Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The Microcellular Polyurethane Foam Market Report is Segmented by Type (High-Density and Low-Density), Manufacturing Process (Extrusion Foaming, Injection Foaming and Blow Molding), End-User Industry (Automotive, Building and Construction, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

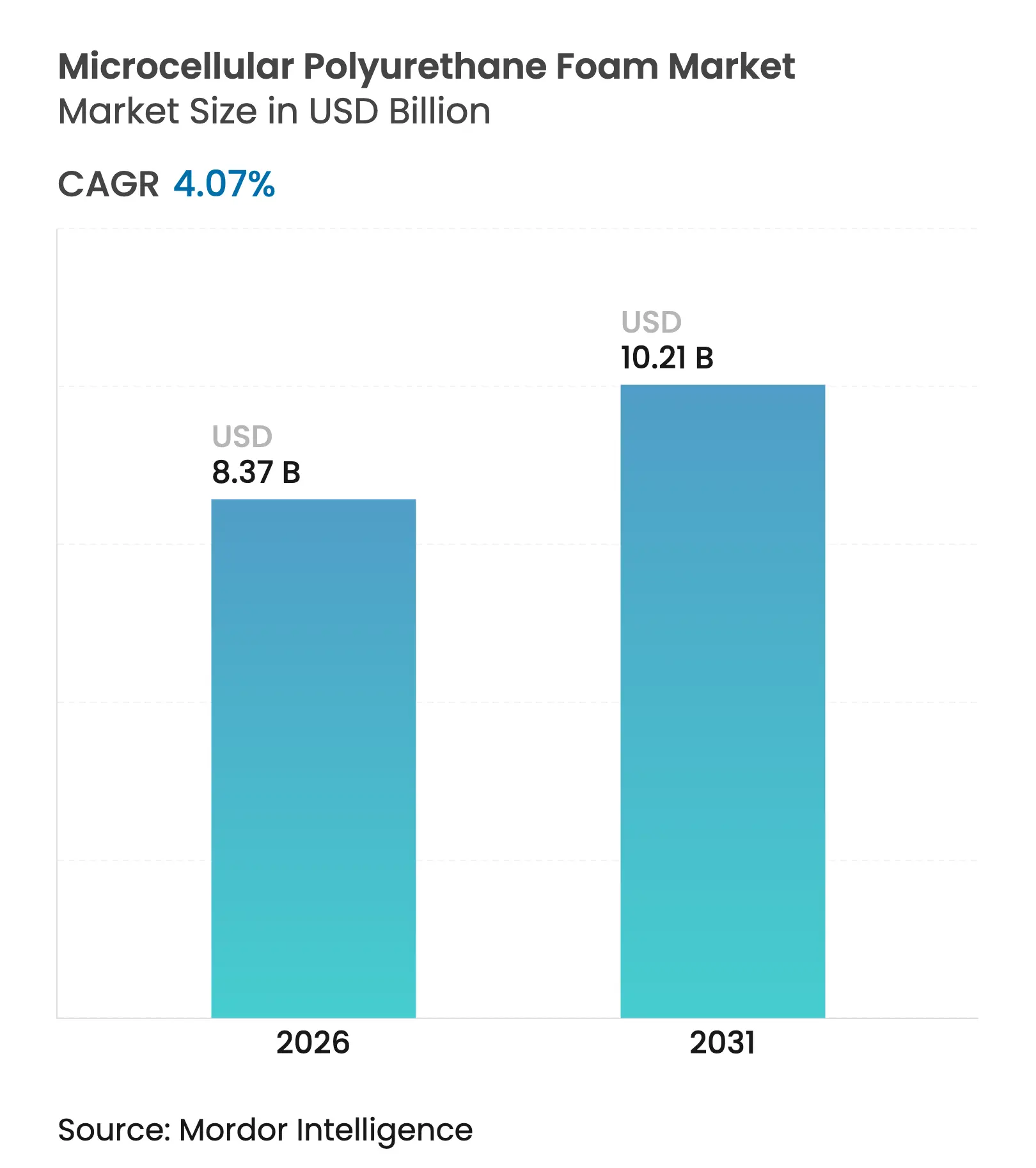

| Market Size (2026) | USD 8.37 Billion |

| Market Size (2031) | USD 10.21 Billion |

| Growth Rate (2026 - 2031) | 4.07 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Microcellular Polyurethane Foam market size is expected to grow from USD 8.04 billion in 2025 to USD 8.37 billion in 2026 and is forecast to reach USD 10.21 billion by 2031 at 4.07% CAGR over 2026-2031. The market benefits from stricter fuel-economy and building-insulation codes that push manufacturers toward lighter, thermally efficient materials. Low-density grades win share because they remove mass from electric vehicles, extend driving range, and simplify interior noise control. Continuous-process technologies such as extrusion foaming are being adopted to cut cycle times, improve quality control, and support higher‐volume orders. Asia-Pacific accounts for nearly half of global demand, and its regulatory shift toward electric mobility and energy-efficient housing is making the region the growth engine for the broader microcellular polyurethane foam market. Meanwhile, recyclability mandates and raw-material volatility set the stage for bio-based and non-isocyanate chemistries that could reset competitive dynamics in the microcellular polyurethane foam market.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Demand for Energy-efficient Insulation in Building

and Construction

Rising Demand for Energy-efficient Insulation in Building

and Construction

| +1.2% | Global, strongest in North America & EU | Medium term (2-4 years) |

( ~ ) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, strongest in North America & EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Lightweighting Push in EV/ICE Automotive Seating and NVH

Parts

Lightweighting Push in EV/ICE Automotive Seating and NVH

Parts

| +0.9% | APAC core, spill-over to North America | Short term (≤ 2 years) | |||

Mandatory Eco-design Regulations Promoting Low-density

Foams

Mandatory Eco-design Regulations Promoting Low-density

Foams

| +0.7% | EU primary, expanding to North America | Long term (≥ 4 years) | |||

Growth of Temperature-controlled E-commerce Logistics

Growth of Temperature-controlled E-commerce Logistics

| +0.5% | Global, early gains in North America, China | Medium term (2-4 years) | |||

Emerging use in Soft Robotics and Wearable Medical Devices

Emerging use in Soft Robotics and Wearable Medical Devices

| +0.3% | North America & EU research hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Energy-efficient Insulation in Building and Construction

Higher R-value codes are turning microcellular polyurethane foam into a compliance tool rather than a discretionary upgrade. International Energy Conservation Code revisions require thinner walls to achieve tighter thermal envelopes, and microcellular grades deliver 30-50% better insulation efficiency than many traditional materials. Utility rebate programs that count air‐sealing benefits add cash incentives on top of code compliance. Huntsman modeling shows that large-scale adoption in U.S. homes could cut annual electricity use by 648.37 Billion kWh, equating to removing 38.9 Million cars from highways[1]Huntsman Corporation, “Spray Foam Energy Impact Study,” huntsman.com. Net-zero building pledges in New York, California, and leading European Union (EU) cities reinforce the need for high-performance foams. Early adopters are already recording measurable payback periods, and published case studies accelerate market acceptance in the wider microcellular polyurethane foam market.

Lightweighting Push in EV/ICE Automotive Seating and NVH Parts

Automakers link every kilogram saved to extra battery range, so they now specify low-density microcellular solutions for seat cushioning, headliners, and acoustic panels. Covestro testing shows density cuts of up to 20% without losing resilience, directly translating to longer driving ranges or lower battery costs. The same microcellular structure absorbs road and wind noise that becomes more noticeable once silent electric powertrains replace combustion engines. Dual-functionality reduces part count and simplifies vehicle assembly, a critical cost lever in mass-market electric vehicle (EV) programs. As EV uptake climbs in China, Europe, and the United States, supply contracts stipulate microcellular polyurethane foam market volumes that exceed historical levels for interior trim foams.

Mandatory Eco-design Regulations Promoting Low-density Foams

EU circular-economy rules now measure material efficiency alongside energy use, giving microcellular grades a compliance edge. Low-global-warming-potential blowing agents became mandatory in January 2025, and microcellular processes that use less agent per volume automatically score higher under the new eco-design metrics. Carbon border adjustment mechanisms will charge importers for embedded emissions from 2026, signaling cost pressure for high-density foams produced abroad. As a result, European converters are pivoting toward density-reduction research and development (R&D) programs, and North American builders expect similar rules within the decade. These policy shifts are reshaping capital-investment priorities across the microcellular polyurethane foam market.

Growth of Temperature-controlled E-commerce Logistics

Direct-to-consumer vaccines, biologics, and chilled food rely on thermal packaging that keeps contents within narrow temperature windows for 48-72 hours. Microcellular polyurethane foam’s low thermal conductivity supports smaller, lighter boxes that meet pharmaceutical guidelines. Phase-change inserts embedded in the foam cut heat ingress by 68% relative to conventional materials. Lower weight translates to reduced shipping fees, a decisive cost factor in parcel-priced logistics. Demand accelerated during the pandemic and continues as tele-health prescription models are established in North America and China. The packaging opportunity, therefore, serves as an incremental growth lever in the microcellular polyurethane foam market.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent Isocyanate and VOC Emission Norms Stringent Isocyanate and VOC Emission Norms | -0.8% | EU primary, expanding globally | Short term (≤ 2 years) |

( ~ ) % Impact on CAGR Forecast

:-0.8% |

Geographic Relevance

:EU primary, expanding globally |

Impact Timeline

:Short term (≤ 2 years) |

High Volatility of MDI/TDI Feedstock Prices High Volatility of MDI/TDI Feedstock Prices | -0.6% | Global, with acute impact in APAC | Medium term (2-4 years) | |||

Competitive Pressure from Bio-based and Recycled Foams Competitive Pressure from Bio-based and Recycled Foams | -0.4% | North America & EU leading, APAC following | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Isocyanate and VOC Emission Norms

Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) restrictions in August 2023 limit diisocyanate concentrations unless plant workers complete certified safety training. Compliance demands extra investment in protected equipment and monitoring systems, hitting small converters hardest. United States spray-foam installers must now observe 14-day Volatile Organic Compound (VOC) off-gassing intervals before building handover, lengthening project schedules and raising working-capital needs. The tightening rules encourage research into non-isocyanate routes, diverting R&D budgets that would otherwise expand conventional capacity in the microcellular polyurethane foam market.

High Volatility of MDI/TDI Feedstock Prices

Methylene Diphenyl Diisocyanate (MDI) and Toluene Diisocyanate (TDI) account for up to 60% of total foam production cost, and quarterly price swings can exceed 20% when feedstock plants shut down for maintenance. Manufacturers, therefore, embed dynamic surcharges into contracts, creating budget uncertainty for downstream users. BASF’s new 300 kiloton MDI line in Geismar and its Zhanjiang build-out will ease tight supply by 2027, but construction delays leave the near-term microcellular polyurethane foam market exposed to cost spikes. Energy-price volatility further amplifies the raw-material challenge because MDI synthesis is power-intensive.

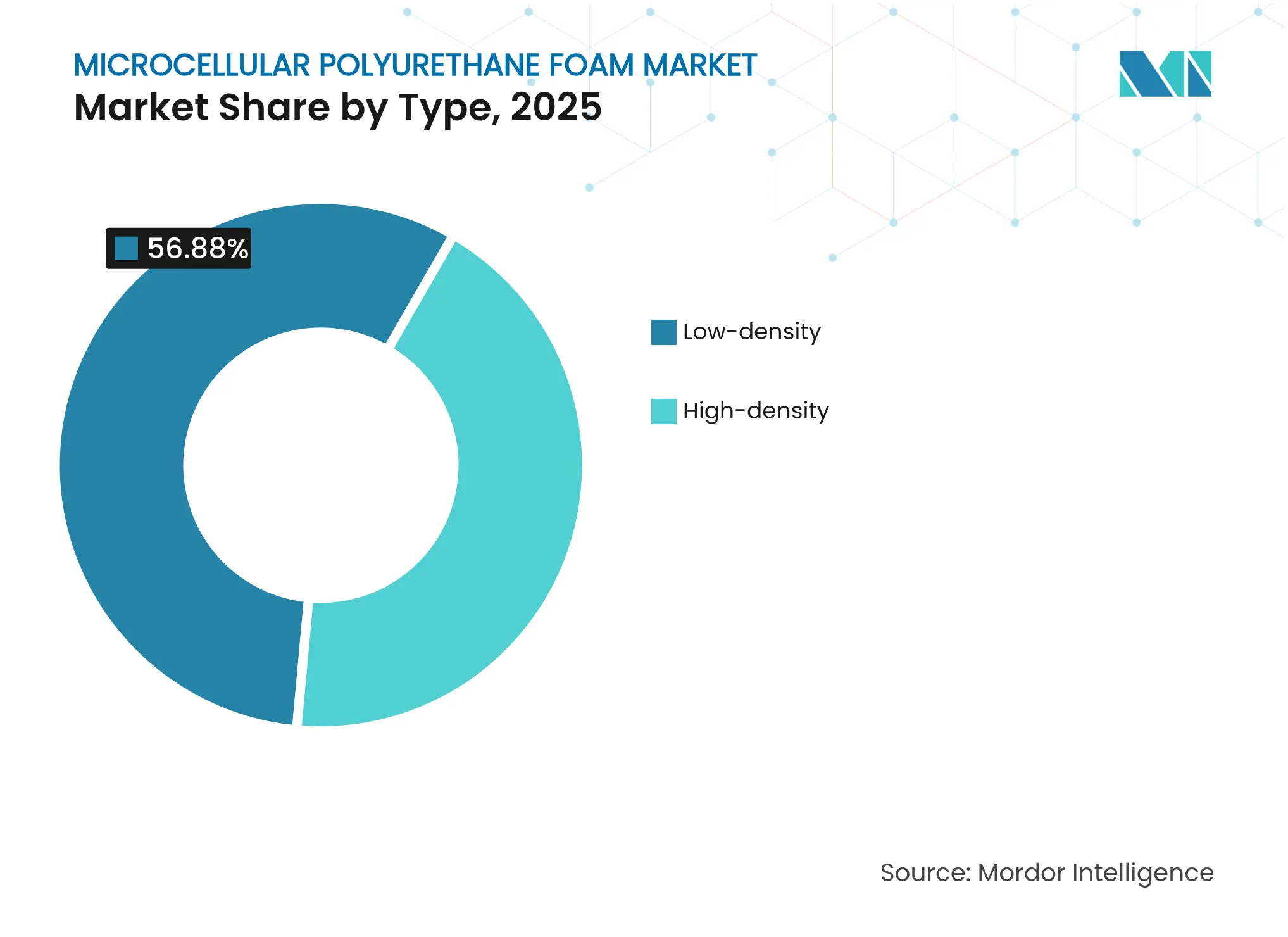

By Type: Low-density Dominance Reflects Lightweighting Imperatives

Low-density grades held 56.88% of the Microcellular Polyurethane Foam market share in 2025 and are expected to grow at a 4.72% CAGR to 2031. Automakers favor these grades because shaving 1 kg of mass can boost EV range by 6-11 km, turning density control into a primary engineering objective. The microcellular polyurethane foam market size for low-density variants is projected to reach USD 5.99 Billion by 2031, reflecting stable demand from car seating, headliners, and acoustic barriers.

High-density foams remain essential in aircraft flooring panels, load-bearing building elements, and heavy-duty industrial seats, but they grow more slowly because regulatory incentives seldom reward extra mass. Bio-based low-density foams, now in pilot production at INOAC (Innovation and Action), contain 50% renewable polyols and cut embodied carbon without compromising mechanical strength. Advanced super-critical foaming lets converters create gradient-density parts that place stiff cores under soft skins, combining comfort and structural integrity in one molded article within the microcellular polyurethane foam market.

Note: Segment shares of all individual segments available upon report purchase

By Manufacturing Process: RIM Leadership Faces Extrusion Challenge

Reaction Injection Molding captured 44.63% of the Microcellular Polyurethane Foam market share in 2025, thanks to its long track record in automotive and furniture shells. The Microcellular Polyurethane Foam market size tied to Reaction Injection Molding (RIM) parts is projected to expand to USD 4.54 Billion by 2031, even as its share erodes. Continuous extrusion foaming is growing faster, at 4.78% CAGR, because it supports inline quality monitoring and lower scrap rates that large Original Equipment Manufacturers (OEMs) demand.

Covestro’s next-generation Reaction Injection Molding (RIM) resins accept recycled Polyethylene Terephthalate (PET) polyols, closing material loops while preserving fast cure cycles. Extrusion foaming, meanwhile, has adopted super-critical CO₂ blowing technology that avoids flammable agents and reduces post-expansion shrinkage. Injection foaming and blow molding defend niches like shoe midsoles and office armrests where complex geometries matter. Process selection thus hinges on part size, throughput needs, and sustainability scorecards across the microcellular polyurethane foam market.

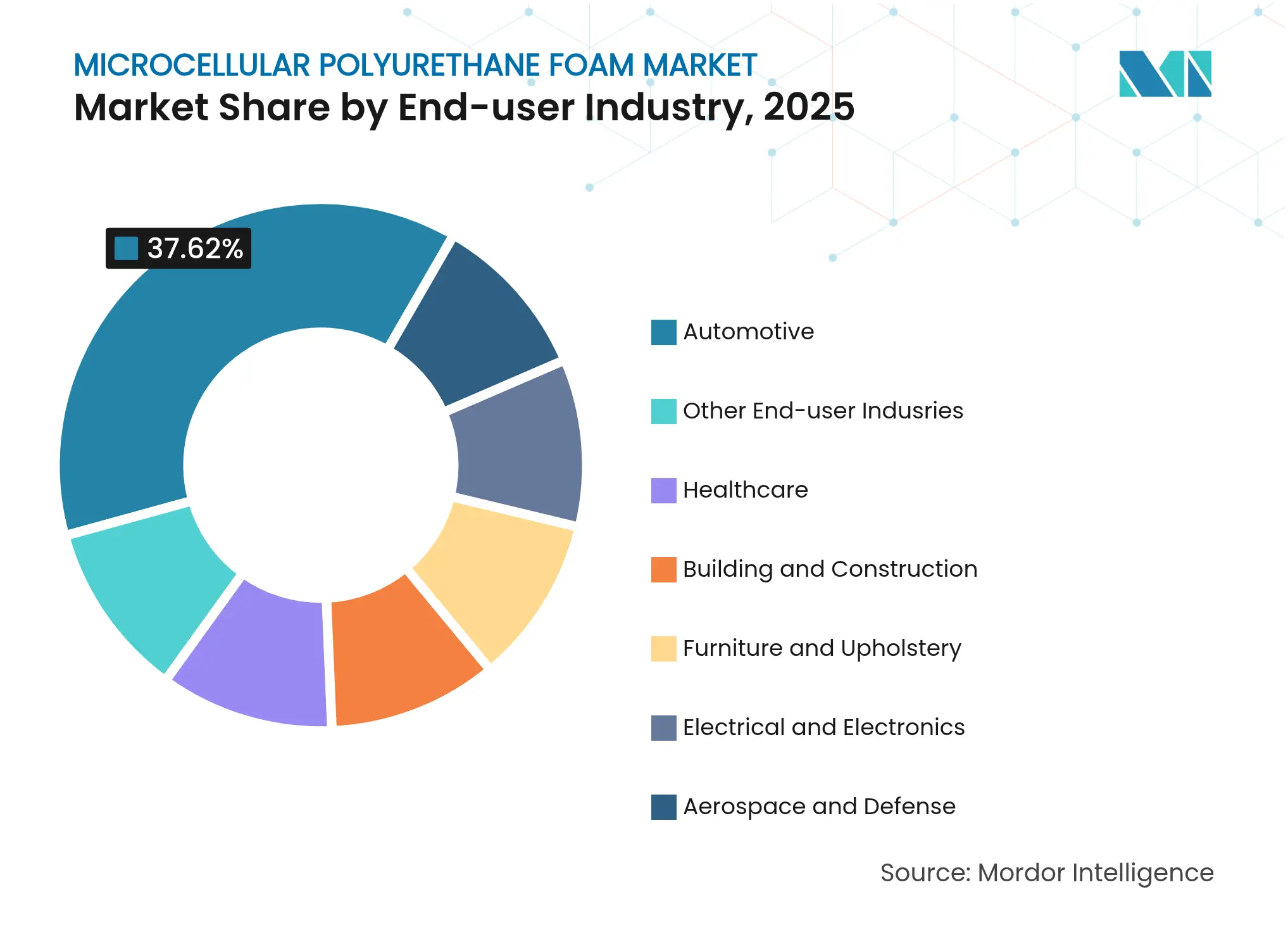

By End-user Industry: Healthcare Growth Outpaces Automotive Maturity

Automotive commanded 37.62% of the Microcellular Polyurethane Foam market share in 2025 and is expected to advance at a steady 3.88% CAGR through 2031. OEM demand is diversified across seating cushions, vibration dampers, battery protection pads, and acoustic liners. Yet healthcare’s 5.12% CAGR is faster, lifting the microcellular polyurethane foam market size for medical applications to USD 1.29 Billion by 2031 as soft-robotic braces, wound-care dressings, and implantable devices scale up.

Building and construction represents a resilient mid-growth segment as national codes tighten R-value standards. Furniture and upholstery maintain consistent pull but face competition from latex and memory-foam substitutes. Aerospace, defense, and high-power electronics consume specialty fire-retardant grades that must meet demanding smoke, toxicity, and outgassing rules, supplying smaller but margin-rich pockets in the microcellular polyurethane foam market.

Note: Segment shares of all individual segments available upon report purchase

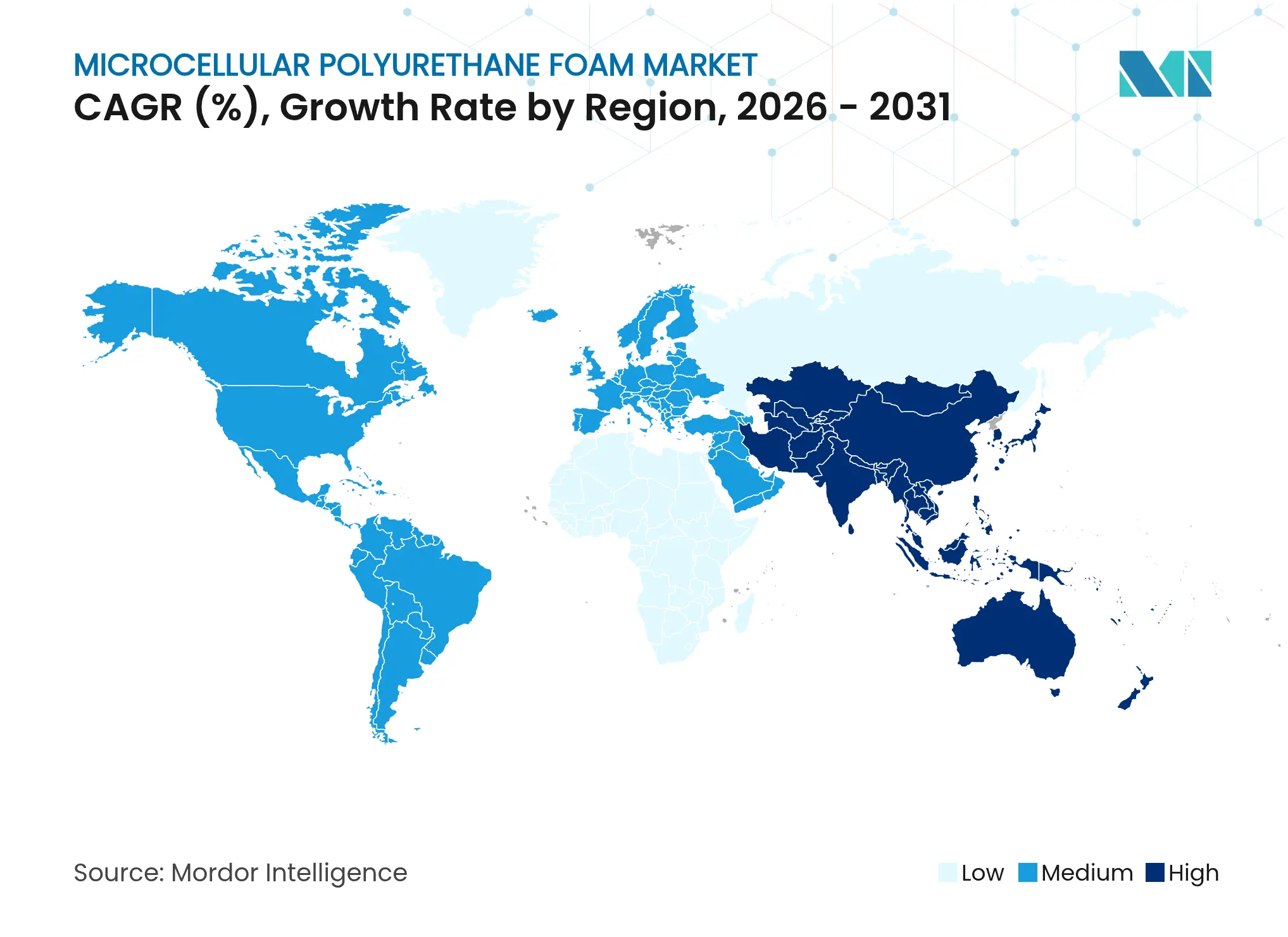

Asia-Pacific accounted for 46.25% of the Microcellular Polyurethane Foam market share in 2025 and is predicted to grow at a 4.95% CAGR to 2031. China’s EV assembly output and India’s housing boom underpin continuous order books for low-density insulation and seating foams. Japanese Tier-1 suppliers upgrade process automation, while Korean electronics firms specify microcellular pads for thermal management in next-generation smartphones and servers. Regional demand is also fueled by ASEAN nations attracting furniture and automotive relocations, which require local foam supply lines to shorten lead times in the microcellular polyurethane foam market.

North America ranks second in value because the United States vehicle lightweighting mandates and energy-efficient retrofit programs justify premium microcellular grades that cut both mass and heat loss. The region's microcellular polyurethane foam market size is projected to exceed USD 2.74 Billion by 2031. Canadian provinces adopt net-zero building codes that emulate European frameworks, while Mexican auto plants seek cost-effective extrusion foams to serve export models. Europe remains technology-focused, channeling investment into circular-economy innovations such as recycled-polyol foams and non-isocyanate chemistries, sustaining demand despite slower construction growth.

South America and the Middle East & Africa together account for less than 10% of the microcellular polyurethane foam market size today, yet pockets of growth appear. Brazil’s automotive recovery, Saudi Arabia’s Vision 2030 projects and South Africa’s mining equipment markets require lightweight, durable cushioning and insulation. Currency volatility and fragmented building standards temper immediate expansion, but capacity investments by Huntsman and local converters indicate confidence in long-term regional integration inside the microcellular polyurethane foam market.

Market Concentration

The Microcellular Polyurethane Foam market shows moderate concentration. Major players like BASF, Covestro AG, and Huntsman Corporation command a significant share due to vertically integrated MDI/TDI supply, proprietary resin recipes, and global technical-service networks. Medium-scale players fill regional gaps with specialty offerings such as bio-polyol systems, flame-retardant grades, and functionally graded foams. Covestro AG’s transformation program, targeting USD 400 Million in annual savings by 2028, combines cost synergies with investment in continuous foaming lines that accommodate recycled feedstocks. BASF broke ground on a Cellasto plant in Dahej, India, slated to launch in 2026, reinforcing its commitment to localized supply for Asian automotive platforms. Intellectual-property filings cluster around super-critical processing, catalyst-free formulations, and robotic spraying systems, underscoring a transition from commodity volumes to technology-driven differentiation in the Microcellular Polyurethane Foam market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The Microcellular Polyurethane Foam market report includes:

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.