Electric Traction Motor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.35 Billion |

| Market Size (2031) | USD 26.33 Billion |

| Growth Rate (2026 - 2031) | 8.70% CAGR |

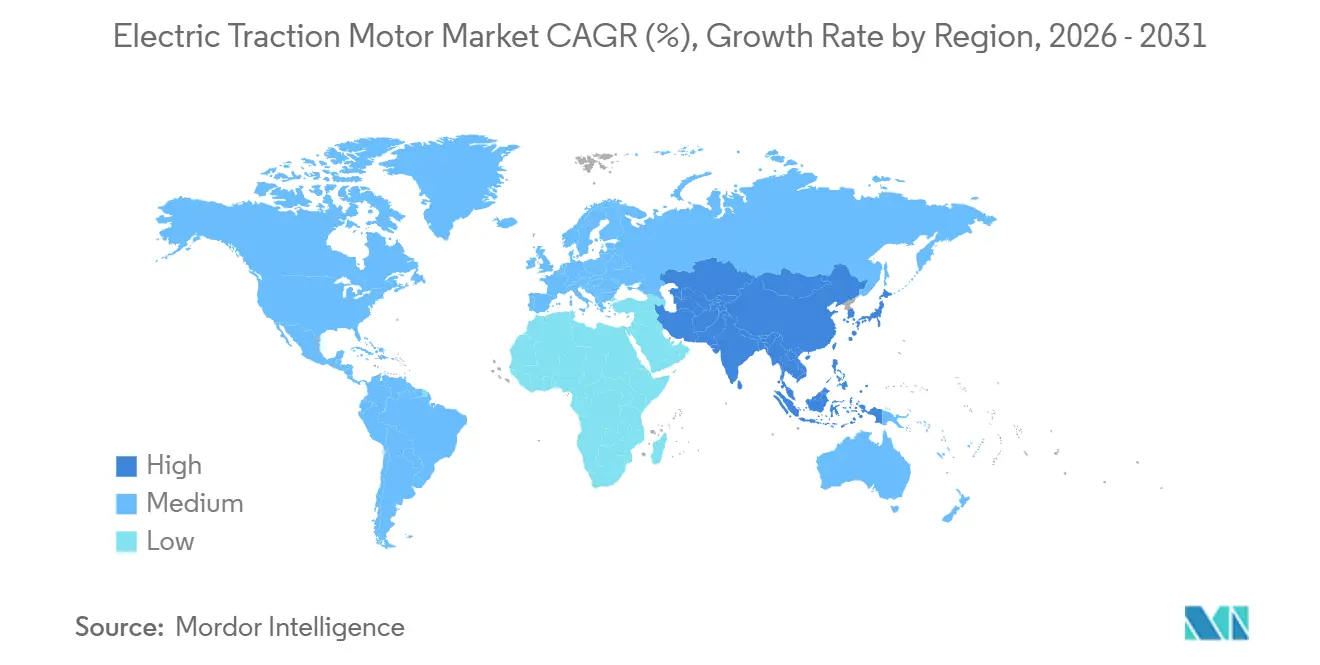

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

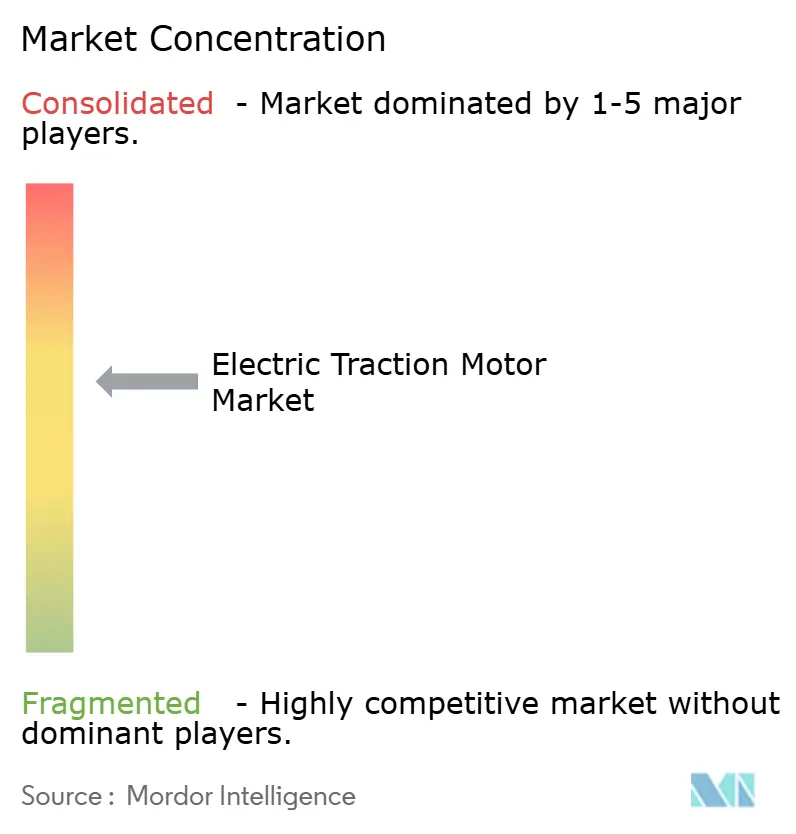

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Traction Motor Market Analysis by Mordor Intelligence

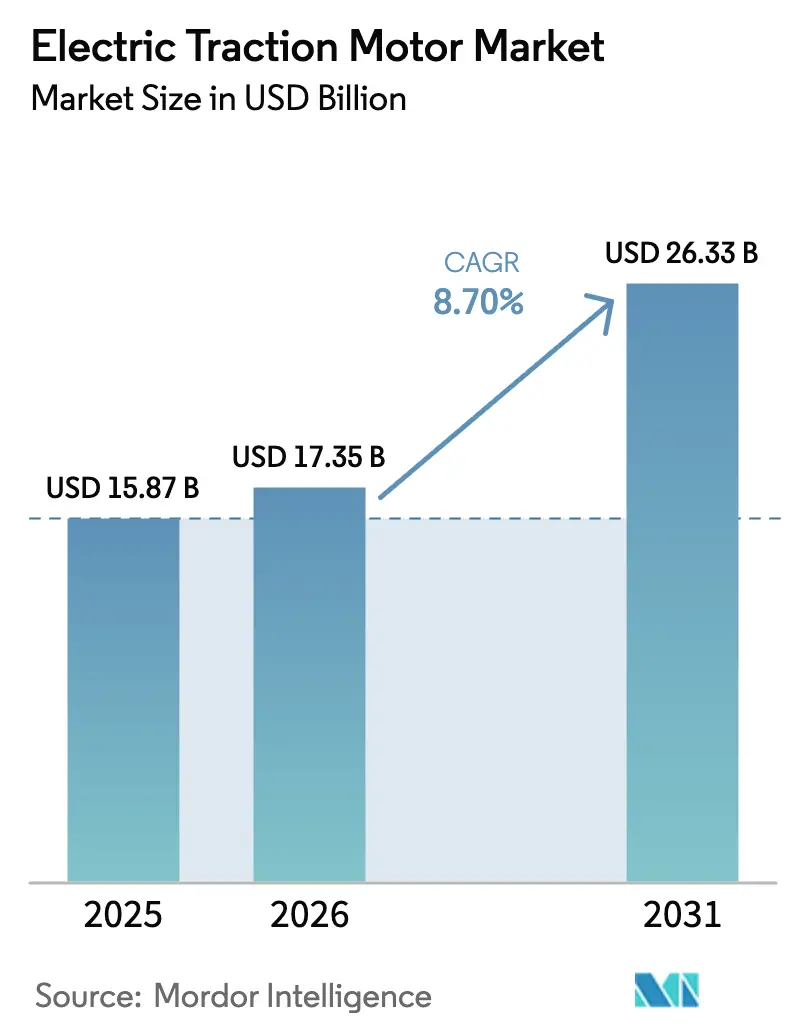

The Electric Traction Motor Market size was valued at USD 15.87 billion in 2025 and is estimated to grow from USD 17.35 billion in 2026 to reach USD 26.33 billion by 2031, at a CAGR of 8.70% during the forecast period (2026-2031).

The growth path reflects rapid rail electrification programs in Asia-Pacific, the spread of 800-volt automotive platforms, and the fast adoption of silicon-carbide inverters that let designers cut motor weight below 70 kilograms without losing torque density. Rising price pressure on rare-earth magnets has eased after new mining capacity in Australia and the United States, while localization mandates in the European Union and India continue to pull new factories closer to end markets. Competition is shifting as premium vehicle makers bring e-axle production in-house, prompting incumbent suppliers to move into higher power and service-oriented niches. Thermal management above 400 kilowatts, uneven rail procurement cycles in South America, and slow rare-earth recycling roll-outs in Europe remain near-term brakes on the electric traction motor market.

Key Report Takeaways

- By type, alternating-current motors held 65.3% revenue share in 2025, and the same is expanding at a 12.1% CAGR through 2031.

- By application, the railway captured 45.4% of the electric traction motor market size in 2025, whereas electric vehicles are advancing at a 15.8% CAGR to 2031.

- By cooling method, air-cooled units led with 59.6% share of the electric traction motor market size in 2025; liquid-cooled systems record the highest projected CAGR at 11.3% through 2031.

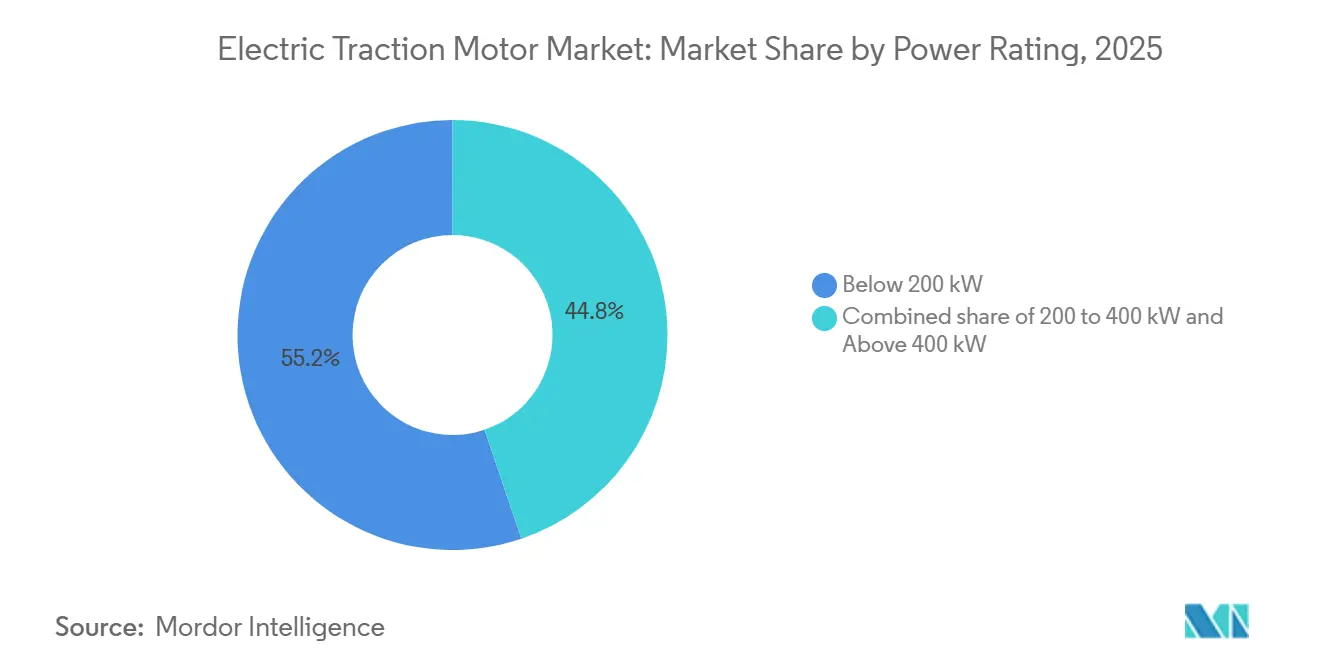

- By power rating, sub-200-kilowatt motors accounted for a 55.2% share of the electric traction motor market size in 2025, while the 200-kilowatt to 400-kilowatt band is forecast to grow at a 10.2% CAGR.

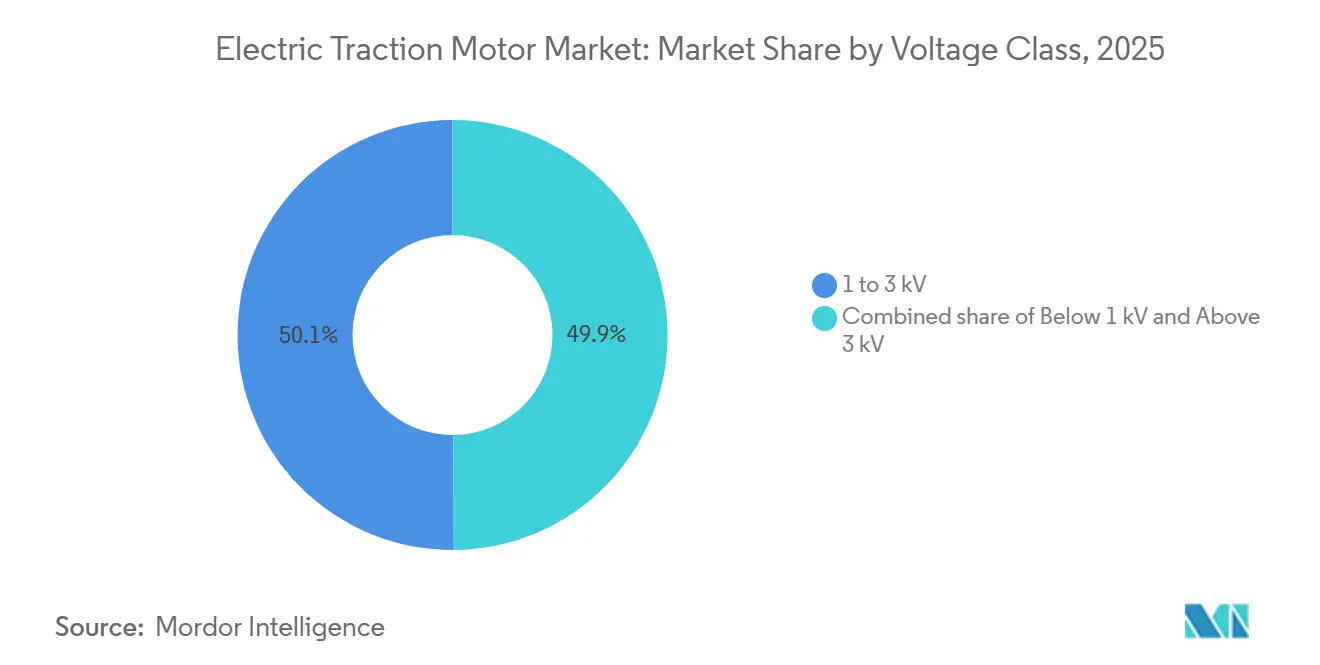

- By voltage class, the 1-kilovolt to 3-kilovolt segment commanded a 50.1% share in 2025; the sub-1-kilovolt class posts the fastest growth at a 10.4% CAGR through 2031.

- By geography, Asia-Pacific led with 49.5% electric traction motor market share in 2025 and is projected to post a 10.0% CAGR, outpacing Europe and North America.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Traction Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in High-Speed Rail Electrification Projects Across Asia | 2.1% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| OEM Shift Toward In-House e-Axle Integration Using 800-V Traction Motors in Premium EVs | 1.8% | Global, led by Europe & North America | Short term (≤ 2 years) |

| Adoption of Silicon Carbide (SiC) Inverters Enabling Higher-Frequency Motors Below 70 kg | 1.5% | Global | Short term (≤ 2 years) |

| Government-Backed Localisation Mandates for Motor Manufacturing in India and EU CBAM | 1.3% | India, European Union | Medium term (2-4 years) |

| Rapid Decline in NdFeB Magnet Prices Post-China Supply Diversification | 1.2% | Global, early gains in North America & Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in High-Speed Rail Electrification Projects Across Asia

Governments in China, India, and Southeast Asia are accelerating high-speed rail corridors to lower aviation emissions and ease highway congestion. China’s CR450 prototype entered trial runs in 2025 at 400 kilometers per hour using permanent-magnet motors that add 22 megawatts of continuous power over the CR400 platform.[1]Railway Gazette International, “CR450 Sets New Benchmark in High-Speed Rail Trials,” railwaygazette.com India’s Mumbai–Ahmedabad corridor is ordering 24 trainsets that carry 305-kilowatt motors per axle for delivery by 2028. Japan’s N700S expansion uses silicon-carbide inverters that trim traction energy by 7% relative to legacy systems. Thailand, Malaysia, and Indonesia have open tenders that reward suppliers able to localize assembly under IEC 60349 rules.

OEM Shift Toward In-House 800-V E-Axle Integration in Premium EVs

Premium automakers are adopting e-axle design to secure thermal control, software optimization, and bill-of-materials savings. BMW’s Gen6 eDrive reduced system mass by 30 kilograms and lifted efficiency to 93% across the duty cycle in models launched during 2024.[2]BMW Group, “Gen6 eDrive Technology Briefing,” bmwgroup.com Volkswagen’s unified e-axle platform, produced at Kassel and Salzgitter, targets a 15% cost cut and pushes over-the-air calibration updates across multiple brands. Stellantis committed EUR 500 million to produce 800-volt motors in France for 1 million units yearly by 2027.

Adoption of Silicon-Carbide Inverters for Sub-70 kg Motors

Silicon-carbide devices switch above 20 kilohertz, letting engineers downsize magnetic cores and copper windings. Wolfspeed’s 1,200-volt MOSFET modules reach inverter efficiencies of 98.5% at up to 175 °C junction temperature.[3]Wolfspeed, “1200 V SiC Power Module Roadmap,” wolfspeed.com Mitsubishi Electric’s full-SiC inverters on the E956 test train delivered a 10% energy cut and a 20% weight drop in 2024. Marelli and Fraunhofer unveiled a 400-volt SiC module housed within four liters, targeting space-constrained A- and B-segment cars.

Government-Backed Localization Mandates in India and EU CBAM

India’s Production Linked Incentive scheme reimburses up to 13% of incremental sales for locally produced traction motors and related parts, driving new green-field capacity.[4]Press Information Bureau of India, “PLI Scheme for Auto Components,” pib.gov.in Tata Motors opened a Sanand plant able to ship 500,000 motors each year by 2027. Europe’s Carbon Border Adjustment Mechanism begins full enforcement in 2026 and raises landed costs of imported motors by up to 12%, prompting Siemens and ABB to add lines in Poland and Romania.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Rare-Earth Recycling Infrastructure Constraining Permanent-Magnet Motor Supply in Europe | -0.9% | Europe, spill-over to North America | Medium term (2-4 years) |

| Thermal Management Challenges Above 400 kW in Compact EV Platforms | -0.7% | Global, acute in premium EV segment | Short term (≤ 2 years) |

| Fragmented Rail Procurement Cycles Causing Lumpy Demand in South America | -0.5% | South America, primarily Brazil & Argentina | Medium term (2-4 years) |

| High Certification Costs under EN 45545-2 Fire Safety for Rail Traction Motors | -0.4% | Europe, extending to export markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Rare-Earth Recycling Infrastructure Constraining Permanent-Magnet Motor Supply in Europe

Recycling plants in Europe process less than 2% of end-of-life motor magnets. Solvay’s pilot facility in France handled only 50 tons in 2024. The Critical Raw Materials Act calls for 15% recycled content by 2030, yet collection and sorting networks remain fragmented. Metrea opened a 1,200-ton plant in Belgium in 2025, but is ramping slowly due to inconsistent feedstock quality.

Thermal Management Challenges Above 400 kW in Compact EV Platforms

Motors above 400 kilowatts generate heat that air or jacket cooling cannot expel inside tight passenger-car engine bays. BorgWarner’s direct-oil system adds an extra pump and exchanger, lifting the cost by USD 150-200 per motor. Laboratory tests show rotor hotspots above 180 °C demagnetize neodymium segments without dysprosium doping. Porsche’s Taycan relies on motor derating to 320 kilowatts for continuous output.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Permanent-Magnet Synchronous Dominance Drives AC Leadership

Alternating-current machines held 65.3% of the electric traction motor market share in 2025 and are advancing at a 12.1% CAGR on the back of permanent-magnet synchronous designs that exceed 96% peak efficiency. Model 3, BYD Seal, and many rail sets rely on these high-density rotors. Induction units still serve industrial hoists and freight locomotives because they shrug off voltage transients and need little maintenance. Switched-reluctance motors attract cost-sensitive buyers by removing magnets, although torque ripple keeps them out of luxury models.

Direct-current machines fill legacy metro cars and niche drones where simple control outweighs efficiency loss. Brushed units in Delhi Metro’s early phases will be swapped for AC drives by 2027. Brushless DC propulsors power eVTOL aircraft such as Joby’s S4, where low weight and smooth thrust are critical. As more operators retrofit aging fleets with variable-frequency drives, the AC segment is slated to widen its lead.

By Power Rating: Sub-200 kW Segment Anchors Volume, Mid-Range Accelerates

Sub-200-kilowatt motors commanded a 55.2% share of the electric traction motor market size in 2025. Passenger cars and light rail favor this range because cost and packaging take priority. Economies of scale stem from annual automotive volumes above 10 million units. The 200-kilowatt to 400-kilowatt bracket is set to rise at a 10.2% CAGR as delivery vans, buses, and medium trucks electrify. Volvo’s FH Electric combines twin 250-kilowatt units to match diesel payloads.

Motors above 400 kilowatts remain a premium niche, under 10% of shipments, yet command high margins under IEC 60349 certification rules. CRRC’s CR400 trainset uses eight 550-kilowatt motors for 350 kilometers per hour service. Demand for continuous high power without derating is steering commercial fleets toward dual-motor layouts rather than single ultra-high-power units.

By Cooling Type: Liquid Systems Gain as Power Density Climbs

Air-cooled units led with 59.6% share in 2025, dominating sub-100 kilowatt classes where forced ventilation suffices. Nissan’s Leaf e+ shows that a 2% efficiency trade-off is acceptable when avoiding coolant plumbing. Liquid cooling is expanding fastest at an 11.3% CAGR. Direct-oil circuits extract heat 40% better than water-glycol jackets and allow densities above 5 kilowatts per kilogram. Dana’s Sumo HP reaches 6.2 kilowatts per kilogram for Class 8 trucks.

Self-ventilated motors hold pockets in industrial conveyors where ambient temperatures stay moderate. Nevertheless, rising continuous-power targets in premium EVs and new high-speed trains are shifting the pendulum toward liquid cooling despite higher bill-of-materials cost.

By Voltage Class: Sub-1 kV Surges on EV Adoption, Rail Anchors Mid-Range

The 1-kilovolt to 3-kilovolt class held 50.1% of the electric traction motor market size in 2025, reflecting entrenched rail standards such as 1.5 kilovolts DC and 3 kilovolts DC; many rail networks also operate at 25 kilovolts AC. Below 1 kilovolt, motors are growing at a 10.4% CAGR as automakers standardize 400-volt and 800-volt packs. Porsche’s 800-volt system cuts charging to 18 minutes and trims copper mass by a quarter. Hyundai’s E-GMP suits 160- to 430-kilowatt units across multiple models.

Ratings above 3 kilovolts live mainly in high-speed rail and freight locomotives. Alstom’s Avelia Horizon for Amtrak runs sixteen 1.6-megawatt motors optimized for 25 kilovolt grids. Automotive economies of scale continue to push sub-1 kilovolt architectures toward higher voltage within that bracket, aiming to cut resistive losses without breaking current safety norms.

By Application: Railway Dominates Revenue, EVs Lead Growth

Railway accounted for 45.4% of the electric traction motor market share in 2025, thanks to multi-decade contracts and high unit values. One high-speed trainset can need up to 48 motors. Electric vehicles, in contrast, are the volume engine, expanding at 15.8% CAGR as battery prices fall and carbon limits tighten. China sold 9.5 million passenger EVs in 2024, up 35% year on year.

Industrial machinery, including cranes and mining trucks, records steadier but lower growth. Konecranes fits four 75-kilowatt motors in each automated guided vehicle to raise uptime in ports. Emerging uses such as drones and eVTOL aircraft remain small yet draw venture capital.

Geography Analysis

Asia-Pacific led the electric traction motor market with 49.5% share in 2025 and is on track for a 10.0% CAGR. China’s CR450 testing employed permanent-magnet motors rated at 550 kilowatts per axle and moved into revenue trials on the Beijing–Shanghai line in late 2025. India reserved USD 3.5 billion for advanced components under its PLI plan, unlocking large domestic capacity additions. Japan’s rail operators are retrofitting silicon-carbide inverters to cut energy by up to 10%. ASEAN metro tenders now specify local assembly clauses, opening room for joint ventures.

Europe keeps the second-largest share. The Carbon Border Adjustment Mechanism, which starts full enforcement in 2026, adds 8-12% cost on motors shipped from outside the bloc. Volkswagen ramped in-house capacity to 1.2 million motors per year by the end of 2025. Germany, France, and Italy are converting diesel loco fleets to battery-electric for branch lines, giving traction to modular retrofit kits.

North America is adding plants in Mexico and the southern United States. GM’s joint venture with LG is targeting 1 million motors a year by 2027. Tesla’s Texas factory shipped 1.8 million units in 2024. Freight rail trials use four 500-kilowatt motors in Wabtec’s FLXdrive locomotive. South American demand remains cyclical, and the Middle East and Africa still account for modest volume, with Saudi Arabia’s Riyadh Metro providing the main near-term lift.

Competitive Landscape

The top five suppliers, ABB, Siemens, CRRC, Nidec, and Bosch, held about 45% of revenue in 2025, so the market shows moderate concentration. Siemens and ABB dominate rail by bundling long service contracts and proprietary control software. Automotive traction is fragmenting as Volkswagen, BMW, and Stellantis internalize e-axles, squeezing Tier-1 margins. CRRC’s fully integrated chain from rare-earth mining to final assembly produces motors at up to 25% lower cost, yet export ambitions face Buy America clauses in the United States rail projects.

White-space growth lies in motors above 500 kilowatts for freight, rare-earth-free topologies for budget passenger cars, and direct-drive solutions that skip gearboxes in industrial equipment. Nidec’s 2024 purchase of Embraco’s motor assets broadens its reach in adjacent electrification segments. Valeo joined Siemens in 2025 to build 800-volt e-axles for trucks, pooling thermal and control know-how. Patent filings for switched-reluctance control and silicon-carbide thermal management jumped 35% in 2024, underscoring a technology race that will reshape rankings in the next model cycle.

Electric Traction Motor Industry Leaders

Siemens AG

CRRC Corporation Limited

ABB Ltd

Nidec Corporation

Toshiba Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Siemens Mobility secured an order for 50 Vectron Dual Mode locomotives from Akiem, with an option for 40 more, spotlighting greener rail traction capable of 2.4 MW electric operation.

- June 2024: CRRC Corporation Limited, a prominent Chinese manufacturer specializing in railway components and locomotives, introduced a high-speed train comprising four cars. The train boasts a top speed of 160 km/h while maintaining a steady operational speed of 120 km/h. Notably, it is outfitted with permanent magnet traction motors, enabling it to conquer gradients as steep as 50%.

- March 2024: ABB Ltd, a Swiss manufacturing company, made a deal worth USD 150 million with the Hyundai Rotem Company to supply the traction packages, including traction motors for 65 trains being manufactured for Queensland, Australia.

- February 2024: Kolkata's Eastern Railway (ER) rolled out the traction motor dropping detection system in 14 locomotives, bringing the total implementation to 78 locomotives. The system enables automatic brake application in instances of loosely fastened traction motors, significantly bolstering train safety.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electric traction motor market as all factory-built rotating machines that directly propel rail vehicles, on-road electric vehicles, and select industrial transports by converting electrical energy into tractive mechanical torque. The assessment tracks motors sold to OEMs and the aftermarket across AC, DC, and permanent-magnet topologies in power classes below 200 kW, 200-400 kW, and above 400 kW.

Scope exclusion: motors used only for fixed-speed industrial drives or regenerative generators are outside the boundary.

Segmentation Overview

- By Type

- Alternating Current (Induction, Permanent-Magnet Synchronous, Switched Reluctance)

- Direct Current (Brushed, Brushless DC)

- By Power Rating

- Below 200 kW

- 200 to 400 kW

- Above 400 kW

- By Cooling Type

- Air-Cooled

- Liquid-Cooled

- Self-Ventilated

- By Voltage Class

- Below 1 kV

- 1 to 3 kV

- Above 3 kV

- By Application

- Railway

- Electric Vehicles

- Industrial Machinery

- Other Applications (Drones, eVTOL)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

To refine assumptions, we interviewed rolling-stock integrators in Europe, EV driveline engineers in China, and North American transit buyers, probing real-world duty cycles, warranty return rates, and forecast platform volumes. These discussions helped us stress-test utilization factors and regional ASP deltas before locking the model.

Desk Research

We began with publicly available time-series such as the International Union of Railways fleet electrification statistics, Eurostat traction equipment trade codes, and the International Energy Agency's EV stock outlook, which anchor install-base and replacement pools. Annual reports and Form 10-Ks of leading motor suppliers provide shipment splits by application and voltage class, while transport ministry tender databases reveal regional pricing corridors. Our analysts also extracted shipment-weighted average selling prices from customs filings available through D&B Hoovers and import-export trackers such as Volza to ground the global ASP curve.

Complementary insights were drawn from peer-reviewed journals on SiC inverter efficiency gains and patents logged on Questel that signal future design shifts. The sources listed illustrate our desk research spine; numerous additional datapoints were consulted for verification and context.

Market-Sizing & Forecasting

A top-down construct converts rail vehicle kilometers, EV production, and industrial shuttle output into installed motor counts that are then multiplied by region-specific ASPs. Selective bottom-up checks, supplier revenue roll-ups, and channel stock audits align the totals. Key variables include high-speed rail route additions, BEV penetration, rare-earth oxide spot prices, average motor power rating drift, and cooling-system mix shifts. Multivariate regression with scenario analysis projects each driver to 2030, and gaps in bottom-up evidence are bridged using conservative midpoint estimates vetted with experts.

Data Validation & Update Cycle

Mordor analysts subject every draft to variance checks against independent price indices and production trackers, escalating anomalies for peer review before sign-off. Models refresh annually, with interim updates triggered by material events such as subsidy revisions. A final pre-publication sweep ensures clients receive the most current view.

Why Mordor's Electric Traction Motor Baseline Earns Maximum Trust

Published figures often diverge because providers select different application mixes, currency bases, and refresh cadences. By adhering to a full-chain scope and verifying both volume and price levers, Mordor delivers a balanced reference point that decision-makers can confidently cite.

The comparison shows that scope breadth, price realism, and annual refresh discipline drive the spread in numbers. By capturing all end-uses and corroborating with field intel, Mordor Intelligence supplies a dependable, transparent baseline that withstands scrutiny.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.87 B (2025) | Mordor Intelligence | - |

| USD 12.57 B (2024) | Global Consultancy A | Focuses solely on BEV motors; omits rail and industrial segments |

| USD 18.25 B (2024) | Industry Association B | Applies aggressive PHEV uptake and limited rare-earth cost escalation |

| USD 15.36 B (2024) | Trade Journal C | Relies on uniform global ASP without primary validation |

The comparison shows that scope breadth, price realism, and annual refresh discipline drive the spread in numbers. By capturing all end-uses and corroborating with field intel, Mordor Intelligence supplies a dependable, transparent baseline that withstands scrutiny.

Key Questions Answered in the Report

What is the projected size of the electric traction motor market by 2031?

The market is forecast to reach USD 26.33 billion by 2031.

Which segment is growing fastest within traction motors?

Electric-vehicle applications post the highest growth at a 15.8% CAGR through 2031.

Why are OEMs bringing traction-motor production in-house?

Automakers want tighter control of thermal performance, software updates, and cost, which improves margins and reduces supply risk.

How does the Carbon Border Adjustment Mechanism affect suppliers?

CBAM raises the imported motor cost into Europe by 8-12%, encouraging local production to avoid tariffs.

Which cooling method is gaining share in high-power motors?

Liquid cooling, especially direct-oil systems, is expanding at 11.3% CAGR because it handles higher heat loads efficiently.

Page last updated on: