Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Polyurethane Microspheres Market Report is Segmented by Microsphere Type (Solid, Hollow, Expandable/Thermo-blowing), Raw Material (Aromatic Polyurethane, Aliphatic Polyurethane), Application (Encapsulation, Paints and Coatings, Adhesives, Cosmetics, and More), End-Use Industry (Automotive, Electronics and Electrical, Healthcare and Life Sciences, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

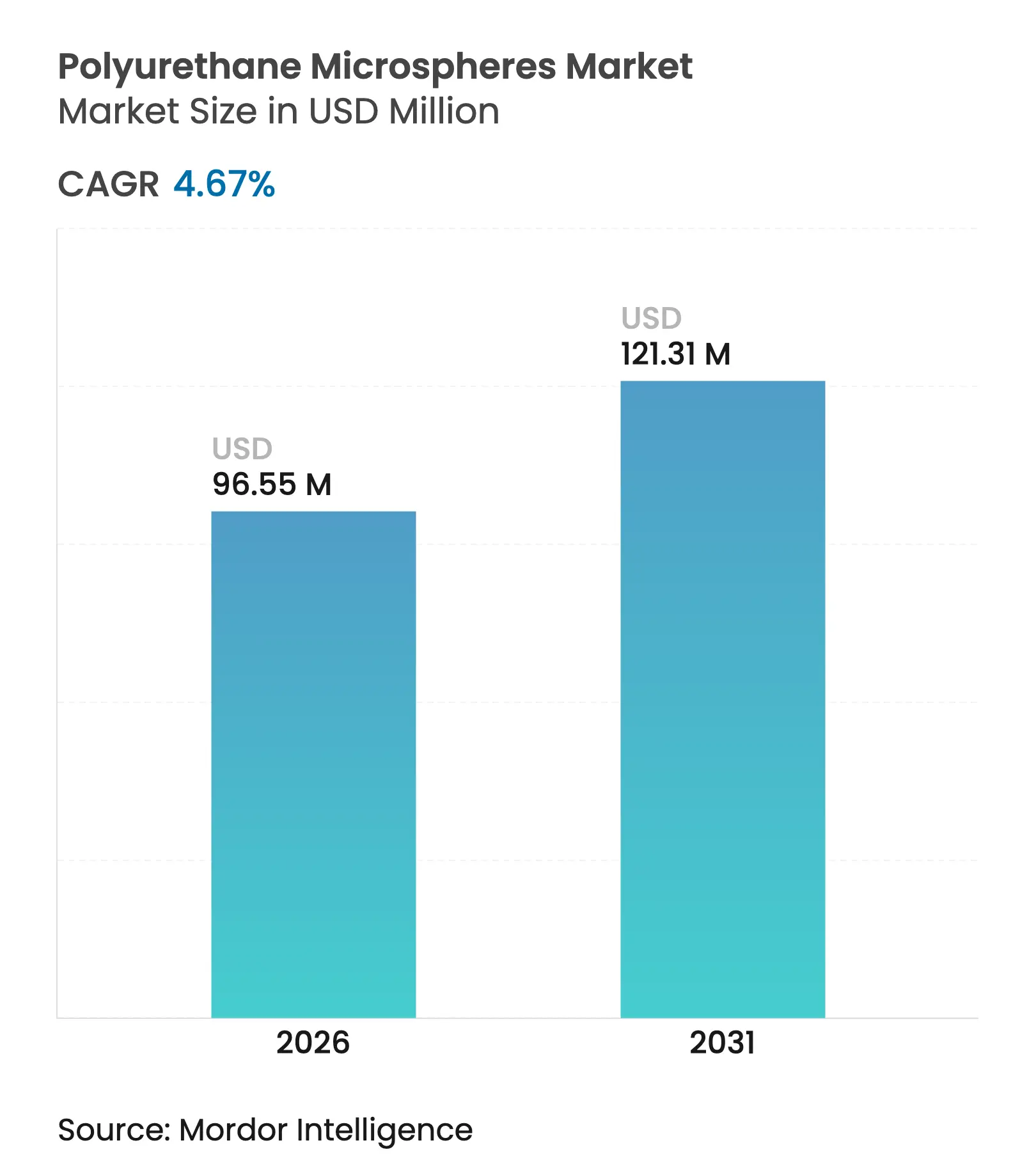

| Market Size (2026) | USD 96.55 Million |

| Market Size (2031) | USD 121.31 Million |

| Growth Rate (2026 - 2031) | 4.67 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Polyurethane Microspheres Market size in 2026 is estimated at USD 96.55 million, growing from 2025 value of USD 92.24 million with 2031 projections showing USD 121.31 million, growing at 4.67% CAGR over 2026-2031. Demand is concentrated in high-performance sectors that value functional attributes such as weight reduction, thermal insulation and controlled release over sheer volume, allowing producers to defend premium pricing. Asia-Pacific supplies almost half of global volumes thanks to integrated supply chains and a dense electronics manufacturing base that accelerates product qualification cycles. Hollow variants dominate because they can cut coating density by up to 46% without sacrificing mechanical strength. At the same time, expandable grades are climbing fastest as 3-D printing, automotive and construction users search for lightweight foamed structures. Regulatory moves-—notably the EU REACH rule mandating training for workers handling products with more than 0.1% diisocyanate—are steering R&D budgets toward low-emission and bio-based chemistries.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand from paints and coatings Rising demand from paints and coatings | +1.20% | Global, with strong growth in APAC and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.20% | Geographic Relevance:Global, with strong growth in APAC and North America | Impact Timeline:Medium term (2-4 years) |

Surge in high-performance micro-encapsulation for pharma and agrochemicals Surge in high-performance micro-encapsulation for pharma and agrochemicals | +0.80% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Growth of 3-D printing inks and UV-curable coatings Growth of 3-D printing inks and UV-curable coatings | +0.60% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Expansion in reactive hot-melt electronics adhesives Expansion in reactive hot-melt electronics adhesives | +0.40% | APAC core, spill-over to North America | Short term (≤ 2 years) | |||

Integration in fragrance micro-capsules for detergents Integration in fragrance micro-capsules for detergents | +0.30% | Global, with premium market focus | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand from Paints and Coatings

Automotive, industrial and architectural coaters deploy hollow polyurethane microspheres to cut wet-film weight by up to 46% while maintaining mechanical resilience. U.S. automakers alone consumed 142 million lb of polyurethane coatings in 2023, split almost evenly between OEM and refinish operations. Regulatory caps on VOCs are directing formulators toward waterborne and UV-curable binders that pair effectively with microspheres for reduced solvent demand. Thermal-insulation coatings incorporating the spheres deliver 45.2% lower thermal conductivity and lift tensile strength from 14.16 to 22.14 MPa, a key selling point for energy-efficient buildings. Nouryon’s 2024 launch of partially bio-based Expancel BIO grades aligns with OEM sustainability pledges while preserving recovery performance under 350 bar spray pressure.

Surge in High-Performance Micro-Encapsulation for Pharma and Agrochemicals

Polyurethane microspheres enable oral, injectable and transdermal drug products that modulate release kinetics, boosting patient adherence and minimizing side effects. Emulsion and polycondensation routes permit insertion of targeting ligands, while AI-driven formulation tools streamline excipient selection for precise payload delivery. In agrochemicals, encapsulated actives reduce runoff and volatilization, extending field efficacy windows and curbing environmental impact. Bio-based diisocyanates from D-galactose promise to eliminate phosgene, advancing green-chemistry credentials without compromising shell strength. Resulting demand underpins a rising premium niche within the polyurethane microspheres market.

Growth of 3-D Printing Inks and UV-Curable Coatings

Additive-manufacturing platforms such as digital light processing rely on UV-curable polyurethane oligomers that reach tensile strengths of 36.8 MPa and Shore hardness 91 in complex lattice parts. Hyperbranched waterborne systems achieve 80% C=C conversion in 50 s while preserving water resistance, enabling on-demand label and package graphics that comply with VOC limits. Rubber-seed-oil acrylates lower critical exposure energy to 15.2 mJ cm², enhancing print throughput versus petro sources. Expandable microspheres add foamed internal structures that cut part weight yet retain dimensional accuracy, a key advantage for footwear midsoles and drone casings. These performance gains sustain a robust, high-margin corridor within the polyurethane microspheres market.

Integration in Fragrance Micro-Capsules for Detergents

Consumer brands embed polyurethane/urea capsules with up to 73% fragrance payload that withstand spray-dry temperatures yet release aroma on fabric friction. Multi-stimuli shells that burst under UVA or humidity cues deliver premium sensory experiences in detergents and apparel, generating brand-differentiation premiums. The technology safeguards volatile oils, lowers dosage and reduces packaging footprint, boosting sustainability metrics. Detergent formulators therefore represent a steadily expanding niche buyer group inside the polyurethane microspheres market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High production and processing costs High production and processing costs | -0.90% | Global, particularly affecting smaller manufacturers | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.90% | Geographic Relevance:Global, particularly affecting smaller manufacturers | Impact Timeline:Short term (≤ 2 years) |

Volatility in MDI and polyol prices Volatility in MDI and polyol prices | -0.50% | Global, with regional variations in supply chains | Medium term (2-4 years) | |||

Stringent emission regulations on di-isocyanates Stringent emission regulations on di-isocyanates | -0.70% | Global, with EU leading through REACH, followed by North America and expanding to APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Production and Processing Costs

Suspension and interfacial polymerization lines require explosion-proof reactors, precise temperature control and advanced QA instruments, pushing capex beyond the reach of many SMEs[1]U.S. Environmental Protection Agency, “Methylene Diphenyl Diisocyanate (MDI) Action Plan,” epa.gov. REACH now obliges retraining every five years for any job role exposed to greater than or equal to 0.1% diisocyanate, further lifting overheads. Micro-emission hot-melts containing less than 0.1% free isocyanate mitigate the regulatory load but demand extra R&D and reformulation effort. Pharmaceutical-grade spheres pass through cGMP audits and extractables testing that inflate unit costs, whereas bio-based feedstocks still price above petro equivalents due to scale limits. These pressure points drag growth by an estimated 0.9 pp in the short term.

Volatility in MDI and Polyol Prices

MDI and polyols account for up to 70% of finished-sphere cost structures, making EBITDA margins extremely price sensitive. Outages at world-scale plants can spike MDI prices, while propylene-glycol expansions like Dow’s 80 kt y-¹ unit in Thailand aim to cushion swings yet take time to filter through. Currency shifts amplify volatility for APAC exporters serving dollar-denominated contracts. Although long-term supply deals and vertical integration dampen shocks for majors, smaller polyurethane microspheres industry entrants often pass costs to customers or defer capacity additions, trimming CAGR by 0.5 pp over the medium term.

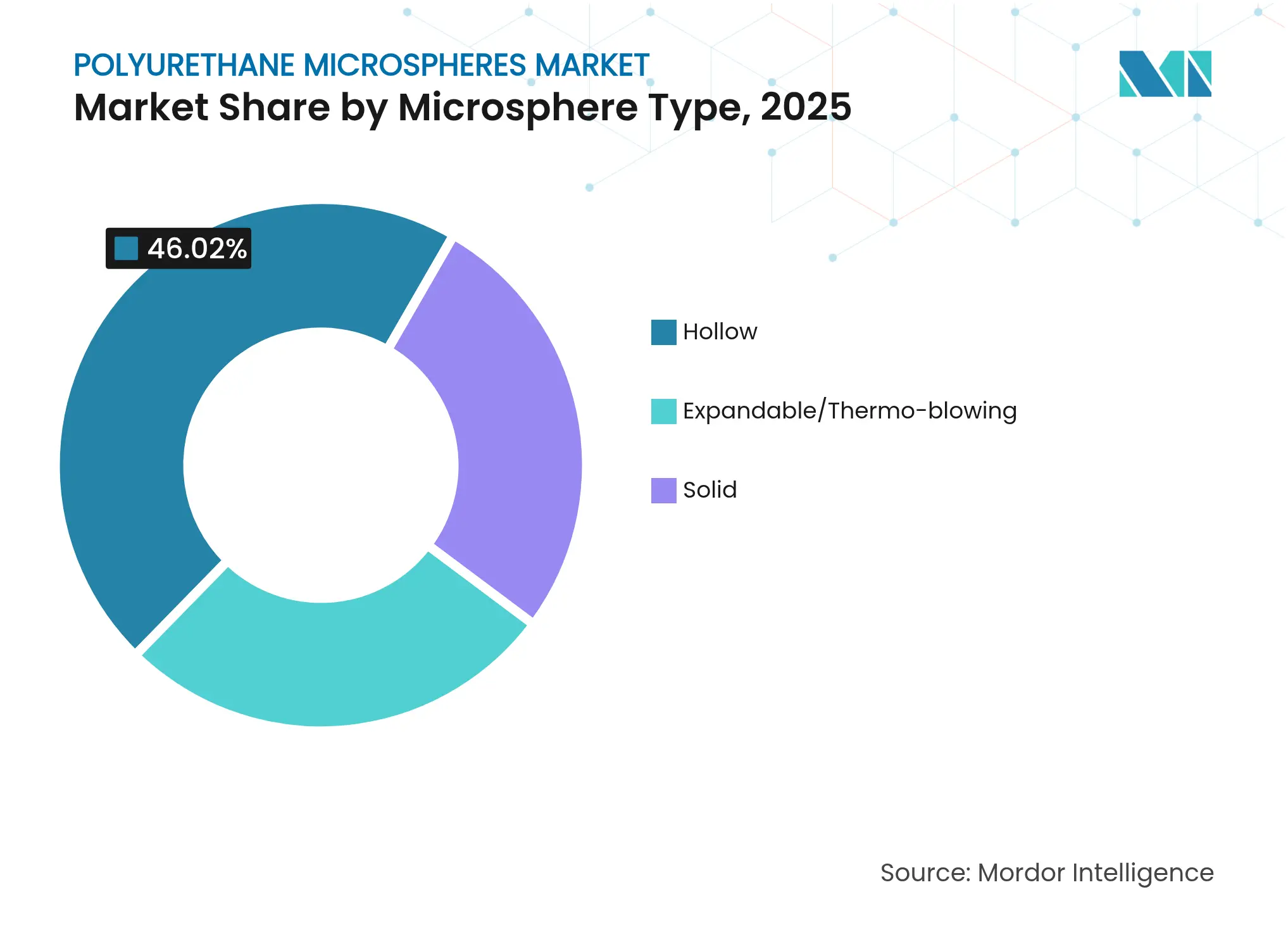

By Microsphere Type: Hollow Variants Drive Lightweight Innovation

Hollow grades captured 46.02% of the polyurethane microspheres market share in 2025, reflecting their ability to cut composite density by as much as 46% in automotive panels and insulation paints. The segment anchors the polyurethane microspheres market because transportation OEMs prioritize mass reduction to extend EV range and meet CO₂ targets. Electrospraying now furnishes porous-shell spheres with tunable diameters down to 5 µm, boosting surface area for adsorbent and drug-delivery uses.

Expandable variants, though smaller in volume, are forecast to post a 4.82% CAGR, the fastest within the polyurethane microspheres market, as construction panels, footwear foams and 3-D printed lattices benefit from their 3.4-4.3× expansion ratio at around 112 °C. Solid spheres remain niche staples for abrasion-resistant coatings and high-purity pharma carriers where structural integrity trumps weight savings.

Note: Segment shares of all individual segments available upon report purchase

By Raw Material: Aromatic Dominance Faces Aliphatic Challenge

Aromatic systems held 59.88% of 2025 revenue, underpinned by cost-efficient MDI supply integrated into automotive and industrial coating chains. Yet aliphatic formulations are projected to outpace the overall polyurethane microspheres market at 5.01% CAGR because UV stability and non-yellowing traits appeal to premium outdoor coatings and luxury automotive topcoats.

Bio-based diisocyanates synthesized from D-galactose mark a turning point: they remove phosgene and lower carbon impact while matching aromatic reactivity. Meanwhile, CO₂-derived polyols can displace up to 30% fossil feedstock, providing cost hedges against crude swings and burnishing ESG scores.

By Application: Encapsulation Emerges as Growth Leader

Paints and coatings commanded 35.10% of polyurethane microspheres market size in 2025, benefiting from the ongoing shift toward lightweight fillers in automotive and architectural finishes. Durable shells withstand shear up to 350 bar, satisfying robotic spray booth demands.

In contrast, encapsulation is projected to clock a 4.81% CAGR to 2031, the quickest inside the polyurethane microspheres market, propelled by controlled-release drugs, fragrance textiles and agrochemicals that require tight payload protection. Adhesives for electronics and smart-textile coatings add incremental volume, whereas cosmetics leverage the silky tactile feel and optical blurring of microspheres to differentiate premium SKUs.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

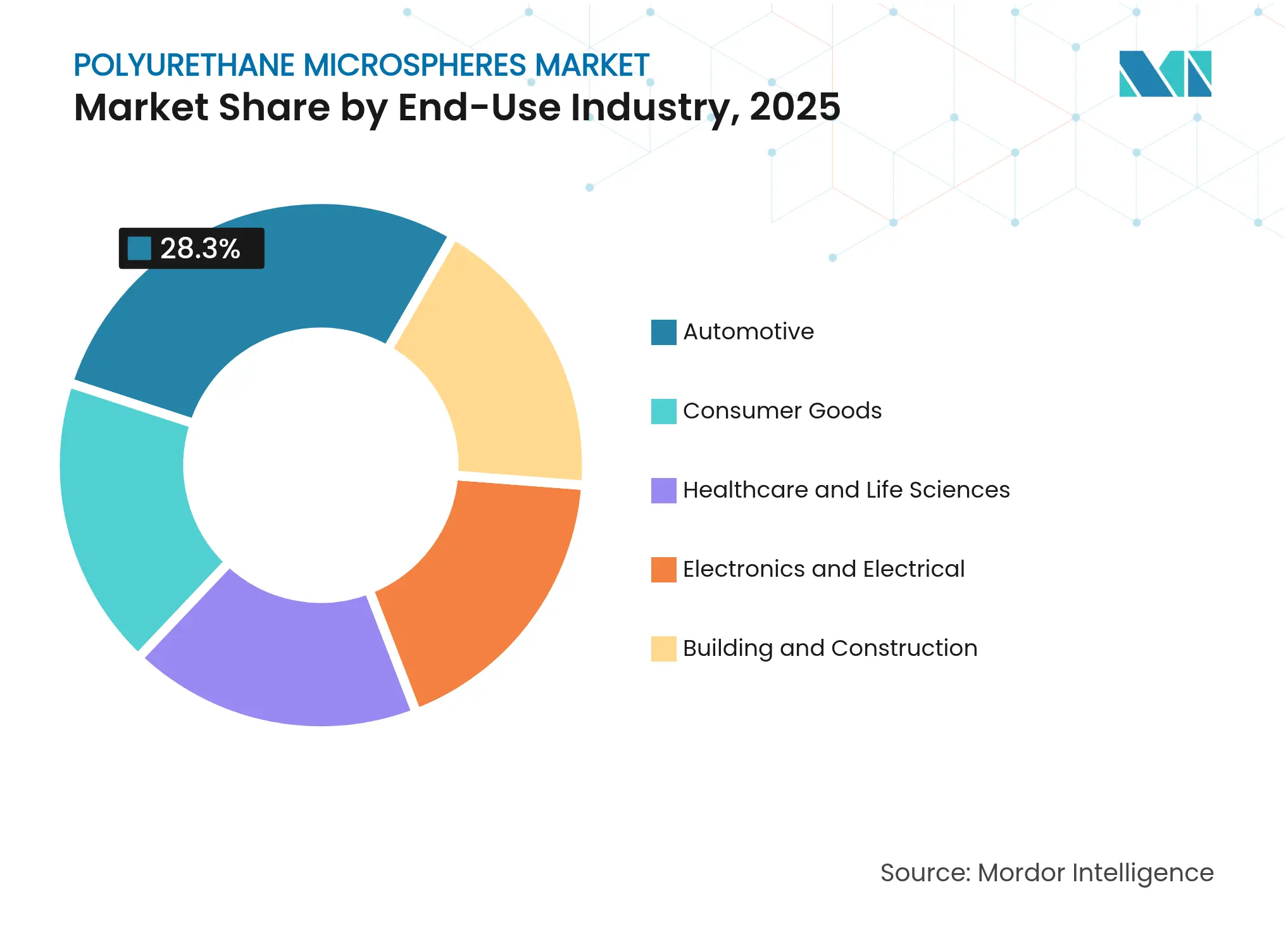

By End-Use Industry: Electronics Sector Accelerates Growth

Automotive applications held 28.30% revenue share in 2025; coatings, NVH foams and lightweight structural inserts anchor this lead. Yet electronics is predicted to grow at 5.02% CAGR, topping all sectors, as semiconductor packaging turns to microsphere fill for ESD suppression and low-κ dielectrics.

Flexible printed circuit boards integrate spheres to balance thermal and mechanical stresses, while wearable devices exploit porous morphologies for breathable sensor housings. Healthcare follows with expanding drug-delivery pipelines and minimally invasive device coatings that demand biocompatible carriers.

Note: Segment shares of all individual segments available upon report purchase

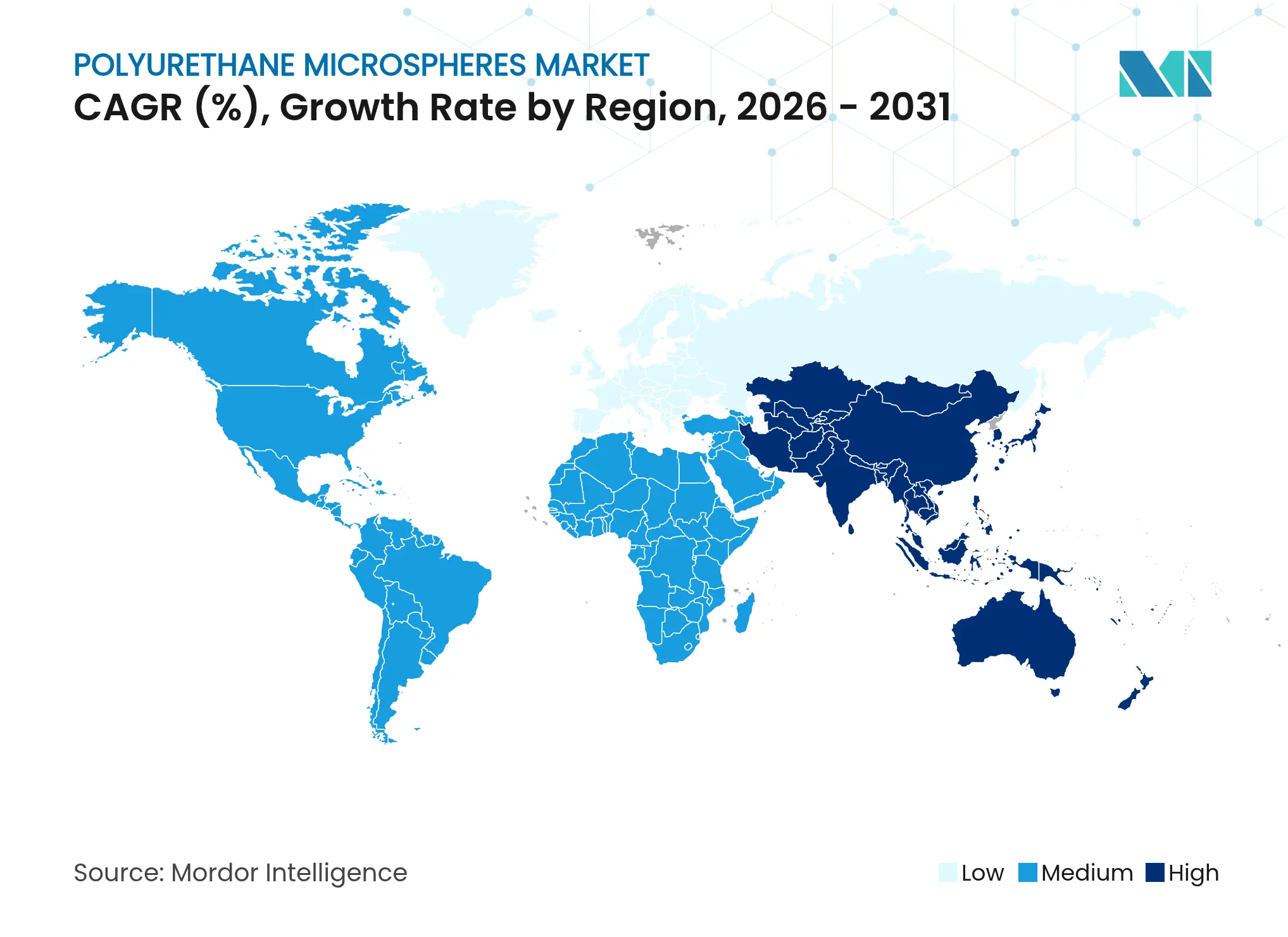

Asia-Pacific retained 45.20% of global volume in 2025 and is expected to chart the fastest 4.73% CAGR through 2031, confirming its central role in the polyurethane microspheres market. China concentrates feedstock and downstream converters in clusters such as Guangdong, trimming logistics costs and accelerating product customization cycles. India’s production-linked-incentive scheme for electronics keeps demand momentum strong, while Japanese firms leverage quality reputations to supply micro-encapsulation to leading pharma brands.

North America represents a technology-driven yet mature buyer base. U.S. automakers coated 142 million lb of vehicle surfaces with polyurethane chemistry in 2023, and OEM push for lighter EV architectures keeps the polyurethane microspheres market engaged. Mexico’s ascent to the fourth-largest polyurethane consumer aligns with near-shoring trends that invite component suppliers to cluster around North-American final assembly hubs.

Europe wields global regulatory influence through REACH and proposed diisocyanate OELs, effectively setting safety baselines for the polyurethane microspheres industry worldwide. German and Italian specialty chemical firms innovate in UV-curable and bio-based systems, while UK policies continue mirroring EU norms post-Brexit. South America plus Middle East & Africa trail in share but record double-digit import growth for construction and mining coatings that value the energy-saving profile of hollow spheres.

Market Concentration

The polyurethane microspheres market displays moderately fragmented concentartion. Chase Corporation generated USD 293.3 million in 2021, with its Adhesives, Sealants & Additives arm supplying aerospace and medical customers that demand tight particle-size controls. Covestro AG couples captive MDI/TDI manufacture with downstream dispersions, enabling cost leverage and rapid new-grade rollouts.

Strategic moves emphasize sustainability: Nouryon opened a Wisconsin Expancel line in 2023 to cut delivery lead-times for North American clients. HB Fuller is commercializing polyurethane polyols with up to 40% captured CO₂, underscoring carbon-reduction ambitions. Henkel’s micro-emission adhesive line addresses REACH compliance while preserving bond strength, offering a template for smaller players confronting regulatory barriers.

Patent filings on micro-encapsulation—such as US 3516941A—remain active, indicating white-space competition in shell chemistries and stimuli-responsive release systems. Acquisition appetite persists: Tosoh’s earlier buy-out of Nippon Polyurethane reflects long-term integration logic that could repeat as Asian producers chase economy-of-scale advantages. Overall, market rivalry hinges on R&D differentiation, regulatory fluency and supply security.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The Polyurethane Microspheres Market report include:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.