Microcrystalline Cellulose Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

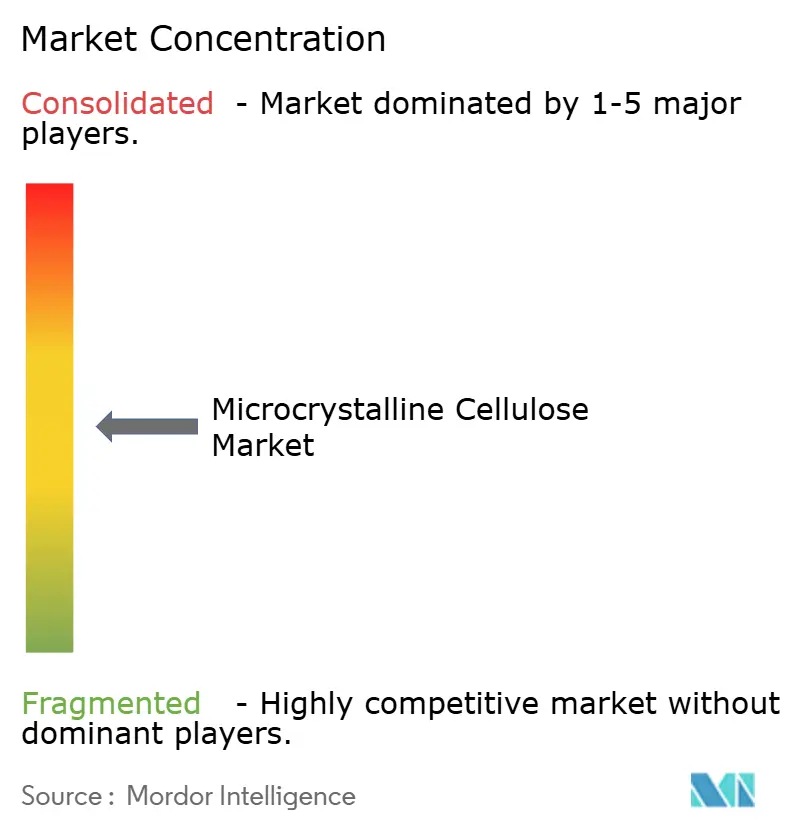

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microcrystalline Cellulose Market Analysis by Mordor Intelligence

The microcrystalline cellulose market size was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.43 billion in 2026 to reach USD 1.94 billion by 2031, at a CAGR of 6.23% during the forecast period (2026-2031). The underlying growth comes from sustained tablet production in emerging pharmaceutical hubs, intensifying clean-label reformulations in packaged foods, and rapid uptake of plant-derived rheology modifiers in natural cosmetics. Energy-efficient steam-explosion lines, agro-residue feedstocks, and regulatory support for biodegradable feed additives further expand the addressable opportunity while mitigating supply-chain and sustainability risks. Moderate competitive intensity keeps innovation centred on process optimisation and geographic proximity to end-users, as producers balance rising power tariffs with tightening dust-emission thresholds.

Key Report Takeaways

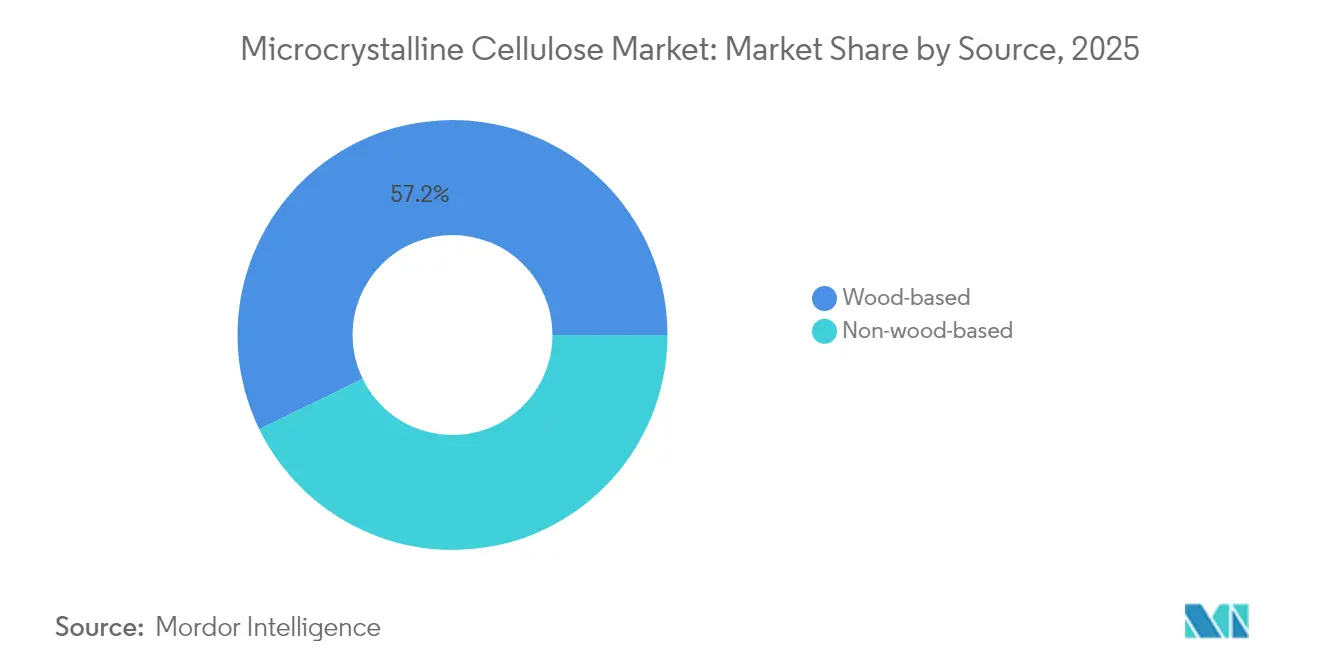

- By source, wood-based microcrystalline cellulose market led with 57.22% revenue share in 2025; non-wood alternatives are projected to expand at a 7.02% CAGR through 2031.

- By process, acid hydrolysis captured 39.72% of the Microcrystalline Cellulose market share in 2025, while steam explosion is forecast to advance at a 6.78% CAGR to 2031.

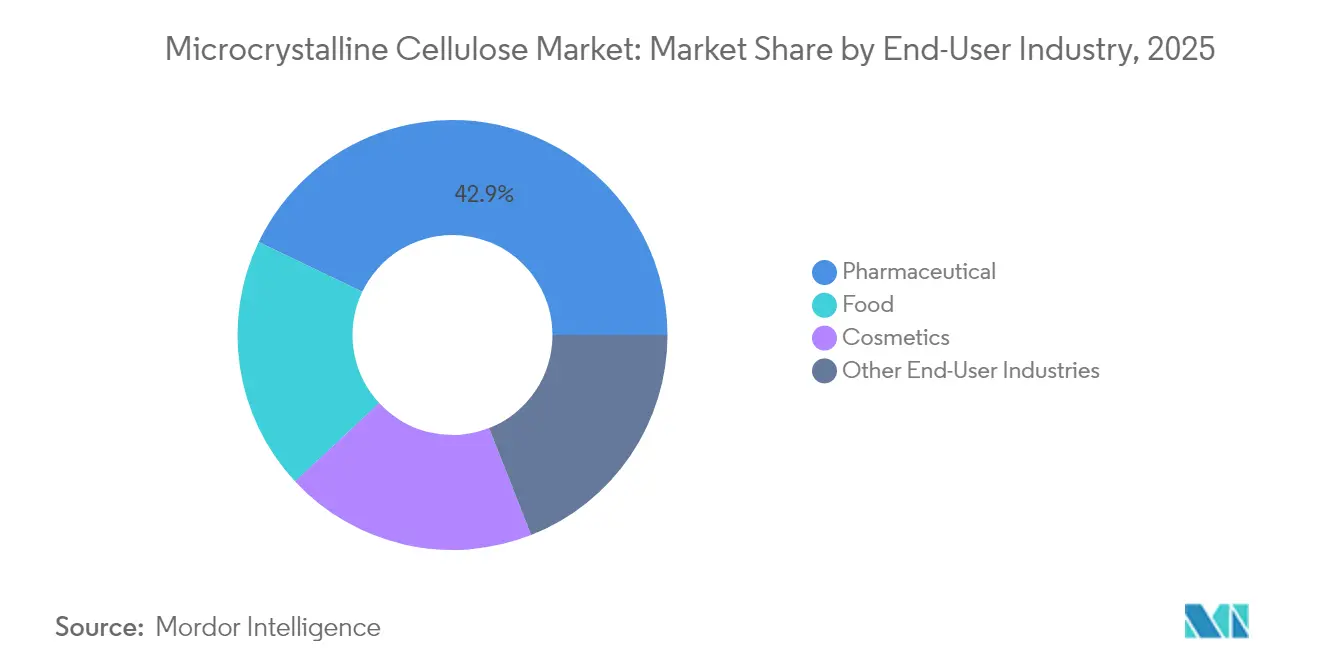

- By end-user, pharmaceuticals accounted for 42.88% of the Microcrystalline Cellulose market size in 2025; cosmetics exhibit the fastest growth at 6.96% CAGR toward 2031.

- By geography, the microcrystalline cellulose market size was led by Asia-Pacific which commanded 37.18% revenue share in 2025 and will remain the fastest-growing region at 6.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microcrystalline Cellulose Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Pharmaceutical Tablet Manufacturing in Emerging Markets | +1.8% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Clean-label Low-fat Food Demand | +1.2% | Global, concentrated in North America & EU | Long term (≥ 4 years) |

| Cosmetics Shift to Natural Rheology Modifiers | +0.9% | Global, early adoption in EU | Medium term (2-4 years) |

| Adoption of Agro-residue Feedstocks (Rice Straw, Bamboo) | +0.7% | APAC core, emerging in South America | Long term (≥ 4 years) |

| Regulations Favouring Biodegradable Feed Additives | +0.5% | EU leadership, expanding to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Pharmaceutical Tablet Manufacturing in Emerging Markets

Pharmaceutical manufacturing migration to cost-advantaged regions accelerates MCC demand as generic drug production scales exponentially in India, China, and Southeast Asia. Sigachi Industries exemplifies this trend, operating three manufacturing plants at over 95% capacity utilization while expanding capacity by 50% to meet export demand that comprises 75% of sales. Intensifying generic-drug output in India, China, and Southeast Asia propels the microcrystalline cellulose market as producers move toward direct-compression tablets that avoid wet granulation steps. Sigachi Industries’ three Indian plants now run above 95% utilisation, with capacity expansion of 50% underpinning 32.1% FY24 revenue growth. Global regulatory harmonisation by World Health Organization (WHO) and Food and Drug Administration (FDA) strengthens demand for premium Microcrystalline Cellulose (MCC) grades, cementing the ingredient’s role as a low-risk excipient amid supply-chain relocation to cost-advantaged regions.

Clean-label Low-fat Food Demand

Consumer health consciousness drives food manufacturers toward MCC as a multifunctional ingredient that enables fat reduction without compromising texture or mouthfeel, supporting growth in the microcrystalline cellulose market. Research demonstrates MCC's superior performance as a fat replacer in reduced-calorie formulations, with studies showing 25% fat replacement in shortcrust biscuits maintaining sensory acceptability while enhancing fiber content. The clean-label movement benefits MCC due to its simple nomenclature and natural wood pulp origin, contrasting favorably with synthetic alternatives facing consumer resistance. European Food Safety Authority (EFSA)'s re-evaluation confirming MCC safety across all food applications, with no numerical acceptable daily intake required, strengthens regulatory confidence for expanded food use. Roquette's MICROCEL product line targeting bakery, snacks, and plant-based meat applications illustrates industry commitment to food-grade MCC development. The intersection of obesity concerns and clean-label preferences creates sustained demand growth as food companies reformulate products to meet evolving consumer expectations.

Cosmetics Shift to Natural Rheology Modifiers

Natural cosmetics formulation trends favor MCC as manufacturers replace synthetic thickeners and stabilizers with plant-derived alternatives that align with sustainability messaging. Patent applications demonstrate MCC's efficacy in decorative cosmetics, where it enhances wrinkle-hiding properties and mattifying effects while improving product stability. JRS's Vivapur and Vivastar brands showcase MCC applications in solid and water-free formulations, addressing consumer preferences for concentrated products with reduced packaging waste. The regulatory advantage of MCC's established safety profile accelerates adoption compared to novel natural ingredients requiring extensive testing. Bacterial cellulose-carboxymethyl cellulose combinations demonstrate surfactant-free formulation potential, addressing market demand for simplified ingredient lists. This transition reflects broader industry recognition that natural positioning commands premium pricing while MCC's functional versatility enables formulators to maintain product performance standards, in the microcrystalline cellulose market.

Adoption of Agro-residue Feedstocks (Rice Straw, Bamboo)

Agricultural waste valorization transforms MCC production economics as manufacturers develop processes to extract cellulose from rice straw, bamboo, and other lignocellulosic residues, strengthening the microcrystalline cellulose market. Research demonstrates rice straw's potential for MCC production with 92.4% cellulose content achievable through organosolv fractionation and alkaline bleaching. Bamboo-derived MCC exhibits superior crystallinity of 77.2% under optimized extraction conditions, positioning it as a viable alternative to wood-based feedstocks. The circular economy imperative drives investment in agro-residue processing as companies seek to reduce dependence on virgin wood pulp while addressing agricultural waste disposal challenges. Steam explosion pretreatment technologies enhance cellulose accessibility from agricultural residues, with process optimization reducing energy requirements compared to traditional acid hydrolysis methods. This feedstock diversification strategy mitigates supply chain risks while potentially reducing raw material costs as agricultural residues typically command lower prices than dedicated wood pulp.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy-intensive Manufacturing Cost | -1.4% | Global, acute in regions with high electricity costs | Short term (≤ 2 years) |

| Substitutes – CMC and Modified Starch | -0.8% | Global, concentrated in food applications | Medium term (2-4 years) |

| Stricter Dust Emission Norms for Fine Powders | -0.6% | North America & EU regulatory leadership | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy-intensive Manufacturing Cost

MCC production's inherent energy intensity creates margin pressure as electricity costs escalate globally and manufacturers confront sustainability reporting requirements. According to techno-economic analyses, acid hydrolysis processes require substantial steam generation and temperature maintenance, with energy representing 15-20% of total production costs. Rising natural gas prices particularly impact European producers, where energy costs exceeded historical averages throughout 2024, forcing operational adjustments and pricing strategies. Manufacturers in microcrystalline cellulose market increasingly evaluate renewable energy integration and process optimization to maintain competitiveness as carbon pricing mechanisms expand globally. The energy intensity constraint particularly affects smaller producers lacking scale economies to invest in efficient technologies, potentially accelerating industry consolidation toward larger, more efficient operations.

Substitutes – CMC and Modified Starch

Carboxymethyl cellulose and modified starch al ternatives challenge MCC in applications where water solubility provides functional advantages over MCC's insoluble characteristics. Comparative studies demonstrate CMC's superior performance in liquid detergent formulations, where thickening properties and cost-effectiveness create competitive pressure on MCC applications. Modified starch derivatives offer cost advantages in food applications where functional benefits cannot justify MCC's premium pricing. The substitution threat intensifies in price-sensitive segments where procurement decisions prioritize cost over performance differentiation. Technological developments in cellulose modification create hybrid products that combine MCC's mechanical properties with improved solubility characteristics, potentially mitigating substitution risks while expanding application possibilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sustainability Drives Non-wood Uptake

Wood-derived feedstock retained 57.22% revenue in 2025 thanks to validated performance and existing qualification dossiers among pharmaceutical customers in the microcrystalline cellulose market. Nonetheless, non-wood alternatives are widening at a 7.02% CAGR as circular-economy legislation favours low-carbon agro-residues with resilient local supply chains. Rice-straw and bamboo extraction technologies reaching ≥92% cellulose yield demonstrate feasibility, underpinning regional mill projects in China and India.

Intensified forestry-management scrutiny in Europe and North America accelerates diversification; in the microcrystalline cellulose market processors utilising cotton-textile waste further embed waste-valorisation credentials while reducing exposure to pulp-price volatility.

By Process: Efficiency Repositions Technology Choices

Acid hydrolysis dominated with 39.72% revenue in 2025 and remains entrenched for legacy multipurpose plants in the microcrystalline cellulose market. Yet steam explosion is ascending at 6.78% CAGR, offering chemical-use reductions and lower effluent burdens, an attractive proposition under emerging carbon-pricing regimes. Reactive-extrusion pilots combine mechanical shear with in-situ neutralisation, flagging potential for single-step continuous manufacture as power-grid greening progresses.

Enzyme-mediated methods, though niche, open specialty-grade avenues requiring minimal mineral impurities, appealing to high-value ophthalmic and injectable formulations. Process flexibility is becoming a procurement criterion as buyers seek suppliers able to pivot raw-material inputs without quality variance.

By End-User Industry: Pharmaceuticals Anchor, Cosmetics Surge

The pharmaceutical sector's 42.88% market share in 2025 reflects MCC's entrenched position as a preferred excipient for tablet manufacturing, where regulatory acceptance and functional consistency outweigh cost considerations. Cosmetics applications demonstrate 6.96% growth acceleration through 2031, driven by natural ingredient preferences and regulatory advantages of MCC's established safety profile. Food applications benefit from clean-label trends and fat replacement functionality, with EFSA safety confirmations supporting expanded use across food categories.

Other end-user industries encompass emerging applications in construction materials, textiles, and biodegradable composites where MCC serves as a sustainable reinforcement agent. The pharmaceutical dominance reflects industry conservatism and regulatory barriers that favor established excipients with extensive safety data and manufacturing experience. However, cosmetics growth acceleration indicates successful market expansion beyond traditional applications as formulators recognize MCC's versatility in natural product development. This end-user diversification strategy reduces pharmaceutical dependence while capturing higher-growth segments aligned with sustainability trends.

Geography Analysis

Asia-Pacific accounted for 37.18% of global revenue in 2025 and is growing fastest at 6.85% CAGR through 2031in the microcrystalline cellulose market size. China’s vertically integrated pharmaceutical ecosystem, India’s excipient export focus, and plentiful agricultural residues underpin the region’s dominance. Japanese and South Korean suppliers contribute high-purity grades, elevating regional quality benchmarks.

North America continues to drive innovation in processing technology and advanced drug-delivery formats, though growth moderates as mature demand equilibrates. The United States benefits from FDA oversight that favours established MCC suppliers with extensive Drug Master File (DMF) dossiers. Europe’s sustainability legislation and European Food Safety Authority (EFSA)’s unconditional safety opinion reinforce demand in both food and cosmetics, positioning the bloc as a regulatory bellwether.

Latin America, the Middle East, and Africa collectively remain nascent but strategically important. Brazil pairs rising pharmaceutical capacity with abundant agro-residues, suggesting future non-wood expansion. Saudi Arabia’s Vision 2030 pharma build-out and South Africa’s generics initiatives represent early-stage beachheads for regional supply chains.

Competitive Landscape

The Microcrystalline Cellulose market is moderately fragmented with the presence of major players, such as J. Rettenmaier & Söhne GmbH + Co KG, DFE Pharma, Asahi Kasei Corporation, and Roquette Frères. Roquette’s 2024 acquisition of IFF Pharma Solutions broadened its drug-delivery excipient suite and secured captive MCC demand for downstream formulations[2]Roquette Press Office, “Roquette Completes Acquisition of IFF Pharma Solutions,” roquette.com. Borregaard AS leverages biorefinery expertise to market sustainably sourced grades from Norwegian wood feedstock, differentiating via low carbon intensity. Emerging disruptors explore nanocellulose gels and textile-waste feedstocks targeting medical-device coatings and 3-D-printing resins. Such niching strategies provide price-premium buffers yet require extensive validation, slowing near-term revenue contributions.

Microcrystalline Cellulose Industry Leaders

Roquette Frères

Asahi Kasei Corporation

DFE Pharma

J. Rettenmaier & Söhne GmbH + Co KG

Sigachi Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nordic Bioproducts Group (NBG) has teamed up with C.Q. Massó to enhance the accessibility of Microcrystalline Cellulose (MCC) for cosmetics manufacturers across Europe. This collaboration aims to bolster supply chain reliability, diminishing the dependence on ingredient suppliers outside the EU.

- February 2023: In Kurashiki, Okayama, Japan, Asahi Kasei completed the construction of its second Ceolus Microcrystalline Cellulose (MCC) plant at its Mizushima Works to address the surging demand for its MCC products.

Global Microcrystalline Cellulose Market Report Scope

Microcrystalline cellulose is a purified, partly depolymerized cellulose made by combining mineral acids with alpha-cellulose obtained as a pulp from fibrous plant content. Air, dilute acids, and most organic solvents are insoluble, although ethanol is partially soluble in a 20% alkali solution. It has a wide variety of applications in prescription excipients and can be used specifically for dry powder tableting. The microcrystalline cellulose market is segmented by source, process, end-user industry, and geography. The market is divided into wood-based and non-wood-based products based on their source. By process, the market is segmented into reactive extrusion, enzyme-mediated, steam explosion, and acid hydrolysis. By end-user industry, the market is segmented into pharmaceutical, food, cosmetics, and other end-user industries. The report also covers the market size and forecasts for the microcrystalline cellulose market in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of revenue (USD million).

| Wood-based |

| Non-wood-based |

| Reactive Extrusion |

| Enzyme Mediated |

| Steam Explosion |

| Acid Hydrolysis |

| Pharmaceutical |

| Food |

| Cosmetics |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Wood-based | |

| Non-wood-based | ||

| By Process | Reactive Extrusion | |

| Enzyme Mediated | ||

| Steam Explosion | ||

| Acid Hydrolysis | ||

| By End-User Industry | Pharmaceutical | |

| Food | ||

| Cosmetics | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for global microcrystalline cellulose demand to 2031?

The market is expected to rise at a 6.23% CAGR from USD 1.35 billion in 2025 to USD 1.94 billion by 2031.

Which end-user currently drives the highest offtake?

Pharmaceuticals hold 42.88% of 2025 volumes because MCC is a preferred direct-compression excipient.

Why is Asia-Pacific both the largest and fastest-growing region?

Consolidated generic-drug manufacturing, lower operating costs, and abundant non-wood feedstocks underpin a 37.18% share and 6.85% growth rate.

How are producers tackling high energy costs in MCC production?

Firms adopt continuous steam-explosion or enzyme-assisted lines that slash steam usage by up to 24%, while co-locating plants near renewable-energy sources.

What sustainability trends influence MCC sourcing?

Rising circular-economy policies drive adoption of rice-straw, bamboo, and textile-waste feedstocks to cut carbon intensity and diversify supply.

Page last updated on: