Honeycomb Core Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.73 Billion |

| Market Size (2031) | USD 7.30 Billion |

| Growth Rate (2026 - 2031) | 9.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Honeycomb Core Materials Market Analysis by Mordor Intelligence

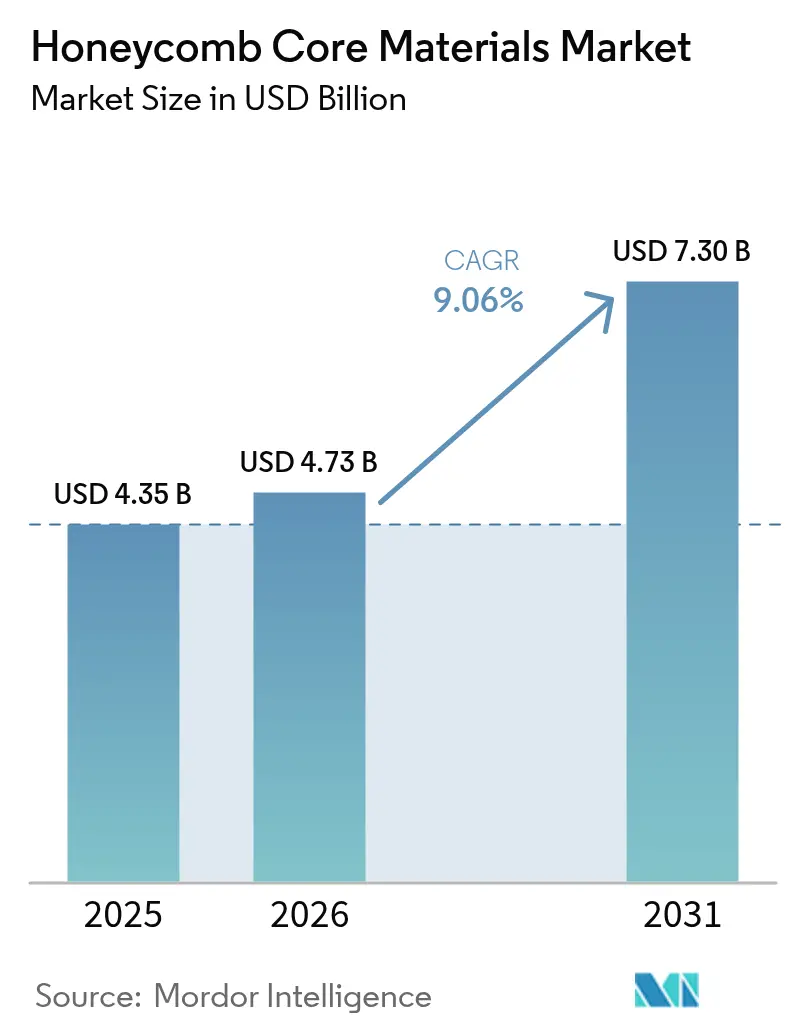

The Honeycomb Core Materials Market size is expected to grow from USD 4.35 billion in 2025 to USD 4.73 billion in 2026 and is forecast to reach USD 7.30 billion by 2031 at 9.06% CAGR over 2026-2031. Rising output of single-aisle jets, expanding fleets of high-speed trains, and the migration of electric-vehicle battery enclosures to thermoplastic cores are the primary growth engines for the Honeycomb core materials market. Increased use of composite sandwich panels in hypersonic prototypes further lifts demand, while weight-reduction mandates in rail and automotive add a steady pull. The supply base continues to consolidate around qualified aerospace vendors, yet new entrants using recycled polyolefins and additive manufacturing are broadening material choices. Suppliers able to guarantee moisture resistance, recycle-ready chemistries, and short lead times are best positioned to capture incremental Honeycomb core materials market opportunities.

Key Report Takeaways

- By product type, aluminum cores led with 38.28% of the Honeycomb core materials market share in 2025, while thermoplastic cores are poised to expand at a 10.98% CAGR to 2031.

- By end-user, aerospace dominated with a 62.89% share in 2025; the other end-user industries segment is the fastest, rising at an 11.27% CAGR to 2031.

- By manufacturing technology, expansion processes captured 55.32% revenue in 2025, whereas 3D printing is forecast to advance at an 11.69% CAGR over 2026-2031.

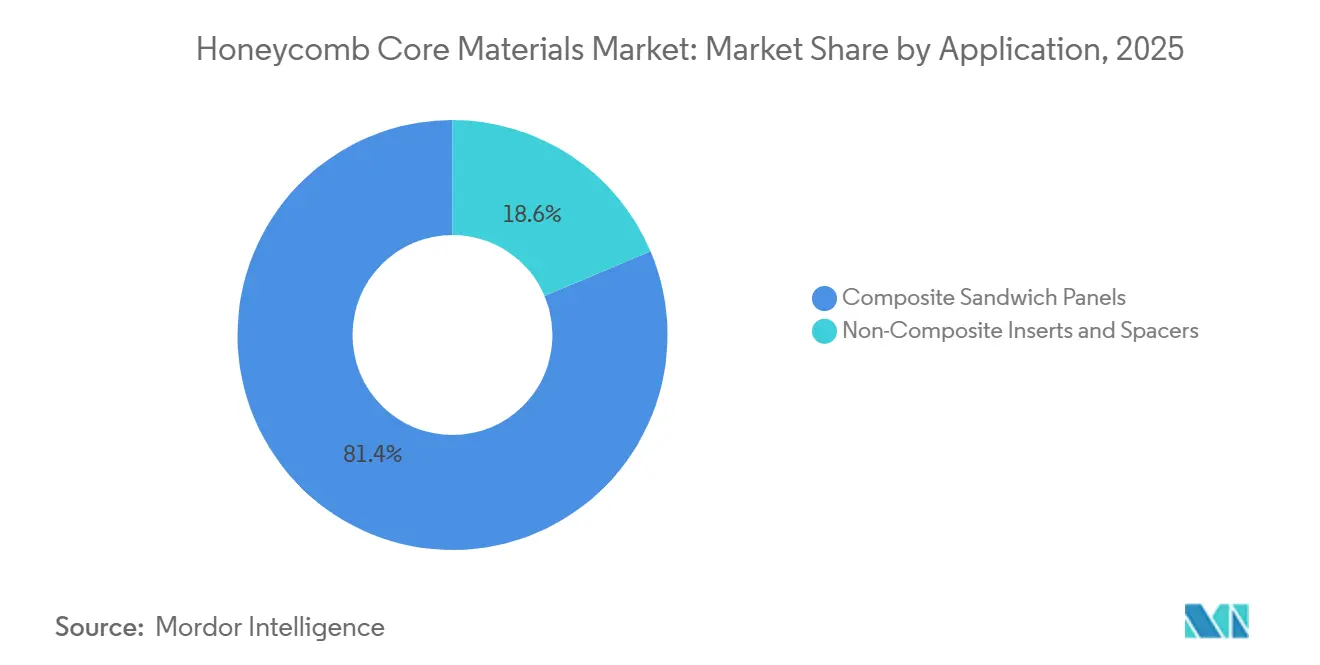

- By application, composite sandwich panels accounted for 81.37% of the Honeycomb core materials market size in 2025 and are projected to grow at an 11.85% CAGR through 2031.

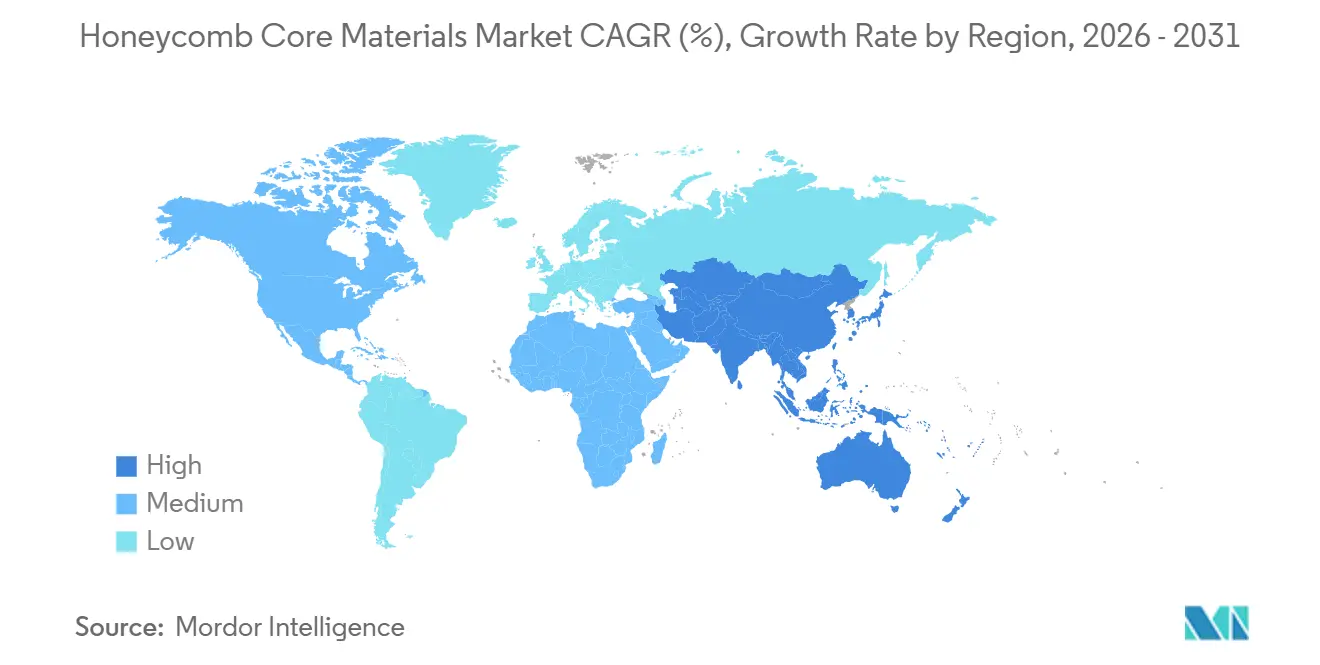

- By geography, North America commanded 35.21% revenue in 2025, while Asia-Pacific is projected to register the quickest 11.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Honeycomb Core Materials Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for lightweighting in next-gen single-aisle aircraft | +2.3% | Global, concentrated in North America and Europe (Airbus, Boeing final assembly) | Medium term (2-4 years) |

| Shift to composite sandwich panels in airframes | +2.1% | Global, with Asia-Pacific spill-over as COMAC/KAI expand composite adoption | Medium term (2-4 years) |

| Weight-reduction mandates in inter-city high-speed rail coaches | +1.8% | Asia-Pacific core (China, Japan, South Korea), Europe secondary | Short term (≤ 2 years) |

| Adoption of polypropylene cores in EV battery enclosures | +1.5% | Global, early gains in China, Germany, United States | Medium term (2-4 years) |

| Defense push for high-temperature super-alloy honeycomb in hypersonics | +1.2% | North America and select Asia-Pacific (U.S., China classified programs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Lightweighting in Next-Gen Single-Aisle Aircraft

In 2025, A320neo production hit record monthly rates, driving up demand for aluminum and Nomex cores used in floor panels and interior partitions. Boeing's adoption of generative-design partitions slashed panel weight, boosting the value of each installed core without adding mass. Japanese suppliers dominate the scene, providing the world's carbon fiber and solidifying their role in the feedstock chain for composite-heavy airframes. Hexcel's decision to double its Moroccan capacity, positioning it closer to Airbus's final assembly lines, underscores the industry's emphasis on localization to mitigate logistics risks. These developments collectively suggest a stable demand for honeycomb core materials in the single-aisle segment over the next few years.

Shift to Composite Sandwich Panels in Airframes

OEMs are shifting sandwich construction from secondary fairings to load-bearing ribs and frames, raising the bar for core compression strength. Hexcel’s HRH-302 mid-temperature core, now qualified for the MQ-25 program, opens up nacelle and hot-zone applications that aluminum cannot fulfill. Toray's new 400 °C press enables simultaneous co-curing of PEEK organosheets and honeycomb, reducing both scrap and labor. To counter intensified thermal gradients from quicker cure cycles, suppliers are now providing graded-density cores that prevent crushing during autoclave ramps. In the Honeycomb core materials market, price premiums on mid-temperature grades are balancing out the increased costs of resin and energy, thus safeguarding profit margins.

Weight-Reduction Mandates in Inter-City High-Speed Rail Coaches

Chinese operators have reduced coach floor mass by replacing steel with honeycomb-cored panels, successfully adhering to stringent kWh-per-seat-kilometer regulations. Traction energy decreases with weight savings, ensuring swift returns on investment. In Europe, builders are being directed by EN 45545 fire standards to opt for phenolic and aramid cores due to their reduced smoke toxicity. Meanwhile, Japan's N700S trains are experimenting with thermoplastic sandwich panels to counterbalance battery weight in their hybrid models. While honeycomb panels used in rail applications can withstand greater lateral impacts than their aerospace counterparts, the thicker cell walls, though more expensive, still surpass energy efficiency benchmarks.

Adoption of Polypropylene Cores in EV Battery Enclosures

Polypropylene cores absorb minimal moisture compared to balsa or plywood, significantly extending the durability of battery packs. Additionally, polypropylene enhances vibration damping, safeguarding electrical interconnects on bumpy roads. EconCore has ramped up its ThermHex output to support auto lines producing high volumes annually. With structural packs gaining traction, core usage per car is expected to increase by the decade's close. As these designs gain traction, the honeycomb core materials market is poised for a steady automotive boost.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Moisture ingress and out-of-plane strength loss | -1.4% | Global, acute in marine and outdoor applications | Short term (≤ 2 years) |

| Persistent price volatility in aramid-paper supply chain | -1.1% | Global, concentrated impact in North America and Europe (Nomex production hubs) | Medium term (2-4 years) |

| Limited large-format 3D-printing capacity for complex cores | -0.8% | Global, bottleneck in North America and Europe research and development centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Moisture Ingress and Out-of-Plane Strength Loss

High humidity exposure can significantly reduce core energy absorption and instigate corrosion at bond lines. While barrier films and closed-cell coatings mitigate these risks, they also inflate costs and decelerate throughput. Marine panels, despite enduring the harshest conditions, are still mandated by IMO rules to use honeycomb, incurring additional protection expenses. Hygric testing can prolong certification, immobilizing capital for both OEMs and suppliers. The Honeycomb core materials market grapples with the challenge of balancing durability and speed to market.

Persistent Price Volatility in Aramid-Paper Supply Chain

With only two global producers catering to aerospace grades, Nomex paper commands a variable price range[1]U.S. Government Accountability Office, “Critical Materials: Action Needed to Implement Requirements That Reduce Supply Chain Risks,” gao.gov . Given that capacity additions require a 3-5 year qualification period, any outage leads to a surge in spot prices. Integrated fabricators benefit from long contracts, enhancing their cost advantage over independent players. This volatility also influences decisions, prompting tier-one companies to internalize honeycomb production during price surges. Furthermore, the reliance on tungsten-tooling supply upstream presents an additional risk, one that remains largely unaccounted for in most cost models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Thermoplastics Challenge Aluminum Incumbency

Aluminum cores held a 38.28% Honeycomb core materials market share in 2025, firmly establishing their dominance in aerospace interiors and control surfaces. Meanwhile, thermoplastic polypropylene cores are forecast to post a 10.98% CAGR, thanks to their moisture uptake and recyclability benefits. Super-alloy cores carve out a specialized niche for hypersonic applications, while paper cores cater to the demand for cost-effective packaging.

Polypropylene's unique property allows it to fuse in situ with PEKK face sheets, eliminating adhesive lines that can trap moisture. EconCore’s ThermHex line has achieved scale economies that compete with traditional expansion methods, particularly for automotive volumes. In Colorado, Toray’s expansion of thermoplastic tape paves the way for co-consolidated rail panels, designed for recyclability at the end of their lifecycle. With OEMs increasingly emphasizing circularity, the penetration of thermoplastics is on the rise, signaling a gradual reduction in aluminum's lead in the honeycomb core materials market.

By End-User Industry: Diversification Beyond Aerospace Concentration

Aerospace contributed 62.89% of the 2025 demand, anchoring the Honeycomb core materials market size, yet other industries are set to expand 11.27% annually as cost curves fall. Rail coaches, marine bulkheads, and EV battery enclosures now justify sandwich panels on total-cost savings alone.

Both the packaging and construction sectors are eyeing paper and thermoplastic cores, seeking cost-effective options. In China and Europe, rail mandates are pushing for floor and roof substitutions, achieving energy paybacks in just two years. Marine builders, prioritizing IMO fire compliance, are opting for higher densities and accepting margin premiums. Meanwhile, defense programs, though sporadic, are offering lucrative contracts for super-alloy cores. Collectively, these trends are reducing the industry's reliance on aerospace, diversifying the revenue streams of the Honeycomb core materials market.

By Manufacturing Technology: Additive Methods Disrupt Expansion Dominance

In 2025, expansion processes accounted for a 55.32% share of sales, leveraging decades of FAA data to deliver substantial output per shift. While 3D printing currently holds a minor share, it's set to expand at an 11.69% annual rate, driven by DIW's carbon-fiber epoxy cores boasting impressive energy absorption rates.

Additive methods eliminate tooling lead times, which can stretch significantly and incur high costs for intricate parts. Graded honeycomb, used in a 2.8 m blade, achieved a notable weight reduction compared to uniform cores, all while maintaining stiffness[2]S.I. Molina et al., “Large-format additive manufacturing of polymer extrusion-based systems,” Progress in Additive Manufacturing, springer.com . Extrusion and lamination lines, like ThermHex, now reach substantial output levels, aligning with expansion economics for automotive production. As OEMs accelerate their iterations, the influence of additives will grow, yet expansion processes are poised to remain the cornerstone of the Honeycomb core materials market through 2031.

By Application: Sandwich Panels Dominate Structural Use Cases

Composite sandwich panels represented 81.37% of the Honeycomb core materials market size in 2025 and should climb at an 11.85% CAGR to 2031. Panels combine high bending rigidity with low mass, making them indispensable for aircraft floors, rail roofs, and marine bulkheads.

Innovative core technologies adeptly mitigate jet noise without adding weight, showcasing the evolution of panels into multifunctional systems. Meanwhile, advanced press technology enables simultaneous co-curing of thicker cores and thinner face sheets, achieving a notable reduction in labor. Designers are increasingly opting for thicker cores paired with lighter face sheets to enhance stiffness. However, this strategy introduces a heightened risk of crush during handling, subsequently driving the demand for higher-density grades in critical load paths. While inserts and spacers command a niche segment, holding a smaller share of the honeycomb core materials market, their growth is expected to lag behind panels. This is largely due to OEMs' shift towards redesigning joints for co-cure construction.

Geography Analysis

North America controlled 35.21% of revenue in 2025 due to deep aerospace supply chains and classified hypersonic funding. Hexcel’s Moroccan plant, supplying Airbus, will staff workers by late 2026. The U.S. FY 2023 budget earmarked significant amounts for hypersonic research and development, underpinning demand for super-alloy cores. Canada and Mexico add incremental growth through automotive and industrial assemblies.

Asia-Pacific is forecast to expand at an 11.10% CAGR, the quickest regional pace. China’s high-speed rail weight rules drove floor mass cuts in CRH5 coaches, sharply boosting core consumption. Japan supplies the majority of global carbon fiber, cementing its role in composite supply. South Korea, India, and ASEAN nations are localizing honeycomb fabrication for fighter and rail programs. Domestic Chinese suppliers are reverse-engineering Inconel cores, but certification lags imported grades by several years.

Europe maintains a substantial share of Airbus output and EN 45545 rail standards that favor phenolic and aramid cores. However, higher energy and compliance costs trim competitiveness. German automakers test polypropylene cores in EV packs to reach 25% recycled content by 2028. Nordic shipyards buy moisture-resistant cores for cold-water yachts. South America and the Middle East remain small today, yet projects like Saudi Arabia’s NEOM and Embraer’s supply chain could open localized Honeycomb core materials market pockets.

Value Chain Analysis

The honeycomb core materials value chain starts with upstream feedstocks such as aluminum foil, aramid paper (aerospace grades), recycled paper (high-test liner and kraft paper for paper honeycomb in the EU), and thermoplastic resins (including high-performance grades used for transportation and e-mobility). These inputs move into core formation and conversion steps, mainly expansion and corrugation for metallic and aramid cores, and extrusion and lamination or continuous processes for thermoplastic cores. The flow then continues through coating and barrier treatments, cutting and kitting, and qualification testing for demanding end uses such as aerospace interiors, rail coach panels, marine structures, and EV battery enclosures. Qualification lead times for aerospace-grade materials and the limited number of aerospace-grade aramid paper producers remain a bottleneck, which can amplify volatility when capacity is tight.

Midstream, engineered core suppliers and panel fabricators integrate adhesive films, skins, and protective layers to build sandwich structures, then distribute through direct OEM and tier supply chains and specialized composites distributors. Collaboration with adhesive and resin suppliers is increasingly visible in high-growth thermoplastic structures and FST-compliant panels. In May 2025, Kiilto announced development of a tailored polyurethane adhesive used by Potma for aluminum honeycomb structures in shipbuilding and rail, while thermoplastic honeycomb development commonly pairs material providers (for example, SABIC, Covestro, Toray) with process technology firms (for example, EconCore) to meet FST requirements. Downstream demand is concentrated among aerospace OEMs and certified tier suppliers, while automotive and mass transportation programs rely more on scalable, energy-efficient continuous manufacturing routes that reduce conversion cost and shorten lead times.

Competitive Landscape

The honeycomb core materials market is moderately fragmented. EconCore’s recycled-PET cores meet auto circularity targets yet await aerospace sign-off, giving incumbents a window to counter. Additive specialists backed by ORNL demonstrate tooling-free core production, but throughput confines them to prototypes for the decade. Smaller firms compete on niche grades yet lack the capex muscle for full aerospace qualification. Players that secure aramid supply, localize near OEM lines, and co-develop recyclable systems will defend or grow Honeycomb core materials market positions.

Honeycomb Core Materials Industry Leaders

Hexcel Corporation

Plascore

Euro-Composites

Corex Honeycomb

The Gill Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A gap is emerging around recyclable and thermoplastic honeycomb cores that can meet fire, smoke, and toxicity requirements for mass transportation and selected aerospace interior applications, while also addressing moisture-ingress constraints that limit uptake in marine and outdoor exposure. Activity in the segment is supporting this shift from development to commercialization. Partnerships that link process technology with material and adhesive suppliers, such as EconCore with partners including Toray and Bostik on FST-certified thermoplastic honeycomb panels, point to qualification and system-level performance, rather than core geometry alone, as the commercialization gate.

Capacity and localization initiatives are also widening competitive options beyond the traditional aerospace-qualified supply base. In April 2026, HolyCore (Zhejiang Huaju Composite Materials Co., Ltd.) opened its QingShan Lake manufacturing base in Hangzhou, China, with 12 honeycomb core production lines and stated annual capacity of 5 million square meters of thermoplastic panels and 1 million square meters of thermoset composite panels. This reinforces Asia-Pacific as a manufacturing center for transportation panels and industrial sandwich structures. On the process side, continuous, energy-efficient honeycomb production approaches are being positioned as a cost lever for automotive-scale demand, consistent with the report's emphasis on polypropylene cores in EV battery enclosures. Separately, research into cell-wall geometry, graded structures, and advanced carbon-based honeycombs targets higher-temperature and improved dimensional stability in applications where conventional aluminum or aramid solutions face performance ceilings.

Recent Industry Developments

- June 2026: Hexcel announced a long-term industrial partnership and supply agreement with Deutsche Aircraft to support the D328eco regional aircraft program with advanced composite solutions, including honeycomb products. The agreement ties qualified core supply more closely to an aircraft production ramp and supports continuity in certified materials for interior and structural sandwich applications.

- September 2025: Schuetz Group announced the acquisition of Euro-Composites S.A., expanding its global composites footprint and technical capabilities. The deal adds scale and integration around composite structures and panels, influencing procurement options for honeycomb-based sandwich construction in transportation and industrial end uses.

- December 2024: Hexcel partnered with Boeing to test Flex-Core HRH-302 honeycomb for the MQ-25 Stingray unmanned tanker program. The program-level evaluation highlights ongoing qualification work for higher-temperature and higher-performance honeycomb cores in defense aerospace applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers honeycomb core materials sold as lightweight core structures used inside sandwich panels or as cores in engineered parts, where pricing is captured at the material supply level in USD.

Scope exclusions: finished end products where the core is embedded and cannot be separated as a sold core material value, along with services such as design consulting and installation.

Segmentation Overview

- By Product Type

- Nomen

- Aluminum

- Thermoplastic

- Other Product Types (Paper, Super-alloy)

- By End-user Industry

- Aerospace

- Defense

- Marine

- Other End-user Industries (Transportation, Packaging, etc.)

- By Manufacturing Technology

- Expansion

- Corrugation

- Extrusion/Lamination

- 3-D Printing/Additive Core Building

- By Application

- Composite Sandwich Panels

- Non-Composite Inserts and Spacers

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where honeycomb core materials are used and how demand shows up in real-world data. We rely on public sources such as the US Census Bureau and US International Trade Commission trade statistics, FAA and EASA aircraft and safety publications, and defense and aerospace budget documents where available.

To keep assumptions grounded, we also review customs and tariff schedules, technical papers from peer-reviewed materials and composites journals, and trade association releases related to composites and lightweight structures. On the supply side, company annual reports, investor presentations, and product catalogs are used to understand typical product mix and the stated end-use exposure. Select paid subscriptions for company financials and for patent databases are also referenced to cross-check scale signals and innovation activity. This list is illustrative, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to convert the desk view into practical sizing inputs, especially where public data is not granular enough. We speak with material suppliers, converters, panel fabricators, distributors, and procurement and engineering roles at end users across aerospace, defense, marine, and industrial applications. Coverage includes APAC, EMEA, and the Americas so regional demand patterns are not overgeneralized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 52% |

| Mid tier: 53% | Functional/Unit leaders: 32% | EMEA: 29% |

| Smaller Players: 20% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where aerospace build rates, composites and sandwich-panel adoption, and trade-linked supply movement are used to reconstruct the demand pool, and then it is converted into value using typical price bands by core material family. Because these indicators do not perfectly show mix changes, the output is corroborated with selective bottom-up approximations, such as checks on sample supplier revenue splits, channel feedback on volumes, and sampled ASP multiplied by estimated consumption.

Key inputs tracked (illustrative) include aircraft production and deliveries, fleet retrofit activity that drives interior panels, defense procurement cadence for lightweight structures, share shifts between aluminum and non-metal cores, and manufacturing route adoption where it affects yield and pricing. When a bottom-up view has gaps for smaller countries or fragmented industrial uses, we use proxy penetration rates tied to manufacturing output and then adjust with interview-led sanity checks.

Forecasting uses scenario analysis supported by trend lines from aircraft and defense build plans, and then refined through expert views on price progression, substitution risk, and capacity additions. A simple regression-style sensitivity is also applied to test how strongly demand follows aircraft output and industrial production before the final trajectory is locked.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as reported end-market production levels, trade flows, and observed price ranges, and then the biggest variances are flagged for a second review. If a region or material type moves outside a realistic band, the assumptions are revisited, and follow-up questions are sent back to industry contacts when needed.

Before sign-off, calculations are reviewed in multiple steps so unit conversions, currency treatment, and time alignment are consistent across regions. The report is refreshed each year, and interim updates are made when material events occur, such as major capacity changes or sharp shifts in aerospace build schedules. Right before delivery, there is a final pass to ensure the latest public data and market signals are reflected.

Mordor Intelligence's Honeycomb Core Materials Market Size Compared With Other Published Estimates

Published market sizes for honeycomb core materials can look far apart even when they refer to the same end uses. The gaps usually come from what is counted as a core material sale, how end markets are mapped into demand drivers, and whether pricing is treated as a stable average or adjusted year by year.

By tracking demand signals like aircraft production and defense procurement and refreshing scope boundaries in the way Mordor Intelligence counts core-only revenues (instead of finished sandwich panel values), the estimate avoids double counting that can inflate totals when downstream panel and part values get mixed into the same number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.35 B (2025) | |

| Global Research Publisher A | USD 3.81 B (2025) | Uses a different base-year anchor and growth curve, and the scope description suggests a broader mix of applications where some downstream components may be blended with core material revenues. |

| Industry Publisher B | USD 3.50 B (2025) | Treats 2025 as the base and applies a smoother CAGR path with limited visibility on how material mix, yield, and price bands are updated, which can pull the starting value down. |

The comparison shows that most of the spread is explained by scope boundaries and how pricing and mix are refreshed over time. When the demand pool is tied back to observable end-market activity and the counted value stays at the core-material level, the resulting number is easier to replicate and update as conditions change.

Key Questions Answered in the Report

How large is the Honeycomb core materials market in 2026?

The Honeycomb core materials market size is projected at USD 4.73 billion in 2026, reaching USD 7.30 billion in 2031, registering a CAGR of 9.06%.

Which region will grow the fastest through 2031?

Asia-Pacific is forecast to register an 11.10% CAGR, the highest among all regions.

What segment holds the biggest Honeycomb core materials market share today?

Composite sandwich panels lead with 81.37% of 2025 revenue.

Why are thermoplastic cores gaining traction?

Polypropylene and rPET cores offer low moisture uptake, recyclability, and cost parity at automotive scales.

How is additive manufacturing impacting core supply?

3D printing cuts tooling time from months to weeks, enabling rapid prototypes, though throughput still limits large-volume production.

What is driving defense demand for honeycomb cores?

Hypersonic programs need super-alloy cores that survive temperatures above 650 °C, sustaining a niche but high-value stream.

Page last updated on: