Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

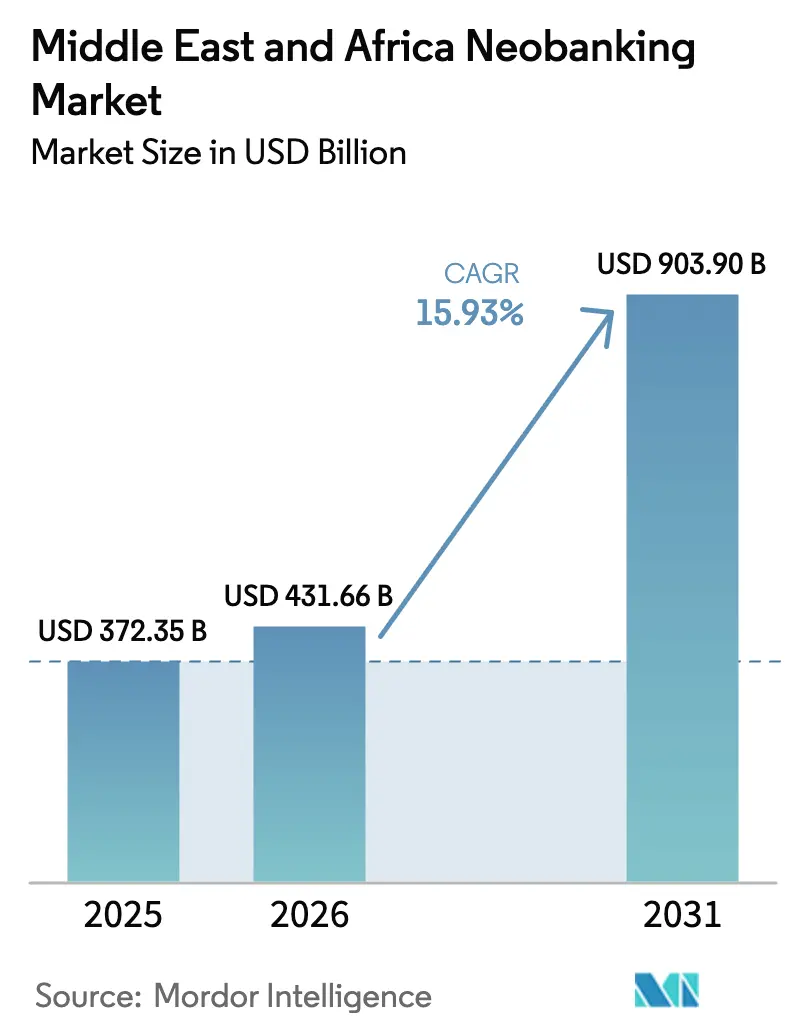

| Base Year Market Size (2025) | USD 372.35 Billion |

| Market Size (2026) | USD 431.66 Billion |

| Market Size (2031) | USD 903.9 Billion |

| Growth Rate (2026 - 2031) | 15.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Neobanking Market Analysis by Mordor Intelligence

Middle East & Africa neobanking market size in 2026 is estimated at USD 431.66 billion, growing from 2025 value of USD 372.35 billion with 2031 projections showing USD 903.9 billion, growing at 15.93% CAGR over 2026-2031. Rapid smartphone adoption, supportive open-banking regulations, and persistent financial-inclusion gaps underpin the region’s digital banking momentum[1]European Investment Bank, “Finance in Africa – Unlocking investment in an era of digital transformation and climate transition,” eib.org. . Leading telecom operators are converting mobile-money wallets into full-service banks, while incumbent institutions accelerate cloud migrations to defend their share. Cross-border remittance corridors between the Gulf Cooperation Council and sub-Saharan Africa are creating lucrative fee pools for low-cost digital channels, and Sharia-compliant product design is widening addressable demand among Muslim-majority populations. Despite these tailwinds, capital adequacy rules and cybersecurity mandates heighten compliance costs for independent entrants.

Key Report Takeaways

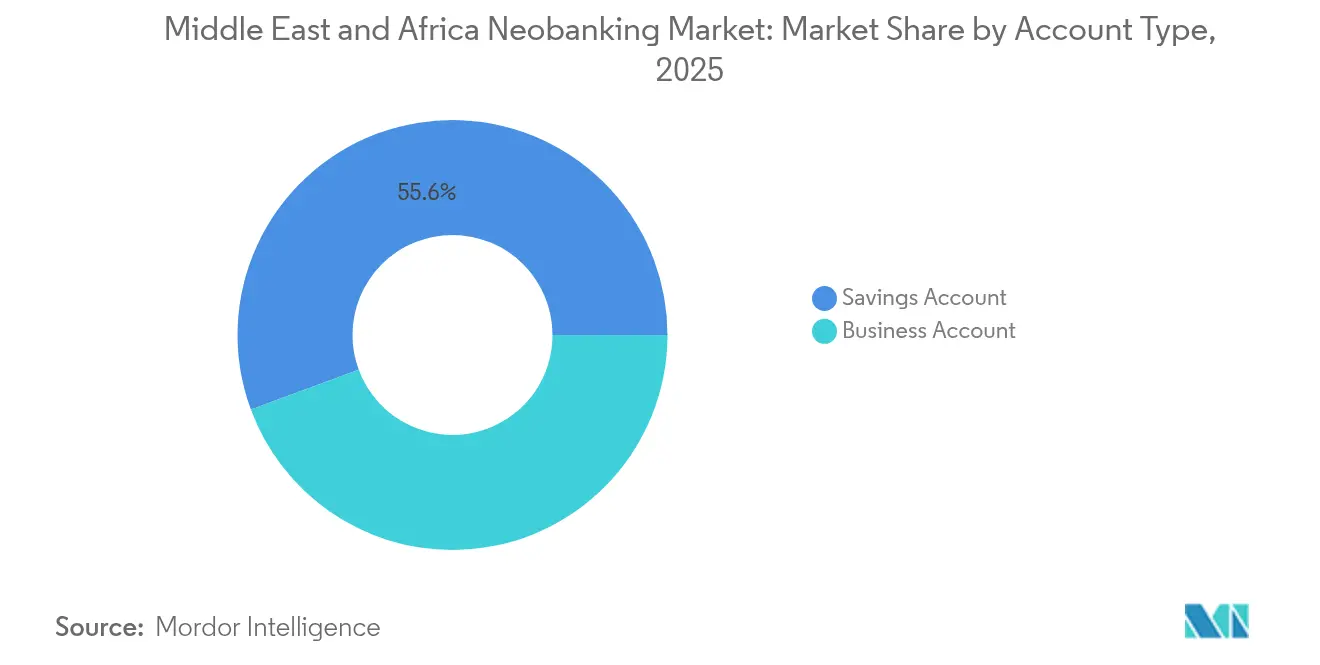

- By account type, savings accounts led with 55.64% of the Middle East & Africa neobanking market share in 2025, whereas business accounts are projected to expand at a 20.62% CAGR through 2031.

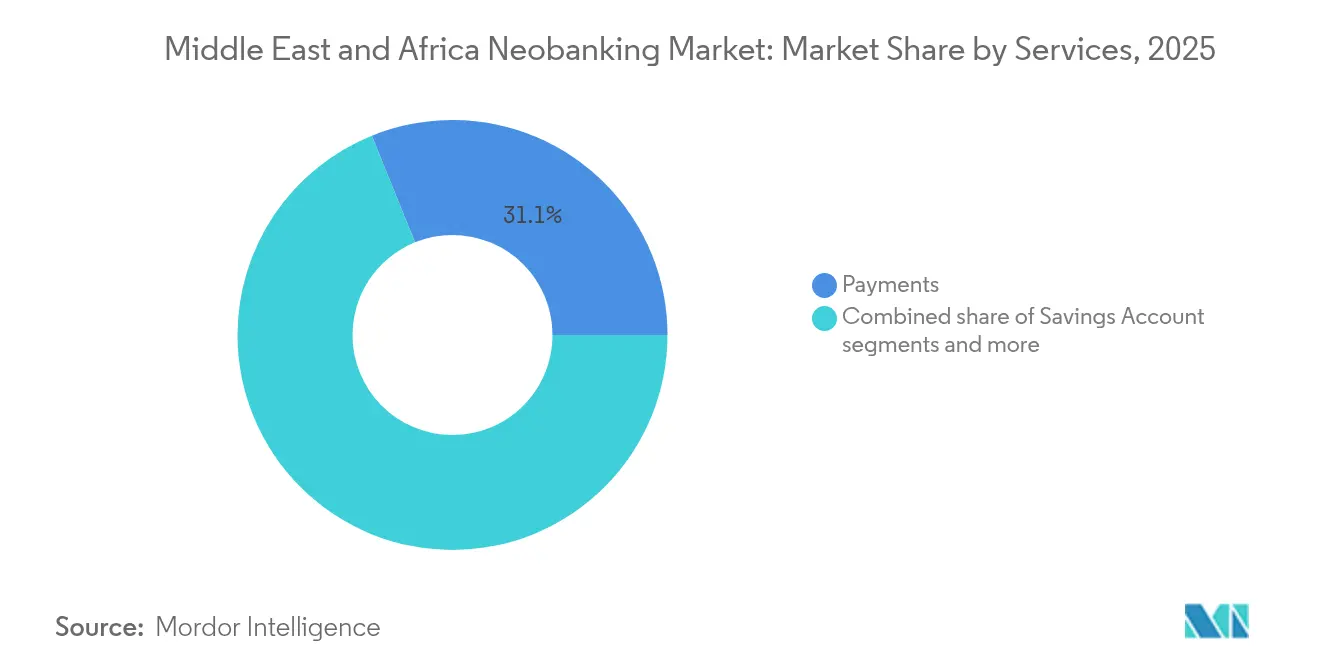

- By services, payments contributed 31.12% of the Middle East & Africa neobanking market size in 2025; loans recorded the quickest trajectory at a 23.51% CAGR to 2031.

- By application, personal usage commanded a 66.55% share of the Middle East & Africa neobanking market size in 2025, while enterprise adoption is growing at a 18.74% CAGR between 2026 and 2031.

- By geography, Saudi Arabia accounted for 34.84% of regional value in 2025; Nigeria is forecast to lead growth at 22.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Neobanking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone penetration leapfrogging traditional banking infra | +6.0% | Global, with highest impact in sub-Saharan Africa | Medium term (2-4 years) |

| Unbanked and under-banked population demand digital-first accounts | +7.0% | Nigeria, Kenya, Ghana, with spillover to MENA | Long term (≥ 4 years) |

| Regulatory sandboxes & open banking frameworks in GCC | +4.0% | Saudi Arabia, UAE, Bahrain | Short term (≤ 2 years) |

| Sharia-compliant Islamic fintech propositions | +3.0% | GCC core, expanding to North Africa | Medium term (2-4 years) |

| Cross-border remittance corridors require low-cost digital channels | +5.0% | GCC-Africa corridors, diaspora markets | Medium term (2-4 years) |

| Telecom-led super-app ecosystems bundling financial services | +5.0% | Saudi Arabia, South Africa, Nigeria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smartphone penetration leapfrogs branch networks

Mobile connections far outnumber bank accounts across much of sub-Saharan Africa, enabling digital challengers to bypass costly physical infrastructure. The European Investment Bank reported that mobile-money usage captured 74% of global transaction volumes in 2023, up from 59% in 2021, with Africa accounting for the majority. Orange MEA and Mastercard will furnish 37 million wallet holders with virtual debit cards by 2025, validating scale economics[2]Fintech Finance News, “Orange Middle East and Africa and Mastercard Partner to Digitize Payments for Millions Across Africa by 2025,” ffnews.com.. Device affordability improvements, lower data tariffs, and super-app ecosystems bundled by telcos reinforce usage frequency. As regulators digitize identity verification, onboarding friction continues to decline. Collectively, these trends raise daily active users and transaction velocities, directly lifting fee revenue for neobanks.

Demand from unbanked and under-banked segments

Financial-exclusion levels above 50% persist in multiple African states. Kenya reduced exclusion from 25% in 2013 to 11.6% in 2021 through tiered-KYC mobile wallets, signalling untapped demand curves. Nigeria’s central bank licensed 153 digital credit providers by September 2025, collectively disbursing KSh 76.8 billion (USD 594 million) via mobile channels. Tiered deposits, nano-loans, and embedded insurance expand lifetime revenue per customer while broadening inclusion mandates. Development-finance institutions channel concessional capital toward platforms that target women and youth segments, further intensifying momentum. Consequently, addressable volumes for savings and micro-credit products are set to grow faster than GDP.

GCC regulatory sandboxes and open-banking rules

Gulf Cooperation Council economies have implemented comprehensive regulatory innovation frameworks that systematically reduce barriers to neobank market entry and interoperability. Saudi Arabia's Central Bank (SAMA) approved Google Pay integration in 2024 while advancing Payment Initiation Services regulation, complementing the UAE's Central Bank open finance regulation that enables third-party access to customer financial data with explicit consent. Bahrain's regulatory sandbox has attracted international players including Fidor Bank's Middle East operations, while Qatar National Bank became the first GCC institution to launch unified digital wallet acceptance via Mastercard Gateway's Hosted Checkout in August 2025. These frameworks comply with ISO/IEC 27001:2022 and SOC 2 Type 2 standards, ensuring cybersecurity requirements align with international best practices.

Sharia-compliant digital finance propositions

Islamic banking principles create differentiated product opportunities for neobanks serving Muslim-majority populations across MENA and parts of sub-Saharan Africa. Gulf International Bank's meem platform operates as the region's first Sharia-compliant neobank, while digital Islamic banking propositions increasingly integrate profit-sharing arrangements and asset-backed financing structures that traditional banks find operationally complex to deliver at scale. The regulatory influence of Sharia supervisory boards extends to digital banking product design, requiring neobanks to demonstrate compliance with Islamic finance principles through transparent fee structures and permissible investment vehicles that avoid interest-based transactions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent capitalization & cybersecurity licence requirements | -6.0% | Global, particularly affecting standalone neobanks | Short term (≤ 2 years) |

| Consumer trust deficit in branch-less entities | -5.0% | Rural and conservative markets across MEA | Long term (≥ 4 years) |

| Interoperability gaps with legacy payment rails | -4.0% | Nigeria, Kenya, fragmented payment systems | Medium term (2-4 years) |

| Political instability & FX volatility deterring investors | -6.0% | Sub-Saharan Africa, select MENA markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent capitalization & cybersecurity rules

Regulatory authorities across the region have implemented increasingly demanding capital adequacy and cybersecurity compliance standards that disproportionately impact standalone neobank entrants compared to incumbent-backed digital platforms. Nigeria's banking recapitalization requirements, effective March 2024, mandate minimum paid-up capital ranging from NGN 10 billion to NGN 500 billion depending on license type, while Kenya's Business Laws Amendment Act 2024 raised minimum core capital for banks from KES 1 million to KES 10 million (approximately USD 6,800 to USD 68,000) with compliance required by December 2029. The Cybercrimes Amendment Act 2024 mandates reporting cyber incidents to National CERT within 72 hours, aligning with data protection breach reporting requirements that create substantial compliance overhead for digital-only institutions lacking established risk management frameworks.

Consumer Trust Deficit in Branch-less Entities

Cultural preferences for physical banking relationships and scepticism toward app-only financial services continue to limit neobank adoption rates, particularly in rural markets and among older demographic segments. The European Investment Bank's 2024 survey of 51 sub-Saharan African banks identified consumer trust and digital literacy gaps as primary constraints to digital banking expansion, with traditional banks citing competition from telcos and fintechs as a key strategic challenge. South Africa's Reserve Bank Digital Payments Roadmap, published in April 2024, specifically addresses trust-building through enhanced consumer protection measures and financial literacy programs designed to support digital payment adoption across underserved communities[3]South African Reserve Bank, “The SARB releases Roadmap towards inclusive digital payments,” resbank.co.za..

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Account Type: Business accounts catalyse SME digitization

Business accounts are growing at a 20.62% CAGR, positioning them as the prime growth lever of the Middle East & Africa neobanking market. Demand stems from micro-, small-, and mid-sized enterprises seeking consolidated cash-management, payroll, and FX modules without legacy-bank paperwork. Nigeria’s Payment System Vision 2025 explicitly champions API-driven account aggregation for merchants, encouraging fintech-bank collaborations. Concurrently, Kenyan regulators lifted a decade-long bank-licensing moratorium in July 2025, unlocking charter pathways for vertical-specialist SME banks.

Market maturity in savings accounts persists because low-fee, mobile-first vaults attract first-time depositors. The segment’s 55.64% share signals entrenched usage for store-of-value needs, supported by seamless cash-in rails at agent outlets and interoperable QR networks across GCC jurisdictions. Competitive intensity is rising, driving commoditization; hence, providers bundle budgeting analytics and yield-boosting goal posts to retain balances. For business accounts, transaction-linked credit-scoring unlocks working-capital lines, embedding sticky revenue streams and reducing churn probability relative to consumer cohorts.

By Services: Payments dominate; loans accelerate

Payments service command 31.12% market share in 2025, reflecting their foundational role in digital banking ecosystems and the natural progression from mobile money platforms to comprehensive financial services. The segment benefits from established regulatory frameworks and consumer familiarity, with Orange Middle East and Africa's partnership with Mastercard enabling 37 million wallet holders across seven countries to access global merchant networks through virtual and physical debit cards. Mobile banking and money transfer services capture significant transaction volumes but face margin pressure from increasing competition and regulatory fee caps.

Loans emerge as the fastest-growing service category at 23.51% CAGR through 2031, driven by sophisticated credit scoring algorithms that leverage alternative data sources including mobile money transaction histories, utility payment patterns, and social network analysis. Kenya's Central Bank licensed 27 additional digital credit providers in September 2025, bringing the total to 153 approved operators who have disbursed USD 522.45 million (KSh 76.8 billion) through mobile apps and USSD channels. The regulatory framework increasingly emphasizes consumer protection through interest rate transparency and debt collection standards, with Kenya's proposed Non-Deposit Taking Credit Providers regime introducing tiered licensing based on paid-up capital thresholds that will consolidate the digital lending sector while improving borrower safeguards.

By Application: Enterprise uptake narrows consumer lead

Personal applications dominate with 66.55% market share in 2025, reflecting the consumer-centric origins of most neobanking platforms and the large addressable market of unbanked and underbanked individuals across the region. Consumer-focused neobanks benefit from simplified onboarding processes, intuitive mobile interfaces, and product features designed around everyday financial needs, including bill payments, peer-to-peer transfers, and basic savings functionality. The segment's maturity creates competitive pressure on customer acquisition costs and necessitates differentiation through specialized services such as Sharia-compliant products or diaspora remittance solutions.

Enterprise applications demonstrate superior growth potential at 18.74% CAGR through 2031, as businesses increasingly demand integrated financial services that combine traditional banking with supply chain finance, trade documentation, and cross-border payment capabilities. MaxAB-Wasoko's acquisition of Fatura, approved by EFG Finance in May 2025, illustrates how B2B e-commerce platforms are integrating embedded fintech services to capture merchant credit demand, with the combined entity's fintech business now financing over 9% of e-commerce sales across Egypt and expanding to Morocco. Regulatory frameworks established by competition authorities increasingly support embedded finance models that enable non-bank platforms to offer banking services through licensed partnerships while maintaining consumer protection standards.

Geography Analysis

Saudi Arabia maintains the largest geographic market share at 34.84% in 2025, leveraging comprehensive regulatory frameworks, high smartphone penetration, and government initiatives supporting Vision 2030's digital transformation objectives. The kingdom's success reflects coordinated policy implementation including SAMA's approval of Google Pay integration, advancement of Payment Initiation Services regulation, and the successful transformation of STC Pay into a full-service digital bank in January 2025. The UAE contributes significant market value through Emirates NBD's Liv platform and the Central Bank's open finance regulation enabling third-party access to customer financial data, while Mastercard and Zand's cross-border payments solution launch demonstrates the market's sophistication in supporting international transaction flows.

Nigeria emerges as the fastest-growing geography at 22.61% CAGR through 2031, driven by the Central Bank's comprehensive regulatory modernization including Payment System Vision 2025, revised IMTO guidelines enabling formal remittance channels, and new account types for diaspora banking services effective January 2025. South Africa demonstrates steady growth supported by the Reserve Bank's Digital Payments Roadmap published April 2024 and Tyme Bank’s achievement of unicorn status with USD 250 million Series C funding, while smaller markets including Ghana benefit from new digital banking platform launches such as the Codebase Technologies-MojoPay partnership announced September 2025. The regulatory influence of regional economic communities increasingly supports cross-border interoperability, with the Africa Digital Financial Inclusion Facility dedicating 14% of resources to policy harmonization across member states.

Competitive Landscape

The Middle East and Africa Neobanking market remains moderately concentrated, with the top five players holding a significant but not dominant share. This creates ample room for new entrants and opportunities for regional expansion, especially in underserved and underbanked areas. Digital platforms backed by traditional banks are showing strong scalability, leveraging existing infrastructure and customer trust. For instance, Emirates NBD’s Liv has grown rapidly toward a million users, while STC Bank has evolved from a payment app into a full-service neobank with a multi-million user base. These examples highlight how legacy institutional support and digital innovation together can accelerate user acquisition and market growth.

The intensity of competition varies widely across regions, driven by local consumer behaviour and infrastructure maturity. In the GCC, bank-sponsored digital brands tend to outperform, benefiting from trust and established customer bases. In contrast, sub-Saharan African markets have seen more success from independent neobanks leveraging mobile money systems and agent networks. These standalone players are often better suited to local needs, especially in areas with limited access to traditional banking. As a result, geographic and operational adaptability has become a key competitive factor.

Strategic consolidation is picking up pace, signalling a maturing digital banking ecosystem across the region. A prime example is FairMoney’s planned USD 20 million acquisition of Umba, marking a significant cross-border deal aimed at expanding Nigerian operations into Kenya. Technology partnerships are also becoming critical to market leadership. Standard Bank’s collaboration with Volante Technologies and M2P Fintech’s USD 100 million funding round are both aimed at scaling advanced digital financial services. Meanwhile, new disruptors are targeting niches like cross-border remittances, SME finance, and embedded finance, while established players build super-app ecosystems that combine banking with telecom, retail, and lifestyle services.

Middle East And Africa Neobanking Industry Leaders

Liv. (Emirates NBD)

STC Pay

TymeBank

Mashreq Neo

Bank Zero

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Mastercard and Zand launched a cross-border payments solution in the UAE, utilizing Mastercard Move's payments suite to enable deposit and cash pickup services, representing a significant advancement in GCC-Africa remittance corridor digitization and financial inclusion initiatives.

- January 2025: STC Bank officially launched full banking services in Saudi Arabia, transitioning from STC Pay's digital wallet platform to serve over 12 million customers with comprehensive neobanking capabilities, including savings accounts, loans, and investment products, marking the largest telecom-to-bank transformation in MENA history.

- October 2024: Standard Bank and Volante Technologies announced a continent-wide Payments-as-a-Service partnership described as Volante's most ambitious engagement to date, targeting comprehensive payments infrastructure modernization across African markets with implications for cross-border transaction processing and digital banking interoperability.

- September 2024: M2P Fintech secured USD 100 million Series D funding led by Helios Investment Partners to expand Banking-as-a-Service capabilities across Africa, valuing the India-based platform at over USD 785 million and positioning it to compete with established core banking vendors in emerging markets.

Middle East And Africa Neobanking Market Report Scope

Neobanks is a bank that operates online without having a physical presence, it is part of fintech that provides digital and mobile-first services like payments, debit cards, money transfers, lending, and more. Middle East and Africa Neobanking Market is segmented By Account type (Business Account and Savings Account), By Service (Mobile Banking, Payments & money transfer, Savings account, Loans, and Others), By Application (Enterprise, Personal, and Others), and By Country (Saudi Arabia, United Arab Emirates, South Africa, Bahrain, Oman, Qatar, and Others)

By Account Type

| Business Account |

| Savings Account |

By Services

| Mobile-Banking |

| Payments |

| Money-Transfers |

| Savings Account |

| Loans |

| Others |

By Application

| Personal |

| Enterprise |

| Other Application |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Rest of Middle East & Africa |

| By Account Type | Business Account |

| Savings Account | |

| By Services | Mobile-Banking |

| Payments | |

| Money-Transfers | |

| Savings Account | |

| Loans | |

| Others | |

| By Application | Personal |

| Enterprise | |

| Other Application | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

Key Questions Answered in the Report

What is the forecast value of the Middle East & Africa neobanking space by 2031?

The market is projected to reach USD 903.9 billion by 2031, expanding at a 15.93% CAGR.

Which country currently contributes the largest revenue?

Saudi Arabia leads with 34.84% of 2025 regional revenue owing to initiative-taking open-banking regulations and strong telecom-bank conversion.

Which service line is growing fastest among regional neobanks?

Digital lending posts the highest CAGR at 23.51% as AI-driven credit scoring scales nano-loan volumes.

How concentrated is provider competition?

The top five players hold 48.90% share, indicating a moderately concentrated but still competitive arena.

What regulatory change most benefits new entrants in East Africa?

Kenya’s July 2025 decision to lift its decade-long bank-license moratorium opens fresh charter opportunities under clearer capital rules.

Why are business accounts gaining traction?

SMEs seek integrated cash-management and cross-border payment tools, propelling business-account revenue at a 20.62% CAGR.

Page last updated on: