Magnesium Hydroxide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

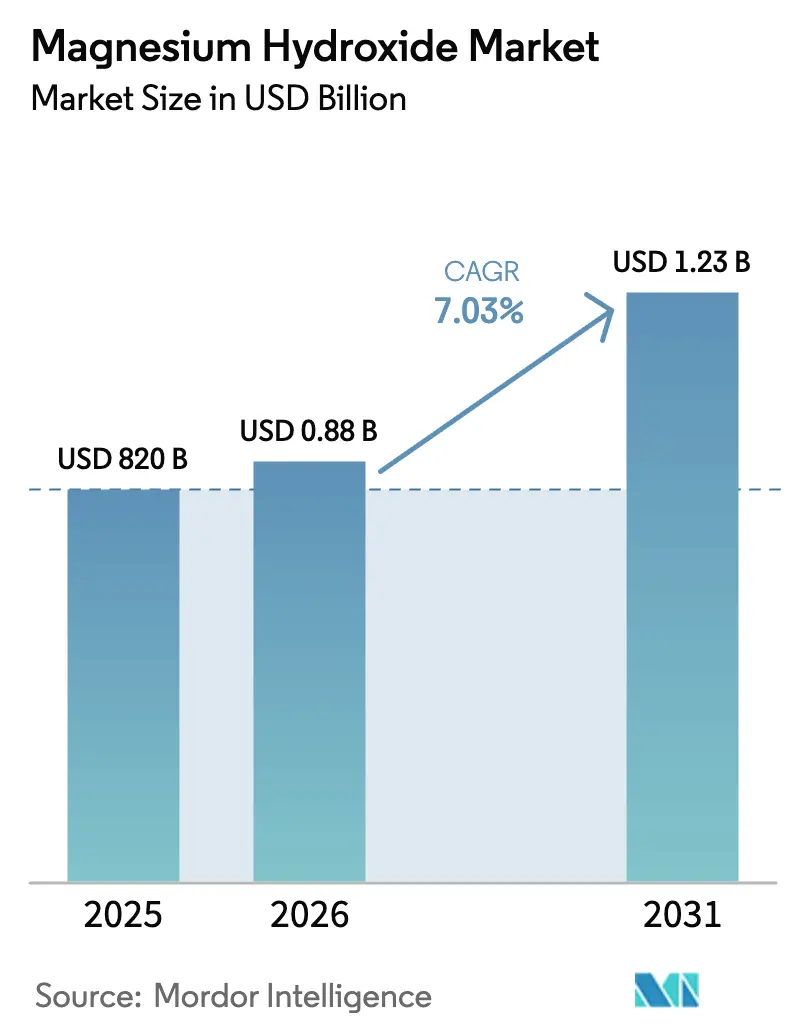

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

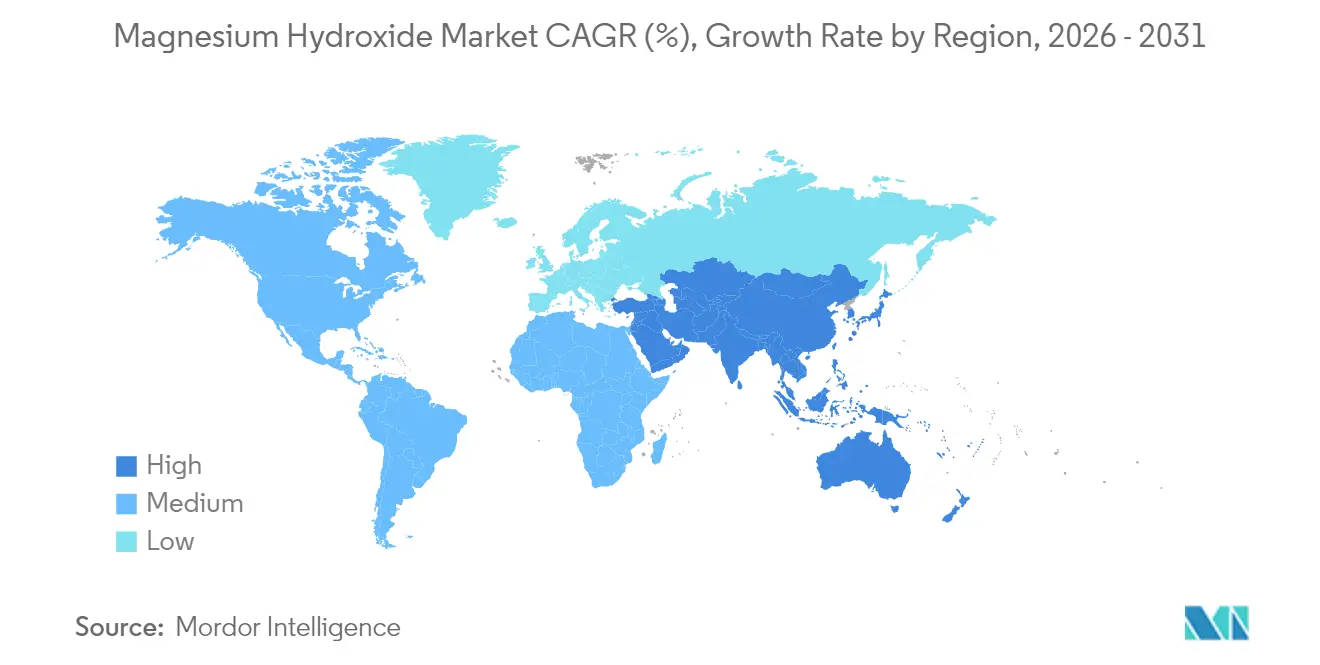

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

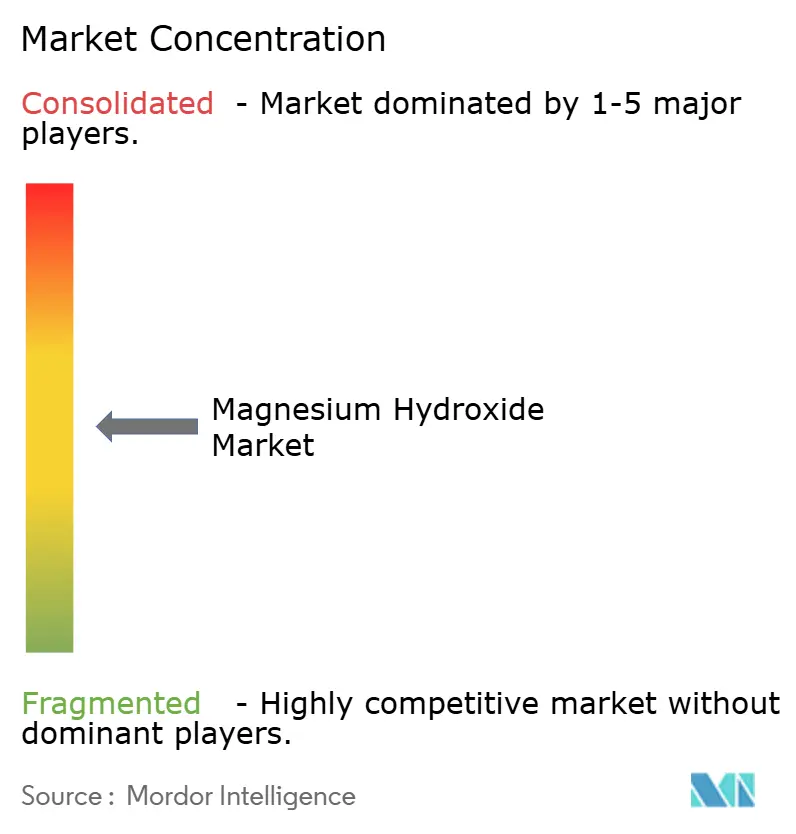

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnesium Hydroxide Market Analysis by Mordor Intelligence

The Magnesium Hydroxide Market size is expected to grow from USD 820 million in 2025 to USD 877.65 million in 2026 and is forecast to reach USD 1.23 billion by 2031 at 7.03% CAGR over 2026-2031. Growth stems from regulatory moves that favor non-halogenated flame retardants, a broadening pharmaceutical footprint, and a steady rise in environmental technologies that consume high-purity grades. Flame-retardant demand remains the anchor, yet carbon-capture, ocean-alkalinization, and circular-brine projects are opening fresh revenue pools. Industrial users are shifting to slurry grades for safer dosing and worker protection, while healthcare buyers pay premiums for ultra-pure powders. Regional supply chains continue to move toward Asia-Pacific, where large captive feedstock, bigger polymer processing clusters, and desalination brine projects coexist to keep costs in check. Midstream integration, acquisitions targeting niche know-how, and step-change innovations such as electrodialysis-generated magnesium hydroxide keep competitive pressures intense.

Key Report Takeaways

- By form, slurry products held 53.62% of magnesium hydroxide market share in 2025; suspension/paste grades are projected to post the fastest 7.09% CAGR to 2031.

- By grade, industrial variants accounted for 65.48% of magnesium hydroxide market share in 2025, while pharmaceutical grades are set to pace the field with an 8.32% CAGR through 2031.

- By manufacturing method, chemical precipitation delivered 50.54% of magnesium hydroxide market size in 2025, whereas brine-electrolysis co-products are forecast at an 8.94% CAGR to 2031.

- By application, industrial uses represented 63.81% of magnesium hydroxide market size in 2025; pharmaceuticals and nutraceuticals are primed for a 9.15% CAGR to 2031.

- By geography, Asia-Pacific commanded 46.72% of magnesium hydroxide market share in 2025 and is projected to register an 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Magnesium Hydroxide Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift away from halogenated flame-retardants | +1.8% | EU, North America, global spill-over | Medium term (2-4 years) |

| Tightening wastewater discharge norms | +1.5% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Growing demand from pharmaceutical industry | +1.2% | North America, Europe, APAC | Long term (≥ 4 years) |

| Increasing demand from industrial manufacturing | +1.0% | Asia-Pacific core, MEA spill-over | Medium term (2-4 years) |

| Circular sourcing from desalination brine | +0.8% | Middle East, Australia, Mediterranean | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Away from Halogenated Flame-Retardants

Governments in the EU and North America are phasing out brominated and chlorinated retardants in electronics, construction panels, and wire insulation, prompting polymer compounders worldwide to convert to magnesium hydroxide masterbatches that release only water vapor and MgO at 330 °C instead of corrosive hydrogen halides. The compound also outperforms aluminum trihydroxide above 300 °C, making it suitable for polycarbonate and PBT[1]Huber Advanced Materials, “Flame Retardant Hydroxides,” huberadvancedmaterials.com . Standardization by global OEMs means a regulatory change in one region now cascades through supply chains, multiplying demand across Asia-Pacific production hubs. Fire-test data confirm parity with ATH at loading levels 30 % lower, preserving mechanical properties and reducing weight, thus fueling adoption in transport and appliance casings.

Tightening Wastewater Discharge Norms

Wastewater codes increasingly cap effluent pH and heavy-metal loads, and magnesium hydroxide slurries buffer at pH 10.5, providing safer handling than caustic soda at pH 14 while supplying essential Mg nutrients to biological reactors. Municipal digesters in the United States cut alkali usage by 36% when switching from NaOH to magnesium hydroxide, even after higher unit prices, as dosage volumes fell and sludge dewatering improved. Asia’s push to curb industrial pollution accelerates first-time deployments in food, textile, and electronics clusters, driving immediate volume orders for ready-to-dose slurry grades.

Growing Demand from Pharmaceutical Industry

Pharmaceutical manufacturers are broadening usage from antacids into renal phosphate binding and novel nutraceuticals after EFSA cleared magnesium L-threonate as a novel ingredient in 2024[2]EFSA Panel, “Safety of Magnesium L-threonate,” efsa.europa.eu. Clinical evidence indicates lower vascular calcification risk than calcium binders, and new IBS guidelines list magnesium hydroxide as a frontline osmotic laxative. These shifts push API-grade purity levels, lifting premium pricing and spurring capacity additions in Europe and North America. Contract development organizations cite double-digit order growth for powder lots meeting ICH Q3D elemental-impurity limits.

Increasing Demand from Industrial Manufacturing Industry

Refiners inject magnesium hydroxide into crude-unit desalter trains to neutralize naphthenic acids, cutting corrosion costs in high-TAN crudes. Steelmakers and cement plants dose nanoparticle forms for biocide control, and sewer-network operators spray Mg(OH)₂ onto concrete to arrest biogenic sulfide attack, extending pipe life by 20 years. Such multisector adoption ensures base-load consumption that insulates suppliers from cyclic swings in individual end-markets.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of caustic magnesia feedstock | -1.2% | Import-dependent regions worldwide | Short term (≤ 2 years) |

| Competition from synthetic aluminum trihydroxide | -0.8% | North America, Europe | Medium term (2-4 years) |

| Availability of other alkaline bulk chemicals | -0.6% | Global, cost-sensitive uses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Caustic Magnesia Feedstock

China controls more than two-thirds of global magnesite, and energy-policy-driven shutdowns in 2021 spiked export prices fourfold, compressing margins at downstream magnesium hydroxide plants. Quality swings add cost: high-iron MgO demands extra purification, lowering yield and raising waste disposal bills. Diversification into serpentine ores and waste-slag recovery offers long-run relief, yet these routes require CAPEX-heavy kilns and process licenses that few midsized producers can underwrite, leaving the magnesium hydroxide market exposed to periodic supply-side shocks.

Competition from Synthetic Aluminum Trihydroxide

ATH retains entrenched logistics and a robust recycling chain, letting it undercut magnesium hydroxide in cable compounds that operate below 250 °C. Surface-treated ATH grades now withstand 350 °C, overlapping magnesium hydroxide’s turf and eroding its differentiation in high-temp plastics. Budget-focused buyers in parts of Latin America and Africa weigh price over toxicity profiles, slowing magnesium hydroxide penetration even as regulations tighten elsewhere. Suppliers respond by bundling technical-service packages but face a persistent cost gap of roughly USD 200-250 per metric ton versus ATH.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Slurry Dominance Drives Operational Efficiency

Slurry products delivered 53.62% of magnesium hydroxide market share in 2025 as industrial users favored dust-free handling and automated dosing systems that cut labor hours and reduce inhalation hazards. Suspension/paste variants are forecast to expand at a healthy 7.09% CAGR, propelled by concrete-corrosion lining jobs and 3D-printed building parts needing thixotropic rheology. Powder grades, indispensable in pharmaceuticals and nutraceutical blends, retain relevance but post slower growth because additional equipment and explosion-mitigation steps add cost in bulk chemical sites.

Process engineers appreciate slurry’s buffered pH and moderate ionic strength, which safeguard downstream biology in aeration basins. Recent rheology breakthroughs use chelating dispersants to keep solids higher than 60 wt%, slicing freight bills per active unit. Research on ionic-exchange membrane crystallizers hints at generating pharmaceutical-grade slurries directly from brine, bypassing kiln calcination and milling. These inventions, if scaled, could reorder cost curves and redefine the magnesium hydroxide market size for higher-grade streams through 2031.

By Grade: Industrial Applications Anchor Market Foundation

Industrial grades occupied 65.48% of magnesium hydroxide market share in 2025 as flame-retardant compounding, flue-gas desulfurization, and wastewater neutralization continued to buy bulk quantity at moderate purity. Price-sensitive plastics choose 96-97 % Mg(OH)₂ assays, balancing cost and fire performance. Pharmaceutical grades, though only a fraction of tonnage, are set for an 8.32% CAGR owing to renal-care binders, novel laxatives, and high-dose nutraceutical powders now EU-approved. Food-grade demand grows in chewing-gum bases and sugar refining but trails pharma in momentum.

Regulators push for tighter heavy-metal specs—arsenic below 2 ppm and Pb below 0.5 ppm—forcing new purification trains. Some Chinese refineries deploy novel ion-exchange columns to hit sub-ppm boron for injectable suspensions bound for U.S. FDA filings. The magnesium hydroxide market size for pharma is small but commands margins topping USD 4,500 per ton, quadruple bulk industrial rates, justifying tailored logistic channels, dedicated dryers, and GMP-validated warehouses.

By Manufacturing Method: Chemical Precipitation Maintains Technological Leadership

Tried-and-tested precipitation routes using brucite ore and caustic soda maintained 50.54% of magnesium hydroxide market size in 2025 because plants are fully depreciated and permit rapid debottlenecking via agitator upgrades. Brine-electrolysis coproducts, however, are roaring ahead at 8.94% CAGR. Every cubic-meter of desalination brine holds 1.3 g of magnesium: once regarded as waste, it now yields Mg(OH)₂ in situ and slashes disposal charges.

Energy-recovery schemes feed chlorine and caustic back into nearby chlor-alkali cells, closing loops and cutting net emissions. Seawater-lime routes still serve small island grids where limestone is cheaper than shipping brucite. Pilot schemes in Greece combine solar calcined lime with wave-powered agitators to keep CO₂ intensity below 300 kg/t. Over the forecast window, incremental capital will chase flexible hybrid plants able to swing among solid ore, brine, and serpentine feed, thereby smoothing raw-material shocks that often buffet the magnesium hydroxide market.

By Application: Industrial Demand Anchors Market Growth

Industrial end-uses absorbed 63.81% of magnesium hydroxide market size in 2025, spanning flame-retardant plastics, FGD, refinery desulfurization, and sewer-pipe corrosion inhibitors. Polymer compounders in Asia deploy high-loading masterbatches that triple ignition delay in PP furniture while preserving tensile elongation. Pressure-oxidation gold mines in the Americas ran pilot neutralization steps and cut lime sludge by 40%, citing smoother pH control between 9.5 and 10.2.

Pharmaceutical and nutraceutical buyers will clock a 9.15% CAGR through 2031. EFSA clearance for cognitive-health formats lifts powder demand, compounded by rising CKD prevalence that drives oral phosphate binders. Medical-grade magnesium hydroxide industry suppliers advertise BET surface areas exceeding 180 m²/g for rapid ion exchange. The result is a profitable bifurcation: bulk industrial tonnage secures plant utilization, whereas small-lot GMP streams deliver margin lift and insulating diversification.

Geography Analysis

Asia-Pacific generated 46.72% of global revenue in 2025 and will accelerate at an 8.56% CAGR to 2031 as China, India, and Southeast Asia boost polymer compounding, electronics assembly, and municipal wastewater capacity. Domestic magnesite ore and coal-fired kilns confer cost advantage, yet Beijing’s energy-intensity rules create intermittent supply gaps, prompting Vietnam and Australia to eye serpentine and brine assets. India’s pharmaceuticals corridor in Gujarat scales tooth-paste and antacid lines, soaking up pharma-grade powders, while Singapore’s petrochem complex secures slurry contracts for cracker wastewater.

North America retains a balanced demand base across industrial and healthcare sectors. U.S. municipalities, incentivized by federal infrastructure funds, retrofit anaerobic digesters with magnesium hydroxide dosing, spurring multi-year supply contracts. Canadian mining camps combat acid-rock drainage with onsite mobile slurry plants, pairing them with reagent recovery to shrink truck traffic. Acquisition deals, notably Calix’s move for Inland Environmental Resources, aim to merge application know-how with proprietary flash-calcination IP.

Europe contributes steady but slower growth as mature flame-retardant mandates now transition into carbon-removal and ocean-alkalinization pilots along Mediterranean coasts. German Tier-1 auto suppliers specify less than 1,000 ppm chloride powder for under-hood PBT, sustaining high-purity demand. Nordic pulp mills evaluate magnesium hydroxide for biogas desulfurization, an application leveraging their existing lime loops. EU taxonomy rules prioritize circular inputs, making brine-derived magnesium particularly attractive for new subsidies.

Competitive Landscape

The magnesium hydroxide market exhibits moderate fragmentation. Vertically integrated producers such as Huber Advanced Materials, Nedmag, and Kyowa Chemical maintain mine-to-slurry chains, hedging feedstock swings. Japanese players leverage decades-old brine electrolysis units to sell pharma-grade powders with 99.5% purity into neuroscience supplements. Chinese companies focus on scale, but regulatory headwinds over energy intensity press them to upgrade kilns and seek lower-carbon serpentine routes.

Strategic moves center on specialized know-how: Calix uses flash-calcination to make reactive nano-MgO that hydrates into high-surface-area magnesium hydroxide well suited for CO₂ mineralization. Dutch producer Nedmag is piloting seawater-lime hybrid lines aiming at zero-waste discharge. Patent filings surge in electrodialysis systems that pair NaOH recovery with Mg(OH)₂ precipitation, indicating new white-space claims that could reset entry barriers. Customers favor partners offering application labs to fine-tune fire-test recipes or wastewater titration protocols, pushing suppliers to bundle chemistry with service.

Magnesium Hydroxide Industry Leaders

Huber Engineered Materials

ICL

Kyowa Chemical Industry Co., Ltd.

Martin Marietta Magnesia Specialties

Konoshima Chemical Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Huber Advanced Materials (HAM), a division of Huber Engineered Materials (HEM) and a part of the J.M. Huber Corporation portfolio, has announced a global price increase ranging from 5% to 15%, subject to product specifications and contractual terms. This adjustment, effective January 1, 2025, includes magnesium hydroxide.

- January 2024: The European Food Safety Authority (EFSA) approved magnesium l-threonate as a novel food ingredient under Regulation (EU) 2015/2283. This approval expands the use of pharmaceutical-grade magnesium compounds in the nutraceutical market, with a maximum allowable intake of 3000 mg/day, as reported in the EFSA Journal.

Global Magnesium Hydroxide Market Report Scope

Magnesium hydroxide is an alkaline compound formed by the reaction of magnesia and water in controlled conditions. This bulk chemical is widely used in chemical manufacturing for desulphurization and wastewater treatment applications. In the pharmaceutical industry, it is used as an antacid and laxative and as an intermediary for different chemical reactions. The magnesium hydroxide market is segmented into industrial, pharmaceutical, and other chemical industries on basis of application. By geography, the market is segmented into Asia-Pacific, North America, Europe, South America, the Middle East, and Africa. The report also covers the market sizes and forecasts for the Magnesium Hydroxide market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD Million).

| Slurry |

| Powder |

| Suspension/Paste |

| Industrial Grade |

| Pharmaceutical Grade |

| Food Grade |

| Chemical Precipitation |

| Seawater-Lime Process |

| Brine Electrolysis By-product |

| Other Methods |

| Industrial |

| Pharmaceuticals |

| Other Applications (Pulp and Paper, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Philippines | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa | |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Slurry | |

| Powder | ||

| Suspension/Paste | ||

| By Grade | Industrial Grade | |

| Pharmaceutical Grade | ||

| Food Grade | ||

| By Manufacturing Method | Chemical Precipitation | |

| Seawater-Lime Process | ||

| Brine Electrolysis By-product | ||

| Other Methods | ||

| By Application | Industrial | |

| Pharmaceuticals | ||

| Other Applications (Pulp and Paper, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Magnesium Hydroxide Market size?

The magnesium hydroxide market size is USD 877.65 million in 2026 and is projected to reach USD 1.23 billion by 2031.

Which region leads the global magnesium hydroxide market?

Asia-Pacific holds the top position with 46.72% share in 2025 and the fastest CAGR of 8.56% through 2031.

What drives the pharmaceutical demand surge?

EFSA’s novel-food approval, new clinical uses as phosphate binders, and expanded laxative recommendations are propelling an 8.32% CAGR for pharmaceutical-grade magnesium hydroxide.

How is desalination brine affecting supply?

Electrodialysis and mineralization technologies recover high-purity magnesium hydroxide from brine, contributing the fastest 8.94% CAGR among manufacturing methods while lowering carbon footprints.

Page last updated on: