Microfiber Synthetic Leather Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.80 Billion |

| Market Size (2031) | USD 3.5 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

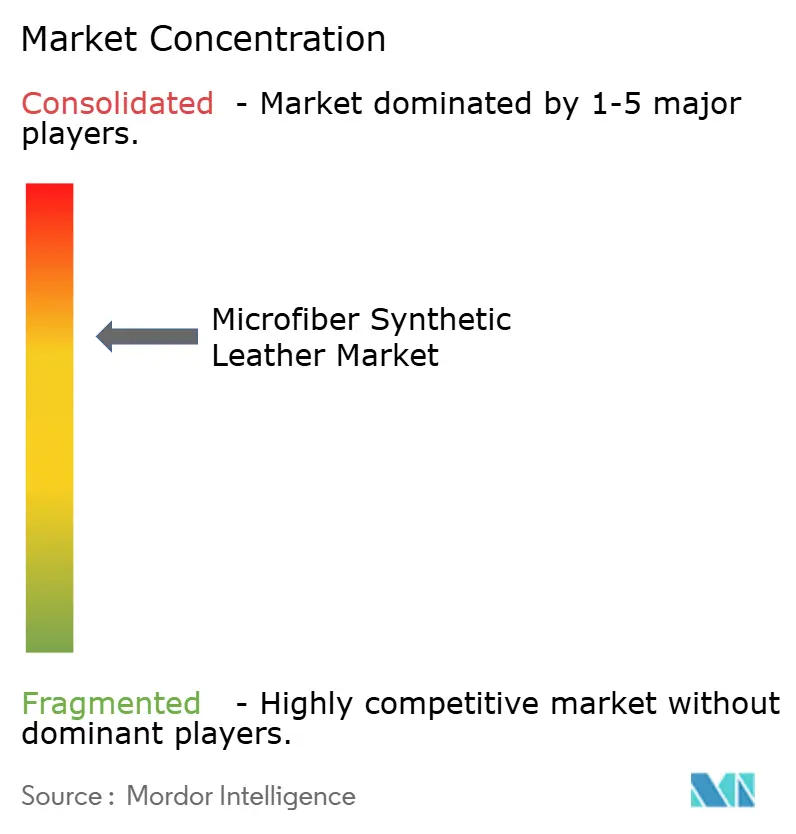

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microfiber Synthetic Leather Market Analysis by Mordor Intelligence

The Microfiber Synthetic Leather Market size was valued at USD 2.68 billion in 2025 and is estimated to grow from USD 2.80 billion in 2026 to reach USD 3.5 billion by 2031, at a CAGR of 4.56% during the forecast period (2026-2031). Supply‐chain verticalization in Asia, capacity expansions for bio-based substrates, and stricter animal-welfare policies worldwide are reshaping procurement strategies across automotive, fashion, and furniture customers. Composite-spinning know-how formerly monopolized by Japanese incumbents is diffusing into China, compressing prices and broadening adoption. Electric-vehicle (EV) interior designers are accelerating the specification of microfiber synthetics to comply with the EU EUDR without sacrificing abrasion resistance. Waterborne polyurethane’s share of total output has already reached the mid-twenties owing to solvent-emission curbs in California and impending PFAS bans in France and Denmark.

Key Report Takeaways

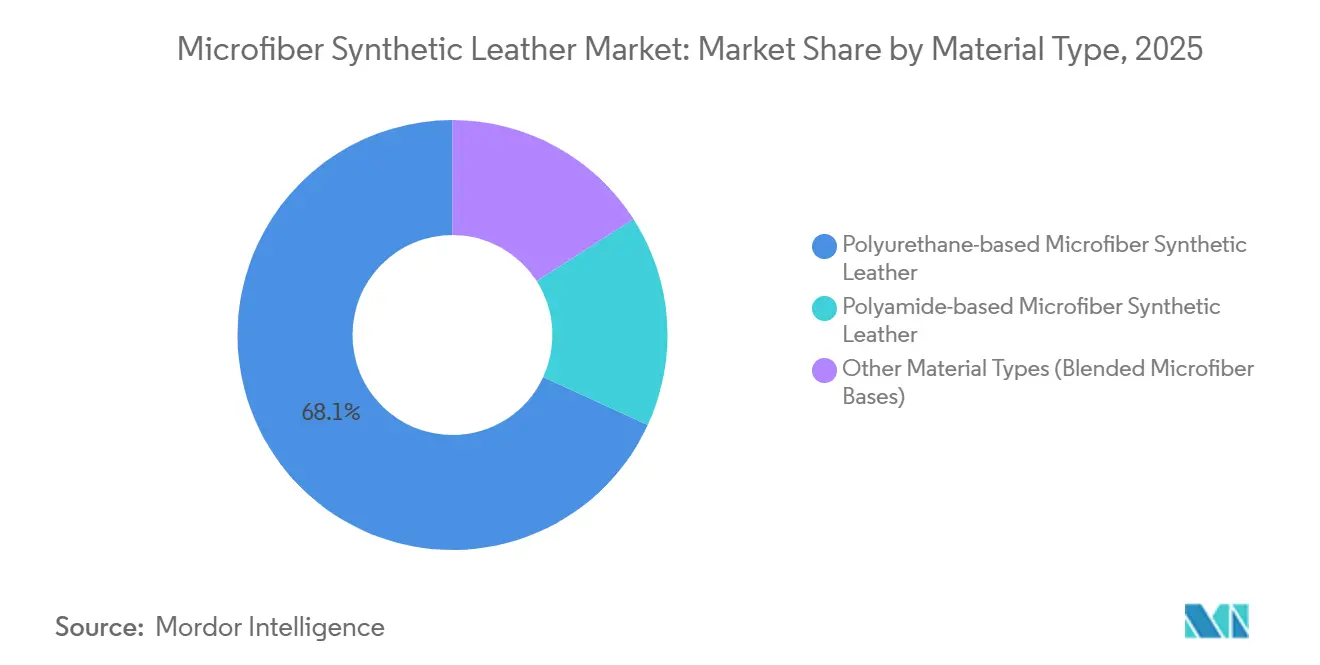

- By material type, polyurethane-based microfiber synthetic leather captured 68.12% of the Microfiber Synthetic Leather market share in 2025. However, other material types accounted for the fastest 4.96% CAGR through 2031.

- By texture, suede microfiber leather accounted for 46.56% of the market in 2025, while embossed/printed microfiber leather is expected to increase at the fastest CAGR of 5.11% during the forecast period (2026-2031).

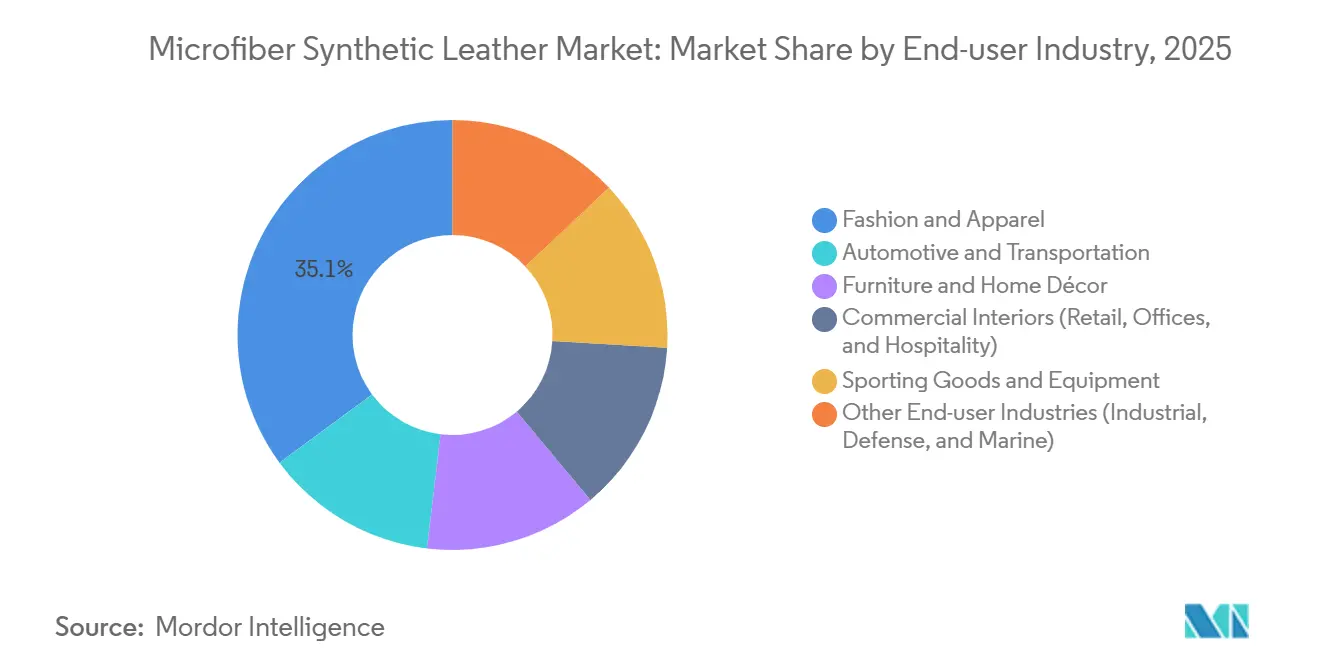

- By end-user industry, fashion and apparel accounted for the highest share of 35.12% in 2025. However, the automotive and transportation industry is expanding at the fastest CAGR of 5.31% to 2031.

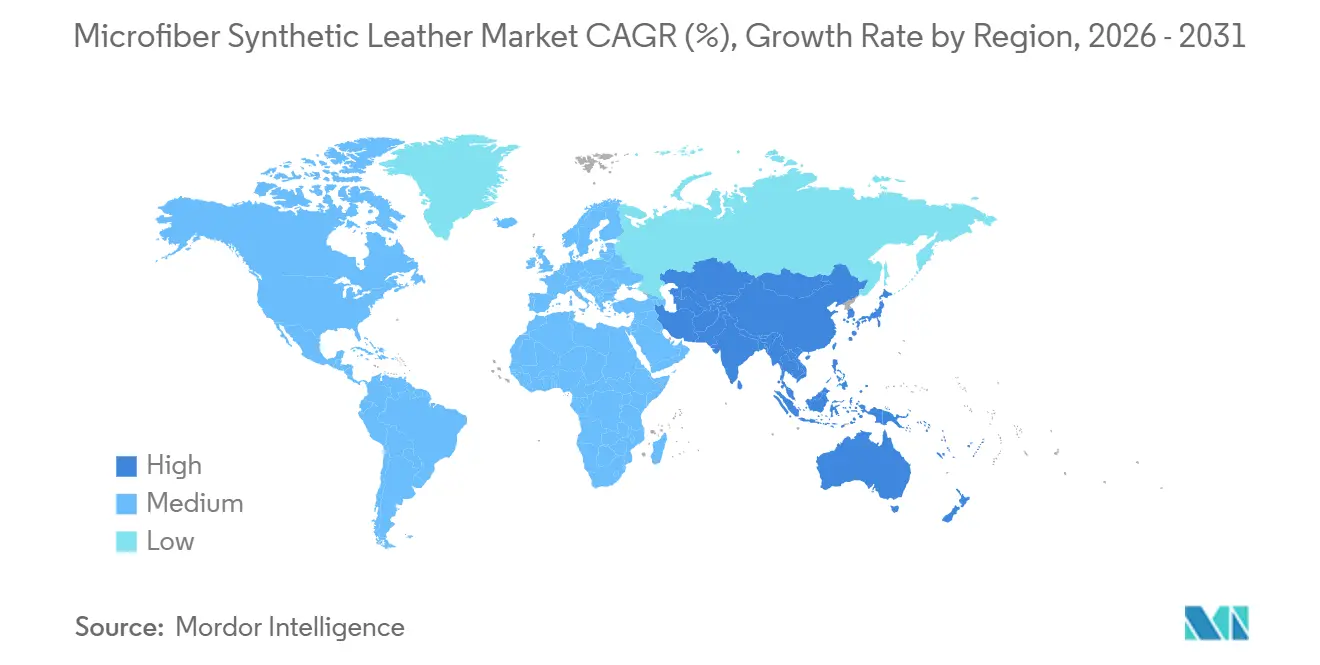

- By geography, Asia-Pacific led with 54.44% of the Microfiber Synthetic Leather market share in 2025 while registering the highest 5.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microfiber Synthetic Leather Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of vegan and sustainable fashion across regions | +1.2% | Global, with concentration in North America, EU, and urban APAC markets | Medium term (2-4 years) |

| Performance advantages vs PU/PVC synthetics (abrasion and breathability) | +0.9% | Global, particularly automotive-heavy regions (Germany, Japan, South Korea, China) | Short term (≤ 2 years) |

| Expanding use in automotive interiors and luxury upholstery | +1.5% | APAC core (China, Japan, South Korea), spill-over to North America and EU | Medium term (2-4 years) |

| Government bans/restrictions on genuine-leather imports | +0.6% | India, select ASEAN countries, EU (indirect via EUDR) | Short term (≤ 2 years) |

| Adoption in high-end consumer electronics casings | +0.4% | Global, early gains in China, South Korea, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Vegan and Sustainable Fashion Across Regions

Mainstream labels such as H&M and Stella McCartney formed a joint Insight Board in spring 2026 to fast-track next-generation synthetics, underscoring microfiber’s new branding power[1]H&M Group, “H&M Group Sustainability News,” hmgroup.com. Luxury houses, including Hugo Boss, are committed to phasing out virgin polyester and polyamide by 2030, spurring interest in microfiber formulas engineered for chemical depolymerization. Toray’s Ultrasuede BX, built on 30% plant-based polyester, has been adopted across premium EV models, proving bio-content can command pricing premiums. Solvent regulations from California SB 707 and EU PFAS prohibitions are pushing converters toward waterborne polyurethane, which already accounts for roughly a quarter of global microfiber output. Meanwhile, environmental NGOs spotlight microfiber shedding, measured at 68.5 mg kg during washing, keeping biodegradability on the policy agenda.

Performance Advantages Versus PU/PVC Synthetics (Abrasion and Breathability)

Laboratory tests show microfiber synthetic leather achieves burst force of 374 N and tear strength of 139 N, sharply higher than natural hides, justifying its use in high-wear seating. Nissan’s TailorFit seat coverings introduced in March 2026 boast more than 100,000 abrasion cycles and a 40-60% cost edge over genuine leather. SEIREN couples microfiber substrates with Viscotec's digital printing; this small-lot model satisfies automakers seeking bespoke interiors without raising inventory risk. Limitations persist in very cold or hot climates, where natural leather’s thermal stability still wins adoption. Breakthroughs such as Spiber’s Brewed Protein fiber point to future competition from fermentation-derived materials that replicate collagen architecture without polyurethane.

Expanding Use in Automotive Interiors and Luxury Upholstery

Automotive OEMs prefer microfiber to sidestep EUDR (European Union Deforestation Regulation) traceability obligations while lowering seat mass for EV range gains. Ferrari’s Purosangue features Alcantara with 68% recycled polyester, reframing synthetic suede as “conscious luxury” rather than cost saving. Toray earmarked CNY 240 billion (USD 35 billion) for Ultrasuede capacity expansions tied to electrification of its Japanese lines, cutting scope-1 emissions by roughly 7,100 tonCO2-equivalent annually. BASF’s solvent-free Haptex 4.0, adopted by NIO in July 2024, underlines that circularity credentials are now baseline for Tier 1 bids.

Government Bans/Restrictions on Genuine-Leather Imports

India’s May 2025 policy package removed port testing and granted duty-free access for synthetic footwear inputs, redirecting buyers toward microfiber. The EU EUDR heightens compliance costs for leather, accelerating substitution in fashion supply chains. China’s GB 25038-2024 standard aligns safety tests for synthetic and natural uppers, removing legacy bias toward hides. Wanhua Chemical’s 33.8% global MDI share underscores that greener leather replacements still depend on petrochemical intermediates until bio-isocyanates are commercialized.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited biodegradability vs natural hides | -0.7% | Global, acute in EU and North America with stringent EPR regulations | Medium term (2-4 years) |

| Supply-chain concentration in East Asia creating dependency risks | -0.5% | Global, most acute for North America and EU converters | Short term (≤ 2 years) |

| Lack of drop-in recycling streams for microfiber composites | -0.4% | Global, particularly EU with ESPR textile-destruction ban (July 2026) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Biodegradability Versus Natural Hides

Polyurethane-polyamide architecture resists enzymatic breakdown, leaving microfiber waste persistent in landfills, whereas natural hides degrade within four decades. The EU ESPR (Ecodesign for Sustainable Products Regulation) prohibition on destroying unsold textiles from July 2026 compels design for disassembly, yet composite delamination adds double the processing cost relative to PET recycling[2]European Commission, “Textile Strategy and ESPR,” europa.eu. BASF’s Haptex 4.0 removes polyamide layers to allow closed-loop PET recovery, but commercial roll-out remains limited to one Electric Vehicle Original Equipment Manufacturer. If extended-producer-responsibility fees expand, brands could lose the current 40-60% cost gap over leather.

Supply-Chain Concentration in East Asia Creating Dependency Risks

Wanhua’s 1.5 million tons per annum MDI complex came online in Q2 2026, cementing regional price leadership. Red Sea shipping disruptions in late 2025 spiked European MDI spot quotes 247% year-over-year, and Western converters paid USD 200-300 per ton surcharges from BASF and Covestro in early 2026. Japanese spinning IP still dominates premium suede output, but Huafeng’s CNY 3.6 billion (USD 524.98 million) 2026 expansion shows the moat is eroding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyurethane Dominance Masks Bio-Based Shift

Polyurethane grades led the microfiber synthetic leather market with 68.12% revenue share in 2025, owing to 100,000+ abrasion-cycle durability and ready compatibility with existing tannery equipment. Other material types (blended microfiber bases) are forecast to post the fastest 4.96% CAGR during the forecast period (2026-2031) as luxury OEMs chase circular content. Polyamide microfiber captures niche athletic and heavy-duty seating that values tear strength over cost. Waterborne polyurethane already comprises about one-quarter of global output after regulations clamped down on DMF usage, and bio-based polyurethane capacity reached 520,000 tons in 2024.

Investment centers on research and development that elevates bio-content without compromising physical performance. Alcantara’s 68% recycled-polyester formulation in Ferrari’s Purosangue demonstrates consumer appetite for premium green suede. Asahi Kasei and Aquafil’s cellulose-reinforced PA6 targets closed-loop ambitions, while ECOLORICA’s drum-dyed full-grain microfiber commands luxury accessory margins without price convergence to mass-market PVC. Composite designs able to meet both California Prop 65 and REACH standards enjoy quicker OEM approval cycles.

By Texture/Grain Type: Digital Production Enables Customization

Suede maintained 46.56% of the microfiber synthetic leather market share in 2025 on the strength of flagship brands such as Ultrasuede and Alcantara. Embossed and printed variants are slated for the fastest 5.11% CAGR through 2031 as on-demand digital embossing multiplies SKU offerings.

Software-driven patterning shortens design-to-shelf timelines for fashion capsules and special-edition vehicles. SEIREN’s Viscotecs platform eliminates engraved-roller capex, reducing minimum order volumes and democratizing entry for boutique designers. Split microfiber remains a budget suede alternative, but its lower 70,000-cycle abrasion ceiling restricts commercial seating uptake. Keyi Fujian’s 2025 laminating patent boosts bond durability under flex, mitigating delamination claims that have dogged printed synthetics.

By End-user Industry: Automotive Electrification Drives Substitution

Fashion still led demand with 35.12% in 2025, yet automotive and transportation are poised to outrun at a 5.31% CAGR during the forecast period (2026-2031) on the back of EV penetration. EV makers leverage microfiber’s lighter mass to extend range and dodge leather traceability red tape.

Nissan’s TailorFit seats and Toyota’s Spiber-infused covers illustrate how OEMs frame microfiber as a premium, not a compromise. Hospitality seating, office furnishings, and commercial fit-outs now trial low-VOC microfiber as a greener alternative to PVC, but fragmented procurement slows aggregate volumes. Sporting-goods brands, including FootJoy, promote breathability benefits to justify USD 100-plus price points. Defense and marine sectors remain negligible until thermal stability and fire-retardant grades mature.

Geography Analysis

Asia-Pacific dominated with a 54.44% revenue share in 2025 and is projected to log a 5.32% CAGR through 2031. China alone supplies 36% of global polyurethane, backed by Wanhua Chemical’s 1.5 million tpa MDI facility that came online in 2026. Huafeng’s CNY 3.6 billion 2026 upgrade will add 200,000 tons of spandex and polyurethane liquids, signaling China’s push into premium suede previously cornered by Japan. India’s duty waivers on synthetic footwear inputs plus SEIREN’s localized finishing plant are catalyzing demand growth in South Asia.

Europe and North America pivot on circularity. BASF’s Haptex 4.0 approval by NIO underscores solvent-free credentials, while the ESPR ban on destroying unsold stock from July 2026 forces design-for-recycling. High energy and labor costs sustain an Asia price gap even as European gas tariffs remain 120% above 2019 levels, prompting Covestro to lift MDI contract prices by USD 200 per ton in February 2026. Italy’s ECOLORICA benefits from luxury buyers willing to pay traceability premiums.

Latin America and MEA remain embryonic. Brazilian footwear OEMs trial microfiber uppers, and San Fang’s NTD300 million (USD 9.45 million) 2025 expansion targets these mid-income markets. Lack of regional isocyanate plants and ocean-freight volatility, however, inhibit profit pools until supply bases localize.

Competitive Landscape

The Microfiber Synthetic Leather market is moderately concentrated. Regulatory readiness is a rising weapon. BASF’s US 20240247094 patent covers waterborne polyurethane dispersions able to clear California Prop 65 without post-cure baking, winning early orders from North American furniture makers. Keyi Fujian’s 2025 laminating machine patent guards against embossed-grain delamination, catering to fashion clients facing stricter warranty claims.

Microfiber Synthetic Leather Industry Leaders

Kuraray Co., Ltd.

Alcantara S.p.A.

San Fang Chemical Industry Co., Ltd.

Asahi Kasei Corporation

Seiren Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nissan Motor Corporation unveiled TailorFit for its Nissan and INFINITI models across North America. TailorFit is a synthetic polyurethane-based seating material and mimics the tactile feel of traditional leather.

- July 2024: BASF launched Haptex 4.0, a polyurethane solution for producing synthetic leather that is 100% recyclable. Synthetic leather made with Haptex 4.0 and polyethylene terephthalate (PET) fabric can be recycled using a formulation and recycling technical pathway without needing a layer peel-off process.

Global Microfiber Synthetic Leather Market Report Scope

Microfiber synthetic leather is a high-tech artificial material designed to closely mimic the appearance, texture, and physical properties of natural animal hide. Often referred to as microfiber leather or vegan leather, it is widely considered the highest-grade version of synthetic leather currently available.

The Microfiber Synthetic Leather market is segmented by material type, texture/grain type, end-user industry, and geography. By material type, the market is segmented into polyurethane-based microfiber synthetic leather, polyamide-based microfiber synthetic leather, and other material types (blended microfiber bases). By texture/grain type, the market is segmented into suede microfiber leather, nappa microfiber leather, split microfiber leather, and embossed/printed microfiber leather. By end-user industry, the market is segmented into fashion and apparel, automotive and transportation, furniture and home décor, commercial interiors (retail, offices, and hospitality), sporting goods and equipment, and other end-user industries (industrial, defense, and marine). The report also covers the market size and forecasts for microfiber synthetic leather in 17 countries across major regions. The market sizes and forecasts are provided in value (USD).

| Polyurethane-based Microfiber Synthetic Leather |

| Polyamide-based Microfiber Synthetic Leather |

| Other Material Types (Blended Microfiber Bases) |

| Suede Microfiber Leather |

| Nappa Microfiber Leather |

| Split Microfiber Leather |

| Embossed/Printed Microfiber Leather |

| Fashion and Apparel |

| Automotive and Transportation |

| Furniture and Home Décor |

| Commercial Interiors (Retail, Offices, and Hospitality) |

| Sporting Goods and Equipment |

| Other End-user Industries (Industrial, Defense, and Marine) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Polyurethane-based Microfiber Synthetic Leather | |

| Polyamide-based Microfiber Synthetic Leather | ||

| Other Material Types (Blended Microfiber Bases) | ||

| By Texture/Grain Type | Suede Microfiber Leather | |

| Nappa Microfiber Leather | ||

| Split Microfiber Leather | ||

| Embossed/Printed Microfiber Leather | ||

| By End-user Industry | Fashion and Apparel | |

| Automotive and Transportation | ||

| Furniture and Home Décor | ||

| Commercial Interiors (Retail, Offices, and Hospitality) | ||

| Sporting Goods and Equipment | ||

| Other End-user Industries (Industrial, Defense, and Marine) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big will microfiber synthetic leather demand be by 2031?

The Microfiber Synthetic Leather Market size was valued at USD 2.68 billion in 2025 and is estimated to grow from USD 2.80 billion in 2026 to reach USD 3.5 billion by 2031, at a CAGR of 4.56% during the forecast period (2026-2031).

Which segment grows fastest inside microfiber synthetics?

Embossed and digitally printed textures post the quickest 5.11% CAGR during the forecast period (2026-2031) because on-demand patterning lowers inventory risk for fashion brands.

Why are automakers switching to microfiber seating?

Electric-vehicle makers specify microfiber to avoid leather traceability, trim seat mass, and still meet 100,000-cycle abrasion durability targets.

What keeps microfiber leather from full circularity today?

Polyurethane-polyamide composites need costly solvent delamination before chemical recycling, and no large-scale facility yet exists in Europe.

Page last updated on: