Mexico OTT TV And Video Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

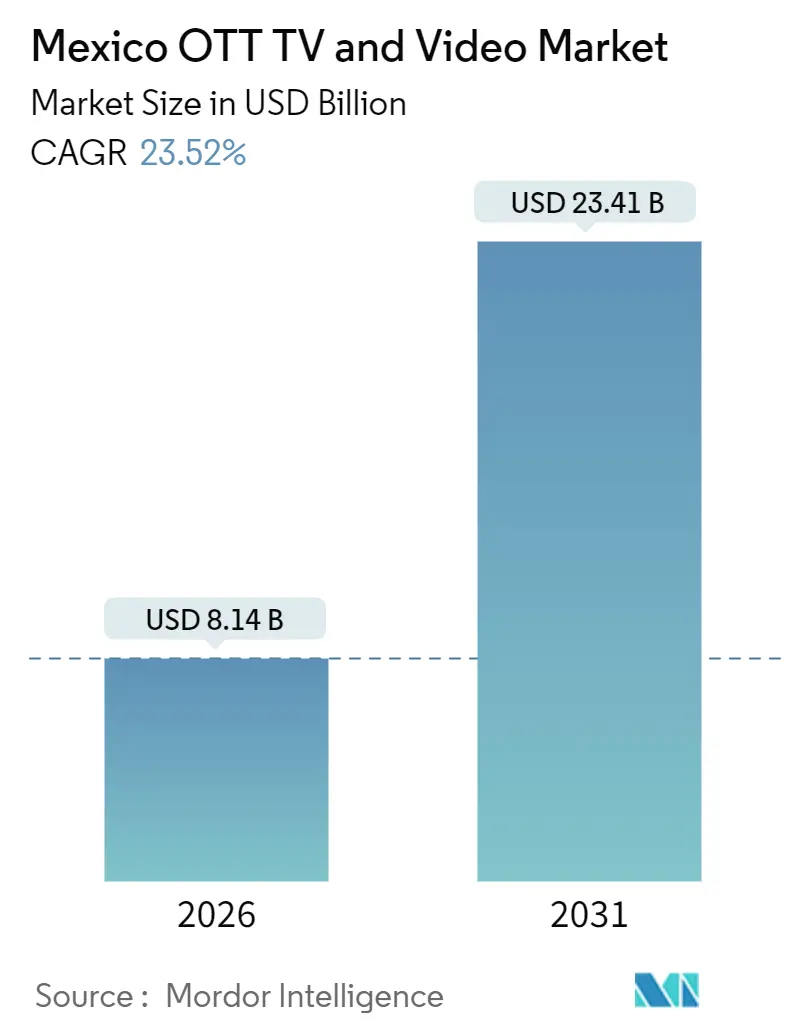

| Market Size (2026) | USD 8.14 Billion |

| Market Size (2031) | USD 23.41 Billion |

| Growth Rate (2026 - 2031) | 23.52% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico OTT TV And Video Market Analysis by Mordor Intelligence

The Mexico OTT TV and Video market size stood at USD 8.14 billion in 2026 and is forecast to reach USD 23.41 billion in 2031, registering a robust 23.52% CAGR over the period. Structural changes in Mexican viewing habits, telco bundling of streaming services, and a USD 1 billion content commitment by Netflix are collectively accelerating adoption. Rapid fiber rollouts in high-density corridors, a nationwide shift toward hybrid ad-supported models, and intensified local production of Spanish-language originals deepen engagement and lift time-spent per viewer. Meanwhile, alternative payment rails such as OXXO Pay and SPEI expand the reachable base beyond the 40% credit-card penetration threshold, reducing friction for first-time payers. Advanced audience analytics elevate programmatic campaign efficiency, giving advertisers stronger return-on-investment signals and encouraging larger budgets. Simultaneously, piracy and macro volatility temper near-term profitability, prompting platforms to balance price points with household purchasing power.

Key Report Takeaways

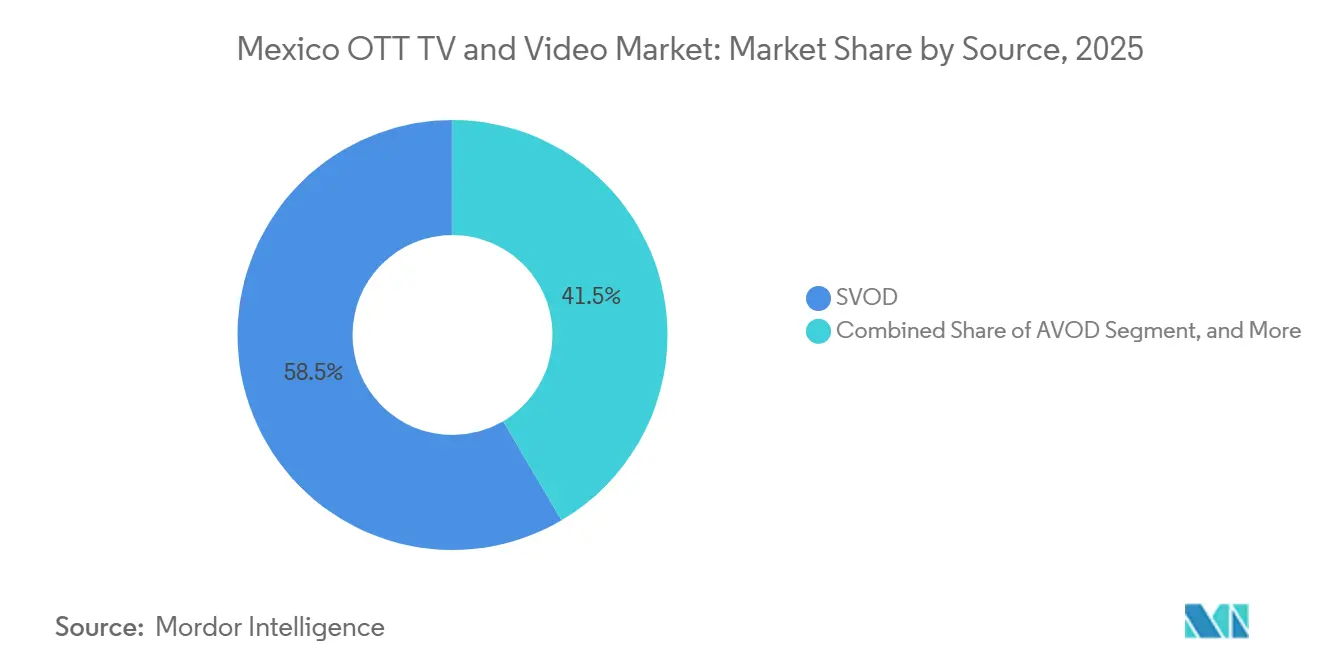

- By source, subscription video on demand led with 58.47% revenue share in 2025; advertising-supported video on demand is projected to advance at a 24.79% CAGR through 2031.

- By device type, smart televisions commanded 46.31% revenue share in 2025, while smartphones are set to grow at 24.11% CAGR to 2031.

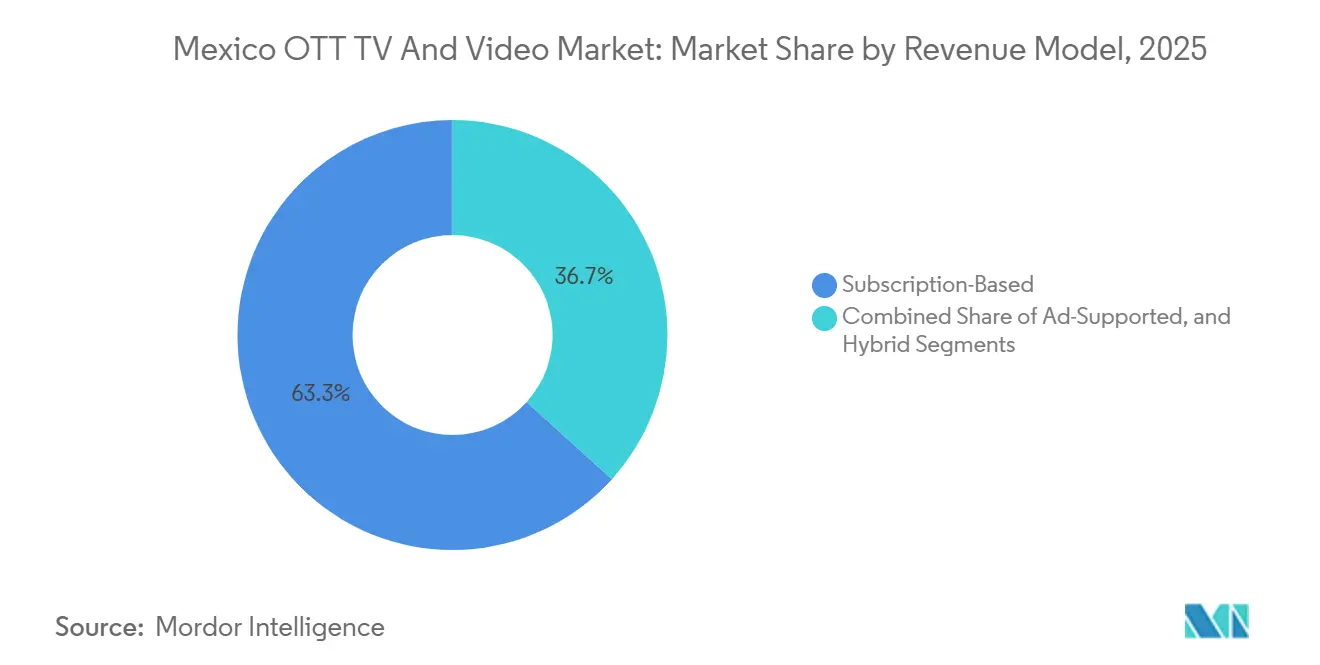

- By revenue model, subscription-based services accounted for 63.29% of the Mexico OTT TV and Video market size in 2025, whereas hybrid offerings are on track for 23.98% CAGR expansion.

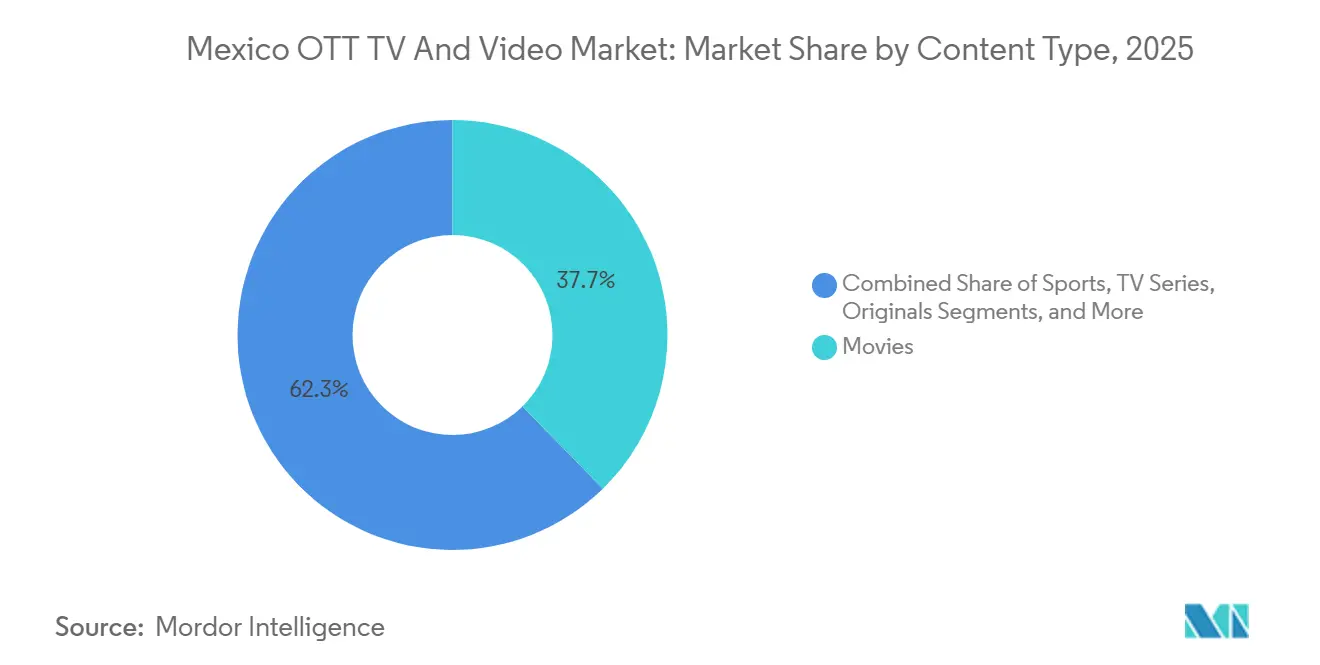

- By content type, movies held 37.67% of value in 2025, and originals are forecast to climb at a 24.78% CAGR to 2031.

- By end-user age group, millennials generated 41.22% of spending in 2025, but Generation Z shows the fastest momentum with a 25.03% CAGR outlook.

- By geography, Central Mexico captured 48.18% of revenue in 2025; Northern Mexico is projected to post the highest growth at 25.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico OTT TV And Video Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Penetration of Smart TVs and Ubiquitous Broadband | +4.20% | National, with concentration in Central Mexico urban centers | Medium term (2-4 years) |

| Rising Original Spanish-Language Content Investment | +5.10% | National, with production hubs in Mexico City and Guadalajara | Long term (≥ 4 years) |

| Growing Adoption of Hybrid AVOD-SVOD Models | +3.80% | National, accelerating in Northern Mexico | Short term (≤ 2 years) |

| Expansion of Mobile-First, Low-Cost Plans | +4.50% | National, with higher uptake in rural and lower-income areas | Medium term (2-4 years) |

| Telco Bundling of OTT Subscriptions | +3.90% | National, led by Telmex, Totalplay, Megacable footprints | Short term (≤ 2 years) |

| Advanced Audience Analytics Driving Targeted Ads | +2.70% | National, with early adoption in programmatic CTV inventory | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Penetration of Smart TVs and Ubiquitous Broadband

Smart-TV ownership passed the 46% threshold by 2025, while fixed broadband lines reached 27.9 million, underpinned by rapid fiber deployments that lift average download speeds above 50 Mbps.[1]Instituto Federal de Telecomunicaciones, “Estadísticas del Sector de Telecomunicaciones,” ift.org.mx Operators with faster, more stable networks can command premium fees from streaming partners and keep churn low by guaranteeing seamless 4K playback. Yet only 800 000 rural residents have consistent streaming access, revealing a digital divide. Price sensitivity remains acute: a budget handset still equals nearly three quarters of a monthly income in Chiapas, forcing platforms to offer adaptive bitrate streams and budget tiers.

Rising Original Spanish-Language Content Investment

Netflix’s four-year USD 1 billion pledge announced in 2025 accelerates a trend that already sees Mexico generate one quarter of all Spanish-language shows worldwide.[2]Daniel Rook, “Netflix says to spend USD 1 billion producing content in Mexico,” Grand Junction Sentinel, gjsentinel.com Local productions now obtain roughly half of their lifetime revenue from streaming rights, overturning box-office dependency. Amazon Prime Video strengthened the production ecosystem by installing Latin America’s first virtual-production LED stage at Churubusco Studios, cutting location costs and enabling complex visuals. Government alignment is visible in the 2025 Foreign Ministry agreement that lets Mexican embassies showcase domestic titles abroad, reinforcing cultural diplomacy.

Growing Adoption of Hybrid AVOD-SVOD Models

ViX’s freemium blueprint demonstrates the ceiling for ad-supported reach, logging more than 50 million monthly users worldwide by mid-2024 and converting a tenth into pay subscribers. Disney Plus followed with an MXN 149 (USD 8.51) ad tier in June 2025, mirroring HBO Max’s price point. Lower entry fees resonate in a country where less than 40% of adults hold credit cards, and cash still dominates small-ticket transactions. Platforms that marry first-party viewing data with programmatic buying secure premium CPMs, cushioning subscription erosion.[3]Secretaría de Relaciones Exteriores, “Foreign Ministry-Netflix Collaboration Agreement,” gob.mx

Expansion of Mobile-First, Low-Cost Plans

Smartphone penetration is projected to reach at least 85% by 2030. Median mobile speeds rose nearly 39% year-over-year to 45.2 Mbps in 2024, enabling HD streaming during commutes. ViX, Disney Plus, and TelevisaUnivision exploit this mobility wave through bundles distributed via OXXO vouchers and Mercado Libre wallets, capturing users outside the banking mainstream. Compression codecs, download-for-offline options, and per-day passes become critical features in bandwidth-constrained provinces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Credit-Card Penetration Limiting Paid Conversions | -2.80% | National, most acute in southern and rural states | Medium term (2-4 years) |

| Piracy and Illegal Streaming Devices | -3.10% | National, with higher incidence in border states | Long term (≥ 4 years) |

| High Local Content Licensing Costs | -1.60% | National, concentrated in production hubs | Medium term (2-4 years) |

| Macroeconomic Volatility Impacting Disposable Income | -2.30% | National, with greater sensitivity in lower-income segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Credit-Card Penetration Limiting Paid Conversions

Only 58% of Mexicans held a formal financial account in 2025, and credit-card ownership lags even further, compelling platforms to weave in voucher-based or real-time transfer options.[4]World Bank, “Financial Inclusion in Mexico,” worldbank.org The added friction raises customer-acquisition costs and slows recurring revenue growth. Netflix’s 2024 clamp-down on password sharing amplified price sensitivity, leading to higher churn among multi-household account sharers. Freemium and ad tiers serve as safety nets, but processing cash and bank transfers involves elevated commission fees and reconciliation complexity.

Piracy and Illegal Streaming Devices

Mexico ranked second globally for illicit camcording incidents in the 2024 USTR Special 301 Report. Pre-loaded set-top boxes and modified streaming adapters proliferate in open-air markets, undercutting legitimate services. Platforms counter with forensic watermarking and device authentication, yet aggressive controls risk alienating legitimate travellers and multi-device households. The 2025 telecom overhaul set up new regulators but left questions about enforcement priorities, creating uncertainty for long-term anti-piracy initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Subscription Models Anchor Revenue, Ad-Supported Tiers Accelerate

Subscription video on demand held 58.47% revenue share in 2025 within the Mexico OTT TV and Video market. Hybrid ad-supported formats, however, are marching toward a 24.79% CAGR through 2031 as viewers seek flexible pricing and as advertisers chase incremental reach. ViX proves that free tiers can monetize at scale, while Disney Plus’ ad plan validates a dual-stream future. Transactional rentals and downloads cater to cinephiles looking for niche premieres, yet rampant piracy and deep catalogue subscription plans strip away their growth headroom. Platforms that integrate transparent brand-safety controls reassure advertisers and help throttle invalid traffic, a known pain point in the connected-television arena.

A second dynamic is regulatory: the 2025 ban on foreign government advertising on digital outlets removes a small but stable revenue slice for global news channels, nudging them toward diversified sponsorship models. Although this policy shift introduces short-term turbulence, the long-run impact on the Mexico OTT TV and Video market should be muted because domestic consumer brands remain highly active buyers.

By Device Type: Smart TVs Dominate Viewing Hours, Smartphones Expand Reach

Smart televisions contribute 46.31% of 2025 revenues and remain the centerpiece for evening co-viewing and live events. Roku continues to ship the majority of streaming sticks, but television OEMs embed native operating systems that push consumers straight into branded tiles, raising the bar for app storefront visibility. The Mexico OTT TV and Video market share tied to smartphones will accelerate behind a 24.11% CAGR, reflecting a nation where nearly all internet users carry a handset. Tablets, laptops, consoles, and legacy set-top boxes service specialized settings such as children’s bedrooms or gaming dens, but each faces cannibalization risk as multi-screen functionality improves.

Differentiation hinges on context-aware features: automatic bitrate adjustment on congested mobile networks, quick-resume tokens synchronized across screens, and 4K Dolby Vision support for living-room sessions. Operators like Totalplay, clocking 53.9 Mbps average downstream speeds, provide the bandwidth backbone that lets households stream concurrently on multiple devices without buffering.

By Revenue Model: Subscription Dominance Encounters Hybrid Disruption

Subscription-centric plans still delivered 63.29% of the 2025 value, but hybrid strategies are disrupting the status quo. ViX’s three-tier structure draws a wide funnel: free users, ad-tier subscribers, and premium ad-free households. Disney Plus mirrored the approach, pegging its ad plan at MXN 149 (USD 8.51) per month to entice cost-conscious families. The Mexico OTT TV and Video market size attributable to hybrid revenue architectures is projected to expand rapidly as advertisers demand audience reach that linear television can no longer guarantee. Elevated connected-television fraud rates in Mexico, however, force platforms to invest in verification tech before ad buyers accept higher CPMs.

Subscription-only players still hold leverage where blockbuster franchises or exclusive sports rights create must-see value. Yet even they increasingly view advertising as a downside hedge against macro shocks and currency swings that compress disposable income.

By End-User Age Group: Millennials Anchor Spending, Generation Z Fuels Mobile Growth

Millennials generated 41.22% of 2025 revenue as they straddle peak earnings and entrenched subscription habits. Generation Z, however, is the fastest riser, set for a 25.03% CAGR through 2031 as mobile-first behaviour aligns with shorter, snackable formats. Seniors and Boomers remain tethered to linear channels but are slowly sampling streaming via bundled ISP packages.

Content strategy must therefore balance serialized dramas and true-crime series for millennials with short-form influencer collaborations for younger viewers. ViX and Disney Plus harness cross-demographic appeal by packaging live football with animation and Hollywood tent-poles.

By Content Type: Movies Lead Share, Originals Differentiate

Movies commanded 37.67% of 2025 spend, buoyed by first-run studio titles and evergreen library hits. Originals, benefiting from Netflix’s USD 1 billion four-year pact and Amazon’s LED volume stage, are forecast to grow at 24.78% CAGR as platforms chase proprietary catalogues to curb licensing outlays. Long-form series bolster binge engagement and retention, while live sports such as Liga MX and UEFA Champions League create appointment viewing underpinned by dual-screen social chatter. User-generated video, epitomized by YouTube, already holds a double-digit share of total television minutes, blurring lines between professional and creator economies.

Economic stakes are substantial: a single tent-pole production such as Pedro Páramo injected USD 18 million into local supply chains in 2025, illustrating the multiplier effect of original content on jobs and ancillary sectors. Platforms that co-finance production infrastructure gain bargaining power, ensuring priority access to talent and IP pipelines.

Geography Analysis

Central Mexico generated 48.18% of 2025 revenues within the Mexico OTT TV and Video market, underwritten by dense fiber coverage, higher disposable incomes, and better payment-card availability. Mexico City’s role as a production hub also magnetizes original content spend. Yet saturation raises competitive intensity; every global and regional platform vies for stack position within telecom bundles.

Northern Mexico is forecast to post a stellar 25.32% CAGR through 2031. Industrial corridors and cross-border commerce lift earnings, while lower piracy rates and bilingual households encourage dual-language content consumption. Megacable’s investment surge, MXN 5.1 billion (USD 291 million) in first-half 2024, reflects a strategic bet on this region’s upside potential.

Southern and rural territories present a contrasting picture. Only 800 000 rural residents possess adequate connections for OTT viewing. Handset prices can swallow over half a monthly wage, and fixed broadband remains patchy. Nevertheless, mobile broadband at 58% penetration acts as an entry ramp. Bundles that integrate OXXO Pay vouchers or Mercado Libre wallets accommodate the high-cash culture prevalent in these areas, broadening the Mexico OTT TV and Video market reach.

Competitive Landscape

Competition is moderate, with Netflix, Disney Plus, Amazon Prime Video, and HBO Max sharing the field with Spanish-language specialist ViX and telco-backed Claro Video. Netflix still dominates premium SVOD catalogues, but ViX’s hybrid model and exclusive football rights render it the fastest climber. Telcos such as Totalplay and Telmex leverage broadband bundles to boost stickiness; Totalplay invoiced only MXN 8.5 million (USD 0.49 million) in direct OTT commissions during Q1 2025, signalling that bundles are more about churn control than immediate profit.

Sports streaming is the next battleground. Fox’s June 2025 acquisition of Caliente TV signals fresh bids for Liga MX fragments, while TelevisaUnivision holds an Olympic Games lock-in through 2032. User-generated platforms like YouTube capture significant viewing minutes but still trail in average revenue per user. Emerging niche players, from arthouse-focused Mubi to domestic film curator FilminLatino, add texture yet command limited scale.

Strategic levers that will define leadership include first-party data analytics, anti-piracy investments, co-financed local productions, and innovative payment integrations that offset low banking penetration. Platforms mastering this matrix can capture disproportionate Mexico OTT TV and Video market share.

Mexico OTT TV And Video Industry Leaders

Netflix, Inc.

Amazon.com, Inc.

América Móvil, S.A.B. de C.V.

Televisa, S. de R.L. de C.V.

Telefónica, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Grupo Televisa finalized the integration of Izzi and Sky, unlocking cost synergies earmarked for a future buyout of ATandT’s Sky stake.

- August 2025: CBS Sports teamed with TelevisaUnivision to air English-language Liga MX matches in the United States, extending the monetization horizon for Mexican football rights.

- June 2025: Fox acquired Caliente TV to widen its live-sports footprint and prepare bids for forthcoming rights auctions.

- June 2025: TelevisaUnivision and Disney Entertainment forged a distribution pact that bundles Disney Plus with ViX for Mexican consumers.

Mexico OTT TV And Video Market Report Scope

The Mexico OTT TV and Video Market Report is Segmented by Source (SVOD, TVOD, Rental, Download to Own, AVOD), Device Type (Smart TV, Smartphone, Tablet, PC/Laptop, Game Console, Set-Top Box), Revenue Model (Subscription-Based, Ad-Supported, Hybrid), Content Type (Movies, TV Series, Sports, User-Generated Content, Originals), End-User Age Group (Generation Z, Millennials, Generation X, Baby Boomers, Seniors), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| SVOD |

| TVOD |

| Rental |

| Download to Own (DTO) |

| AVOD |

| Smart TV |

| Smartphone |

| Tablet |

| PC/Laptop |

| Game Console |

| Set-Top Box |

| Subscription-Based |

| Ad-Supported |

| Hybrid |

| Generation Z (Up to 25 years) |

| Millennials (26-41 years) |

| Generation X (42-57 years) |

| Baby Boomers (58-76 years) |

| Seniors (Above 77 years) |

| Movies |

| TV Series |

| Sports |

| User-Generated Content |

| Originals |

| By Source | SVOD |

| TVOD | |

| Rental | |

| Download to Own (DTO) | |

| AVOD | |

| By Device Type | Smart TV |

| Smartphone | |

| Tablet | |

| PC/Laptop | |

| Game Console | |

| Set-Top Box | |

| By Revenue Model | Subscription-Based |

| Ad-Supported | |

| Hybrid | |

| By End-User Age Group | Generation Z (Up to 25 years) |

| Millennials (26-41 years) | |

| Generation X (42-57 years) | |

| Baby Boomers (58-76 years) | |

| Seniors (Above 77 years) | |

| By Content Type | Movies |

| TV Series | |

| Sports | |

| User-Generated Content | |

| Originals |

Key Questions Answered in the Report

How large is the Mexico OTT TV and Video opportunity today?

It generated USD 8.14 billion in 2026 and is projected to reach USD 23.41 billion by 2031 at a 23.52% CAGR.

Which revenue model is expanding the fastest in Mexico's streaming space?

Hybrid plans that blend ad-supported and subscription tiers are on a 23.98% CAGR path through 2031.

Why is Northern Mexico viewed as the next streaming growth hotspot?

Fiber roll-outs along industrial corridors, higher disposable incomes, and lower piracy exposure are propelling a 25.32% CAGR.

How are platforms overcoming low credit-card penetration?

They integrate voucher systems such as OXXO Pay, real-time SPEI transfers, and digital wallets to capture cash-reliant households.

What content strategy best differentiates services for local viewers?

Heavy investment in Spanish-language originals, Netflix alone committed USD 1 billion over four years - helps secure loyal audiences and reduce licensing costs.

Which age group is driving the biggest uptick in mobile streaming hours?

Generation Z, forecast to expand spending at 25.03% CAGR, streams mainly on smartphones and favors short-form and creator-led video.

Page last updated on: