Poultry Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 9.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

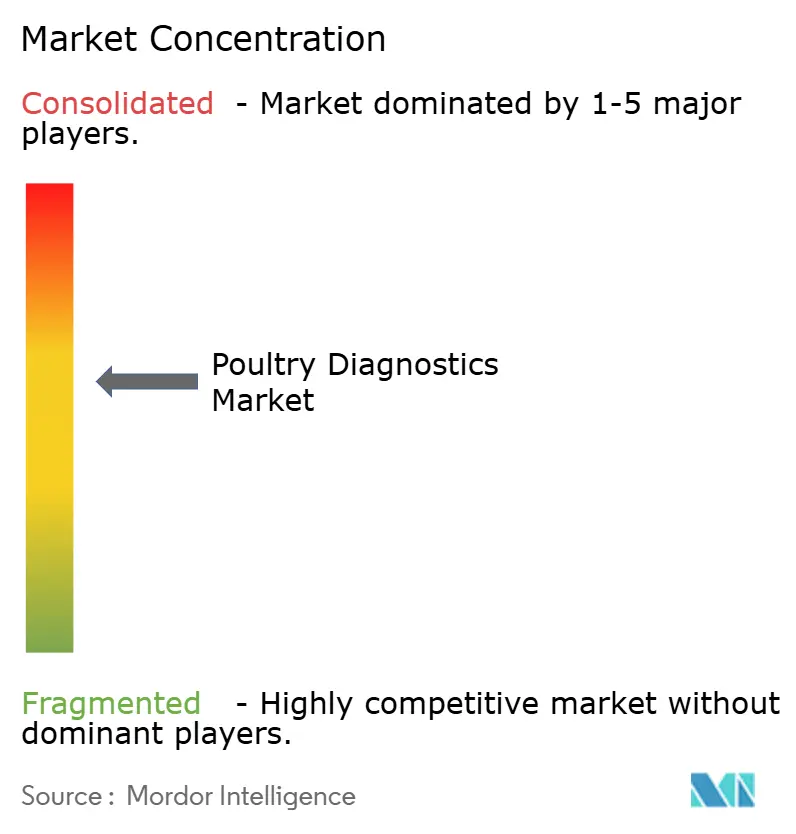

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poultry Diagnostics Market Analysis by Mordor Intelligence

Poultry diagnostics market size in 2026 is estimated at USD 1.02 billion, growing from 2025 value of USD 930 million with 2031 projections showing USD 1.62 billion, growing at 9.74% CAGR over 2026-2031. The growth reflects widespread adoption of sophisticated flock-health programs, the shift toward molecular confirmation of emerging pathogens, and tighter surveillance requirements that link export access to documented testing. Government vaccination and monitoring schemes following recent highly pathogenic avian influenza episodes reinforce steady demand for routine screening, while artificial-intelligence tools that analyze hatchery data in real time are moving diagnostics from a reactive function to a preventive pillar. Integrated producers are standardizing testing protocols across multi-site operations to protect high-value genetics, and reference laboratories are scaling automation to mitigate persistent shortages of trained technologists. In parallel, point-of-care devices are gaining traction on farms that cannot wait for off-site results, giving the poultry diagnostics market additional momentum in low-infrastructure regions.

Key Report Takeaways

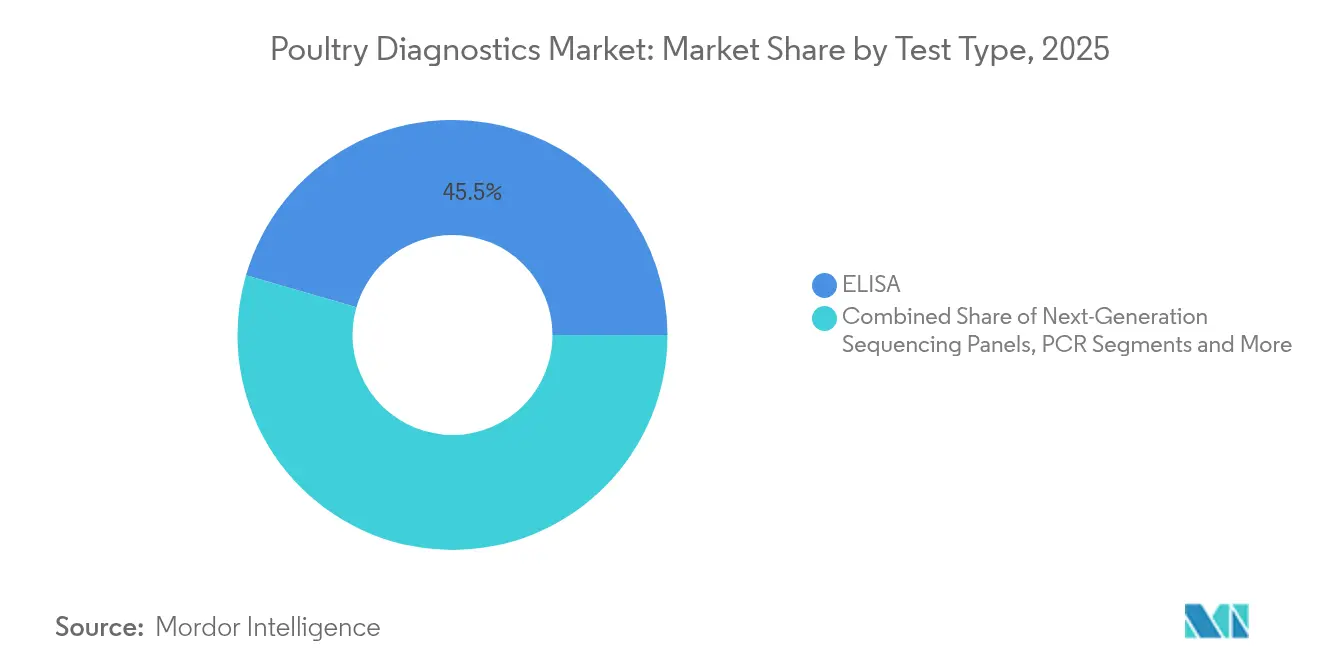

- By test type, ELISA led with 45.52% revenue share in 2025, while PCR is projected to post the fastest 10.12% CAGR through 2031.

- By disease type, infectious diseases accounted for 37.78% of the poultry diagnostics market share in 2025; parasitic diseases are on track for a 10.55% CAGR to 2031.

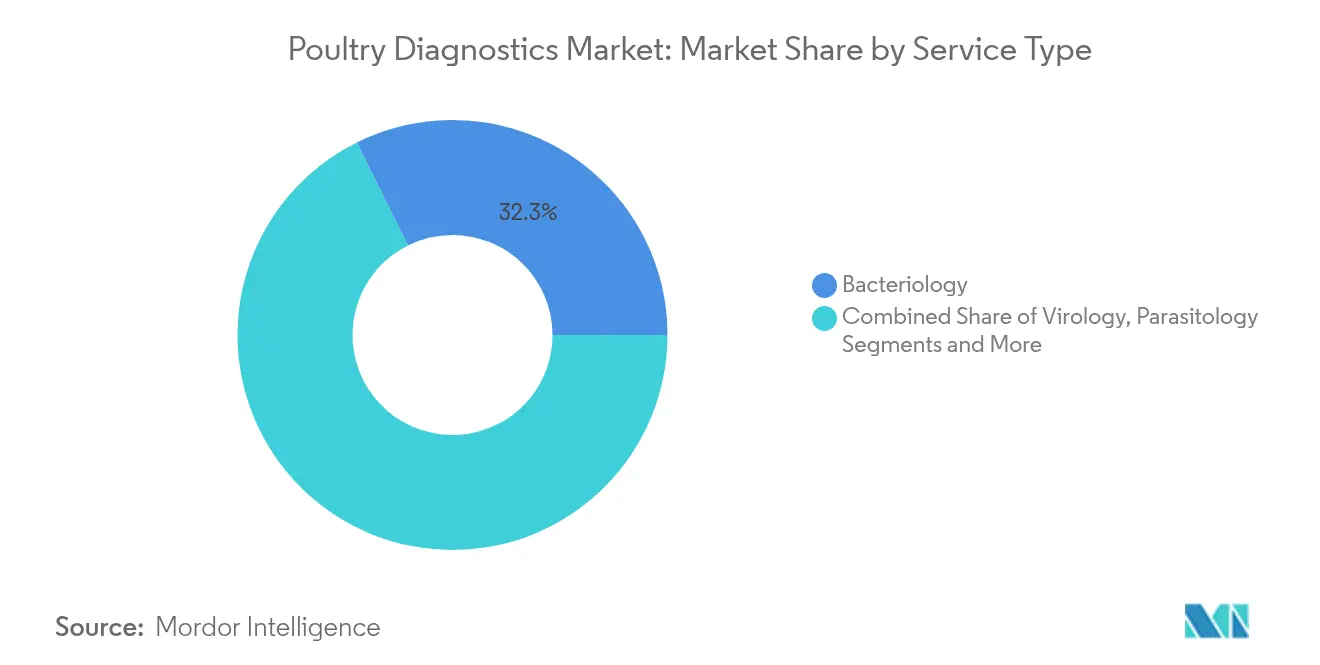

- By service type, bacteriology held 32.34% of the poultry diagnostics market size in 2025, whereas virology is set to expand at 10.71% CAGR.

- By end user, veterinary reference laboratories captured 42.68% share in 2025; on-farm point-of-care units record the highest 11.02% CAGR outlook.

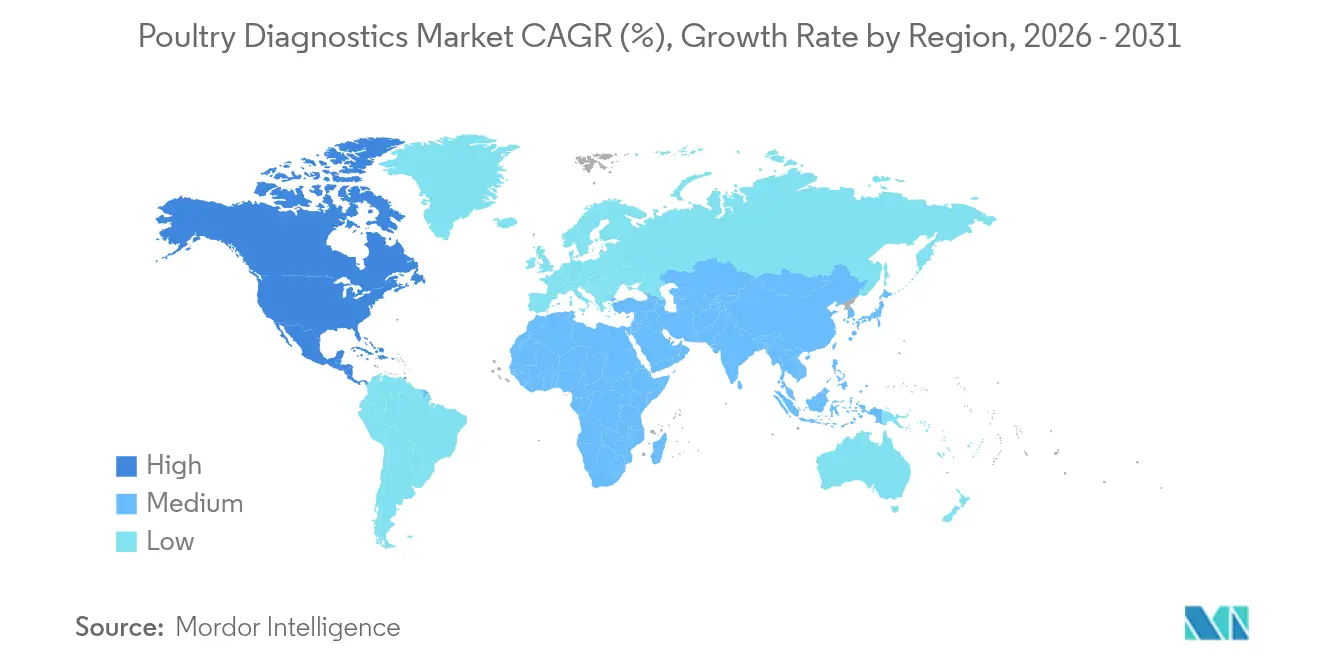

- By geography, North America dominated with 41.73% revenue share in 2025, but Asia-Pacific is the fastest-rising region at 11.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Poultry Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Government & NGO Surveillance Programs | +2.1% | Global, with early gains in APAC, North America | Medium term (2-4 years) |

| Escalating Avian-Influenza & Zoonotic Outbreaks | +2.8% | Global, concentrated in Asia-Pacific, North America | Short term (≤ 2 years) |

| Surging Demand For Poultry Protein In Emerging Economies | +1.9% | Asia-Pacific core, spill-over to MEA, Latin America | Long term (≥ 4 years) |

| Rapid Adoption Of ELISA, PCR And Other Molecular Assays | +1.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expansion Of Large Integrated Poultry Operations | +1.2% | Global, with concentration in Southeast Asia, Brazil | Long term (≥ 4 years) |

| AI-Driven Predictive Analytics For Hatchery Health | +0.8% | North America, EU, select APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Government & NGO Surveillance Programs

Regulatory bodies treat veterinarians and diagnostic labs as the first barrier against zoonotic spill-over, which has elevated routine testing volumes across commercial flocks. The United States Department of Agriculture enforces the National Poultry Improvement Plan, linking program compliance to interstate movement privileges, while its avian-influenza monitoring protocols can suspend flock accreditation for non-conformance [1]United States Department of Agriculture, “National Poultry Improvement Plan,” usda.gov. Similar frameworks in the European Union mandate accredited testing before export certification. These policies turn diagnostics from a discretionary cost into an operational necessity. International funding from the World Organisation for Animal Health supports laboratory upgrades in Southeast Asia, further expanding the testing footprint. Together, these initiatives exert structural upward pressure on the poultry diagnostics market.

Escalating Avian-Influenza & Zoonotic Outbreaks

Highly pathogenic avian influenza continues to circulate in wild migratory birds, triggering recurrent culls in commercial operations and creating surges in sample submissions. The Centers for Disease Control and Prevention documented viral fragments in three veterinarians after routine farm visits, illustrating cross-species risk and reinforcing the need for high-sensitivity molecular assays [2]Centers for Disease Control and Prevention, “Update on Highly Pathogenic Avian Influenza in Humans,” cdc.gov. Vaccine field trials run by the USDA demonstrated near-complete protection but highlighted the parallel need for diagnostics that can differentiate infected from vaccinated animals, sustaining long-term testing demand. Real-time PCR panels capable of sub-typing H5, H7 and H9 strains within 60 minutes are now standard in reference labs, and automated workflows ensure capacity during outbreak spikes. These dynamics intensify reliance on rapid, accurate diagnostics across every production tier.

Surging Demand For Poultry Protein In Emerging Economies

Economic growth and urban diets in South and Southeast Asia are projected to lift regional broiler output by 4–5% annually until 2030, expanding the addressable flock base for diagnostics. India’s compartmentalized health-certification scheme, recently endorsed as HPAI-free by the World Organisation for Animal Health, illustrates how robust surveillance earns market access for exports. Rising disposable income also boosts domestic consumption, prompting integrators to safeguard supply security through regimented monitoring. Governments in Indonesia and the Philippines provide matching grants for laboratory construction, combining public health goals with agri-export ambitions. As herd sizes swell, each incremental bird added to commercial inventories directly multiplies the test volume required, supporting the long-run expansion of the poultry diagnostics market.

Rapid Adoption Of ELISA, PCR And Other Molecular Assays

Labs facing shortages of qualified technologists are turning to high-throughput immunoassay and PCR platforms that automate most steps, cutting manual pipetting and interpretation errors. IDEXX’s Catalyst series provides quantitative readouts for multiple parameters in under 10 minutes and now processes avian samples through a validated menu expansion. Zoetis opened a 32,000-square-foot reference lab in Louisville with robotics that move samples from accessioning to result without human touch points. These investments allow facilities to sustain double-digit volume growth while labor markets remain constrained. As automated systems become the new baseline, throughput gains translate into broader access for smaller farms, accelerating the mainstreaming of molecular testing in the poultry diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Molecular Tests & Consumables | -1.4% | Global, acute in LMICs and rural areas | Short term (≤ 2 years) |

| Limited Skilled Lab Workforce In Low-Income Regions | -0.9% | APAC emerging markets, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Compliance Burden From Evolving Bio-Security Protocols | -0.7% | Global, concentrated in major export markets | Medium term (2-4 years) |

| Reagent Supply Disruptions During Trade Bans | -0.5% | Global, with regional concentration during crises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost Of Molecular Tests & Consumables

Consumables for multiplex PCR panels remain priced beyond reach for many smallholders, particularly in regions where farm-gate margins run thin. Shipping buffers and cold-chain requirements add logistical mark-ups that can raise landed costs by 25% in remote locations. Public laboratories subsidize fees, but budget cycles and competing human-health priorities limit scope. Manufacturers are responding with lyophilized reagents stable at ambient temperatures and cartridge systems that integrate extraction, amplification and detection. While innovations promise gradual cost relief, near-term affordability continues to restrain full penetration of the poultry diagnostics market.

Limited Skilled Lab Workforce In Low-Income Regions

Veterinary diagnosticians and laboratory technicians remain scarce in several emerging economies. The American Veterinary Medical Association projects a deficit of 15,000 professionals in North America by 2030, a gap echoed on a smaller scale across Africa and South Asia [3]American Veterinary Medical Association, “Workforce Report 2025,” avma.org . Limited staff prolongs turnaround times, discouraging farmers who need rapid responses. Remote microscopy powered by cloud-based artificial intelligence partially alleviates the shortage, yet connectivity constraints hamper field adoption. Multilateral capacity-building programs provide training, but migration to higher-paying sectors erodes retention. Unless workforce supply improves, sustained talent gaps will temper growth potential for the poultry diagnostics market in underserved geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Technologies Drive Innovation

ELISA generated 45.52% of global revenue in 2025, reflecting its role as the backbone of surveillance and vaccination monitoring. These assays combine low cost with reliable throughput, which keeps them entrenched even as new modalities emerge. The poultry diagnostics market size for ELISA-based offerings stood at USD 464.7 million in 2026 and is forecast to edge past USD 714.2 million by 2031. PCR platforms, while starting from a lower baseline, are projected to record 10.12% CAGR, driven by regulatory mandates for molecular confirmation during H5 or H7 outbreaks. Manufacturers bundle validated reagents with automated thermocyclers, reducing hands-on time and contamination risk. Next-generation sequencing panels sit at the cutting edge, capable of characterizing entire viromes in a single workflow, yet remain confined to reference laboratories until costs fall further.

The lateral-flow segment addresses on-farm triage needs with cartridges that deliver qualitative answers within 15 minutes. Demand rises where immediate culling decisions can avert severe financial losses, especially in integrated operations that house millions of birds. Hemagglutination-inhibition tests, still required by several export authorities, continue to secure a niche share. Vendors now develop digital-image capture solutions that interpret titer patterns objectively, improving consistency. Together, these dynamics ensure that the poultry diagnostics market offers a wide technology continuum, allowing users to balance price, speed and sensitivity.

By Disease Type: Infectious Pathogens Retain Primacy

Infectious agents commanded 37.78% revenue share in 2025 and remain the economic focal point for producers wary of trade bans and mass depopulation orders. Sample submissions spike each winter when migratory birds intersect commercial flocks in the northern hemisphere, underscoring the seasonal volatility embedded in the poultry diagnostics market. The sector responds with multiplex PCR panels detecting avian influenza, Newcastle disease and infectious bronchitis in a single run, improving cost efficiency. Researchers also refine DIVA (Differentiation of Infected from Vaccinated Animals) assays to support widespread immunization strategies without compromising surveillance.

Parasitic diseases, led by coccidiosis, exhibit the fastest 10.55% CAGR, expanding the poultry diagnostics market size for this niche from USD 154.8 million in 2026 to an expected USD 255.3 million by 2031. Automated oocyst-counting instruments reduce subjectivity and staff fatigue, boosting test reliability. Concurrent interest in metabolic and nutritional disorders signals a broader trend toward precision husbandry, where wearable sensors track body temperature and activity to pre-empt welfare issues. Although these categories remain smaller today, their growth rate suggests a gradual diversification of diagnostic demand away from an exclusive pathogen focus.

By Service Type: Virology Accelerates Within Lab Menus

Bacteriology retained the top slot with 32.34% contribution in 2025 owing to food-safety driven Salmonella monitoring mandates. National programs in the United States and the European Union compel processors to demonstrate ongoing compliance, ensuring a dependable baseline for culture and serotyping services. Despite that stability, the most dynamic expansion happens in virology, which is projected to rise at 10.71% CAGR through 2031. Next-generation sequencing now supports routine viral genotyping, giving veterinarians insights into antigen drift that could erode vaccine efficacy. Reference laboratories leverage high-throughput robotics to meet soaring demand during outbreak peaks, integrating bioinformatic pipelines that deliver full reports within 48 hours.

Parasitology leverages image-analysis hardware capable of distinguishing oocyst morphology across Eimeria species, cutting analysis times from hours to minutes. Immunology and serology hold steady roles in monitoring post-vaccination antibody titers, and necropsy plus histopathology remain indispensable for complex mortality events where gross lesions guide further testing. The multi-discipline nature of laboratory menus underscores why the poultry diagnostics market rewards providers that can bundle diverse services under one roof.

By End User: Point-of-Care Adoption Rises From Lower Base

Veterinary reference laboratories captured 42.68% revenue share in 2025 by offering centralized expertise and bulk pricing. IDEXX alone processes millions of avian samples annually through an international network that operates 24-hour shifts during epidemic alerts. Consolidation trends accelerate as regional labs sell to global chains seeking geographic reach. Nevertheless, on-farm testing units deliver the highest 11.02% CAGR, reflecting producers’ need for immediate action on high-density sites. Cartridge-based hematology and molecular readers now plug into mobile apps that archive data for audit compliance, narrowing the performance gap with centralized facilities.

Academic institutions and public research centers continue to pilot emerging technologies, such as CRISPR-based detection that could bypass thermocycling. While their direct share of the poultry diagnostics market remains modest, they play an outsized role in validating methodologies later adopted by the commercial sector. Collectively, the spread of competencies across end-user groups ensures resilience in diagnostic capacity and drives continuous innovation.

Geography Analysis

North America remained the largest revenue block with 41.73% share in 2025, an outcome of stringent food-safety legislation, advanced cold-chain infrastructure and widespread insurance schemes that reimburse disease-control expenses. The region invests heavily in biocontainment upgrades and supports a network of more than 60 accredited veterinary diagnostic labs that handle avian submissions, underpinning the mature demand profile. Even so, the United States faces a projected gap of qualified diagnosticians by 2030, which has prompted subsidies for automation upgrades, shaping the medium-term outlook for the poultry diagnostics market.

Asia-Pacific is the fastest-growing territory at 11.42% CAGR to 2031, underpinned by population growth, urbanization and policy drives to boost domestic protein self-sufficiency. China, India and Indonesia collectively plan multi-billion-dollar investments in slaughter and cold-storage capacity, and each mandates routine disease monitoring for export certification. Public-private partnerships fund regional laboratory networks that offer reduced-fee PCR screening, embedding diagnostics in standard production economics. As a result, the poultry diagnostics market size in Asia-Pacific is expected to surpass USD 459.3 million by 2031, up from USD 267.4 million in 2026.

Europe preserves steady demand through harmonized veterinary legislation and mutual-recognition protocols handled by the Veterinary Batch Release Network, ensuring cross-border movement of poultry without redundant testing. Latin America and the Middle East & Africa register double-digit growth on small absolute bases, supported by multinational integrators establishing vertically aligned complexes that include on-site laboratories. While infrastructure deficits remain in parts of Sub-Saharan Africa, multilateral donors channel grants for mobile labs that can travel between farms, setting foundations for future expansion of the poultry diagnostics market.

Regulatory Landscape

Official poultry diagnostics demand is anchored to notifiable-disease control and trade certification frameworks that specify where and how tests must be run. In the United States, the National Poultry Improvement Plan (NPIP) program standards define approved assays, sanitation procedures, and requirements for authorized laboratories, and USDA APHIS oversight also applies to diagnostic products intended to detect antigens, antibodies, or nucleic acid sequences for infectious agents (including PCR and genetic sequencing). Internationally, the World Organisation for Animal Health (WOAH) Terrestrial Manual provides the baseline for recognized laboratory diagnostic test standards used by competent authorities in import-export certification.

Recent tightening around biosecurity and audited compliance reinforces the role of accredited labs and validated methods. NPIP initiated its 2026 Authorized Lab Service Review process to confirm laboratories are performing official Plan assays in line with current program standards, including the June 2025 standards update. In other regulated markets, device-registration pathways also shape market entry. For example, South Africa's SAHPRA requires veterinary medical devices to be registered and, for higher-risk classes, recognizes pre-market approval evidence from established jurisdictions (including the United States and Europe), which affects the documentation expectations for diagnostic manufacturers serving export-oriented poultry systems.

Value Chain Analysis

The poultry diagnostics value chain runs from assay design and regulated manufacturing (ELISA and PCR kits, primers/probes, controls, sample-collection consumables, and instruments) through distribution and cold-chain logistics, into testing execution by veterinary reference laboratories, integrated poultry company labs, and public or university laboratories. Surveillance and reporting requirements connect farms, veterinarians, hatcheries, live-bird transport, and processors to laboratory networks, with programs such as the US NPIP and international WOAH-aligned standards guiding which tests support certification for movement and trade.

Downstream, results increasingly feed flock-health decisioning and compliance documentation, which elevates data handling and integration as a core service layer alongside the wet-lab workflow. Institutional examples such as the University of Guelph Animal Health Laboratory interactive poultry disease dashboards show how laboratory outputs can be translated into monitoring tools, and 2026 research on multimodal sensing and data-fusion highlights the shift toward combining molecular confirmation with continuous, farm-generated signals. Bottlenecks persist around skilled labor availability and turnaround-time expectations, which supports adoption of automation in reference laboratories and on-farm point-of-care testing where immediate containment decisions are economically critical.

Competitive Landscape

The poultry diagnostics market shows moderate concentration. The combined revenue of the top five suppliers sits just above 60%, giving mid-tier entrants room to specialize. IDEXX Laboratories leads global share and posted 6.56% year-over-year revenue growth in 2024 on the back of expanded molecular menus. Zoetis follows through strategic acquisitions that knitted Ethos Diagnostic Science, Phoenix Lab and ZNLabs into a unified reference-lab network covering cytology, chemistry and microbiology. Thermo Fisher Scientific leverages its qPCR franchise to supply reagents to national labs during outbreak surges.

Technology is the decisive battleground. IDEXX will launch a lymphoma-screening panel for canines in 2025, but its underlying flow-cytometry platform has avian applications that could cross-pollinate market segments. Zoetis deploys artificial-intelligence algorithms within its Vetscan Imagyst ecosystem to read fecal smears automatically, cutting analysis times for coccidiosis from 20 minutes to under 4 minutes. Emerging firms focus on portable PCR devices that work without refrigeration, targeting low-resource countries. While patents and regulatory approvals form barriers to entry, customer stickiness also arises from data-integration services that feed laboratory results directly into farm management software.

Regional manufacturers navigate local content policies by partnering with state agribusiness corporations to assemble diagnostic kits domestically. This strategy limits exposure to import tariffs and secures public-tender eligibility. Conversely, global incumbents safeguard brand equity through third-party proficiency testing that certifies assay reproducibility, a prerequisite for premium pricing. Overall, the competitive landscape remains dynamic, with innovation velocity and acquisition moves driving shifts in share allocations within the poultry diagnostics market.

Poultry Diagnostics Industry Leaders

Idexx Laboratories, Inc.

Zoetis, Inc.

Thermo Fisher Scientific

Biochek

Megacor Diagnostik GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is opening around earlier warning and compliance-ready surveillance stacks that combine official confirmation testing with continuous monitoring and improved data interoperability. Policy-linked biosecurity rigor provides a practical entry point for vendors to embed diagnostics into audited workflows, including NPIP-related requirements that tie biosecurity plan maintenance and auditing to indemnity conditions for avian influenza. At the same time, field programs and lab networks operating under WOAH-aligned standards continue to emphasize validated, high-sensitivity assays for notifiable diseases, supporting opportunities for platforms that reduce hands-on time, stabilize reagents for constrained cold chains, or simplify sample-to-answer workflows for integrators operating across multiple sites.

Technology pull is also visible in funded and published work that moves diagnostics beyond episodic swabbing toward fused sensing and analytics. In June 2026, UC Riverside reported a USD 1.8 million USDA APHIS grant to develop an AI-proteomics HPAI surveillance tool for poultry farms, reflecting public investment in next-generation detection approaches that can complement laboratory PCR and ELISA confirmation. Parallel 2026 research activity around privacy-preserving federated learning for poultry disease classification and multimodal sensing platforms points to demand for solutions that address data ownership barriers while enabling cross-farm learning, which diagnostic providers can package as integrated software, decision support, and reporting layers tied to their assays and service menus.

Recent Industry Developments

- July 2026: Zoetis announced a definitive agreement to acquire VitalRADS, a veterinary teleradiology platform, with closing targeted for the third quarter of 2026. The move expands Zoetis digital diagnostic workflow capabilities and supports broader integration of diagnostics and decision support across animal health service networks.

- March 2026: Zoetis announced a definitive agreement to acquire Neogen Corporation's animal genomics business for USD 160 million. Adding genomics capabilities strengthens precision animal health offerings that can complement infectious-disease testing and flock management programs used by integrated poultry producers.

- March 2024: Harch Tech Group acquired NYtor to enhance PCR-based screening aimed at improving male-chick survivability. The acquisition underscores continued interest in molecular tools that move beyond outbreak response into production efficiency and early-life flock performance applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the poultry diagnostics market covers the value of tests and related lab services used to detect, confirm, and monitor diseases in commercial poultry flocks. This includes routine screening and outbreak investigation work for producers and through veterinary channels.

Scope exclusions: We exclude diagnostics for companion birds, broad wildlife surveillance programs, and general livestock diagnostics that are not poultry-specific.

Segmentation Overview

- By Test Type

- ELISA

- PCR

- Lateral-Flow Immunoassays

- Hemagglutination-Inhibition & AGID

- Next-Generation Sequencing Panels

- Other Diagnostic Tests

- By Disease Type

- Metabolic & Nutritional Disorders

- Infectious Diseases

- Parasitic Diseases (Coccidiosis, Helminths)

- Other Disease Types

- By Service Type

- Bacteriology

- Virology

- Parasitology

- Serology & Immunology

- Necropsy & Histopathology

- By End User

- Poultry Farms & Integrators

- Veterinary Reference Laboratories

- Point-of-Care / On-Farm Testing Units

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and the disease and trade context before building the market model. We referenced public sources such as the World Organisation for Animal Health (WOAH) for notifiable disease reporting, FAOSTAT for poultry production indicators, and USDA and Eurostat for agriculture and trade series that help explain testing intensity by region.

We also reviewed sources such as national animal health agencies, veterinary laboratory and poultry association publications, and peer-reviewed journals on avian influenza, Newcastle disease, and Salmonella monitoring to understand typical testing pathways. For market structure and company mapping, we used company filings, investor presentations, and reputable press coverage, supported by paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data where it helped validate reagent and kit flows. This list is illustrative only, and many other public sources were consulted for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary discussions were completed with diagnostic laboratory leaders, poultry veterinarians, integrator and hatchery health teams, and distribution side participants who see ordering patterns for kits and reagents. Respondent input was used to confirm which tests are routinely run by disease and by bird type, how often retesting happens, and how pricing varies by region and service mix. Assumptions were then rechecked across APAC, EMEA, and the Americas to avoid single-market bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 16% | Managers: 50% | Americas: 27% |

Market-Sizing & Forecasting

Sizing started with a top-down build where poultry population, commercial production volumes, and notifiable disease incidence were translated into an addressable testing pool, then adjusted using typical testing frequency by disease programs. To keep the math realistic, we treated ELISA and PCR volumes differently because they show up in different stages of screening and confirmation. We also separated routine surveillance from event-driven spikes.

The model uses inputs such as poultry meat and egg production trends, outbreaks and control measures for avian influenza and Newcastle disease, lab capacity expansion signals, the shift toward faster kits for on-farm decisions, and average price ranges for test panels and lab services. Forecasts were run using scenario analysis around outbreak intensity and export-driven surveillance requirements, followed by a smoothing step so one-off shocks do not distort the full period. Results were then corroborated using selective bottom-up checks, such as sampled ASP times test volumes for key regions, channel checks on kit consumption patterns, and distributor level mix assumptions. Where a country series was incomplete, gaps were handled through conservative interpolation.

Data Validation & Update Cycle

Outputs were checked against independent signals such as disease notification trends, poultry production growth, and lab network expansion to make sure the market trajectory stays consistent with real-world demand drivers. When large variances appeared across regions or test types, assumptions were revisited, and follow-up calls were triggered to revalidate pricing, test frequency, and the share of services versus kits.

Before sign-off, the full model goes through a multi-step analyst review so arithmetic errors, inconsistent unit conversions, and unrealistic growth jumps are removed. The report is refreshed annually, and interim updates are made when material events occur, such as major outbreaks or changes in surveillance rules. A final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Poultry Diagnostics Market Size Measured Against Other Published Estimates

Published market sizes for poultry diagnostics often do not match because the scope and counting logic vary more than it looks at first glance. Differences usually come from whether services are counted alongside kits and instruments, how on-farm rapid testing is treated, which bird types are included, and how outbreak years are normalized in the forecast.

Another common driver is the base year and pricing approach, since some estimates keep pricing flat while others build aggressive ASP increases for molecular tests, followed by different currency timing for converting regional values into USD. The spread also widens when an estimate relies mainly on high-level animal health totals without rechecking the implied test volumes and lab throughput, followed by limited refresh when surveillance rules change in key export markets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.02 B (2026) | |

| Global Research Publisher A | USD 0.83 B (2024) | Uses an earlier base year and a revenue build that leans more on product sales, with services and confirmation testing intensity captured more lightly, which can understate value in regions where reference labs do most of the work. |

| Global Research Publisher B | USD 1.05 B (2025) | Applies a higher growth runway and a broader price escalation assumption for advanced assays, and it can also reflect wider inclusion of adjacent poultry health spending beyond core diagnostics. |

The table shows that the main spread comes from year alignment and what gets counted as diagnostic revenue, especially lab services and follow-on confirmation tests after screening. By linking the demand pool to poultry production and outbreak-linked testing cycles, then only counting diagnostic revenue when it is tied to poultry-specific test workflows, the estimate stays traceable to practical variables, a choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current Poultry Diagnostics Market size?

The poultry diagnostics market is valued at USD 1.02 billion in 2026 and is projected to reach USD 1.62 billion by 2031.

Who are the key players in Poultry Diagnostics Market?

Idexx Laboratories, Inc., Zoetis, Inc., Thermo Fisher Scientific, Biochek and Megacor Diagnostik GmbH are the major companies operating in the Poultry Diagnostics Market.

Which is the fastest growing region in Poultry Diagnostics Market?

Asia-Pacific leads growth with an expected 11.42% CAGR through 2031, driven by rapid expansion of commercial poultry farming.

Which region has the biggest share in Poultry Diagnostics Market?

In 2025, the North America accounts for the largest market share in Poultry Diagnostics Market.

Why are molecular assays gaining popularity?

Regulatory bodies increasingly require molecular confirmation during notifiable disease investigations, and automated PCR platforms deliver speed, sensitivity and reduced dependence on skilled labor.

Page last updated on: