Spray Polyurethane Foam Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 3.96 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spray Polyurethane Foam Market Analysis by Mordor Intelligence

Spray Polyurethane Foam Market size in 2026 is estimated at USD 3.06 billion, growing from 2025 value of USD 2.91 billion with 2031 projections showing USD 3.96 billion, growing at 5.27% CAGR over 2026-2031. This expansion occurs as building-energy codes tighten, low-GWP regulations take effect, and cold-chain investment accelerates, driving higher-value insulation demand. Manufacturers are swapping high-GWP HFCs for hydrofluoroolefin and other next-generation blowing agents to comply with the EPA’s Technology Transitions Restrictions rule that began on 1 January 2025 epa.gov. Consolidation among installers, growing retrofit activity, and ESG-linked financing further reinforce momentum across residential, commercial, and industrial projects, while innovation in CO₂-based polyols positions suppliers for long-term sustainability gains.

Key Report Takeaways

- By product type, two-component high-pressure spray foam led with 37.02% of spray polyurethane foam market share in 2025, whereas semi-rigid spray foam is projected to grow at a 6.84% CAGR to 2031.

- By application, insulation commanded 38.74% of the spray polyurethane foam market size in 2025; concrete lifting and other specialty uses are expected to expand at 7.05% CAGR through 2031.

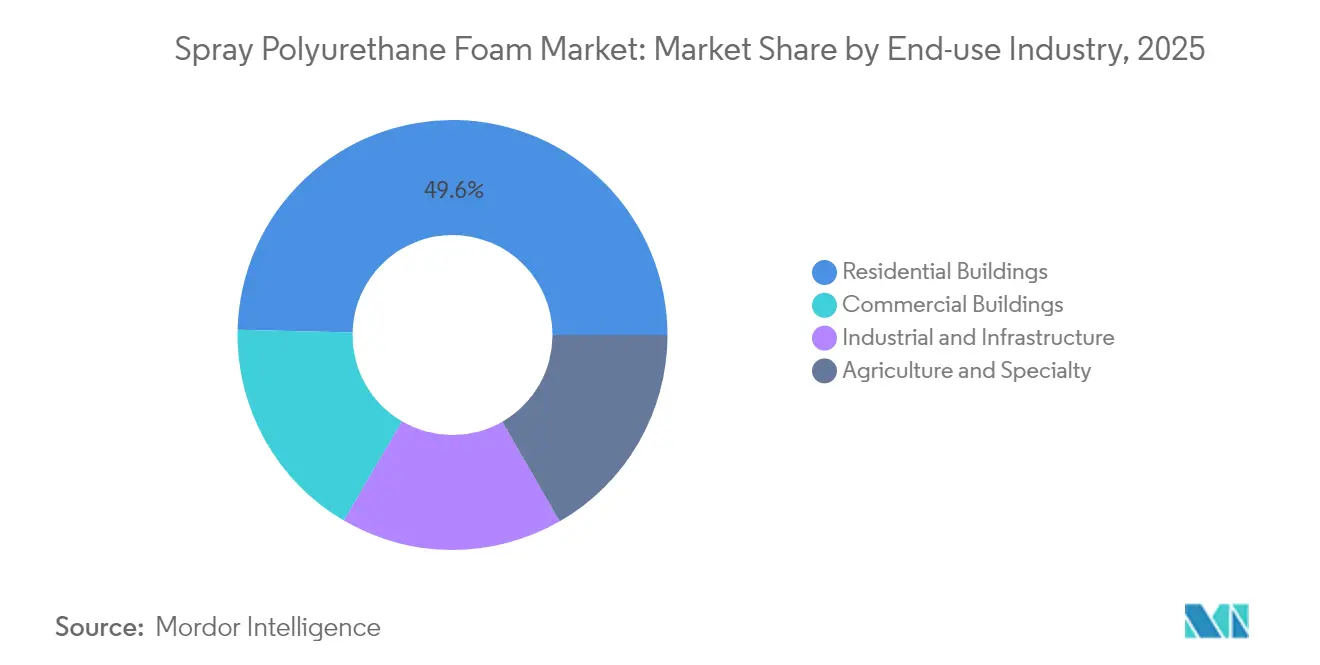

- By end-use industry, residential buildings accounted for 49.62% of the spray polyurethane foam market size in 2025, while industrial and infrastructure is advancing at a 7.39% CAGR to 2031.

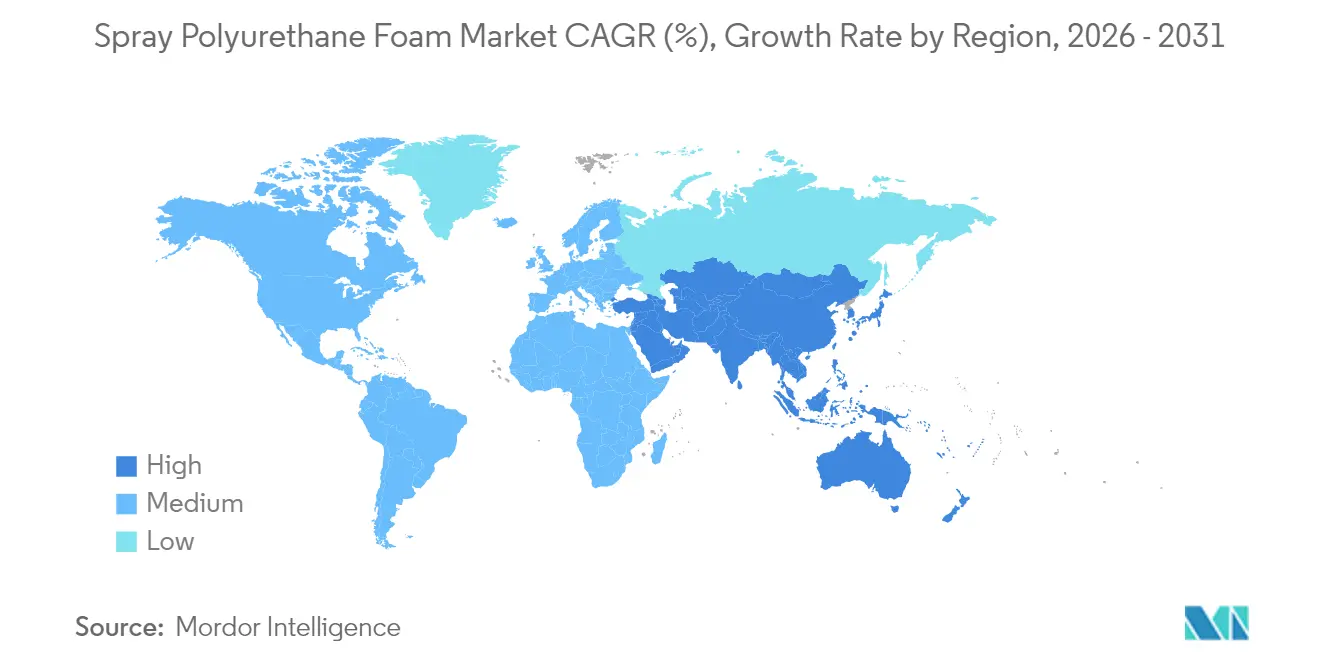

- By geography, Asia-Pacific held 47.66% spray polyurethane foam market share in 2025 and is forecast to grow at 7.21% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spray Polyurethane Foam Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict building-energy codes and retrofit mandates | +1.2% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Rising concerns over GHG emissions | +0.8% | Global, particularly APAC and North America | Long term (≥ 4 years) |

| Growth in cold-chain and refrigerated logistics | +0.6% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| ESG-linked "green bond" financing for SPF upgrades | +0.4% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| High-lift foam demand for solar-ready roofs | +0.3% | North America and EU, with emerging APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Building-Energy Codes and Retrofit Mandates

The 2024 International Energy Conservation Code elevates closed-cell spray foam as a preferred air-barrier solution, compelling architects to specify higher R-values and moisture control measures. California’s 2023 standards and Florida’s 2026 code update both streamline retrofit approvals, lowering removal costs and accelerating demand, particularly for low-slope commercial roofs[1].Florida Roof, “2026 Florida Building Code Updates,” floridaroof.com These rule changes widen the retrofit addressable base, encourage hybrid insulation assemblies, and push contractors toward more training and equipment investment that favors two-component systems.

Rising Concerns Over GHG Emissions

Corporate net-zero goals merge with building-owner cost targets, highlighting spray foam’s ability to cut heating-and-cooling energy by up to 10% according to the EPA’s Energy Star program. Installed Building Products reported a 55% CO₂ reduction from spray foam use since 2020 while materially increasing output, showing the technology’s decoupling of growth from emissions. Manufacturers such as Johns Manville logged double-digit drops in absolute emissions even as energy-saving product volumes rose, underscoring alignment between sustainability and profitability.

Growth in Cold-Chain and Refrigerated Logistics

Americold operates 239 facilities totaling 1.4 billion ft³ and holds 17.8% North American capacity share, illustrating how temperature-controlled warehouses create steady insulation demand. The Global Cold Chain Alliance’s 1,280-facility membership highlights global reach and growing need for high-performance, low-permeability insulation. Spray foam’s superior air-sealing delivers measurable energy savings in these power-intensive operations, reinforcing adoption across new builds and retrofits as e-commerce grocery delivery rises.

ESG-Linked Green-Bond Financing for SPF Upgrades

Capital markets increasingly tie funding costs to building-level carbon metrics, making spray foam retrofits eligible for lower-rate green bonds. HB Fuller’s work with CO₂-rich Converge polyols illustrates how material innovation attracts investors searching for verifiable emissions reductions. As LEED and BREEAM frameworks award points for airtightness and energy performance, owners monetize spray foam benefits through higher asset valuations and operating savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from fiberglass and cellulose | -0.5% | Global, particularly North America residential | Short term (≤ 2 years) |

| Regulations and restrictions on di-isocyanates | -0.3% | Global, with stricter enforcement in EU and North America | Medium term (2-4 years) |

| HFO blowing-agent supply volatility | -0.2% | Global, with acute impact in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Fiberglass and Cellulose

Cost-focused residential builders still default to fiberglass batts, supported by long-standing installer networks and low equipment requirements. Home Innovation Research Labs data showed an 11% to 8% pullback in spray foam share amid multifamily growth and material cost saving, highlighting price sensitivity. Fiberglass makers are narrowing performance gaps with higher-density offerings, while cellulose leverages recycled content branding to appeal to eco-minded consumers. Spray foam suppliers must therefore sharpen value messaging around lifecycle energy savings to overcome higher upfront spend.

Regulations and Restrictions on Di-Isocyanates

EU rules effective August 2023 compel contractor training for products containing more than 0.1% di-isocyanates, raising compliance costs and documentation burdens[2]European Chemicals Agency, “Restriction on Di-Isocyanates,” echa.europa.eu. The US EPA’s significant‐new-use regulation layers additional PPE and engineering-control mandates, particularly affecting smaller installers. While large manufacturers can embed training into distribution channels, cost impacts risk shifting demand toward emerging isocyanate-free chemistries, demanding ongoing R&D investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Two-Component Systems Drive Market Leadership

The segment anchored by two-component high-pressure systems held a 37.02% spray polyurethane foam market share in 2025, reflecting consistent on-site mixing, superior R-values, and code acceptance in commercial construction. BASF’s new isocyanate and TPU lines in Zhanjiang strengthen local supply chains, reinforcing the segment’s dominance in Asia-Pacific. Semi-rigid spray foam is expanding at a 6.84% CAGR as infrastructure projects need flexibility for vibration and temperature swings. One-component cans address small-project convenience, while low-pressure kits cover sensitive substrates where reduced exothermic heat is critical.

A push for integrated brands illustrates competitive strategy: Holcim’s Enverge® label merges Gaco™ and SES™ portfolios, giving installers a single specification path for roof, wall, and specialty foams. Product diversification frames cross-selling opportunities, with semi-rigid innovations aimed at solar-ready roofs and bridge decks, and intumescent-infused systems targeting fire-resistance regulations. Suppliers that maintain broad catalogs and regional technical centers remain best positioned to seize specification wins.

By Application: Insulation Dominance Faces Emerging Diversification

Insulation accounted for 38.74% of the spray polyurethane foam market size in 2025 and benefits from its dual role as air barrier under the 2024 IECC, which elevates whole-building airtightness requirements. In refrigerated warehouses, closed-cell formulations routinely deliver energy payback periods under four years, reinforcing specification in cold-chain projects. Concrete lifting, void filling, and geotechnical stabilization represent the fastest-growing “other applications” bucket, advancing at 7.05% CAGR as infrastructure spending catches up with deferred maintenance.

Waterproofing demand grows in podium-deck and green-roof designs where continuous membranes protect occupied space below. Sealants capitalize on spray foam’s self-adhering expansion, reducing thermal bridges around fenestration openings. Intumescent-embedded products like NCFI’s Staycell ONE STEP foam remove the need for separate thermal barriers, saving labor and satisfying NFPA 286 fire testing protocols. Diversified usage insulates the spray polyurethane foam market from cyclical new-build cycles by opening revenue in maintenance and infrastructure segments.

By End-use Industry: Residential Leadership Meets Industrial Growth

Residential buildings retained a 49.62% spray polyurethane foam market size share in 2025 thanks to rising energy-efficient home standards and homeowner awareness of lifetime utility savings. Tax incentives under IRA Section 25C reimburse up to 30% of envelope upgrades, stimulating retrofit volumes. Industrial and infrastructure projects, growing at 7.39% CAGR, anchor new capacity for cold-storage, food processing, and distribution centers; Americold’s 1.4 billion ft³ portfolio underscores this structural demand.

Commercial buildings offer steady institutional demand as offices and hospitals adopt tighter envelope requirements. Specialty agriculture and greenhouse facilities rely on closed-cell foam for condensation control and bio-security, while transport infrastructure adopts spray foam for sound damping and vibration isolation. Consolidation moves, such as TopBuild’s USD 39 million Texas Insulation purchase, give national installers leverage to serve multiple end markets with unified safety and quality‐control protocols.

Geography Analysis

Asia-Pacific captured 47.66% of spray polyurethane foam market share in 2025 and is forecast to climb at 7.21% CAGR, driven by rapid urbanization, factory expansions, and energy-code adoption. China’s real-estate slowdown redirects stimulus toward urban renewal, boosting retrofit insulation spend, while India’s HVAC sector is set to hit USD 30 billion by 2030 on a 15.8% CAGR pathway, raising demand for building envelope upgrades. Japan and South Korea enforce stringent envelope requirements in seismic zones, favoring lightweight, high-adhesion insulation such as spray foam. ASEAN nations expand cold-chain capacity for seafood and vaccine storage, pulling regional demand upward. BASF’s multi-year USD 19.5 billion Asia-Pacific investment plan exemplifies supplier confidence in the region’s absorption capacity.

North America remains a mature but stable arena where federal HFC phase-outs harmonize compliance and keep specification complexity low. Canada’s cold climates sustain thick-layer attic spray foam usage, while Mexico emerges as the world’s fourth-largest polyurethane consumer on near-shoring momentum and automotive manufacturing growth. Consolidation among contractors enables national builders to standardize envelope solutions across the US and Canada, reinforced by TopBuild’s network expansion.

Europe’s net-zero directives and renovation wave stimulate demand despite tepid macro-economics. Di-isocyanate training rules introduce friction but ultimately favor well-capitalized manufacturers with robust EHS programs. Covestro’s DreamResource project introduces rigid foam containing 20% CO₂ as feedstock, demonstrating European leadership in circular chemistry. University of Liège advances isocyanate-free foams with 70-90% biobased content, underscoring regional academic–industry collaboration. In South America and the Middle East and Africa, energy-efficiency codes are tightening gradually; early movers in Brazil, Saudi Arabia, and the UAE adopt spray foam in commercial megaprojects, signaling future volume uplift.

Regulatory Landscape

Regulation of spray polyurethane foam is tightening around climate impact and worker safety, which is shaping blowing-agent and system selection. In the United States, the EPA Technology Transitions restrictions under the AIM Act framework (85% HFC phasedown by 2036) prohibit use of higher-GWP HFCs in relevant polyurethane foam end uses from January 1, 2025, accelerating conversion to low-GWP alternatives such as HFOs and other next-generation options. EPA updates in May 2026 further clarified compliance timing and subsector-specific limits in the Technology Transitions program materials.

In Europe, the EU F-Gas framework drives a near-total phase-out of HFCs for foam blowing by 2030, reinforcing reformulation and qualification of substitute blowing agents across construction insulation supply chains. Separately, chemical-safety rules add installer and contractor obligations: the REACH Annex XVII restriction on diisocyanates requires mandatory training for industrial and professional users from August 24, 2023, increasing compliance documentation needs and favoring suppliers and installers with scalable training, stewardship, and audited EHS programs.

Value Chain Analysis

The spray polyurethane foam value chain starts with upstream production of isocyanates (notably MDI) and polyols, followed by additive and blowing-agent supply, then downstream blending by systems houses into A-side and B-side packages. Large chemical producers such as BASF, Dow, and Huntsman anchor upstream feedstocks, while regional and independent formulators tailor B-side systems for local codes and installer preferences. Two-component systems also make the installer channel a key conversion point, since they require specialized proportioning equipment, job-site controls, and documented training, supported by programs such as the Spray Polyurethane Foam Alliance (SPFA) Professional Certification Program.

Regulatory-driven reformulation has become a core operational step in the chain, especially the shift away from legacy HFC blowing agents for closed-cell foam after January 1, 2025. This increases dependence on qualified low-GWP formulations and consistent supply of compliant blowing agents and additives. Standards and testing infrastructure then shape downstream acceptance and specification, including CAN/ULC-712.1-2024 (published June 5, 2024) for spray-applied semi-rigid polyurethane foam, with evaluation and code pathways influencing how manufacturers, distributors, and contractors document performance, fire testing, and installation quality.

Competitive Landscape

Fragmentation characterizes the spray polyurethane foam market as only 19% of commercial contractors currently offer SPF services, yet 67% of those firms improved sales from 2023 to 2024. The installer gap incentivizes roll-ups and private equity involvement—evident in Accella’s takeover of Quadrant’s spray unit and TopBuild’s regional tuck-ins—that aim to secure geographic coverage and trained labor. Large chemical companies including BASF, Covestro, Dow, and Huntsman compete on upstream integration, proprietary blowing-agent blends, and technical training programs, allowing them to guard share against regional formulators.

Sustainability is now an overt differentiator. Huntsman’s Building Solutions division converts PET bottles into polyurethane, aligning with circular-economy messaging that resonates with green-bond investors. Covestro and BASF commercialize CO₂-based polyols, while smaller innovators pursue isocyanate-free paths to pre-empt future toxicology regulation. Technology packages that include digital yield-tracking sprayers and cloud-based QA portals further separate premium suppliers from commodity blenders by reducing job-site waste and providing verifiable performance data to building owners.

Regional dynamics affect strategy. In Asia-Pacific, multinational suppliers localize output to avoid tariffs and reduce shipping times, while domestic producers leverage price to win commodity housing projects. North American players focus on code compliance and low-GWP composition, whereas European companies invest in biobased content and circular feedstocks. Across all regions, supplier collaborations with universities and additive companies accelerate product differentiation in flame retardancy, acoustics, and weatherability.

Spray Polyurethane Foam Industry Leaders

BASF SE

Dow Chemical Company

Huntsman Corporation

Covestro AG

Carlisle Companies Inc. (CSFI)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is emerging for compliance-ready, lower-embodied-carbon SPF systems that help owners and contractors meet tightening blowing-agent and chemical-safety requirements while still hitting envelope performance targets. BASF and Dow actions show how mass-balance and certified inputs are moving from corporate sustainability messaging into SPF-relevant raw materials and systems, including BASF launching a biomass-balance isocyanate for North American SPF systems (April 2026) and Dow securing ISCC PLUS certification for its Freeport, Texas MDI facility (October 2025). This creates room for system houses and installers to differentiate bids using third-party backed product attributes and documentation aligned with green-building and owner reporting requirements.

Another opportunity is standardization and installer capability building, since labor and quality bottlenecks affect SPF adoption. The International Code Council completed a public review in March 2026 for ICC 1100 (Spray-applied Polyurethane Foam Plastic Insulation), a step toward a clearer, adoptable standard across jurisdictions that can reduce ambiguity in approvals and performance requirements. In parallel, SPFA launched FoamItRight.org in February 2026 to simplify the pathway to Professional Certification Program participation, supporting contractor scaling and more consistent job-site outcomes as code enforcement and diisocyanate training obligations increase administrative load for smaller installers.

Recent Industry Developments

- April 2026: BASF launched ELASTOSPRAY BMB isocyanate for North American spray polyurethane foam systems, using a biomass balance approach to support lower embodied-carbon claims for SPF components. The move broadens the set of formulation options system houses can offer building owners who want documented sustainability attributes alongside code-compliant insulation performance.

- October 2025: Dow received ISCC PLUS certification for its MDI manufacturing facility in Freeport, Texas, enabling mass-balance offerings that support bio-based or circular feedstock attribution. This strengthens downstream supply chains pursuing EPD and LCA documentation and helps align SPF raw materials with sustainability-linked procurement requirements.

- June 2024: Huntsman Building Solutions added Icynene Xpress 55 to its Icynene Series, an open-cell spray foam designed for unventilated attics and crawl spaces and positioned around AC-377 Appendix X fire-test requirements. The product addition expands contractors’ choices for code-oriented assemblies in residential retrofit and new-build applications where fire testing and attic performance drive specification.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from spray-applied polyurethane foam systems used to create insulation and protective layers on buildings and other surfaces, covering both new build and retrofit activity. Revenue is counted at the point of sale for the foam system.

Scope exclusions: We exclude non-spray polyurethane foam formats (such as slabstock, molded, or board stock insulation) and downstream installation labor priced as a separate service where it is not bundled with the foam system.

Segmentation Overview

- By Product Type

- Two-Component High-Pressure Spray Foam

- Two-Component Low-Pressure Spray Foam

- One-Component Foam (OCF)

- Semi-Rigid Spray Foam

- By Application

- Insulation

- Waterproofing

- Asbestos Encapsulation

- Sealant

- Other Application (Concrete Lifting / Void Filling, etc.)

- By End-use Industry

- Residential Buildings

- Commercial Buildings

- Industrial and Infrastructure

- Agriculture and Specialty

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where SPF demand is actually created, which is mainly construction insulation, roofing, and weatherization, then linking that to how foam systems are sold. Public sources are used to anchor model inputs, such as construction output and permits from the US Census Bureau, macro and industry indicators from the World Bank, energy efficiency and building envelope references from the US DOE, and environment and chemicals information from the US EPA.

We also review trade association publications and technical literature (including peer-reviewed articles on insulation performance and blowing agent transitions) to confirm how open cell and closed cell usage differs by climate and building codes. Company filings, investor presentations, and reputable press are used to check capacity additions, raw material availability, and pricing commentary. These are compared with patterns from paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records. Desk research inputs are not exhaustive, and many other public and paid sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews are used to pressure test the desk assumptions that most affect the value model, especially application mix, average selling price ranges, and the pace of low GWP blowing agent adoption by region. We spoke with a mix of raw material stakeholders, foam system suppliers, distributors, contractors, and large end users, so the final view reflects both supply-side realities and jobsite demand signals across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 42% |

| Mid tier: 59% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 14% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

The core sizing logic starts with a top-down build where construction and retrofit activity is converted into an addressable insulation and sealing demand pool, then SPF penetration is applied by region and application. To keep the numbers realistic, results are corroborated with selective bottom-up approximations, mainly a sampled ASP times volume approach for key applications, and a supplier and channel check that helps adjust for underreported smaller contractors.

Key inputs used in the model include residential and nonresidential construction output, roofing and insulation demand indicators, building energy code direction, shifts between open cell and closed cell usage driven by climate and performance needs, and raw material and blowing agent pricing signals that flow into ASP progression. Where gaps exist in the bottom-up checks, we interpolate using nearby country patterns and contractor feedback on typical project sizes, then re-test the totals against the top-down demand pool.

For forecasting, scenario analysis is applied around construction cycles and retrofit policy support, followed by a smoothing step on pricing and mix changes so one-off spikes do not distort the curve. Assumptions for penetration and pricing are reviewed with interviewees, and we only carry forward what can be explained through observable indicators and repeatable steps.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals. Model totals are checked against construction and insulation activity trends, trade flows for key chemicals, and stated capacity or demand commentary from public disclosures. When a variance looks unusual, the driver is isolated, the input is revisited, and a follow-up discussion is triggered with a relevant expert so the adjustment is not guesswork.

Before sign-off, the work goes through a multi-step internal review that includes logic checks, unit consistency checks, and cross-region reasonableness tests. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive an up to date view.

Mordor Intelligence's Spray Polyurethane Foam Market Size Compared Against Other Published Estimates

Published market numbers for spray polyurethane foam do not always match because the same term is used for slightly different product baskets and pricing points. Differences also come from the year selected as the main reference, whether the estimate is tied to construction demand signals or to supplier shipment narratives, and how often assumptions are refreshed.

In this study, the main gap drivers are whether one component cans are blended into the same total as two component systems, how roofing and waterproofing uses are treated versus general insulation, and whether the model uses a steady ASP curve or a faster price escalation assumption during raw material volatility. When currency conversion timing and base year choices differ, even similar volume views can show a meaningful spread in USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.06 B (2026) | |

| Global Consultancy A | USD 3.06 B (2025) | Uses 2025 as the base year and presents a polyurethane spray foam total that may blend adjacent polyurethane spray foam value pools and a different price base, which can shift the starting point versus a 2026 anchored series. |

| Industry Publisher B | USD 3.05 B (2025) | Starts from a 2025 base and uses a broad end-use list that can allow overlap between insulation, roofing, and sealant applications, which may change how application mix and ASP weighting are applied. |

The table shows that the spread is less about long-term direction and more about base year alignment and what gets counted inside the SPF system value. By separating two component system revenues from adjacent polyurethane foam formats and re-checking penetration and pricing against construction and retrofit indicators, the 2026 value stays traceable to clear inputs, a choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the spray polyurethane foam market?

The spray polyurethane foam market size is USD 3.06 billion in 2026 and is projected to climb to USD 3.96 billion by 2031 at a 5.27% CAGR.

Which region leads the spray polyurethane foam market?

Asia-Pacific holds 47.66% market share in 2025 and is also the fastest-growing region with a 7.21% CAGR through 2031.

Which product segment dominates sales?

Two-component high-pressure systems lead with 37.02% market share in 2025 due to their strong R-value performance and contractor familiarity.

What factor most accelerates spray foam demand?

Tightening building-energy codes worldwide drive adoption because closed-cell spray foam provides simultaneous insulation and air-barrier performance.

How are suppliers addressing environmental regulations?

Leading manufacturers are shifting to low-GWP blowing agents, investing in CO₂-based polyols, and developing isocyanate-free chemistries to comply with emerging regulatory frameworks.

Page last updated on: