Hydrazine Hydrate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

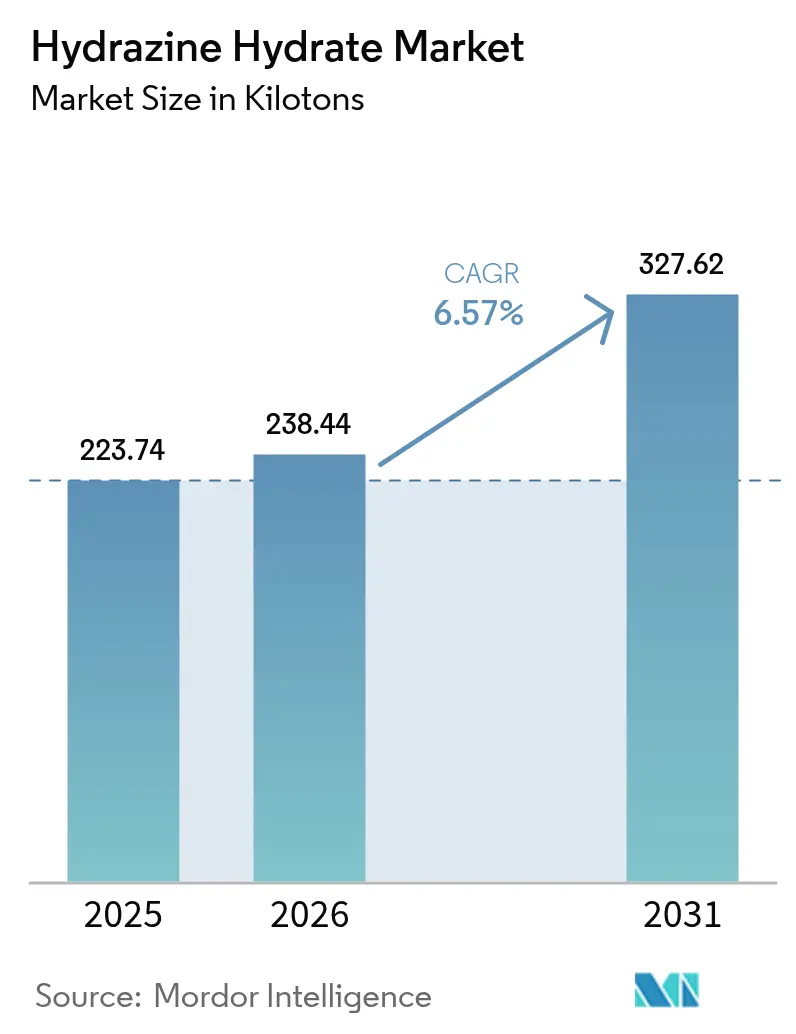

| Market Volume (2026) | 238.44 kilotons |

| Market Volume (2031) | 327.62 kilotons |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

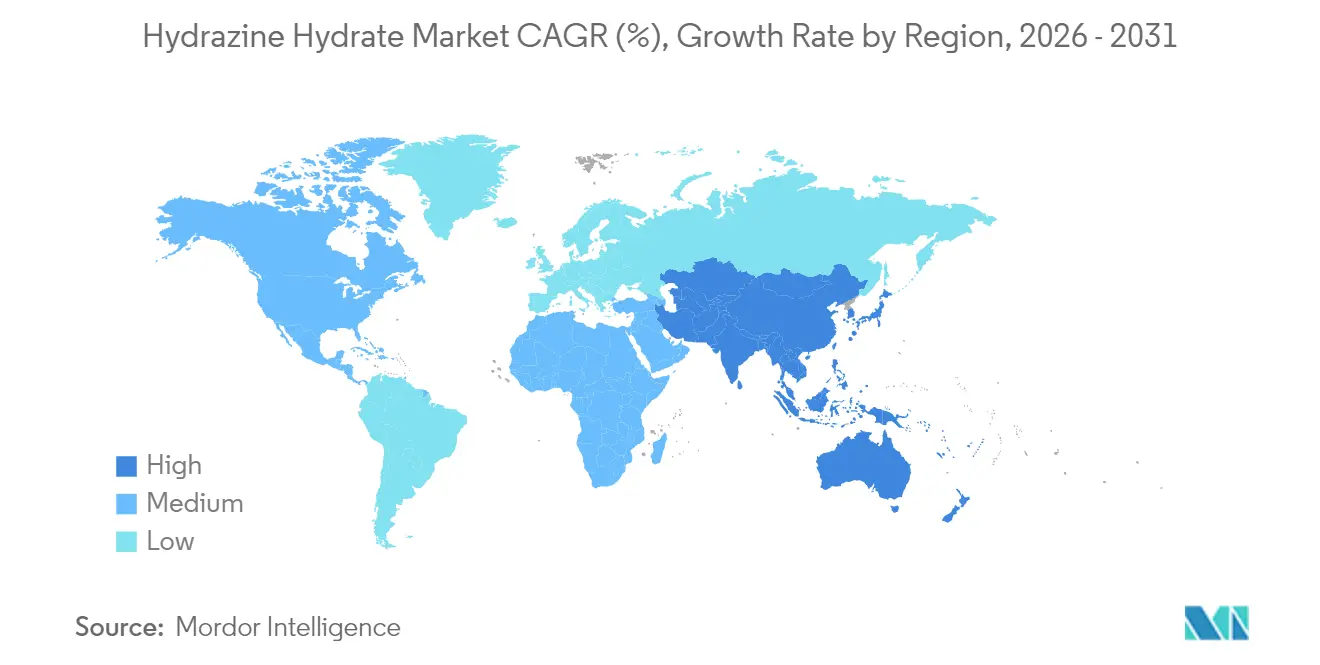

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

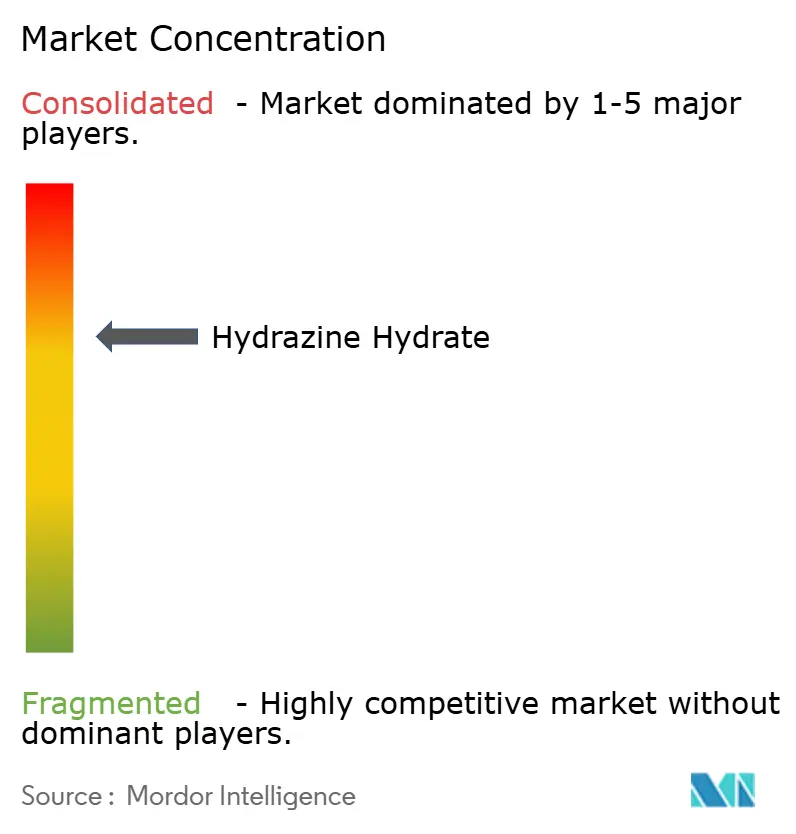

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrazine Hydrate Market Analysis by Mordor Intelligence

The Hydrazine Hydrate Market size was valued at 223.74 kilotons in 2025 and estimated to grow from 238.44 kilotons in 2026 to reach 327.62 kilotons by 2031, at a CAGR of 6.57% during the forecast period (2026-2031). Strong momentum comes from polymerization, blowing-agent use, expanding pharmaceutical API output, and first-generation deployments of direct hydrazine fuel cells. Process innovations—especially in the H₂O₂–ketazine route—continue to lower energy intensity and waste streams, improving cost positions for integrated producers. Growing demand for high-purity grades in aerospace and defense keeps margins firm even as mainstream industrial applications face tighter environmental scrutiny. Technology licensing, feedstock integration, and on-site hydrogen peroxide capacity are emerging as decisive competitive differentiators in the hydrazine hydrate market.

Key Report Takeaways

- By production process, the Bayer Ketazine Process led with 45.23% of hydrazine hydrate market share in 2025, while the H₂O₂–Ketazine Process is set to register the fastest 7.29% CAGR through 2031.

- By concentration, the 80–100% grade commanded 51.82% share of the hydrazine hydrate market size in 2025, and the 100% anhydrous category is poised to advance at a 7.36% CAGR between 2026 and 2031.

- By application, polymerization and blowing agents captured 42.10% revenue share in 2025; the “other applications” bucket—which includes rocket propellants and energy systems—shows the highest 7.68% CAGR outlook to 2031.

- By geography, Asia-Pacific retained 52.70% share of the hydrazine hydrate market in 2025 and is projected to expand at a 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrazine Hydrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from polymerization and blowing-agent manufacturers | +1.80% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Expanding pharmaceutical API production | +1.20% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Stricter global effluent norms boosting water-treatment usage | +0.90% | Global, particularly developed markets | Medium term (2-4 years) |

| Adoption of hydrazine-based corrosion inhibitors in stationary fuel cells | +0.70% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Process innovations lowering energy cost of H₂O₂-ketazine route | +0.60% | Global, led by technology leaders in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Polymerization and Blowing-Agent Manufacturers

Regulatory phase-outs of high-GWP hydrofluorocarbons have pushed polymer producers toward hydrazine-based chemical blowing agents, giving the hydrazine hydrate market sustained volume visibility. Demand is most vivid in rigid and flexible polyurethane foams used across building insulation and automotive lightweighting. Hydrazine’s dual role as chain extender and stabilizer trims formulation complexity and improves cell uniformity, which helps converters meet tighter energy-efficiency codes[1]Walter Brunner, “TEAP May 2024: Progress Report,” United Nations Environment Programme, ozone.unep.org . Foam makers adopting fourth-generation hydrofluoroolefins tend to retain hydrazine systems because processing windows overlap, curbing changeover costs. Bio-based polymer initiatives add another leg of demand as producers test renewable feedstocks compatible with hydrazine-mediated reactions.

Expanding Pharmaceutical API Production

National reshoring policies championed in the United States and Europe have triggered a wave of continuous-manufacturing investments that favor hydrazine hydrate’s flow-chemistry compatibility. The compound is central to synthesizing modified nucleosides and nucleotides now embedded in antiviral and oncology pipelines. China and India continue to scale multipurpose API blocks, reinforcing Asia-Pacific’s lead in the hydrazine hydrate market. Novel zero-background fluorescence probes allow real-time hydrazine detection inside reactors, sharpening quality control and minimizing batch failures. Long drug-development timelines anchor predictable offtake, insulating pharmaceutical demand from short-cycle swings in other end markets.

Stricter Global Effluent Norms Boosting Water-Treatment Usage

Power producers and process plants intensify boiler-feed conditioning programs as regulators tighten discharge limits on iron, copper, and residual dissolved oxygen. Hydrazine remains the most rapid oxygen scavenger available, forming harmless nitrogen and water while doubling as a pH buffer—a dual benefit that helps operators rationalize chemical inventories. Although non-toxic carbohydrazide and amine-based alternatives gain mindshare, many high-pressure systems continue using hydrazine because of proven kinetics under elevated temperature and pressure. Municipal utilities deploy it selectively in specialized polishing loops where full oxygen removal is critical for membrane protection.

Adoption of Hydrazine-Based Corrosion Inhibitors in Stationary Fuel Cells

Data-center backup, telecom towers, and remote microgrids are adopting direct hydrazine fuel cells for quiet, instant-start power. These units operate at room temperature, sidestepping bulky compressed-hydrogen storage and enabling simpler permitting. Catalyst breakthroughs have removed platinum, trimming stack costs and supporting broader commercial roll-out. Military applications require high-energy-density cartridges that rely on ultra-pure hydrazine, boosting margins for qualified suppliers. Parallel research on decoupled electrolysis positions hydrazine oxidation as a means to improve hydrogen production efficiency, creating additive demand streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent toxicity and transport regulations | -1.40% | Global, particularly EU and North America | Short term (≤ 2 years) |

| High insurance / handling costs due to explosion risk | -0.80% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Feed-stock shortages of high-grade H₂O₂ in Asia | -0.60% | Asia-Pacific core, spill-over to global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Toxicity and Transport Regulations

Hydrazine’s listing as a substance of very high concern under EU REACH forces producers and users into costly authorization dossiers and drives R&D into safer analogues. Shipping is equally complex: United Nations Model Regulations classify hydrazine as a Class 8 corrosive and Class 3 flammable liquid, obliging insulated, pressure-rated containers and certified handlers. The United States harmonized domestic rules with updated international standards in 2024, prompting relabeling and extra training across the supply chain[2]U.S. Department of Transportation, “Hazardous Materials: Harmonization with International Standards,” federalregister.gov . Aerospace primes lobby for extended use exemptions, but alternative propellant programs backed by EUR 1.4 million in EU funding signal political intent to phase down hydrazine over the long run.

High Insurance and Handling Costs Due to Explosion Risk

Recent plant incidents have pushed insurers to recalibrate loss-expectancy models, inflating premiums for facilities storing more than 10 tons of hydrazine. Operators must add blast-resistant walls, advanced gas-detection arrays, and redundant inert-gas purging—all of which inflate capital outlays. Thermo-reversible gels under evaluation can immobilize hydrazine for transit, but commercial adoption hinges on cost-benefit proof in bulk logistics. Smaller formulators increasingly outsource hydrazine-based processing steps to toll manufacturers with specialized infrastructure, consolidating demand among fewer, larger players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Ketazine Routes Drive Efficiency Revolution

The Bayer Ketazine Process retained a commanding 45.23% hydrazine hydrate market share in 2025 because of long-established global capacity networks and robust catalyst know-how. H₂O₂–ketazine lines, while newer, are adding units at a brisk 7.29% CAGR, underpinned by lower energy intensity and simplified waste treatment.

Plant debottlenecking strategies now involve membrane-based ketazine purification that recovers solvent and drives overall plant capacity without major plot-space additions. Licensing houses bundle digital twins with process packages, allowing real-time energy optimization and predictive maintenance. OEMs supplying titanium reactors report rising backlogs as Asia-Pacific customers race to meet local content rules and avoid import exposure. These dynamics keep the hydrazine hydrate market on an innovation trajectory that rewards energy-efficient flowsheets.

By Concentration: Anhydrous Grade Captures Premium Applications

High-concentration streams (80–100%) represented 51.82% of demand in 2025 as customers favor lower shipping weight and extended shelf life. Within this band, 100% anhydrous hydrazine is forecast to grow 7.36% annually to 2031, lifted by rocket-propellant blending and advanced sensor-cleaning formulations. The hydrazine hydrate market size for lower-grade 55–80% solutions remains steady in water-treatment circuits where on-site dilution aligns with dosing equipment.

Membrane pervaporation coupled with vacuum distillation allows single-pass upgrading from 80% to 100% purity, slashing steam use and lowering greenhouse-gas footprints. Aerospace buyers, now bound by stringent propellant purity specs from space-agency audits, lock in multiyear contracts that provide volume visibility to specialty producers. Meanwhile, semiconductor fabs test ultra-dry hydrazine for surface passivation, a niche that could further reinforce anhydrous demand by the decade’s end.

By Application: Energy Sector Disrupts Traditional Demand Patterns

Polymerization and blowing-agent applications dominated 42.10% of volume in 2025, anchored by insulation demand and light-weighting initiatives in transportation. Yet the “other applications” category—covering propellants, fuel cells, and decoupled electrolysis—outpaces every segment with an 7.68% CAGR, underscoring diversification within the hydrazine hydrate market. Pharmaceutical intermediates hold mid-single-digit growth as mRNA derivative pipelines standardize hydrazine‐enabled synthesis routes.

Direct hydrazine fuel cells show round-trip efficiencies competitive with lithium-ion storage when waste-heat recovery is integrated, prompting telecom and data-center pilots. Ag-chem players face tightening residue limits that crimp hydrazine-based growth regulator volumes, yet specialty herbicide niches still rely on its unique functional profile where no drop-in replacements exist. This diversification insulates the hydrazine hydrate industry from single-segment downturns and sustains broad-based investment appetite.

Geography Analysis

Asia-Pacific anchored 52.70% of global consumption in 2025, reflecting deep vertical integration from upstream hydrogen peroxide to downstream polymer foam converters. China holds a significant share of the world's installed capacity and continues to add H₂O₂–ketazine lines, although recent feedstock outages reminded buyers of latent supply-chain fragility. India’s production-linked incentives for APIs are catalyzing brownfield expansions that could lift national demand by 30 kilo tons before 2030. Japan maintains a niche leadership in high-purity grades for fuel-cell and semiconductor use, leveraging proprietary metallurgy for hydrazine handling systems.

North America demonstrates significant growth, driven by defense-grade propellant offtake, domestic API reshoring, and early-stage stationary fuel-cell rollouts. Federal grants for microgrid resilience include funding carve-outs for direct hydrazine technology testbeds, potentially deepening demand if cost targets are met. Canada’s specialty chemical hubs in Ontario and Quebec source hydrazine hydrate under long-term contracts, insuring against cross-border transport constraints tightened in 2024.

Europe represents a mixed picture: REACH authorization costs and SVHC status raise compliance barriers, nudging some downstream users toward alternative chemistries, yet aerospace and advanced materials firms secure exemptions to prevent supply disruptions. Continental producers invest in green-hydrogen-linked hydrogen peroxide electrolyzers to decarbonize feedstocks, positioning for premium pricing once scope-3 reporting becomes mandatory. Together, these dynamics keep the hydrazine hydrate market firmly global while spotlighting regional regulatory divergence as a structural determinant of trade flows.

Competitive Landscape

The hydrazine hydrate market exhibits moderately consolidated concentration: the five largest players collectively control around 61% of global capacity. Integrated producers spanning hydrogen peroxide, ketazine intermediates, and downstream formulations command cost and quality advantages that smaller formulators struggle to match.

Leading incumbents prioritize vertical integration and geographic diversification to cushion against regional transport restrictions and insurance cost spikes. Capital budgets favor H₂O₂–ketazine retrofits, effluent-reduction units, and high-purity isolation trains. Technology partnerships with membrane vendors and advanced analytics firms aim to unlock incremental yield gains and energy savings that translate directly into margin uplift.

Policy uncertainty around future toxicity classifications incentivizes parallel R&D tracks: while legacy hydrazine lines secure REACH authorization, companies explore ammonium dinitramide, nitrous oxide, and hydroxylammonium nitrate as next-generation propellants. Those holding process patents for hydrazine hydrate also license know-how to emerging-market entrants—both extending revenue streams and tightening global supply discipline.

Hydrazine Hydrate Industry Leaders

Arkema

LANXESS

Lonza

Otsuka Chemical Co.,Ltd.

Yibin Tianyuan Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: LANXESS showcased its extensive product portfolio and industry expertise at Chemspec Europe 2025. Represented by six business units, the company featured products such as hydrazine hydrate, which is part of its portfolio of industrial intermediates, chemical base materials, and fine chemicals.

- July 2023: Gujarat Alkalies and Chemicals Limited (GACL) has successfully commenced the production of the first batch of Hydrazine Hydrate with an 80% concentration. In 2022, the company invested approximately INR 405 Crores to establish a commercial-scale plant in Dahej, which is designed to produce 10,000 MTA of the product.

Global Hydrazine Hydrate Market Report Scope

Hydrazine hydrate is an oxygen scavenger for water used in high-pressure steam generators and industrial boilers. It is used to produce agricultural chemicals, pharmaceuticals, and blowing agents. It can be used as food additives, polymerization catalysts, soldering fluxes, and in manufacturing detergents, surfactants, and plasticizers. The hydrazine hydrate market is segmented by application and geography. Based on application, the market is segmented into pharmaceuticals, polymerization and blowing agents, agrochemicals, water treatment, and other applications. The report also covers the market sizes and forecasts for the hydrazine hydrate market in 15 countries across major regions. The market sizing and forecasts are based on each segment's value (USD million).

| Raschig Process |

| Bayer Ketazine Process |

| Urea Process |

| H₂O₂–Ketazine Process |

| Less than 55% |

| 55–80% |

| 80–100% |

| 100% (Anhydrous) |

| Polymerization and Blowing Agents |

| Pharmaceuticals |

| Agrochemicals |

| Water Treatment |

| Other Applications (Rocket Propellants and Energy, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Production Process | Raschig Process | |

| Bayer Ketazine Process | ||

| Urea Process | ||

| H₂O₂–Ketazine Process | ||

| By Concentration | Less than 55% | |

| 55–80% | ||

| 80–100% | ||

| 100% (Anhydrous) | ||

| By Application | Polymerization and Blowing Agents | |

| Pharmaceuticals | ||

| Agrochemicals | ||

| Water Treatment | ||

| Other Applications (Rocket Propellants and Energy, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current hydrazine hydrate market size and its growth outlook?

The hydrazine hydrate market size is 238.44 kilo tons in 2026 and is projected to reach 327.62 kilo tons by 2031, reflecting a 6.57% CAGR.

Which region leads global consumption of hydrazine hydrate?

Asia-Pacific dominates with 52.70% share and is also the fastest-growing region at a 7.18% CAGR through 2031.

Why is the H₂O₂–ketazine process gaining popularity?

It reduces hot-utility demand by nearly 67%, lowers effluent loads, and aligns with green-hydrogen-peroxide feedstocks, making it the most energy-efficient production route.

How do regulatory changes in Europe affect hydrazine hydrate demand?

EU REACH classification as an SVHC raises authorization costs and encourages research into safer propellants, but aerospace and defense exemptions keep essential demand intact.

What drives the surge in high-purity anhydrous hydrazine?

Growing rocket-propellant needs, semiconductor cleaning, and premium fuel-cell cartridges require 100% purity grades, pushing this sub-segment to a 7.36% CAGR.

How concentrated is the competitive landscape?

The market is moderately consolidated with the top five suppliers controlling around 61% of capacity.

Page last updated on: