Alcohol Ethoxylates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

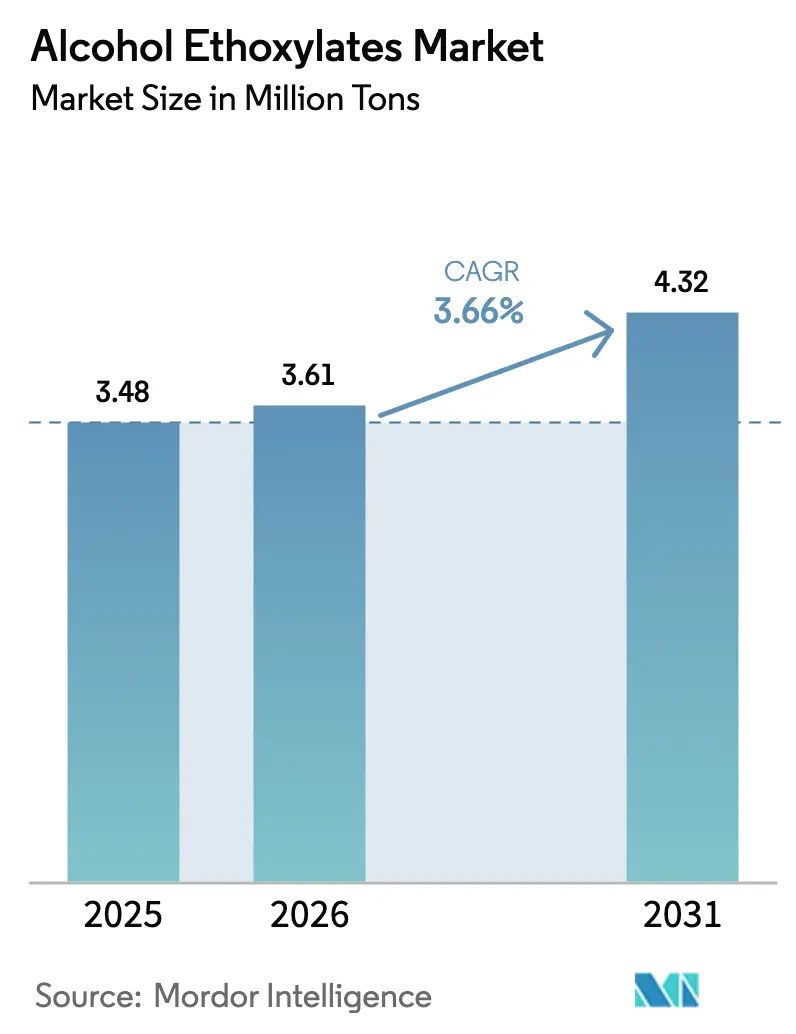

| Market Volume (2026) | 3.61 Million tons |

| Market Volume (2031) | 4.32 Million tons |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

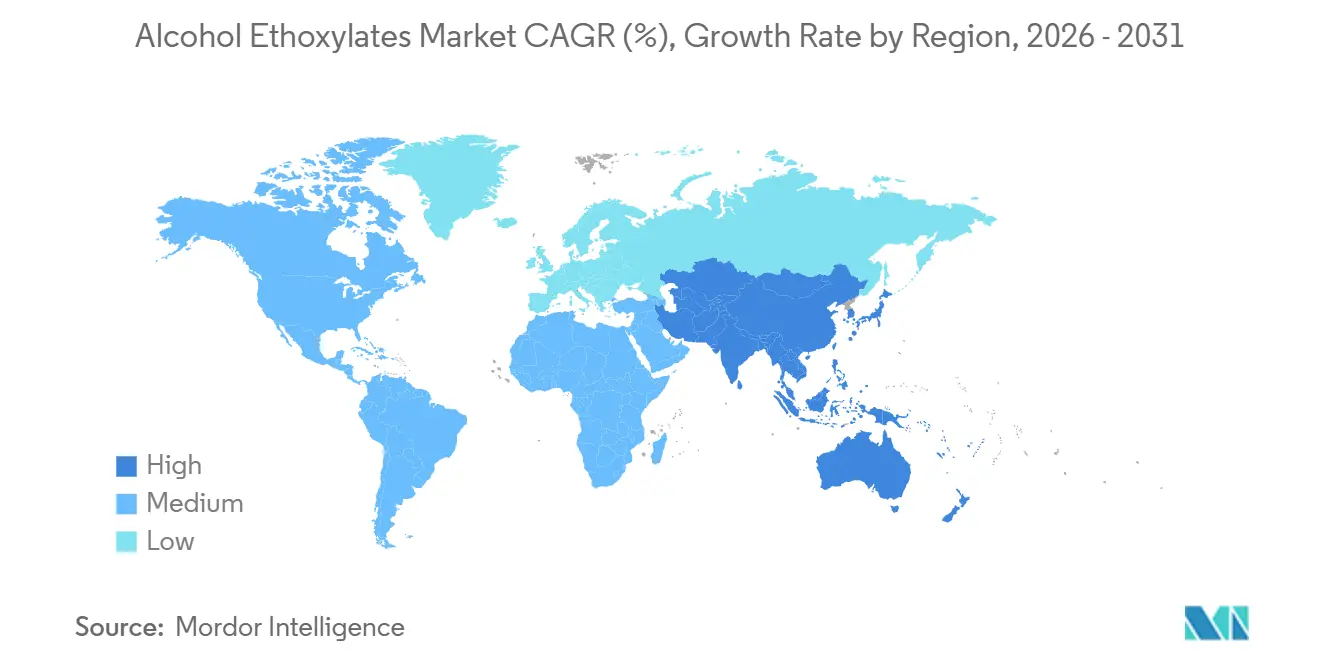

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alcohol Ethoxylates Market Analysis by Mordor Intelligence

The Alcohol Ethoxylates Market size is projected to expand from 3.48 million tons in 2025 and 3.61 million tons in 2026 to 4.32 million tons by 2031, registering a CAGR of 3.66% between 2026 to 2031. Oleochemical feedstocks, RSPO-certified supply chains, and corporate renewable-carbon pledges are accelerating the pivot away from petrochemical routes, while tightening eco-toxicity rules in North America and Europe are steering formulators toward biodegradable nonionic surfactants that align with green-label programs. Brand owners are prioritizing ultra-mild detergency in personal-care and institutional-cleaning products, which supports premium pricing for narrow-range grades even when feedstock costs spike. Rapid build-outs of integrated ethylene-oxide and alkoxylation plants in China, India, and Saudi Arabia are squeezing merchant margins, yet the regionally balanced demand profile sustains long-term volume growth opportunities for both bulk and specialty producers. Competitive strategies now revolve around backward integration into fatty-alcohol production, enzyme-catalyzed process technology, and mass-balance certification that enables incremental sustainability claims without a full oleochemical cost premium.

Key Report Takeaways

- By origin type, oleochemical grades held 58.32% of the alcohol ethoxylates market share in 2025 and are expanding at a 3.97% CAGR to 2031.

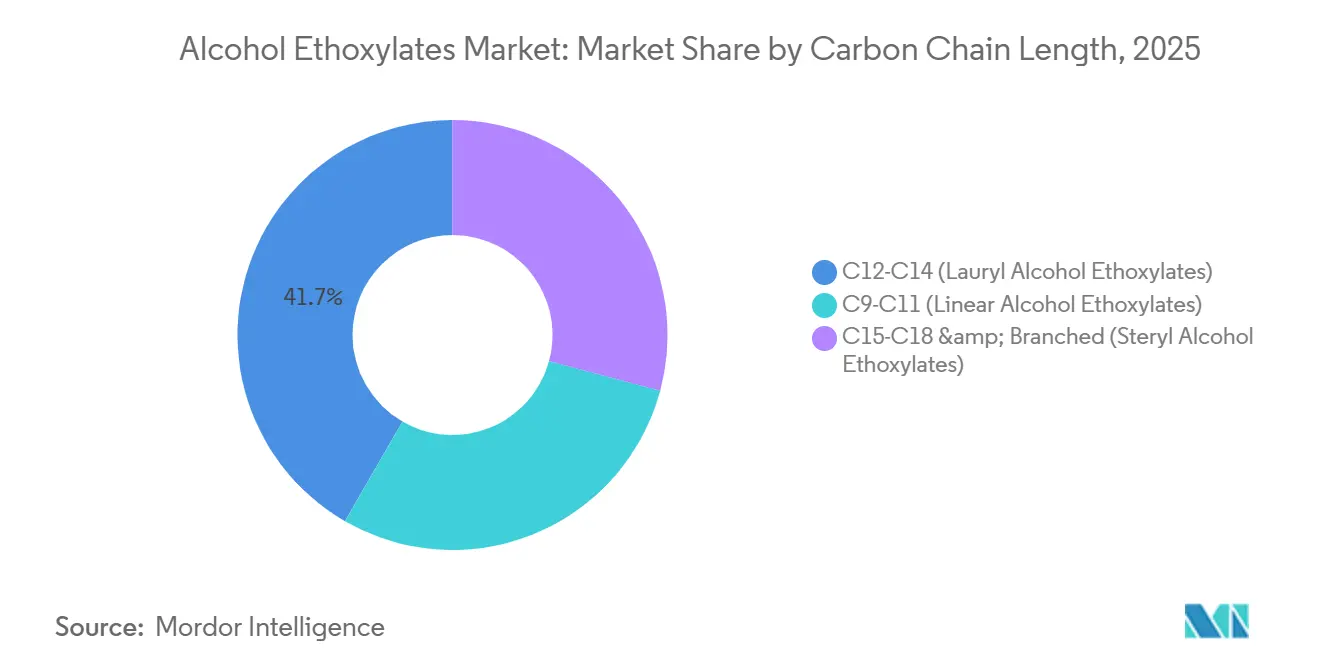

- By carbon chain length, C12-C14 grades captured 41.66% revenue share in 2025; the same segment is forecast to grow at a 4.12% CAGR through 2031.

- By form, liquid products accounted for 62.93% of the alcohol ethoxylates market size in 2025 and are advancing at a 4.35% CAGR to 2031.

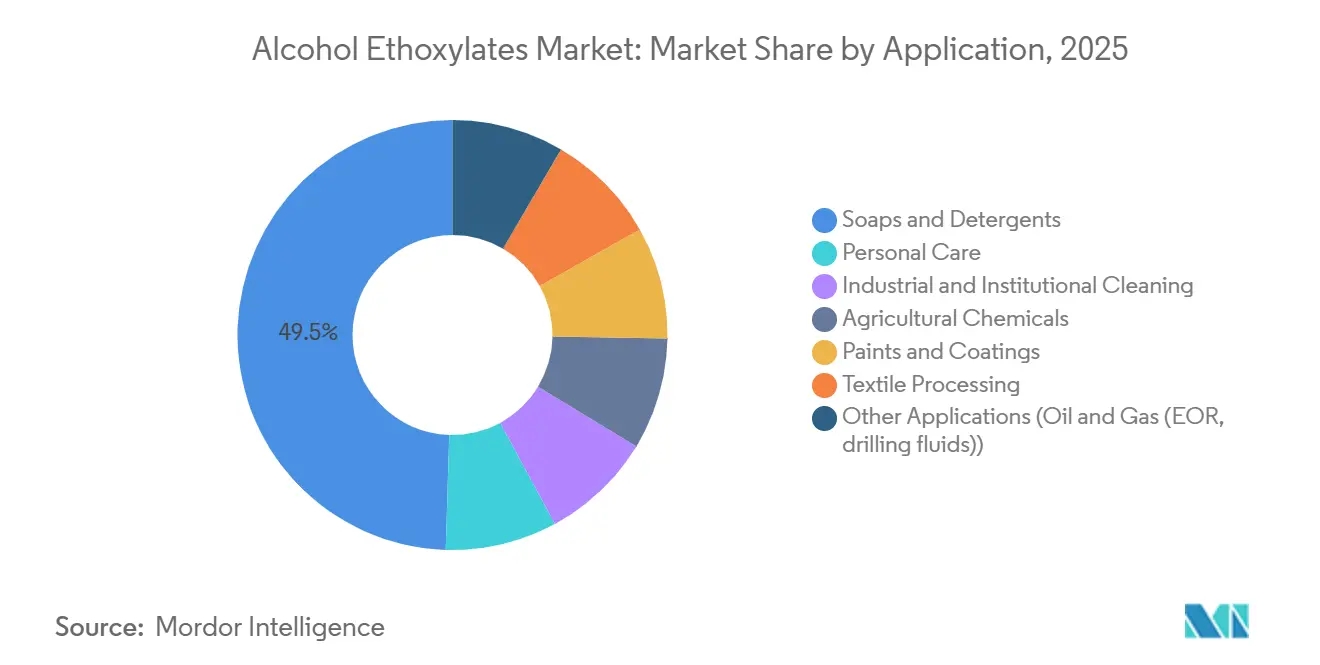

- By application, soaps and detergents led with 49.51% share of the alcohol ethoxylates market size in 2025, while personal-care recorded the highest projected CAGR at 4.42% through 2031.

- By geography, Asia-Pacific accounted for 52.34% of the alcohol ethoxylates market size in 2025 and is growing with the fastest CAGR of 4.82% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alcohol Ethoxylates Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging personal- and home-care demand across Asia-Pacific | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Expanding industrial and institutional cleaning formulations | +0.9% | North America and Europe, emerging in ASEAN | Short term (≤ 2 years) |

| Growing agrochemical use as sustainable adjuvants | +0.6% | Global, with concentration in North America, Brazil, India | Long term (≥ 4 years) |

| Rapid build-out of dedicated EO/alkoxylation capacity | +0.7% | Asia-Pacific (China, India, Thailand), Middle East | Medium term (2-4 years) |

| Shift to enzyme-catalyzed, bio-based ethoxylation processes | +0.4% | Europe and North America, pilot scale in Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Personal- and Home-Care Demand Across Asia-Pacific

Urbanization, rising disposable incomes, and government-sponsored sanitation programs in China, India, and ASEAN economies are lifting per-capita consumption of liquid detergents, fabric softeners, and rinse-off personal-care products that rely on alcohol ethoxylates for mildness, foam control, and cold-water detergency. China’s tier-2 and tier-3 cities are replacing bar soap with liquid handwash at a mid-single-digit annual pace, while India’s rural detergent penetration sits below 50%, providing a multiyear runway as e-commerce and direct-to-consumer logistics expand access. Clean-beauty brands across the region are quickly swapping sulfated anionics for C12-C14 alcohol ethoxylates that deliver comparable lather with lower skin irritation, mirroring Western reformulation patterns but accelerating through social-media influence. The preference for RSPO-certified, palm-kernel-based lauryl alcohol streamlines supply chains and shortens lead times compared with petrochemical alternatives, locking in regional feedstock advantages. As demand concentrates in liquids and single-dose pods, premium formulations maintain pricing power even when feedstock volatility compresses merchant margins.

Expanding Industrial and Institutional Cleaning Formulations

Healthcare facilities, food-service operators, and hospitality chains are tightening hygiene protocols to comply with post-pandemic standards and green-building certifications, driving adoption of low-foaming alcohol ethoxylates in automated scrubbers and central dosing systems. U.S. EPA Safer Choice and EU Ecolabel criteria reward readily biodegradable nonionics, triggering a shift from alkylphenol ethoxylates to linear grades that meet OECD 301 benchmarks. Institutional buyers value performance consistency across variable water hardness, enabling formulators to absorb feedstock swings and preserve margin, a resilience not always feasible in price-sensitive consumer detergents. Concentrated cleaning capsules typically contain 10-15% alcohol ethoxylates by weight, letting distributors reduce packaging waste in line with corporate ESG mandates. The growing network of third-party-certified suppliers consolidates procurement, further entrenching linear alcohol ethoxylates as the default workhorse surfactant in the institutional channel.

Growing Agrochemical Use as Sustainable Adjuvants

Regulators in the United States, European Union, and Brazil are tightening maximum-residue limits on crop-protection actives, spurring herbicide and insecticide formulators to incorporate alcohol ethoxylates that improve spray retention and canopy penetration, lowering active-ingredient loading without compromising efficacy[1]U.S. EPA, “Pesticide Registration Manual,” epa.gov. C9-C11 and C12-C14 grades with 8-12 ethylene-oxide units balance wetting, emulsification, and low phytotoxicity, meeting new ecotoxicity thresholds that nonylphenol ethoxylates can no longer satisfy. Brazil’s soybean and sugarcane sectors adopt domestic, oleochemical-derived adjuvants from Oxiteno to meet export sustainability criteria, while U.S. and Indian growers retrofit tank-mix regimes for lower chemical usage. Long formulation approval cycles lock in alcohol ethoxylates for 3-5 years, giving producers a stable, counter-cyclical revenue stream that offsets detergent seasonality. As climate variability heightens pest pressure, demand for high-efficacy adjuvants strengthens through 2031.

Rapid Build-Out of Dedicated EO/Alkoxylation Capacity

Integrated petrochemical and oleochemical players commissioned more than 400,000 tons of new ethoxylation capacity between 2024 and 2025, with BASF’s Zhanjiang unit, Stepan’s Pasadena expansion, Evonik’s Singapore and Shanghai projects, and Sasol’s Nanjing facility anchoring the wave[2]BASF, “Press Release—Zhanjiang Verbund Site Update 2024,” basf.com. Captive ethylene-oxide supply lowers variable cost, allowing regional champions to squeeze merchant tollers on standard grades. Spot prices for C12-C14 liquid alcohol ethoxylates dipped 4% in early 2026 as Chinese producers ramped up utilization, pressuring high-cost European plants to differentiate via enzyme-catalyzed narrow-range products. Middle-East players leverage advantaged gas-based ethylene to supply Africa and South Asia, eroding freight-cost protection historically enjoyed by Southeast-Asian exporters. Additional capacity also intensifies feedstock competition, prompting fatty-alcohol refiners to lock multi-quarter contracts with ethoxylators to secure throughput in volatile palm-oil cycles.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock (ethylene oxide and fatty alcohol) price volatility | -0.8% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Tightening eco-toxicity regulations on ethoxylates/NPEs | -0.5% | North America, Europe, and emerging in Asia-Pacific | Medium term (2-4 years) |

| Competition from bio-based alternative surfactants | -0.8% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Unplanned cracker outages drove U.S. Gulf Coast ethylene-oxide spot prices up 30% in December 2024, while Malaysian flooding and Indonesian export quotas lifted fatty-alcohol prices 25% month-on-month, creating a margin vice for ethoxylators without upstream integration. European and North American tollers face dual exposure: imported C12-C14 feedstocks from Southeast Asia and regional ethylene-oxide supply subject to energy-price shocks. Multi-quarter supply contracts hedge risk but tie up working capital, limiting flexibility for specialty-grade development. Vertically integrated players such as SABIC, Shell, and Sasol exploit their feedstock control to undercut independents and capture share, accelerating industry consolidation. Persistent volatility also nudges formulators toward alternative surfactants like alkyl polyglucosides when budget certainty outranks performance differentiation.

Tightening Eco-Toxicity Regulations on Ethoxylates/NPEs

California’s 2024 listing of nonylphenol ethoxylates as a Priority Product mandates phase-out by 2027, forcing industrial degreasers and textile auxiliaries to transition to linear alcohol ethoxylates. The U.S. EPA’s Significant New Use Rule freezes legacy NPEs out of new product development, and ECHA’s Annex XVII caps residual NPE at 0.01% in EU-market formulations. Compliance requires aquatic-toxicity and biodegradation testing that can exceed USD 500,000 and delay launches by up to 18 months, a burden smaller regional formulators struggle to absorb. Although regulations create pull-through demand for linear alcohol ethoxylates, they also open niches for biosurfactants and glucosides as formulators diversify portfolios to future-proof against further restrictions. Multinationals with turnkey regulatory dossiers seize shelf space vacated by local brands unable to navigate the compliance maze.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Origin Type: Oleochemical Dominance Reflects Sustainability Mandates

Oleochemical alcohol ethoxylates held 58.32% volume share in 2025, and their 3.97% CAGR through 2031 is set to widen the gap over petrochemical grades as brand owners pledge 100% renewable carbon by 2030. The alcohol ethoxylates market benefits from Southeast-Asian vertical integration, where palm-oil refiners downstream into fatty-alcohols and ethoxylation, capturing value while guaranteeing RSPO mass-balance certification at competitive cost structures. Petrochemical variants remain essential in the Middle East and U.S. Gulf Coast, where captive ethylene and propylene chains offset sustainability premiums, sustaining supply into commodity oilfields and industrial cleaners. Mass-balance accounting schemes from BASF and Dow offer a hybrid pathway, allocating renewable-feedstock credits across global networks, though acceptance varies by certification body. Emerging technologies that synthesize ethylene oxide from bio-ethanol or ferment sugars directly into fatty alcohols hint at a third, fully bio-based pathway that could command premium pricing in pharma excipients where traceability outweighs cost.

Oleochemical supply resilience is reinforced by Indorama Ventures’ USD 1.3 billion purchase of Oxiteno, which extended its fatty-alcohol footprint into Latin America and created a USD 3.6 billion surfactant segment potentially poised for a public listing. Wilmar, KLK OLEO, and Musim Mas invest aggressively in renewable electricity and methane-capture to lower scope-1 emissions, raising the barrier to entry for smaller tollers unable to achieve comparable ESG scores. The alcohol ethoxylates market, therefore, rewards producers that can certify chain-of-custody, optimize carbon intensity, and guarantee logistics agility during feedstock shocks.

By Carbon Chain Length: C12–C14 Balances Performance and Mildness

C12-C14 alcohol ethoxylates accounted for 41.66% of volume in 2025 and are projected to grow at a 4.12% CAGR to 2031, outperforming shorter and longer chain segments due to their hydrophilic-lipophilic balance of 12-15 that yields superior detergency and skin-mild foam. RSPO-certified lauryl alcohol represents roughly 70% of global C12-C14 fatty-alcohol supply, ensuring ample feedstock for both bulk detergents and premium personal-care applications. Narrow-range variants that concentrate the ethylene-oxide distribution around the target molar ratio command 15-20% premiums, as formulators value lower irritation indexes and improved foam aesthetics in sulfate-free shampoos. C9-C11 grades, while lower-foaming and favored in hard-surface cleaners, face odor and volatility limitations in cosmetics. C15-C18 and branched steryl chains serve high-temperature oilfield and polymerization end-uses where emulsion stability at >100 °C is critical, but the energy transition and coatings reformulations cap their expansion prospects.

Demand for C12-C14 grades also benefits from European energy-efficiency mandates that encourage cold-wash detergents, where lauryl ethoxylates maintain soil removal at 20-30 °C, enabling electrical-utility savings for consumers. In emerging Asia-Pacific, increasing liquid-detergent penetration amplifies volume, as liquids require higher active-matter loading than powders. Headwinds include competing biosurfactants and alkyl polyglucosides, but cost and performance differentials keep C12-C14 alcohol ethoxylates entrenched in mainstream formulations.

By Form: Liquid Grades Dominate on Handling and Formulation Ease

Liquid alcohol ethoxylates held 62.93% share in 2025 and are advancing at a 4.35% CAGR through 2031, reflecting formulators’ preference for ambient-temperature handling and compatibility with automated filling lines. Liquids simplify just-in-time blending, essential for personal-care contract manufacturers managing batch sizes from 500 kg to 50,000 kg in fast turnover cycles. Cold-water solubility supports growth in detergent pods and sachets popular among urban millennials in China and Indonesia, where storage space is at a premium. Paste and solid forms retain relevance in powder detergents and certain agrochemical adjuvants, where low water content minimizes hydrolysis risk and cuts freight weight by up to 30% on intercontinental routes. However, the global shift toward liquid laundry formats erodes paste demand, particularly as e-commerce platforms favor compact, spill-resistant packaging.

Industrial segments such as metal degreasing and textile scouring continue using high-active-matter pastes (90-95%) to reduce tankage footprint, yet the rise of centralized toll blending threatens this niche. Solid flakes and prills find limited use in enhanced oil recovery, dissolved onsite into high-salinity brines, but oilfield operators increasingly specify liquid concentrates to minimize dust exposure and streamline logistics. Consequently, liquid grades will solidify their majority stake in the alcohol ethoxylates market through the forecast horizon.

By Application: Personal Care Accelerates as Detergents Plateau

Soaps and detergents comprised 49.51% of volume in 2025 but are growing below the overall alcohol ethoxylates market as saturation in developed economies tempers incremental demand. In contrast, personal-care formulations expand at a 4.42% CAGR to 2031, the fastest among end-uses, as clean-beauty brands phase out sulfated anionics in favor of gentle, nonionic blends led by C12-C14 alcohol ethoxylates. Industrial and institutional cleaning maintains steady momentum, fueled by post-pandemic hygiene upgrades in healthcare and hospitality that value linear alcohol ethoxylates’ low-foaming and biodegradation credentials. Agrochemicals, paints, coatings, and textile processing are witnessing rising ethoxylate consumption, with agrochemicals the standout as tighter residue limits spur adoption of efficiency-boosting adjuvants.

Paints and coatings leverage alcohol ethoxylates for pigment wetting and foam control during high-shear dispersion, but construction cycles and silicone-based substitute additives restrict upside. Textile processing faces relocation of garment manufacturing to South Asia and Africa, regions where specialty chemical supply chains remain thin, slowing adoption of advanced surfactants. Oilfield use cases, including drilling fluids and enhanced recovery, grow modestly as operators extract additional barrels from mature reservoirs.

Geography Analysis

Asia-Pacific commanded 52.34% of global volume in 2025 and is poised to advance at a 4.82% CAGR through 2031, underscored by rising disposable incomes, urban migration, and sanitation campaigns proliferating liquid-detergent usage in China, India, and key ASEAN markets. China’s transition from bar soaps to liquid handwash continues at a mid-single-digit pace, supported by e-commerce penetration in lower-tier cities. India’s rural detergent gap offers multi-year upside as government hygiene initiatives and micro-distribution models bridge last-mile access. ASEAN hubs such as Indonesia and Vietnam attract greenfield ethoxylation investments to sidestep import tariffs and localize value chains, while mature Japan and South Korea target high-value narrow-range grades for cosmetics.

In North America and Europe, market maturity and stringent eco-toxicity rules limit incremental tonnage. Uptake of linear alcohol ethoxylates in institutional cleaning accelerates, yet biosurfactant substitution in premium personal-care products moderates overall growth. Both regions deploy bio-based ethoxylation capacity—Croda’s Snaith plant and BASF’s Ludwigshafen retrofit—to capture incentives under the EU Green Deal and U.S. BioPreferred program. Regulatory rigor fuels demand for turnkey, fully compliant surfactant systems, giving integrated majors an edge over smaller, regional suppliers.

South America and the Middle East and Africa are witnessing rising demand for alcohol ethoxylates. Brazil’s oleochemical ecosystem, centered on Oxiteno’s integrated facilities, serves domestic agrochemical and home-care sectors that value local content and RSPO-certified supply. Argentina’s macroeconomic volatility constrains surfactant imports, while the Middle East leverages low-cost ethylene to export petrochemical-derived alcohol ethoxylates into Africa, eroding freight advantages once enjoyed by Asian producers. South Africa’s detergent shift toward liquids is tempered by infrastructure gaps and price sensitivity that keep powder formats dominant across sub-Saharan markets.

Competitive Landscape

The alcohol ethoxylates market is fragmented. Integrated petrochemical producers leverage captive ethylene-oxide streams to undercut independent plants on commodity grades, forcing differentiation through RSPO-certification, ultra-narrow distributions, or custom molar ratios that command 15-20% premiums in personal-care and pharma. Strategic plays include Indorama’s USD 3.3 billion surfactant build-out via Huntsman EO (2020) and Oxiteno (2022) acquisitions, BASF’s Zhanjiang vertical integration, and Evonik’s specialty-line commissions in Shanghai and Singapore targeting Asia-Pacific growth corridors. Process innovations such as digital twin modeling and continuous-flow alkoxylation raise asset utilization and safety; SABIC’s 50% batch-size uplift and 19% energy-cut in 2024 exemplify the margin gains available to early adopters. Compliance hurdles, including ISO 14001 and RSPO audits, elevate fixed costs, prompting smaller tollers either to exit commoditized grades or partner with majors to co-develop high-value specialties.

Alcohol Ethoxylates Industry Leaders

BASF

Dow

Clariant

Sasol Ltd

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Evonik commissioned an 80,000-ton specialty-surfactants line at Shanghai Chemical Industry Park, supplying narrow-range alcohol ethoxylates and alkoxylated amines to Asia-Pacific personal-care and agrochemical customers.

- December 2024: BASF brought an integrated ethoxylation unit online at its Verbund complex in Zhanjiang, China, linking captive ethylene oxide with oleochemical fatty-alcohols to serve domestic detergent brands.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the alcohol ethoxylates market as every non-ionic surfactant created when natural or synthetic C9-C18 fatty alcohols react with ethylene oxide and then sold in liquid, paste, or solid grades to detergent, cleaning, personal-care, agrochemical, textile, oilfield, paint, and other industrial formulators. According to Mordor Intelligence, we follow producer output and recorded trade flows rather than valuing finished consumer goods.

Scope exclusion: Packaged cleaners, shampoos, and cosmetics that only contain alcohol ethoxylates lie outside our numbers.

Segmentation Overview

- By Origin Type

- Oleochemical-derived

- Petrochemical-derived

- By Carbon Chain Length

- C9-C11 (Linear Alcohol Ethoxylates)

- C12-C14 (Lauryl Alcohol Ethoxylates)

- C15-C18 and Branched (Steryl Alcohol Ethoxylates)

- By Form

- Liquid

- Paste / Solid

- By Application

- Personal Care

- Soaps and Detergents

- Industrial and Institutional Cleaning

- Agricultural Chemicals

- Paints and Coatings

- Textile Processing

- Other Applications (Oil and Gas (EOR, drilling fluids))

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Our interviews with detergent blenders, oleochemical traders, technology licensors, and plant managers across Asia-Pacific, Europe, the Americas, and the Middle East confirmed substitution trends, contract prices, and typical ethoxylation yields that screens alone miss.

Desk Research

We first mapped supply and demand through open sources such as UN Comtrade shipment codes, OECD industrial output tables, the American Cleaning Institute surfactant census, ECHA REACH tonnage bands, and US EPA TSCA volumes. Company filings and news captured via Dow Jones Factiva, plus revenue snapshots from D&B Hoovers, anchored capacity and regional price bands. Numerous additional public records rounded out the picture.

Market-Sizing & Forecasting

A top-down model aligns regional capacity and utilization with net trade to establish the baseline volume. Focused bottom-up checks sampled producer revenue divided by average selling price; these keep totals within a specified band. Multivariate regression then links demand to ethylene oxide spreads, fatty-alcohol supply, detergent and personal-care output indices, new reactor starts, and tightening wastewater norms. Scenario analysis tests feedstock shocks, while gaps for very small firms are filled with peer averages vetted during calls.

Data Validation & Update Cycle

Outputs are compared with customs flows, quarterly detergent production, and major producer disclosures. Any variance beyond two standard deviations triggers an analyst re-run; we refresh annually and issue interim updates when regulation or feedstock prices move materially.

Why Mordor's Alcohol Ethoxylates Baseline Commands Reliability

Published figures often diverge because some groups bundle downstream blends, apply a single global price, or simply roll forward old CAGRs.

Mordor's disciplined tonnage boundary, live capacity checks, and yearly refresh narrow these gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 3.53 million tons (2025) | Mordor Intelligence | - |

| USD 7.45 billion (2025) | Global Consultancy A | Revenue view, includes formulated blends, CAGR roll-forward |

| USD 7.35 billion (2025) | Trade Publisher B | Single world ASP, omits small Asian suppliers, two-year refresh |

These contrasts show why our balanced, transparent baseline is the dependable starting point for decision makers.

Key Questions Answered in the Report

Which segment is growing fastest in alcohol ethoxylates personal-care applications?

Personal-care formulations are forecast to expand at a 4.42% CAGR through 2031 as clean-beauty brands replace sulfated anionics with milder C12-C14 alcohol ethoxylates.

How large is the alcohol ethoxylates market by 2031?

The market is expected to reach 4.32 million tons by 2031, growing at a 3.66% CAGR.

What share do liquid alcohol ethoxylates hold today?

What share did liquid alcohol ethoxylates hold in 2025?

Which region dominates demand growth?

Asia-Pacific drives more than half of global volume and is projected to grow at a 4.82% CAGR through 2031 on the back of urbanization and rising incomes.

Page last updated on: