueled 62% of residential growth. The short-cycle surge improves near-term revenue but heightens dependence on timely project deliveries. Firms hedging exposure with secondary-market listings and diversified service lines stand better protected when off-plan appetite cools.

Foreign Investor Inflows Increasing Demand for Valuation and Property Management Services

International capital now underpins a growing share of transactions, making third-party valuations a gatekeeper for mortgage approvals and tax compliance. Global investors from India, the United Kingdom, and the GCC request RICS-aligned appraisals and ESG-ready facility upkeep, prompting CBRE, JLL, and Knight Frank to scale valuation teams and pursue ISO 14001 credentials. Dubai’s real-estate-tokenization pilot foresees USD 16.3 billion worth of fractional assets by 2033, adding complexity that pushes valuation toward real-time blockchain-audited models. Providers fusing PropTech with cross-border regulatory insight can capture a larger wallet share per client.

Government Digital Land and Tenancy Platforms Streamlining Transaction Processes

Dubai Land Department’s Digital Sale service, AI Investor Assistant, and Madmoun QR-code regime cut paperwork and curb mispricing by auto-correcting 29% of online ads in 2025. Instant settlement through DubaiPay and optional cryptocurrency clearing reduces clearance time from days to minutes. Abu Dhabi’s tenancy-contract portal offers parallel utility, signaling federal convergence by 2027. As core transactions commoditize, brokerages that add tax structuring, compliance navigation, and portfolio-optimization advice defend margins. API hooks into government stacks, such as Emaar’s Vyom platform processing USD 1.1 billion in 2024 payments, illustrate the new normal.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commission pressure from intense broker competition and digital models | -0.9% | Nationwide | Short term (≤ 2 years) |

| Real estate price cycle volatility impacting transaction-based revenues | -0.6% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Stringent licensing and compliance requirements increasing operating costs | -0.4% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commission Pressure from Intense Broker Competition and Digital Models

The broker count in Dubai hit 29,577 after 6,714 new registrations in H1 2025, crowding a finite deal pool. Developers pay up to 12% on speculative launches, yet master developers cap at 5%, forcing agents to pick between volume and margin[2]Arabian Business, “Dubai Developers Lift Off-Plan Commissions,” arabianbusiness.com. Aggregators like Property Finder shift marketing budgets onto brokers via pay-per-lead plans while retaining client data, squeezing smaller shops. Only agencies that pair top-decile productivity with high-value consulting can absorb rising fixed costs.

Real Estate Price Cycle Volatility Impacting Transaction-Based Revenues

Dubai booked 270,000 deals worth USD 249.4 billion in 2025, but commissions were front-loaded in H1, highlighting lumpiness tied to sentiment swings. Off-plan sales, 65% of volume, remain vulnerable to construction delays or financing shocks. Brokerages without counter-cyclical income, such as lease renewals, property management, or valuation, may struggle when sales stall. Firms that balance residential, commercial, and logistics clients smooth earnings as asset cycles rarely align.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Residential Leads While Commercial Accelerates

Residential services held 60.9% of the UAE real estate services market in 2025, buoyed by USD 77.8 billion worth of off-plan apartment sales that captured 65% of residential volume. Commercial services are growing fastest at a 5.89% CAGR as Grade A offices inside DIFC approached full occupancy and Abu Dhabi rents rose 31.3% through Q3 2025. Apartment leasing dominates because investors favor cash-yielding units in master communities, whereas villa demand skews toward ultra-high-net-worth end users. Logistics remains small yet delivers the highest 7% yield, prompting brokerages to add warehouse site-selection and leaseback structuring to remain competitive.

Prime residential corridors such as Palm Jumeirah and Saadiyat Island now layer concierge management and branded-residence advisory on top of core brokerage. In commercial, flexible offices and life-science labs are capturing premiums as corporates chase ESG-certified space. Knight Frank guided 1.28 million square feet of new corporate demand in 2024, led by tech and professional services, indicating runway for advisory firms with tenant-representation verticals.

By Service: Brokerage Still Largest, Property Management Scaling Fast

Brokerage retained 42.3% of the UAE real estate services market share in 2025 after commissions spiked to USD 878 million in Dubai alone. Property management posts the quickest 6.12% CAGR, shielded by annuity-style contracts tied to lease duration and building size. Farnek’s USD 187.7 million contract haul and Emrill’s One Za'abeel mandate, covering 530,000 square meters, show developer trust migrating toward technology-rich FM partners.

Valuation and advisory, though smaller, monetize regulatory complexity and foreign investor demand. The UAE real estate services market size for valuation is projected to expand alongside planned tokenization worth USD 16.3 billion, demanding blockchain-validated pricing. Brokerages that bolt on FM, tenant vetting, and rent collection hedge cyclicality and amplify lifetime client value.

By Client Type: Corporates and SMEs Gain Momentum

Individuals still accounted for 51.1% of 2025 revenue, but corporates and SMEs are pacing a 6.23% CAGR thanks to new business registrations and headquarters relocations[3] DIFC, “Operating Review 2025,” difc.ae. Business services and technology absorbed 64% more office space in 2024 than in 2023, often on flexible terms that outsource FM to landlords. Institutions and family offices form a lucrative “other” segment demanding ESG stewardship, tax planning, and multi-asset rebalancing.

Corporate clients favor advisors who marry site selection with fit-out and operational analytics. Aldar’s USD 10.3 billion Dubai pipeline and USD 16.3 billion Al Maryah Island expansion underline how sovereign-linked developers want end-to-end management, pushing independents to specialize or partner for scale.

Geography Analysis

Dubai controlled 58.4% of the UAE real estate services market share in 2025, the largest slice in the country. The emirate logged 270,000 deals worth USD 249.4 billion that year, underpinned by full-cycle digital processing. Prime office rents climbed 16.8% through Q3 2025 as DIFC vacancies tightened. QR-verified ads and instant DubaiPay settlements now cut closing times to minutes. Developers such as Emaar use in-house apps to fold brokerage, leasing, and facilities management into one ecosystem.

Abu Dhabi ranked second, registering USD 38.6 billion in transactions during 2025. Grade A office rents jumped 31.3% through Q3 2025, reflecting tight supply in the capital’s core. Foreign buyers drove 62% of residential sales growth and demanded RICS-compliant valuations. The USD 16.3 billion Al Maryah Island expansion is set to double prime office stock and add 3,000 waterfront homes by 2030. Green-building subsidies and LEED mandates keep ESG consulting in steady demand.

Ras Al Khaimah is projected to post the fastest 6.48% CAGR to 2031 within the UAE real estate services market size, thanks to lower land costs. The 300,000-square-meter THi Smart Manufacturing Park is anchoring new industrial-leasing and FM contracts. Sharjah, Ajman, Umm Al Quwain, and Fujairah expand more gradually on affordable housing that favors low-fee agents. Multi-emirate service providers that master each municipality’s rules and price points can scale without margin loss.

Competitive Landscape

Competition is intense at the transactional layer, where 29,577 registered brokers chase higher but thinning commissions and digital portals own client origination. Property Finder’s USD 170 million raise and Bayut’s pay-per-lead model externalize marketing costs while absorbing data, forcing agents to compete on execution speed and advisory finesse. Master developers such as Emaar and Dubai Holding harness in-house platforms like Vyom and Hawkeye to internalize the sales funnel.

Mid-stream consolidation gains steam in facilities management, with Farnek and Emrill picking up multi-year, multi-property mandates that leverage IoT sensors and predictive analytics. Aldar and Mubadala’s joint retail and logistics ventures, cumulatively topping USD 8.2 billion, illustrate vertical integration that locks in recurring income across development, leasing, and FM. Niche specialists defend turf by focusing on logistics brokerage, tokenized-asset valuation, or LEED-compliant FM.

Technology remains the decisive differentiator. The DIFC PropTech Hub nurtures startups in virtual staging and blockchain titles, while the Dubai Land Department’s AI governance modified 29% of 2025 listings, proving that algorithmic oversight curbs mis-priced ads. Firms embedding API connectivity, ESG dashboards, and token-ready appraisal engines outpace peers reliant on manual inputs.

United Arab Emirates Real Estate Services Industry Leaders

Emaar Properties

Aldar Properties

DAMAC Properties

Nakheel

Dubai Properties

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Aldar and Dubai Holding added two Dubai plots worth USD 10.3 billion to deliver 14,000 homes, extending Aldar’s integrated brokerage-to-FM mode.

- January 2026: Property Finder secured USD 170 million from Mubadala to scale its AI-driven aggregation platform.

- January 2026: Sobha Realty unveiled the USD 13.6 billion Sobha Sanctuary community with 20,000 planned homes, anchoring long-term FM revenue.

- January 2026: Meraas announced an 18 million square-foot expansion of Dubai Design District aimed at LEED Silver certification.

United Arab Emirates Real Estate Services Market Report Scope

By Property Type

| Residential | Apartments and Condominums |

| Villas and Landed Houses | |

| Commercial | Office |

| Retail | |

| Logistics | |

| Others |

By Service

| Brokerage Services |

| Property Management Services |

| Valuation Services |

| Others |

By Client Type

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Emirate

| Dubai |

| Abu Dhabi |

| Sharjah |

| Ras Al Khaimah |

| Rest of UAE |

| By Property Type | Residential | Apartments and Condominums |

| Villas and Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Logistics | ||

| Others | ||

| By Service | Brokerage Services | |

| Property Management Services | ||

| Valuation Services | ||

| Others | ||

| By Client Type | Individuals / Households | |

| Corporates & SMEs | ||

| Others | ||

| By Emirate | Dubai | |

| Abu Dhabi | ||

| Sharjah | ||

| Ras Al Khaimah | ||

| Rest of UAE | ||

Key Questions Answered in the Report

What was the size of the UAE real estate services sector in 2025 and what value is it forecast to reach by 2031?

It stood at USD 19.22 billion in 2025 and is projected to hit USD 26.57 billion by 2031, reflecting a 5.54% CAGR.

Which service line is expanding fastest within UAE real-estate services?

Property management is the pace-setter, advancing at a 6.12% CAGR as landlords prioritize stable fee income over one-off brokerage commissions.

Why are developers in the UAE pivoting toward long-term property-management contracts?

Retaining rental stock delivers predictable cash flow; large portfolios such as Nakheel’s 55,000 units and Dubai Holding’s 18,000 units now require IoT-enabled facilities management that sustains margin beyond initial sales.

How are foreign buyers shaping demand for valuation services in the UAE?

Overseas investors drove 62% of Abu Dhabi’s 2025 residential growth, prompting a surge in RICS-compliant appraisals and cross-border tax reporting that local firms now bundle with portfolio management.

Which emirate is expected to record the quickest growth through 2031?

Ras Al Khaimah, helped by projects like the 300,000-square-meter THi Smart Manufacturing Park, is set to pace a 6.48% CAGR.

What technology trends are redefining brokerage operations across the UAE?

AI-driven listing portals such as Property Finder, blockchain tokenization pilots, and Dubai Land Department’s QR-verified advertising are automating discovery and settlement, pushing brokers to focus on high-skill advisory.

Page last updated on: