Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

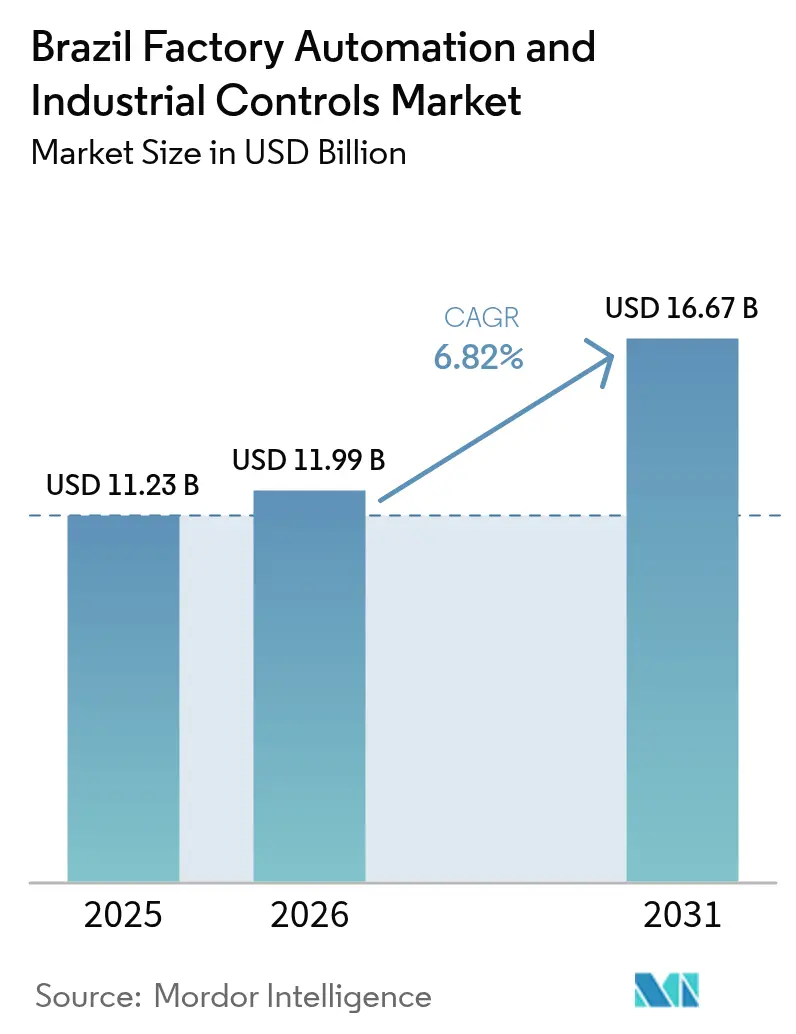

| Base Year Market Size (2025) | USD 11.23 Billion |

| Market Size (2026) | USD 11.99 Billion |

| Market Size (2031) | USD 16.67 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

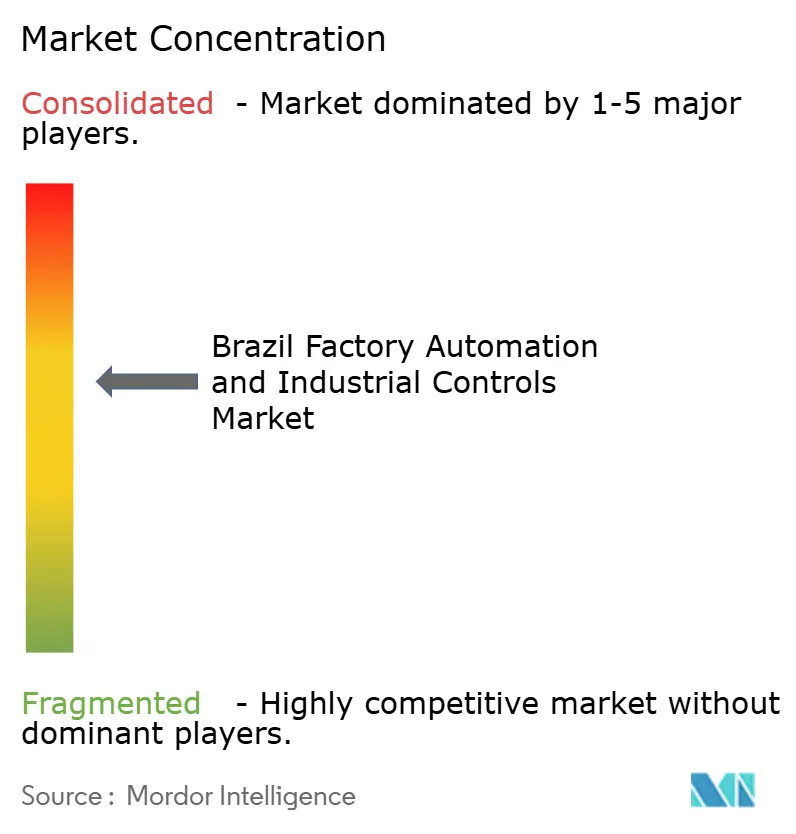

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The Brazil factory automation and industrial controls market size is expected to grow from USD 11.23 billion in 2025 to USD 11.99 billion in 2026 and is forecast to reach USD 16.67 billion by 2031 at 6.82% CAGR over 2026-2031. The upward trajectory springs from government-backed Industry 4.0 incentives, higher labor costs, and faster digital transformation across manufacturing. Tax advantages for automation imports, large-scale industrial policy spend, and private 5G roll-outs shorten payback periods and unlock new return-on-investment thresholds. Domestic suppliers capitalize on proximity, while global incumbents pursue ecosystem partnerships to capture rising software and services demand. Cyber-security gaps, skilled-labor shortages, and tariff volatility temper the otherwise bullish outlook for the Brazil factory automation and industrial controls market.

Key Report Takeaways

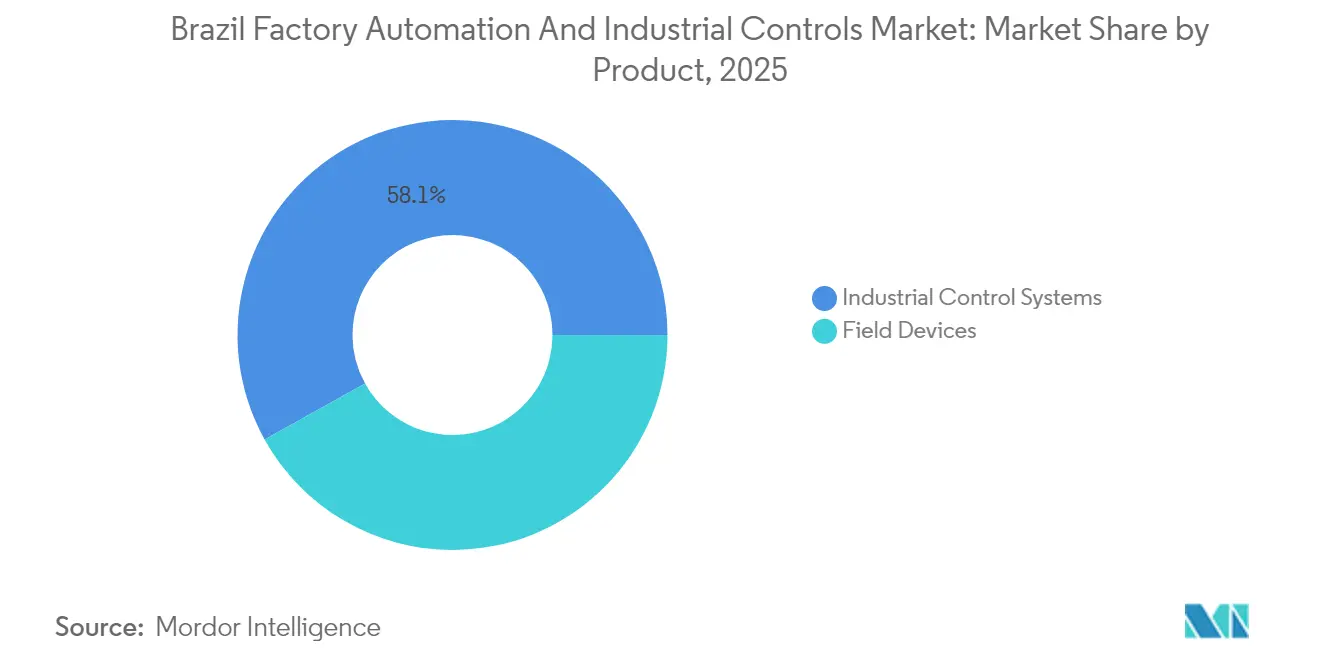

- By product, Programmable Logic Controllers led with 58.07% of Brazil factory automation and industrial controls market share in 2025. Machine vision systems are projected to expand at a 7.20% CAGR between 2026-2031.

- By end-user, the automotive sector commanded a 24.39% share of the Brazil factory automation and industrial controls market size in 2025. Pharmaceutical manufacturing is advancing at a 7.07% CAGR through 2031.

- Hardware accounted for a 52.02% share of the Brazil factory automation and industrial controls market size in 2025, while software components recorded the fastest growth at a 7.42% CAGR.

- On-premises deployment retained 74.35% share of the Brazil factory automation and industrial controls market size in 2025; cloud-based solutions are scaling at an 7.82% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentive packages for Industry 4.0 | +1.2% | National, with early gains in São Paulo, Rio de Janeiro, Minas Gerais | Medium term (2-4 years) |

| Rising labor cost pushing automation ROI | +1.0% | National, concentrated in industrial centers | Short term (≤ 2 years) |

| Proliferation of industrial IoT platforms | +0.8% | National, spill-over to manufacturing clusters | Medium term (2-4 years) |

| Automotive OEM re-investment in Brazilian plants | +0.7% | São Paulo, Minas Gerais, Rio Grande do Sul | Short term (≤ 2 years) |

| Tax-credit Law 14.184/2021 accelerating digital CAPEX | +0.6% | Export Processing Zones, industrial parks | Long term (≥ 4 years) |

| Roll-out of 5G private networks in industrial parks | +0.5% | São Paulo, Rio de Janeiro, major industrial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentive Packages for Industry 4.0

Federal and state programs directly subsidize automation investments and allow accelerated tax deductions on R&D, changing the cost equation for manufacturers. The Nova Indústria Brasil program earmarks USD 33.9 billion for digitalization, while the Neoindustrialização platform channels subsidized credit to 200,000 SMEs to upgrade production assets. Stacked with Lei do Bem benefits and below-market BNDES financing, qualifying projects now recoup outlays in 18-24 months instead of the traditional 3-5 year cycle. Local champions such as WEG top corporate innovation rankings by funneling these incentives into expanded product lines and in-house R&D centers.[1]WEG, “PC Factory MES 4.0,” weg.net

Rising Labor Cost Pushing Automation ROI

Brazil’s labor-cost index touched 175.6 points in March 2025, and wages in industrial hubs are rising 8-12% annually.[2]Trading Economics, “Brazil Labour Costs,” tradingeconomics.com At the same time, average automation hardware prices have fallen 15-20%. The narrowing gap makes robots attractive even in labor-intensive sectors such as textiles and food packing. Manufacturers now aim to cut costs rather than merely boost output; Novelis saved 2,700 hours yearly through robotic process automation, and Florisa doubled productivity on automated looms.

Proliferation of Industrial IoT Platforms

Nationwide deployments of private 5G pave the way for ultra-low-latency data flows between sensors, controllers, and edge servers. Vivo-Nokia’s network at Ambev shaved maintenance expenses by 40% through predictive analytics, and Telit-Nestlé achieved a 25% energy drop via real-time optimization. WEG’s PC Factory MES 4.0 integrates 70 AI models for anomaly detection, strengthening domestic technology stacks.

Automotive OEM Re-investment in Brazilian Plants

Global automakers revitalize local plants to assemble electric drivetrains and flexible vehicle platforms. Stellantis secured BNDES funding to automate assembly and quality-control systems, mirroring sector-wide moves to ensure export-grade standards. The automotive domain’s 24.74% share signals deep, capex-heavy automation needs, from robotic welding to battery testing lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of skilled automation engineers | -0.9% | National, acute in interior regions | Long term (≥ 4 years) |

| High upfront CAPEX for SMEs | -0.7% | National, concentrated in smaller industrial centers | Medium term (2-4 years) |

| Mercosur tariff volatility on electronic components | -0.4% | National, import-dependent manufacturers | Short term (≤ 2 years) |

| Cyber-security gaps in legacy SCADA assets | -0.3% | National, legacy industrial facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Skilled Automation Engineers

Although SENAI expanded programs to accommodate 115,000 trainees, demand still exceeds supply by roughly 40-50% in main clusters. Salaries for automation engineers sit 25-35% above other engineering roles, pressuring margins and lengthening roll-out timelines. Partnerships with multinational suppliers aim to standardize curricula, but the average 18-month training cycle means bottlenecks will linger.

High Upfront CAPEX for SMEs

A meaningful automation package costs USD 200,000-500,000, equating to 2-5 years of profits for typical small manufacturers. Even with subsidized credit, many companies struggle to meet collateral or documentation requirements. The misalignment limits penetration in food processing, textiles, and metal fabrication, threatening a two-speed landscape where large firms widen productivity gaps over SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: PLCs Anchor Control Architecture

Industrial Controls held 58.07% of Brazil factory automation and industrial controls market share in 2025. Their role as the digital backbone binds equipment, sensors, and higher-level applications, supporting broad compatibility needs. Field Devices are forecast to outpace all other categories with a 7.20% CAGR as quality standards tighten. A study at the Federal University of Santa Catarina recorded 100% defect-detection accuracy in PCB inspection, underscoring efficiency gains. Robots, sensors, motors, and SCADA solutions converge to deliver integrated, data-rich environments where predictive algorithms continually refine process parameters. In this framework, PLC upgrades remain recurring purchases, securing the platform position of leading vendors.

Hardware commoditization nudges differentiation toward software overlays and connectivity protocols. SCADA suites now integrate cloud dashboards and mobile alerts to slash response times. Motors and drives embrace variable-speed elements and diagnostics to cut energy use and prevent unplanned downtime. Even low-profile devices such as relays adopt smart sensing for predictive failure, extending system-wide visibility.

By End-user: Pharmaceutical Accelerates Digital Transformation

The pharmaceutical domain is projected to record the fastest 7.07% CAGR, stimulated by stringent regulatory compliance and capacity expansion. Novo Nordisk’s USD 1.16 billion Montes Claros facility will feature aseptic lines and automated labs, setting a reference for industry peers. In contrast, the automotive domain maintains leadership at 24.39% of the Brazil factory automation and industrial controls market size, but growth moderates as prior robotics investments mature. Utilities modernize grids with real-time monitoring, as evidenced by Siemens Energy’s USD 55 million contracts with Eletrobras for substation upgrades. Food and beverage producers automate traceability to satisfy safety and export rules, while oil and gas companies integrate cyber-secure SCADA frameworks to protect critical assets.

By Component: Software Solutions Drive Digital Integration

Hardware retained 52.02% share in 2025, yet software is set to expand 7.42% annually as manufacturers connect MES, ERP, and AI layers. Copersucar’s adoption of GE Vernova’s iFIX HMI/SCADA and Historian delivered overtime savings and real-time KPIs accessible on mobile dashboards. Local solution providers such as SKA tailor MES logic to Brazilian tax and compliance rules, capturing accounts where global off-the-shelf options lack localization. Long-term service contracts, including cybersecurity patching and predictive maintenance, add recurring revenue streams and deepen customer lock-in.

By Deployment Model: Cloud Migration Accelerates

On-premises architectures remain mainstream with 74.35% share in 2025, reflecting legacy asset bases and security mindsets. Even so, cloud-native deployments are on an 7.82% CAGR as private 5G and edge gateways ensure deterministic response while granting scalable analytics. Hybrid approaches place control loops on edge devices and feed operational data to cloud AI engines, satisfying latency constraints. SMEs benefit from “platform-as-a-subscription” offers that shift capex to opex and provide elastic analytics without in-house IT teams.

Regulatory Landscape

Brazil’s factory automation and industrial controls environment is shaped by national standardization and industrial policy. Conmetro and Inmetro sit at the core of metrology and conformity assessment under the SINMETRO framework (Law 5.966), influencing how automation hardware and electrical-electronic components are qualified for industrial use. On the industrial-policy side, the Nova Industria Brasil (NIB) program launched in January 2024 sets explicit digital transformation targets through 2026 and 2033, and its Mission 4 prioritizes domestic capability in industrial robots, semiconductors, and advanced digital services, linking incentives to modernization and localization agendas.

Connectivity and cybersecurity requirements increasingly intersect with industrial automation deployments that rely on telecom networks. ANATEL has published cybersecurity requirements for equipment and, in November 2024, issued guidelines for auditing telecom equipment suppliers’ cybersecurity policies, reinforcing security-by-design expectations for networked infrastructure that underpins private cellular and industrial IoT connectivity. Separately, the Federal Council of Industrial Technicians (CFT) Resolution 260/2024 clarifies professional attribution for technicians in instrumentation and automation, which affects workforce compliance and contracting practices for plant modernization projects.

Competitive Landscape

The Brazil factory automation and industrial controls market shows moderate fragmentation. Domestic manufacturer WEG leads local hardware supply and invests USD 122 million over five years to expand embedded electronics, bolstered by CADE-approved acquisitions such as Reivax. NOVA Smar extends its System302 platform to capture continuous-process industries. Global multinationals, Siemens, ABB, Schneider Electric- bundle hardware, software, and service layers, forming technology partnerships with local integrators to address Brazilian standards. Hitachi Energy’s USD 218 million transformer expansion underscores power-system automation growth.[3]Energia Limpa, “Hitachi Energy anuncia investimento de mais de R$ 1,2 bilhão no Brasil,” energialimpa.live

White-space opportunities lie in SME financing solutions, cyber-secure retrofits for legacy SCADA, and AI-rich cloud MES. Start-ups such as Automni, funded with BRL 5.5 million, target mobile robotics for warehouses. Value-added features, energy optimization, predictive maintenance, mobile insights, differentiate offers, and create adoption stickiness. Vendors with certified domain solutions gain preference where sector-specific regulations prevail, such as ANEEL guidelines in utilities or GMP in pharmaceuticals.

Brazil Factory Automation And Industrial Controls Industry Leaders

Rockwell Automation Inc.

Honeywell International Inc.

Schneider Electric SE

ABB Ltd.

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is in aligning automation portfolios with Brazil’s industrial-policy instruments that reward local production and measurable digital progress. Interministerial Ordinance No. 159 (January 2026) updated the Basic Productive Process (PPB) for locally made industrial automation assets, including rules tied to frequency converters/inverters. This supports suppliers and assemblers that can localize drives, panels, and control components while maintaining required manufacturing steps. In April 2026, Inmetro launched an Industry 4.0 Maturity Classification Program that standardizes how companies assess and accredit digital advancement, giving manufacturers and solution providers a clearer basis for roadmaps, vendor selection, and documentation tied to a national benchmark rather than fragmented frameworks.

End-market investment programs are also creating whitespace for integrated control, safety, electrification, and data layers, particularly in process industries and other network-dependent operations. Petrobras-linked modernization work provides a concrete example, with Schneider Electric integrating electrical and automation systems, including Foxboro DCS and Triconex safety, for the Abreu e Lima refinery Train 2 project. This points to demand for brownfield control upgrades and safety-instrumented retrofits. Connectivity-driven automation extends beyond traditional factories as well, with Vivo’s March 2026 partnership with Sao Martinho to deploy 4G, NB-IoT, and LTE-M across 3 million hectares to support telemetry and automation use cases in agro-industrial operations, expanding demand for sensors, edge gateways, and cloud-connected SCADA/MES integrations.

Recent Industry Developments

- June 2026: Honeywell announced it will provide modular Ecofining process technology plus integrated control and safety systems for Acelen Renewables biofuel production in Bahia. The package couples process technology with automation and safety layers, supporting demand for modern DCS, SIS, and advanced control in Brazil’s renewable fuels buildout.

- April 2026: Rockwell Automation said it was selected as an end-to-end integration partner for Vale’s Carajas Plant 1 retrofit, deploying PlantPAx distributed control systems to support waterless iron ore processing. The project underscores the role of integrated DCS platforms in large brownfield retrofits where sustainability targets drive instrumentation, control, and systems modernization.

- April 2025: Novo Nordisk announced a BRL 6.4 billion (USD 1.16 billion) expansion of its Montes Claros plant, adding automated aseptic lines and new jobs. The investment reinforces pharmaceutical manufacturing as a high-compliance automation buyer, increasing demand for validated MES/SCADA, traceability, and automated quality-control systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated in Brazil from factory automation and industrial control solutions that monitor, control, and optimize industrial operations, including industrial control systems and factory floor devices used across process and discrete manufacturing.

Scope exclusions: We exclude general-purpose IT hardware, office software, and building automation systems that are not primarily used for industrial process or machine control.

Segmentation Overview

- By Product

- Field Devices

- Machine Vision

- Robotics

- Sensors

- Motors and Drives

- Relays and Switches

- Other Field Devices

- Industrial Control Systems

- SCADA

- DCS

- PLC

- MES

- PLM

- ERP

- HMI

- Other Industrial Control Systems

- Field Devices

- By End-user Industry

- Automotive

- Chemical and Petrochemical

- Power and Utilities

- Pharmaceutical

- Food and Beverage

- Oil and Gas

- Other End-user Industries

- By Component

- Hardware

- Software

- Services

- By Deployment Model

- On-premises

- Cloud-based

- Hybrid / Edge

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for Brazil manufacturing activity, industrial investment, and technology adoption patterns that influence automation spending. We relied on public sources such as IBGE industrial production and national accounts series, Brazil Central Bank macro indicators, MDIC/Comex Stat trade data for relevant equipment categories, and statistics from organizations such as the International Federation of Robotics.

To translate these signals into a usable model, we also reviewed company filings and investor presentations, product documentation, association publications, and credible press coverage tied to automation projects and plant upgrades. Where it helped validate company exposure and cross-check revenue splits, we also used paid subscriptions for company financials and intelligence, news and financials, and patent databases to sanity-check innovation intensity and supplier positioning. The desk sources listed above are illustrative, and many other public references were also used to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with people involved in buying, specifying, integrating, and maintaining automation and control systems in Brazil, including end users and channel participants. We used these discussions to test adoption timing, typical replacement cycles, pricing movement, and how projects are phased across industries, and then to resolve unclear points from public data before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | |

| Mid tier: 48% | Functional/Unit leaders: 26% | |

| Smaller Players: 22% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs Brazil automation demand from manufacturing output and capex signals, and then allocates that spend into automation and control categories based on observed adoption and replacement behavior. The model is then corroborated with selective bottom-up checks, such as sampled ASP times shipment or install volumes for common device classes, partner channel checks, and supplier exposure checks, so totals are adjusted when the two views drift.

Key inputs that were tracked include manufacturing production trends, automation penetration across major end-user industries, typical project lead times, replacement cycles for controls and field devices, and pricing movement for core hardware and software. When a data series was incomplete, we filled gaps using ranges validated in interviews and then applied conservative smoothing so one-off project spikes did not distort the base.

For forecasting, scenario analysis was used because demand depends heavily on industrial investment timing and policy or currency-driven import costs. Assumptions on growth drivers were reviewed with practitioners so the forecast stays tied to practical triggers, such as plant modernization waves, Industry 4.0 programs, and deployment shifts toward connected architectures.

Data Validation & Update Cycle

Outputs are checked against independent signals, such as industrial production direction, trade flow behavior for key equipment categories, and expected capex cycles by industry. If a segment shows an unusual jump or drop, we re-check the underlying drivers, revisit interview notes, and rerun sensitivity cases until the variance is understood and documented.

Before sign-off, the model goes through stepwise analyst reviews that focus on unit consistency, price and volume logic, and year-to-year continuity. Reports are refreshed annually, and interim updates are triggered when material events occur, such as regulatory changes, major investment announcements, or sharp currency shifts that can change imported equipment pricing. Right before delivery, we do a final pass so clients receive the most current view available.

Mordor Intelligence's Brazil Factory Automation and Industrial Controls Market Size Compared Against Other Published Estimates

Published market sizes for Brazil factory automation and industrial controls can vary because groups often count different product boundaries, apply different pricing paths, and do not always align on what portion of plant spending is truly automation related. Timing also matters, since estimates can be anchored to different base years and converted into USD using different exchange-rate windows.

In practice, the widest gaps come from whether field devices and industrial control systems are both included at full value, how software and services are treated, and whether the estimate reflects project-based demand spikes or a normalized replacement cycle. Another driver is refresh cadence, where older assumptions on hardware pricing and cloud adoption can keep figures from matching current buying behavior, which is why the scope and checks built into the model matter for decision-making, a discipline applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.23 B (2025) | |

| Global Consultancy A | USD 11.10 B (2025) | Uses a similar year anchor but can differ on whether certain software layers and supporting services are counted as part of industrial controls revenue, which narrows the scope slightly and lowers the total. |

| Industry Publisher B | USD 4.65 B (2024) | Anchored to an earlier base year and appears to use a tighter inclusion set that may emphasize control systems over the broader factory automation stack, which reduces the measured market value. |

The comparison shows that even small scope choices, like how software and services are handled, can shift the total, and base-year selection can widen the spread further. By keeping the variables traceable to manufacturing activity, adoption, replacement timing, and price movement, the resulting estimate stays easier to reproduce and audit across update cycles.

Key Questions Answered in the Report

How large is the Brazil factory automation market in 2026?

The Brazil factory automation market size is USD 11.99 billion in 2026 and is projected to reach USD 16.67 billion by 2031 at a 6.82% CAGR.

Which sector is expanding fastest in Brazilian factory automation?

Pharmaceutical manufacturing leads with a 7.07% CAGR as firms upgrade quality control and expand capacity.

Why are Brazilian manufacturers moving to cloud-based automation?

Private 5G networks and edge gateways now let plants access scalable analytics without compromising real-time control, driving an 7.82% CAGR in cloud deployments.

What is the main barrier to wider automation adoption among Brazilian SMEs?

High upfront capital needs, typically USD 200,000-500,000, remain a hurdle despite subsidized credit schemes.

Which company is the leading domestic player in Brazilian automation hardware?

WEG stands out, backed by a USD 122 million investment program and recent acquisitions to expand power-electronics automation.

Page last updated on: