Nanocellulose Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

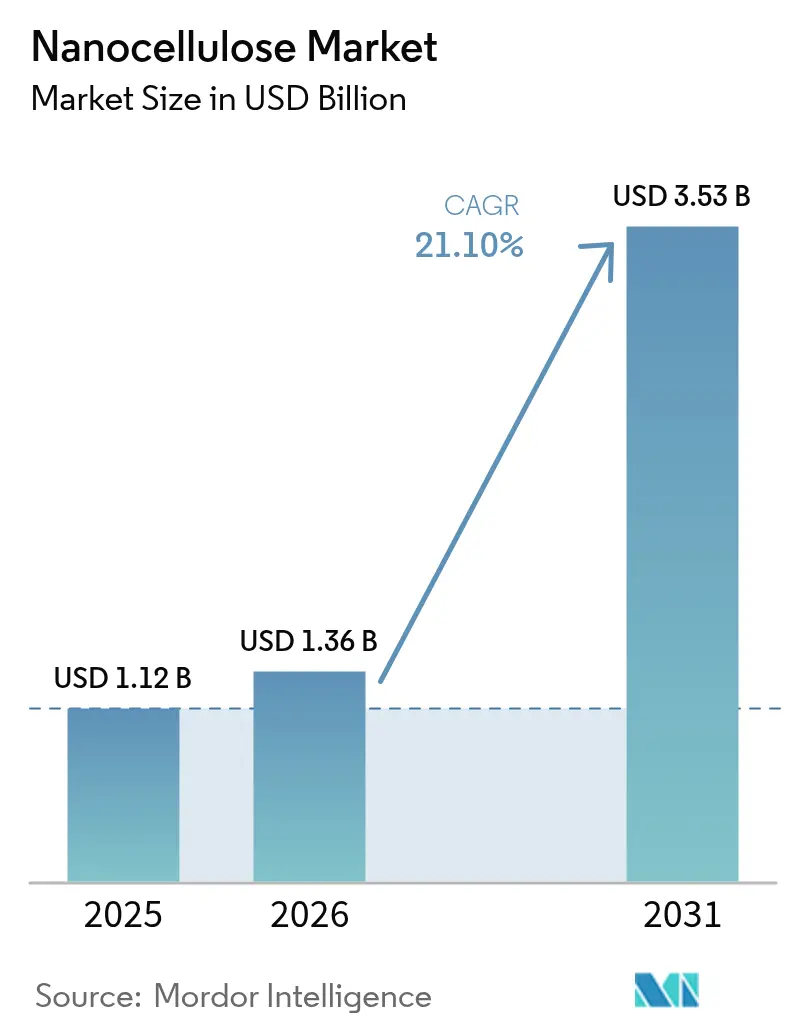

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 3.53 Billion |

| Growth Rate (2026 - 2031) | 21.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nanocellulose Market Analysis by Mordor Intelligence

Nanocellulose market size in 2026 is estimated at USD 1.36 billion, growing from 2025 value of USD 1.12 billion with 2031 projections showing USD 3.53 billion, growing at 21.1% CAGR over 2026-2031. Escalating sustainability mandates, volatile petrochemical prices, and rapid material science breakthroughs converge to create a clear runway for double-digit expansion. Automotive lightweighting, recyclable barrier films, and biomedical scaffolds headline near-term demand, while enzymatic low-energy processes unlock future cost competitiveness. North American incumbents leverage mature pilot lines and close original equipment manufacturer (OEM) ties, yet Asian producers narrow the gap through lower conversion costs and proximity to electronics and packaging clusters. Raw-material flexibility shifting from wood pulp to agricultural residues further de-risks supply chains and anchors circular-economy business models. Established pulp majors expand tonnage on the competitive front, whereas biotech start-ups chase premium therapeutic niches, resulting in an active partnership and licensing landscape that accelerates application rollout.

Key Report Takeaways

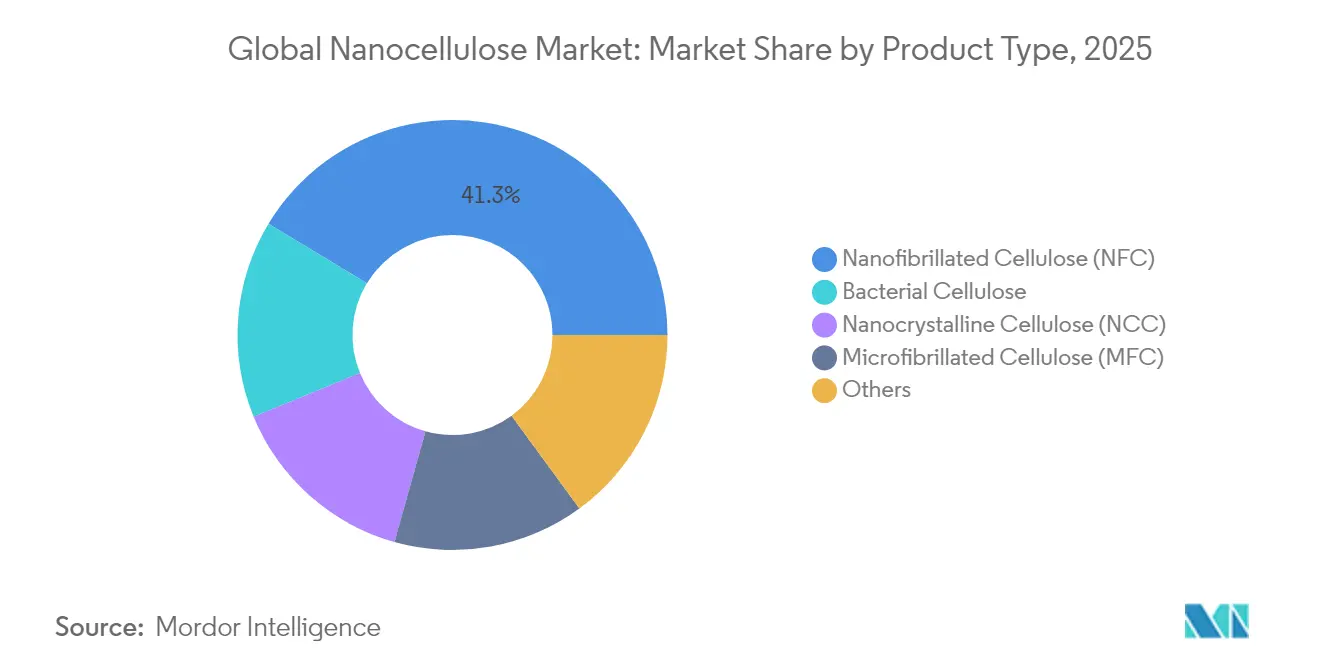

- By product type, Nanofibrillated Cellulose led with 41.35% of the Nanocellulose market share in 2025, while Bacterial Cellulose is forecast to clock a 35.40% CAGR through 2031.

- By source, Wood Pulp commanded 57.80% of the Nanocellulose market size in 2025, but Agricultural Residues are projected to expand at a 22.95% CAGR between 2026 and 2031.

- By form, Gel accounted for 39.65% of the Nanocellulose market share in 2025; Suspension is advancing at a 22.10% CAGR through 2031.

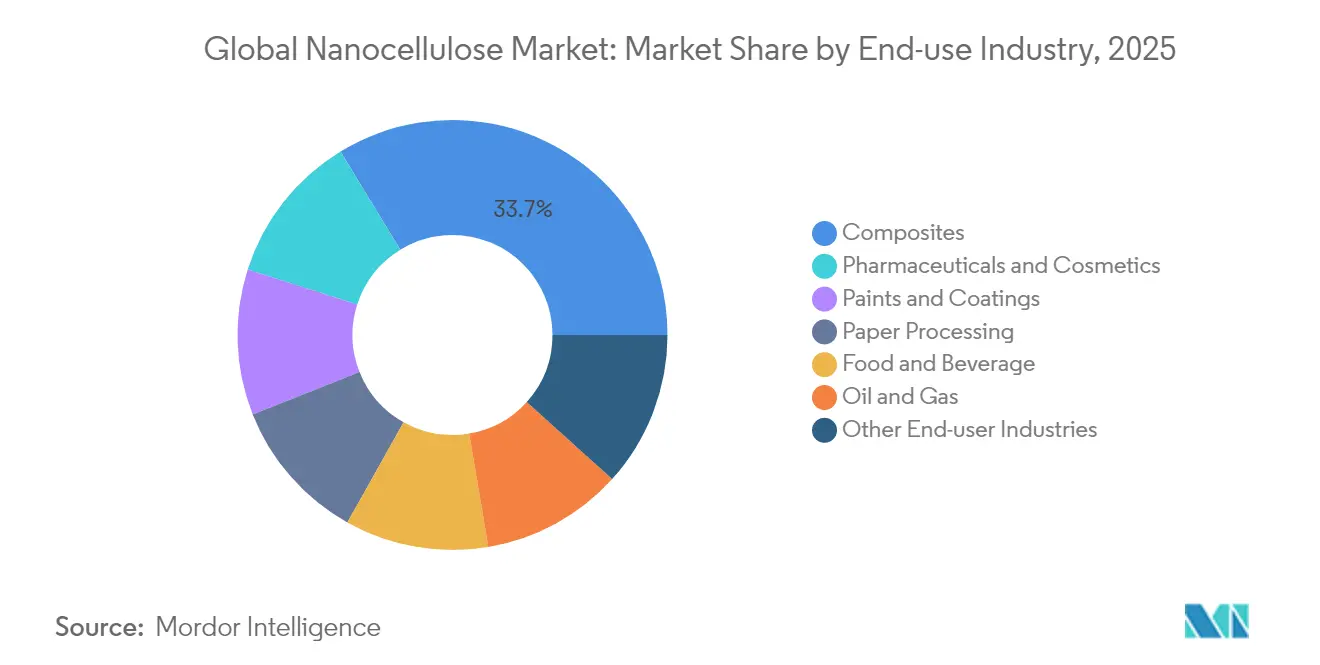

- By end-use industry, Composites captured 33.72% of the Nanocellulose market size in 2025, whereas Pharmaceuticals and Cosmetics are set to grow at a 24.90% CAGR to 2031.

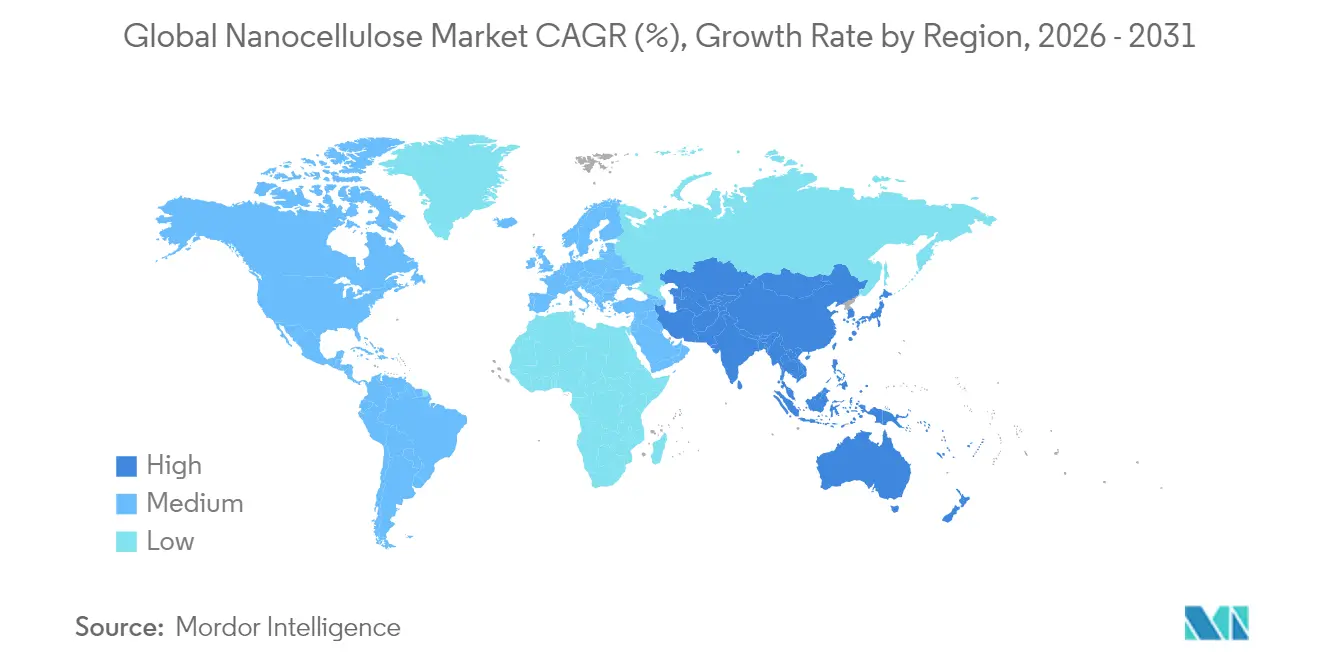

- By geography, North America dominated with 43.25% revenue share of nanocellulose industry in 2025, while Asia-Pacific records the highest projected CAGR at 23.70% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nanocellulose Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Superior Mechanical and Barrier Properties | +4.2% | North America, Europe, global OEM clusters | Medium term (2-4 years) |

| Sustainable Packaging Demand Surge | +5.8% | EU led, expanding to Asia-Pacific and North America | Short term (≤ 2 years) |

| Regulatory Push to Replace Single-use Plastics | +3.7% | EU primary, North America secondary, APAC emerging | Long term (≥ 4 years) |

| Rising R&D Pilot Facilities and Funding | +2.9% | North America and Europe, APAC scaling | Medium term (2-4 years) |

| Enzymatic Low-energy Production Breakthroughs | +3.1% | Brazil and Finland early adopters, global roll-out | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Superior Mechanical and Barrier Properties

Nanocellulose’s tensile strength of 4.9–7.5 GPa (Gigapascals) and elastic modulus of 100–200 GPa position it close to carbon fiber in weight-sensitive components, making it attractive for automotive body panels and aircraft interiors within the nanocellulose market. Oak Ridge National Laboratory validated this potential in 2025 by showing 50% higher tensile strength and nearly double toughness in carbon-nanofiber-enhanced nanocellulose composites versus conventional glass-fiber alternatives. The high aspect ratio and surface area foster tight bonding with polymer matrices, minimizing delamination risk and boosting fatigue life. Japanese automakers project a 20 kg per-vehicle weight cut when nanocellulose substitutes selected metal and plastic parts, translating into meaningful fuel savings and lower lifecycle emissions. Beyond load-bearing parts, ultrathin nanocellulose films block oxygen and water vapor better than Ethylene Vinyl Alcohol (EVOH) or Polyvinylidene Chloride (PVDC), yet remain recyclable and compostable. These dual mechanical and barrier advantages underpin the material’s broad addressable market, from consumer electronics casings to pharmaceutical blister packs.

Sustainable Packaging Demand Surge

Retail, e-commerce, and food brands rush to replace petroleum films, driving a steep demand curve for bio-based barriers. European chains in Belgium, France, and Luxembourg replaced pilot-scale plastic trays with cellulose packs in the 2024 R3PACK trial, eliminating thousands of tonnes of single-use plastics. European Union (EU) directives mandate that all packaging be reusable or recyclable by 2030, prompting converters to qualify nanocellulose coatings that upgrade ordinary paperboard. Bacterial cellulose films show superior ultraviolet (UV) shielding and tensile strength, reducing spoilage in light-sensitive foods while holding up under cold-chain logistics. Swedish start-up lines achieved cost parity with Low Density Polyethylene (LDPE) wrap by optimizing drying energy and roll-to-roll coating speeds, removing the final economic roadblock. Food and Drug Administration (FDA)’s Generally Recognized As Safe (GRAS) nod for fibrillated cellulose in food contact further derisks adoption for North American suppliers [1]FDA, “Substances Generally Recognized as Safe,” fda.gov. As brand owners lock in multi-year supply contracts, the nanocellulose market secures a predictable revenue base for capacity expansions.

Regulatory Push to Replace Single-use Plastics

Public policy shifts demand rather than merely encourages sustainable substitutes within the nanocellulose market. The EU’s 2025 bio-technology strategy tags wood-derived nanocellulose as a priority material for medical, construction, and consumer uses, unlocking access to public grants and fast-track regulatory reviews. Lenzing’s 2024 rollout of Lyocell Dry fibers exemplifies how incumbents pivot to meet tightening standards on wipes, diapers, and feminine hygiene products. The United States ban on expanded polystyrene (EPS) food containers adds volume pull as quick-service restaurants trial nanocellulose-reinforced molded fiber bowls. Asia-Pacific regulators lag but plan convergent frameworks, which could trigger a rapid catch-up phase in the South Korea and Thailand markets. Predictable compliance deadlines encourage investors to back multi-line mills, confident that substitution will shift from optional to mandatory over the forecast window.

Rising R&D Pilot Facilities and Funding

The nanocellulose industry shifts from lab curiosity to pre-commercial scale. Nippon Paper established a dedicated cellulose nanofibrils (CNF) line at Ishinomaki Mill, proving that a pulp major can repurpose legacy assets into high-value biomaterial hubs. The United States Department of Agriculture (USDA)’s Forest Products Laboratory moved from gram-scale to 4 kg batch runs, informing continuous-production design and in-line quality control protocols. UPM Biomedicals launched FibGel, the first injectable nanocellulose hydrogel cleared for implantable devices, marking regulatory trust in medical-grade cellulose. Venture funding now tilts toward application pilots rather than exploratory chemistry, tying grants to demonstrable payback periods. Co-development agreements between mills and end-users shorten the feedback loop, ensuring that new grades meet exact rheology or purity targets before full commercialization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Cost and Scale-up Risk | -6.3% | Global, pronounced in emerging economies | Medium term (2-4 years) |

| Competition From Other Bio-nanomaterials | -2.8% | Global, with regional preference shifts | Long term (≥ 4 years) |

| Food-contact Safety and Inhalation Concerns | -1.9% | EU and North America, spreading worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Scale-up Risk

Even with hydrolysis optimization, minimum selling prices hover at USD 10,031 per dry tonne for acid routes, and USD 65,740 per dry tonne for current enzymatic yields, dwarfing commodity polymer benchmarks. Continuous papermaking pilots halve capex per output kilogram, yet sustained quality control remains elusive as retention tops out at 73%. Capex intensity restricts large-scale units to pulp majors and state-backed entities, marginalizing innovators in emerging markets that lack patient capital. Life-cycle assessments show a 6.5-fold environmental win once plants exceed 20,000 tpa, but financing such nameplates requires off-take certainty that few downstream users can underwrite today. This chicken-and-egg dynamic tempers otherwise strong demand signals and prompts phased debottlenecking rather than greenfield mega-mills.

Competition From Other Bio-nanomaterials

Lignin nanoparticles offer superior ultraviolet (UV) absorption and tunable color, giving them an edge in smart food packaging and automotive coatings within the nanocellulose market. Xanthan gum, an established bacterial polysaccharide, enjoys mature supply chains and costs that undercut nanocellulose in viscosity-modification duties. As each bio-nano candidate excels in a specific performance niche, end-users mix and match, preventing nanocellulose from claiming monopoly status. Regional bias deepens fragmentation: Scandinavian converters lean toward wood-based cellulose chemistries, while Brazilian packagers favor bagasse-derived lignin blends. This competitive tapestry keeps pricing power in check and challenges producers to sharpen value propositions rather than rely on a generic sustainability narrative.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bacterial Cellulose Drives Premium Applications

Nanofibrillated Cellulose (NFC) commands 41.35% market share in 2025 within the nanocellulose market, reflecting its established production infrastructure and broad applicability across paper processing and composites applications. However, Bacterial Cellulose is the fastest-growing segment with 35.40% CAGR through 2031, driven by its ultra-pure properties and premium positioning in pharmaceuticals and biomedical applications. The production dichotomy reveals strategic positioning where NFC leverages mechanical processing scalability, while bacterial cellulose targets high-value applications, justifying fermentation costs.

Nanocrystalline Cellulose (NCC) maintains steady growth through its crystalline structure advantages in reinforcement applications, particularly where dimensional stability and thermal resistance prove critical. Microfibrillated Cellulose (MFC) is a bridge technology, offering enhanced properties over conventional cellulose while remaining cost-competitive with traditional additives in paper and packaging applications.

By Source: Agricultural Residues Challenge Wood Dominance

Wood Pulp maintains its dominant position with 57.80% market share in 2025, leveraging established supply chains and processing infrastructure developed over decades of pulp and paper industry evolution. Yet, Agricultural Residues as a source demonstrate the strongest growth trajectory at 22.95% CAGR, fundamentally challenging wood pulp's long-term dominance through cost advantages and circular economy alignment. The shift toward agricultural residues reflects economic optimization and sustainability mandates favoring waste valorization over virgin resource consumption.

Micro-algae, seaweed, and bacterial hosts supply specialty volumes for cosmetic serums and ophthalmic solutions where absolute purity trumps cost. These bio-sources allow closed-loop cultivation, minimizing pesticide carry-over and easing Genetically Modified Organism (GMO)-free certification. European consortiums study hemp hurd and flax shive feedstocks, leveraging regional fiber crops to offset pulpwood shortages. However, residue logistics remain complex: seasonal availability demands wet-storage silos or densification pellets, adding hidden capex. Wood pulp producers counter with chain-of-custody certification and guaranteed year-round supply, arguing reliability for mass-market packaging volumes. The competitive dance ensures continuous innovation and locks the nanocellulose market into a multi-feedstock future.

By Form: Suspension Technologies Enable New Applications

Gel retained 39.65% of the Nanocellulose market share in 2025 because papermakers and resin compounders are already set up for slurry handling. Nevertheless, new high-solids suspensions at 8–10 wt% enable lower shipping costs and direct incorporation into waterborne coatings. Suspension forms surge at a 22.10% CAGR as vacuum-degassed concentrates travel in intermediate bulk containers (IBCs) totes without settling for six months. Dry powder remains a technical curiosity for now, limited to controlled-release tablets and epoxy prepregs where moisture intolerance dictates anhydrous inputs.

Rheology control is the headline benefit: a 0.3% w/v nanocellulose suspension delivers yield stress values identical to 0.8% xanthan, letting paint makers lower formulation weight. Injectable biomedical hydrogels rely on nano suspensions that shear-thin under needle pressure but re-form a viscoelastic matrix in vivo. Foam forming lines test aerated suspensions that trap air for thermal-insulation panels, cutting panel density by 55%. As process equipment evolves, converters request bespoke particle size, zeta potential, and pH windows to fit dosing pumps. Producers answer by installing in-line homogenizers and UV-sterilization loops, fine-tuning suspension stability even as volumes exceed 5,000 tpa.

By End-use Industry: Pharmaceuticals Accelerate Beyond Composites

Composites captured 33.72% of the nanocellulose market size in 2025, riding on stricter fleet CO₂ limits that push automakers toward light yet tough structural parts. A 1 mm CNF-polypropylene skin trimmed 20 kg off a midsize sedan body-in-white, boosting fuel economy without compromising crashworthiness. Aerospace interiors follow suit; nanocellulose-filled phenolic panels pass 60-second vertical burn tests, essential for Federal Aviation Administration (FAA) qualification. Despite this scale, Pharmaceuticals and Cosmetics outpace all segments at 24.90% CAGR, powered by injectable gels for cartilage repair and nano-structured masks that lock in active ingredients while permitting skin breathability.

Paper processing remains a steady yet smaller revenue pillar as mills blend 1% NFC to raise recycled linerboard tensile strength by 97%. Paints and Coatings integrate <1% CNC to halt pigment sedimentation and raise scratch resistance in UV-curable lacquers. Oil and Gas drill fluid suppliers add nanocellulose to plug micro-fractures, reducing fluid loss and environmental harm; biodegradable fibers decompose in place, avoiding costly well clean-out . Food and Beverage brands experiment with CNF as a stabilizer in dairy alternatives and an oxygen barrier in flexible pouches once toxicology dossiers satisfy regulators. Each application cluster scales at its own pace, but collectively they cement the nanocellulose market as a cross-industry material platform.

Geography Analysis

North America leads the Nanocellulose market with a 43.25% revenue share in 2025, backed by early USDA and DOE grants that underwrote pilot lines and strong pull from automotive and aerospace original equipment manufacturers (OEMs). The region enjoys deeply integrated pulp-and-paper logistics, letting mills quickly pivot digesters toward cellulose nanofibrils without greenfield capital expenditure (CAPEX). Tier-1 suppliers collaborate with state universities to optimize automotive sheet-molding compounds that meet Insurance Institute for Highway Safety (IIHS) crash standards. Regulatory frameworks on sustainable packaging are less stringent than in the European Union (EU), yet brand commitments by big box retailers ensure stable offtake. As a result, the nanocellulose market size across North America remains the anchor against which global producers benchmark pricing.

Asia-Pacific records a 23.70% CAGR that challenges North America’s leadership by 2031. Japanese corporations commercialized cellulose nanofiber years ahead of rivals by repurposing depreciated paper machines, while Chinese start-ups deploy low-cost, high-pressure homogenizers built domestically to evade import duties. Electronics assemblers in Shenzhen specify nanocellulose barrier films to protect Organic Light Emitting Diode (OLED) modules from oxygen ingress, creating captive demand and shortening supplier qualification cycles. Agricultural residue abundance in India and Thailand cuts feedstock bills by 40%, and enzyme licensing deals accelerate adoption. Consequently, the Nanocellulose market attracts continuous plant announcements around ASEAN ports where export logistics converge.

Europe secures mid-teen growth on the back of the world’s strictest single-use-plastic bans. Converters in Belgium and the Nordics qualify Nanocellulose coatings to meet 95% paper recyclability thresholds. While higher energy prices squeeze margins, EU innovation grants de-risk pilot investments that showcase circular-bioeconomy leadership. South America, buoyed by sugarcane bagasse supplies, emerges as a low-cost export hub once CelOCE enzyme plants go commercial. Middle East and Africa start from a small base yet eye nanocellulose enhanced cement composites to curb desert construction dust, with multinational cement majors funding test pours near Gulf megaprojects. This geographic mosaic mirrors differing policy, resource, and industrial profiles, underpinning a balanced global growth picture for the nanocellulose market.

Competitive Landscape

The Nanocellulose market is moderately consolidated with the presence of players, such as Borregaard AS, NIPPON PAPER INDUSTRIES CO., LTD., Sappi Ltd., FiberLean, and CelluForce. Pulp majors such as Borregaard, CelluForce, and NIPPON PAPER INDUSTRIES CO., LTD. scale tonnage by upgrading idle sulfite lines to continuous nanofibril mills. Their tactic focuses on cost leadership and bulk supply to paper, packaging, and composite clients. Collaborations proliferate as scale and specialization rarely co-exist inside one firm. CelluForce licenses sulfur-free nanocrystal technology to European specialty-chemicals groups that blend it into anti-scratch coatings. Borregaard AS partners with packaging converter Elopak to co-develop recyclable liquid cartons, embedding a multi-year offtake that secures mill EBITDA.

Nanocellulose Industry Leaders

NIPPON PAPER INDUSTRIES CO., LTD.

CelluForce

FiberLean

Sappi Ltd.

Borregaard AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: UPM Biomedicals launched FibGel, a nanofibrillar cellulose hydrogel made from birch wood cellulose and water for permanent implantable medical devices.

- March 2024: Greenworksbio Products (GBPL) received process technology from CSIR-IICT to produce nanocellulose engineered starch granules for compostable plastics.

Global Nanocellulose Market Report Scope

Nanocellulose is a light solid substance obtained from plant matter and consists of nanosized cellulose fibers. Nanocellulose has excellent barrier properties, as nanofibers form a dense network held together by inter-fibril solid bonds.

The nanocellulose market is segmented by end-user industry, product type, and geography. By end-user industry, the market is segmented into paper processing, paints and coatings, oil and gas, food and beverage, composites, pharmaceutical and cosmetics, and other end-user industries (packaging, textiles, etc.). By product type, the market is segmented into nanofibrillated cellulose (NFC), nanocrystalline cellulose (NCC), bacterial cellulose, microfibrillated cellulose (MFC), and other product types (tempo oxidized nanocellulose, cellulose nanocomposites, etc.). The report also covers the market sizes and forecasts for the nano cellulose market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Nanofibrillated Cellulose (NFC) |

| Nanocrystalline Cellulose (NCC) |

| Bacterial Cellulose |

| Microfibrillated Cellulose (MFC) |

| Others |

| Wood Pulp |

| Agricultural Residues |

| Micro-algae & Other Bio-sources |

| Others |

| Dry (Powder) |

| Gel |

| Suspension |

| Paper Processing |

| Paints and Coatings |

| Oil and Gas |

| Food and Beverage |

| Composites |

| Pharmaceuticals and Cosmetics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Qatar | |

| Egypt | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Nanofibrillated Cellulose (NFC) | |

| Nanocrystalline Cellulose (NCC) | ||

| Bacterial Cellulose | ||

| Microfibrillated Cellulose (MFC) | ||

| Others | ||

| By Source | Wood Pulp | |

| Agricultural Residues | ||

| Micro-algae & Other Bio-sources | ||

| Others | ||

| By Form | Dry (Powder) | |

| Gel | ||

| Suspension | ||

| By End-use Industry | Paper Processing | |

| Paints and Coatings | ||

| Oil and Gas | ||

| Food and Beverage | ||

| Composites | ||

| Pharmaceuticals and Cosmetics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Nigeria | ||

| Qatar | ||

| Egypt | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the Nanocellulose market?

The Nanocellulose market size stands at USD 1.36 Billion in 2026 and is projected to reach USD 3.53 Billion by 2031.

Which region leads global demand?

North America holds the largest share at 43.25%, owing to early pilot adoption and strong automotive and aerospace pull.

Which segment is growing fastest?

Pharmaceuticals and Cosmetics applications are advancing at a 24.90% CAGR through 2031 due to injectable hydrogels and premium skincare films.

Why are agricultural residues gaining momentum as a feedstock?

Enzymatic breakthroughs now double conversion efficiency from residues such as sugarcane bagasse, lowering cost and aligning with circular-economy goals.

What is the biggest obstacle to wider adoption?

High production cost and scale-up risk remain the primary restraints, reducing competitiveness against commodity polymers until large-scale plants drive economies.

Page last updated on: