Microlearning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

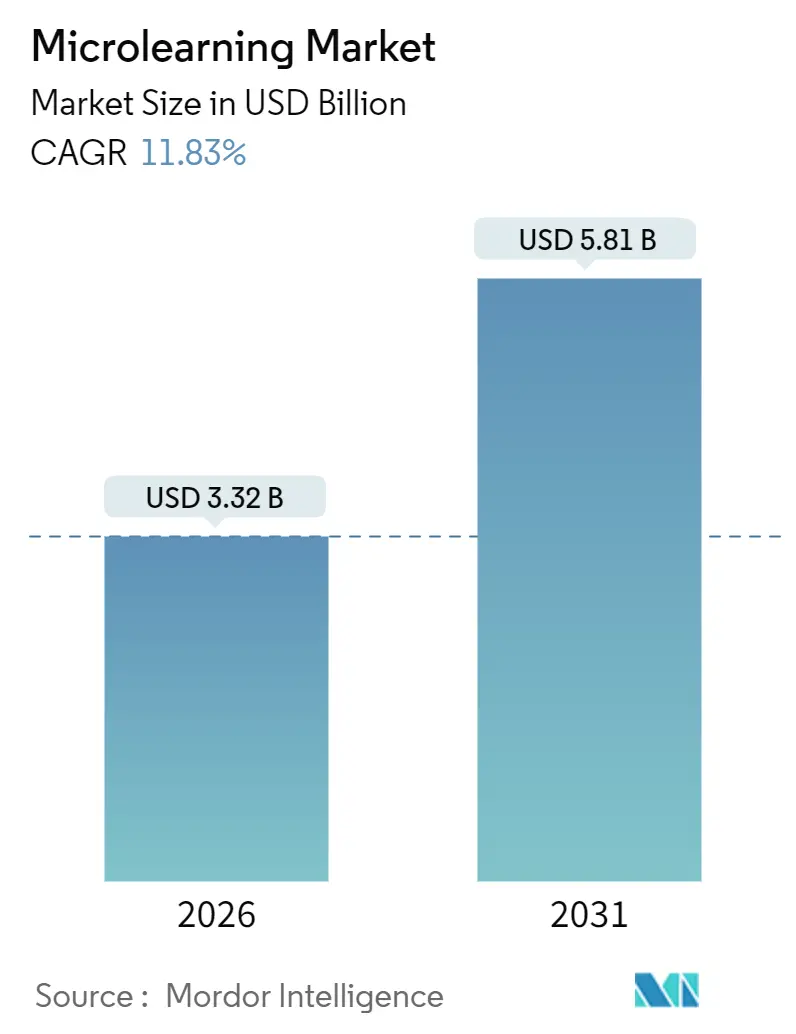

| Market Size (2026) | USD 3.32 Billion |

| Market Size (2031) | USD 5.81 Billion |

| Growth Rate (2026 - 2031) | 11.83% CAGR |

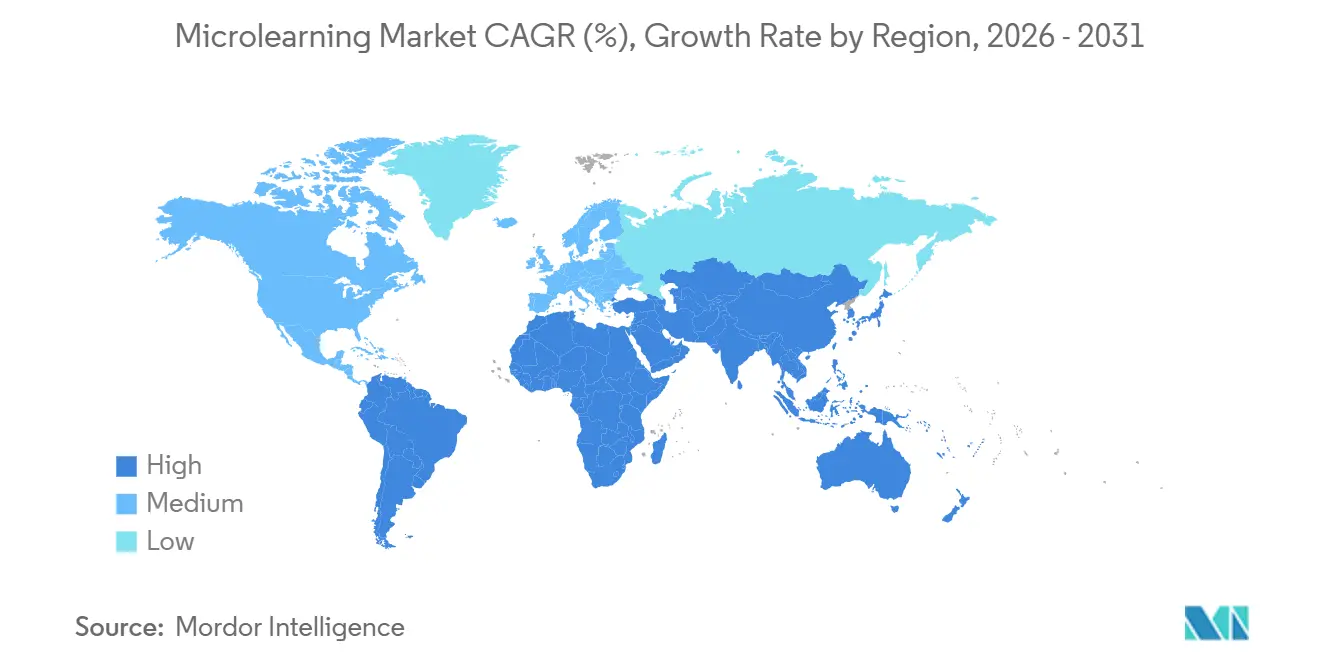

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

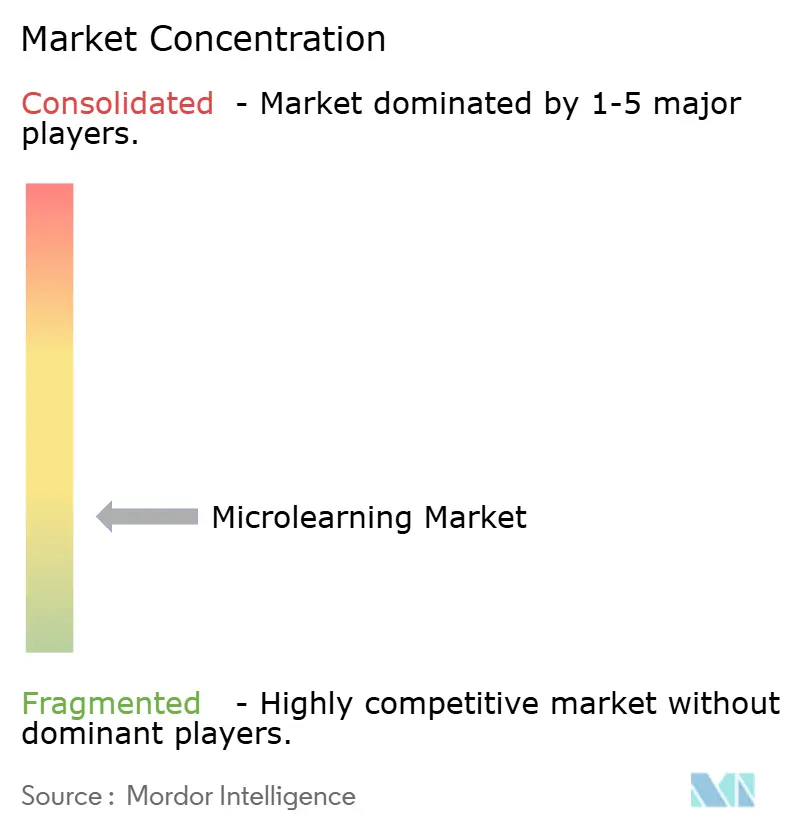

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microlearning Market Analysis by Mordor Intelligence

The microlearning market size reached USD 3.32 billion in 2026 and is forecast to advance at an 11.83% CAGR to USD 5.81 billion by 2031. Escalating demand for skills-based, just-in-time learning that fits the flow of work is steering enterprises toward mobile-first delivery models, especially in sectors with high turnover and stringent compliance needs. Platform vendors are atomizing courses into 3- to 10-minute modules that deskless and remote staff can launch on smartphones during natural workflow pauses, lifting adoption and cutting seat-time costs. ISO 27001 and SOC 2 Type II certifications have made cloud architectures credible with chief information security officers, while generative-AI authoring tools are shrinking development timelines for new content. Rivalry is intensifying as incumbent learning-management-system providers embed bite-sized content to shield installed bases, even as pure-play specialists leverage gamification and AI-driven personalization to win net-new accounts.

Key Report Takeaways

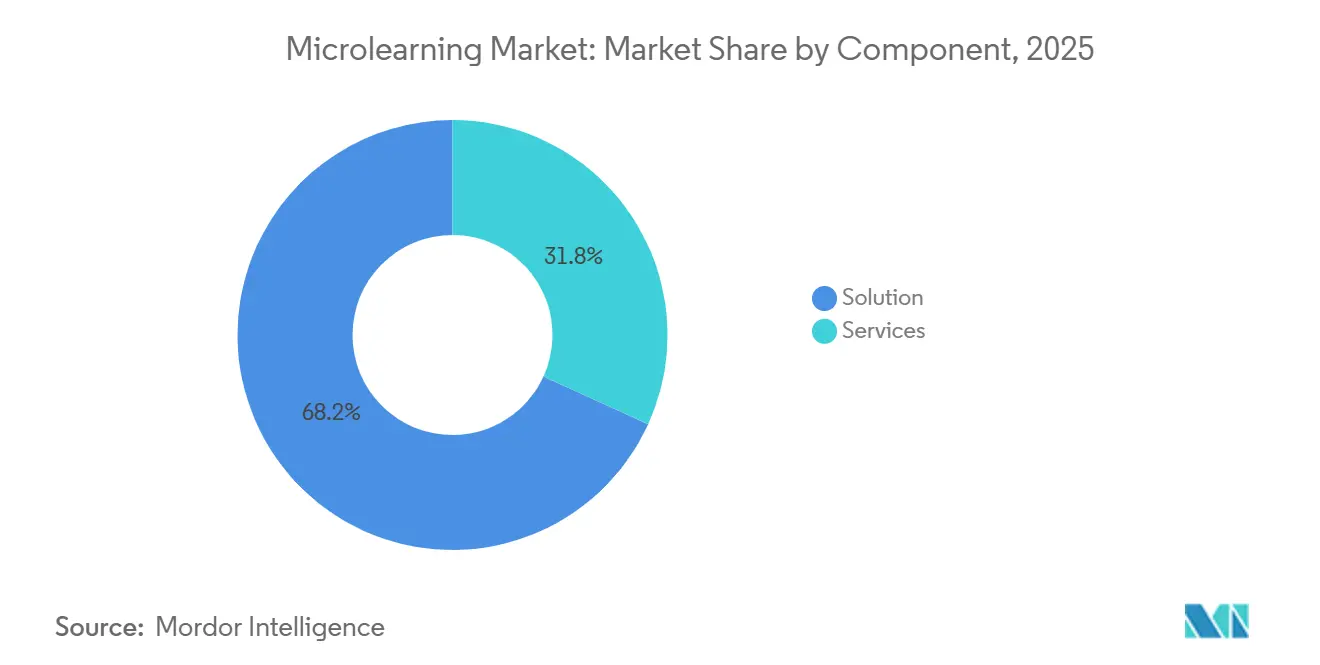

- By component, solution offerings led with 68.19% revenue share in 2025, and services are projected to grow at a 13.43% CAGR through 2031.

- By organization size, large enterprises commanded 54.72% of microlearning market share in 2025, whereas small and medium-sized enterprises are on track for a 14.59% CAGR to 2031.

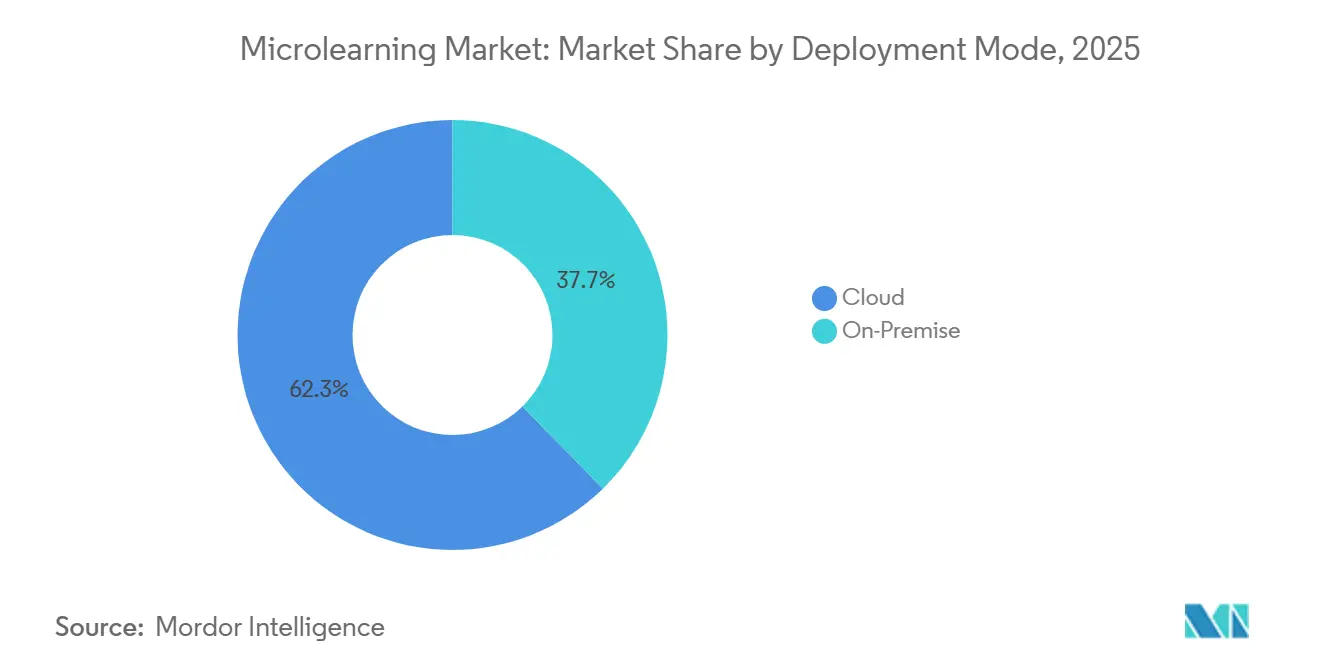

- By deployment mode, cloud platforms captured 62.33% share in 2025 and are poised to expand at a 15.19% CAGR through 2031.

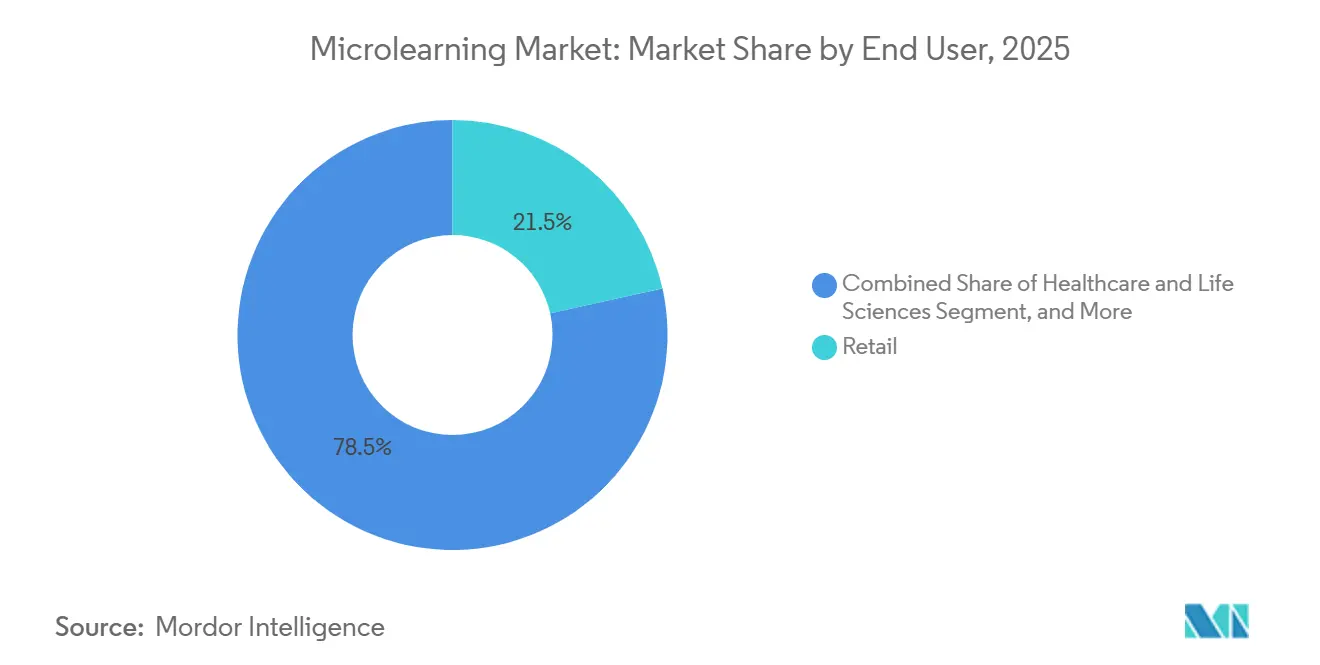

- By end user, retail held 21.53% of revenue in 2025, while healthcare and life sciences are forecast to post the fastest 15.22% CAGR.

- By geography, North America accounted for 37.61% of 2025 revenue, yet Asia Pacific is expected to log a 14.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microlearning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Mobile-First Workforce Learning Platforms | +2.80% | Global, with accelerated adoption in Asia Pacific and North America | Medium term (2-4 years) |

| Growing Need for Skills-Based, Just-in-Time Training | +3.10% | Global, particularly in manufacturing, retail, and logistics sectors | Long term (≥ 4 years) |

| Gamification Enhancing Learner Engagement and Retention | +1.90% | North America and Europe core, expanding to Asia Pacific | Short term (≤ 2 years) |

| AI-Driven Personalization of Micro-Content | +2.40% | North America and Europe early adopters, Asia Pacific following | Medium term (2-4 years) |

| Integration of Microlearning into Flow-of-Work Productivity Tools | +2.20% | Global, with enterprise concentration in North America and Europe | Medium term (2-4 years) |

| Regulatory Push for Continuous Compliance Training in Highly Regulated Industries | +1.70% | North America, Europe, Asia Pacific (BFSI and healthcare focus) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Mobile-First Workforce Learning Platforms

Roughly 2.7 billion frontline and deskless employees now rely on smartphones for daily tasks, and adoption of microlearning market solutions that launch natively on iOS and Android removes the desktop bottleneck. Beverage chain Chatime reached 91% learner uptake with sub-5-minute modules accessed during pre-shift briefings, while Pet Supermarket logged 79% completion rates and cut turnover by 15% using similar tactics.[1]SC Training, “Pet Supermarket Case Study,” sctraining.com AWS projects Asia Pacific will require 5.7 billion digital training interventions by 2025, a scale only feasible with asynchronous mobile delivery.[2]Amazon Web Services, “Building Asia Pacific's Digital Workforce,” aws.amazon.com Broader 5G coverage is enabling latency-free video and simulation on phones, making immersive formats viable for field technicians and clinicians.

Growing Need for Skills-Based, Just-In-Time Training

Enterprises moving away from annual course calendars toward role-triggered interventions are fuelling microlearning market demand. Workers asked to master new equipment, regulations, or product features benefit more from a 5-minute refresher than a half-day workshop. Internal mobility and retention gains of up to 3 times have been documented when skills-based pathways replace generic curricula. Tagging every module with competency metadata lets platforms surface content the instant an ERP or CRM system detects a workflow change, shortening time-to-productivity for new hires.

Gamification Enhancing Learner Engagement and Retention

Short lessons risk passive scrolling, so vendors deploy points, badges, and leaderboards to activate dopamine reward cycles. A 2024 TalentLMS survey showed gamified content boosting engagement by 83% and completion by 48% across retail, healthcare, and tech cohorts.[3]TalentLMS, “Gamification Survey 2024,” talentlms.com Extrinsic rewards best suit procedural or compliance topics, while narrative challenges foster deeper mastery in leadership and strategy programs. Spaced-repetition engines that surface quizzes at scientifically timed intervals further cement retention, yet over-gamification can dilute seriousness in safety-critical contexts.

AI-Driven Personalization of Micro-Content

Large language models integrated into microlearning market platforms generate adaptive paths that tailor sequence and difficulty to each learner’s prior knowledge. Adobe Learning Manager introduced retrieval-augmented recommendations that pull from proprietary wikis and policy libraries to serve 3-minute explainers exactly when performance data flags a skills gap.[4]Adobe, “Learning Manager AI Personalization,” adobe.com Studies in 2024 recorded 23% better outcomes versus static playlists, with the greatest lift among below-average performers. Privacy concerns push banks and hospitals to deploy on-premises or private cloud instances, so training data stays inside controlled borders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Transforming Legacy Content into Micro-Modules | -1.80% | Global, with acute impact on large enterprises in North America and Europe | Short term (≤ 2 years) |

| Difficulty in Measuring ROI Versus Traditional L&D Approaches | -1.20% | Global, particularly in organizations with immature learning-analytics capabilities | Medium term (2-4 years) |

| Data-Privacy and Security Concerns in Cloud-Based Learning Platforms | -0.90% | Europe (GDPR), Asia Pacific (data-residency laws), North America (sector-specific regulations) | Long term (≥ 4 years) |

| Content Fatigue from Over-Fragmentation of Learning Assets | -0.70% | Global, with higher incidence in organizations deploying high-frequency push notifications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Transforming Legacy Content into Micro-Modules

Articulate benchmarking shows converting a single traditional course into micro-units’ costs USD 10,000 to USD 50,000 and demands up to 184 development hours per finished hour. Enterprises with 100-course libraries confront multiyear efforts that force them to run legacy and microlearning market platforms in parallel. Scarce subject-matter experts further slow progress, prompting buyers to favour vendors offering content-as-a-service bundles that slash lead times but may lack industry-specific nuance.

Difficulty in Measuring ROI Versus Traditional L and D Approaches

Legacy Kirkpatrick or Phillips models were built for classroom events, not continuous pipelines of 3-minute videos. Only a quarter of companies track post-training behaviour change, making it hard to justify microlearning market budgets to finance leaders. Correlating completions with promotion velocity, retention, or productivity requires data engineering many teams lack, and inconsistent vendor success metrics complicate platform comparisons. Until standardized dashboards emerge, skepticism around ROI will temper spending growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum

Solution licenses generated 68.19% of 2025 revenue, yet services are projected to outstrip the broader microlearning market at a 13.43% CAGR to 2031. As organizations re-platform, they increasingly outsource content audits, integration, and change management, favouring vendors that bundle advisory with technology. Consulting engagements map competencies, redesign learning pathways, and configure APIs, while support contracts provide ongoing upgrades and helpdesk access that convert into predictable annual recurring revenue.

Many large enterprises maintain catalogues exceeding 100 legacy courses, a workload internal teams cannot re-author quickly. Vendors such as Skillsoft and Cornerstone now position content-as-a-service to shrink deployment from 18 months to 6 months, addressing worries that microlearning sacrifices depth. The result is expanding professional-services pipelines that stabilize cash flows and deepen customer lock-in.

By Organization Size: SMEs Accelerate Adoption

Large enterprises held 54.72% of microlearning market share in 2025, leveraging bigger L&D budgets and IT support. However, SMEs are expected to grow at 14.59% through 2031 as cloud subscriptions remove upfront infrastructure costs. Freemium tiers from EdApp or TalentCards let firms pilot with ten users, while AI authoring converts PDFs and SOPs into mobile-ready modules, eliminating instructional-design bottlenecks.

The OECD found European SMEs allocate just 1.2% of revenue to training, so low-cost, high-impact interventions resonate. Yet subject-matter experts, not learning professionals, create most small-business content, risking pedagogical gaps. Vendors counter with template-driven storyboards and automated assessment generation that align microlearning market experiences with adult-learning principles without inflating budgets.

By Deployment Mode: Cloud Captures Majority Share

Cloud captured 62.33% of deployments in 2025 and is projected to post the fastest 15.19% CAGR, thanks to zero-trust compatibility and automatic feature upgrades. Native links to Okta and Azure Active Directory speed user provisioning, while ISO 27001 and SOC 2 Type II audits address security due diligence for regulated buyers. These traits make cloud offerings the default for fresh implementations, driving the microlearning market size at the platform layer.

On-premises persists in government and financial segments bound by data-sovereignty rules. GDPR and China’s Personal Information Protection Law force some buyers to keep learning records on national soil, so vendors maintain private-cloud and self-hosted editions. However, manual patching, capital spending for servers, and slower innovation cycles tilt economics toward SaaS wherever regulations permit.

By End User: Healthcare Leads Growth Curve

Retail remained the largest adopter at 21.53% revenue share in 2025, reflecting huge frontline populations and constant product updates. Yet healthcare and life sciences are forecast for the sharpest 15.22% CAGR, propelled by continuing-medical-education rules and Joint Commission competency standards. Ten-minute micro-modules let clinicians earn credits between patient rounds, making the microlearning market indispensable for hospitals facing staffing shortages.

BFSI institutions use bite-sized anti-money-laundering and cybersecurity refreshers to comply with FFIEC and FINRA rules, while telecom and tech firms employ microlearning for 5G and cloud skill gaps that evolve faster than certification bodies can update syllabi. Manufacturing and logistics embed short safety drills accessible on rugged tablets at the point of work, cutting incident rates without halting production lines.

By Delivery Format: Interactive Simulations Gain Traction

Video remains the default because it conveys emotion and procedure effectively, but interactive simulations are growing for tasks where hands-on practice determines proficiency. Computers and Education reported simulation-based microlearning improving outcomes by 31% for troubleshooting and maintenance tasks. Simulations demand up to 300 development hours per finished hour yet deliver measurable performance lifts that justify investment in safety-critical settings.

Podcasts and audiobooks serve knowledge workers during commutes, while gamified quizzes reinforce compliance concepts that mainly require memorization. Infographics and micro-blogs communicate quick policy updates, although their static nature can dampen engagement. Blended format libraries enable learning leaders to match media to complexity and cognitive load, enriching the microlearning market ecosystem without overwhelming budgets.

Geography Analysis

North America generated 37.61% of 2025 revenue. High LMS penetration, dense vendor clusters, and stringent banking and healthcare regulations ensure steady recurring spend. The FFIEC’s 2024 update to Bank Secrecy Act guidance emphasized adaptive, role-based training, validating microlearning solutions for compliance workflows. Private-equity interest peaked with Cornerstone’s USD 5.2 billion take-private, signalling confidence in continued consolidation. Saturation is a looming headwind, so growth now hinges on upselling AI personalization and skills-intelligence modules.

Asia Pacific is forecast to record the fastest 14.81% CAGR as smartphone ubiquity meets government upskilling mandates. Singapore’s Digital Enterprise Blueprint targets 95% SME tech adoption by 2025, funding AI courses that already trained 2,000 workers. Indonesia’s Kartu Prakerja enrolled 14.3 million citizens, supplying IDR 32 trillion (USD 2.1 billion) in grants for bite-sized digital skills courses. AWS estimates 819 million regional workers need new digital abilities by 2025, heralding massive microlearning market potential. Regional data-residency rules raise infrastructure costs, but vendors with in-country data centers gain first-mover advantage.

Europe’s trajectory is shaped by GDPR, which classifies learning records as personal data, compelling vendors to keep servers inside the European Economic Area. Homegrown providers such as Valamis leverage regional hosting to win public-sector accounts, while global players invest in Frankfurt and Dublin regions to comply. Germany’s dual-training model encourages apprentices to use microlearning for theory between shop-floor rotations, and France’s medical-education requirements are boosting demand in healthcare. Latin America, the Middle East, and Africa remain early-stage but show promise as multinationals deploy standardized programs across subsidiaries, using the microlearning market to avoid travel costs and classroom downtime.

Competitive Landscape

The top five suppliers account for roughly 35-40% of revenue, indicating moderate concentration. Cornerstone OnDemand, Docebo, Skillsoft, Udemy Business, and IBM lead by breadth of content, integrations, and enterprise footprint. Pure-play challengers such as Axonify, EdApp, and Qstream win deals with mobile-first design and rapid deployment times. Feature parity is narrowing: most platforms now support video, quizzes, gamification, and AI-driven recommendations, pushing price and customer success to the forefront.

Clearlake Capital’s purchase of Cornerstone provides capital for multi-year R&D, while Skillsoft’s acquisition of SumTotal adds performance-management modules to fight suite vendors like SAP SuccessFactors.

Docebo bundles APIs for Microsoft Teams and Salesforce so learning appears inside employee workflows, a tactic mirrored by IBM’s watsonx integration that answers natural-language questions with 3-minute clips. Vendors race to secure ISO 27001 and SOC 2 attestations as procurement teams bake security into RFP scoring. Emerging players harness generative AI to convert SOPs into lessons within hours, courting SMEs priced out of custom development. As scale becomes essential for continuous innovation, further mergers are likely.

Microlearning Industry Leaders

Mindtree Limited

IBM Corporation

SwissVBS

Axonify Inc.

Bigtincan Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Docebo announced the expansion of its AI-powered learning suite with enhanced integration capabilities for Microsoft Teams and Slack, enabling organizations to deliver microlearning content directly within collaboration platforms.

- September 2025: Skillsoft launched Percipio 2.0, a redesigned learning experience platform featuring AI-driven content curation and personalized learning pathways based on role, skill level, and career aspirations.

- August 2025: EdApp (SafetyCulture) secured a major enterprise contract with a global retail chain operating over 5,000 locations, deploying mobile-first microlearning modules for frontline worker training across 15 countries.

Global Microlearning Market Report Scope

The Microlearning Market Report is Segmented by Component (Solution, Services), Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), Deployment Mode (On-Premise, Cloud), End User (Retail, Manufacturing, BFSI, Telecom and IT, Healthcare and Life Sciences, Logistics, Education, Media and Entertainment), Delivery Format (Video-Based Learning, Interactive Simulations, Podcasts and Audiobooks, Quizzes and Assessments, Infographics, Micro-Blogs and Text Nuggets), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solution | |

| Services | Consulting and Implementation |

| Support and Maintenance |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Premise |

| Cloud |

| Retail |

| Manufacturing |

| Banking, Financial Services and Insurance |

| Telecom and IT |

| Healthcare and Life Sciences |

| Logistics |

| Education |

| Media and Entertainment |

| Video-Based Learning |

| Interactive Simulations |

| Podcasts and Audiobooks |

| Quizzes and Assessments |

| Infographics |

| Micro-Blogs and Text Nuggets |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | GCC |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| North Africa | |

| Rest of Africa |

| By Component | Solution | |

| Services | Consulting and Implementation | |

| Support and Maintenance | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End User | Retail | |

| Manufacturing | ||

| Banking, Financial Services and Insurance | ||

| Telecom and IT | ||

| Healthcare and Life Sciences | ||

| Logistics | ||

| Education | ||

| Media and Entertainment | ||

| By Delivery Format | Video-Based Learning | |

| Interactive Simulations | ||

| Podcasts and Audiobooks | ||

| Quizzes and Assessments | ||

| Infographics | ||

| Micro-Blogs and Text Nuggets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| North Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the microlearning market expected to grow through 2031?

It is projected to advance at an 11.83% CAGR, lifting value from USD 3.32 billion in 2026 to USD 5.81 billion by 2031.

Which segment is expanding faster than the overall market?

Services, which include consulting, implementation, and support, are forecast to grow at a 13.43% CAGR to 2031, slightly ahead of the total market pace.

Why are small and medium-sized enterprises adopting microlearning?

Cloud subscriptions remove infrastructure costs, freemium pilots cut risk, and AI authoring converts existing documents into lessons, enabling SMEs to upskill staff without large budgets.

What drives healthcare to be the fastest-growing end user?

Continuing-medical-education requirements and Joint Commission competency standards push hospitals to deliver short, mobile modules clinicians can finish between patient appointments.

How do security certifications influence deployment choices?

ISO 27001 and SOC 2 Type II audits reassure risk officers, enabling 62.33% of buyers to favor cloud deployments while highly regulated entities keep limited on-premises instances.

Which regions offer the highest growth potential?

Asia Pacific leads with a forecast 14.81% CAGR, boosted by government upskilling grants and the region's large mobile workforce.

Page last updated on: