Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

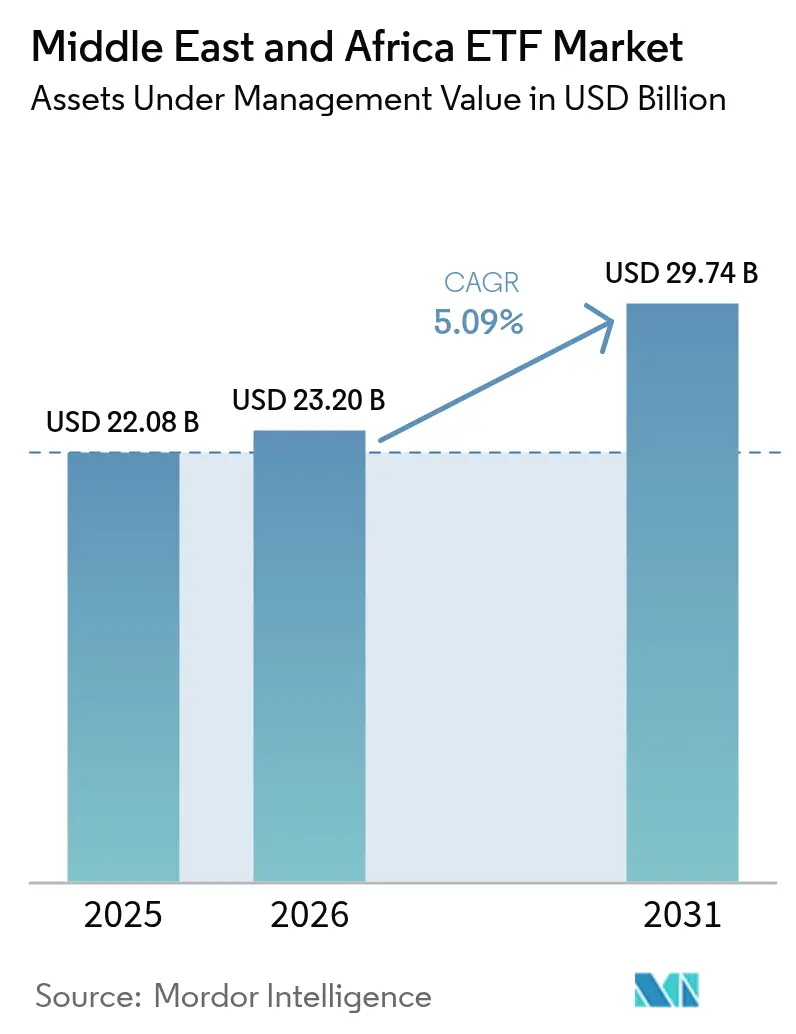

| Base Year Market Size (2025) | USD 22.08 Billion |

| Market Size (2026) | USD 23.2 Billion |

| Market Size (2031) | USD 29.74 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa ETF Market Analysis by Mordor Intelligence

Middle East and Africa ETF market size in 2026 is estimated at USD 23.2 billion, growing from 2025 value of USD 22.08 billion with 2031 projections showing USD 29.74 billion, growing at 5.09% CAGR over 2026-2031. The region’s rapid capital-market reforms, rising digital-platform penetration, and growing demand for Sharia-compliant fixed-income products are reinforcing momentum. Sovereign-wealth-fund allocations, exemplified by the Saudi Public Investment Fund’s USD 200 million anchor commitment to a Saudi bond ETF, highlight the institutional pull that continues to deepen liquidity and product breadth. Digital-first retail adoption, regulatory fee waivers on exchange trading, and post-trade infrastructure upgrades are collectively lowering transaction frictions and improving price discovery. At the same time, the gradual rotation from commodity-heavy portfolios toward global equity exposure is broadening the investor base and attracting international issuers keen to capture first-mover advantages in the Middle East and Africa ETF market.

Key Report Takeaways

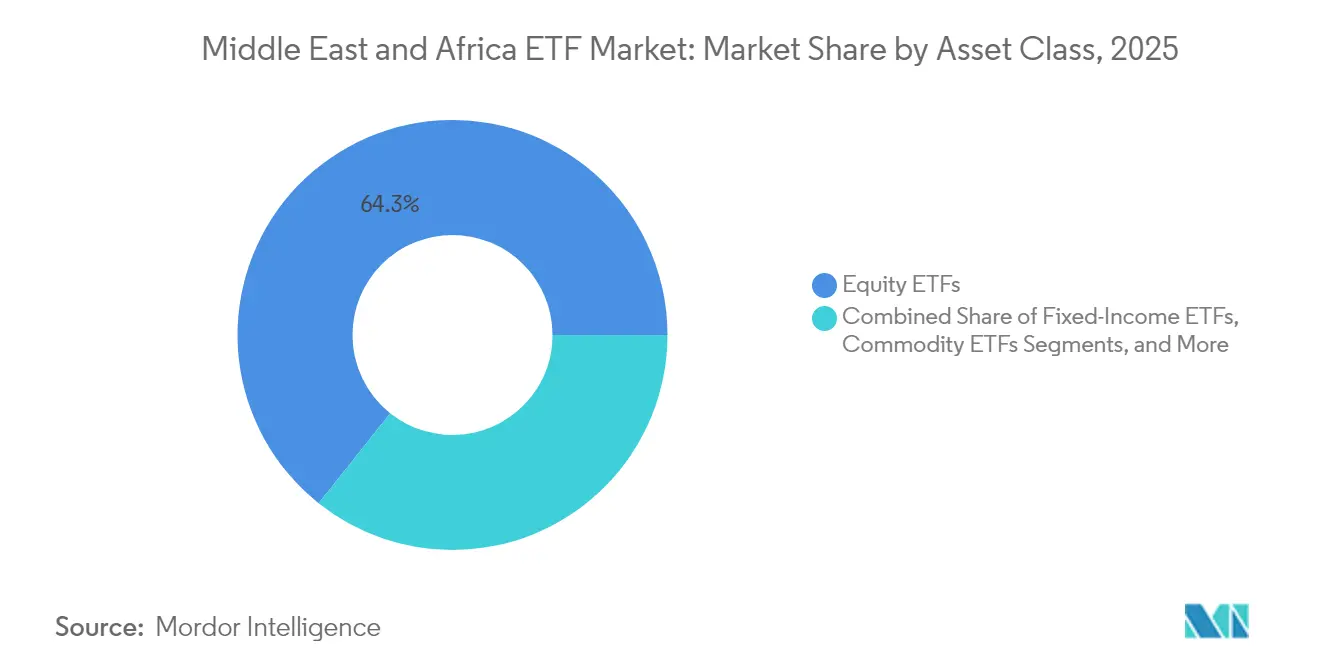

- By asset class, equity ETFs led with 64.30% of Middle East and Africa ETF market share in 2025, while fixed-income ETFs are projected to compound at a 6.52% CAGR through 2031.

- By investment strategy, passive products dominated with 76.10% of the Middle East and Africa ETF market share in 2025; active ETFs are expected to post the fastest growth at 7.02% CAGR to 2031.

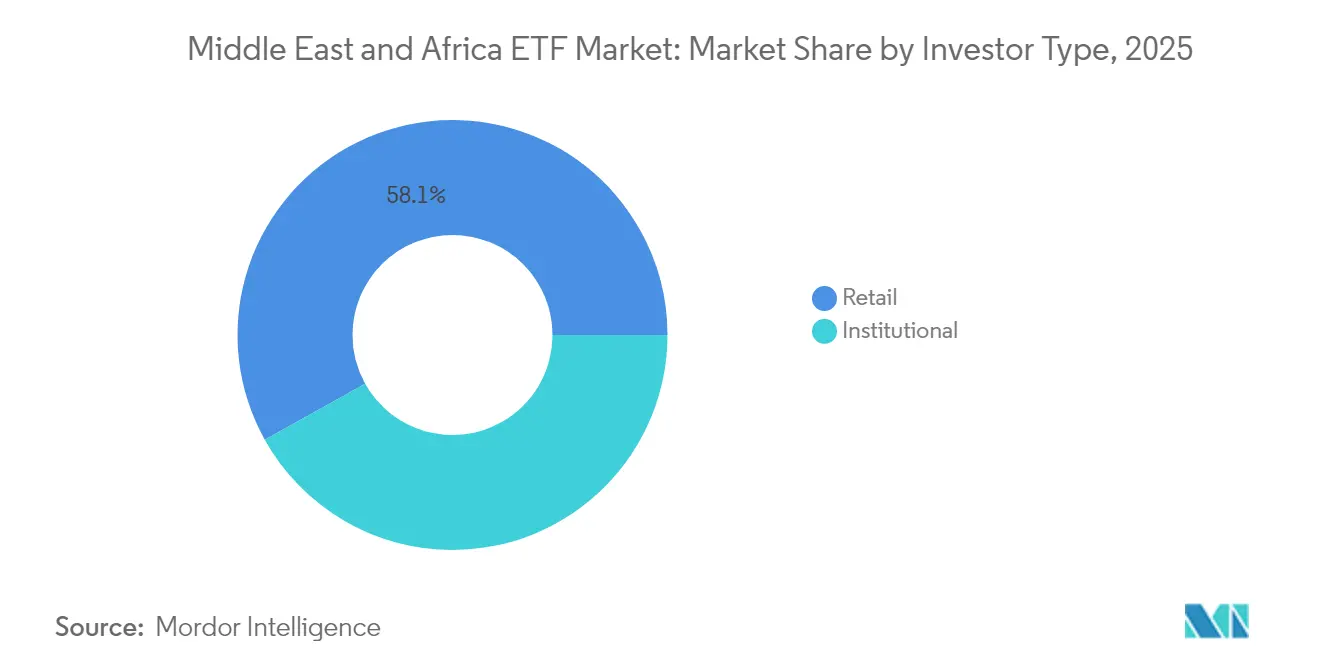

- By investor type, retail investors accounted for 58.10% of the Middle East and Africa ETF market share in 2025; institutional flows are slated to rise at a 5.92% CAGR through 2031.

- By distribution channel, direct and digital retail platforms captured 35.60% share of the Middle East and Africa ETF market size in 2025 and are expanding at 7.48% CAGR to 2031.

- By geography, Saudi Arabia held 21.45% of the Middle East and Africa ETF market in 2025, whereas the United Arab Emirates is forecasted to grow the fastest at a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa ETF Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GCC Capital-Market Reforms & Index Upgrades | +1.2% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Qatar & Saudi Fee Waivers Boosting On-Exchange ETF Liquidity | +0.9% | Qatar, Saudi Arabia | Short term (≤ 2 years) |

| Commodity-to-Equity Portfolio Diversification | +0.8% | GCC countries, South Africa | Long term (≥ 4 years) |

| Rise of Sharia-Compliant Sukuk ETFs | +0.7% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| CBDC and Digital-Asset Frameworks | +0.5% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Pension-Fund Auto-Enrolment in Nigeria & Kenya | +0.5% | Nigeria, Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GCC Capital-Market Reforms & Index Upgrades (MSCI/FTSE)

Foreign equity inflows doubled to USD 60 billion by end-2024 after Saudi Arabia’s MSCI Emerging Markets weight rose to 4.4%. Post-trade system upgrades on the Saudi Exchange improved creation and redemption cycles, narrowing ETF tracking error and attracting global issuers eager to scale in the Middle East and Africa ETF market[1]Saudi Exchange, “Post-Trade Transformation Program Completion,” saudiexchange.sa.

Qatar & Saudi Fee Waivers Boosting On-Exchange ETF Liquidity

Trading-fee eliminations compressed bid-ask spreads, lifting lendable inventory in Saudi Arabia by 190% year-on-year in early 2025[2]State Street Global Advisors, “Global ETF Flows Report 2025,” ssga.com. Heightened turnover has spurred market-maker participation, accelerating volume growth in fixed-income funds across the Middle East and Africa ETF market.

Rise of Sharia-Compliant Sukuk ETFs

Sovereign-wealth-fund demand for sukuk exposure underpins the 6.7% CAGR outlook for fixed-income ETFs. The May 2025 debut of an Asia-listed Saudi sukuk ETF illustrates global appetite for these instruments, further internationalizing the Middle East and Africa ETF market.

CBDC and Digital-Asset Frameworks

Regulatory sandboxes in the UAE and Saudi Arabia are paving the way for crypto-linked ETFs. These frameworks enhance custody clarity and settlement efficiency, laying the groundwork for diversified digital-asset strategies within the Middle East and Africa ETF market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Listing Rules | -0.4% | Pan-regional | Medium term (2-4 years) |

| Low Liquidity Outside GCC & South Africa | -0.3% | Nigeria, Kenya, Egypt, Rest of MEA | Short term (≤ 2 years) |

| Foreign-Ownership Caps | -0.2% | Egypt, Nigeria, Kuwait | Long term (≥ 4 years) |

| High Withholding-Tax Leakage | -0.2% | Pan-regional | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Listing Rules Raising Tracking-Error Costs

Differing disclosure and creation-redemption protocols force issuers to run bespoke processes, inflating expense ratios and widening deviations between market price and NAV. Although a GCC passporting initiative is slated for 2025, initial coverage will exclude ETFs, preserving cost headwinds across the Middle East and Africa ETF market.

Low Secondary-Market Liquidity Outside GCC & South Africa Elevates Bid-Ask Spreads

Wide spreads—often exceeding 100 bps—discourage large trades in Nigeria, Kenya, and Egypt. Limited market-maker depth undermines confidence, particularly in thematic funds, hindering fuller participation in the Middle East and Africa ETF market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Fixed-Income ETFs Accelerate on Sukuk Demand

Equity ETFs dominated the Middle East and Africa ETF market with a 64.30% share in 2025, yet sukuk launches provide diversified yield for investors wary of rate volatility. Fixed-income products, though smaller than equities, are projected to grow 6.52% annually, powered by sovereign-wealth-fund allocations to sukuk mandates. Commodity funds, chiefly gold-linked, offer inflation protection, while currency and real-estate strategies remain niche. The Franklin Global Sukuk Fund’s regional allocation underscores mounting institutional appetite for Islamic-compliant credit.

Broader adoption of sukuk ETFs is deepening secondary-market depth, narrowing spreads, and encouraging cross-border listings. As foreign investors gain confidence in Saudi and UAE sovereign curves, fixed-income exposure within the Middle East and Africa ETF market is expected to converge toward global best practices in portfolio construction and liquidity management.

By Investment Strategy: Active ETFs Gain Traction Amid Market Inefficiencies

Passive segment held a 76.10% share of the Middle East and Africa ETF market in 2025. Active strategies are forecasted to see 7.02% CAGR through 2031, capitalizing on price dislocations and sectoral imbalances. Regulatory adjustments now permit non-transparent structures, allowing managers to implement proprietary screens while retaining ETF liquidity benefits. Sovereign-wealth-fund mandates are increasingly carving out allocations for tactical active overlays, reinforcing demand across the Middle East and Africa ETF market.

Evolving investor preferences for outcome-oriented solutions, such as dividend quality or low-volatility screens, are pressing issuers to differentiate through active wrappers. Enhanced digital distribution funnels these strategies into retail portfolios, providing accessible exposure to specialized themes without traditional fund minimums.

By Investor Type: Retail Dominance Sustained as Institutional Flows Accelerate

Retail clients accounted for 58.10% of the Middle East and Africa ETF market in 2025, reflecting intuitive app-based access and sub-USD 100 entry points. Younger demographics leverage ETFs for core holdings, supporting steady inflows to the Middle East and Africa ETF market. Meanwhile, institutions are scaling exposure, especially to fixed-income products, amid reforms that encourage defined-contribution structures across GCC pension systems. The institutional segment is projected to grow at a CAGR of 5.92% between 2026 and 2031.

As auto-enrolment frameworks mature in Nigeria and Kenya, institutional penetration is set to expand. Multi-asset model portfolios increasingly embed ETF cores, lowering operational complexity and boosting transparency for trustees and regulators alike.

By Distribution Channel: Digital Platforms Reshape Access

Direct and Digital Retail Platforms commanded a 35.60% share and display the fastest growth at 7.48% CAGR. Fractional trading, robo-advisory integration, and commission-free pricing democratize ownership for first-time investors. Hybrid partnerships between incumbent banks and fintech firms blend advisory depth with technological scalability, reinforcing the Middle East and Africa ETF market’s distribution transformation.

Financial advisers still wield influence for affluent segments, but fee compression pushes them toward asset-allocation services rather than product selection. Institutional channels remain pivotal for block trades and bespoke baskets, particularly in Saudi Arabia, where sovereign-wealth-fund trades can exceed USD 100 million per ticket.

Geography Analysis

Saudi Arabia retained a 21.45% share of the Middle East and Africa ETF market in 2025, underpinned by Vision 2030 reforms, post-trade automation, and index inclusions that lifted foreign inflows. Completion of the TASI 50 benchmark facilitates granular exposure, while USD 1 trillion in planned infrastructure outlays presents scope for thematic launches in logistics, green hydrogen, and banking.

The United Arab Emirates exhibits the region’s quickest trajectory at a 6.31% CAGR through 2031. Regulatory clarity from Dubai’s Virtual Assets Regulatory Authority supports crypto-linked fund structures, and the expansion of the DEWS pension scheme channels steady contributions toward passive solutions. ESG and clean-energy themes resonate with the government’s net-zero ambitions, nudging issuers to cross-list sustainable strategies on Abu Dhabi’s ADX.

South Africa features the continent’s most mature ETF ecosystem, anchored by Satrix, 1nvest, and Sygnia Itrix. While liquidity concentrates in flagship indices, actively managed wrappers are gaining share as retail demand for tactical plays rises. The Johannesburg Stock Exchange’s robust settlement backbone makes the market a regional benchmark for trading efficiency within the Middle East and Africa ETF market.

Competitive Landscape

Global giants such as BlackRock’s iShares, State Street Global Advisors, and Invesco compete alongside regional specialists including Emirates NBD Asset Management, Chimera Capital, and Satrix. Product pipelines increasingly target first-to-market status in Sharia-compliant fixed income and digital-asset baskets, reflecting the strategic importance of differentiation in the Middle East and Africa ETF market.

White-label platforms lower barriers for boutique managers seeking rapid entry, while sovereign-wealth-fund endorsements provide scale advantages to domestically domiciled issuers. Technology upgrades on the Saudi Exchange and the UAE’s adoption of streamlined listing rules enable quicker time-to-market and support efficient creation-redemption cycles.

Competitive dynamics are sharpening as active ETFs proliferate. Global issuers leverage quantitative research pedigrees to launch rule-based active funds, while regional managers highlight local-market insights. Strategic alliances, such as co-branded sukuk products between Hong Kong and Saudi entities, signal growing cross-border collaboration aimed at deepening the Middle East and Africa ETF market linked to the wider global investor base.

Middle East And Africa ETF Industry Leaders

Satrix

1nvest

Sygnia Itrix

Tabula Investment Management

STANLIB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Premia Partners and BOCHK Asset Management listed Asia’s first investment-grade Saudi government sukuk ETF in Hong Kong, tracking the iBoxx Tadawul Government & Agencies Sukuk Index and charging a 0.35% total-expense ratio.

- April 2025: Robeco introduced the 3D Emerging Markets ETF, blending quantitative signals to capture long-run EM growth opportunities, including allocations to the Middle East and Africa ETF market.

- March 2024: State Street Global Advisors reported robust non-US inflows, citing heightened demand for emerging-market exposures within its SPDR suite.

- January 2025: Saudi Public Investment Fund anchored USD 200 million in the SPDR J.P. Morgan Saudi Arabia Aggregate Bond UCITS ETF, Europe’s first Saudi sovereign-bond fund.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Middle East & Africa exchange-traded fund (ETF) market as the total value of locally domiciled and cross-listed ETFs whose primary listing venue lies within GCC states, wider MENA bourses, or key Sub-Saharan exchanges; valuation is captured at calendar-year close price × units outstanding. Index-tracking funds, actively managed ETFs, smart-beta products, and Sharia-compliant Sukuk ETFs are all included.

Scope exclusion: closed-end funds, exchange-traded notes, and ETFs solely marketed to European investors but lacking a MEA listing are omitted.

Segmentation Overview

- By Asset Class

- Equity ETFs

- Fixed-Income ETFs

- Commodity ETFs

- Currency ETFs

- Real-Estate ETFs

- Alternative ETFs

- By Investment Strategy

- Active

- Passive

- By Investor Type

- Retail

- Institutional

- By Distribution Channel

- Direct and Digital Retail Platforms

- Financial Advisors and Wealth Managers

- Institutional Channels

- Traditional Banks and Full-Service Brokers

- By Country

- United Arab Emirates

- Saudi Arabia

- Qatar

- Kuwait

- Oman

- Bahrain

- Egypt

- South Africa

- Nigeria

- Rest of Middle East and Africa

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews with ETF issuers, custodians, digital broker CEOs, and regional regulators allowed us to validate secondary numbers, gauge true retail participation, and understand upcoming passporting rules across GCC markets.

Surveys of portfolio managers in Saudi Arabia, UAE, South Africa, and Nigeria clarified practical adoption rates by asset class and typical bid-ask spreads that influence effective assets under management.

Desk Research

We gathered foundational statistics from open regulators such as the Saudi Capital Market Authority, Dubai Financial Market, and the South African FSCA, which publish monthly ETF AUM, unit creation files, and fee circulars. Macroeconomic anchors came from IMF Financial Access surveys and World Bank Global Financial Development datasets. Trade associations including ETFGI, Gulf Bond & Sukuk Association, and the African Securities Exchanges Association supplied product counts and asset splits. Company filings, prospectuses, and investor presentation decks helped us capture average fee compression trends. D&B Hoovers and Dow Jones Factiva supported cross-checks on sponsor revenue exposure.

These sources illustrate, but do not exhaust, the material referenced when Mordor analysts compiled historical flows, sponsor launches, and liquidity metrics that feed our base year model.

Market-Sizing & Forecasting

Top-down modeling begins with exchange-published ETF AUM end-balances, converted to USD at average annual FX rates, then adjusted for cross-listing duplication before growth from net creations and price appreciation is forecast through multivariate regression on drivers such as GDP per capita, equity turnover, number of new ETF listings, and average all-in expense ratios. Bottom-up validation samples sponsor-level AUM, unit growth, and indicative average spreads to ensure the aggregate does not materially deviate; any gap beyond two percentage points triggers analyst review. Forecasts to 2030 employ ARIMA with expert-guided scenario overlays to reflect fee-waiver programs, GCC fund-passporting rollout, and shifts toward Sukuk ETFs.

Data Validation & Update Cycle

Outputs pass automated variance checks against independent ETFGI flow tallies and Lipper regional AUM. Senior reviewers interrogate anomalies and, if material events occur mid-cycle, analysts re-open the model. Reports refresh every twelve months, and a final sense-check is completed immediately before client release.

Why Our Middle East And Africa ETF Baseline Commands Credibility

Published estimates differ because firms choose divergent asset universes, apply contrasting FX conversions, or roll forward price appreciation in aggressive ways. We acknowledge these gaps upfront and show how Mordor's disciplined scope and annual refresh cadence deliver a steadier decision-grade baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.1 B | Mordor Intelligence (2025) | - |

| USD 92.5 B | Global Consultancy A (2024) | Counts global-domiciled MENA themed ETFs and values them at peak intra-year AUM, inflating base. |

| USD 46.3 B | Trade Journal B (2024) | Covers Africa only, yet scales figure to 'MEA' without deducting double-listed Gulf funds. |

Taken together, the comparison shows that once duplicate listings, out-of-region domiciles, and end-month spikes are removed, Mordor's figure remains the most reproducible and transparent anchor for strategic planning in the MEA ETF arena.

Key Questions Answered in the Report

What is the current value of the Middle East and Africa ETF market?

The market is valued at USD 23.2 billion in 2026 and is forecast to reach USD 29.74 billion by 2031.

Which asset class is growing fastest within the region’s ETF universe?

Fixed-Income ETFs, propelled by sukuk demand, are projected to expand at a 6.52% CAGR between 2026 and 2031.

How important are retail investors to regional ETF growth?

Retail accounts for 58.10% of turnover and remains the primary volume driver thanks to digital-platform accessibility and low investment thresholds.

Why are active ETFs gaining momentum in the Middle East and Africa ETF market?

Active wrappers appeal to investors seeking to exploit market inefficiencies and sector opportunities unique to the region, leading to an expected 7.02% CAGR.

Which country leads the region in ETF assets under management?

Saudi Arabia holds the largest share at 21.45%, supported by post-trade infrastructure upgrades and sovereign-wealth-fund sponsorship.

What regulatory development could most improve cross-border ETF distribution?

The planned GCC fund passporting system, expected to roll out after 2025, aims to harmonize rules and reduce listing-cost fragmentation across member exchanges.

Page last updated on: