Market Overview

| Study Period | 2020 - 2031 |

|---|---|

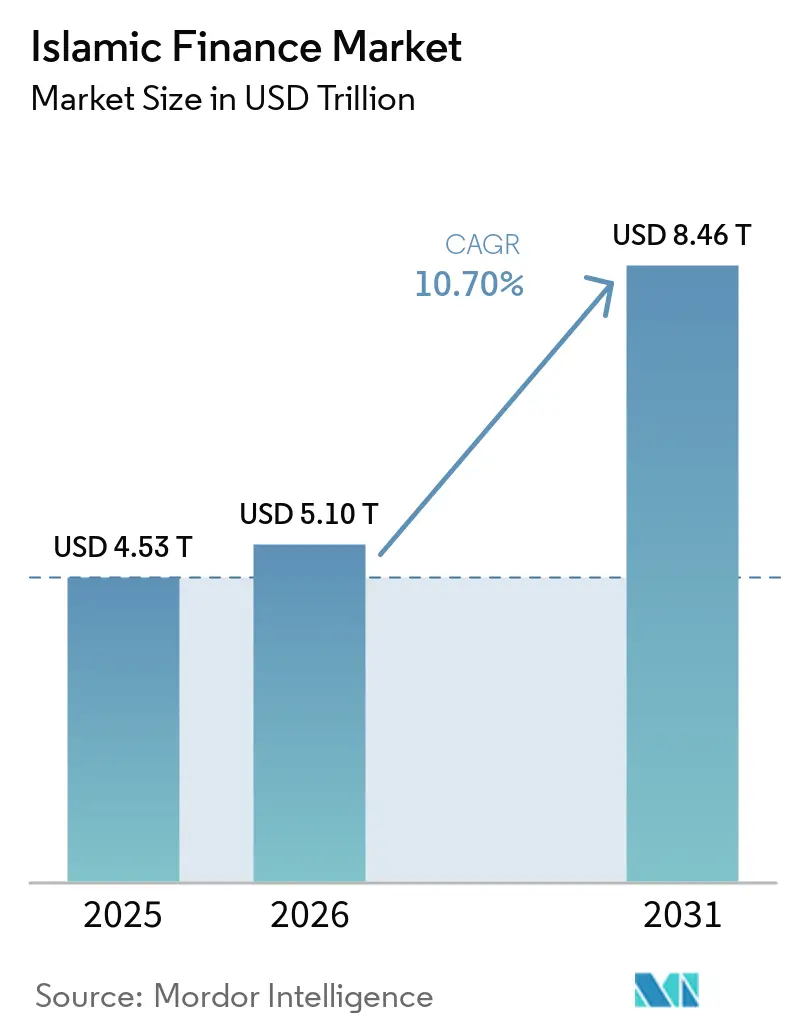

| Market Size (2026) | USD 5.10 Trillion |

| Market Size (2031) | USD 8.46 Trillion |

| Growth Rate (2026 - 2031) | 10.70% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Middle East and Africa |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Islamic Finance Market Analysis by Mordor Intelligence

The Islamic Finance Market size is projected to be USD 4.53 trillion in 2025, USD 5.10 trillion in 2026, and reach USD 8.46 trillion by 2031, growing at a CAGR of 10.70% from 2026 to 2031.

The market size and CAGR figures set a clear growth runway supported by policy mandates, rising demand for Shariah-aligned assets, and expanding digital distribution channels. New issuance patterns also reinforce the momentum, as ESG-linked sukuk gain institutional traction and create a diversified funding base that aligns with climate finance mandates. Governments are accelerating the shift with conversion timelines and national strategies that elevate Islamic banking and capital markets to policy priorities. Tokenization pilots, lower investment thresholds, and standardized ESG frameworks further widen access and improve transparency for investors and issuers.

Key Report Takeaways

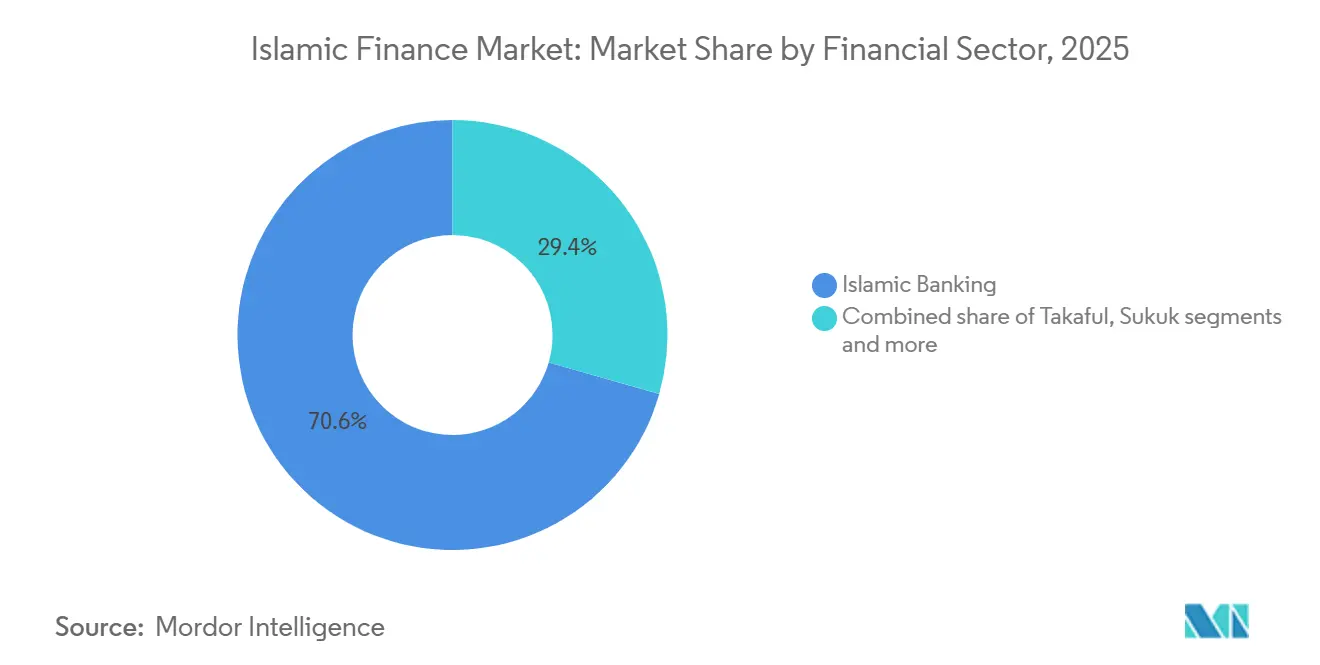

- By financial sector, Islamic banking led with 70.58% market share in 2025, while takaful is forecasted to expand at a 12.80% CAGR through 2031.

- By customer type, businesses held a 58.13% share in 2025, and retail consumers are projected to grow at a 11.40% CAGR through 2031.

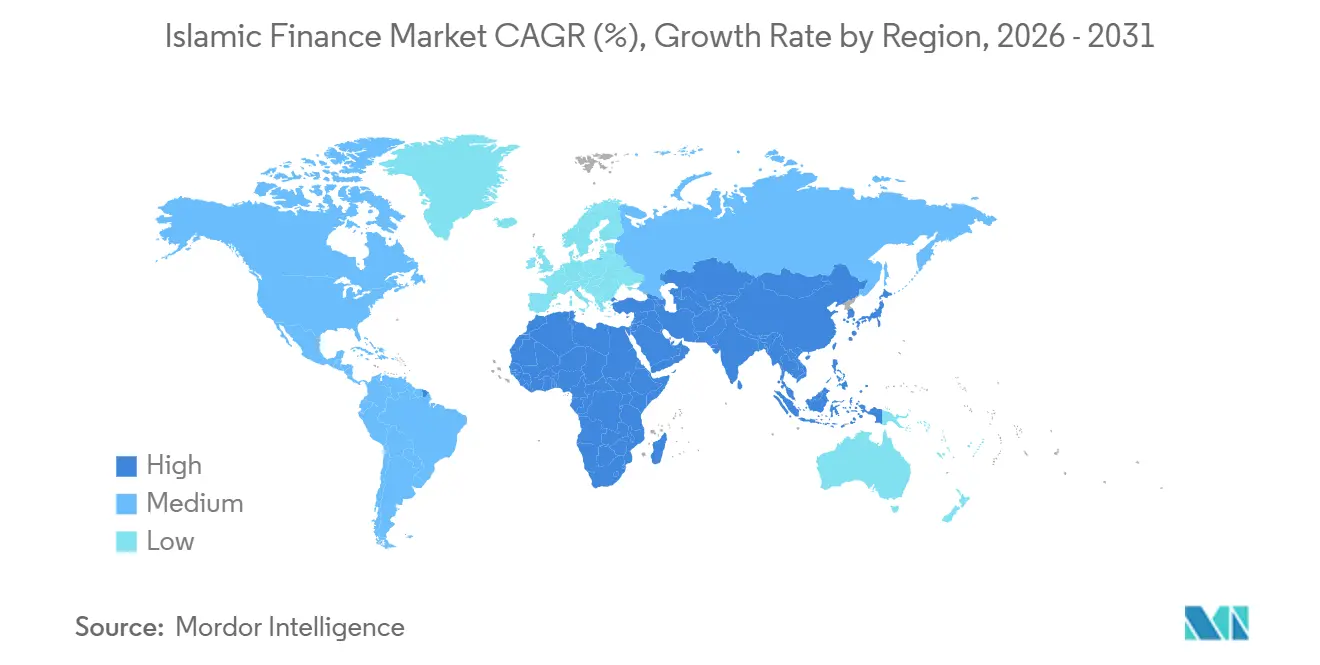

- By geography, the Middle East and Africa accounted for 69.82% of the Islamic finance market in 2025, while Asia-Pacific is projected to expand at a 11.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Islamic Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Muslim Affluence & Demand for Sharia-Compliant Products | +3.2% | Global, with early gains in Malaysia, Indonesia, Saudi Arabia, UAE | Medium term (2-4 years) |

| Government Policy Pushes & Regulatory Harmonisation | +2.8% | National, with concentrated impact in Pakistan, the UAE, Saudi Arabia, and Indonesia | Short term (≤ 2 years) |

| Surge in ESG/Green Sukuk Issuance | +2.1% | Global, led by GCC and Indonesia | Medium term (2-4 years) |

| Cross-Border Islamic FinTech Platforms Opening Micro-Investment Pools | +1.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Blockchain-Enabled Tokenised Sukuk Lowering Issuance Costs | +1.6% | GCC markets with regulatory sandboxes, Malaysia’s capital markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Muslim Affluence & Demand for Sharia-Compliant Products

The global Muslim population of 2 billion in 2025 is projected to expand to 2.8 billion by 2050, yet raw demographic growth masks a subtler catalyst - rising per-capita incomes in Organization of Islamic Cooperation countries are lifting Muslim consumer spending to USD 2.43 trillion as of 2023, creating a middle class that views Shariah compliance not as a premium feature but as a baseline expectation[1]The Star, “Empowering Trade in Muslim Markets,” The Star, www.thestar.com. In Malaysia, a meaningful portion of Islamic finance customers identify as non-Muslim, which signals that product appeal now aligns to broader ESG preferences rather than religious segmentation alone. Retail participation in sovereign sukuk programs in Southeast Asia also shows a durable investor base that returns in each issuance cycle. The Islamic finance market sees this adoption pattern reinforced by digital onboarding and low-ticket investment options that fit the savings behavior of younger cohorts. Institutional allocations that apply exclusion criteria to conventional investments are finding Shariah-compliant instruments that fit standard ESG mandates, which improves liquidity and deepens secondary markets over time.

Government Policy Pushes & Regulatory Harmonisation

Regulatory intent is now a visible growth catalyst for the Islamic finance market as several governments set explicit asset targets and conversion timelines that redirect funding to Shariah channels. Pakistan’s parliamentary mandate to eliminate Riba by 2027 sets a compressed window for conversion that reorients treasury and risk practices at incumbent lenders. The UAE's Islamic Finance Strategy 2025-2031 targets AED 2.56 trillion in banking assets and AED 660 billion in sukuk listings by 2031, embedding Islamic finance as a sovereign wealth diversification lever rather than a niche offering[2]IFSB, “Islamic Financial Services Industry Stability Report 2025,” IFSB, ifsb.org . Other markets are advancing harmonization through legal reforms and supervisory alignment, which lowers cross-border friction and aids the distribution of sukuk and takaful products. Pan-regional efforts in West Africa and selected African sovereigns also show early signs of coordination that could support scale and reduce structuring complexity for the Islamic finance market.

Surge in ESG/Green Sukuk Issuance

ESG sukuk outstanding surpassed USD 55 billion at end-September 2025, with year-to-date issuance of USD 13.5 billion setting a new annual record, yet the critical inflection lies in market-share dynamics: ESG sukuk claimed over 40% of all emerging-market ESG bond issuance (excluding China) in the first nine months of 2025, up from 18% in 2024, a velocity that no other fixed-income asset class has matched[3]Arab News, “ESG Sukuk Outstanding Surpasses $55 Billion,” Arab News, www.arabnews.com. The alignment between Shariah principles and ESG objectives enables more consistent disclosure practices and portfolio tagging for institutional mandates. Joint guidance on green, social, and sustainability sukuk standardizes frameworks and strengthens comparability with conventional ESG bonds. This clarity encourages more sovereign and financial issuers to adopt sustainable formats and increases the pool of assets that meet both ESG and Shariah screens.

Cross-Border Islamic FinTech Platforms Opening Micro-Investment Pools

The Islamic fintech market expanded from USD 138 billion in 2024 to a projected trajectory exceeding USD 300 billion by 2027, yet the transformative element is not aggregate valuation but the democratization of access through platforms such as Wahed. The UAE's Ruya secured regulatory approval in April 2025 to offer Shariah-compliant virtual assets, marking the first instance of an Islamic bank receiving authorization for crypto-adjacent products, a precedent that blurs the line between traditional Islamic banking and decentralized finance. Bahrain's Central Bank licensed Rain and CoinMENA as Shariah-compliant crypto platforms, embedding Islamic jurisprudence into blockchain custody and trading protocols. Bank Aladin Syariah's partnership with Flip in August 2025 launched Super Flip, granting 15 million users the ability to open Islamic savings accounts within a payments app, a Banking-as-a-Service architecture that circumvents costly branch expansion. The cross-border dimension is equally disruptive - Boubyan's Nomo Bank serves UK customers digitally, and fintech firms now number over 512 globally, with projections exceeding 1,000 by 2027, fragmenting market share away from incumbent institutions that rely on physical infrastructure[4]Global Banking Finance Review, “Islamic Fintech's Global Rise: Innovation, Ethics and the Road Ahead,” Global Banking Finance Review, www.globalbankingandfinance.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Shariah Standards Across Jurisdictions | -1.7% | Global, with acute divergence between Southeast Asia and the Middle East | Medium term (2-4 years) |

| Shortage of Certified Shariah Scholars & Risk Professionals | -1.3% | Global, particularly challenging in Malaysia, GCC fintech hubs | Long term (≥ 4 years) |

| Cyber-Security Vulnerabilities in Digital Islamic Banks/FinTechs | -1.1% | Global, with elevated risk in rapid-digitization markets, GCC, and Southeast Asia | Short term (≤ 2 years) |

| Climate-Stress Exposure of Asset-Heavy Islamic Banks in GCC | -0.8% | GCC markets, spill-over to institutions with GCC exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Shariah Standards Across Jurisdictions

Divergent jurisprudence and local interpretations create inconsistent screening thresholds, contract treatments, and asset eligibility, which adds cost to cross-border issuance and distribution. Proposed changes around true asset ownership in sukuk structures can alter the debt-like character of many outstanding instruments and may affect pricing and investor appetite. Uneven adoption of standards across jurisdictions results in selective compliance, which weakens the benefits of harmonization and slows product standardization. Malaysia and several GCC markets maintain distinct frameworks that reflect local legal traditions and supervisory priorities, which complicates scalability for global programs. Issuers and investors navigating multiple regimes incur higher documentation and legal review costs than in conventional markets, which narrows the investor base for the Islamic finance market.

Cyber-Security Vulnerabilities in Digital Islamic Banks/FinTechs

Digital rollouts across mobile and online channels have expanded customer access, but cyber risk is now a top operational concern for many Islamic financial institutions. Surveyed institutions rank cybersecurity higher than traditional credit or liquidity risks, highlighting a need for stronger controls, monitoring, and response capabilities. Integration complexity, data quality gaps, and legacy systems elevate vulnerability during technology migrations and expose new attack surfaces. Smaller institutions face resource constraints that slow the adoption of zero-trust architectures and real-time threat detection, which can weaken incident response. Regulators and industry associations are increasing focus on supervisory frameworks for digital Islamic finance, but implementation capacity is uneven, and risk awareness is still evolving in several fast-digitizing markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Financial Sector: Takaful Overtakes Banking Growth

Islamic banking commanded 70.58% of the Islamic finance market size in 2025, reflecting an asset base that has scaled across core geographies and now underpins credit intermediation at national levels. The Islamic finance market continues to see banks act as anchor issuers and key distribution channels, while takaful has emerged as the fastest-growing segment with a 12.80% CAGR projected through 2031. GCC reforms that mandate coverage in motor and medical lines, combined with new licenses across frontier markets, are sustaining contribution growth and extending reach to underserved segments. In several GCC markets, regulatory capital thresholds are shaping consolidation dynamics, which can reduce fragmentation and raise operating efficiency for the Islamic finance market. Malaysia’s depth in family and general takaful demonstrates that policy support and product breadth can shift household coverage preferences when awareness and access improve.

The Islamic finance market benefits from a wider mix of sovereign, quasi-sovereign, financial, and corporate issuers in 2024 and a rising share of corporate placements. A near-term maturity wall, including USD 105 billion due in 2025, is supporting refinancing activity and anchoring steady primary volumes. Islamic funds reached USD 308 billion in assets under management in 2024, although the long tail of small funds points to scale challenges and fee pressure. Exchange-traded formats and robo-advisory channels are expanding product access, and tokenization pilots indicate pathways to lower investment thresholds without compromising Shariah governance for the Islamic finance market.

By Customer Type: Retail Digital Surge Narrows Corporate Lead

Businesses accounted for 58.13% of the Islamic finance market share in 2025, reflecting a lending mix led by working capital, trade finance, and infrastructure-related credit. Corporate sukuk volumes have expanded since 2020 and now provide a competitive alternative to syndicated loans in multiple markets. Surveys of large enterprises indicate that many first-time issuers are driven by pricing, ESG alignment, and new investor access rather than by prior experience with Islamic products. This is most visible in sectors with asset-backed cash flows and tangible collateral, where Shariah structures align well with project and supply-chain financing needs. These factors are consolidating corporate demand, while improving disclosure practices and investor education broaden the appeal of the Islamic finance market to a wider base of treasurers and CFOs.

Retail consumers are the fastest-growing customer group, expanding at a 11.40% CAGR through 2031 as high mobile- and online-transaction ratios become standard at leading banks. Digital-first propositions, Banking-as-a-Service integrations, and micro-investment features draw younger users who favor seamless onboarding and low ticket sizes. Robo-advisory models and exchange-traded products are building new retail investor bases for sukuk and Islamic funds, which raises the long-term savings pool for the Islamic finance market. The cost-to-serve advantages in digital channels support unit economics that can improve return profiles even as competition shifts pricing in select retail categories.

Geography Analysis

Middle East and Africa held 69.82% of the global base in 2025, and GCC markets accounted for a significant share of asset growth as national programs leaned on sukuk and Shariah-compliant lending. Saudi Arabia has one of the highest Islamic banking penetration levels, supported by steady sovereign and agency issuance pipelines that reinforce market depth. Qatar, Kuwait, and Bahrain maintain strong positions in Islamic banking and are building fintech sandboxes and digital-asset labs that support experimentation in custody and tokenization. Oman and Egypt show momentum with double-digit growth in Islamic assets and increasing transaction volumes, although penetration remains below regional leaders. Sub-Saharan Africa has a growing footprint of banks and windows across many jurisdictions, yet most institutions remain subscale and rely on policy support and multilateral partnerships to extend reach in the Islamic finance market.

Asia-Pacific is the fastest-growing region at a 11.20% CAGR for the Islamic finance market size through 2031, with Indonesia, Malaysia, and Pakistan setting the pace. Malaysia combines deep capital markets with a high share of Shariah financing and has signaled its intent to expand retail access through tokenized lots. Indonesia has established itself as a benchmark sovereign for green sukuk, which attracts ESG-focused mandates from Europe and other regions while building a domestic retail investor base. Pakistan’s conversion timeline introduces execution challenges but also creates a roadmap that could reconfigure market structure and accelerate product innovation. The region’s digital-first banking approaches and mobile adoption rates support seamless retail growth for the Islamic finance market.

Europe and the Rest of the World contribute smaller shares but carry strategic weight through listings and specialization. The United Kingdom operates five standalone Islamic banks and multiple windows, while the London Stock Exchange captures a leading share of hard-currency sukuk listings. Retail growth has been solid as digital channels expand product access and align with ethical investing trends among diverse communities. Cross-border fintech links are expanding the number of platforms and providers that operate in new corridors and enable Islamic savings and investment solutions. Partnerships among regional agencies and international standard-setters are building harmonized frameworks that can reduce friction and improve scale for Islamic finance.

Competitive Landscape

Market concentration is bifurcated by geography and scale, with the top five markets controlling a majority of global assets while more than 1,980 institutions operate across 90-plus jurisdictions. This structure leaves a long tail of small and mid-sized players that face rising technology and compliance costs. Leading banks are shifting focus from branch expansion to digital transformation and low-ticket investment access that opens sukuk and funds to retail users. ESG integration and tokenization are now mainstream themes across front-runners, which improves transparency and broadens the distribution footprint for the Islamic finance market. Regional consolidation continues where capital requirements and scale economics favor mergers or strategic alliances.

Technology adoption is a key differentiator as institutions deploy smart sukuk platforms and tokenized issuance to reduce costs and settlement times. Lowering minimum subscription sizes from institutional thresholds to retail-friendly levels is shifting the investor base and raising secondary-market liquidity potential. Standards bodies and market utilities have demonstrated tokenized sukuk proofs-of-concept for institutional investors, which supports operational readiness for wider rollout. Retail access initiatives from exchanges and regulators are also creating pathways for micro-investments that can accelerate household participation. These moves support a broader rebalancing of the Islamic finance market toward digitally enabled growth.

Multilateral partnerships are expanding the funding base for private credit and infrastructure finance that align with asset-backed Shariah structures. Programs that mobilize public and private capital for micro, small, and medium enterprises aim to direct a larger share of financing into productive sectors. Cross-border regulatory cooperation is also advancing in West Africa and other regions, which can streamline licensing and governance for new entrants. These collaborative models reinforce the international orientation of the Islamic finance market and reduce the reliance on single-country demand cycles. Institutions that treat compliance as a narrow objective risk ceding ground to digital-first challengers that operate at lower structural costs and adapt faster to standardization.

Islamic Finance Industry Leaders

Al Rajhi Bank

Dubai Islamic Bank

Kuwait Finance House

Qatar Islamic Bank

Maybank Islamic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Saudi Arabia approved its Annual Borrowing Plan for 2026, totaling SAR 217 billion (~USD 58 billion), outlining sovereign debt issuance (including bonds and sukuk) to cover the projected budget deficit and debt-maturity obligations while deepening its local capital markets.

- December 2025: Sammilito Islami Bank PLC (Bangladesh’s largest state-owned Shariah bank) officially began operations after the merger of five troubled Shariah-based banks (EXIM Bank, First Security Islami Bank, Global Islami Bank, Social Islami Bank, Union Bank), consolidating assets and stabilising the Islamic banking sector.

- October 2025: The Islamic Development Bank raised EUR 500 million through a five-year Green benchmark sukuk issuance under its enhanced sustainable finance framework, achieving strong investor demand and oversubscription, supporting ESG-aligned Shariah-compliant financing.

- May 2025: The UAE Cabinet approved the National Strategy for Islamic Finance and the Halal Industry, aiming to significantly expand the sector’s scale — including raising Islamic banking assets to AED 2.56 trillion and boosting sukuk issuances to over AED 660 billion by 2031.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Islamic finance market as the aggregate value of assets, liabilities, and fee-based services that pass a recognized Sharia supervisory board, covering Islamic banking deposits and loans, sukuk outstanding, takaful contributions, Sharia-compliant investment funds, and other licensed Islamic financial institutions. According to Mordor Intelligence, figures are reported in current U.S. dollars and span more than seventy jurisdictions.

Scope Exclusions: We exclude unregulated crypto tokens lacking formal Sharia certification, as well as informal peer-to-peer lending circles.

Segmentation Overview

- By Financial Sector

- Islamic Banking

- Takaful (Islamic Insurance)

- Sukuk (Islamic Bonds)

- Islamic Funds

- Other Islamic Financial Institutions (OIFIs)

- By Customer Type

- Retail Consumers

- Businesses

- By Region

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- Kuwait

- Bahrain

- Oman

- Egypt

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

- Malaysia

- Indonesia

- Pakistan

- Bangladesh

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Rest of Europe

- Rest of the World

- Middle East and Africa

Detailed Research Methodology and Data Validation

Primary Research

We conducted structured interviews with Sharia scholars, treasury heads at GCC and Southeast Asian banks, and Islamic fintech founders to validate certification practices, asset-mix shifts, and product-rollout timelines. Follow-up surveys with institutional investors and takaful managers sharpened assumptions on average ticket sizes and regional growth triggers.

Desk Research

We compiled macro-economic indicators, banking statistics, and Islamic capital-market bulletins from sources such as the Islamic Financial Services Board, IMF Financial Access Survey, and national sukuk prospectuses. Additional context on fintech adoption and ESG sukuk pipelines was gathered from leading academic journals, respected business dailies, and central-bank monetary reports. Our team also tapped Dow Jones Factiva for company filings and Questel for patent trends on blockchain-enabled settlement. This listing is illustrative; many more references informed data collection and validation.

Market-Sizing & Forecasting

Our model starts with a top-down asset reconstruction built from central-bank Islamic windows, sukuk registries, and takaful gross written premiums. It then corroborates totals with sampled balance-sheet roll-ups and average-spread analysis. Key variables like Muslim population growth, oil-price-linked liquidity, cross-border sukuk issuance volume, digital account penetration, and regulatory capital buffers feed a multivariate regression with scenario analysis. Bottom-up provider checks adjust any gaps, especially in emerging jurisdictions where disclosure remains thin.

Data Validation & Update Cycle

Modeled outputs pass three analyst reviews, where variance thresholds trigger re-contact of field sources. Reports refresh annually, and extraordinary events such as major policy shifts or large default episodes lead to interim updates. A final analyst pass ensures clients receive the latest view.

Why Mordor's Islamic Finance Baseline Commands Market Confidence

Published estimates often diverge because firms choose different asset buckets, convert currencies on different dates, and refresh models at uneven intervals.

Key gap drivers include whether sukuk are recorded at par or market value, if off-balance-sheet mudarabah pools are counted, and how fintech-related fee income is imputed before growth is compounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.47 Trn (2025) | Mordor Intelligence | |

| USD 5.98 Trn (2024) | Global Consultancy A | Combines conventional bank Islamic windows and applies year-end FX averages that inflate totals. |

| USD 5.00 Trn (2025) | Trade Journal B | Omits family takaful assets and uses a single growth factor without granular product validation. |

The comparison shows that Mordor analysts ground forecasts in verifiable regulatory filings, reconcile product-level detail, and refresh data soon after fiscal releases, giving decision-makers a balanced, transparent baseline they can trace and replicate.

Key Questions Answered in the Report

What is the current size and projected growth of the Islamic finance market by 2031?

The Islamic finance market reached USD 6.10 trillion in 2026 and is projected to grow at an 11.56% CAGR to USD 10.54 trillion by 2031.

Which region leads in share, and which grows fastest through 2031 for Islamic finance ?

Which region leads in share, and which grows fastest through 2031 for Islamic finance?

Which financial sector category is expanding the fastest within Islamic finance?

Takaful is the fastest-growing financial sector, projected at a 14.92% CAGR through 2031, while Islamic banking remains the largest by share.

How are ESG sukuk shaping investor demand in Islamic finance?

ESG sukuk are drawing strong oversubscription and benefit from standardized guidance that aligns with investor ESG screens, which improves liquidity and disclosure.

What role will tokenization play in expanding access to sukuk?

Tokenization pilots and smart sukuk platforms are lowering investment thresholds, enabling retail access, and targeting faster settlement with greater transparency.

What are the key operational risks facing digital Islamic banks and fintechs?

Cybersecurity ranks as a top operational risk due to integration complexity and data quality gaps, which require stronger controls and consistent supervisory frameworks.

Page last updated on: