Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The United States Micro LED Market Report is Segmented by Application (Smartwatch, Near-To-Eye Devices (AR/VR), and More), End-User Industry (Consumer Electronics, Aerospace and Defense, and More), Panel Size (Micro-Display (Less Than 1 Inch), Small and Medium (1 Inch To 55 Inch), and More), Manufacturing Method (Monolithic Integration, Mass-Transfer Printing, and More) The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

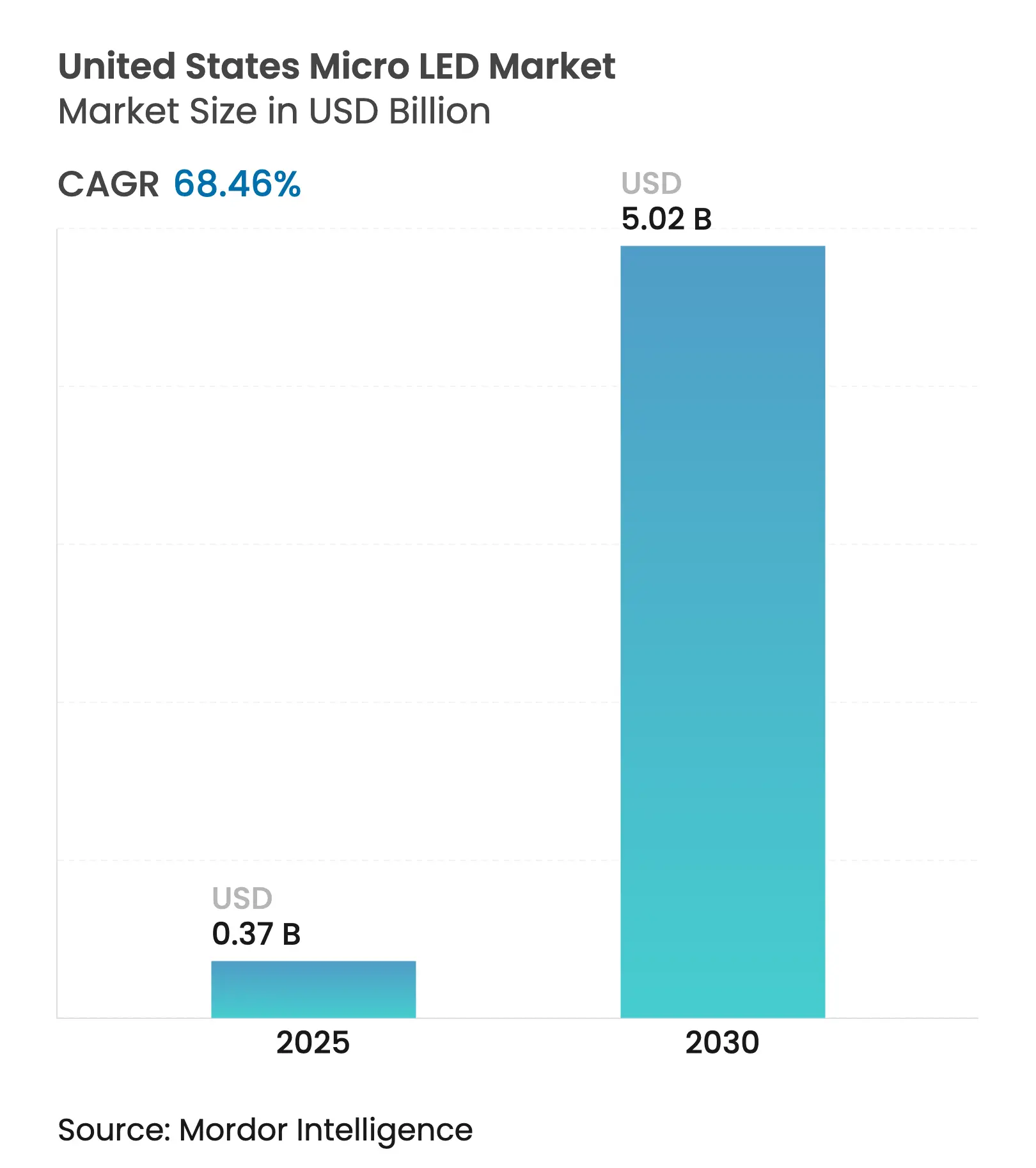

| Market Size (2025) | USD 0.37 Billion |

| Market Size (2030) | USD 5.02 Billion |

| Growth Rate (2025 - 2030) | 68.46 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The United States micro LED market is valued at USD 0.37 billion in 2025 and is forecast to reach USD 5.02 billion by 2030, advancing at a 68.46% CAGR. Federal incentives that promote on-shore semiconductor capacity, breakthroughs in mass-transfer equipment, and early adoption in premium wearables, vehicle head-up displays, and defense optics collectively underpin this very steep growth curve. The CHIPS and Science Act is supplying multibillion-dollar grants and tax credits that lower capital barriers for new fabs, while private‐sector pledges such as TSMC’s USD 65 billion Arizona project confirm that the ecosystem now views the United States as a viable production base.[1]Wayne Wang, “TSMC Arizona Expansion Advances,” tsmc.com Concurrently, the United States patent holders control roughly one-third of global micro LED intellectual property, reinforcing domestic technology leadership. Micro-display demand from AR/VR prototypes under development at leading platform companies is accelerating near-term volume, and automotive suppliers are integrating high-brightness micro LED head-up displays to meet advanced driver assistance requirements. Supply-chain resilience strategies further motivate brands to dual-source away from East Asian capacity, placing additional upside pressure on domestic output.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for ultra-bright power-efficient premium displays Rising demand for ultra-bright power-efficient premium displays | +12.5% | Global with hubs in California | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+12.5% | Geographic Relevance:Global with hubs in California | Impact Timeline:Medium term (2-4 years) |

United States CHIPS Act incentives for on-shore micro-display fabs United States CHIPS Act incentives for on-shore micro-display fabs | +8.2% | Arizona, Texas, New York | Long term (≥ 4 years) | |||

Accelerating adoption in AR/VR headsets by FAANG companies Accelerating adoption in AR/VR headsets by FAANG companies | +15.3% | West Coast expanding to Northeast | Short term (≤ 2 years) | |||

DoD soldier-worn AR procurement pipeline DoD soldier-worn AR procurement pipeline | +6.8% | Virginia and California facilities | Medium term (2-4 years) | |||

Automotive HUD mandates for windshield-integrated micro LED Automotive HUD mandates for windshield-integrated micro LED | +9.4% | Michigan automotive corridor | Long term (≥ 4 years) | |||

Domestic tool-maker breakthroughs in high-throughput mass-transfer Domestic tool-maker breakthroughs in high-throughput mass-transfer | +11.1% | California, Massachusetts, New York | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising demand for ultra-bright, power-efficient premium displays

Micro LEDs comfortably exceed the 10,000-nit brightness threshold that smartwatch, HUD, and outdoor signage brands now specify, yet they still operate at lower power than OLED or LCD counterparts. In 2024 Mojo Vision demonstrated a 14,000 pixels-per-inch red micro-display that validated quantum-dot color conversion as an efficient route to wide-gamut output. High luminance at low energy draw solves the visibility challenge that limits AR eyewear in sunlight and simultaneously extends battery life in wearables. Supporting technologies such as perovskite color layers further raise achievable color volume while sidestepping rare-earth supply constraints. The net effect is rising OEM willingness to pay for micro-LED performance

United States CHIPS Act incentives for on-shore micro-display fabs

The CHIPS and Science Act allocates grants, loans, and investment tax credits that now cover a meaningful share of fab construction outlays. Entegris, for example, secured USD 77 million to build an advanced materials plant that supports domestic filter pod and slurry production. TSMC’s decision to bring N4 and N3 lines to Arizona elevates U.S. access to leading-edge process technology, an essential foundation for micro LED backplanes. New York’s selection as the first National Semiconductor Technology Center broadens the geography of federal support and reduces single-site risk.[2]New York State Governor’s Office, “New York Lands First National Semiconductor Technology Center,” governor.ny.govOver the long term, cost-share incentives are expected to close the operating-expense delta versus traditional Asian manufacturing clusters.

Accelerating adoption in AR/VR headsets by FAANG companies

Platform companies continue to prototype micro-LED near-to-eye modules even after Apple ended its smartwatch display program. Meta’s Orion prototype, developed with Plessey, achieves multi-million-nit peak luminance that is indispensable for outdoor AR use cases. Foxconn added GaN-on-Si capability via a tie-up with Porotech and intends to begin volume production of AR glasses in 2025. These moves shorten learning curves, divert 6-inch wafer capacity toward micro-display die, and validate demand pipelines sufficient to attract equipment suppliers.

DoD soldier-worn AR procurement pipeline

Military programs offer early commercial traction because extreme performance requirements justify premium pricing. Kopin reported that 82% of its 2024 revenue came from defense contracts, underscoring how soldier-worn optics create stable, high-margin orders.[3]Restraint (~) % Impact on CAGR Forecast Geographic Relevance Impact TimelineRestraint (~) % Impact on CAGR Forecast Geographic Relevance Impact TimelineThe FY 2024 National Defense Authorization Act authorizes streamlined acquisition for critical microelectronics, including micro-LED displays. Program of record schedules typically convert prototypes into multi-year production within two to four years, bringing revenue visibility that lowers investor risk.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capex and yield losses High capex and yield losses | -18.7% | Global with acute pressure on U.S. startups | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:-18.7% |

Geographic Relevance

:Global with acute pressure on U.S. startups |

Impact Timeline

:Short term (≤ 2 years) |

Mass-transfer process complexity Mass-transfer process complexity | -14.2% | Arizona, California pilot lines | Medium term (2-4 years) | |||

Compound-semiconductor talent shortage Compound-semiconductor talent shortage | -8.9% | California, Massachusetts, Texas | Long term (≥ 4 years) | |||

Narrow U.S. sapphire-wafer supply base Narrow U.S. sapphire-wafer supply base | -6.3% | East Coast and Midwest fabs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High capex and yield losses

Commercial viability requires yields far above 99.9999% because a single defective diode can spoil an entire panel. Samsung and LG Display reduced micro-LED TV rollouts in mid-2024 after unit economics proved unsustainable for volumes that remain below 2,000 sets per year. Specialized transfer and inspection tools increase fab cost well beyond an equivalent CMOS line, and volatility in high-purity quartz supply, as observed after Hurricane Helene, can raise consumables prices and push break-even further out. Until pilot lines demonstrate repeatable yields, financing remains expensive for newer entrants.

Mass-transfer process complexity

Most manufacturing bottlenecks stem from placing millions of dice onto a backplane with ±1.5 μm precision at industrial speeds. Research published in 2025 achieved 99.3% single-die placement yields using laser-induced forward transfer, yet industry still lacks consensus on how to scale that method to 300 mm wafers. VueReal’s MicroSolid Printing platform claims higher throughput and lower consumable cost, but its USD 40.5 million Series C raise illustrates how capital intensive commercialization remainse. Until the sector converges on a dominant transfer architecture, competing approaches dilute supplier scale benefits.

By Application: AR/VR Drives Next-Generation Adoption

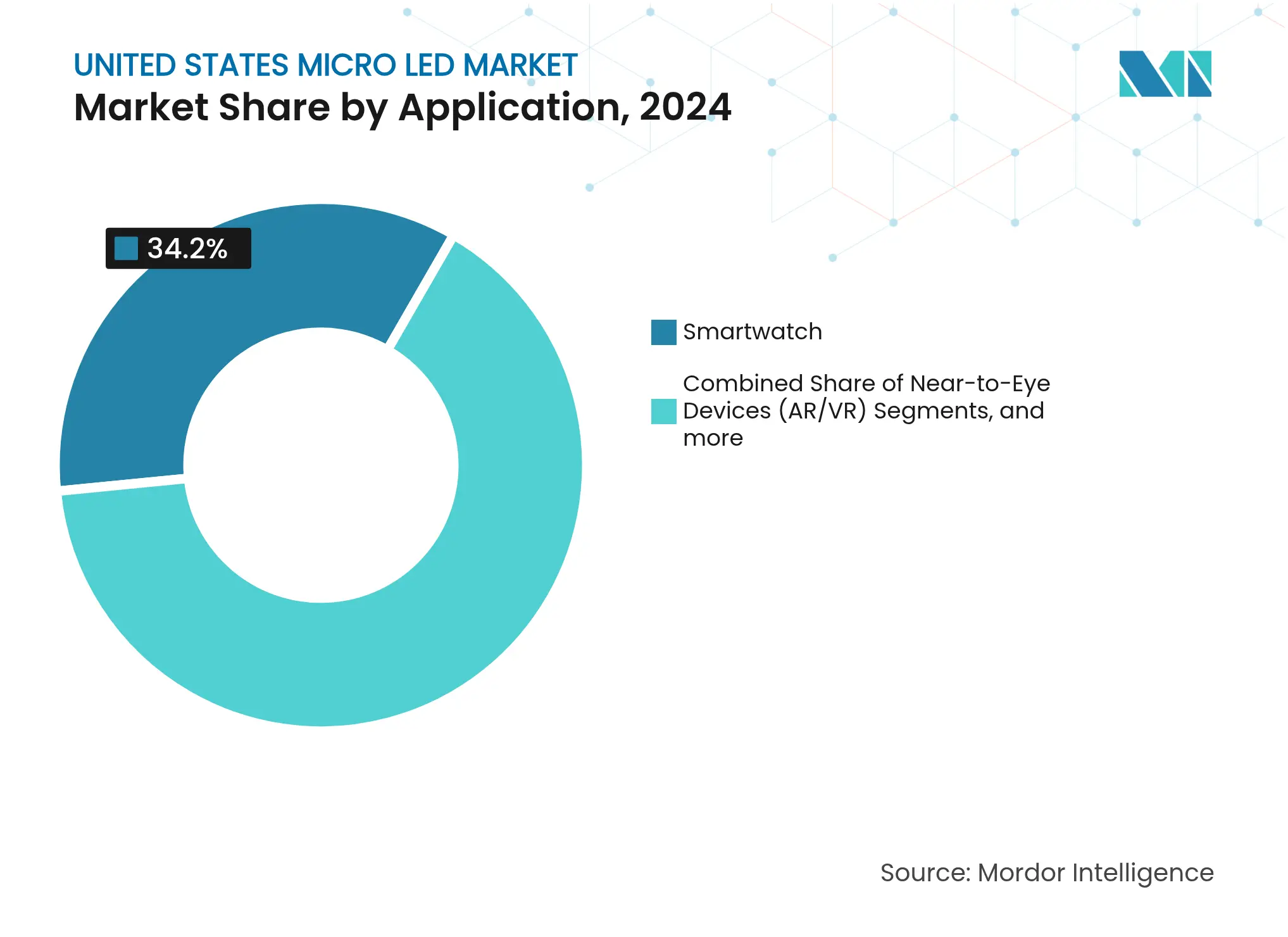

The near-to-eye AR/VR segment records a blazing 72.80% CAGR, making it the fastest-growing slice of the United States micro LED market despite smartwatch displays holding the highest 34.20% revenue share in 2024. Consortium-managed engineering samples such as Meta’s Orion headset show that 6 million-nit micro-LED modules can fit inside lightweight optics, a feat OLED and LCoS struggle to match. As software ecosystems align around spatial-computing use cases, device makers prioritize ultra-high pixel densities that micro LEDs can already reach. In parallel, smartwatch brands experiment with lower-resolution but higher-brightness displays that extend battery life for outdoor fitness. The coexistence of mature and emerging use cases helps diversify fab loading.

Television panels above 55 inches represent a niche yet strategically visible market where micro LEDs deliver bezel-free modularity attractive to luxury consumers. Production economics still restrain volume because the required diode count exceeds 25 million per set, driving yield risk exponentially. Smartphone integration remains technically possible but commercially distant due to extreme cost sensitivity. Monitor and laptop panels fall between those extremes: pixel densities align with present transfer equipment capabilities, and enterprise buyers accept premiums for low burn-in risk and superior HDR.

By End-User Industry: Automotive Acceleration Outpaces Consumer Electronics

Consumer electronics command 61.70% of United States micro LED market size in 2024, yet automotive contracts are on track for a 74.30% CAGR, the fastest among all verticals. Automakers intend to embed micro-LED head-up displays that project vivid driver-assistance cues directly onto windshields, addressing NHTSA proposals that encourage situational-awareness features. Premium vehicle buyers accept higher component prices, which in turn improve supplier margins and de-risk capex. Aerospace and defense remain high-value niches where ruggedized micro-displays operate in harsh environments. Advertising installations enjoy micro LED’s 10,000-nit output for daylight-visible billboards, though that channel adopts at a measured pace as display rental models evolve.

BOE’s prototype transparent HUD and Tianma’s low-reflection panels confirm willingness among tier-one suppliers to pivot toward micro LED solutions. The predictable engineering timeline of automotive platforms, often five years long, affords micro-LED toolmakers an opportunity to align equipment roadmaps with vehicle launch cycles. Meanwhile the consumer electronics sector remains price competitive, pressuring OEMs to find cost reductions through monolithic processes and wafer-level testing.

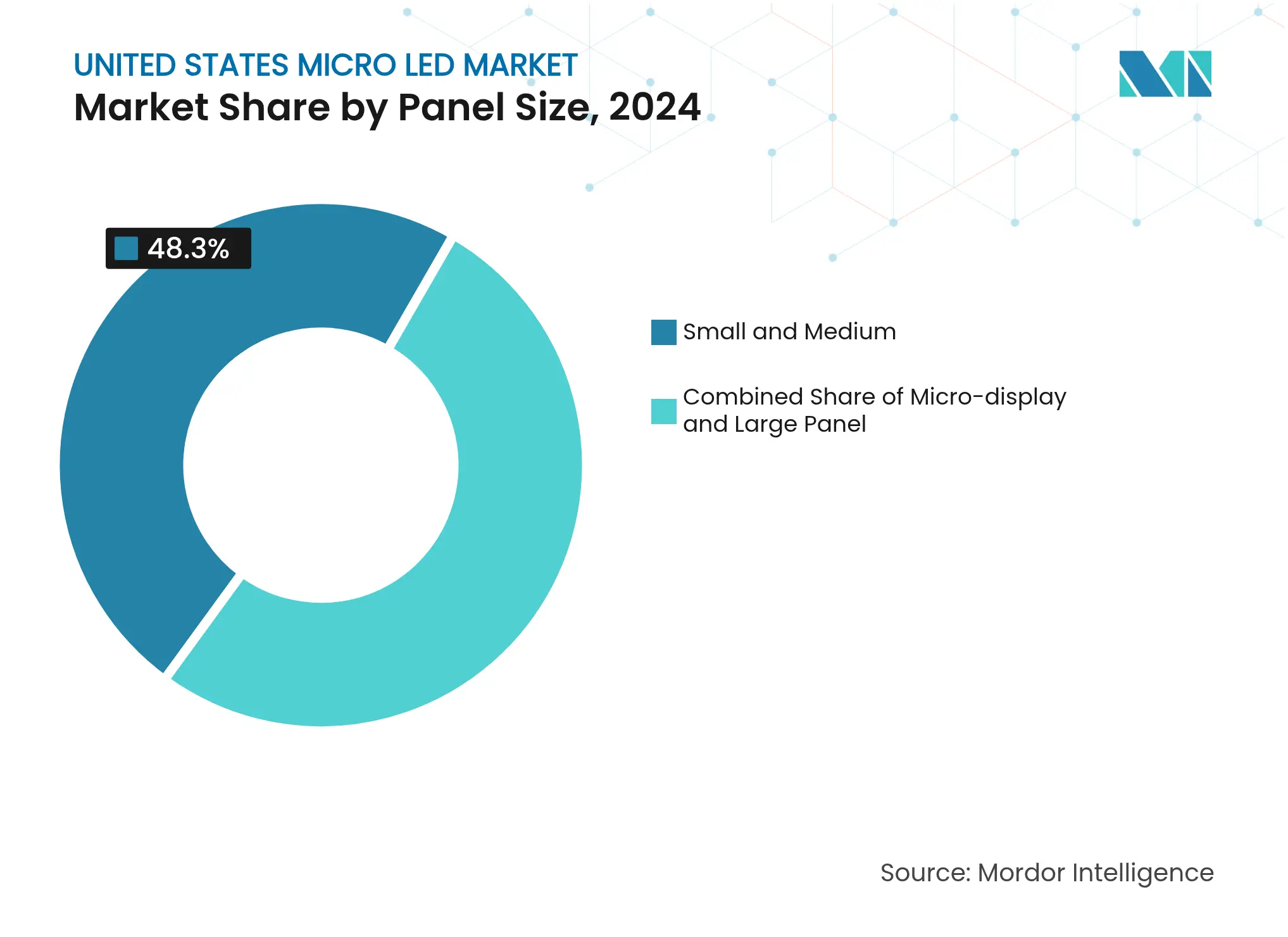

By Panel Size: Micro-Displays Lead Innovation Despite Manufacturing Challenges

Panels smaller than 55 inches accounted for 48.30% of United States micro LED market share in 2024 because smartwatch faces, automotive clusters, and industrial handhelds all demand compact, rugged displays. Micro-displays under 1 inch show the highest 76.40% CAGR through 2030, driven by AR optics and defense scopes that require pixel densities above 3,000 PPI. Researchers recently demonstrated a 0.7-inch active-matrix micro-LED engine at 3,175 PPI, proving that diffraction issues can be mitigated even at visible wavelengths. These breakthroughs validate wafer-level processes able to place tens of thousands of sub-micron LEDs with negligible misalignment.

Large-format TVs and commercial signage panels confront a different set of challenges: the diode count scales with area, and each extra die compounds yield risk. Some vendors pursue a tile-and-seamless-stitch architecture where smaller micro-LED modules form an ultra-large display, though achieving invisible seams remains a work in progress. As mass-transfer costs decline and inspection speeds rise, cost curves are expected to cross below OLED at sizes above 100 inches, opening a new ultra-premium living-room category.

By Manufacturing Method: Monolithic Integration Gains Momentum

Mass-transfer printing retains 57.60% share today because it fits inside existing pick-and-place process flows and can leverage identical backplane geometries used in mini-LED edge-lit modules. However, monolithic integration is projected to surge at 73.20% CAGR by 2030 because it removes the expensive transfer step and improves overall device reliability. ALLOS’ GaN-on-Si wafers allow foundries to grow red, green, and blue emitters directly on 300 mm silicon, avoiding price-volatile sapphire substrates and smoothing the yield curve. Smartkem and AUO demonstrated rollable transparent micro-LED foil displays that rely on low-temperature organic TFT backplanes, suggesting cost parity with OLED for certain form factors.[4]Smartkem PLC, “Rollable Transparent Micro-LED Displays,” ir.smartkem.comHybrid bonding processes occupy the middle ground, combining monolithic epi growth on Si for two colors with transfer of the third to meet color gamut targets while keeping throughput acceptable.

The manufacturing diversification illustrates industry hedging: smartwatch OEMs may stick to transfer printing where toolcap is sunken, whereas AR glasses startups lean toward monolithic epi because volume per part is lower yet yield requirements are more forgiving. Over the forecast horizon, a bifurcation is probable where mass-transfer serves large-area TV panels and monolithic methods dominate micro-displays.

The West Coast generated 43.10% of United States micro LED market revenue in 2024, with California anchoring design wins, venture funding, and university research. Silicon Valley hosts most micro-display startups, while Southern California defense primes validate rugged prototypes against stringent environmental tests. Oregon provides legacy flat-panel talent and fab real estate that can be retooled for micro-LED pilot lines. The region’s 75.10% CAGR to 2030 is underpinned by proximity to FAANG headset programs and an unparalleled pool of compound-semiconductor engineers. VueReal’s fund-raise and Smartkem-AUO collaboration both channel resources into West Coast development centers, reinforcing cluster effects.

The Southwest, namely Arizona and Texas, represents the fastest-growing manufacturing node thanks to concurrent federal and state incentives. Arizona hosts TSMC’s megaproject, which will deliver N3 process capability needed for Si CMOS backplanes that drive micro-LED current sources. Texas lawmakers created the Semiconductor Innovation Consortium and funded a grant program that taps the state’s 43,000-person semiconductor workforce. Together these steps diversify domestic supply risk away from coastal zones prone to natural disasters, while giving equipment vendors a second anchor customer base.

The Northeast focuses on R&D rather than high-volume output. New York won the National Semiconductor Technology Center bid and therefore coordinates large-scale pilot lines and workforce-training curricula NYS. The financial centers of New York City and Boston help emerging micro-LED companies secure growth capital, and federal labs collaborate on advanced heterogeneous integration. The broader Midwest also gathers momentum: Ohio’s Midwest Microelectronics Consortium received federal backing to scale SiC and GaN power fabs that share material science talent with micro-LED epi lines. This multi-node arrangement reduces single-factor dependency and widens the talent funnel.

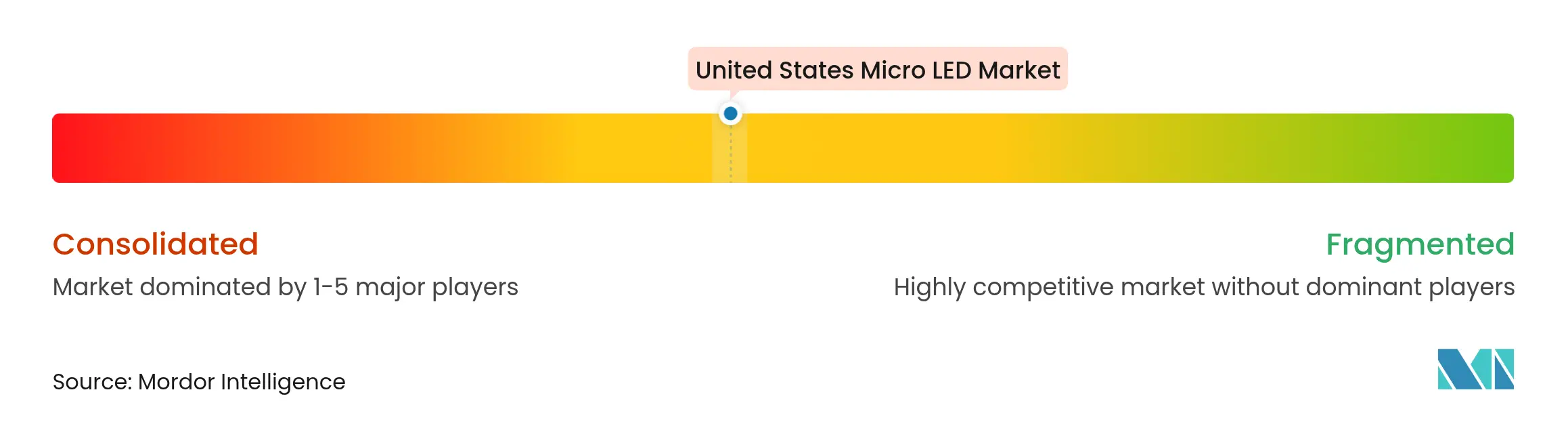

Market Concentration

The United States micro LED market remains moderately fragmented. Legacy panel giants such as Samsung and LG Display slowed micro-LED TV roadmaps in 2024 after confronting steep cost curves, thereby creating white space for niche innovators. VueReal’s USD 40.5 million infusion will boost its MicroSolid Printing capacity and strikes a template for focused scale-up that does not rely on traditional television volume. Several tool vendors with roots in the semiconductor capital-equipment sector pivoted toward micro-LED pick-and-place heads or wafer bonding gear, enhancing domestic supply autonomy.

Intellectual property concentration is a defining barrier: U.S. applicants control 31% of worldwide micro-LED patents, ahead of China and South Korea. Recent litigation success by Seoul Semiconductor at the Unified Patent Court against infringers illustrates the increasing commercial value of patents that cover epitaxy layouts and mass-transfer mechanics. Company roadmaps hint at diversification plans: AUO invests in transparent vehicle displays; ams OSRAM leverages optoelectronic depth to target micro-LED backlighting for lidar sensors; and Foxconn integrates GaN epi into its contract-manufacturing stack, expanding beyond handset assembly.

Price pressure persists, yet high-margin niches in defense, medical imaging, and outdoor signage afford early cash flow. Strategic alliances between material suppliers, epitaxial wafer producers, and toolmakers mirror the complex needs of heterogeneous integration and reduce the risk that one failure node stalls an entire build-of-materials chain. Consolidation is expected once a dominant transfer technology surfaces and cost curves bend toward mass-market television.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. Market Size & Growth Forecasts (Values)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the United States micro-LED market as the annual revenue generated from newly manufactured, emissive display and lighting modules whose individual sub-pixels are formed by gallium-nitride or gallium-arsenide micro-scale LEDs (typically <=100 um) that are directly addressed on glass, silicon, or flexible backplanes. These units span wearable, infotainment, automotive, signage, and specialty lighting form factors and include integrated driver ICs and transfer services.

(Scope exclusion) Mini-LED back-lighting arrays, conventional LED packages, and replacement components for legacy LCD/OLED products are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed U.S. equipment makers, AR/VR headset engineers, and sapphire wafer suppliers on the West Coast, as well as procurement managers at tier-one auto OEMs. These discussions validated realistic transfer yields, average selling prices, and regional subsidy uptake, helping us align model assumptions with on-ground sentiment.

Desk Research

We began with public statistics from sources such as the US International Trade Commission, the Bureau of Industry and Security's CHIPS program disclosures, and import shipment trackers like Volza for GaN wafers. Trade bodies, including the Consumer Technology Association and SEMI, offered adoption benchmarks for wearables and display fabs, while peer-reviewed optics journals clarified yield limits for mass transfer. Company 10-Ks and patent filings enriched our cost curves, and proprietary databases, D&B Hoovers for financials and Dow Jones Factiva for deal flow, rounded out competitive landscaping. This list illustrates, yet does not exhaust, the breadth of secondary material reviewed.

Market-Sizing & Forecasting

A top-down build starts with U.S. smartwatch shipments, near-eye headset volumes, automotive display area, and outdoor advertising square-footage, which are then linked to micro-LED penetration rates and panel sizes. Select bottom-up cross-checks, such as sampled FOB prices x unit counts from supplier roll-ups, calibrate totals. Key model variables include transfer yield progression, average die size, sapphire wafer ASPs, subsidy-driven fab ramp schedules, and AR/VR headset penetration in gaming households. A multivariate regression, back-tested against 2019-2024 demand inflections, projects the 2025-2030 CAGR, while scenario analysis cushions policy and capex shocks. Data gaps in emerging segments were bridged by applying conservative adoption ramps derived from expert interviews before final triangulation.

Data Validation & Update Cycle

Outputs pass a three-step peer review, anomaly flags trigger model re-runs, and material events, such as major fab announcements, device launches, or subsidy awards, prompt interim updates. Reports refresh annually; a final analyst sweep occurs just before release to ensure clients receive the most current view.

Why Our United States Micro LED Baseline Commands Reliability

Benchmark comparison

Published estimates differ because firms select dissimilar device mixes, conversion rates, and refresh cadences.

Key gap drivers include some studies that count only display-class panels, others that extrapolate from headline capacity instead of shipped modules, and several that convert revenues using mid-2023 ASPs that ignore rapid cost erosion following CHIPS-funded lines.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 0.37 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 0.18 B (2024) | Global Consultancy A | Narrow display scope; single-year CAGR overlay; limited primary validation | ||

USD 0.11 B (2024) | Industry Association B | Capacity-based estimate; aggressive 95 % yield assumption; excludes AR/VR modules |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.