Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.09 Billion |

| Market Size (2031) | USD 13.55 Billion |

| Growth Rate (2026 - 2031) | 8.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulin Pens Market Analysis by Mordor Intelligence

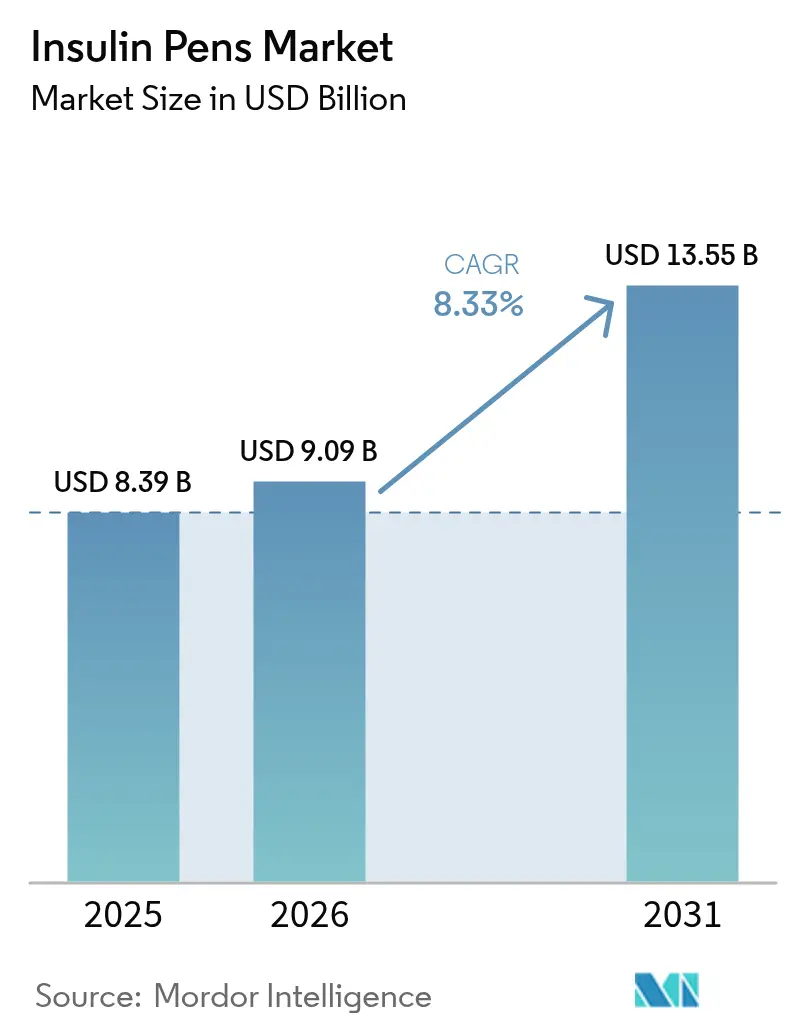

The insulin pens market size was valued at USD 8.39 billion in 2025 and estimated to grow from USD 9.09 billion in 2026 to reach USD 13.55 billion by 2031, at a CAGR of 8.33% during the forecast period (2026-2031). Strong momentum originates from the climbing global diabetes burden, the rapid normalization of smart-connectivity features, and the steady shift from hospital-centric to home-based diabetes care. Manufacturers are injecting capital into capacity scale-ups—Novo Nordisk is spending USD 4.1 billion on new capacity in North Carolina, while Eli Lilly is allocating USD 5.3 billion in Indiana—as they juggle insulin pen demand with parallel GLP-1 production priorities. Supply tightness, visible through Tresiba FlexTouch shortages that persist until January 2026, has nudged prescribers toward reusable and smart alternatives. In parallel, the diabetes population is projected to rise from 529 million in 2021 to 1.31 billion by 2050, a trend that hardwires structural volume growth into the insulin pens market[1]Centers for Disease Control and Prevention, “National Diabetes Statistics Report 2023,” CDC, cdc.gov.

Key Report Takeaways

- By product type, disposable pens held 55.12% of 2025 revenue, while smart/connected pens are projected to expand at a 10.15% CAGR through 2031.

- By diabetes type, type 2 patients accounted for 60.05% of 2025 demand, whereas gestational and other atypical categories are poised for a 9.54% CAGR to 2031.

- By end user, home-care settings represented 50.02% of 2025 consumption, while the “other” segment—including workplace programs and long-term care facilities—will advance at a 10.48% CAGR over the forecast period.

- By technology, mechanical spring-loaded systems captured 45.21% of 2025 sales, yet Bluetooth/NFC-enabled smart devices will record the fastest growth at an 11.28% CAGR through 2031.

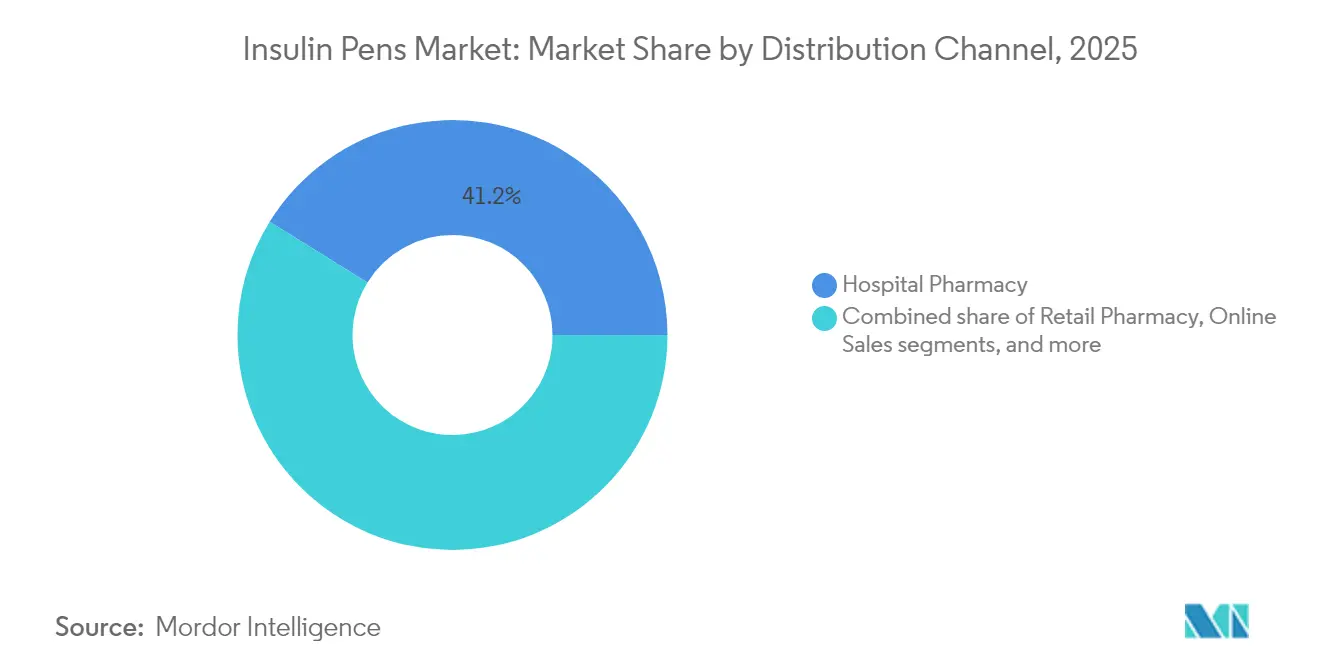

- By distribution channel, hospital pharmacies led with 41.18% share in 2025, whereas online sales are set to grow at a 12.22% CAGR between 2026 and 2031.

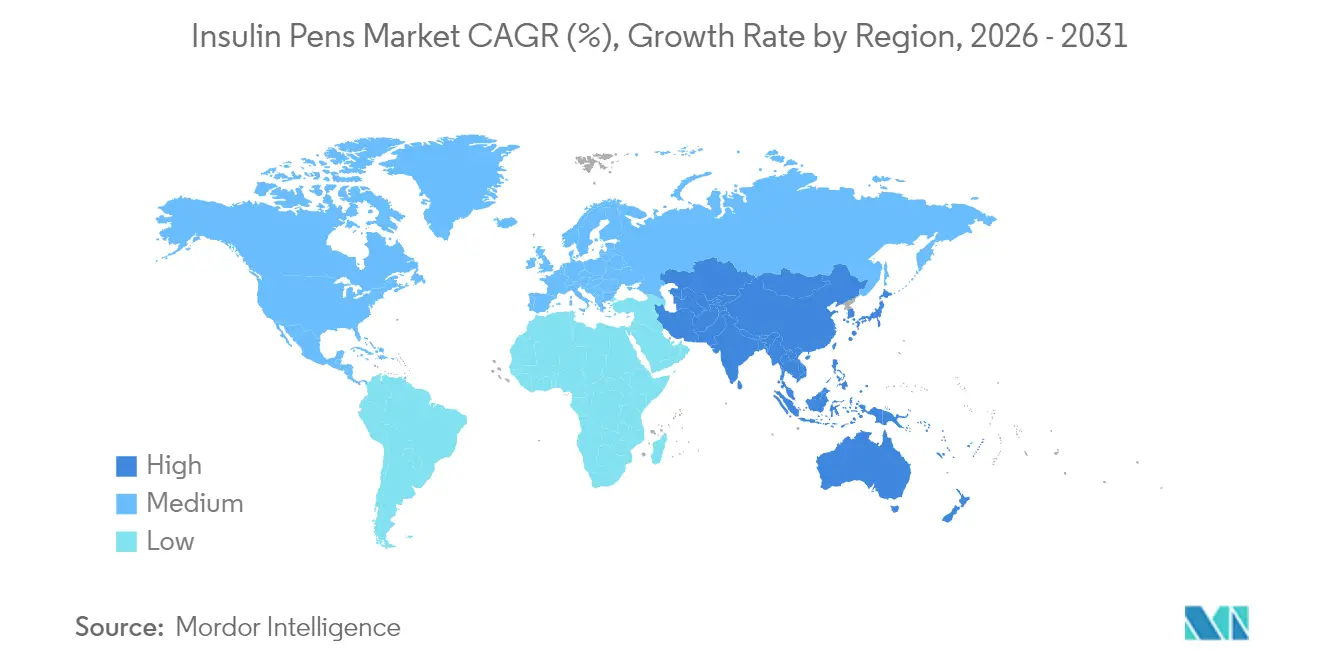

- By geography, North America dominated with 41.02% revenue share in 2025, while Asia-Pacific is expected to log a 9.52% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulin Pens Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Diabetes Prevalence | +2.1% | Global — highest in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Rising Adoption Of User-Friendly Insulin Delivery Devices | +1.8% | North America, Europe, expanding to emerging markets | Medium term (2-4 years) |

| Technological Advancements In Smart Pen Connectivity | +1.5% | Developed markets first, then worldwide | Medium term (2-4 years) |

| Growing Preference For Home-Based Diabetes Management | +1.3% | Global, accelerated by post-pandemic care shifts | Short term (≤ 2 years) |

| Expansion Of Reimbursement Coverage For Pen Devices | +0.9% | North America and Europe primarily | Medium term (2-4 years) |

| Ecosystem Partnerships Integrating Pens With Digital Therapeutics | +0.6% | Technology-advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Diabetes Prevalence

Global diabetes prevalence continues to swell, with type 2 diabetes comprising 96% of total cases and prompting sustained demand for reliable insulin delivery. The International Diabetes Federation projects 783.2 million cases by 2045, and middle-income nations are set to shoulder a 21.1% relative jump that magnifies insulin pens market demand[2]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” IDF, idf.org. Emerging economies wrestle with resource constraints even as their patient pools expand, compelling manufacturers to balance volume with affordability. Brazil typifies the surge, where type 2 prevalence could rise from 9.2% to 27.0% by 2036 amid obesity rates that doubled between 2003 and 2019. Such epidemiological patterns lock-in baseline growth for the insulin pens market, regardless of technology cycles or competitive moves.

Rising Adoption of User-Friendly Insulin Delivery Devices

Close to 60% of global insulin users favor pens over syringes because pens offer consistent dosing, portability, and lower injection anxiety. Uptake accelerates where health-literacy programs and supply chains expand together, especially across Latin America and Southeast Asia. Clinical studies show measurable adherence gains when patients switch to pens, with fewer missed bolus doses and improved time-in-range glucose metrics[3]National Center for Biotechnology Information, “Impacts of China’s National Volume-Based Procurement on Insulin,” PubMed, pubmed.ncbi.nlm.nih.gov. Device makers that refine ergonomic design and needle micro-sharpness boost competitive stickiness, as shorter 4–5 mm needles reduce pain while sustaining accuracy. Such human-factor improvements reinforce patient loyalty and secure recurring cartridge revenue.

Technological Advancements in Smart Pen Connectivity

Connectivity has shifted from a premium add-on to a mainstream expectation. FDA-cleared platforms such as Medtronic’s InPen, now featuring missed-meal dose detection, illustrate how software turns dosing data into predictive insights. Novo Nordisk’s NovoPen 6 and Echo Plus log up to 800 doses and sync automatically with partner apps, allowing clinicians to verify real-world adherence without requiring manual diaries. Integration with continuous glucose monitors, exemplified by Dexcom’s link-up with Novo Nordisk pens, positions the insulin pens market at the center of closed-loop therapy ecosystems. The resulting data fabric encourages value-based care contracts that hinge on measurable outcomes rather than unit sales.

Growing Preference for Home-Based Diabetes Management

Pandemic-era telehealth adoption reshaped diabetes care pathways, lifting home-care to 50.34% of end-user demand in 2024. Expanded Centers for Medicare & Medicaid Services coverage for implantable continuous glucose monitors further legitimizes at-home management approaches[4]Centers for Medicare & Medicaid Services, “Expanded Coverage for Continuous Glucose Monitors,” CMS, cms.gov. Direct-to-consumer distribution, device coaching apps, and remote consultation integrations extend support previously tethered to clinic visits. Such decentralization enforces design priorities around ease of use, on-pen instruction cues, and cloud-enabled troubleshooting, favorably positioning smart pen suppliers for durable growth.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Pen Technologies | -1.2% | Emerging markets; pockets of developed economies | Medium term (2-4 years) |

| Stringent Regulatory Approval Processes | -0.8% | Global, intensity varies by region | Long term (≥ 4 years) |

| Environmental Concerns Over Disposable Plastic Waste | -0.6% | Europe and North America leading, global expansion | Long term (≥ 4 years) |

| Competitive Threat From Alternate Insulin Delivery Systems | -0.4% | Technology-advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Pen Technologies

Smart pens bundle sensors, processors, and connectivity modules that inflate bill-of-materials costs, limiting affordability in price-sensitive countries despite clinical gains. Asia-Pacific studies highlight that upfront device prices remain the chief hurdle to insulin adoption among uninsured urban populations. Manufacturers are piloting subscription models that amortize device costs over cartridge purchases and exploring outcome-based discounts that hinge on real-world glycemic improvements. Continued silicon cost declines and design for manufacturability efforts should ease this restraint over the medium term.

Stringent Regulatory Approval Processes

Combination drug-device rules require dual compliance tracks. FDA guidance on essential delivery outputs stipulates exhaustive bench testing that can extend development timelines by 24 months or more for first-generation smart pens. Smaller innovators often outsource regulatory submissions, raising cash burn and diluting returns. Harmonization progress between the FDA, EMA, and Japanese PMDA remains uneven, making simultaneous multi-region launches complex and costly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Connectivity Drives Premium Segment Growth

Disposable pens retained 55.12% of 2025 revenue as their one-piece format remains the default prescription starting point in most formularies. Familiar design lowers training costs and underpins the insulin pens market size leadership at the entry price tier. Reusable models deliver cartridge savings for high-volume users yet still hinge on manual record keeping. Smart Bluetooth/NFC pens, expanding at a 10.15% CAGR, embed memory chips and wireless radios that auto-log every bolus; this feature shortens clinic consultations by replacing paper diaries with objective data streams. As insurers reimburse the added value, experts expect connectivity to become table stakes by 2028, positioning smart pens to capture progressively larger slices of incremental growth within the insulin pens market.

Manufacturers are re-platforming entire portfolios to ensure feature parity. Sanofi’s AllStar Connect demonstrates how incremental electronics can coexist with established mechanical architecture, minimizing retraining hurdles. Dose-capture dashboards give clinicians line-of-sight to time-in-range metrics, reinforcing pay-for-performance models. The competitive spotlight thus shifts from hardware to analytics, prompting device makers to partner with algorithm specialists and cloud-hosting providers for holistic care offerings.

By Diabetes Type: Type 2 Dominance Shapes Market Dynamics

Type 2 patients generated 60.05% demand in 2025, reflecting epidemiological reality rather than product preference. Later-stage progression to insulin therapy, plus higher volumes per patient, propels this cohort’s share of the insulin pens market size. Automated insulin dosing clearances for adults with type 2 diabetes extend the addressable market for connected pens that feed data to closed-loop algorithms. Type 1 users, though fewer, adopt premium devices earlier because they manage glycemia from diagnosis onward, making them critical early adopters of smart features.

Specialty categories—gestational and other atypical forms—grow at 9.54% CAGR as testing protocols improve and therapy guidelines recommend precise basal-bolus titration. Weekly insulin icodec trials promise lower injection burdens, yet clinicians still prescribe pens for prandial spikes, maintaining relevance across diabetes sub-types. For type 2, lifestyle comorbidities like obesity ensure a stable influx of new insulin initiations, solidifying volume prospects for the insulin pens market.

By End User: Home Care Transformation Accelerates

Home-care absorbed 50.02% of 2025 shipments because self-administration aligns with patient convenience, cost containment, and infection-control priorities. Direct-to-consumer digital platforms now ship starter kits, schedule virtual training, and issue cartridge refill reminders, translating into consistent adherence and cartridge pull-through. Hospital and clinic channels remain essential for initiation and device troubleshooting but represent a diminishing share as care decentralizes. The “other” category—which includes corporate wellness programs and long-term care homes—will advance 10.48% CAGR, drawing on bulk purchasing and integrated population-health dashboards that rely on automated dose logging.

The home-first model reshapes supply chains: cold-chain fulfillment partners optimize last-mile temperature stability, while insurers reimburse telehealth-based device education. Smart pens that provide real-time alerts and share data with caregivers cater to seniors aging in place, reinforcing home-care primacy across the insulin pens market.

By Distribution Channel: Online Sales Disruption Accelerates

Hospital pharmacies captured 41.18% share in 2025 thanks to their prescribing role at diagnosis. Retail pharmacies balance convenience and counseling but face margin pressure from e-commerce entrants. Online channels, growing at a 12.22% CAGR, leverage subscription refills and transparent pricing to pull chronic users away from in-store queues. Amazon Pharmacy’s nationwide rollout bundled same-day shipping and coupon integration, pushing traditional chains to upgrade mobile experiences or partner with digital-health startups.

Cross-border e-pharmacy regulations continue to tighten to curb counterfeit risk, yet accredited platforms now maintain validated cold-chain records and serialized barcodes. Manufacturers experiment with direct-fulfillment portals that capture real-world usage data in exchange for loyalty pricing, though payer formularies still dictate brand selection in insured segments.

By Technology: Smart Features Become Standard

Mechanical spring-loaded pens owned a 45.21% revenue slice in 2025 and will remain foundational where price sensitivity dominates. Embedded cap sensors represent a bridge tech, adding dose-capture capability without full wireless stacks, suitable for cost-controlled health systems transitioning toward data visibility. Fully connected Bluetooth/NFC pens show 11.28% CAGR momentum, underpinned by component price declines and standardization around low-energy communication protocols. Smart features catalyze physician buy-in by resolving adherence blind spots, making them a natural default in tech-literate regions.

Low-power chipsets, molded antenna inserts, and extended-life coin cells have flattened bill-of-materials curves, narrowing the price gap with mechanical peers. Regulators increasingly request digital traceability for medication errors, encouraging health systems to specify connected devices in procurement tenders. The near-term road map points to embedded cellular or ultra-wideband modules that enable over-the-air firmware updates, further future-proofing connected platforms inside the insulin pens market.

Geography Analysis

North America commanded 41.02% revenue in 2025, buoyed by comprehensive insurance coverage, strong clinician adoption of smart pens, and policy caps on insulin co-pays that expand patient access. Advanced interoperability standards facilitate rapid EHR integration, making connected pens attractive for hospital systems pursuing value-based contracts. Supply constraints stemming from GLP-1 line prioritization have nudged prescribers to trial alternative pen SKUs, preserving unit demand despite brand-level shortages.

Europe, characterized by centralized tendering and a high biosimilar uptake rate, maintains robust volume but exerts price pressure on brand leaders. Environmental legislation is steering procurement toward recyclable or reusable formats, prompting lifecycle assessments that feed into tender scoring. Segment-specific reimbursement for connectivity, already active in Germany’s DiGA framework, paves a path for subscription reimbursement attached to digital therapeutic companions.

Asia-Pacific is the fastest climber at 9.52% CAGR through 2031. Rising middle-class disposable income, state insurance rollouts, and urban diabetes hotspots converge to accelerate pen penetration. China’s National Volume-Based Procurement initiative cut insulin list prices yet also stipulates tighter quality and supply guarantees, rewarding companies with local production footprints. India’s National Digital Health Mission fosters electronic prescription uptake, laying groundwork for smart pen data-sharing uptake once device ASPs align with market affordability. Southeast-Asian private insurers bundle mobile coaching with connected pens, compressing the adoption curve often seen in Western markets.

Latin America and the Middle East post mid-single-digit CAGRs; government-funded chronic-disease programs drive pen purchases yet still emphasize low unit cost. Smart connectivity remains niche but is gaining traction in private clinics catering to affluent urban populations.

Africa remains the smallest region by value; global foundations focus on basal insulin vial access, but pilot smart-pen donations in South Africa’s private sector hint at future beachheads.

Competitive Landscape

The insulin pens market is moderately consolidated. Novo Nordisk, Eli Lilly, and Sanofi held roughly 70% combined share in 2024, leaning on proprietary insulin analog portfolios and high-volume manufacturing campuses that deliver scale advantages. Their depth in endocrine sales forces and formulary negotiating clout yields stickiness at both physician and payer levels. Smart-pen extensions such as NovoPen 6 and Lilly’s Tempo Pen embed device hooks that reinforce brand pull-through on matching insulin cartridges.

Second-tier players like Medtronic and BD push differentiation through platform interoperability and specialty biologic delivery capabilities rather than basal-bolus insulin volumes. BD’s tie-up with Ypsomed adds high-viscosity biologic competence, opening therapeutic frontiers beyond diabetes. Biosimilar entrants are targeting price-sensitive hospital tenders; FDA approval of Sanofi’s Merilog biosimilar to NovoLog underscores a pivot toward branded-biosimilar pen formats that pressure incumbent pricing while keeping delivery convenience intact .

Strategic partnerships and M&A center on data integration. Dexcom’s 2025 linkage with Novo Nordisk pens demonstrates how real-time glucose-dose pairing can unlock closed-loop recommendations for non-pump users. Device makers ink cloud-storage deals that facilitate HIPAA-compliant analytics dashboards for payers and research cohorts, converting raw dose logs into longitudinal evidence packs useful for regulatory submissions and formulary renewals. Meanwhile, sustainability pledges push leaders to decarbonize plastics, invest in chemical-recycling pilots, and design for disassembly, adding ESG credentials as a potential selection criterion in institutional tenders.

Insulin Pens Industry Leaders

Novo Nordisk A/S

Eli Lilly

Sanofi

Ypsomed

BD (Becton, Dickinson and Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Dexcom integrated its CGM platform with Novo Nordisk smart pens, enabling single-dashboard visibility of glucose curves and dose history.

- February 2025: FDA approved Merilog (insulin-aspart-szjj) biosimilar to NovoLog in prefilled pen and vial formats, widening U.S. rapid-acting insulin competition.

- January 2025: Tandem Diabetes Care and Abbott agreed to link automated insulin delivery with next-gen glucose-ketone sensing to help patients pre-empt diabetic ketoacidosis incidents.

- December 2024: Novo Nordisk earmarked USD 409 million for a new quality-control lab in Hillerød, Denmark, as part of a USD 6.8 billion network expansion.

- November 2024: Medtronic received FDA clearance for an upgraded InPen app that flags missed meal doses, paving the way for its Smart MDI suite.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the insulin pens market as the annual gross sales value of disposable insulin pens and refill cartridges for reusable pens that deliver prescription human or analog insulin to people with diabetes across all distribution channels worldwide.

Scope Exclusion: Syringes, insulin pumps, inhaled formulations, software-only subscriptions, and veterinary uses sit outside our measurement.

Segmentation Overview

- By Product Type

- Disposable Insulin Pens

- Reusable Insulin Pens

- Smart / Connected Insulin Pens

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- Gestational / Other

- By End User

- Hospitals & Clinics

- Home-Care Settings

- Other End Users

- By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Sales

- Diabetes Clinics

- By Technology

- Mechanical Spring-Loaded

- Smart (Bluetooth / NFC)

- Embedded Dose-Tracking Cap

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed endocrinologists, hospital pharmacists, diabetes educators, and regional wholesalers in North America, Europe, Asia-Pacific, Latin America, and the Gulf. Conversations clarified pen replacement cycles, channel mark-ups, and the emerging appetite for connected pens, allowing us to fine-tune model drivers.

Desk Research

We relied on open datasets from bodies such as the World Health Organization, the International Diabetes Federation, the U.S. FDA device register, Eurostat customs codes HS-3004, and national tender portals that reveal prevalence, approval status, and import flows. Public company 10-Ks, investor decks, and clinical journals on adherence trends enriched context. We also drew selectively on D&B Hoovers for revenue splits and Dow Jones Factiva for shipment-linked news to benchmark players. These inputs let us stitch together patient pools, channel mix, and price corridors. The list is illustrative; many additional statistical digests and trade bulletins were screened to firm up assumptions.

Market-Sizing & Forecasting

We begin with a prevalence-to-treated cohort build-up that multiplies insulin-dependent patient counts by verified usage frequency and average selling prices. The totals are reconciled against a top-down reconstruction created from manufacturer output and customs values, which are then balanced in a feedback loop. Core variables such as diabetes prevalence, pen adoption ratio, smart-pen penetration, reimbursement ceilings, and regional ASP inflation feed a multivariate regression projecting demand to 2030. Supplier roll-ups and channel checks act as guardrails where bottom-up signals diverge.

Data Validation & Update Cycle

We run anomaly checks, peer review each pass, and test variance against quarterly shipments before sign-off. Reports refresh annually, with mid-cycle edits when policy or supply shifts materially alter demand.

Why Mordor's Insulin Pens Baseline Deserves Highest Trust

Published estimates diverge because firms set different scopes, price bases, and refresh rhythms. We flag those contrasts so decision-makers can interpret gaps confidently.

External studies place the 2024 market at USD 9.60 billion and USD 7.79 billion, while an association lists USD 9.90 billion for 2022 and Mordor Intelligence arrives at USD 8.39 billion for 2025.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.39 B (2025) | Mordor Intelligence | - |

| USD 9.60 B (2024) | Global Consultancy A | Scope folds in veterinary and OTC imports |

| USD 7.79 B (2024) | Trade Journal B | Omits premium smart pens; applies single global ASP |

| USD 9.90 B (2022) | Industry Association C | Uses historic FX without inflation re-base |

By anchoring numbers to traceable patient counts and refreshed price curves, our baseline offers the most reproducible and balanced view for strategic planning.

Key Questions Answered in the Report

What is the current size of the insulin pens market?

The insulin pens market stands at USD 9.09 billion in 2026 and is projected to reach USD 13.55 billion by 2031, expanding at a CAGR of 8.33% during 2026-2031.

Which product segment is growing fastest?

Smart and connected pens show the highest momentum, advancing at a 10.15% CAGR through 2031 on the back of Bluetooth and NFC adoption.

How big is home-care demand for insulin pens?

Home-care users accounted for 50.02% of global shipments in 2025, reflecting the shift toward self-managed diabetes care.

Which region leads and which grows quickest?

North America holds the largest share at 41.02%, while Asia-Pacific registers the fastest growth with a 9.52% CAGR through 2031.

Who are the key players in the insulin pens market?

Novo Nordisk, Eli Lilly, and Sanofi together control about 70% of global revenue, with Medtronic and BD leading in smart-pen platform partnerships.

What major FDA approvals have shaped the market recently?

Key clearances include Merilog biosimilar insulin in 2025 and expanded automated insulin dosing indications for type 2 diabetes in 2024.

Page last updated on: