Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

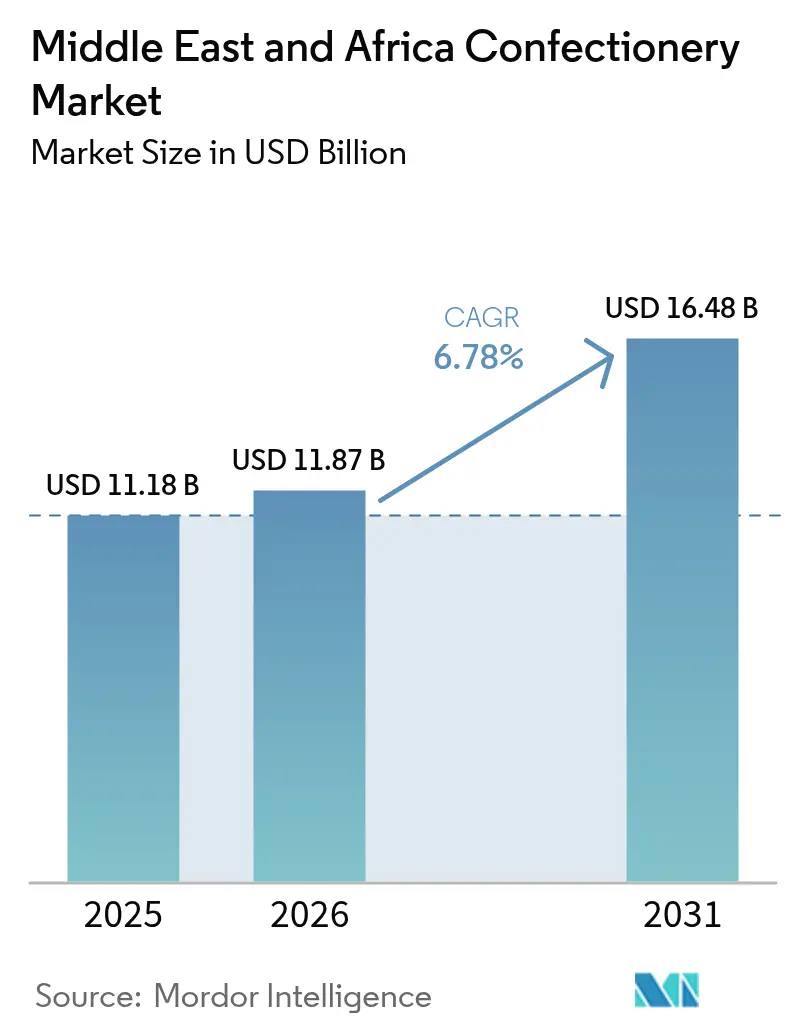

| Base Year Market Size (2025) | USD 11.18 Billion |

| Market Size (2026) | USD 11.87 Billion |

| Market Size (2031) | USD 16.48 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Confectionery Market Analysis by Mordor Intelligence

The Middle East and Africa confectionery market size was USD 11.18 billion in 2025 and is projected to expand to USD 11.87 billion in 2026 and to USD 16.48 billion by 2031, registering a CAGR of 6.78% between 2026 and 2031. Consumers in large urban centers are purchasing more indulgent sweets as disposable income rises, and this shift is encouraging local and multinational players to widen their distribution footprints. Premium chocolate gifts posted the sharpest unit gains in 2025, helped by higher tourist traffic in the United Arab Emirates and Saudi Arabia. Local artisans have also popularized date-filled, camel-milk, and vegan variants that command retail prices above mass products. Meanwhile, hypermarkets in South Africa and Egypt are testing self-service pick-and-mix bays that lower labor costs and expand the share of private-label assortments, squeezing margins for smaller domestic competitors.

Key Report Takeaways

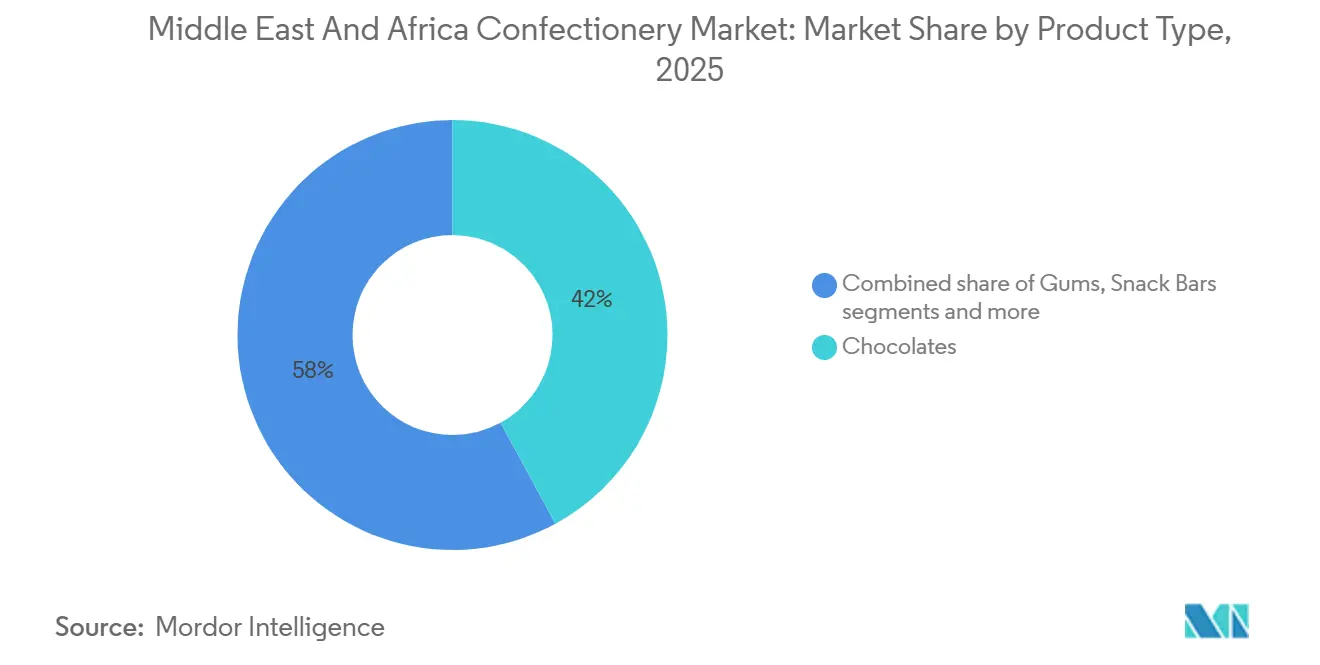

- By product type, chocolates led with 42.05% of the Middle East and Africa confectionery market share in 2025, while snack bars are forecast to post the fastest 6.87% CAGR through 2031.

- By packaging type, flexible packaging accounted for 61.21% of the Middle East and Africa confectionery market size in 2025, whereas blister packs are projected to rise at a 7.05% CAGR between 2026 and 2031.

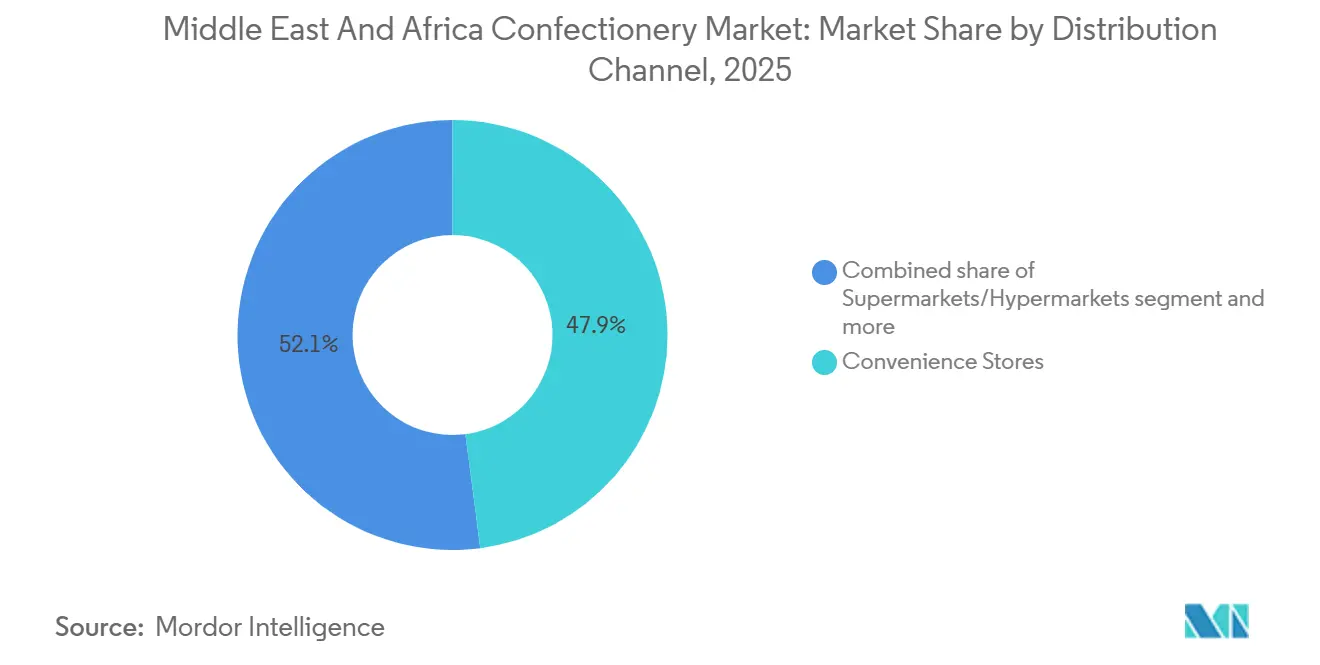

- By distribution channel, supermarkets and hypermarkets captured 47.94% of the Middle East and Africa confectionery market share in 2025; online retail stores are expected to expand at a 7.23% CAGR during 2026-2031.

- By geography, Saudi Arabia represented 23.57% of 2025 revenue, yet Nigeria is on track for an 8.06% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Confectionery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for premium and artisanal chocolate products | +1.2% | Global, with stronger influence in GCC countries | Medium term (2-4 years) |

| Seasonal consumption driven by cultural and religious celebrations | +1.8% | Middle East core, moderate impact in North Africa | Long term (≥ 4 years) |

| Launch of new flavors and diverse product offerings | +0.9% | Urban centers across Middle East and Africa, strongest in the United Arab Emirates and Saudi Arabia | Short term (≤ 2 years) |

| Growth in tourism contributing to market expansion | +1.1% | GCC countries, Egypt, Morocco, Turkey | Medium term (2-4 years) |

| Proliferation of modern retail outlets and online grocery platforms | +1.3% | Saudi Arabia, United Arab Emirates, Egypt, South Africa | Medium term (2-4 years) |

| Growing urbanization and disposable income levels | +0.7% | High-income segments in GCC and urban Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising preference for premium and artisanal chocolate products

Manufacturers report that affluent shoppers in Dubai, Riyadh, and Cape Town trade up to single-origin dark chocolate and filled pralines priced above USD 80 per kilogram. Boutique chains such as Patchi and Bateel highlight transparent bean-to-bar sourcing and halal-certified recipes, which resonate with health-conscious millennials. Duty-free stores inside Abu Dhabi’s Zayed International Airport increased shelf space for gift assortments in 2025, reinforcing impulse purchases. Global suppliers have responded by launching small-batch lines co-branded with regional pastry chefs, broadening mass appeal without alienating luxury buyers. Over the medium term, the rising popularity of such offerings is forecast to lift average unit values across the Middle East and Africa confectionery market.

Seasonal consumption driven by cultural and religious celebrations

Ramadan, Eid, and Christmas drive pronounced volume spikes in the Saudi confectionery market. In 2025, Saudi households boosted confectionery spending during Ramadan week alone, underscoring the holiday's significance. Companies schedule limited-edition packaging themed around crescent moons, lanterns, or local heritage icons, which elevates perceived exclusivity and drives consumer interest. Corporate gifting also surges during these festive times, with banks and telecom operators ordering bespoke boxes for clients, highlighting the importance of these occasions. Stability in crude-oil receipts is enabling higher discretionary budgets among Gulf employers, reinforcing this gift-centric culture and further boosting sales. The short-term effect of these holiday campaigns is a positive lift to unit sales and gross margins ahead of summer slowdowns, showcasing the effectiveness of targeted marketing strategies.

Launch of new flavors and diverse product offerings

Younger consumers look for novelty, prompting an uptick in spicy, floral, and fruit-forward flavor launches. In 2025, over 120 stock-keeping units featured hibiscus, cardamom, or date inclusions. Ferrero introduced a saffron-infused Rocher variant in Kuwait, and domestic brand Afrikoa shipped orange-peel dark bars to specialty grocers in Johannesburg. Snack bars formulated with chia, quinoa, or almond butter compete directly with breakfast biscuits, targeting on-the-go professionals. Such experimentation differentiates portfolios and mitigates raw-material volatility by enabling flexible sourcing. The strategy is expected to unlock fresh demographics and drive a steady uptick in premium shelf space allocation.

Growth in tourism contributing to market expansion

The growth of tourism drives the expansion of the Middle East and Africa confectionery market, particularly in Gulf Cooperation Council (GCC) countries. Tourists generate additional demand for confectionery products through direct consumption and souvenir purchases. Dubai's position as a travel hub significantly influences this market through its duty-free retail sector, hotel minibar offerings, and destination-specific confectionery products that serve international visitors. The tourism-driven demand increases sales and encourages confectionery manufacturers to develop products targeting tourists. For instance, according to the Department of Economy and Tourism, Dubai recorded 9.88 million overnight visitors in the first half of 2025, representing a 6% increase from the same period in 2024 [1]Source: Department of Economy and Tourism, "Tourism Performance Report January - June 2025", dubaidet.gov.ae. These visitor numbers demonstrate Dubai's importance as a travel destination and its impact on the confectionery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adherence to strict regulatory compliance | -0.8% | Global, with varying intensity across countries | Medium term (2-4 years) |

| Competition with traditional local confectionery | -1.1% | Strongest in North Africa and traditional markets | Long term (≥ 4 years) |

| Volatility in raw material prices | -1.4% | Global impact, particularly affecting chocolate segments | Short term (≤ 2 years) |

| Health concerns over high sugar consumption | -0.9% | Sub-Saharan Africa and rural areas across Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adherence to strict regulatory compliance

Food authorities across the GCC require import permits, halal certificates, and Arabic labeling whose wording must match approved nutritional profiles. These stringent measures aim to ensure food safety and authenticity in the region. However, they also pose challenges for international suppliers navigating the complex regulatory landscape. Saudi Arabia’s SFDA tightened cocoa butter equivalents thresholds in 2025, forcing European suppliers to reformulate or pay higher inspection fees. This move underscores Saudi Arabia's commitment to maintaining stringent food standards. European suppliers, now facing unexpected costs, are reevaluating their strategies in the GCC market. Egypt introduced front-of-pack warning icons on high-sugar items, elevating packaging costs. This initiative aligns with global trends prioritizing public health and transparency. Yet, the added costs and adjustments have stirred debates among local manufacturers. Such delays can mean missed market opportunities and diminished competitive edge.

Health concerns over high sugar consumption

Rising obesity and diabetes rates in South Africa and Turkey are prompting public-health campaigns that link confectionery intake to lifestyle diseases. These campaigns aim to raise awareness about the health risks associated with excessive sugar consumption. As a result, many consumers are reevaluating their dietary choices in light of these warnings. Nigeria’s finance ministry imposed a NGN 10 per gram sugar excise, and similar debates are active in Kenya and Morocco [2]Source: Global Health Advocacy Incubator, "Nigerian Advocates Celebrate Sugar-Sweetened Beverage Tax Signed into Law", advocacyincubator.org. These discussions highlight the growing concern over sugar's impact on public health. Policymakers in these nations are weighing the potential benefits of such taxes against the economic implications. This skepticism is fueled by debates on the effectiveness of such measures in curbing sugar consumption. Meanwhile, schools are taking proactive steps, with many even introducing healthier snack options. Brands counteract the narrative with portion-controlled packs, sugar-free mints, and protein-fortified snack bars, but uptake remains niche.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chocolates Retain Lead While Snack Bars Accelerate

In 2025, chocolates accounted for a significant 42.05% of the revenue, and experts predict this trend will continue as gifting traditions remain strong. The Middle East and Africa's confectionery market is witnessing a surge in chocolate sales, driven by a trend towards premiumization, with chocolate segment revenues outpacing volume increases in the broader category. According to the Saudi Press Agency through the Zakat, Tax and Customs Authority, “the Kingdom’s chocolate imports exceeded 123 million kg in 2024, reflecting increased demand [3]Source: Saudi Press Agency, "Kingdom Imports over 123 million Kilograms of Chocolates in 2024", spa.gov.sa. Milk chocolate variants dominate, due to a family-oriented preference for sweeter flavors. However, dark chocolate is gaining traction in expatriate communities, especially where European tastes are prominent, hinting at a lucrative margin potential.

Snack bars are on a growth trajectory, boasting the highest forecasted CAGR of 6.87%, as urban professionals increasingly gravitate towards convenient, portion-controlled energy options. Major retail chains are strategically placing protein and fruit-and-nut bars next to cold-brew coffee fridges, a move that underscores the power of cross-merchandising. While multinational cereal giants are swiftly scaling up by tapping into established granola supply chains, they face stiff competition from local date-based bars by Al Barari, which are winning consumers over with their authenticity messaging.

By Packaging Type: Flexible Formats Dominate Yet Blister Packs Gain Momentum

Flexible pouches and flow wraps, accounting for 61.21% of 2025 unit sales, are favored for their ability to accommodate multiple piece counts and safeguard moisture-sensitive contents. Their cost-efficiency not only appeals to budget-conscious families but also plays a pivotal role in promotional strategies. Moreover, multilayer barrier films enhance product appeal by allowing photo-realistic graphics, bolstering premium chocolate positioning without the need for glassine inserts. While the flexible share may see a slight dip due to sustainability pushes favoring recyclable rigid alternatives, the absolute volume is set to grow in tandem with the overall category expansion.

Blister packs, with a projected CAGR of 7.05% through 2031, have found favor with pharmacy chains, especially for pocket-size breath mints positioned near check-out lanes. Beyond just convenience, this format's tamper-evidence feature not only meets regulatory standards but also provides peace of mind to mothers buying for school lunches. Furthermore, the Middle East and Africa's confectionery market, already seeing a surge in blister pack adoption, could witness even greater growth if oral-care brands introduce xylitol mints as a functional offering. While machinery investments in the region remain robust, there's a notable trend of co-packing partnerships emerging in Turkey and Egypt, signaling a strategic move to mitigate capital risks.

By Distribution Channel: Supermarkets Command Share, Online Retail Surges

Supermarkets and hypermarkets delivered 47.94% of 2025 sales as they aggregate weekly household shopping trips. These retail giants have long been the go-to destination for families, consolidating their shopping needs under one roof. However, the Middle East and Africa confectionery market share for this channel is expected to erode slowly, though, as home-delivery platforms close assortment gaps. As convenience becomes paramount, these platforms are swiftly adapting, ensuring they meet the diverse needs of consumers. Chains, including Spinneys and Pick n Pay, deploy electronic shelf labels that synchronize in-store and online prices, offering transparency that shoppers reward with loyalty-card engagement. This tech-savvy approach not only boosts customer trust but also enhances the overall shopping experience, setting these chains apart in a competitive landscape.

Online retail is forecast to rise at a 7.23% CAGR, lifted by click-and-collect lockers that eliminate heat-exposure risk. Shoppers appreciate same-day fulfillment during festive seasons when traffic congestion impedes store visits. Live-stream snack showcases on Instagram and TikTok spur impulse checkouts through embedded links, propelling cross-border demand from diaspora communities craving heritage treats. Despite cold-chain challenges, the Middle East and Africa confectionery market size accessible via digital channels should more than double by 2031, driving data-driven personalization and targeted promotions.

Geography Analysis

Saudi Arabia generated 23.57% revenue in 2025, buoyed by premium chocolate gifts exchanged during religious festivals. These festivals, deeply rooted in tradition, see families and friends exchanging gifts, with premium chocolates becoming a favored choice. Touristic pilgrimage flows to Mecca spur brisk sales of small souvenir assortments, while Vision 2030 retail reforms attract international franchise operations. The Middle East and Africa confectionery market size in the Kingdom benefits from favorable import duty bands on finished candy, provided halal certificates accompany shipments.

Nigeria is forecast to be the fastest-growing at 8.06% CAGR through 2031. With a youthful demographic and rapid mobile penetration, e-commerce adoption is on the rise. Domestic manufacturers are now leveraging cassava-based glucose syrups, a cost-effective alternative to imported corn sweeteners, enhancing their price competitiveness. Investments in mass-market brands, priced at NGN 50 per piece, are strategically placed in informal kiosks. This move not only brings impulse candy closer to low-income segments but also broadens the consumer base, setting the stage for future premium trade-ups.

South Africa remains the southern anchor, where sugar-reformulation mandates push R&D outlays but also encourage functional snack bars. The push for healthier alternatives has led to a surge in demand for these bars, with consumers increasingly prioritizing health. Egypt’s large population and rising tourist arrivals to the Red Sea corridor provide incremental volume for souvenir confectionery. Meanwhile, the United Arab Emirates keeps its role as a re-export hub, aggregating bulk shipments and redistributing them to smaller Gulf and East African markets under free-zone advantages.

Competitive Landscape

Retail channel divergence shapes regional demand patterns. Gulf Cooperation Council countries typically purchase high-end chocolate boxes through duty-free or boutique stores. This consumer behavior elevates average selling prices, allowing global firms to test micro-lot innovations. By contrast, North African economies favor sugar confectionery sold in multi-serve packs, appealing to value-oriented households. Government subsidy frameworks on refined sugar indirectly lower manufacturing costs, boosting local output. As a result, these regional preferences not only influence pricing strategies but also shape the product offerings of global brands. Such dynamics underscore the importance of understanding local tastes in the global confectionery market.

Political stability and logistics infrastructure remain decisive. Turkey leverages customs-union privileges with the European Union to import semi-finished chocolate and re-export finished pralines with Arabic labeling. Morocco’s Tanger-Med port expansion halves container dwell times, increasing freshness for temperature-sensitive bars destined for West Africa. South-South trade corridors, including the African Continental Free Trade Area, gradually erode tariff barriers, which could disperse sourcing networks and heighten competition. These logistical advantages and political maneuvers not only bolster Turkey and Morocco's positions in the market but also set the stage for potential shifts in regional trade dynamics. As countries navigate these waters, the balance of power in the confectionery trade could see notable changes.

Currency volatility presents mixed implications. Depreciation of the Egyptian pound inflates import bills for cocoa mass and hazelnuts, nudging factories to explore indigenous peanut or sesame fillings. In Nigeria, local currency weakness increases input costs, yet it also shelters domestic players from cheap Asian imports, creating space to scale capacity. Firms hedging via multi-origin ingredient procurement gain flexibility to weather macro swings. Such strategies highlight the adaptive nature of businesses in the face of economic challenges. As firms navigate these currency fluctuations, their choices could redefine competitive landscapes in the confectionery sector.

Middle East And Africa Confectionery Industry Leaders

-

Mars, Incorporated

-

Mondelēz International, Inc.

-

Nestlé S.A.

-

Ferrero SpA

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Kreol Travel Retail introduced Petit Gourmet's Pistachio Kunafa Chocolate at Riyadh Duty Free in King Khalid International Airport. The 470g sharing-size bar, exclusive to travel retail, combines traditional Middle Eastern flavors in a premium format designed for regional and international travelers.

- February 2025: Nestlé launched KitKat Tablets in South Africa, offering three variants: Double Chocolate, Hazelnut, and Salted Caramel. The company introduced this product to provide consumers with a new taste experience.

- April 2024: FULFIL Chocolate Protein Bars entered the South African market through Spar Stores and Clicks nationwide. The protein bars are available in four flavors: Salted Caramel, Peanut and Caramel, Hazelnut Whip, and Chocolate Brownie.

Middle East And Africa Confectionery Market Report Scope

Confectionery refers to food products that are primarily made with sugar or sweeteners and are typically consumed as sweets or treats. The Middle East and Africa Confectionery Market is Segmented by Product Type (Chocolates, Gums, Sugar Confectionery, Snack Bars, and Others), by Packaging Type (Flexible Packaging, Rigid Packaging, Blister Packs, and Others), by Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online Retail Stores, and Other Distribution Channels), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Chocolates | Dark |

| Milk/White | |

| Gums | Chewing Gum |

| Bubble Gum | |

| Sugar Confectionery | Hard Candy |

| Lollipops | |

| Mints | |

| Pastilles, Gummies, and Jellies | |

| Toffees and Nougats | |

| Others | |

| Snack Bars | Protein Bar |

| Cereal Bar | |

| Fruit and Nut Bar | |

| Others |

By Packaging Type

| Flexible Packaging |

| Rigid Packaging |

| Blister Packs |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Chocolates | Dark |

| Milk/White | ||

| Gums | Chewing Gum | |

| Bubble Gum | ||

| Sugar Confectionery | Hard Candy | |

| Lollipops | ||

| Mints | ||

| Pastilles, Gummies, and Jellies | ||

| Toffees and Nougats | ||

| Others | ||

| Snack Bars | Protein Bar | |

| Cereal Bar | ||

| Fruit and Nut Bar | ||

| Others | ||

| By Packaging Type | Flexible Packaging | |

| Rigid Packaging | ||

| Blister Packs | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the value of the Middle East and Africa confectionery market in 2026?

It stood at USD 11.87 billion.

Which product type currently dominates confectionery sales in the region?

Chocolates held 42.05% of 2025 revenue.

Which channel is projected to be the fastest-growing for confectionery purchases?

Online retail stores are forecast to rise at a 7.23% CAGR from 2026-2031.

Which country is expected to record the quickest confectionery growth to 2031?

Nigeria is projected to expand at an 8.06% CAGR.

Page last updated on: