Polyethylene Foam Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

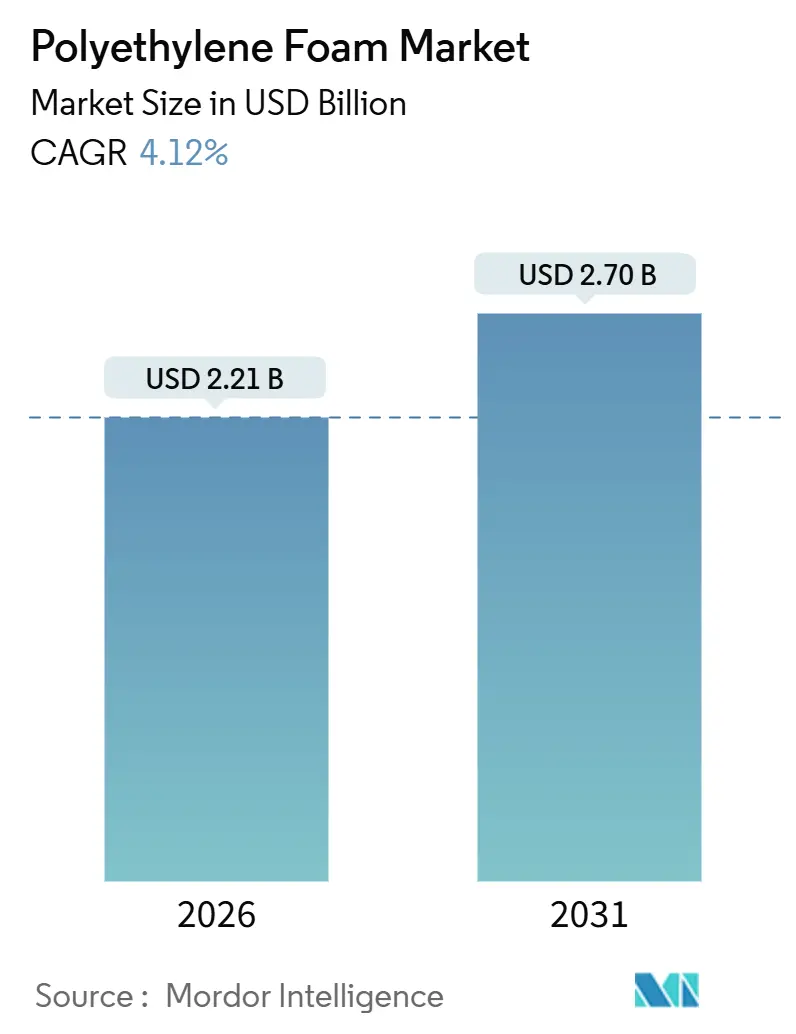

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.70 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyethylene Foam Market Analysis by Mordor Intelligence

The Polyethylene Foam Market size is estimated at USD 2.21 billion in 2026, and is expected to reach USD 2.70 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). Asia-Pacific is steering growth as automotive lightweighting, construction retrofits, and pharmaceutical cold-chain logistics expand the addressable base of the Polyethylene foam market, while single-use plastic regulations in North America and Europe temper demand in consumer e-commerce packaging. Non-cross-linked grades still dominate because they thermoform quickly and cost less to ship, yet cross-linked variants are gaining share where building codes and battery safety rules mandate moisture resistance and dimensional stability. Feedstock economics favor integrated petrochemical hubs in China and the Middle East, creating regional price spreads that push converters to relocate extrusion capacity eastward. Competitive strategies now revolve around delivering recycled-content blends that keep tensile strength intact, and on capturing white space in insulation, cold-chain, and electric-vehicle (EV) noise-vibration-harshness applications.

Key Report Takeaways

- By type, non-XLPE foam led with 57.42% revenue share in 2025, while XLPE foam is forecast to expand at a 5.24% CAGR through 2031.

- By application, packaging captured 39.36% of 2025 revenue; the “other applications” bucket shows the fastest 5.18% CAGR to 2031.

- By end-user, automotive generated 31.28% of 2025 demand, yet pharmaceutical and healthcare are set to grow the quickest at 6.22% CAGR through 2031.

- By geography, Asia-Pacific contributed 48.53% of 2025 revenue and is predicted to sustain a 6.03% annual rise to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyethylene Foam Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce protective packaging | +0.8% | North America, Europe, ASEAN | Short term (≤ 2 years) |

| Construction retrofits demanding closed-cell insulation | +1.2% | North America, Europe, India | Medium term (2-4 years) |

| Lightweight NVH solutions in electric vehicles | +1.0% | China, South Korea, spill-over to Europe | Medium term (2-4 years) |

| Cold-chain expansion for biologics and meal kits | +0.9% | North America, Europe, global pharma corridors | Long term (≥ 4 years) |

| Recyclate-compatible compatibilizer breakthroughs | +0.7% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Protective Packaging

While fulfillment centers are automating their pack-out lines and reducing void fill per parcel, global B2B shipments of electronics and machinery continue to rely on polyethylene foam inserts for anti-static and moisture-barrier protection. By late 2024, Amazon had already eliminated plastic air pillows and was now aiming for paper filler by June 2025. This move is contributing to a decline in North American demand for light-density foam. In Europe, extended producer responsibility rules are accelerating the shift to paper. Meanwhile, ASEAN electronics exports are keeping industrial cushioning volumes steady[1]“ASEAN Investment Report 2022,” ASEAN Secretariat, asean.org. Despite a contraction in retail packaging, precision die-cut foam remains the go-to choice for semiconductor logistics, ensuring consistent baseline consumption.

Construction Retrofits Demanding Closed-Cell Insulation

California's Title 24 and the updated EU building codes emphasize high R-values and minimal water absorption for crawlspace and below-grade insulation, leading to a preference for cross-linked polyethylene (XLPE) foam. India's construction output is forecast to grow annually until 2029, expanding the market for closed-cell insulation. XLPE's dimensional stability and resistance to mold have made it the go-to choice for insulated concrete forms, structural insulated panels, and retrofit crawlspace liners. Despite increasing scrutiny on single-use plastics, these code-driven retrofits provide consistent momentum for the Polyethylene foam market.

Lightweight NVH Solutions in Electric Vehicles

China’s new-energy vehicle parc reached a record in 2024, intensifying lightweighting needs. While polyurethane dominates battery-pack flame barriers, polyethylene foam holds a niche in door seals, trunk liners, and under-body panels where recyclability and cost trump thermal performance. Automakers moving toward mono-material interiors for easier disassembly under the EU End-of-Life Vehicles Directive increasingly specify polyethylene foam laminates. As EV assembly localizes across Southeast Asia, regional foam demand benefits from proximity to gigafactories and component clusters.

Cold-Chain Expansion for Biologics and Meal Kits

mRNA vaccines and monoclonal antibodies need passive shippers that sustain −80 °C to +8 °C for up to 96 hours, a spec XLPE foam meets when paired with reflective barriers. Meal-kit providers such as HelloFresh continue double-digit subscriber growth, testing recyclable liners that mix bio-based polyethylene with phase-change gels to reduce box weight without sacrificing insulation. The result is incremental but durable demand for high-R-value foam panels that comply with FDA and EMA validation protocols, anchoring an attractive niche within the Polyethylene foam market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile ethylene feedstock pricing | −0.6% | Europe, North America, global exposure | Short term (≤ 2 years) |

| Intensifying bans on single-use plastic foams | −0.9% | Europe, California, select ASEAN economies | Medium term (2-4 years) |

| Collection and sorting hurdles for foam recycling | −0.5% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Ethylene Feedstock Pricing

Steam-cracked ethylene output swings with naphtha prices and LNG availability, squeezing converter margins during upcycles. China’s new petrochemical complexes elevate regional production and suppress spot prices, while European crackers bear higher energy costs, prompting converters to shift extrusion lines close to low-cost feedstock hubs. Electrified furnace pilots by Dow, BASF, and others could dull volatility over the next decade, yet near-term price shocks remain a downside risk to the Polyethylene foam market.

Intensifying Bans on Single-Use Plastic Foams

The EU banned expanded polystyrene foodware in 2021 and now imposes recycled-content targets across all foam packaging. California and many U.S. municipalities restrict polystyrene foodservice articles, and public perception frequently lumps polyethylene foam into the same category. As curbside systems rarely segregate foam, converters struggle to source clean post-consumer feedstock, creating compliance and reputational headaches that dampen demand growth[2]“EU Regulation 2025/40 on Packaging and Packaging Waste,” EUR-Lex, eur-lex.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cross-Linking Raises Performance Ceiling

Cross-linked polyethylene (XLPE) captured a premium price and is forecast to post a 5.24% CAGR through 2031, outstripping the Polyethylene foam market’s overall 4.12% pace. Non-XLPE held a 57.42% share in 2025 thanks to low density and rapid thermoformability, yet code changes that mandate closed-cell insulation in moisture-prone assemblies steadily shift demand toward XLPE. A 2025 Angewandte Chemie paper detailed dynamic cross-linkers that let XLPE be reprocessed without sacrificing creep resistance, opening circular-economy pathways. The Polyethylene foam market size for XLPE applications in building envelopes and EV thermal barriers is poised to accelerate as recyclate-ready chemistries narrow the cost gap with commodity grades. Meanwhile, non-XLPE maintains traction in protective packaging where easy die-cutting and existing recycling streams sustain its competitive edge. When European food-contact regulation 2025/351 required high-purity documentation for recycled content, converters with ISO-certified traceability systems locked in long-term contracts, further polarizing market tiers.

By Application: Insulation Becomes the Growth Engine

Packaging controlled 39.36% of 2025 revenue, yet insulation, composites, and other specialty uses grow at a faster 5.18% CAGR. Building codes that raise R-value minimums fuel steady demand for closed-cell foam boards, while aerospace and rail adopt foam-core sandwich panels to cut structural weight. Amazon’s packaging shift removed demand in North America, but industrial electronics exports keep cushioning volumes healthy. The Polyethylene foam market share tied to insulation is widening as modular construction, prefabricated walls, and insulated concrete forms adopt XLPE panels for water-barrier and thermal-bridge control. Composite manufacturers blending foam cores with carbon-fiber skins widen their order books in renewable-energy nacelles and high-speed trains, underpinning a long-run growth channel.

By End-User Industry: Pharma Races Ahead

Automotive accounted for 31.28% of 2025 consumption, but pharmaceutical and healthcare shipments will grow at a 6.22% CAGR. WHO cold-chain guidelines set a 0.040 W/m-K thermal-conductivity ceiling, which XLPE meets when laminated with reflective foil, earning validation in mRNA vaccine shippers. EV adoption keeps automotive demand stable, shifting the mix from under-hood insulation to battery-pack and interior NVH liners. Building and construction ride infrastructure booms in India and ASEAN, while fast-moving consumer goods packaging slows where single-use bans bite. Furniture, bedding, and sports gear remain a durable niche of the Polyethylene foam industry, shielded from ready substitutes by the material’s balance of cushioning, durability, and cost.

Geography Analysis

Asia-Pacific contributed 48.53% of 2025 revenue and is set to grow 6.03% annually through 2031, underpinned by China’s new-energy vehicles and India’s construction sector expansion. Local ethylene oversupply from integrated complexes compresses resin prices, incentivizing multinational converters to expand extrusion capacity in coastal China. Japan and South Korea innovate anti-static and flame-retardant grades for electronics, feeding regional value-added exports.

North America shows flat to low-single-digit growth as Amazon’s paper pivot trims consumer e-commerce foam, though construction retrofits under the Inflation Reduction Act and pharma cold-chain expansions partly offset declines. EU Regulation 2025/40 enforces recycled-content quotas, spurring capital investment in compatibilizer technology and favoring incumbents with ISO-certified quality systems. California Title 24 upgrades sustain demand for vapor-barrier XLPE in crawlspaces.

South America, the Middle East, and Africa together form a small but rising slice of the Polyethylene foam market. Brazil’s urban housing programs and Saudi Arabia’s Vision 2030 petrochemical build-out promise new downstream opportunities. Weak recycling infrastructure limits regulatory pressure, so virgin resin remains the norm, allowing converters to compete mainly on logistics and service rather than circularity credentials.

Competitive Landscape

The polyethylene foam market is moderately fragmented. Technology is the key battleground. Large converters automate die-cutting and lamination to slash labor costs and meet tight tolerances for EV and electronic assemblies. Smaller firms defend their share with custom formulations and fast turnaround. Compatibilizer breakthroughs that allow recycled content without mechanical loss grant first movers pricing power under EU mandates, while laggards face a margin squeeze. Certifications such as ISO 9001 and ISO 14001 become gatekeepers for food-contact and pharma packaging, erecting compliance barriers that accelerate consolidation.

Polyethylene Foam Industry Leaders

Sealed Air

Pregis LLC

JSP

Zotefoams PLC

Armacell

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Armacell has opened a new insulation manufacturing facility in India, which may bolster the regional supply of PE foam insulation materials for industrial and building applications.

- February 2024: Pregis launched certified-circular polyethylene foam packaging developed with ExxonMobil’s advanced recycling feedstock.

Global Polyethylene Foam Market Report Scope

Polyethylene foam is a closed-cell, durable, and lightweight protective material used for packaging industrial products.

The polyethylene foam market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into XLPE foam and non-XLPE foam. By application, the market is segmented into cushioning, packaging, and other applications (insulations, composite materials, etc.). By end-user industry, the market is segmented into automotive, building and construction, FMCG, pharmaceutical, and other end-user industries (furniture and bedding, sports, etc.). The report also covers the market sizes and forecasts for the polyethylene foam market in 18 countries across major regions. For each segment, the market sizing and forecasts are provided on the basis of value (USD) for all the above segments.

| XLPE Foam |

| Non-XLPE Foam |

| Cushioning |

| Packaging |

| Other Applications (Insulations, Composite Materials, etc.) |

| Automotive |

| Building and Construction |

| FMCG |

| Pharmaceutical and Healthcare |

| Other End-user Industries (Furniture and Beedings, Sports, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | XLPE Foam | |

| Non-XLPE Foam | ||

| By Application | Cushioning | |

| Packaging | ||

| Other Applications (Insulations, Composite Materials, etc.) | ||

| By End-user Industry | Automotive | |

| Building and Construction | ||

| FMCG | ||

| Pharmaceutical and Healthcare | ||

| Other End-user Industries (Furniture and Beedings, Sports, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Polyethylene foam market by 2031?

The Polyethylene foam market size is forecast to reach USD 2.70 billion by 2031, up from USD 2.21 billion in 2026, registering a CAGR of 4.12%.

Which application will grow the fastest through 2031?

Insulation and other specialty uses are expected to rise at a 5.18% CAGR, outpacing packaging and cushioning segments.

Why is Asia-Pacific the largest contributor to Polyethylene foam demand?

Rapid EV adoption in China and construction expansion in India push the region’s share to 48.53% of 2025 revenue with a 6.03% forecast CAGR.

Which end-user industry offers the highest growth upside?

Pharmaceutical and healthcare applications, driven by biologics cold-chain shipments, are projected to grow at a 6.22% CAGR through 2031.

Page last updated on: