Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

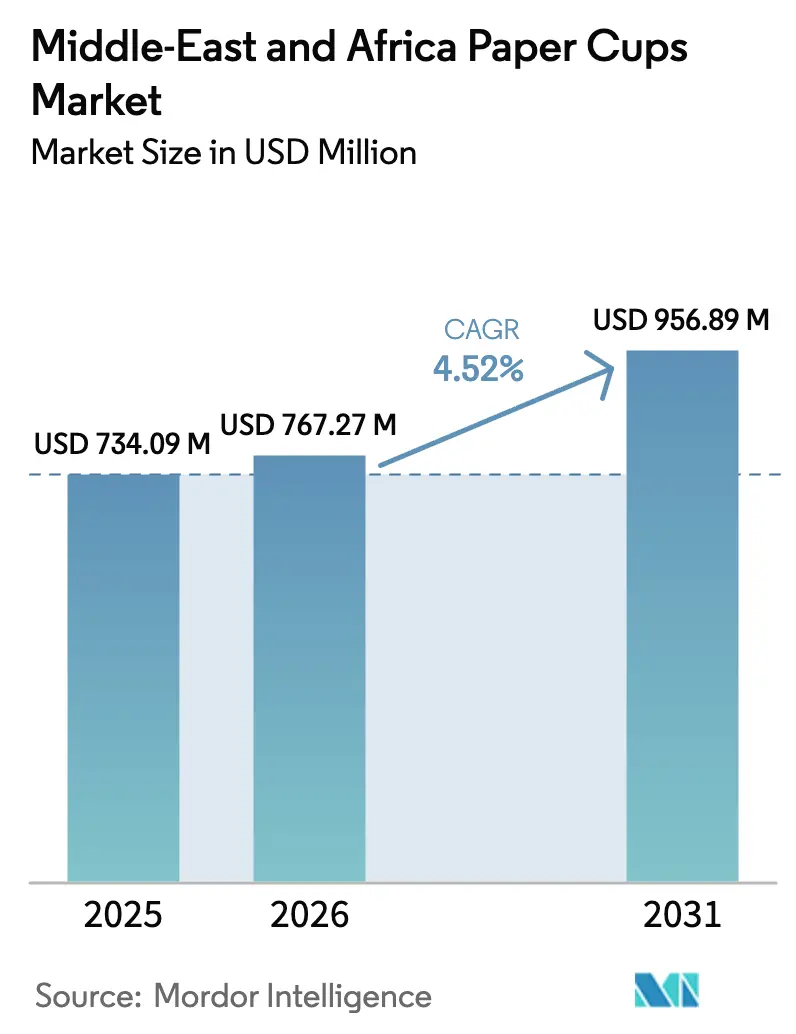

| Base Year Market Size (2025) | USD 734.09 Million |

| Market Size (2026) | USD 767.27 Million |

| Market Size (2031) | USD 956.89 Million |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

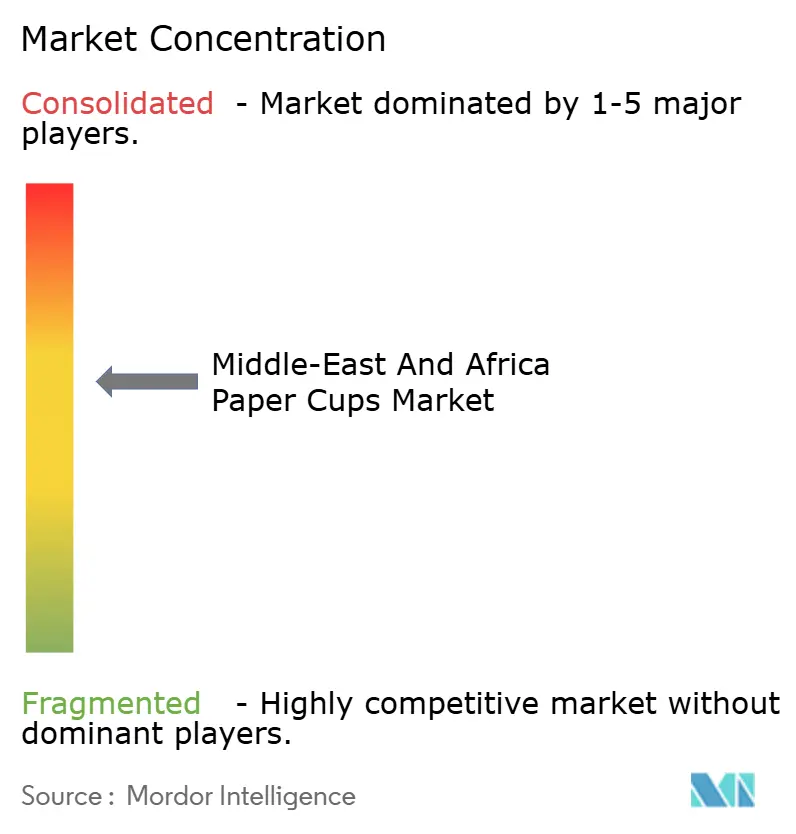

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Paper Cups Market Analysis by Mordor Intelligence

The Middle East and Africa paper cup market size was valued at USD 734.09 million in 2025 and is estimated to grow from USD 767.27 million in 2026 to USD 956.89 million by 2031, at a CAGR of 4.52% during the forecast period (2026-2031). Demand is underpinned by plastic-reduction mandates that took effect across the Gulf Cooperation Council and Southern African Development Community in January 2026, prompting quick-service restaurants and coffee chains to accelerate the phase-out of polystyrene foam and PE-lined cups. Parallel to regulation, specialty coffee culture is deepening its regional foothold, lifting per-capita hot-drink consumption and driving format innovation such as double-wall insulation and short-run digital printing. A contrasting headwind comes from chronic pulp-price volatility tied to currency swings in Egypt, Nigeria, and Kenya, which is squeezing converters’ margins and slowing mill expansions outside the Gulf. As a result, the Middle-East and Africa paper cups market displays a bifurcated growth map where well-capitalized Saudi and Emirati manufacturers scale aggressively while Sub-Saharan operators struggle to secure affordable feedstock.

Key Report Takeaways

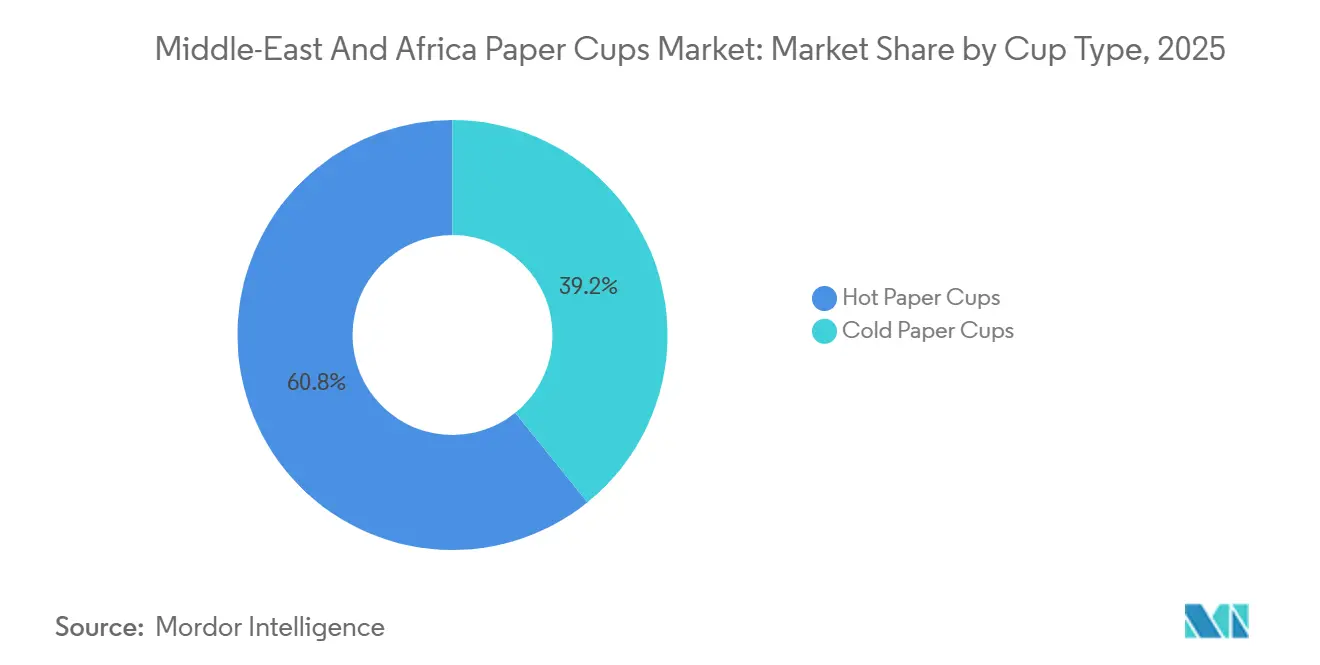

- By cup type, hot formats led with a 60.81% revenue share in 2025, while cold formats are projected to grow at a 4.93% CAGR through 2031.

- By material lining, polyethylene-coated products captured 53.12% of value in 2025; water-based barrier cups are forecast to grow the fastest at 5.08% CAGR through 2031.

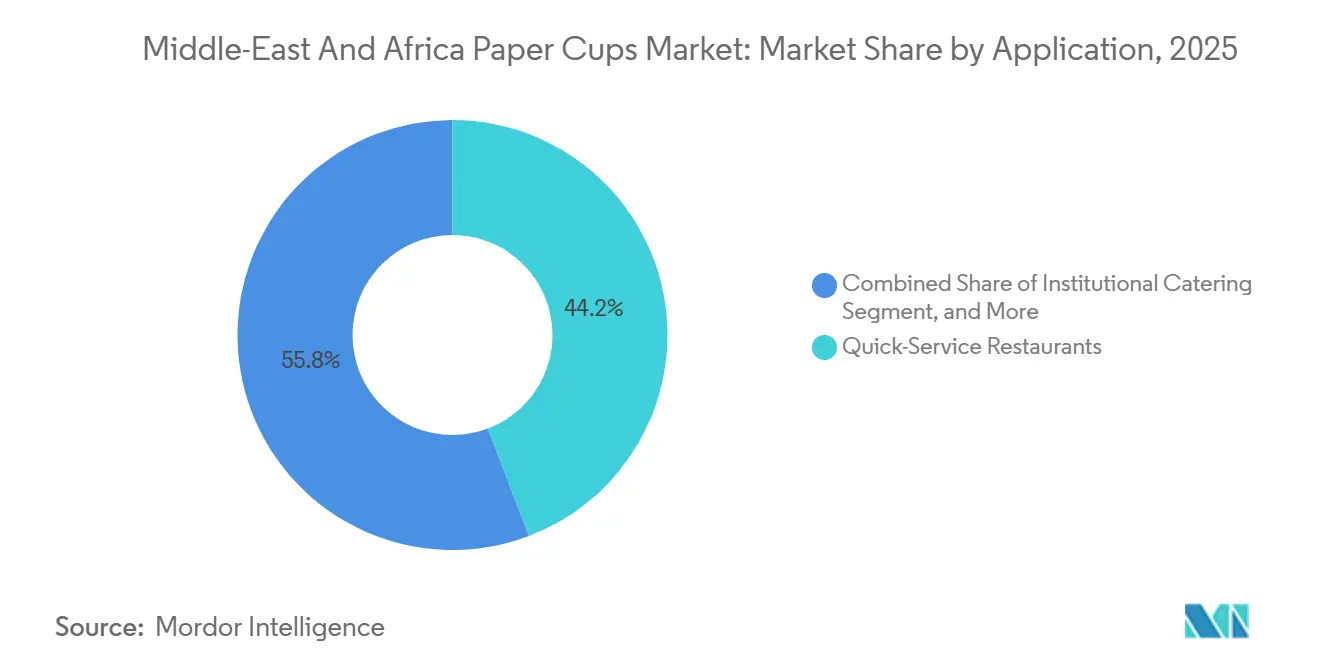

- By application, quick-service restaurants accounted for 44.21% of demand in 2025, yet retail and convenience stores are expected to post the highest growth at a 5.37% CAGR through 2031.

- By capacity, 8-12-ounce cups accounted for 44.12% of the market in 2025; formats above 16 ounces are on track for the fastest expansion, with a 5.31% CAGR through 2031.

- By country, Saudi Arabia dominated with a 24.73% share in 2025, whereas Kenya is projected to be the fastest-growing country at a 6.08% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East And Africa Paper Cups Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging on-the-go hot-drink culture | +1.2% | GCC core, Egypt, Kenya | Medium term (2-4 years) |

| Government single-use plastic bans | +1.5% | GCC, SADC, Kenya, Nigeria | Short term (≤2 years) |

| Food-delivery platform expansion | +0.8% | Major urban centers in UAE, Saudi Arabia, Egypt, South Africa, Nigeria | Medium term (2-4 years) |

| Tourism rebound powering HORECA outlets | +0.6% | UAE, Saudi Arabia, Egypt, South Africa, Kenya | Short term (≤2 years) |

| Data-centric plant efficiency programs | +0.3% | Saudi Arabia, UAE, Egypt, South Africa | Long term (≥4 years) |

| Rise of plastic-free water-based barrier cups | +0.4% | GCC, South Africa, Kenya, Egypt | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging On-The-Go Hot-Drink Culture

Specialty coffee chains, independent roasters, and grab-and-go kiosks continue to multiply in Gulf and North African cities, bringing daily hot-drink transactions into the millions. Long average commute times in Dubai, Riyadh, and Cairo create captive demand for portable beverages, and operators increasingly specify double-wall or ripple-wrap insulated cups that remove the need for separate sleeves, trimming unit costs and improving consumer comfort. Regional suppliers that invest in digital printers capable of seasonal artwork changes earn brand premiums because quick-service chains value short turnaround times for limited-edition campaigns. Independent café owners also seek smaller minimum order quantities, and converters able to amortize set-up costs over diversified runs capture this micro-segment. As consumer palates widen toward flavored lattes and specialty teas, 8-12 ounce formats remain the volume leader, but upsizing during summer months nudges average cup capacities upward.

Government Single-Use Plastic Bans

The regulatory environment has become the strongest near-term catalyst. The United Arab Emirates banned single-use plastic cups effective January 2026, exempting only compostable alternatives that comply with ASTM D6868 and bear certification logos.[1]UAE Ministry of Climate Change and Environment, “Ministerial Decision 380/2022 on Single-Use Plastics,” moccae.gov.ae Kenya’s Legal Notice 181/2024 imposes a 30% recycled-content mandate on all disposable packaging and requires Extended Producer Responsibility labels, raising the compliance bar for both importers and local merchants. Saudi Arabia, Bahrain, and Oman implemented similar prohibitions on EPS foam, while South Africa applies a plastic-bag levy model that policymakers intend to extend to polystyrene cups in 2027. Although enforcement outside capital cities is inconsistent, the bans give organized foodservice operators a clear signal to shift, effectively locking in baseline demand for certified paper alternatives.

Food-Delivery Platform Expansion

Digital aggregators such as Talabat, Deliveroo, and Uber Eats are reshaping consumption habits by normalizing single-use packaging across income tiers. More than half of Middle East and North Africa consumers placed at least one takeaway order every week in 2025, a pattern that raised the region’s online food-delivery market past USD 9 billion and keeps it on a 20%-plus growth path.[2]Middle East Paper Company, “Annual Report 2024,” mep.co Aggregators negotiate bulk contracts for co-branded cups, effectively turning lids into mobile advertisements and giving converters a channel insulated from traditional distributor mark-ups. Because delivery riders store beverages in insulated bags for extended periods, metallized or aqueous-coated cold cups with higher stiffness gain preference, pushing converters to diversify their barrier technologies. The fragmentation of order sizes, however, challenges inventory planning and elevates working-capital needs, especially for smaller Kenyan and Nigerian plants that already face currency exposure.

Tourism Rebound Powering HORECA Outlets

International arrivals surged in 2025 as flight frequencies normalized and mega-projects such as Saudi Arabia’s Red Sea and NEOM attracted leisure travelers. South Africa logged 881,393 visitors in July 2025, a 26% year-on-year increase, while Middle Eastern travelers to the country rose by 57.4%. Hotels, restaurants, and cafés serving these tourists demand branded disposable cups that meet ISO 22000 and BRCGS hygiene standards, steering procurement toward larger converters with certified lines. In Egypt, Nile cruise operators standardized cup volumes and lid designs for onboard cafés, giving local converters predictable order flows. New room inventories planned for 2026-2028 translate into multi-year supply contracts, encouraging converters to invest in flexographic presses capable of high-definition logos and rapid color changes. The tourism uptick, therefore, reinforces premium-cup adoption and helps offset pulp cost inflation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented converter base squeezing margins | -0.7% | Nigeria, Kenya, Tanzania, Uganda, Egypt | Medium term (2-4 years) |

| Chronic pulp price volatility | -1.1% | Egypt, Nigeria, Kenya, South Africa | Short term (≤2 years) |

| Under-developed cup-recycling streams | -0.4% | Sub-Saharan and North Africa | Long term (≥4 years) |

| Electrical-energy shortages | -0.5% | Nigeria, Kenya, Tanzania, Ghana, Zimbabwe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Converter Base Squeezing Margins

Dozens of small-scale plants across Sub-Saharan Africa operate far below optimal throughput, limiting their bargaining power on cupstock and inks. Median EBITDA margins in the global paper-based packaging sector reached 15.4% in 2024, yet many Nigerian and Kenyan converters averaged single-digit returns because under-utilized machinery inflates unit costs. Hotpack Global’s AED 100 million acquisition of Al Huraiz Packaging illustrates how scale advantages enable backward integration into board production and forward expansion into regional distribution. Smaller firms in Kenya, unable to finance Extended Producer Responsibility infrastructure, lose access to formal retail or quick-service chains, effectively capping their growth and creating a two-tier market. Margin compression discourages capital upgrades, slowing the adoption of water-based coating lines and digital printers, which are crucial for compliance and customization.

Chronic Pulp Price Volatility Tied to Currency Swings

Roughly 90% of virgin and de-inked pulp used in Middle Eastern and Africa paper cups is imported and denominated in U.S. dollars. Egypt’s pound depreciated 40% between January 2024 and December 2025, while Nigeria’s naira fell by 30% in the same period, forcing converters either to raise prices or absorb losses.[3] Middle East Paper Company cushions volatility through its WASCO recycling arm, which supplied more than 90% of its fiber needs in 2024 at a controlled cost of SAR 600 per tonne (USD 160 per tonne).[4]Huhtamaki Oyj, “Q1 2025 Interim Report,” huhtamaki.com Most regional converters lack such vertical hedges, and every 10% uptick in Scandinavian pulp list prices can wipe out quarterly profits when local currencies weaken. Delays in letters of credit and higher working-capital requirements for imported raw materials further strain liquidity, keeping capacity additions on hold in Nigeria and Egypt and slowing the overall pace of technology renewal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cup Type: Hot Formats Retain Scale as Cold Cups Accelerate

Hot paper cups accounted for 60.81% of the Middle-East and Africa paper cups market share in 2025, buoyed by entrenched coffee and tea consumption rituals across Saudi Arabia, Egypt, and Kenya. Cold paper cups, although smaller in absolute volume, are forecast to grow at a 4.93% CAGR to 2031, outstripping hot formats as delivery aggregators prioritize chilled drinks, and retailers expand ready-to-drink aisles. The Middle East and Africa paper cups market size gains incremental volume each summer when Gulf temperatures top 45 °C, prompting cafés to upsell iced beverages in moisture-resistant cups. Graphic Packaging’s Cold&Go solution claims 40% lower condensation versus plastic cups, resolving leakage complaints from delivery riders. Converters in South Africa and Dubai are piloting aqueous-coated variants for both hot and cold lines, thereby simplifying inventory for multi-temperature beverage chains.

The stabilizing yet still-growing hot segment serves as a cash generator, as production lines for single-wall and double-wall cups are fully amortized. However, as growth tilts toward cold formats, market leaders allocate new capital mainly to barrier-technology upgrades, including water-based or PLA coatings that perform across temperature ranges. Smaller Sub-Saharan operators risk being locked out of the cold-cup upswing unless they secure financing for higher-spec machines.

By Material Lining: Polyethylene Dominant, Water-Based Barriers Gain Momentum

Polyethylene-coated cups retained 53.12% of value in 2025, reflecting legacy equipment and lower per-unit costs, yet converters see strategic upside in water-based barriers that grew 5.08% in the same year. The UAE’s plastic ban exempts polylactic-acid variants provided they meet certification thresholds, creating a premium segment that Gulf chains pursue for sustainability branding. Huhtamaki’s ProDairy recyclable cup limits PE content to below 5%, allowing straightforward fiber recovery in mills without special pulpers. Experimental coatings made from cellulose nanofibers or chitosan exhibit moisture vapor transmission rates comparable to those of PE while allowing full compostability, as documented in recent peer-reviewed studies. Capital expenditure in aqueous-coating lines is accelerating in Kenya and South Africa, where EPR rules tie license renewals to demonstrable recyclability.

The material shift alters supply-chain economics, pushing board mills to fine-tune surface roughness and fiber orientation suitable for bio-polymer adhesion. Because water-based coatings often require tighter process windows, converters invest in inline quality sensors and closed-loop viscosity controls, an area where Saudi and Emirati plants hold an early lead.

By Application: Quick-Service Chains Lead, Retail Channels Surge

Quick-service restaurants captured 44.21% of value in 2025, their dominance underlined by multi-year framework agreements that global franchisors sign with ISO-certified converters. The retail and convenience-store channel, however, is projected to expand at 5.37% CAGR through 2031, propelled by the proliferation of grab-and-go coolers in fuel stations and supermarkets across Nigeria, Saudi Arabia, and South Africa. Chain operators favor full-graphic customization on cup bodies and lids, creating an advertising medium that justifies higher unit prices. Institutional catering, although still niche, is growing steadily in the Gulf as ministries and corporate campuses outsource foodservice under green-procurement mandates that stipulate compostable or fully recyclable cups.

For independent grocery and kiosk owners, the biggest hurdle to sourcing paper over plastic is the upfront cost. Kenyan micro-converters bridge this gap with unbranded PE-lined stock-keeping units, but once EPR audits tighten, these merchants will have to transition to labeled, traceable cups. Thus, the application mix is shifting toward retail, yet chain managers’ specification clout means converters cannot ignore quick-service volume even as margins compress.

By Capacity: Mid-Range Cups Dominate, Jumbo Formats Capture Youth Demand

The 8-12-ounce band accounted for 44.12% of sales in 2025, aligning neatly with cappuccino and latte portions favored in specialty cafés. Cups above 16 ounces, led by smoothie and bubble tea offerings, are poised for the fastest 5.31% CAGR through 2031 as younger consumers gravitate toward social-media-friendly large drinks. The Middle East and Africa paper cup market is at the larger end, benefiting from higher prices per blank and thicker board specs, partially offsetting pulp inflation for converters. Up to 7-ounce cups hold a stable demand in traditional Arabic coffee rituals but offer limited growth potential.

Production planning grows complex because franchise partners require color-coded differentiation across four capacity tiers. Digital printers that reduce plate-change downtime let converters accept smaller, diversified runs without inflating overhead. Nigerian street vendors selling fruit juices in oversized paper cups illustrate an emerging preference for portability, coupled with sustainability messaging, lifting jumbo-cup volumes despite power-supply disruptions that periodically constrain output.

Geography Analysis

Saudi Arabia contributed 24.73% of the Middle-East and Africa paper cups market in 2025, leveraging Vision 2030 investments that include USD 1.78 billion in new containerboard capacity from Middle East Paper Company. The PM5 machine, due online in Q4 2027, will add 450,000 tonnes annually, doubling company output and providing cupstock for converters across the Gulf. Hotpack Global’s SAR 1 billion (USD 266 million) sustainable-packaging complex in Riyadh further cements local supply, while the kingdom’s population consumes 36 million coffee cups each day, ensuring baseline volumes.

The United Arab Emirates follows closely, fueled by a tourism rebound and its role as the regional headquarters for numerous international quick-service chains. Hotpack’s AED 250 million (USD 68 million) PET and paper hub in Dubai’s National Industries Park integrates e-commerce logistics with production, shrinking delivery lead times to Gulf outlets. Demand surges during global events, such as Dubai Expo spin-off conferences, which place bulk orders for branded hot and cold cups on compressed timelines. Currency stability tied to the U.S. dollar peg shields Emirati converters from pulp-price swings, letting them quote longer-term contracts.

Kenya is the fastest-growing national market, set to advance at 6.08% CAGR through 2031. Legal Notice 181/2024 widens Extended Producer Responsibility mandates, obliging every disposable package to include at least 30% recycled content and a QR-code license. The Nairobi packaging expo drew more than 150 exhibitors from 35 countries in May 2025, showcasing aqueous-coated cup lines tailored for East African climatic conditions. Converters are racing to build local de-inking and fiber-recovery units so they can certify loops and keep licensing fees low.

South Africa anchors Sub-Saharan demand thanks to a sophisticated retail base and Mpact’s integrated fiber-collection network. Detpak’s BRC-certified Johannesburg plant enjoys ready access to post-consumer recovered board, allowing it to position water-based barrier cups for premium coffee chains. International visitor arrivals rose sharply in 2025, and local safari lodges increasingly specify compostable cups to meet eco-tourism marketing claims.

Nigeria offers latent upside with its 230 million population but faces persistent electricity outages that idle lines for up to 40% of scheduled hours. Even so, the packaging sector exceeded USD 2 billion in 2024 and could surpass USD 3.5 billion by 2032, suggesting cup demand will rebound once power-infrastructure projects mature. Ghana, Tanzania, and Ethiopia are smaller today, yet their blanket bans on polystyrene foam position them as future adoption frontiers once local cupstock supply stabilizes.

Turkey’s role is primarily manufacturing for export. Eroglu Global Holding is investing USD 175 million in Egypt’s Suez Canal Economic Zone to build a packaging complex that will ship half of its output back to Turkey and the Levant, adding a new trans-Mediterranean supply node.

Competitive Landscape

Market structure is moderately fragmented. Four multinational converters, Huhtamaki, Graphic Packaging, Hotpack Global, and Detpak, hold commanding positions in organized quick-service and coffee-chain channels, while dozens of regional firms sell unbranded PE-lined cups to informal vendors. Hotpack demonstrates the consolidation playbook: the AED 100 million acquisition of Al Huraiz Packaging doubled corrugated capacity and introduced micro-flute technology suitable for cup carriers, while a subsequent GBP 50 million United Kingdom investment extended the firm’s European footprint.

Graphic Packaging differentiates through technology, securing a 93 recyclability score under CEPI and 4evergreen protocols for its OmniKote-E barrier and reporting 9% year-on-year sales growth for PLA-coated cups in 2024. Its pilot aqueous-line in Jeddah partners with local mills to validate fiber yield, giving the brand a first-mover reputation among sustainability-focused foodservice operators. Huhtamaki, after consolidating three UAE sites into a single Jebel Ali complex, expanded its Ras Al Khaimah plant and is building extra fiber-packaging capacity in Egypt, signaling commitment despite a Q1 2025 sales dip attributed to conflict-related boycotts.

Local challengers exploit market niches. Kenyan converters offer short-run digital prints for pop-up cafés, while Nigerian entrepreneurs assemble manual cup-forming kits to serve street vendors. Access to finance remains their Achilles heel; without capital to secure EPR licenses or upgrade to aqueous coatings, many become acquisition targets once volumes hit strategic thresholds. Meanwhile, Gulf manufacturers deploy Industry 4.0 analytics to boost uptime and reduce trim waste, widening the productivity gap with Sub-Saharan peers.

Middle-East And Africa Paper Cups Industry Leaders

Hotpack Packaging Industries LLC

Huhtamaki Oyj

Graphic Packaging International LLC

Detpak South Africa (Pty) Ltd

Gulf East Paper & Plastic Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Middle East Paper Company’s Juthor unit broke ground on a SAR 345 million (USD 92 million) tissue line in King Abdullah Economic City, doubling tissue capacity and integrating Andritz digital solutions.

- May 2025: Nairobi hosted its tenth packaging, plastics, print, and processing expo, attracting 150 plus exhibitors and spotlighting eco-packaging adoption across East Africa.

- April 2025: Middle East Paper Company approved a USD 475 million containerboard line (PM5) slated for Q4 2027 start-up, appointing Voith as executing contractor.

- November 2024: Hotpack Global unveiled a GBP 50 million (USD 63 million) investment plan for a United Kingdom facility to widen export reach.

Middle-East And Africa Paper Cups Market Report Scope

The Middle-East and Africa Paper Cups Market Report is Segmented by Cup Type (Hot Paper Cups, Cold Paper Cups), Material Lining (Polyethylene Coated, Polylactic-Acid/Compostable, Water-Based Barrier/Plastic-Free), Application (Quick-Service Restaurants, Institutional Catering, Coffee Chains and Cafes, Retail and Convenience Stores), Capacity (Up to 7 oz, 8-12 oz, 13-16 oz, Above 16 oz), and Geography (Saudi Arabia, United Arab Emirates, Egypt, South Africa, Nigeria, Turkey, Kenya, Rest of Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Cup Type

| Hot Paper Cups |

| Cold Paper Cups |

By Material Lining

| Polyethylene (PE) Coated |

| Polylactic-Acid (PLA) / Compostable |

| Water-Based Barrier / Plastic-Free |

By Application

| Quick-Service Restaurants (QSR) |

| Institutional Catering |

| Coffee Chains and Cafes |

| Retail and Convenience Stores |

By Capacity (oz)

| Up to 7 oz |

| 8-12 oz |

| 13-16 oz |

| Above 16 oz |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Egypt |

| South Africa |

| Nigeria |

| Turkey |

| Kenya |

| Rest of Middle East and Africa |

| By Cup Type | Hot Paper Cups |

| Cold Paper Cups | |

| By Material Lining | Polyethylene (PE) Coated |

| Polylactic-Acid (PLA) / Compostable | |

| Water-Based Barrier / Plastic-Free | |

| By Application | Quick-Service Restaurants (QSR) |

| Institutional Catering | |

| Coffee Chains and Cafes | |

| Retail and Convenience Stores | |

| By Capacity (oz) | Up to 7 oz |

| 8-12 oz | |

| 13-16 oz | |

| Above 16 oz | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Turkey | |

| Kenya | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How large is the Middle-East and Africa paper cups market today?

It reached USD 0.767 billion in 2026 and is forecast to climb to USD 0.957 billion by 2031.

What is the expected growth rate for paper cups demand in Kenya?

Kenya is projected to register a 6.08% CAGR between 2026 and 2031, the fastest in the region.

Which cup type is gaining the most momentum?

Cold paper cups are on track for a 4.93% CAGR through 2031, outpacing the larger hot-cup segment.

Why are water-based barrier cups important?

They allow recyclability and compostability without sacrificing moisture resistance, helping converters meet new Extended Producer Responsibility rules.

How are currency swings affecting converters?

Depreciating local currencies raise imported pulp costs, compressing margins for mills in Egypt, Nigeria, and Kenya.

Who are the key players shaping regional supply?

Huhtamaki, Graphic Packaging, Hotpack Global, and Detpak dominate organized channels, while many smaller converters serve informal markets.

Page last updated on: