Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

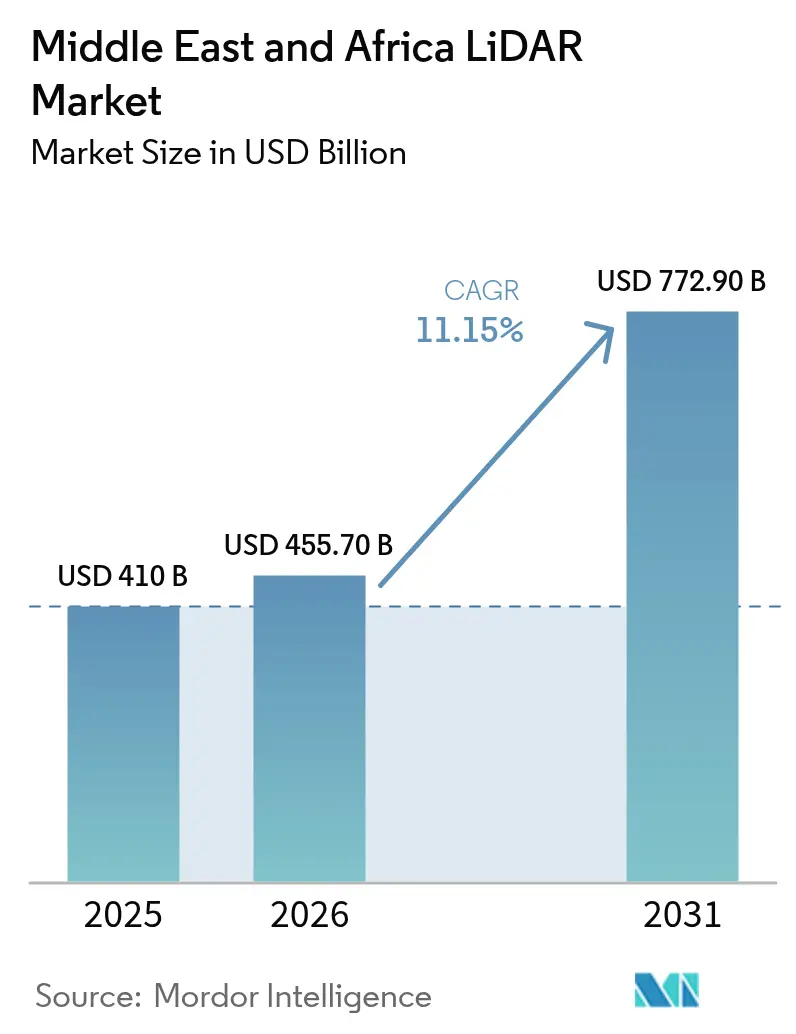

| Base Year Market Size (2025) | USD 410 Billion |

| Market Size (2026) | USD 455.70 Billion |

| Market Size (2031) | USD 772.90 Billion |

| Growth Rate (2026 - 2031) | 11.15% CAGR |

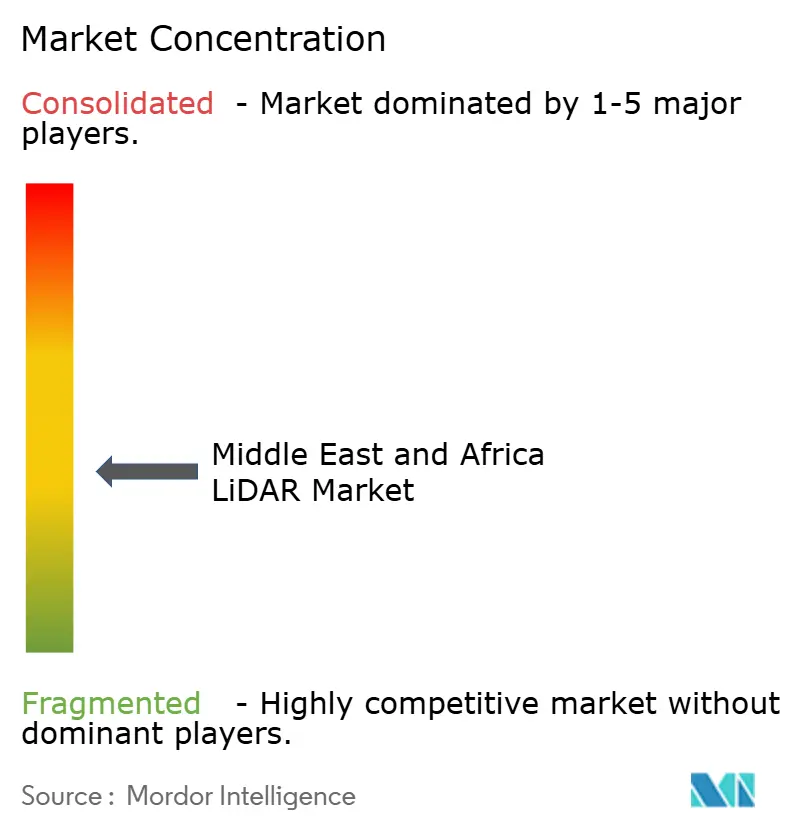

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa LiDAR Market Analysis by Mordor Intelligence

The Middle East and Africa LiDAR market size is expected to grow from USD 410 million in 2025 to USD 455.7 million in 2026 and is forecast to reach USD 772.9 million by 2031 at 11.15% CAGR over 2026-2031. Rapid rollout of giga-projects under Saudi Vision 2030, expanding smart-city programs across the Gulf, and sustained infrastructure spending in Southern Africa are intensifying demand for high-precision, three-dimensional spatial data. Increased pairing of LiDAR with artificial intelligence for automated feature extraction is shortening project cycles in construction monitoring and asset inspection. Solid-state advances such as Geiger-mode sensors are reducing size, weight, power, and cost, enabling deployment on drones that can tolerate harsh desert heat and dust. Automotive original-equipment manufacturers are incorporating LiDAR into advanced driver assistance systems, supported by the UAE plan that requires 25% of city journeys to shift to autonomous vehicles by 2030.

Key Report Takeaways

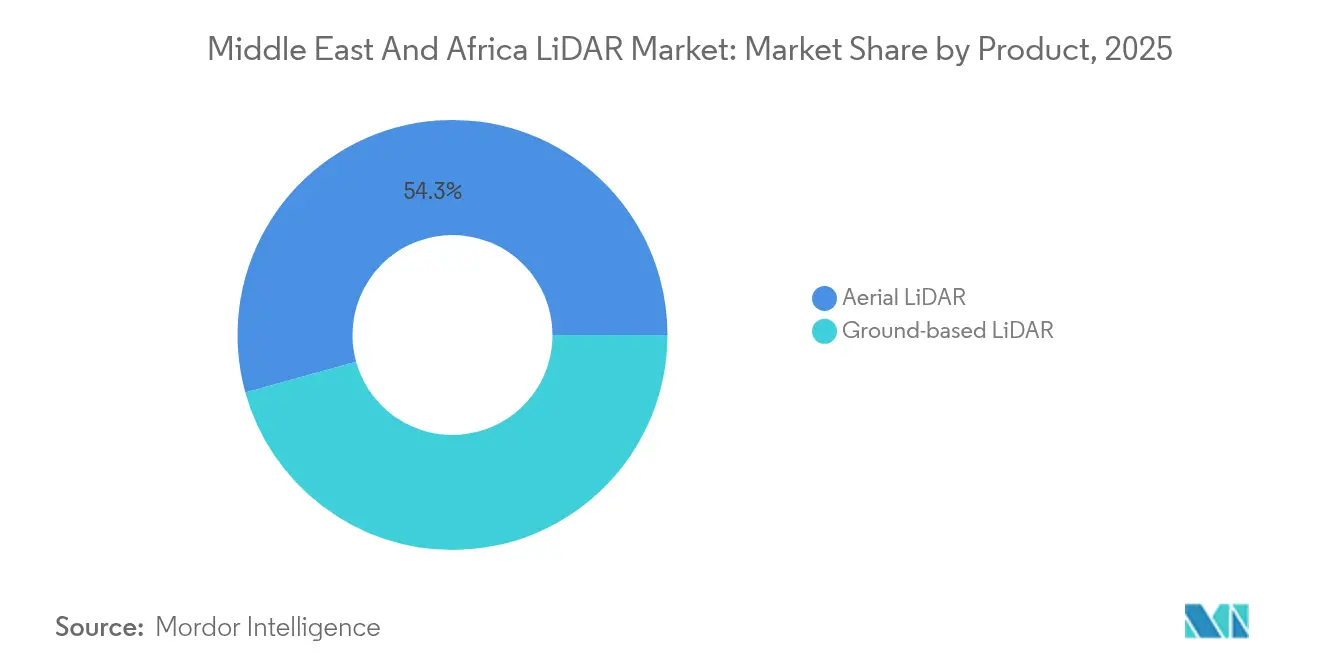

- By product type, aerial systems accounted for 54.30% of the Middle East and Africa LiDAR market share in 2025, while ground-based solutions are forecast to expand at a 13.76% CAGR to 2031.

- By technology, Time-of-Flight devices led with 62.40% revenue share in 2025; Geiger-mode sensors are projected to grow at a 12.85% CAGR through 2031.

- By component, laser scanners captured 47.60% of the Middle East and Africa LiDAR market size in 2025, and inertial measurement units are advancing at a 14.78% CAGR between 2026-2031.

- By deployment platform, terrestrial static tripod systems held 45.50% share in 2025, whereas UAV/drone platforms record the fastest growth at 14.35% CAGR.

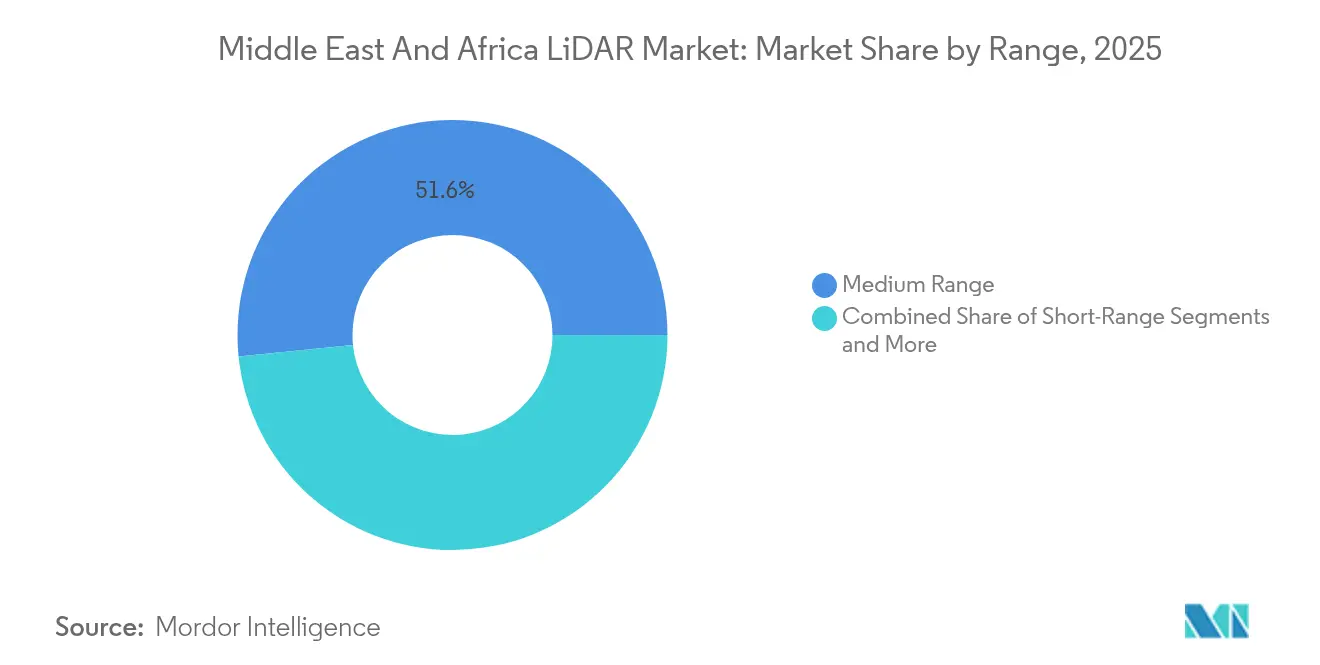

- By range, medium-range units claimed 51.60% share in 2025; short-range sensors are set to rise at 13.62% CAGR to 2031.

- By end-use industry, engineering and construction dominated with 37.50% share in 2025; automotive and ADAS is climbing at a 15.52% CAGR through 2031.

- By geography, Saudi Arabia led with 40.70% share in 2025, while Qatar is on track for the highest 12.74% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa LiDAR Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| LiDAR mandate for smart-city digital twins in GCC | +3.5% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Surge in UAV-borne corridor mapping for Saudi giga-projects | +2.8% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Offshore wind-farm bathymetry needs off Namibia and South Africa | +2.2% | South Africa, Namibia | Medium term (2-4 years) |

| Security-driven perimeter surveillance at UAE critical sites | +1.9% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| High-resolution topography for copper and gold open-pit mines | +1.5% | South Africa, Rest of MEA | Long term (≥ 4 years) |

| Climate-resilience flood-plain modelling across Nile basin | +1.2% | Egypt, Sudan, Ethiopia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LiDAR Mandate for Smart-City Digital Twins in GCC

Gulf governments now require sub-centimeter digital replicas of city assets, making LiDAR indispensable for underground-utility mapping, traffic-flow optimisation, and carbon-footprint analysis. Dubai Municipality is applying mobile scanners to model buried pipes and cables, cutting unplanned outages and excavation re-works. In Qatar, a USD 60 million smart-city platform for Lusail City processes continuous LiDAR feeds to manage 450,000 residents’ services.[1]ST Engineering, “AGIL Smart City Operating System for Lusail City,” computerweekly.com Mandatory BIM adoption in public projects ensures that LiDAR point clouds flow directly into standardised construction models, removing data-format bottlenecks. The result is a unified planning approach that speeds permit approvals and reduces lifecycle cost overruns. GCC authorities also bundle LiDAR procurement with cloud analytics, encouraging local data-centres that comply with sovereignty rules.

Surge in UAV-Borne Corridor Mapping for Saudi Giga-Projects

High-profile programmes such as NEOM’s 170 km linear city require weekly topographic updates over vast tracts that conventional surveys cannot cover in time. Rotary-wing drones equipped with medium-range LiDAR now map up to 100 acres per day at 1-3 cm accuracy, slashing progress-tracking cycles by 70%. Specialist operators like Aeromotus supply turnkey drone-as-a-service packages that combine flight planning, scanning, and cloud processing.[2] Aeromotus, “Drone Solutions Provider,” aeromotus.com Resulting digital twins allow contractors to compare design intent with as-built conditions, catching earthwork deviations early. For linear infrastructure such as high-speed rail spines and desalination pipelines, rapid corridor updates reduce change-order frequency and safeguard delivery milestones.

Offshore Wind-Farm Bathymetry Needs Off Namibia and South Africa

Utility-scale wind projects planned for the Atlantic coast depend on bathymetric LiDAR to chart shallow-water seabeds before turbine foundation installation. Geiger-mode airborne sensors collect dense point clouds through turbid water columns, enabling engineers to spot sand-wave migration and scour-risk zones. National power utilities prefer LiDAR over ship-borne multibeam sonar because it halves survey time and avoids weather-downtime penalties. South African regulators now require high-resolution coastal elevation models to update flood-risk atlases that feed environmental-impact assessments.[3]Kevin P. Corbley, “Going for Gold with LiDAR,” leica-geosystems.com Regional hydrography firms are retrofitting aircraft with green-wavelength lasers that penetrate up to 30 m depth, broadening service portfolios beyond defence contracts.

Security-Driven Perimeter Surveillance at UAE Critical Sites

Energy facilities and airports are installing ground-based LiDAR fences that deliver reliable target detection under smoke, dust, or darkness, conditions that degrade camera performance. The Barakah nuclear plant layers laser arrays with satellite feeds for real-time breach alerts. LiDAR units also spot methane plumes, aligning safety with environmental-compliance mandates. Integration with counter-UAS radars, showcased at the 2025 Counter-UAS Middle East and Africa conference, lets security managers thwart drone incursions. Demand is further propelled by insurance clauses that reward certified 3D surveillance with premium discounts.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarcity of regional calibration labs inflating lead-times | -1.8% | North Africa, Rest of MEA | Medium term (2-4 years) |

| Customs duties on Class-3B laser imports in non-GCC Africa | -1.5% | South Africa, Rest of MEA | Short term (≤ 2 years) |

| Limited GNSS reference-station density outside Gulf states | -1.2% | North Africa, Rest of MEA | Long term (≥ 4 years) |

| Low public-sector CAPEX in post-conflict North Africa | -0.9% | North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Regional Calibration Labs Inflating Lead-Times

Only a handful of accredited laboratories exist between Riyadh and Johannesburg, forcing most operators to ship sensors to Europe for annual recalibration. Logistics lags can stretch to 12 weeks, freezing fleet availability during peak construction phases. Larger contractors respond by leasing pre-calibrated units from providers such as ClearSkies Geomatics, while smaller firms idle crews and absorb liquidated damages. The bottleneck also hampers adoption of advanced solid-state LiDAR, which often requires shorter service cycles to uphold warranty specifications. Several Gulf free-zones have announced incentives for foreign metrology houses to open branches, yet timelines suggest meaningful capacity will not arrive before 2027.

Limited GNSS Reference-Station Density Outside Gulf States

High-accuracy LiDAR relies on centimetre-grade positioning, but Africa’s sparse real-time kinematic networks create error-prone point clouds that inflate post-processing hours. Field teams compensate by deploying extra ground control points, raising survey budgets by up to 25%. Visual-SLAM handheld scanners reduce GNSS dependency for indoor jobs, yet their short range limits open-pit mine uses. Pan-African initiatives to densify reference stations remain under-funded, leaving private telecom tower operators to fill coverage gaps case-by-case. Until infrastructure improves, growth in the Middle East and Africa LiDAR market will keep clustering near Gulf economies where positioning networks are fully operational.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Aerial Systems Dominate Infrastructure Mapping

Aerial platforms generated 54.30% of the Middle East and Africa LiDAR market size in 2025, a position rooted in their ability to survey giga-project footprints that sprawl across arid terrains. Saudi engineering firms rely on helicopter and fixed-wing campaigns to update cut-and-fill quantities weekly, feeding dashboards that flag schedule slippage. The combination of oblique photogrammetry with high-density point clouds helps planners visualise rock-cut faces and desert wadis that influence road alignments. Aerial scanning also underpins coastal-erosion monitoring in Namibia, where green-wavelength laser pulses measure dune migration along tourist beaches.

Ground-based scanners, though holding a smaller share, are slated for 13.76% CAGR as municipalities digitise sewers, bridges, and heritage façades. Wearable systems map multistorey tunnels without GPS, letting inspectors detect spalling concrete behind tiles. The Middle East and Africa LiDAR market benefits from SLAM algorithms that register scans in real time, permitting overnight issuance of clash-detection reports that would once take a week. Hardware miniaturisation means a two-person crew can now capture an entire metro station in an evening, democratising high-precision documentation beyond tier-one contractors.

By Technology: Time-of-Flight Reliability Meets Geiger-Mode Innovation

Time-of-Flight remained the workhorse with 62.40% revenue in 2025, prized for robust performance under dust-laden winds and intense solar glare typical of the Arabian Peninsula. Power utilities employ ToF units for corridor clearance checks on transmission lines, avoiding vegetation-related outages that could stall refinery production. Vendor roadmaps introduce eye-safe 1,550 nm lasers that extend range past 3 km, widening use in open-pit mine slope analysis.

Geiger-mode sensors post a 12.85% CAGR forecast because ultra-high-point densities accelerate environmental modelling. Forestry-carbon projects in Gabon use the technology to refine biomass estimates, an attractive quality as voluntary carbon markets tighten verification standards. Elevated altitude operation supports 366 km²/h coverage, enabling national-scale DEM refreshes on single aircraft sorties. Continued research into compressive sensing promises 64-fold resolution gains without heavier data volumes, enhancing suitability for real-time flood simulations.

By Component: Laser Scanners Lead While IMUs Gain Momentum

Laser scanners commanded 47.60% share in 2025 as the core element dictating range, beam divergence, and pulse rate. Automotive suppliers are transitioning from moving-mirror assemblies to monolithic VCSEL arrays that endure shock on Middle-Eastern desert roads. In oil refineries, ruggedised scanners mounted on robotic arms complete 360° sweeps of pipe racks during shutdowns, providing corrosion maps for maintenance crews.

IMUs, projected at 14.78% CAGR, grow because drone and vehicle platforms demand stable orientation under gusty conditions. MEMS-based units now fuse gyroscope output with barometers and wheel encoders, reducing drift when GNSS is lost. The Middle East and Africa LiDAR market benefits directly, as accurate inertial data shortens cloud-alignment workflows, cutting project delivery times. Integrated camera-LiDAR-IMU pods are emerging, giving surveyors a turnkey payload for both photorealistic meshes and metric point clouds.

By Deployment Platform: Terrestrial Systems Evolve as Drones Accelerate

Terrestrial tripod stations held 45.50% share in 2025, entrenched in applications where millimetre precision trumps speed. Museums in Egypt use long-range static scanners to capture hieroglyphs before tourism-related wear accelerates, archiving artefacts in high resolution for global researchers. Automatic target-recognition software registers successive scans, allowing one operator to document 200-room palaces in a weekend.

Drone-based platforms, climbing at 14.35% CAGR, dominate linear asset inspection. Highway authorities fly LiDAR at dawn to avoid traffic, generating pavement-rutting indices by midday. In Zambia, humanitarian groups map minefields with UAV-LiDAR-imagery combos that detect subtle terrain depressions left by ordnance. Such agility proves pivotal where ground access is dangerous or restricted.

By Range: Medium-Range Versatility Meets Short-Range Growth

Medium-range devices (100-300 m) represented 51.60% revenue in 2025 and remain the default sensor for building façades and quarry monitoring. Their sweet-spot range aligns with drone-flight altitude restrictions across GCC urban airspaces, ensuring clear returns without risking eye safety. Mining firms value the ability to scan highwalls from benches, keeping personnel out of rock-fall zones.

Short-range units (<100 m) rise at 13.62% CAGR on the back of smart-factory automation and security perimeters. Oil terminal operators deploy solid-state flash LiDAR to detect vehicles straying into hazardous zones, triggering audible alarms within 200 milliseconds. Automotive ADAS platforms integrate dual-short-range arrays for blind-spot elimination, a feature Daimler Trucks Middle East plans to include in 2026 heavy-duty models. Long-range sensors (>300 m) preserve niche demand for copper-mine pit-rim stability and border-fence surveillance, especially in rugged Sahel zones where sandstorms impair camera visibility.

By End-Use Industry: Construction Leadership Amid Automotive Surge

Engineering and construction consumed 37.50% of 2025 spending as mega-projects prioritised continuous 3D documentation of earthworks and structural progress. Pairing LiDAR with BIM reduces rework by revealing steel-rebar clashes before concrete is poured, saving contractors days per floor. Middle East and Africa LiDAR market adoption accelerates further because tender documents now stipulate 3D deliverables as payment milestones.

Automotive and ADAS, with 15.52% CAGR, benefits from proactive regulatory stances that fast-track autonomous-vehicle pilots on dedicated lanes. Ride-hail fleets in Dubai already operate Hesai-equipped shuttles that accumulate regional road-edge data for HD-map refinement. Oil and gas companies employ LiDAR for flare-stack deformation checks, while miners validate blast-volume calculations. Forestry concessions in Central Africa integrate multispectral imagery with LiDAR to quantify canopy disturbance for REDD+ reporting.

Geography Analysis

Saudi Arabia, holding 40.70% of 2025 revenue, channels LiDAR into megacities, mining clusters, and irrigated-agriculture master plans. NEOM’s Adassa geospatial engine merges continuous drone LiDAR with AI to flag schedule drift, ensuring linear projects stay aligned. The kingdom’s Minerals Strategy uses airborne scanning to delineate copper and gold prospects, underpinning diversification from hydrocarbons and expanding the Middle East and Africa LiDAR market.

The United Arab Emirates ranks second, driven by a regulatory ecosystem that accelerates pilot testing of smart-mobility tech. Dubai’s Green Spine initiative repurposes highways into shaded promenades using rolling LiDAR updates to simulate micro-climate cooling and tree-canopy growth. Local drone-service vendors provide subscription models, making high-resolution data affordable for mid-sized engineering consultancies. Qatar posts a 12.74% CAGR outlook as Lusail City deploys a national smart-infrastructure platform linked to mandatory BIM submission templates. LiDAR-enriched 3D city models feed utilities’ outage-prediction algorithms and inform resilience planning. Beyond the Gulf, South Africa utilises bathymetric LiDAR for offshore wind siting, while Kenya adopts drone scanning for county-road asset management.

Competitive Landscape

Global suppliers such as Leica Geosystems, Trimble, Hexagon, and RIEGL compete with regional specialists LightWare LiDAR, MENA 3D, and GlobalScan Technologies. Hardware commoditisation is steering competition toward full-stack offerings that combine sensors, AI analytics, and cloud hosting. Partnerships flourish: international OEMs bundle sensors with training delivered by local value-added resellers who understand Arabic procurement norms. Service-based revenue rises as clients outsource data processing to regional centres that comply with data-sovereignty statutes.

White-space opportunities lie in turnkey mining-operations dashboards and oil-and-gas leak-detection packages. Firms that translate point clouds into actionable insights—such as wall-stability indices or methane concentration maps—gain pricing power. Drone-service aggregators like Aeromotus disrupt traditional survey houses by delivering on-demand aerial LiDAR at day rates that undercut crewed aircraft. Dual-use applications attract defence integrators that bundle perimeter surveillance with counter-UAS capabilities, widening addressable budgets and attracting sovereign-wealth-fund backing.

New entrants face barriers from scarce calibration labs and protracted customs clearance for Class-3B lasers. Incumbents counter by stocking buffer inventory in free-zone warehouses and offering equipment-swap guarantees that minimise project downtime. Competitive intensity is expected to intensify as solid-state sensor prices fall, reducing capital outlay and encouraging smaller construction firms to adopt LiDAR.

Middle East And Africa LiDAR Industry Leaders

Innoviz Technologies Ltd

Leica Geosystems Ag

Trimble Inc.

Sick AG

FARO Technologies Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hesai Technology confirmed its long-range LiDAR will equip WeRide autonomous vehicles on Uber’s Dubai platform, supporting the emirate’s 2030 smart-mobility goal.

- March 2025: Hesai Technology confirmed its long-range LiDAR will equip WeRide autonomous vehicles on Uber’s Dubai platform, supporting the emirate’s 2030 smart-mobility goal.

- February 2025: RIEGL announced the latest UAV-LiDAR payloads for infrastructure monitoring at Xponential Europe 2025.

- February 2025: Hesai and BYD agreed to mass-produce more than 10 LiDAR-equipped vehicle models by 2025, boosting automotive deployments in MEA.

Middle East And Africa LiDAR Market Report Scope

LiDAR-based mapping solutions are agile and can be used on a stationary or moving vehicle. Due to this, they are being adopted by a growing number of industries, especially for applications in engineering, construction, environment, and exploration. The Middle East and Africa are segmented by Product, Component, and End-User. The Component section is segmented by GPS, Laser Scanners, Inertial Measurement Unit, Other Components.

By Product

| Aerial LiDAR |

| Mechanical Scanning |

| Solid-state Scanning |

By Technology

| Ground-based LiDAR |

| Time-of-Flight |

| Geiger-Mode |

| Phase-Shift |

| Flash LiDAR |

By Component

| Laser Scanners |

| GPS/GNSS Receiver |

| Inertial Measurement Unit |

| Cameras and MEMS Mirrors |

| Other Components |

By Deployment Platform

| Terrestrial Static Tripod |

| UAV-/Drone-based |

| Mobile Mapping (Vehicle-mounted) |

| Bathymetric/Airborne Hydrographic |

By Range

| Short-Range |

| Medium-Range |

| Long-Range |

By End-Use Industry

| Engineering and Construction |

| Oil and Gas |

| Aerospace and Defense |

| Automotive and ADAS |

| Mining and Quarrying |

| Agriculture and Forestry |

By Country

| Saudi Arabia |

| Qatar |

| Kuwait |

| United Arab Emirates |

| South Africa |

| Kenya |

| Rest of Middle East and Africa |

| By Product | Aerial LiDAR |

| Mechanical Scanning | |

| Solid-state Scanning | |

| By Technology | Ground-based LiDAR |

| Time-of-Flight | |

| Geiger-Mode | |

| Phase-Shift | |

| Flash LiDAR | |

| By Component | Laser Scanners |

| GPS/GNSS Receiver | |

| Inertial Measurement Unit | |

| Cameras and MEMS Mirrors | |

| Other Components | |

| By Deployment Platform | Terrestrial Static Tripod |

| UAV-/Drone-based | |

| Mobile Mapping (Vehicle-mounted) | |

| Bathymetric/Airborne Hydrographic | |

| By Range | Short-Range |

| Medium-Range | |

| Long-Range | |

| By End-Use Industry | Engineering and Construction |

| Oil and Gas | |

| Aerospace and Defense | |

| Automotive and ADAS | |

| Mining and Quarrying | |

| Agriculture and Forestry | |

| By Country | Saudi Arabia |

| Qatar | |

| Kuwait | |

| United Arab Emirates | |

| South Africa | |

| Kenya | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is driving the rapid growth of the Middle East and Africa LiDAR market?

Accelerated smart-city initiatives, Saudi giga-projects, and autonomous-vehicle programs together push the market toward an 11.15% CAGR over 2026-2031.

Which product segment leads regional revenue?

Aerial LiDAR systems accounted for 54.30% of 2025 revenue, dominating large-area mapping for construction and infrastructure.

Why is Geiger-mode LiDAR gaining traction?

Its ability to deliver ultra-dense point clouds at high flight altitudes supports fast national-scale mapping and environmental monitoring.

How do calibration bottlenecks affect project timelines?

Lack of regional labs forces overseas shipments and can delay equipment availability by up to 12 weeks, raising project costs.

Which country is the fastest-growing LiDAR adopter?

Qatar shows a 12.74% CAGR forecast thanks to its Lusail smart-city platform and BIM mandates that embed LiDAR data in every public project.

What role do drones play in market expansion?

UAV-mounted sensors, growing at 14.35% CAGR, deliver rapid corridor mapping and reduce survey times, especially for Saudi Arabia’s linear mega-projects.

How large is the Middle East and Africa LiDAR market in 2026?

The Middle East and Africa LiDAR market is expected to grow from USD 410 million in 2025 to USD 455.7 million in 2026 and is forecast to reach USD 772.9 million by 2031 at 11.15% CAGR over 2026-2031.

Page last updated on: